United States Convenience Food Market Size, Share, Trends and Forecast by Type, Product, Distribution Channel, and Region, 2026-2034

United States Convenience Food Market Size and Share:

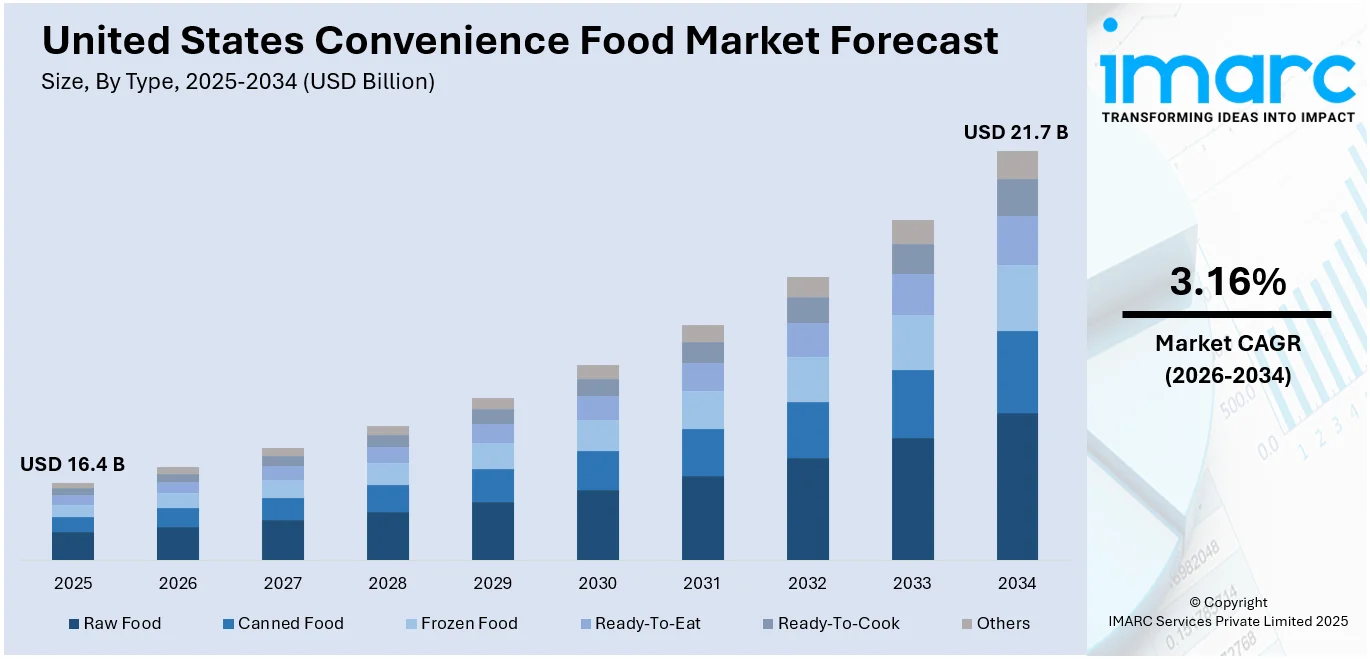

The United States convenience food market size was valued at USD 16.4 Billion in 2025. The market is projected to reach USD 21.7 Billion by 2034, exhibiting a CAGR of 3.16% from 2026-2034. The market is fueled by fast lives, accelerating need for ready-to-consume foods, and growing modern retail distribution. Demand for healthier, fast-preparation meals with nutritional benefits without compromising on convenience increasingly drives consumer choices. Advances in freezing, packaging, and online retailing further enhanced market reach and product variety. Local patterns of health-oriented decisions in the West and value-for-money in the Midwest influence consumption. These forces together are responsible for the growing United States convenience food market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 16.4 Billion |

| Market Forecast in 2034 | USD 21.7 Billion |

| Market Growth Rate (2026-2034) | 3.16% |

One of the major impetuses of the United States convenience food market is the consistent increase in dual-income households and single-person households. These trends have heavily impacted meal patterns, with numerous people turning to fast meal solutions because they do not have time to cook. With the changing configuration of American families, the demand for convenience foods such as ready-to-eat meals, heat-and-serve foods, and pre-packaged foods has grown simultaneously. Urbanization also adds to this trend, as long working hours, travel, and hectic lifestyles leave less room for home preparation of meals. Consumers are looking for food items that reduce preparation time without the loss of taste and variety. For instance, in July 2025, a US-based protein bar manufacturer ventured into the seafood space with frozen wild-caught Pacific cod fillets that were designed to provide a high-protein, low-processed alternative to conventional convenience foods. Moreover, this change toward convenience is also reinforced by the presence of varied products that cater to different culinary tastes and dietary requirements, which in turn enables consumers to incorporate such options into their daily lives. As a result, the market keeps growing as convenience becomes a key factor in food consumption.

To get more information on this market Request Sample

Another major driver of the United States convenience foods market trends is the spread of advanced retail infrastructure and online grocery platforms. The growth of supermarkets, hypermarkets, and web-based food delivery services has revolutionized access to a wide variety of convenience foods. Online retail, in fact, enables consumers to buy microwave meals, frozen foods, and ready-to-cook foods with the simple push of a button, raising the ease of acquisition to unprecedented levels. Contactless payment technologies, subscription meal kits, and planned deliveries further enhance this expansion. Furthermore, improvements in cold chain logistics have allowed manufacturers and retailers to preserve product freshness and shelf life while shipping over broader geographies. The ease of online shopping and on-demand food delivery has not only drawn technology-oriented consumers but also consumers in remote locations, where neighborhood stores might have inadequate supplies. This strong distribution channel helps fuel ongoing increases in product variety and availability, cementing the place of convenience foods in mainstream American eating habits. For example, in April 2025, Walker’s Shortbread, Synear Foods USA, and Pitaya Foods launched gluten-free shortbreads, dumplings, and organic frozen fruits, expanding offerings in the United States convenience food market.

United States Convenience Food Market Trends:

Growing Demand for Time-Saving Foods

The United States convenience food market growth is increasingly influenced by the hectic lifestyles of contemporary consumers, fueling demand for conveniently accessible and time-saving meal solutions. From microwaveable snacks and frozen dinners to canned soups and instant noodles, these products cater to people with less time for conventional meal preparation. Reflecting the trend towards convenience, consumers are opting for products that enable multitasking and minimize cooking time. In November 2024, Nestlé's USD 150 million expansion of its South Carolina frozen food plant is evidence of this trend. The initiative develops a new line of manufacturing targeted at single-serve frozen meals and introduces automation and digital technologies to improve productivity. The United States convenience food industry is therefore transforming as a result of rising urbanization and work-life demands, positioning itself as a critical enabler of efficiency and sustenance in daily American living.

Nutrition and Health Awareness Reshaping Offerings

Although convenience is still a key impetus for product design, increasingly there is consumer awareness about the nutritional consequences of ultra-processing. Convenience foods often utilize methods like freezing, drying, and packaging that prolong shelf life at the cost of adding preservatives, sodium, and sugar. This compromise has resulted in a noticeable trend in consumer demand towards products that provide speed and nutritional equilibrium. Health-oriented consumers now expect low-sodium, organic, gluten-free, and plant-based options within the convenience segment. Brands have set about reformulating current products or launching new products that respond to these requirements. Nissin Foods in June 2025 introduced Kanzen Meal, a nutrient-rich frozen meal specifically designed to address the dietary requirements of those taking GLP-1 weight loss medication. This is part of a wider trend in which the United States convenience food market outlook is being shaped by health-focused priorities, driving innovation in product design and ingredient choice.

Technological Innovation Enhancing Market Responsiveness

Technology is at the center of changing the face of convenience food manufacturing in the United States. Food companies are adopting digital technologies, automation, and intelligent systems to simplify operations, enhance consistency, and act rapidly in response to shifting consumer needs. Investments in cutting-edge equipment, including robot-driven assembly lines and real-time quality testing systems, enable mass production of customized, health-oriented, and single-serve meal alternatives. Similarly, Nestlé's investment in South Carolina indicates this technological shift, where an emphasis is placed on incorporating automated systems to increase the agility of production. Finally, firms are intensely using data analysis to monitor consumer patterns, making it possible for personalized marketing and product design strategies. With innovations such as nutrient optimization and artificial intelligence (AI) driven food formulation taking hold, the United States convenience food market is on the brink of long-term growth. Such innovations not only enhance efficiency but also enable the creation of products that keep up with evolving diet patterns and health objectives.

United States Convenience Food Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the United States convenience food market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on type, product, and distribution channel.

Analysis by Type:

- Raw Food

- Canned Food

- Frozen Food

- Ready-To-Eat

- Ready-To-Cook

- Others

Frozen food dominated the United States convenience food market with 35.6% share in 2025 because of its longer shelf life, convenience of storage, and extensive range of products. Convenience food consumers are increasingly turning towards frozen meals, vegetables, snacks, and breakfast products that can be easily heated and consumed without any preparation. The category is attractive to consumers looking for uniform meal quality and nutritional value, with freezing preserving food freshness without promoting artificial preservatives. The ease of use of frozen offerings also fits into busy lifestyles, especially among urban populations and working adults. In addition, advances in freezing technology and packaging have allowed for better flavor and texture preservation. The increasing demand for portion-controlled and balanced meals has also driven demand in this category, making frozen food a prime segment in the United States convenience food market's changing consumer behavior.

Analysis by Product:

- Meat/Poultry Products

- Cereal-based Products

- Vegetable-based Products

- Others

As per the United States convenience food market analysis, cereal-based products were the top product category in the market in 2025 due to their adaptability, nutritional values, and widespread acceptability among consumers. These include products like breakfast cereals, granola bars, instant oatmeal, and ready-to-eat grain-based meals, which are widely eaten in all age groups. They are popular because they can provide a mix of energy, fiber, and necessary nutrients in an easy-to-consume and convenient form. Especially in families with school-age children or professionals, cereal-based products provide a quick and guaranteed meal or snack option. The category also benefits from broad product innovation, including whole grain, low-sugar, fortified, and gluten-free variants, catering to health-conscious consumers. Their adaptability across different eating occasions—such as breakfast, mid-day snacks, or meal replacements—ensures sustained demand. As consumers prioritize convenience without compromising on health, cereal-based products continue to anchor growth within the United States convenience food market.

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Stores

- Others

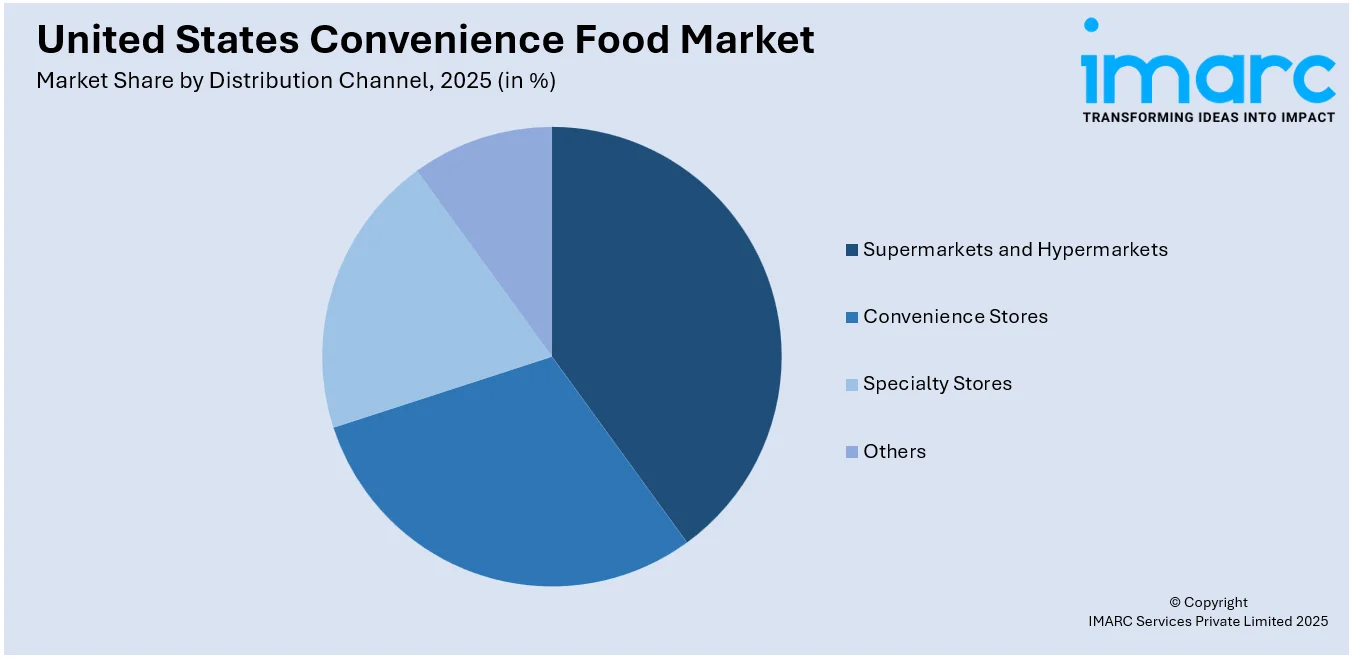

Supermarkets and hypermarkets were the leading distribution channel in the US convenience food industry, accounting for a 40.0% share in 2025. They provide consumers with a one-stop shopping facility, allowing them to get access to a variety of convenience food products under one roof. The attractiveness is based on the wider availability of products, well-laid-out shelving, and regular promotions that appeal to value- and quality-focused purchasers. Major chain retailers also have robust supplier relationships with guaranteed product inventory and turnaround of fresh stock. Visibility of new product introductions and sampling in stores helps drive awareness and trial among consumers for convenience food items. In addition, the in-store experience enables shoppers to examine product packaging and compare nutrition facts, which is critical for consumers with dietary needs. As supermarkets continue to advance with built-in digital services, including online shopping and curbside pickup, they remain at the forefront of the purchase dynamics around convenience food in the United States.

Regional Analysis:

- Northeast

- Midwest

- South

- West

The Northeast convenience food market is boosted by urbanization, hectic commuter lives, and high demand for swift eating. Portability and health are the concerns for the consumers in the region, leading to demand for ready-to-eat and microwaveable products, particularly those providing well-balanced nutrition and minimal preparation time.

In the Midwest, the market for convenience food enjoys broad availability of retail coverage and high demand for frozen and canned foods. Occupants tend to prefer affordable meals that are not difficult to prepare and are good for family dining, leading to popularity in multi-serve foods and long-life goods in rural and suburban regions.

The South registers strong growth in the convenience foods industry with increasing disposable incomes and a taste for added-value, ready-to-eat foods. Consumers become highly accepting of convenience products that blend local taste and convenience, especially in frozen and heat-and-serve meals for daily meal planning.

Western U.S. convenience food market is characterized by a health-focused consumer base and technologically savvy customers adopting online grocery shopping platforms. There is an increasing demand for organic, plant-based, and low-calorie ready meals, driven by regional tastes for healthy, sustainable, and convenient food solutions among urban and suburban consumers.

Competitive Landscape:

The United States convenience food market has a high level of competition characterized by fierce competition between traditional brands, regional producers, and emerging private labels. Firms are emphasizing product innovation, appealing to health-oriented consumers with low-sodium, organic, and plant-based varieties that address changing dietary requirements. Advances in freezing and packaging technology have made product preservation more effective, adding shelf life and quality. Private label products offered by retailers are growing at a fast pace, offering low-cost alternatives that appeal to budget-conscious consumers. Efficiency in distribution through supermarkets, hypermarkets, and digital platforms continues to remain a major differentiator, affecting consumer reach and brand visibility. Marketing strategies, such as loyalty programs and promotional pricing, are also influencing competitive forces. According to the United States convenience food market forecast, competition will continue to strengthen further, fueled by growing demand for healthy but time-saving food products. To remain competitive, companies are aligning their strategies with new consumer trends, prioritizing both convenience and nutritional content.

The report provides a comprehensive analysis of the competitive landscape in the United States convenience food market with detailed profiles of all major companies, including:

- Nestlé S.A.

- Unilever

- General Mills Inc.

- Conagra Brands, Inc.

- Hormel Foods Corporation

- The Kraft Heinz Company

- B&G Foods, Inc.

- Casey's General Stores, Inc.

- 7-Eleven, Inc.

- Alimentation Couche-Tard Inc.

Latest News and Developments:

- February 2025: Bonduelle announced a new line of ready-to-eat meals designed to appeal to "on-the-go eaters everywhere." The "Lunch Bowls" are made with 100% plant-powered ingredients and more than 10 grams of protein.

- June 2025: Nissin Foods is moving beyond the cup and into frozen foods with an offering aimed at GLP-1 users and other health-conscious consumers looking for nutrient-dense meals. Kanzen Meal is the Japanese company’s first U.S. innovation in the single-serve frozen meal category and one it hopes will fill a void in the freezer aisle.

- June 2025: Conagra Brands announced the launch of over 50 new frozen foods, which include vegetable side dishes, multi-serve and single-serve meals, and plant-based and gluten-free options. The new products will be available in convenience stores and e-commerce platforms starting June 2025, significantly expanding the company’s offerings.

- February 2025: Kellanova announced the launch of over 15 new snacks for U.S. convenience stores. The product lineup includes Pop-Tarts, Cheez-It, Rice Krispies Treats, and Pringles, enabling operators and retailers to fulfill customer demand and retain a competitive edge in the dynamic convenience snacks sector.

United States Convenience Food Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Raw Food, Canned Food, Frozen Food, Ready-To-Eat, Ready-To-Cook, Others |

| Products Covered | Meat/Poultry Products, Cereal-based Products, Vegetable-based Products, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Nestlé S.A., Unilever, General Mills Inc., Conagra Brands, Inc., Hormel Foods Corporation, The Kraft Heinz Company, B&G Foods, Inc., Casey's General Stores, Inc., 7-Eleven, Inc., Alimentation Couche-Tard Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States convenience food market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States convenience food market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States convenience food industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Convenience Food Market Report

The convenience food market in the region was valued at USD 16.4 Billion in 2025.

The United States convenience food market is projected to exhibit a CAGR of 3.16% during 2026-2034, reaching a value of USD 21.7 Billion by 2034.

United States convenience food business is mainly propelled by hurried lifestyles, growth in women's workforce participation, and expanding city populations. Growing demand for convenient-to-prepare foods, the advancement in freezing and packaging technology, and increased availability through supermarkets and online platforms also boosts steady market growth across the country.

Frozen food dominates the United States convenience food industry, with a 35.6% market share. Its long shelf life, extensive product range, and minimal preparation time drive its dominance. Consumers favor frozen food for convenience, affordability, and retention of flavor and nutrition when planning meals on a daily basis.

Some of the major players in the United States convenience food market include Nestlé S.A., Unilever, General Mills Inc., Conagra Brands, Inc., Hormel Foods Corporation, The Kraft Heinz Company, B&G Foods, Inc., Casey's General Stores, Inc., 7-Eleven, Inc., Alimentation Couche-Tard Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)