United States Ceramic Roller Bearings Market Size, Share, Trends and Forecast by Type, Product Type, Application, and Region, 2026-2034

United States Ceramic Roller Bearings Market Size, Share, Trends & Forecast (2026-2034)

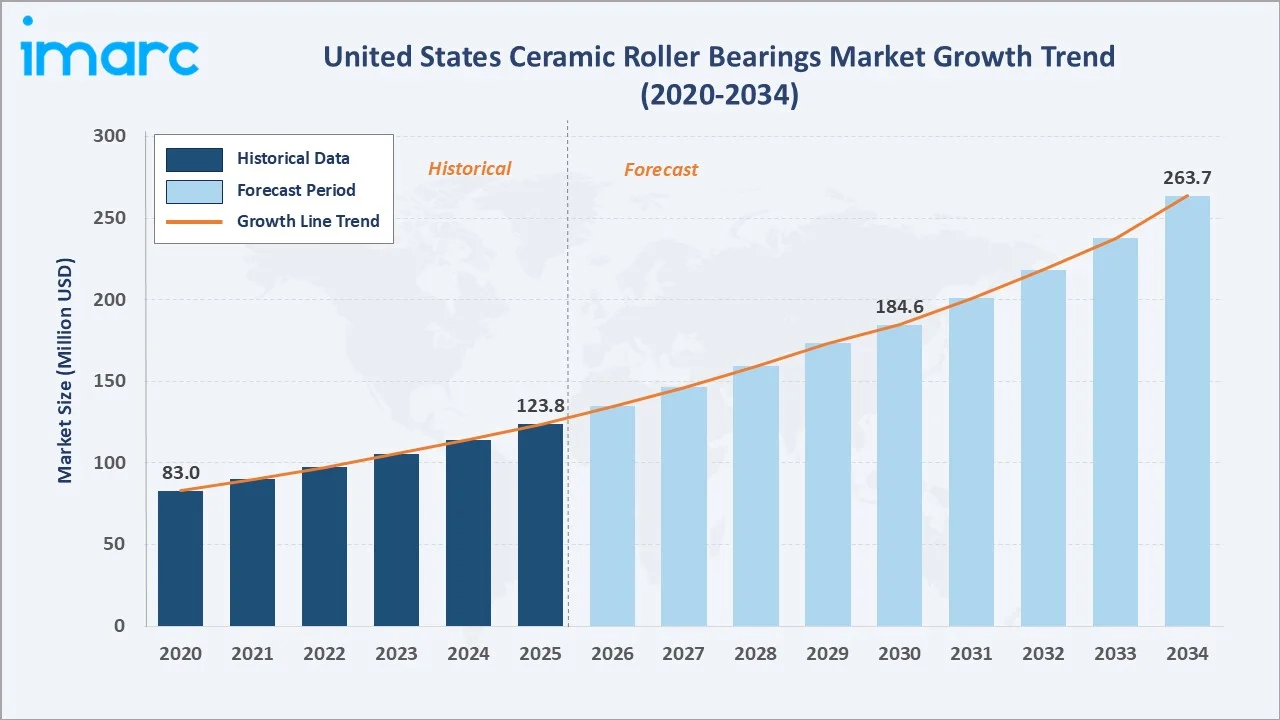

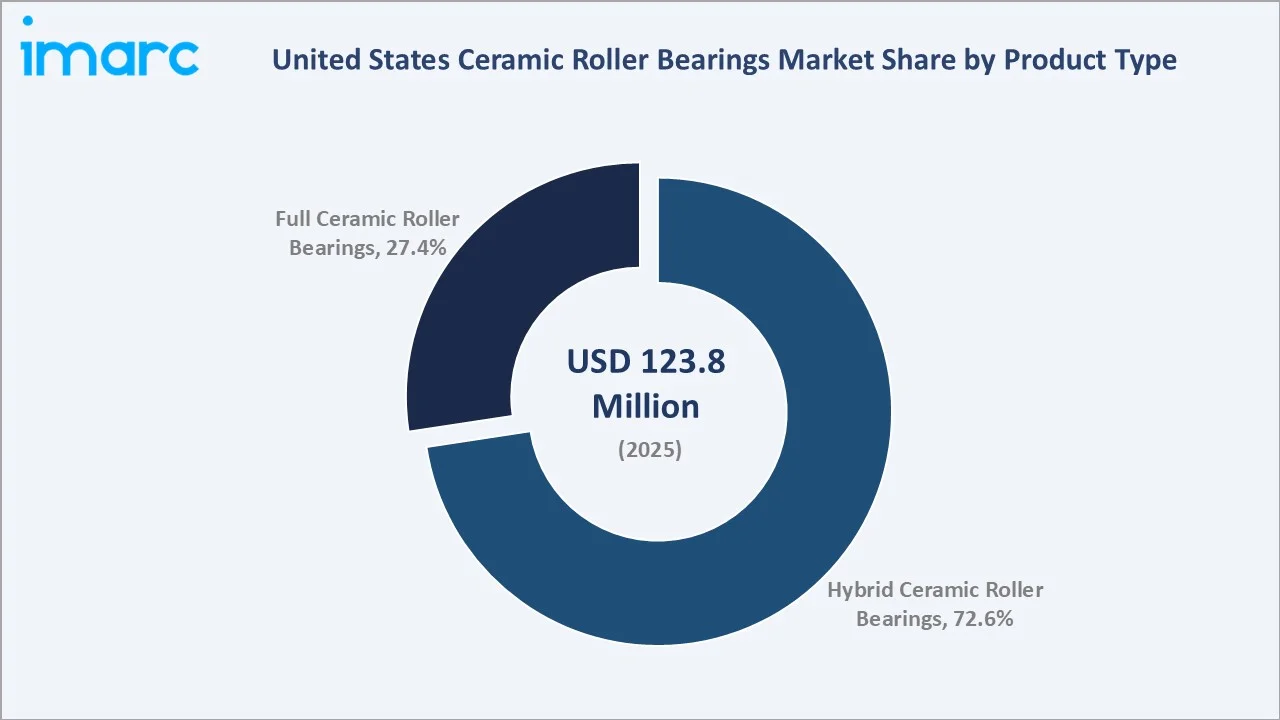

The United States ceramic roller bearings market reached USD 123.8 Million in 2025 and is projected to reach USD 263.7 Million by 2034, growing at a CAGR of 8.33% during 2026-2034. Expanding adoption in aerospace and defense, growing wind energy infrastructure requiring low-maintenance, high-reliability bearings, the rapid growth of semiconductor manufacturing demanding ultra-clean ceramic bearing solutions, and the electric vehicle transition requiring bearings with electrical insulation properties are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 123.8 Million |

|

Forecast Market Size (2034) |

USD 263.7 Million |

|

CAGR (2026-2034) |

8.33% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

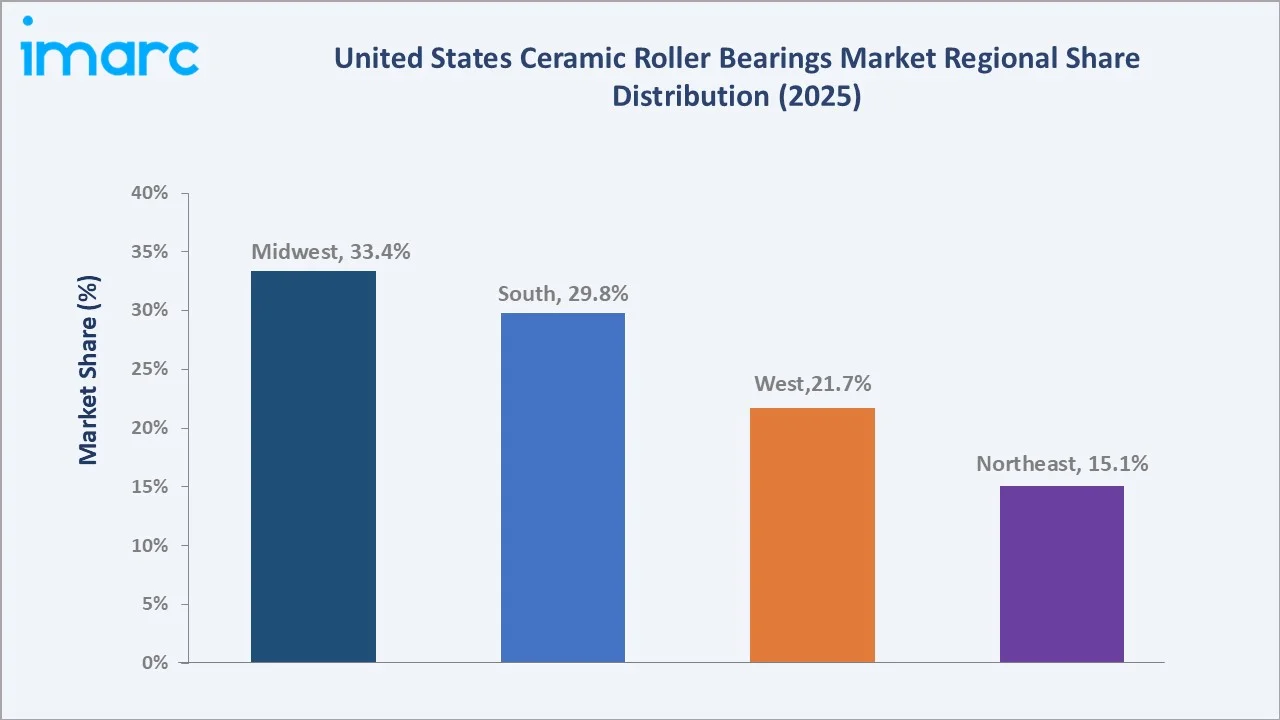

The Midwest leads regionally with a 33.4% market share in 2025, anchored by the highest concentration of wind energy infrastructure, large automotive and industrial manufacturing, and significant aerospace and defense supply chain activity. Silicon nitride commands the dominant 58.4% type share, reflecting its superior combination of high strength, low density, high fracture toughness, and thermal stability that makes it the preferred ceramic material for demanding high-speed and high-temperature bearing applications.

To get more information on this market, Request Sample

The US ceramic roller bearings market is driven by three structural demand forces: the aerospace and defense sector’s requirement for lightweight, high-temperature bearings that reduce maintenance intervals in aircraft engines, helicopters, and weapon systems; the wind energy sector’s adoption of ceramic hybrid bearings to reduce electrical erosion pitting in turbine main shaft and gearbox bearings; and the semiconductor and electronics manufacturing sector’s need for non-magnetic, chemically inert ceramic bearings in wafer processing equipment.

Executive Summary

The United States ceramic roller bearings market is experiencing strong growth, driven by the convergence of demanding performance requirements across multiple high-growth industrial sectors that conventional steel bearings cannot adequately serve. The market was valued at USD 123.8 Million in 2025 and is forecast to reach USD 263.7 Million by 2034, growing at a CAGR of 8.33%.

Silicon nitride accounts for 58.4% of the type segment in 2025, reflecting its position as the highest-performance structural ceramic for demanding bearing applications, including aircraft engine main shaft bearings, high-speed machine tool spindles, and semiconductor process equipment.

Hybrid ceramic roller bearings at 72.6% lead the product type segment, reflecting the market’s pragmatic preference for the performance-cost optimization that hybrid designs provide, including ceramic rolling elements that deliver the speed, electrical insulation, and life benefits while steel rings maintain dimensional compatibility with existing bearing housings.

The Midwest leads regionally at 33.4%, driven by the concentration of wind energy installations across Iowa, Illinois, Kansas, and neighboring Plains states, significant automotive and industrial bearing applications, and established aerospace and defense supply chain activity. Key players compete across precision engineering, material science, and distribution capability.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Silicon Nitride – 58.4% share (2025) |

|

Second Largest Type |

Zirconium Oxide – 29.7% share (2025) |

|

Largest Product Type |

Hybrid Ceramic Roller Bearings – 72.6% share (2025 |

|

Top Companies |

SKF Group, Schaeffler AG, The Timken Company, NSK Ltd. |

Key Analytical Observations Supporting the Above Data:

- Silicon nitride at 58.4% (2025) leads the type segment as its unique combination of high hardness, low density, and thermal stability makes it the only viable ceramic material for the most demanding bearing applications, including jet engine main shaft bearings, high-speed precision machine tool spindles, and semiconductor process equipment where no steel alternative can meet the performance specification.

- Hybrid ceramic roller bearings at 72.6% (2025) dominate as they provide the primary performance benefits of ceramic rolling elements, such as electrical insulation, extended L10 life, reduced friction, and contamination resistance, while maintaining full dimensional interchangeability with standard steel bearing ring housings and shaft interfaces, minimizing OEM redesign requirements.

- Zirconium oxide at 29.7% (2025) serves applications requiring biocompatibility and chemical inertness in aqueous environments. Its fracture toughness makes it preferred for applications subject to impact loading in corrosive media, including chemical process pumps, food and beverage conveyors, and medical implant-grade bearing applications.

- The Midwest’s 33.4% share (2025) reflects the region’s position as the core of US wind energy infrastructure, with Iowa, Illinois, and Kansas collectively representing the highest state-level wind energy capacity, each requiring ceramic hybrid main shaft bearings that prevent electrical erosion from current leakage through turbine drivetrains.

United States Ceramic Roller Bearings Market Overview

Ceramic roller bearings are precision rolling element bearings in which the rolling elements are manufactured from advanced structural ceramics, including silicon nitride, zirconium oxide, aluminum oxide, or silicon carbide (SiC), rather than conventional bearing steel. These bearings serve applications where steel bearings cannot meet performance requirements due to temperature limitations, chemical incompatibility, electrical conductivity, magnetic sensitivity, or lubrication constraints.

Macroeconomic drivers include the U.S. House passing a fiscal 2026 defense spending authorization package on December 2025, allocating nearly USD 900 billion to national security; the United States having the world’s second-largest installed wind energy capacity (over 150 GW) requiring ongoing bearing replacement and upgrade; companies across the US semiconductor ecosystem announcing more than 140 projects across 30 states, totaling over USD 645.3 billion in private investments since 2020.

Market Dynamics

To evaluate market opportunities, Request Sample

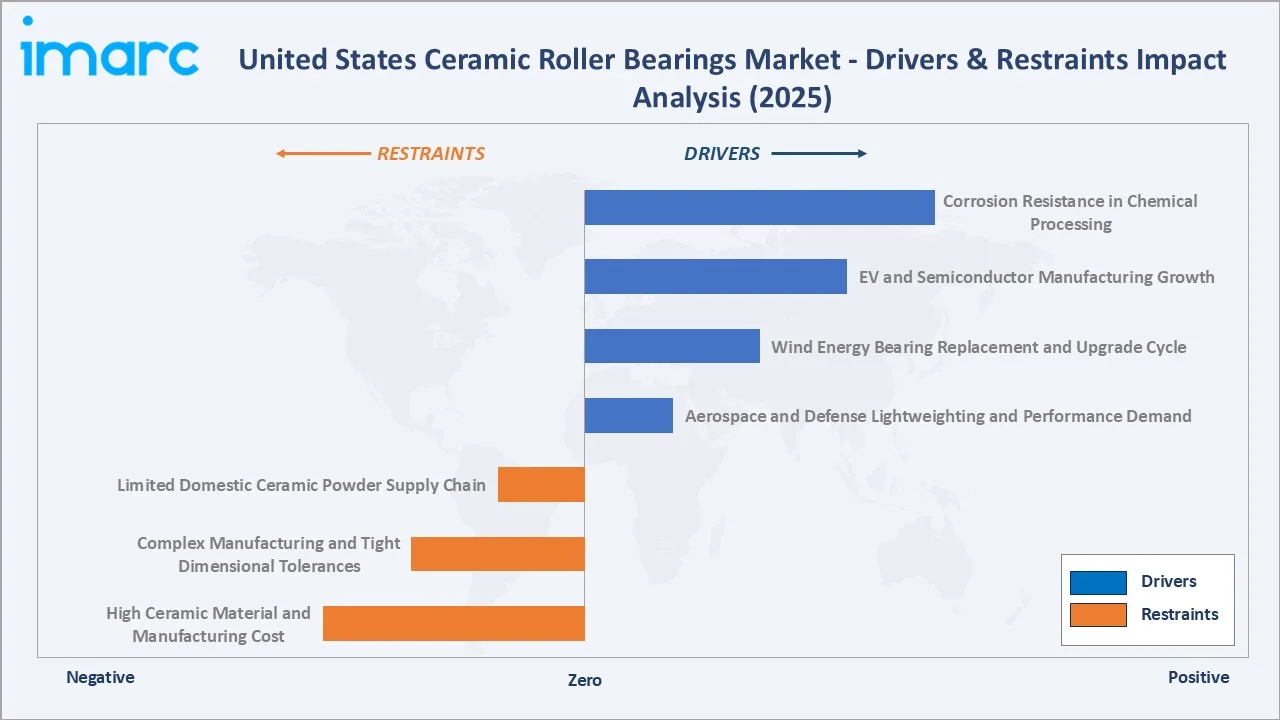

Market Drivers

- Aerospace and Defense Lightweighting and Performance Demand: Silicon nitride ceramic bearings reduce bearing assembly weight by up to 40% compared to steel equivalents, directly contributing to aircraft fuel efficiency and payload improvement. US Department of Defense and NASA programs require ceramic bearings in which lubrication-free operation and high-temperature performance provide critical mission-reliability advantages over steel alternatives.

- Wind Energy Bearing Replacement and Upgrade Cycle: Wind turbine main shaft and gearbox bearings are among the highest-cost maintenance items in wind energy operations, with bearing failures accounting for approximately 25% of wind turbine unplanned downtime. Ceramic hybrid bearings prevent electrical erosion pitting caused by stray currents in turbine drivetrains while delivering extended L10 bearing life, reducing replacement frequency in difficult-to-access nacelle environments.

- EV and Semiconductor Manufacturing Growth: Electric vehicle traction motors generate electrical currents that flow through bearings in the absence of adequate isolation, causing fluting damage that reduces bearing life to a fraction of its rated value. Ceramic hybrid bearings with silicon nitride rolling elements are the primary solution that electrically insulates the motor shaft bearing from current flow.

- Corrosion Resistance in Chemical Processing: Chemical and pharmaceutical processing equipment, including pumps, agitators, and conveyors operating in acidic, alkaline, or solvent environments. Where stainless steel bearings cannot meet corrosion resistance or contamination purity requirements, zirconium oxide ceramic bearings provide full chemical inertness across most industrial chemical environments.

Market Restraints

- High Ceramic Material and Manufacturing Cost: Silicon nitride ceramic balls cost 5–10× more than equivalent precision steel balls due to the energy-intensive sintering process, tight dimensional tolerances requiring extended lapping and grinding cycles, and the capital-intensive nature of ceramic forming and sintering equipment.

- Complex Manufacturing and Tight Dimensional Tolerances: Ceramic bearing components require sintering at temperatures above 1,700°C, followed by precision grinding to ABEC 5-7 tolerances that are challenging given ceramic’s brittleness and resistance to abrasive material removal. Manufacturing yield rates below those achievable with steel bearings add to unit cost, and the specialist equipment required for ceramic bearing production limits the number of qualified domestic suppliers, creating supply chain concentration risk.

- Limited Domestic Ceramic Powder Supply Chain: The United States does not have a large domestic silicon nitride or zirconium oxide powder production industry, creating dependence on Japanese and European ceramic powder suppliers for the primary raw material input. This import dependence creates supply chain vulnerability and pricing exposure that limits cost reduction potential relative to steel bearing alternatives with well-established domestic raw material supply chains.

Market Opportunities

- Hydrogen Economy Bearing Applications: Hydrogen fuel cell systems, electrolyzers, and hydrogen compression equipment require bearings compatible with hydrogen embrittlement risk elimination and high-pressure hydrogen environments. Ceramic roller bearings’ hydrogen-inert material properties make them the preferred option for these applications, and the US government’s USD 7 Billion hydrogen hub investment program is creating near-term procurement opportunities for ceramic bearing suppliers serving this emerging application category.

- CHIPS Act Semiconductor Manufacturing Expansion: The CHIPS and Science Act’s USD 52 Billion investment in US semiconductor manufacturing is driving new fab construction requiring ceramic bearing procurement for clean room robots, wafer handling systems, and precision process equipment. Each new 300mm wafer fab requires hundreds of ceramic bearing sets in high-precision applications, representing a multi-million-dollar procurement opportunity per facility.

Market Challenges

- Ceramic Bearing Application Engineering Complexity: Successful ceramic bearing applications require specialized engineering knowledge in material selection, mounting tolerances, and lubrication selection. The shortage of application engineers with ceramic bearing expertise creates adoption friction, particularly for smaller OEMs without in-house tribology capability.

- Brittleness and Impact Sensitivity: Ceramic materials’ inherent brittleness makes them sensitive to impact loading, sharp edge stress concentrations, and improper mounting that would not damage steel bearings. Applications with shock loading or vibration-induced impact cycles require careful ceramic bearing selection and mounting design, limiting adoption in dynamic loading environments where steel bearings provide more robust performance margins.

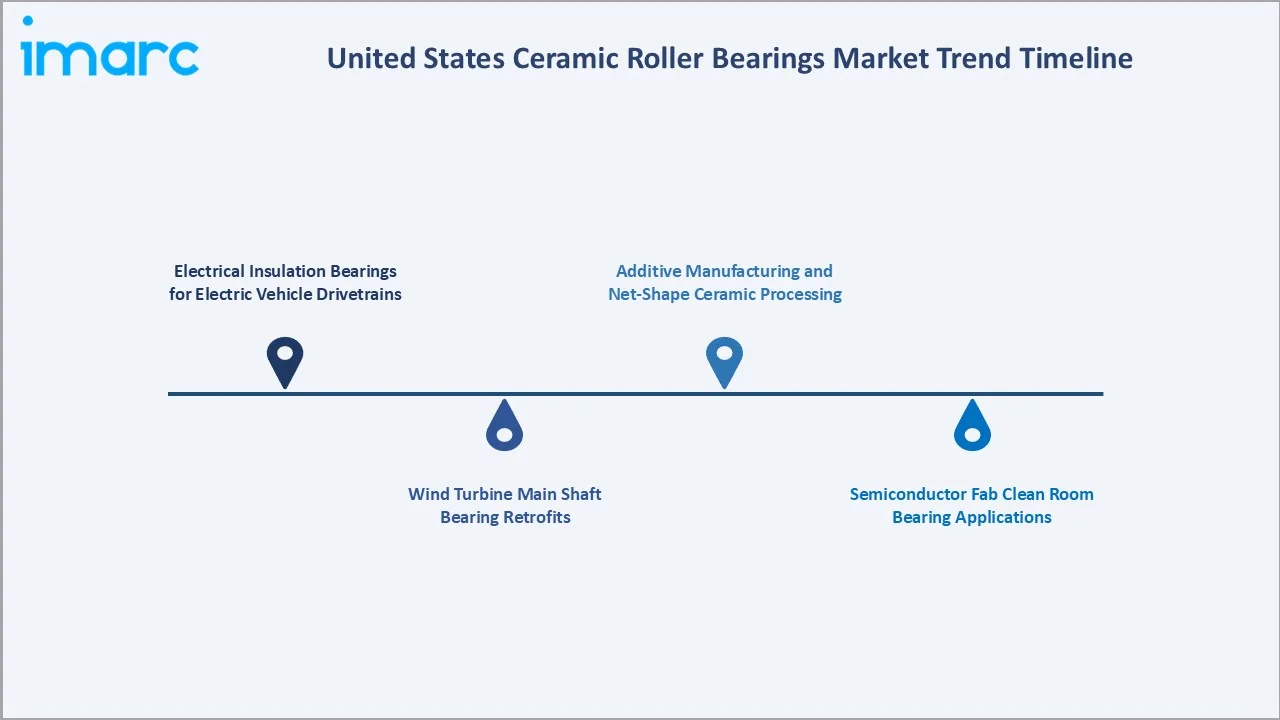

Emerging Market Trends

1. Electrical Insulation Bearings for Electric Vehicle Drivetrains

Approximately 22% of light-duty vehicles sold in the United States in 2025 were hybrid, battery-electric, or plug-in hybrid models, up from 20% in 2024. This is creating structural demand for ceramic hybrid bearings across traction motor, e-axle, and ancillary system applications. Major automotive manufacturers are integrating ceramic hybrid bearing specifications into EV drivetrain designs to prevent current-induced bearing damage from high-frequency inverter switching currents.

2. Wind Turbine Main Shaft Bearing Retrofits

The US’s installed wind turbine fleet, with average asset age increasing toward 15–20 years in the Midwest and Plains states, is driving significant ceramic hybrid bearing retrofit demand for main shaft and gearbox bearing positions. Original turbine main shaft bearings approaching the end of service life are being replaced with ceramic hybrid versions that provide extended service intervals, reducing the turbine nacelle access maintenance events that are the primary cost driver in onshore wind operations.

3. Semiconductor Fab Clean Room Bearing Applications

The CHIPS Act-driven semiconductor fab construction wave across Arizona, Ohio, New York, and Texas is creating new ceramic bearing procurement demand for clean room wafer handling robots, lithography system stage drives, and spin process equipment. These applications require bearings with zero metallic particle generation, magnetic neutrality, and chemical compatibility with aggressive cleaning solvents, performance requirements that only ceramic bearing materials can meet.

4. Additive Manufacturing and Net-Shape Ceramic Processing

Advances in ceramic additive manufacturing, including binder jetting, direct ink writing, and stereolithography of ceramic slurries, are reducing the cost premium for complex ceramic bearing component geometries that are uneconomical to machine from solid ceramic stock. These processing advances are progressively reducing the manufacturing cost barrier for full ceramic bearing designs, potentially accelerating the shift from hybrid to full ceramic bearings in weight-sensitive aerospace and extreme-temperature applications through 2030–2034.

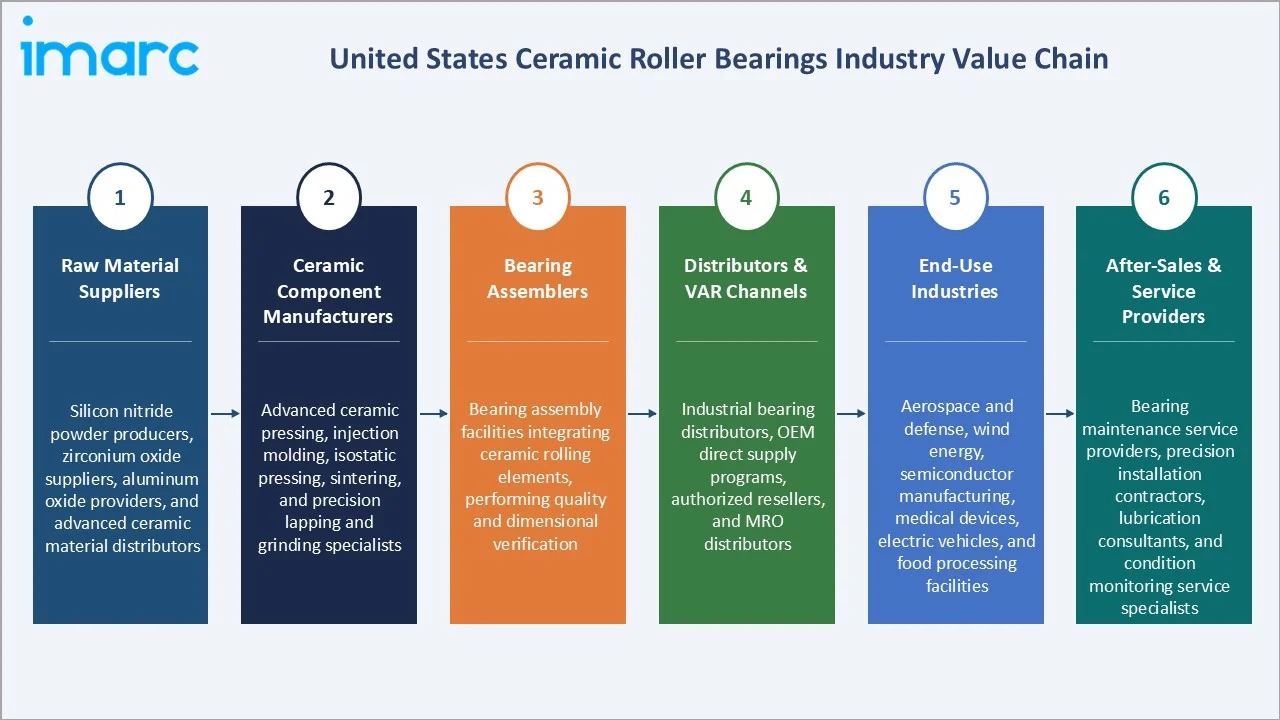

Industry Value Chain Analysis

The US ceramic roller bearings value chain spans from advanced ceramic powder supply through component forming, precision machining, bearing assembly, distribution, and application engineering support. The ceramic component manufacturing tier involves highly specialized processing equipment and materials science expertise concentrated among a small number of domestic and Asian suppliers, creating a technically complex and geographically concentrated supply chain.

|

Stage |

Key Players / Examples |

|

Raw Material Suppliers |

Silicon nitride powder producers, zirconium oxide suppliers, aluminum oxide providers, and advanced ceramic material distributors |

|

Ceramic Component Manufacturers |

Advanced ceramic pressing, injection molding, isostatic pressing, sintering, and precision lapping and grinding specialists |

|

Bearing Assemblers |

Bearing assembly facilities integrating ceramic rolling elements, performing quality and dimensional verification |

|

Distributors & VAR Channels |

Industrial bearing distributors, OEM direct supply programs, authorized resellers, and MRO distributors |

|

End-Use Industries |

Aerospace and defense, wind energy, semiconductor manufacturing, medical devices, electric vehicles, and food processing facilities |

|

After-Sales & Service Providers |

Bearing maintenance service providers, precision installation contractors, lubrication consultants, and condition monitoring service specialists |

Technology Landscape in the United States Ceramic Roller Bearings Industry

Silicon Nitride Material Technology

Silicon nitride is the dominant structural ceramic for high-performance bearing applications, produced through reaction bonding, hot pressing, or hot isostatic pressing sintering processes that achieve densities above 99% of theoretical. Grade 5 silicon nitride ceramic balls achieve surface roughness below 20nm Ra, roundness better than 0.1 micrometers, and dimensional uniformity within 0.25 micrometers, tolerances comparable to the highest precision steel bearing grades.

Hybrid vs Full Ceramic Bearing Design

Hybrid ceramic roller bearings combine silicon nitride or zirconium oxide rolling elements with conventional steel inner and outer rings, retaining full dimensional interchangeability with standard bearing housings while delivering ceramic’s primary performance benefits, including 60% lower rolling element density, electrical insulation, extended fatigue life under mixed lubrication, and reduced heat generation at high speed. Full ceramic bearings provide complete electrical insulation, magnetic neutrality, and chemical inertness but require complete housing redesign for ceramic’s different thermal expansion coefficient and are approximately 3–5× more expensive than hybrid equivalents.

Condition Monitoring and Smart Bearing Integration

US bearing manufacturers are integrating sensor packages including accelerometers, temperature sensors, and acoustic emission transducers into ceramic bearing assemblies, enabling condition monitoring that detects early-stage bearing degradation before failure. These smart ceramic bearing systems are gaining adoption in wind turbines, aerospace, and semiconductor applications where unplanned downtime costs justify the sensor system investment.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Silicon Nitride |

58.4% |

2025 |

|

Product Type |

Hybrid Ceramic Roller Bearings |

72.6% |

2025 |

|

Application |

Automotive and Railways |

🔒 |

2025 |

|

Region |

Midwest |

33.4% |

2025 |

By Type

Silicon nitride leads with a 58.4% share of the United States ceramic roller bearings market in 2025. Silicon nitride’s position reflects its unmatched combination of high hardness, low density, fracture toughness superior to other structural ceramics, and operating temperature capability up to 800–1,000°C. This collectively makes it the standard choice for demanding aerospace, wind energy, semiconductor, and electric vehicle bearing applications where alternative materials cannot meet performance specifications.

To access detailed market analysis, Request Sample

Zirconium oxide at 29.7% serves applications requiring corrosion resistance and biocompatibility, including medical devices, chemical processing, and food and beverage equipment. Its higher fracture toughness versus silicon nitride makes it preferred in impact-exposed applications.

By Product Type

Hybrid ceramic roller bearings lead with a 72.6% share in 2025, reflecting the pragmatic adoption pattern of OEMs transitioning from steel to ceramic bearing solutions as hybrid designs deliver the primary performance benefits of ceramic rolling elements while maintaining full compatibility with existing bearing housing interfaces, eliminating the redesign cost and validation cycle required for full ceramic bearing adoption.

Full ceramic roller bearings at 27.4% serve applications requiring complete electrical insulation, full chemical inertness across metallic contact surfaces, and non-magnetic performance. Aerospace structural applications, semiconductor clean room equipment, medical implant-grade bearing systems, and hydrogen system components represent the primary full ceramic bearing application categories.

Regional Market Insights

The Midwest’s dominant position (33.4%, 2025) reflects the region’s combination of the highest US wind energy installed capacity concentration, a significant automotive and industrial manufacturing base requiring precision bearing solutions, and established aerospace and defense supply chain activity across states, including Illinois, Michigan, Indiana, and Ohio. Wind energy infrastructure in Iowa, Illinois, and Kansas creates sustained hybrid ceramic main shaft bearing demand, while automotive and EV battery plant investment in Michigan and Ohio is driving electrical insulation bearing adoption.

The South at 29.8% is one of the fastest-growing regions, driven by significant aerospace and defense manufacturing expansion in Texas, Alabama, and South Carolina, growing petrochemical and refinery operations requiring corrosion-resistant ceramic bearings, and accelerating wind energy development in Texas, the nation’s single largest wind energy state.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Midwest |

33.4% |

Concentration of wind energy infrastructure, large automotive and industrial manufacturing base, significant aerospace and defense supply chain activity, and established bearing manufacturing and distribution centers |

|

South |

29.8% |

Growing aerospace and defense manufacturing clusters, expanding petrochemical and energy sector requiring corrosion-resistant bearings, rising industrial manufacturing investment, and strong wind energy development activity |

|

West |

21.7% |

Leadership in semiconductor manufacturing requires ultra-clean ceramic bearing applications, strong aerospace and technology sector, growing EV manufacturing investment, and significant wind and renewable energy installations |

|

Northeast |

15.1% |

Established precision manufacturing and defense industry concentration, medical device manufacturing requiring high-purity ceramic bearings, pharmaceutical processing applications, and research institution demand |

The West’s 21.7% share (2025) benefits from semiconductor fab concentration in Arizona, Oregon, and California, creating consistent demand for ultra-clean ceramic bearing solutions. The Northeast at 15.1% represents a smaller but technically sophisticated market driven by defense, pharmaceutical, and precision manufacturing applications.

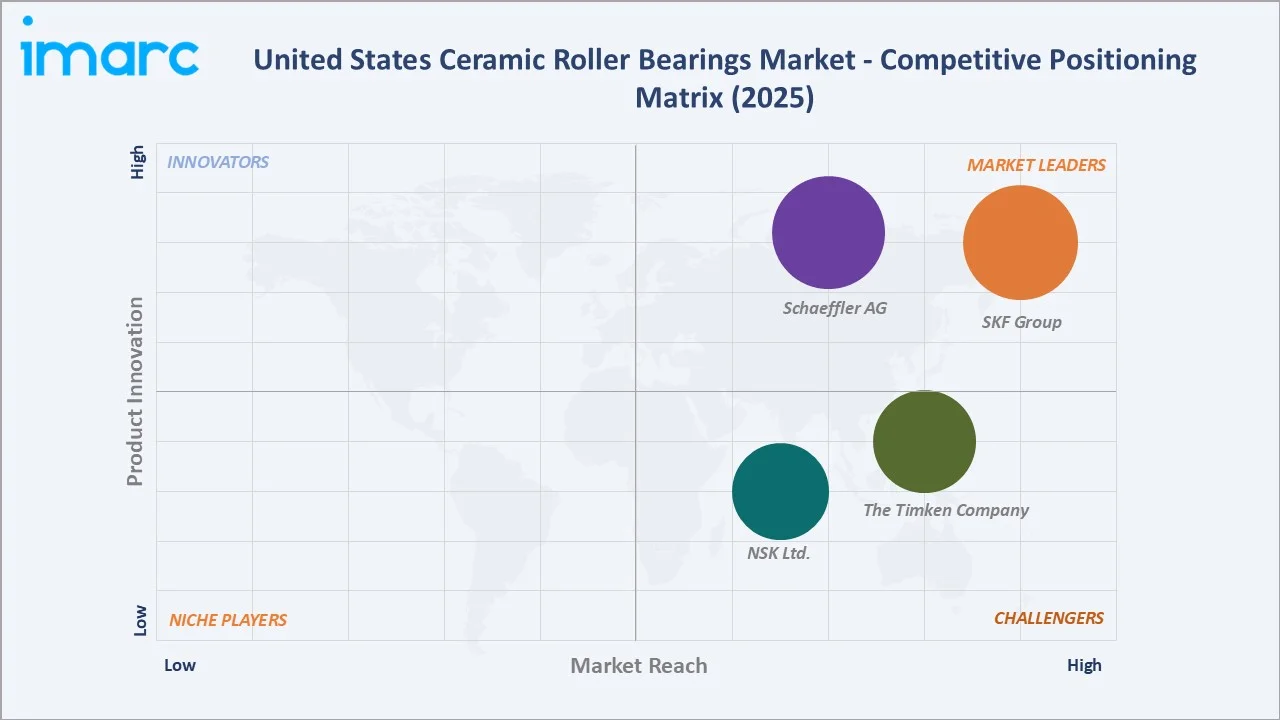

Competitive Landscape

The United States ceramic roller bearings market exhibits moderate-to-high concentration among global bearing majors and specialized ceramic bearing companies. Top players collectively account for approximately 55–60% of US market revenues in 2025, leveraging their broad bearing portfolios, OEM direct supply relationships, and established US distribution infrastructure.

|

Company Name |

Key Products/Brands |

Market Position |

Core Strength |

|

SKF Group |

Hybrid Ceramic Bearings, Hybrid Ceramic Cylindrical Roller Bearings |

Market Leader |

Global market reach, broadest hybrid ceramic bearing portfolio, and strong aerospace and industrial OEM relationships |

|

Schaeffler AG |

Schaeffler Hybrid Bearings, FAG Ceramic Bearing Series |

Market Leader |

Advanced material science capability, large US manufacturing footprint, and deep automotive and industrial customer base |

|

The Timken Company |

Timken Roller Bearings |

Strong Challenger |

US-headquartered leader, strong aerospace and defense customer relationships, and extensive industrial distribution network |

|

NSK Ltd. |

NSK Hybrid Bearings with Ceramic Balls |

Strong Challenger |

High-precision bearing expertise, strong semiconductor and medical applications, and competitive silicon nitride bearing technology |

The competitive dynamics of the market are shaped by the technical complexity of ceramic material selection and application engineering, the aerospace and defense sector’s qualification requirements creating significant new entrant barriers, and the OEM direct supply model that creates long-term customer relationships resistant to competitive displacement.

Key Company Profiles

SKF Group

SKF Group is one of the world’s largest bearing manufacturers and one of the global leaders in hybrid ceramic bearing technology for industrial and automotive applications. Its US operations through SKF USA Inc. serve the aerospace, wind energy, automotive, and industrial markets.

- Product Portfolio: Hybrid ceramic bearings and hybrid ceramic cylindrical roller bearings

- Recent Developments: In November 2025, SKF introduced ARCTIC15, a temperature-resistant and corrosion-tolerant bearing steel for next-generation aeroengine bearings. When paired with ceramic rolling elements, it supports smaller, lighter bearings with higher load, speed, and temperature capacity for more efficient aircraft engines.

- Strategic Focus: EV electrical insulation bearing market leadership; wind turbine main bearing ceramic hybrid upgrade programs; condition monitoring integration with ceramic bearing products; US manufacturing capacity for aerospace-qualified ceramic components.

Schaeffler AG

Schaeffler AG is a global rolling element bearing and motion technology company with significant US operations through its FAG bearing brand. Its ceramic bearing capability spans hybrid ceramic angular contact bearings for high-speed machine tool spindles through full ceramic bearings for chemical and pharmaceutical processing.

- Product Portfolio: FAG ceramic hybrid deep groove & angular contact bearings and Schaeffler hybrid bearings.

- Recent Developments: In September 2025, Schaeffler AG announced the expansion of its hybrid screw drive bearing range with three-row DKLFA bearings using ceramic rolling elements. The bearings improve reliability in short-stroke and oscillating applications by reducing false brinelling and premature bearing failures.

- Strategic Focus: EV drivetrain bearing technology development; wind energy main bearing solutions; aerospace supply chain qualification; digitally integrated smart bearing systems with embedded sensors.

Market Concentration Analysis

The US ceramic roller bearings market exhibits moderate-to-high concentration, with the top global bearing majors holding approximately 55–60% of domestic market revenue. The remaining 40–45% is distributed among specialty manufacturers, which serve specific application niches, prototype requirements, and aftermarket maintenance segments that the global majors do not prioritize for direct supply.

The US market’s concentration is reinforced by aerospace and defense qualification requirements, AS9100 certification, NADCAP special process approval for ceramic sintering, and military standard compliance for material traceability, which create significant barriers to new entrant competition in the highest-value market segments. This qualification moat sustains premium pricing for qualified ceramic bearing suppliers and limits the price-based competition that characterizes commodity industrial bearing markets.

Investment & Growth Opportunities

Fastest Growing Segments

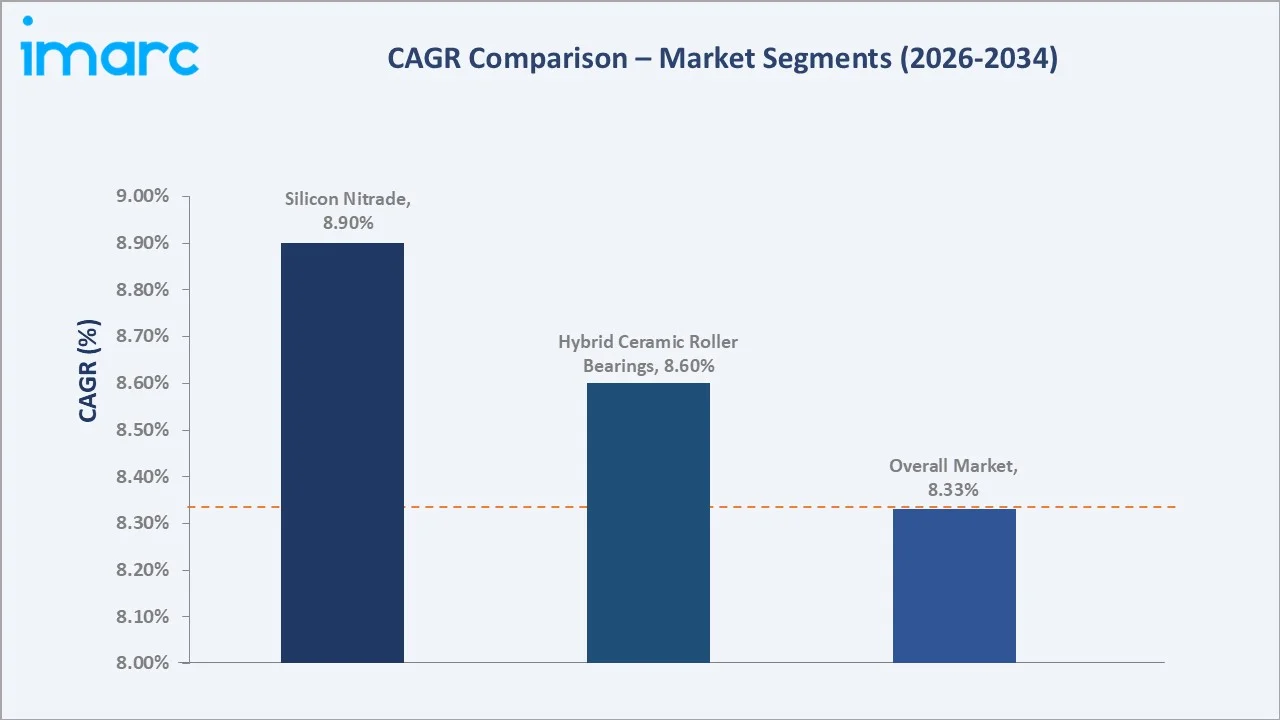

EV electrical insulation ceramic hybrid bearings (~12% CAGR), semiconductor fab ceramic bearing applications (~10% annual growth), and full ceramic bearing solutions for hydrogen system applications (~14% growth) represent the highest-growth investment vectors within the US ceramic roller bearings market through 2034. Wind energy main shaft bearing ceramic retrofit programs are sustaining steady above-market growth as the installed fleet ages toward replacement cycle milestones.

Near-Term Procurement Opportunities

The CHIPS Act semiconductor fab construction program represents the most concentrated near-term procurement opportunity, with multiple new 300mm wafer fabs under construction or planned across Arizona, Ohio, New York, and Texas that collectively require ceramic bearing procurement for hundreds of pieces of wafer handling and process equipment per facility. Combined ceramic bearing procurement across announced CHIPS Act-funded facilities is estimated at USD 15–25 Million over 2025–2030.

Technology Investment Trends

- Ceramic additive manufacturing for net-shape bearing component production is attracting R&D investment as a path to reducing the cost premium of complex full ceramic bearing designs, with binder jetting and photopolymerization of ceramic slurries progressively reducing the machining cost component of full ceramic bearing manufacturing.

- Smart ceramic bearing integration with IoT condition monitoring is attracting investment from major bearing companies seeking to differentiate through service offerings, including predictive maintenance subscriptions that provide recurring revenue beyond the initial hardware sale in wind energy and semiconductor applications.

- US domestic ceramic powder supply chain development is attracting strategic investment to reduce import dependence for silicon nitride precursor materials, with Department of Energy and Department of Defense funding supporting domestic silicon nitride and advanced ceramic production capacity as part of supply chain resilience programs.

Future Market Outlook (2026-2034)

The United States ceramic roller bearings market is positioned for strong and sustained growth through 2034. From USD 123.8 Million in 2025, the market is projected to reach USD 263.7 Million by 2034, representing total incremental value creation of USD 139.9 Million at a CAGR of 8.33%.

This growth is underpinned by the simultaneous expansion of multiple high-value application sectors, EV manufacturing, semiconductor fab construction, wind energy fleet aging and retrofit, and aerospace modernization, each of which creates non-discretionary ceramic bearing demand driven by performance requirements that steel alternatives cannot meet.

The technology composition of the market will evolve toward higher silicon nitride content as EV and semiconductor applications grow their share, while zirconium oxide maintains its position in chemical and medical applications. Full ceramic bearings will gain share relative to hybrid designs as additive manufacturing reduces their cost premium and hydrogen economy applications create new full ceramic bearing demand vectors.

The integration of smart sensing and condition monitoring within ceramic bearing assemblies will progressively transform the market from pure hardware supply toward hardware-plus-service models that provide higher recurring revenue and stronger customer retention.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 55 industry participants in 2024–2025, including ceramic roller bearing manufacturers, ceramic materials suppliers, bearing distributors, aerospace and defense OEM procurement engineers, wind energy operations managers, semiconductor equipment manufacturers, and industrial maintenance engineers. Expert input validated market sizing, segment growth rates, and regional demand estimates.

Secondary Research

Secondary research encompassed bearing company annual reports and investor presentations, American Bearing Manufacturers Association (ABMA) production statistics, Department of Energy wind energy technology reports, CHIPS Act facility announcements and procurement projections, aerospace industry MRO data, American Ceramic Society technical publications, and industry media, including Bearing News, Tribology International, and Machine Design.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating US industrial bearing market segmentation data, ceramic bearing penetration rate modelling by application category, end-user capital expenditure projections for aerospace, wind, semiconductor, and EV sectors, and average selling price trend analysis by ceramic material type.

United States Ceramic Roller Bearings Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

Silicon Nitride, Zirconium Oxide, Others |

| Product Types Covered |

Hybrid Ceramic Roller Bearings, Full Ceramic Roller Bearings |

| Applications Covered |

Automotive and Railways, Industrial and Mechanical Equipment, Power Generation, Aerospace, Others |

| Region Covered | Northeast, Midwest, South, West |

| Companies Covered | SKF Group, Schaeffler AG, The Timken Company, NSK Ltd.,etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Ceramic Roller Bearings Market Report

The United States ceramic roller bearings market reached USD 123.8 Million in 2025 and is projected to reach USD 263.7 Million by 2034.

The market is expected to grow at a CAGR of 8.33% during 2026-2034, driven by aerospace and defense demand, wind energy infrastructure expansion, EV drivetrain electrical insulation requirements, and semiconductor manufacturing growth.

The Midwest leads with a 33.4% share in 2025, driven by the highest concentration of US wind energy infrastructure, significant automotive and industrial manufacturing, and established aerospace and defense supply chain activity across the region.

Silicon nitride leads with a 58.4% share in 2025, reflecting its superior combination of high hardness, low density, fracture toughness, and thermal stability that makes it the standard ceramic material for demanding aerospace, wind energy, semiconductor, and EV bearing applications.

Hybrid ceramic roller bearings lead with a 72.6% share in 2025, reflecting their pragmatic balance of ceramic rolling element performance benefits with full dimensional interchangeability with standard steel bearing housings, minimizing OEM redesign requirements.

Some of the key players include SKF Group, Schaeffler AG, The Timken Company, and NSK Ltd.

Key drivers include aerospace and defense lightweighting requirements, wind turbine bearing replacement and upgrade demand to prevent electrical erosion, semiconductor manufacturing equipment ceramic bearing specifications, and chemical processing corrosion resistance needs.

Key opportunities include EV electrical insulation hybrid ceramic bearing supply, wind turbine main shaft bearing ceramic retrofit programs, aerospace ceramic bearing domestic supply qualification, and hydrogen system full ceramic bearing development.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)