UK Health and Wellness Market Size, Share, Trends and Forecast by Product Type, Functionality, and Region, 2026-2034

UK Health and Wellness Market Size & Forecast 2026-2034

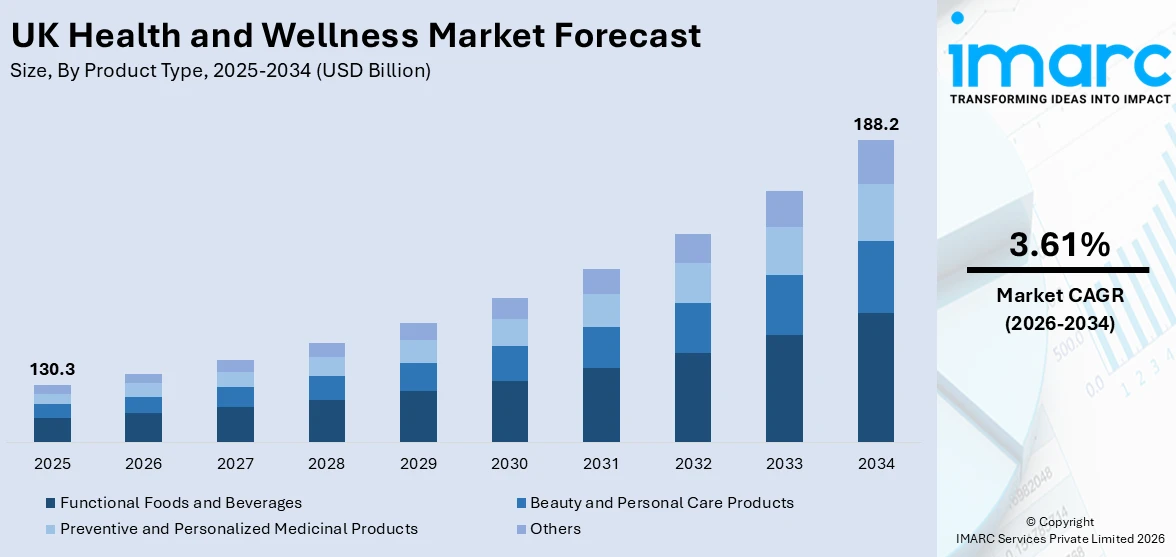

UK health and wellness market size stood at USD 130.3 Billion in 2025, and it is expected to reach USD 188.2 Billion by 2034, with a compound annual growth rate of 3.61% during 2026-2034. The UK health and wellness market is seeing sustained growth, which is being driven by increased consumer health and wellness awareness, government initiatives to reduce obesity through the 10-year health plan, and high innovation levels in functional foods, nutritional solutions, and digital wellness. Nutrition and fitness expenditures in the UK market are up 6% as of early 2025, which is a reflection of the structural shift in preventive health management. The UK government is investing in initiatives, and there is also an aging population and increased premium wellness retail infrastructure supporting the UK market share.

To get more information on this market Request Sample

UK Health and Wellness Industry Analysis: Key Insights

- Functional Foods and Beverages accounted for 32.5% by product type in 2025 of the UK health and wellness market as mainstream retail adoption of fortified plant milks, gut-friendly fermented foods, and protein-enriched dairy has firmly anchored this segment beyond niche consumer groups.

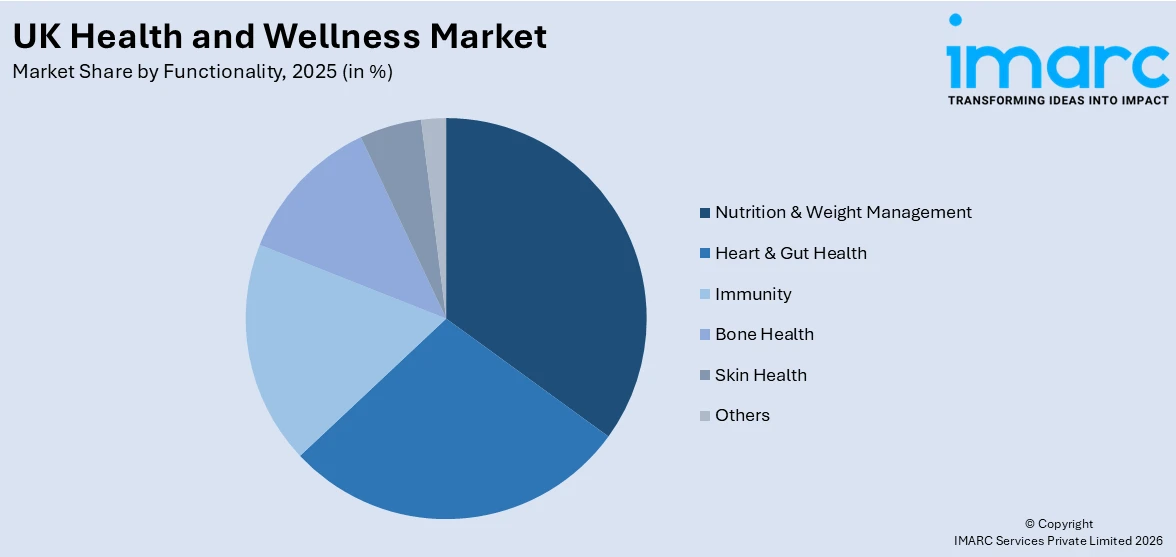

- Nutrition & Weight Management commanded a 24.2% share by functionality in 2025 because obesity costs the NHS £11.4 billion per year and government mandated retailer-level healthy food standards, making weight management the most structurally supported functionality across the entire UK wellness sector.

- London led regionally at 18.3% in 2025, and this reflects the capital's exceptional concentration of premium wellness retailers, health-conscious professionals, and digital health start-ups, establishing it as the country's most sophisticated and highest-spending wellness consumer market.

UK Health and Wellness Market Trends and Dynamic 2026:

Market Trends

Digital Health Integration and Personalised Wellness Technology

The health and wellness market in the UK is undergoing a structural shift, especially in terms of digital and personal health products. This was made evident in May 2025, when Holland & Barrett rolled out its H&B&Me, a wellness app that helps consumers determine their biological age based on 400 million person-years of data, while providing daily coaching and personal nutrition advice. H&B&Me received the Salesforce Customer Experience Gamechanger Award at the Retail Week Awards 2025, signifying the structural shift from transactional retail to lifelong wellness management, thus highlighting the key UK health and wellness market trends.

Functional Nutrition Innovation Driven by GLP-1 Treatment Adoption

Between early 2024 and early 2025, there were over 1 million UK adults taking GLP-1 medicines such as Ozempic, Wegovy, and Mounjaro, with a further 3.3 million considering them. This has created demand for protein-dense, nutrient-optimised functional nutrition formats to fill the nutritional gaps created using these medicines for appetite suppression. PortionIQ, a range of protein-focused nutrition products, was launched in February 2026 by Nestlé, specifically designed for GLP-1 medicine users, bringing together the trend in pharmaceutical weight loss with the innovation in wellness products.

Government Policy Reshaping Retail Health Environments

The UK government has introduced the world-first Healthy Food Standard in June 2025, as part of its 10-year health plan, which requires large retailers to increase the healthiness of the average shopping basket. This has been modelled by Nesta, which has shown the potential for obesity rates to be cut by one in five over three years, with total savings to the NHS to society of £17 billion. This policy-induced reformulation revolution is changing the assortment on the shelves and the product development pipelines of all UK retail routes, which shows the growth of the UK health and wellness market.

- Clean Label and Plant-Based Demand: UK consumers are increasingly looking for natural and clean label products, with more than half of the population looking to cut down on the consumption of ultra-processed foods, thereby changing the product development strategy for food companies.

- Wellness Products for the Ageing Population: The ageing population in the UK has created a demand for bone, joint, and brain health supplements, as well as products designed to manage age-related conditions.

- Mental Wellness: Products in the stress, sleep, and mood enhancement category are growing rapidly, with the need for mental wellness becoming part of the mainstream consumer consciousness for all demographic groups in the UK.

- Wearable and Digital Health: Fitness trackers and AI-powered apps are becoming integrated with supplement regimens, creating the possibility for personalized wellness and high levels of brand loyalty.

Growth Drivers

Rising health consciousness and preventive healthcare adoption

Consumers in the UK are increasingly focusing on preventative healthcare instead of treatment-oriented healthcare at an ever-increasing rate. Experian and Reward data for January 2025 indicated that spending on gym memberships grew by 11% over the Christmas period, and 18- to 34-year-olds registered an 8% rise in spending related to health. Nearly half of consumers in the UK purchased functional nutrition products with most of them being from the two-thirds of Gen Z and millennials age group. These UK health and wellness market trends highlight healthcare as a structural category of spending.

Government investment and public health infrastructure expansion

Public sector health expenditure in the UK has risen to £241.8 billion in 2024/25. The NHS-led 10-year health plan is accelerating the shift from reactive treatment to preventive wellness, which is resulting in systemic drivers for consumers, retailers, and businesses to invest in health and wellness. The increased investment in diagnostic and preventive healthcare infrastructure in underserved UK regions, is supporting the UK health and wellness market forecast.

Expanding retail infrastructure and digital commerce penetration

Total sales of Holland & Barrett for 52 weeks up to September 2025 were £981.0 million, showing an increase of 11% over the previous year’s sales due to 13 net new stores in the UK and Ireland. Their first wellness destination in Cardiff opened in March 2025 and offers yoga and personal health consultations, showing the current trend in retailing where consumers are engaged in a way that is beyond a simple purchase.

- Ageing UK Population: With an increasing number of adults in the 65+ age bracket, there is a growing trend of adults seeking supplements, functional foods, and health solutions to aid mobility, immunity, and brain function.

- Clean Label and Organic Product Demand: With consumers demanding transparency and a cleaner label, there is a growing trend in the premium wellness space in food, beauty, and wellness products.

- E-commerce and Direct-to-Consumer Expansion: Digitally native wellness brands are expanding product accessibility and increasing penetration of specialist health products into all demographics of the UK population.

- Corporate Wellness Programmes: With businesses investing in employee wellness programmes, there is a growing trend of B2B demand in wellness products, creating a parallel revenue stream to B2C brands.

Market Restraints

Affordability barriers and cost of living issues: The premium pricing of health and wellness products creates significant barriers to accessibility, particularly for those consumer segments with affordability constraints. Financial constraints impact the ability of consumers to engage with supplements, functional foods, and personalized wellness products, thereby limiting the overall market reach of the industry beyond the more affluent demographic segment and perpetuating the wellness gap between the deprived and affluent communities of the UK.

Regulatory barriers in substantiation of health and wellness claims: The stringent regulatory environment, which governs the substantiation of health and nutrition-related product claims, creates significant barriers to product development and innovation, with the lengthy and resource-intensive process for the approval of new health-related product claims limiting the scope for innovation, market entry for smaller wellness and functional food companies, and the scope for companies to effectively communicate the benefit of their products in the rapidly changing functional food and supplement market.

Consumer trust deficits and misinformation issues: The rise of unverified wellness product claims and the spread of misinformation on social media are causing trust deficits among consumers in the wellness and health space. This has created hurdles for companies without clear scientific backing and proof, making it difficult for them to gain traction with the more discerning and health-conscious consumer, thereby creating competitive pressure on newer and smaller wellness companies.

.webp)

UK Health and Wellness Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Functional Foods and Beverages | 32.5% | 2025 |

| Functionality | Nutrition & Weight Management | 24.2% | 2025 |

| Region | London | 18.3% | 2025 |

Product Type Insights

Functional Foods and Beverages- 32.5% Market Share (2025) | Leading Product Type

Functional foods and drinks are at the center of the UK’s health and wellness market, and there is retailer support for fortified plant-based milk alternatives, protein-enhanced dairy products, gut-healthy fermented foods, and herbal-based drinks. The market is being driven by consumers’ increasing willingness to adopt ‘food as medicine’, Gen Z and millennials are driving this trend with functional foods and drinks that have obvious physiological benefits.

|

Segment Breakdown Functional Foods and Beverages (32.5%) · Beauty and Personal Care Products · Preventive and Personalized Medicinal Products · Others |

Functionality Insights

Access the comprehensive market breakdown Request Sample

Nutrition & Weight Management- 24.2% Market Share (2025) | Leading Functionality

Nutrition and weight management is the number one functionality for the health and wellness sector in the UK, and there is a significant health imperative for growth. The UK has the third highest adult obesity rate in Europe, and obesity-related illness costs the NHS 11.4 billion pounds annually. There is increasing consumer demand for calorie-controlled products with high protein and nutrient content across all retailer channels in the UK.

|

Segment Breakdown Nutrition & Weight Management (24.2%) · Heart & Gut Health · Immunity · Bone Health · Skin Health · Others |

Regional Insights

London- 18.3% Market Share (2025) | Leading Region

London dominates the UK health and wellness sector with its highest number of premium wellness stores, health-conscious food stores, and digital health start-ups. London has a large number of professionals with higher-than-average disposable incomes and a high level of health and wellness knowledge to support spending on functional foods, beauty wellness products, and supplements. Flagship stores of major retailers such as Holland & Barrett, Planet Organic, and Whole Foods operate in London’s affluent areas and transport hubs with high foot traffic.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

18.3%

|

|

Key States

|

London |

|

Major Growth Drivers

|

High per-capita health spending, premium retail density, digital health start-up ecosystem, young professional demographics |

|

Outlook

|

Sustained regional leadership with premium wellness growth |

|

Regional Breakdown London (18.3%) · South East · North West · East of England · South West · Scotland · West Midlands · Yorkshire and The Humber · East Midlands · Others |

South East:

The South East is the second largest health and wellness hub in the UK. It has good household incomes, good population densities, and is close to London’s wellness retail infrastructure. There is a growing health food store sector in Brighton, Oxford, and Southampton.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Surrey, Kent, Sussex, Hampshire, Berkshire, Oxfordshire |

|

Major Growth Drivers

|

High disposable income, organic food adoption, suburban wellness retail growth, active ageing population |

|

Outlook

|

Strong incremental growth alongside London |

North West:

The North West is a critical UK health and wellness hub. It includes an expanding corporate wellness and retail infrastructure in Manchester. It has a large population of students and graduates who support demand across health food, supplements, and mental wellness products. Its 18-to-34-year-old demographic has an 8 percent year-on-year increase in health spending.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Manchester, Liverpool, Cheshire, Lancashire, Cumbria |

|

Major Growth Drivers

|

Urban young professional demographic, corporate wellness programmes, Greater Manchester health strategy, e-commerce adoption |

|

Outlook

|

Rapid growth backed by urban health investment |

East of England:

The East of England has good health and wellness fundamentals with good household incomes and large aging demographics across Essex, Hertfordshire, and Norfolk. Cambridge has one of Europe’s largest health research hubs at its biomedical campus. It has good investment potential in nutraceuticals and functional ingredients. UK government health advice to consume 10 micrograms of Vitamin D supplementation daily during autumn and winter months translates to consistent demand throughout the year from its aging population and health-conscious commuter population.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Hertfordshire, Essex, Norfolk, Suffolk, Cambridgeshire, Bedfordshire |

|

Major Growth Drivers

|

Ageing demographics, Cambridge health tech cluster, commuter affluence, strong e-commerce penetration |

|

Outlook

|

Steady growth led by preventive health demand |

South West:

The South West health and wellness market is supported by a thriving organic and plant-based food scene revolving around Bristol and Bath. Sports nutrition products, energy management products, and functional foods with clean labels are sustained by the outdoor lifestyle culture of the South West. Bristol has also developed as a center of sustainable health and wellness brands.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Bristol, Devon, Cornwall, Gloucestershire, Somerset, Dorset, Wiltshire |

|

Major Growth Drivers

|

Organic food culture, health tourism, plant-based product adoption, outdoor lifestyle demographics |

|

Outlook

|

Premium wellness growth anchored by Bristol ecosystem |

Scotland:

Scotland’s health and wellness market is supported by the Good Food Nation Act, which requires Scottish Government ministers to publish a national food plan with measurable targets to improve diets across Scotland. In 2024, Scotland published its national food plan. Edinburgh and Glasgow are expanding their health and wellness infrastructure. There is growing demand for functional foods, mental health products, and preventive health supplements from urban professionals and students across Edinburgh and Glasgow.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Glasgow, Edinburgh, Aberdeen, Dundee, Inverness, Stirling |

|

Major Growth Drivers

|

Good Food Nation Act policy tailwind, mental wellbeing demand, urban retail expansion, university city demographics |

|

Outlook

|

Emerging growth market with strong policy support |

West Midlands:

The health and wellness market of the West Midlands is growing with the expanding economy of Birmingham. There is a large South Asian population in the West Midlands, providing strong demand support for herbal supplements and functional foods from this cultural segment.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Birmingham, Coventry, Wolverhampton, Walsall, Dudley, Solihull |

|

Major Growth Drivers

|

Demographic diversity, Birmingham economic growth, herbal supplement demand, expanding retail presence |

|

Outlook

|

Diversified growth driven by multicultural consumption patterns |

Yorkshire and The Humber:

Yorkshire and The Humber is home to Leeds and Sheffield, which are developing wellness retail markets with large student and professional populations. The region is also home to the Tour de Yorkshire, which has created a strong active lifestyle culture, with functional beverage and health retailer development occurring in major urban centers and towns with large student populations.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Leeds, Sheffield, Bradford, Hull, York, Doncaster |

|

Major Growth Drivers

|

Active lifestyle culture, sports nutrition demand, student population, independent health retail growth |

|

Outlook

|

Growth momentum anchored by Leeds wellness economy |

East Midlands:

The East Midlands region has a developing health and wellness market, with Nottingham and Leicester being major retail centers. Leicester has a large South Asian and East African population, which creates strong demand for herbal supplements and functional foods, which are traditional in these cultures and are being supported by developing mainstream wellness retail infrastructure.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Nottingham, Leicester, Derby, Northampton, Lincoln |

|

Major Growth Drivers

|

Student-driven nutrition demand, demographic diversity, cultural wellness products, preventive health adoption |

|

Outlook

|

Steady growth driven by diverse urban consumer base |

Market Outlook 2026-2034

What is the future outlook of the UK health and wellness market?

The UK Health and Wellness market is expected to sustain steady revenue growth through 2034

The UK’s health and wellness market has shown strong growth prospects, with the government’s healthy food initiatives, the country’s growing older population, and the development of functional foods, beauty wellness, and personalized supplements providing strong backing. Digital health, preventive care with the NHS, and the growing health and wellness literacies of the population will ensure the UK’s health and wellness market’s growth prospects remain strong and stable until 2034, with the mass and premium segments of the market providing stable and diversified growth. E-commerce’s growing influence, corporate wellness investments, and the development of the retail infrastructure will ensure the UK’s health and wellness market’s stable and strong growth prospects.

UK Health and Wellness Market: Leading Key Players

The UK health and wellness market is characterized by a competitive market structure of global consumer goods conglomerates, nutraceuticals, and homegrown health and wellness retailers. The competition is driving innovation in functional ingredients, digital health integration, retail network development, and sustainable formulation development, which is increasing market accessibility and sophistication for all consumer groups.

| Company | Leading Brands | Highlights |

|---|---|---|

| Holland & Barrett Retail Limited | H&B Own Brand, Optimum Nutrition, Good Hemp | Total sales of £981.0m in FY2024/25 (+11%); launched H&B&Me wellness app (May 2025) tracking biological age; opened first experiential wellness store in Cardiff (March 2025) featuring yoga and personalised health consultations |

| Unilever PLC | Dove, Knorr, Marmite, Lynx, Ben & Jerry’s | Acquired plastic-free personal care brand Wild (April 2025); launched 12-product Whole Body deodorant range with £12.5m marketing spend (January 2025); broad nutrition and personal care portfolio across 190+ countries |

| Nestlé S.A. | Nestlé Health Science, Garden of Life, Pure Encapsulations | Launched PortionIQ protein-optimised nutrition range for GLP-1 medication users (February 2026); strategic focus on functional nutrition and science-led supplement brand portfolio globally |

Some other major key players in the UK health and wellness market are Vitabiotics Ltd., Bayer AG L’Oréal SA, Procter & Gamble, Herbalife Nutrition Ltd., David Lloyd Leisure Ltd., Fitness First, Danone UK, Reckitt Benckiser Group Plc, GlaxoSmithKline Consumer Healthcare, Myprotein (THG PLC), etc.

Latest Development & News:

- In February 2026, Nestlé launched PortionIQ, a dedicated nutrition range designed for GLP-1 weight-loss medication users, providing pre-portioned, protein-optimised formats to maintain lean mass and adequate nutrient intake during appetite-suppressed weight management. The launch marked a significant convergence of pharmaceutical weight-loss trends and mainstream wellness product innovation, with Nestlé positioning the brand within its Health Science portfolio to serve the growing medically assisted weight management segment across the UK.

- In June 2025, the UK government unveiled a world-first Healthy Food Standard under its 10 Year Health Plan, requiring large retailers and manufacturers to make average shopping baskets measurably healthier. Nesta modelling projected the policy could reduce UK obesity rates by approximately one-fifth over three years, delivering NHS total savings societal benefits of £17 billion. Leading supermarkets signalled readiness to reformulate products, adjust shelf layouts, and significantly expand their health food ranges in response.

- In May 2025, Holland & Barrett launched H&B&Me, a personalised wellness app calculating users’ biological age and providing daily health coaching, earning the Salesforce Customer Experience Gamechanger Award at Retail Week Awards 2025. The platform was developed as part of the retailer’s digital transformation strategy, supported by total capital investment of £96.3 million in its 2024 financial year, representing a structural shift in UK health retail toward lifelong preventive wellness management and data-driven personalisation.

UK Health and Wellness Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Functional Foods and Beverages, Beauty and Personal Care Products, Preventive and Personalized Medicinal Products, Others |

| Functionalities Covered | Nutrition and Weight Management, Heart & Gut Health, Immunity, Bone Health, Skin Health, Others |

| Regions Covered | London, South East, North West, East of England, South West, Scotland, West Midlands, Yorkshire and The Humber, East Midlands, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the UK Health and Wellness Market Report

The UK health and wellness market was valued at USD 130.3 Billion in 2025.

The UK health and wellness market is forecast to reach USD 188.2 Billion by 2034, growing at a CAGR of 3.61% from 2026-2034. Growth will be sustained by government preventive health policies, ageing population dynamics, digital health platform expansion, and continued innovation in functional foods, personalised nutrition, and beauty wellness categories.

Functional foods and beverages dominates the market with a share of 32.5% in 2025, driven by mainstream consumer adoption of fortified plant milks, protein-enriched dairy products, gut-friendly fermented foods, and botanical beverages, as UK consumers increasingly embrace food-as-medicine principles across all demographic groups.

Nutrition & weight management commands the market with a share of 24.2% in 2025, driven by demand for calorie-controlled, high-protein formats alongside government obesity reduction policies and the rapid adoption of GLP-1 weight-loss treatments reshaping how consumers approach dietary management across the UK.

Some of the major players in the UK health and wellness market include Holland & Barrett Retail Limited, Unilever PLC, Nestlé S.A., Vitabiotics Ltd., Bayer AG, L’Oréal SA, Procter & Gamble, Herbalife Nutrition Ltd., David Lloyd Leisure Ltd., Fitness First, Danone UK, Myprotein (THG PLC), etc.

Key trends shaping the UK health and wellness market include the rise of AI-powered personalised wellness platforms, growing consumer demand for adaptogenic and nootropic functional ingredients, the mainstreaming of gut microbiome health products, increasing adoption of sustainable and plastic-free personal care formats, and the convergence of pharmaceutical weight-loss treatment adoption with functional food innovation.

London currently leads the UK health and wellness market, accounting for a share of 18.3% in 2025, because of the region’s high concentration of premium wellness retailers, health-conscious young professionals, digital health start-up ecosystem, and above-average disposable incomes that consistently drive spending across all wellness product categories.

Key growth factors include increasing consumer focus on mental health and emotional wellbeing as part of holistic wellness routines, the growing subscription-based direct-to-consumer wellness market, rising employer investment in corporate health programmes, expanding NHS digital health infrastructure, and demographic tailwinds from an ageing population requiring targeted preventive health products.

Key challenges include persistent affordability barriers limiting premium product access for lower-income consumers, complexity of regulatory health claim substantiation under UK frameworks, rising ingredient and supply chain costs, consumer trust deficits from unverified social media wellness claims, and competitive pressure from pharmacy-grade and prescription health solutions displacing OTC wellness products.

There are strong growth prospects for the UK health and wellness market through 2034. Government-mandated healthy food standards, NHS preventive care expansion, and growing consumer health literacy will drive sustained demand growth. Both mass-market accessible products and premium personalised wellness solutions will contribute to the market’s long-term development across all regions and demographic groups.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)