United States Cancer Diagnostics Market Size, Share, Trends and Forecast by Product, Technology, Application, End User, and Region, 2026-2034

United States Cancer Diagnostics Market Size and Share:

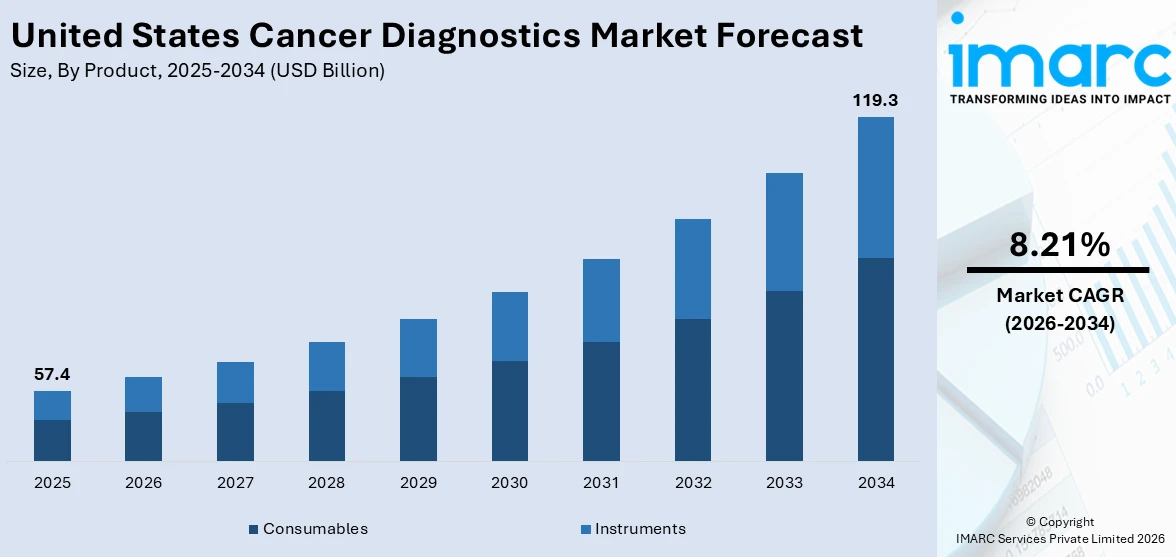

The United States cancer diagnostics market size was valued at USD 57.4 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 119.3 Billion by 2034, exhibiting a CAGR of 8.21% from 2026-2034. The market is driven by the increasing development of personalized therapies that are more effective and less toxic, along with rising demand for detection of genetic mutations associated with cancer.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 57.4 Billion |

| Market Forecast in 2034 | USD 119.3 Billion |

| Market Growth Rate (2026-2034) | 8.21% |

The increasing prevalence of cancer in the United States is positively influencing the market. As cancer remains a leading cause of mortality, the large number of cases is driving the need for accurate diagnostic tools. Early detection helps to improve survival rates and treatment outcomes, for which advanced diagnostic technologies like imaging and molecular testing are required. Diagnostic tools assess the extent of cancer spread in the body and are important to evaluate prognosis. Besides this, as people are becoming more aware about the benefits of preventive treatment, they are seeking regular cancer screening. Cancer diagnostic tools are highly sensitive and specific to minimize false positives or negatives. They guide the selection of therapies, such as surgery, chemotherapy, and radiation, further impelling the market growth.

To get more information on this market Request Sample

Improvements in diagnostic imaging are enhancing the accuracy, speed, and accessibility of cancer detection and monitoring. High-resolution computed tomography (CT) scans, magnetic resonance imaging (MRI), positron emission tomography (PET) scans, and 3D mammography provide detailed visuals of tumors to enable earlier and more precise diagnoses. These advancements can identify even small lesions to evaluate an individual's predisposition to certain cancers. The integration of artificial intelligence (AI) in imaging systems is expanding diagnostic capabilities by assisting in image interpretation and reducing diagnostic errors. Moreover, AI-powered tools streamline workflows and provide radiologists with decision-support systems to increase patient outcomes. With healthcare providers adopting efficient tools, the demand for advanced diagnostic imaging is rising in the US. The IMARC Group’s report shows that the United States diagnostic imaging market is expected to reach USD 14.1 Billion by 2033.

United States Cancer Diagnostics Market Trends:

Growing requirement for precision medicine

The increasing need for precision medicine is driving the demand for highly specific and advanced diagnostic tools. Precision medicine aims to tailor treatment plans based on an individual’s genetic, molecular, and clinical profile, which require detailed diagnostic data to identify unique cancer characteristics. Diagnostics are employed to identify tumor markers and actionable targets to develop personalized therapies that are more effective and less toxic. In line with this, the rise of immunotherapies is catalyzing the demand for precise diagnostics. Treatments like immune checkpoint inhibitors require specific diagnostics to determine whether a patient is a good candidate. Based on that, personalized medicines are prescribed. According to the IMARC Group’s report, the United States precision medicine market is projected to exhibit a growth rate (CAGR) of 7.1% during 2024-2032.

Increasing demand for liquid biopsy

The rising demand for liquid biopsy is offering a transformative and non-invasive approach to cancer detection and monitoring. Unlike traditional biopsies that require surgical tissue extraction, liquid biopsy detects cancer-related biomarkers like circulating tumor cells (CTCs), from bodily fluids like blood, urine, or saliva. This convenience makes it a more patient-friendly and accessible diagnostic option. Liquid biopsy can track cancer progression and treatment response in real time. In addition, as healthcare professionals are emphasizing minimally invasive (MI) procedures, liquid biopsy fits seamlessly into this trend. This is leading to high investments in research and development (R&D) activities so that more advanced and cost-effective liquid biopsy solutions can be produced. The data published on the website of the IMARC Group shows that the United States liquid biopsy market is expected to reach USD 1,775.8 Million by 2033.

Rising integration of next generation sequencing (NGS)

The increasing integration of next-generation sequencing (NGS) is enabling more comprehensive and precise insights into cancer biology. NGS enables the simultaneous sequencing of millions of deoxyribonucleic acid (DNA) or ribonucleic acid (RNA) fragments, which allows for comprehensive analysis of entire genomes, exomes, and targeted gene panels. NGS provides highly accurate results by detecting even low-frequency mutations and rare variants in a tumor’s genetic profile. This precision is critical for tailoring targeted therapies and understanding complex cancer pathways. Innovations in sequencing technology are reducing their costs and minimizing their turnaround times, further supporting the market growth. IMARC Group’s report predicted that the United States next generation sequencing market will exhibit a growth rate (CAGR) of 18.9% during 2025-2033.

United States Cancer Diagnostics Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the United States cancer diagnostics market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on product, technology, application, and end user.

Analysis by Product:

- Consumables

- Antibodies

- Kits and Reagents

- Probes

- Others

- Instruments

- Pathology-Based Instruments

- Imaging Instruments

- Biopsy Instruments

Consumables (antibodies, kits and reagents, probes, and others) include various disposable used during diagnostic procedures. They are very important to produce accurate results in biopsy testing, PCR analysis, and imaging. They are employed to monitor and detect various cancer types. They also assist healthcare professionals to diagnose cancer early and plan treatment.

Instruments (pathology-based instruments, imaging instruments, and biopsy instruments) inculcate medical devices and equipment used to analyze cancerous cells and tumors. This encompasses imaging systems, biopsy tools and molecular diagnostic equipment, and laboratory devices. Precise, efficient, and non-invasive cancer detection is possible through the usage of instruments, contributing to improved patient outcomes.

Analysis by Technology:

- IVD Testing

- Polymerase Chain Reaction (PCR)

- In Situ Hybridization (ISH)

- Immunohistochemistry (IHC)

- Next-Generation Sequencing (NGS)

- Microarrays

- Flow Cytometry

- Immunoassays

- Others

- Imaging

- Magnetic Resonance Imaging (MRI)

- Computed Tomography (CT)

- Positron Emission Tomography (PET)

- Mammography

- Ultrasound

- Biopsy Technique

The in-vitro diagnostic (IVD) testing {polymerase chain reaction (PCR), in situ hybridization (ISH), immunohistochemistry (IHC), next-generation sequencing (NGS), microarrays, flow cytometry, immunoassays, and others} segment includes tests performed on samples taken from the body, such as blood, urine, or tissue, to detect cancer. Improved IVD technologies allow for earlier and more accurate detection of cancer. It provides valuable insights for personalized treatment plans.

Imaging systems {magnetic resonance imaging (MRI), computed tomography (CT), positron emission tomography (PET), mammography, and ultrasound} are used to visualize tumors and abnormal growths. Imaging is crucial for locating and staging cancers, guiding biopsies, and monitoring treatment efficacy. Innovations like AI-powered imaging and enhanced resolution techniques enhance the efficiency of imaging systems.

The biopsy technique is utilized to obtain tissue samples for pathological analysis, such as needle biopsies, endoscopic biopsies, and surgical biopsies. Biopsy procedures are essential for diagnosing and determining the stage of cancer. Liquid biopsy, which uses blood samples for genetic analysis, is opted more due to its non-invasive nature.

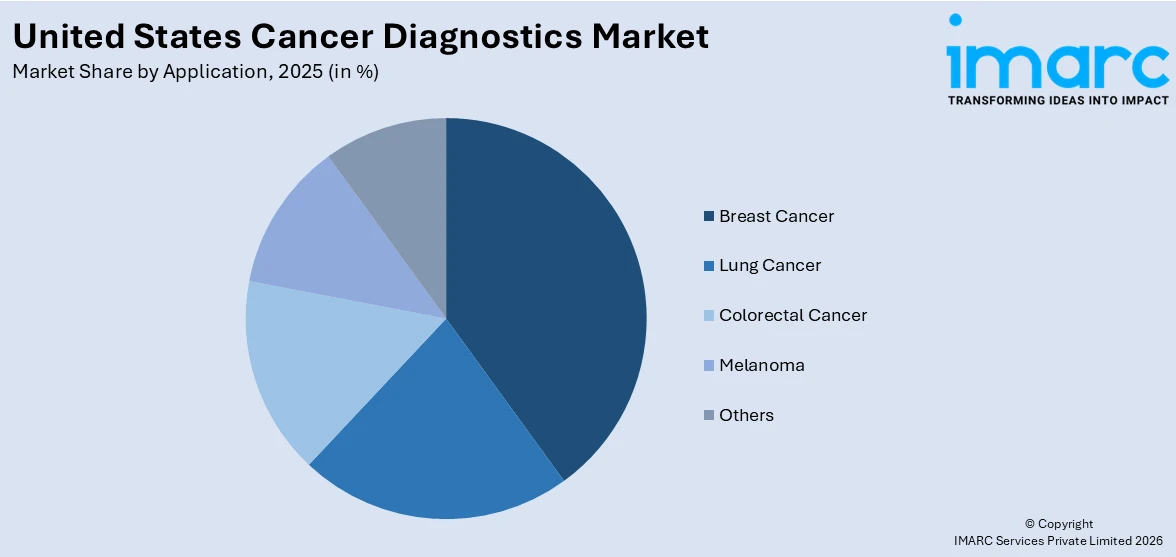

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Breast Cancer

- Lung Cancer

- Colorectal Cancer

- Melanoma

- Others

The breast cancer segment includes tests and technologies focused on detecting breast cancer at early stages. Methods such as mammography, ultrasound, biopsy techniques, and molecular testing are used for the diagnosis of breast cancer. In the US, breast cancer is becoming more prevalent, which creates the need for efficient diagnostic solutions.

Lung cancer is among the leading causes of cancer-related deaths in the US, which makes early diagnosis crucial. Molecular testing and biopsy techniques are employed to detect lung cancer. New diagnostic technologies improve the accuracy and efficiency of lung cancer detection.

The colorectal cancer segment focuses on detecting colorectal cancer through methods like colonoscopy, stool tests, and biopsy. Advanced genetic testing and non-invasive diagnostic options, such as fecal immunochemical tests (FIT), are employed to plan treatment. They also assist in preventive screening.

The melanoma segment in the US is centered around locating skin cancer, particularly melanoma, through visual inspections and enhanced methods. Early detection is crucial for better treatment outcomes, as melanoma is one of the most aggressive forms of skin cancer. People are concerned about skin cancer’s prevalence, which is leading to a rise in the usage of advanced imaging technologies and molecular profiling.

Analysis by End User:

- Hospitals and Clinics

- Diagnostic Laboratories

- Others

In hospitals and clinics, diagnostic tests are performed on cancer patients. These facilities often utilize advanced imaging technologies and biopsy techniques to diagnose and monitor cancer. Cutting-edge diagnostic tools are highly available in healthcare settings. Hospitals and clinics play a key role in providing comprehensive care and treatment.

Diagnostic laboratories are specialized laboratories that perform diagnostic tests to detect cancer. These labs use a variety of tools like genetic testing to provide accurate cancer diagnoses. They are pivotal in offering high-throughput and precise testing services. Moreover, they are experts in analyzing complex samples.

Regional Analysis:

- Northeast

- Midwest

- South

- West

In the Northeast region of the United States, major healthcare hubs like New York and Boston are well-setup. These areas are home to some of the best hospitals and research institutions, where advanced cancer diagnostic technologies are worked upon. The region has a high population density, which requires accurate diagnostic tools for personalized cancer treatment.

In the Midwest part, particularly Chicago and Detroit, healthcare infrastructure in cities like Chicago is rapidly evolving. The region flourishes with high access to innovative cancer detection methods. Rising investments in healthcare services encourage the use of diagnostic technologies like imaging and molecular testing.

In states like Texas, Florida, and Georgia of the South region, there is more population, which require efficient diagnostic services. Enhanced healthcare infrastructures are making cancer diagnostics more accessible. Healthcare providers and individuals focus on improving early detection and preventive screening. Thus, the demand for advanced diagnostic technologies, such as imaging systems and liquid biopsy, is high across the region.

The West region, including states like California, Washington, and Colorado, plays a huge role in shaping the US cancer diagnostics market. It has innovative tech hubs and medical centers, which promote the adoption of AI-powered diagnostic tools and advanced imaging technologies.

Competitive Landscape:

Key players are investing in advancing technology to expand product offerings and form strategic partnerships. Leading companies in the market focus on developing diagnostic tools, such as advanced imaging systems, molecular diagnostics, and liquid biopsy technologies, which improve accuracy and early detection of various types of cancer. Government agencies are encouraging R&D activities to incorporate AI and machine learning (ML) into diagnostic systems, which can enhance precision. Furthermore, strategic collaborations with healthcare providers and pharmaceutical companies enable key players to broaden their reach and develop personalized diagnostic solutions. In addition to technological innovation, key players are actively expanding their market presence through acquisitions, increasing distribution networks, and improving patient access to cutting-edge diagnostic services. For instance, in December 2024, Exact Sciences Corp., a prominent provider of cancer screening and diagnostic tests, collaborated with famous Grammy award-winning artist Lil Jon in the “Get Low #2” campaign to encourage people in the US for colon cancer screening. The partnership emphasized using the Cologuard test, as an effective and non-invasive tool that can improve screening rates for adults 45 and older who are eligible.

The report provides a comprehensive analysis of the competitive landscape in the United States cancer diagnostics market with detailed profiles of all major companies.

Latest News and Developments:

- February 2024: Hologic, Inc., a leading women’s health company, announced the launch of a new FDA-approved Genius Digital Diagnostics System with the Genius Cervical AI algorithm to aid cytologists in assessing cancer cases more precisely and commercialize it, particularly in the United States. The system integrates AI with advanced volumetric imaging technology to help identify pre-cancerous lesions and cervical cancer cells.

- April 2024: Researchers of the National Institutes of Health (NIH), located in Washington DC unveiled the development of an AI tool to aid doctors more precisely in treating cancer. The equipment can predict whether a person’s cancer will respond to a specific drug, which can increase survival rates.

- September 2024: Nanostics Inc., a precision health company, signed an agreement with Protean BioDiagnostics Inc. to launch CDX Prostate, an AI-based tool that can identify the risk of aggressive prostate cancer in men in the US. This assimilation promises to provide critical support to males and their healthcare providers in making better decisions.

United States Cancer Diagnostics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Technologies Covered |

|

| Applications Covered | Breast Cancer, Lung Cancer, Colorectal Cancer, Melanoma, Others |

| End Users Covered | Hospitals and Clinics, Diagnostic Laboratories, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States cancer diagnostics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the United States cancer diagnostics market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States cancer diagnostics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Cancer Diagnostics Market Report

Cancer diagnostics refers to the process of detecting and identifying cancer in the body through various tests and procedures. It involves using advanced technologies and methods to find tumors or abnormal cell growth at an early stage, which allows for timely treatment. Cancer diagnostics include imaging techniques, blood tests, molecular tests, and genetic testing. These diagnostic tools help healthcare providers confirm the presence of cancer, determine its type, stage, and location, and guide personalized treatment decisions.

The United States cancer diagnostics market was valued at USD 57.4 Billion in 2025.

IMARC estimates the United States cancer diagnostics market to exhibit a CAGR of 8.21% during 2026-2034.

The increasing aging population in the US, along with lifestyle changes, is propelling the market growth. Significant investments in healthcare infrastructure, research, and technology are improving the availability of advanced diagnostic services across the country. Moreover, the rising focus on personalized medicine and targeted therapies requires more precise diagnostic tools to identify specific cancer types and genetic mutations, further fueling the market growth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)