United States E-Bike Market Size, Share, Trends and Forecast by Mode, Motor Type, Battery Type, Class, Design, Application, and Region, 2026-2034

United States E-Bike Market Size, Share, Trends and Forecast (2026-2034)

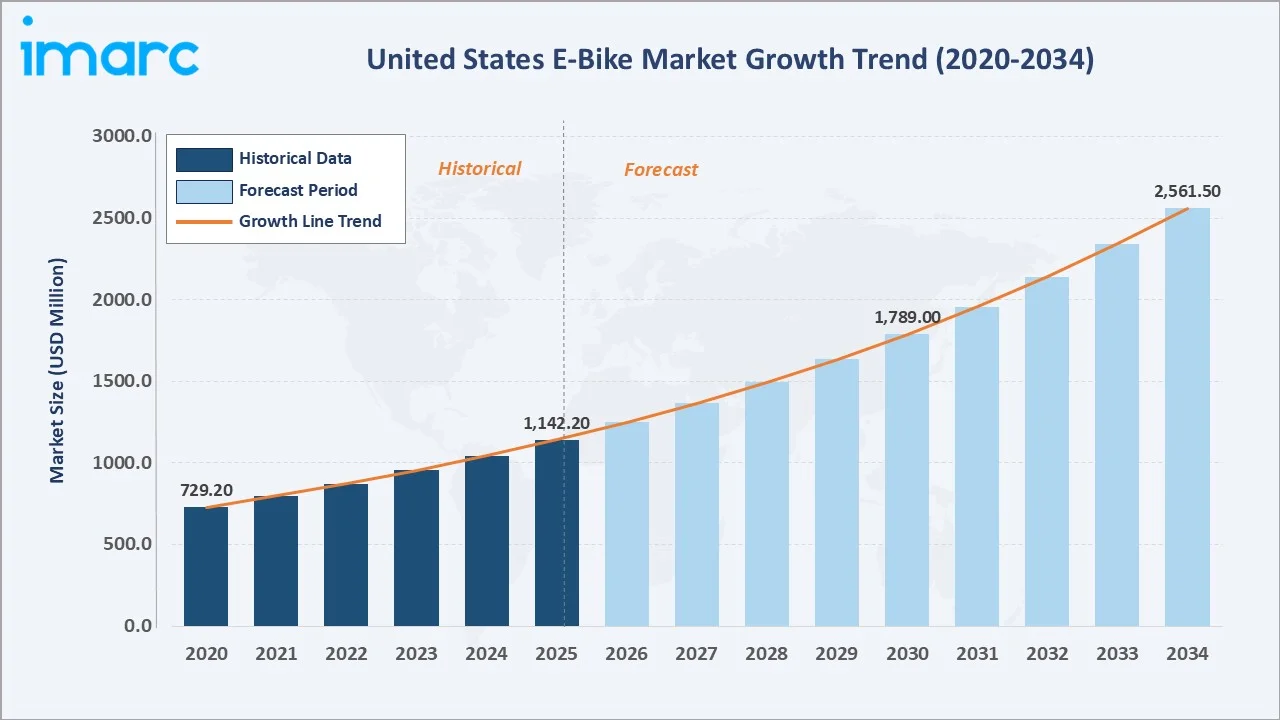

The United States e-bike market size was valued at USD 1,142.2 Million in 2025 and is projected to reach USD 2,561.5 Million by 2034, exhibiting a compound annual growth rate of 9.39% during the forecast period 2026-2034. The market is gaining strong momentum, propelled by rising environmental consciousness among urban consumers, escalating gasoline prices, and increasing government support through incentive programs and expanded cycling infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,142.2 Million |

|

Forecast Market Size (2034) |

USD 2,561.5 Million |

|

CAGR (2026-2034) |

9.39% |

|

Historical Period |

2020-2025 |

|

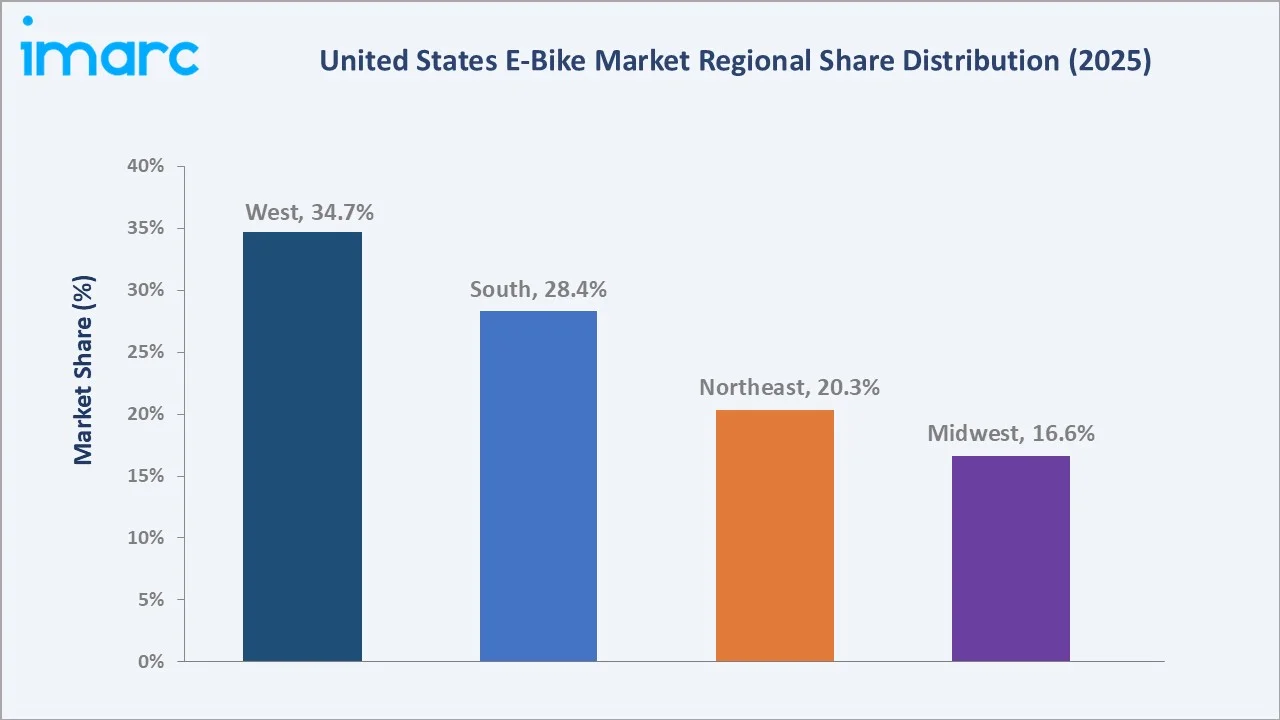

Largest Region (2025) |

West (34.7%) |

|

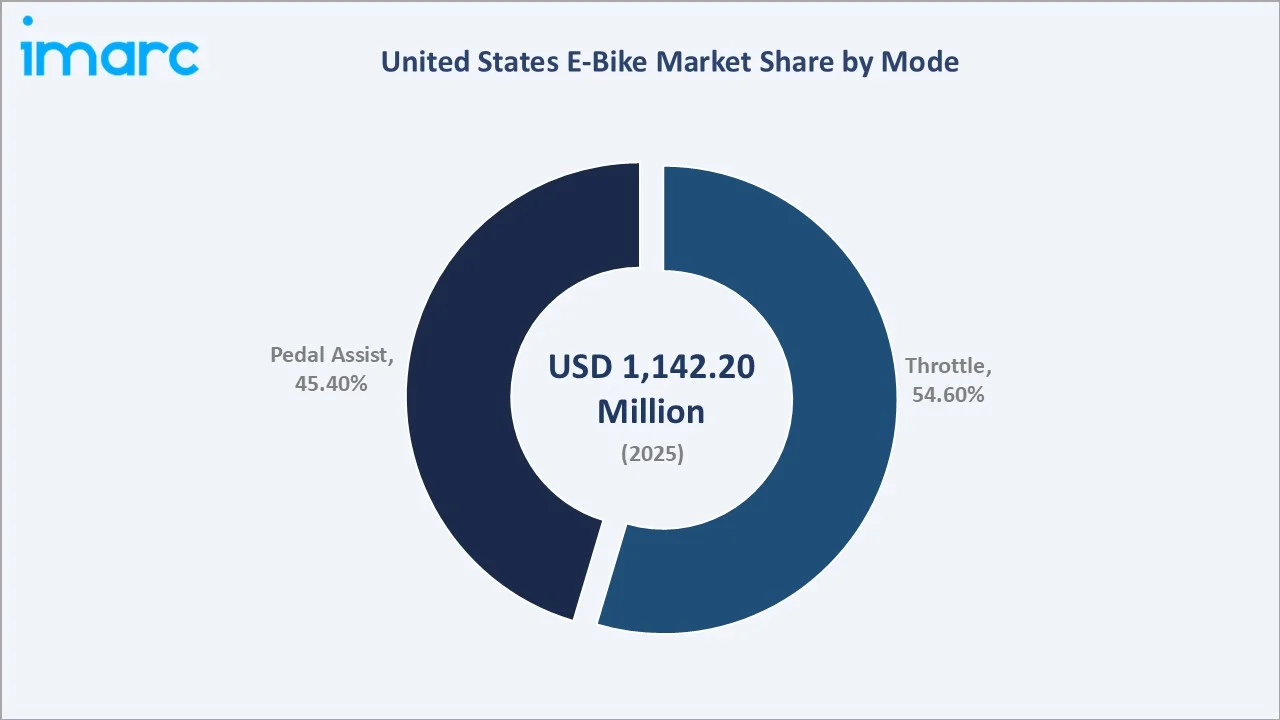

Leading Mode (2025) |

Throttle (54.6%) |

|

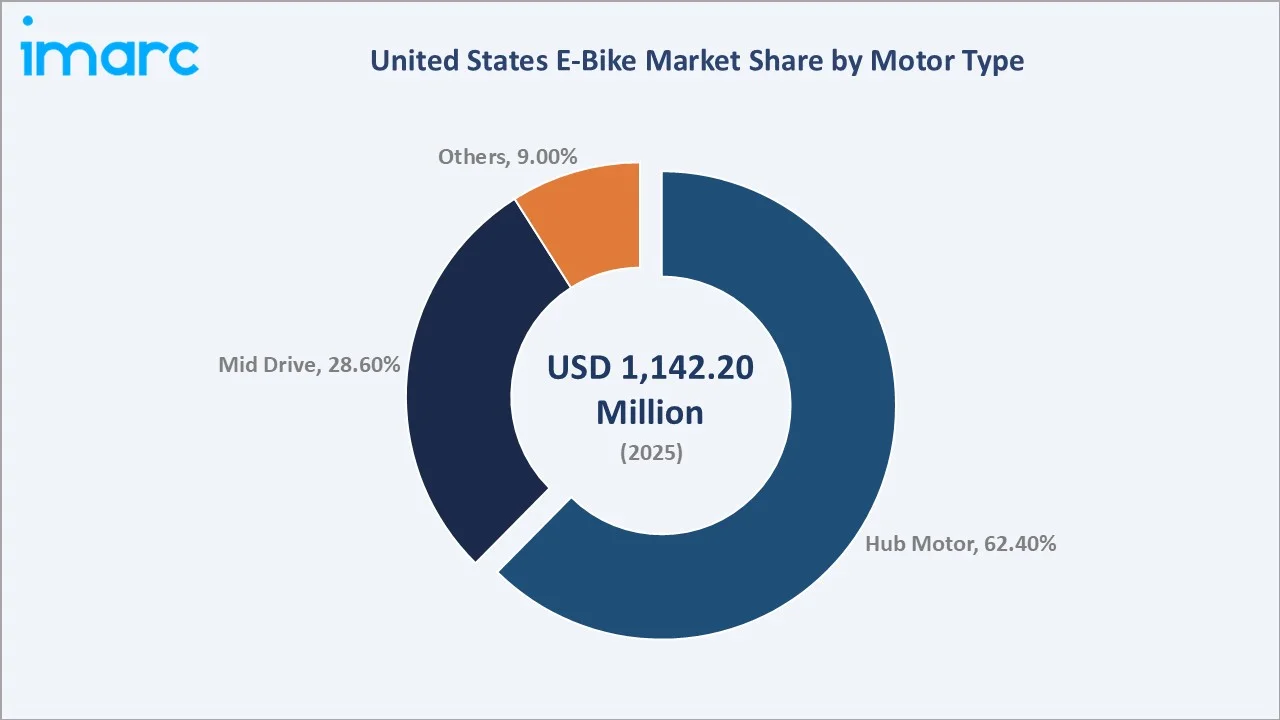

Leading Motor Type (2025) |

Hub Motor (62.4%) |

To get more information on this market, Request Sample

The 9.39% CAGR through 2034 positions the U.S. e-bike market as one of the fastest-growing segments within the broader transportation electrification landscape. Accelerating consumer shift away from gasoline-powered vehicles toward zero-emission alternatives, supported by state and federal incentive frameworks, is set to nearly double the market value from its 2025 base over the nine-year forecast horizon.

Executive Summary

The United States e-bike market reached USD 1,142.2 Million in 2025, propelled by a convergence of environmental awareness, infrastructure investment, and technological improvements across motor and battery systems. The market is projected to achieve USD 2,561.5 Million by 2034 at a CAGR of 9.39%. Key demand drivers include rising urban congestion, escalating fuel costs, and the rapid integration of e-bikes into last-mile logistics operations. Federal policy momentum, including proposed e-bike tax credit legislation, and state-level incentive programs in California, Colorado, and Vermont are augmenting consumer adoption across income segments.

By mode, throttle e-bikes lead with a 54.6% share in 2025, valued for their ease of use and strong adoption in delivery and utility applications. Hub motor configurations dominate the motor type segment at 62.4%, driven by lower costs and widespread compatibility across e-bike categories. Regionally, the West commands 34.7% of 2025 revenues, underpinned by California’s advanced subsidy ecosystem, dense cycling infrastructure, and high environmental consciousness. The competitive landscape is dynamic, with players including Trek Bicycle Corporation, Aventon Bikes, Lectric eBikes, Pedego Electric Bikes, Specialized Bicycle Components, Cannondale, and Segway-Ninebot continually expanding product lineups and distribution networks.

Key Market Insights

|

Insight |

Data |

|

Largest Mode Segment |

Throttle – 54.6% (2025) |

|

Largest Motor Type |

Hub Motor – 62.4% (2025) |

|

Leading Region |

West – 34.7% (2025) |

|

Market Size (2025) |

USD 1,142.2 Million |

|

Market Forecast (2034) |

USD 2,561.5 Million |

|

CAGR (2026-2034) |

9.39% |

|

Key Players |

Trek Bicycle Corporation, Aventon Bikes, Lectric eBikes, Pedego Electric Bikes, Accell Group, Giant Bicycles, Specialized Bicycle Components, Cannondale, Segway-Ninebot |

Key Analytical Observations Supporting the Above Data:

- Throttle’s 54.6% share (2025) reflects its dominant adoption in commercial delivery fleets and among casual riders who prefer full electric propulsion without pedaling requirements, positioning it as the core operational mode in the U.S. e-bike market.

- Hub Motor’s 62.4% lead (2025) is driven by its mechanically simple design, lower manufacturing cost, high compatibility across frame types, and proven reliability in both consumer and commercial applications.

- The West region’s 34.7% share reflects California’s leading position as the single largest state market, backed by advanced subsidy programs, dense cycling infrastructure, and a consumer base with high environmental consciousness and above-average e-bike spending.

United States E-Bike Market Overview

An e-bike is a bicycle equipped with an integrated electric motor and rechargeable battery system that assists rider propulsion. The U.S. e-bike market has evolved from a niche recreational segment to a mainstream mobility solution, now spanning commuter, cargo, recreational, and last-mile delivery applications. Peter Woolery from Bicycle Market Research estimates the industry imported 1.3 million e-bikes last year. Meanwhile, the Light Electric Vehicle Association and eCycleElectric Consultants put the number much higher: 2.2 million e-bikes.

At present, rising concerns about the environment and the need to reduce carbon emissions are encouraging people in the United States to adopt greener transportation options like e-bikes. High fuel prices are making electric bikes a more affordable and practical choice for daily commuting. High urbanization and increasing traffic congestion are leading city dwellers to seek faster and more efficient ways to move around. As per estimates, 83% of the U.S. population lives in urban areas, up from 64% in 1950. By 2050, 89% of the U.S. population and 68% of the world population is projected to live in urban areas, creating sustained demand for efficient micromobility solutions. Innovations in battery technology, motor efficiency, smart connectivity features, and expanding e-commerce access are collectively propelling the United States e-bike market growth.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

- Rising Environmental Consciousness and Government Policy Support: Growing environmental awareness is reshaping U.S. transportation preferences. In United States, total emissions in 2022 were 6,343.2 Million Metric Tons of CO₂ equivalent. In April 2025, Washington State’s WE-Bike initiative provided immediate rebates during a two-week window to encourage e-bike usage, exemplifying the expanding state-level incentive ecosystem. Federal proposals, including the Electric Bicycle Incentive Kickstart for the Environment (E-BIKE) Act, signal growing national-level commitment to subsidizing adoption, which is expected to significantly expand the addressable consumer base during the forecast period.

- Escalating Fuel Costs and Urban Mobility Demand: Rising gasoline prices are making e-bikes an economically attractive alternative for daily commuting. The national average gas price reached USD 3.50 per gallon in March 2024, up USD 0.26 from February 2024, reinforcing the cost-per-mile advantage of electric two-wheelers. High urbanization rates, coupled with persistent traffic congestion in major metropolitan areas such as New York, Los Angeles, and San Francisco, are amplifying demand for agile mobility solutions. E-bikes enable riders to navigate congested corridors and utilize cycling infrastructure unavailable to automobiles, offering measurable time and cost savings for daily commuters.

- Technological Advancements in Battery Systems and Motor Efficiency: Rapid innovation in lithium-ion battery chemistry, mid-drive motor design, and smart connectivity is enhancing e-bike performance, range, and user experience. In January 2025, Bosch eBike Systems launched its Smart System in the U.S. market, integrating real-time tracking, anti-theft technology, and performance tuning via smartphone. In February 2025, Trek has introduced two new electric mountain bikes, the Rail+ G5 and the Powerfly FS+ 4, both designed to push performance limits with improved power, range, and versatility.

Market Restraints

- Limited and Inconsistent Cycling Infrastructure: The uneven development of cycling infrastructure across U.S. regions creates significant variability in e-bike adoption. Many suburban and rural communities lack dedicated bike lanes, safe crossing facilities, or secure parking, limiting practical e-bike usability and dampening market penetration outside of cycling-progressive urban centers.

- High Upfront Acquisition Costs: The upfront purchase price of quality e-bikes remains significantly higher than conventional bicycles. The starting price range can be $1,500-$2,500 with options that can go much higher. The average price of an e-bike is about $2,000. Entry-level electric bikes are about $1,000. High-end e-bikes can cost $6,000 or more. This cost barrier limits adoption among lower-income consumer segments and price-sensitive buyers, particularly in the absence of accessible financing options or sufficient incentive coverage at the state level.

- Regulatory Fragmentation and Safety Concerns: E-bike regulatory classification varies materially across U.S. states, creating inconsistency in permitted use, speed limits, and access rights. Battery fire safety concerns for lower-cost imported e-bikes have attracted regulatory scrutiny in major cities, representing a growing risk dimension that manufacturers must manage as market scale increases.

Market Opportunities

- Last-Mile Delivery Integration: Growing e-commerce volumes and urban delivery demand are creating large addressable opportunities for cargo and utility e-bikes in commercial fleet applications. Rad Power Bikes’June 2025 partnership with Uber Eats to deploy commercial-grade cargo e-bikes for delivery riders across major U.S. cities validated the structural opportunity in this segment.

- E-Bike Sharing and Subscription Models: Urban bike-sharing programs and subscription services such as Upway’s Flex lease-to-own program are reducing the upfront cost barrier, expanding the addressable market to cost-sensitive consumers and occasional users who benefit from flexible, low-commitment access.

- Smart Connectivity and Premium Features: Growing consumer demand for GPS tracking, anti-theft systems, health monitoring integration, and smartphone-connected riding experiences is creating premium product tier opportunities and supporting higher average selling prices across both consumer and commercial segments.

Market Challenges

- High Initial Purchase Cost and Price Sensitivity: Premium e-bikes in the U.S. typically range between $1,500 and $5,000, creating a significant entry barrier for mass-market consumers. While operating costs are lower than cars, the upfront investment limits adoption among price-sensitive segments. The removal or inconsistency of state-level subsidies has further slowed adoption momentum in certain regions.

- Regulatory Fragmentation and Safety Concerns: The U.S. e-bike market faces a patchwork of state and city-level regulations regarding speed limits, throttle use, and bike lane access. This lack of regulatory standardization creates confusion for consumers and manufacturers. Additionally, rising concerns around battery safety (including lithium-ion fire risks) and accidents in urban areas are increasing scrutiny and may lead to tighter regulations.

- Supply Chain Constraints and Component Dependency: The market remains dependent on imported components, particularly batteries and motors from Asia. Disruptions in global supply chains, along with tariffs on Chinese imports, have led to cost pressures and longer lead times. This dependency limits domestic manufacturing scalability and exposes companies to geopolitical and trade-related risks.

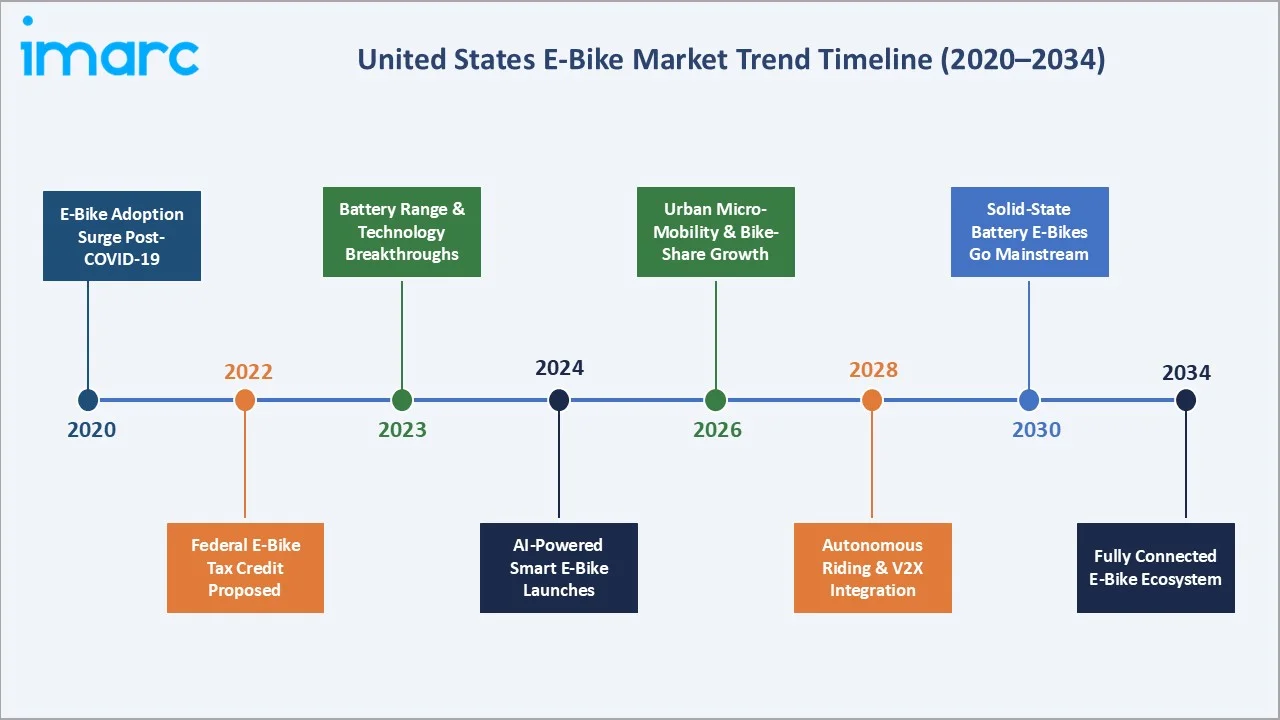

Emerging Market Trends

1. Rising Environmental Consciousness and Sustainable Mobility Adoption

Growing environmental awareness is fundamentally driving consumer preference toward zero-emission transportation. Urban residents in major U.S. cities are increasingly incorporating e-bikes into daily commuting routines as awareness of vehicle carbon contributions rises. More than 1.1 million electric bicycles were sold in the United States in 2022, reflecting the accelerating cultural shift toward clean urban mobility.

2. Expansion of Smart, Connected E-Bike Technology

Consumer demand for smart features is reshaping product development priorities across the e-bike industry. GPS tracking, real-time diagnostics, anti-theft alerts, and app-based performance tuning have transitioned from premium differentiators to increasingly standard features. In March 2026, Bosch eBike Systems has introduced a new digital solution called the Connected Biking platform, designed to expand and streamline services across the e-bike ecosystem. The platform allows various stakeholders, to build and integrate their own digital services directly into Bosch’s system. Smart connectivity is enhancing the consumer value proposition, reducing range anxiety, improving theft deterrence, and enabling personalized riding profiles across both urban commuting and recreational segments.

3. Growth of E-Bikes in Commercial Last-Mile Delivery

The rapid expansion of e-commerce and urban delivery services is creating structural demand for cargo and utility e-bikes as cost-effective, low-emission alternatives to motorized delivery vehicles. In March 2026, Connected Cycle has partnered with Bosch eBike Systems to deliver advanced fleet management capabilities for e-bikes. Through this collaboration, Connected Cycle’s software can now integrate directly with Bosch’s Smart System and ConnectModule, enabling operators to monitor and manage their e-bike fleets more effectively. This commercial adoption wave is expanding the e-bike market beyond personal use into large-fleet procurement, opening a structurally distinct demand channel with different product specifications and purchasing dynamics.

Industry Value Chain Analysis

The U.S. e-bikes market value chain consists of six interconnected stages, spanning from component sourcing to end-user adoption. Each stage requires specialized capabilities in engineering, assembly, distribution, and digital integration to deliver performance, reliability, and user experience expected in premium electric mobility solutions.

|

Stage |

Key Activities |

Representative Players |

|

Raw Material & Component Sourcing |

Lithium-ion battery cells, motors, semiconductors, aluminum frames, drivetrains |

Panasonic (batteries), Samsung SDI, Bosch eBike Systems |

|

Component Manufacturing |

Battery pack assembly, motor systems, controllers, sensors, drivetrain integration |

Bosch, Bafang, Yamaha Motor |

|

E-Bike OEM Assembly |

Design, frame integration, electronics integration, quality testing |

Trek, Specialized, Aventon |

|

Distribution & Retail |

Dealer networks, D2C online sales, specialty bike shops, big-box retail |

REI, Walmart, brand websites, independent bike dealers |

|

After-Sales & Services |

Maintenance, battery replacement, software updates, warranty services |

Local bike shops, brand service centers, mobile repair services |

|

End Consumers |

Commuters, recreational riders, delivery workers, fleet operators |

Urban commuters, gig economy riders, fitness users |

The franchise and brand operations stage is the primary value creation point, it is where product formulation, consumer experience design, and brand equity are built. Leading franchise operators including Gong Cha and Tiger Sugar invest heavily in proprietary recipe development, outlet design aesthetics, and staff training to create premium, Instagrammable product experiences that command price premiums of 20–40% over commodity bubble tea competitors.

Technology Landscape in the US E-Bike Industry

Battery and Powertrain Innovation

Advancements in lithium-ion battery technology are central to the e-bike market, focusing on improving energy density, charging speed, and lifecycle performance. Leading suppliers such as Bosch eBike Systems and Shimano are developing integrated motor-drive systems that enhance torque efficiency, range optimization, and riding smoothness.

Smart Connectivity and Digital Integration

Smart features such as GPS tracking, anti-theft systems, and smartphone connectivity are becoming standard in premium e-bikes, significantly enhancing user experience and product differentiation. Companies like Specialized Bicycle Components are investing in connected ecosystems that allow riders to monitor performance, customize settings, and access predictive maintenance, driving higher customer engagement and brand loyalty.

Fleet and Commercial Use Technology

The growth of e-bikes in last-mile delivery and logistics is accelerating the adoption of fleet management technologies integrated with platforms like Uber Eats. These systems enable real-time tracking, route optimization, and performance monitoring, helping operators improve efficiency, reduce downtime, and scale commercial deployments in urban markets.

United States E-Bike Market Report Segmentation

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Mode |

Throttle |

54.6% |

2025 |

|

Motor Type |

Hub Motor |

62.4% |

2025 |

|

Battery Type |

Lithium Ion |

🔒 |

2025 |

|

Class |

Class I |

🔒 |

2025 |

|

Design |

🔒 |

🔒 |

2025 |

|

Application |

City/Urban |

🔒 |

2025 |

|

Region |

West |

34.7% |

2025 |

By Mode

To access detailed market analysis, Request Sample

Throttle leads the market with a 54.6% share in 2025, driven by its strong adoption in delivery, utility, and casual commuting applications.

Throttle-assisted e-bikes command 54.6% of the U.S. e-bike market in 2025, reflecting their broad appeal among riders who prefer motorized assistance without the requirement of simultaneous pedaling. Throttle models are particularly favored in the delivery and logistics sector, where rider energy conservation over extended shift durations is a key operational requirement.

Pedal-assist e-bikes account for 45.4% of the 2025 market, holding strong appeal among fitness-oriented commuters and recreational riders who seek to combine exercise with electric assistance. Pedal-assist systems, particularly torque-sensing variants, deliver a more natural and intuitive cycling experience that closely replicates conventional cycling dynamics.

By Motor Type

Hub Motor is the largest segment, accounting for 62.4% of the market in 2025, owing to its cost efficiency, low maintenance profile, and broad compatibility across e-bike categories.

Hub motors dominate the U.S. e-bike motor type segment with a 62.4% share in 2025. These motors are integrated directly into the front or rear wheel hub, offering a mechanically simple, low-maintenance drivetrain configuration that is compatible with the widest range of e-bike frame designs and component choices. Lectric eBikes’ December 2024 opening of a new manufacturing and assembly plant in Phoenix, Arizona, to meet surging domestic demand, with hub motor-equipped models forming the core of their value-focused product portfolio, exemplifies the segment’s commercial significance.

Mid-drive motors hold a 28.6% share in 2025, occupying a premium market position valued by performance-oriented riders, mountain bikers, and enthusiasts who prioritize handling dynamics and terrain versatility. Trek’s updated Rail and Powerfly electric mountain bikes, launched in September 2024 with the new Bosch CX motor, exemplify continued investment in premium mid-drive e-bike performance. The Others segment, comprising friction drives and less common motor configurations, accounts for 9.0% of the 2025 market, serving niche applications including retrofit conversions and specialized mobility categories.

Regional Insights

The West holds the largest regional share at 34.7% in 2025, anchored by California’s advanced e-bike incentive ecosystem, high urbanization density, and strong environmental consciousness among residents. The California Department of Finance currently projects that the state’s population will reach 39.7 million in 2030, and 40.5 million by 2040. California’s population is the twelfth youngest in the nation. The median age in California is 38.4, compared to 39.2 nationwide, according to the 2024 American Community Survey. This population increase will lead to more demand of e-bikes among the younger group.

The South represents 28.4% of the 2025 market, driven by a large and growing population base across Texas, Florida, and the Carolinas, combined with accelerating investment in urban cycling infrastructure in metropolitan areas such as Austin, Miami, and Charlotte.

Competitive Landscape

The United States e-bike market features a dynamic and increasingly competitive landscape comprising global bicycle manufacturers, direct-to-consumer brands, and emerging technology-focused entrants. Leading players including Trek Bicycle Corporation, Giant Bicycles, Aventon Bikes, Lectric eBikes, Pedego Electric Bikes, Accell Group, Specialized Bicycle Components, Cannondale, and Segway-Ninebot are competing across price tiers, product categories, and distribution channels.

|

Company |

Market Position |

Primary Strategy |

|

Trek Bicycle Corporation |

Global Premium Leader |

Broad product range, premium performance, extensive dealer network |

|

Aventon Bikes |

Mid-Market Challenger |

Sleek design, aggressive marketing, commuter and cruiser segments |

|

Lectric eBikes |

Value Leader |

US-based DTC operations, headquartered in Phoenix |

|

Pedego Electric Bikes |

Retail Network Leader |

Community retail |

|

Accell Group |

Global Scale Player |

Multi-brand portfolio, international manufacturing, broad category coverage |

|

Giant Bicycles |

Manufacturing Leader |

Vertical integration, cost efficiency, broad range from entry to premium |

|

Specialized Bicycle Components |

Premium Performance |

Innovation-led, premium mountain and road e-bike categories, dealer-first |

|

Cannondale |

Premium Heritage Brand |

Performance innovation, e-MTB segment, Pon Holdings portfolio |

|

Segway-Ninebot |

Technology Innovator |

Smart integration, futuristic design (Xafari/Xyber, 2025), U.S. dealer build-out |

The key players include Trek Bicycle Corporation, Aventon Bikes, Lectric eBikes, Pedego Electric Bikes, Accell Group, Giant Bicycles, Specialized Bicycle Components, Cannondale, Segway-Ninebot, and others.

Key Company Profiles

Trek Bicycle Corporation

Trek Bicycle Corporation is one of the largest and most established bicycle manufacturers in the United States, with a strong presence in the premium e-bike segment. Founded in 1976 and headquartered in Wisconsin, the company has built a global reputation for high-performance bicycles and advanced engineering capabilities.

- Product Portfolio: Performance e-bikes, commuter e-bikes, mountain e-bikes (e-MTB), road e-bikes, and hybrid electric bikes under brands such as Allant+, Verve+, and Rail series.

- Strategic Focus: Premium product innovation, strong dealer network expansion, sustainability initiatives, and leadership in performance-oriented e-bike categories.

Aventon Bikes

Aventon Bikes is a fast-growing U.S.-based e-bike brand recognized for combining performance, design, and affordability. Founded in California, the company has rapidly expanded through a hybrid distribution model that includes both direct-to-consumer sales and retail partnerships.

- Product Portfolio: Commuter e-bikes, fat tire e-bikes, folding e-bikes, and urban mobility solutions, including popular models such as Pace, Level, and Aventure series.

- Recent Developments: In March 2026, Aventon introduced its new high-performance full-suspension electric mountain bike, featuring an advanced mid-drive motor system and a large 800 Wh battery capable of delivering up to 169 km of range on a single charge. The model is designed to combine trail-ready performance, strong torque output, and integrated smart features, positioning it competitively within the premium e-MTB segment.

- Strategic Focus: Omnichannel retail strategy, product innovation with smart features, competitive pricing, and expansion into mainstream urban mobility segments.

Lectric eBikes

Lectric eBikes is one of the fastest-growing e-bike companies in the U.S., known for its aggressively priced, foldable electric bikes targeting mass-market consumers. Founded in 2018, the company has gained significant traction through its value-driven approach and online-first sales model.

- Product Portfolio: Foldable e-bikes, commuter e-bikes, and lightweight urban electric bikes, with flagship models such as the XP series designed for affordability and convenience.

- Recent Developments: In November 2024, Lectric eBikes introduced upgraded features for its off-road model, enhancing performance and durability while maintaining the existing price point. The updated model incorporates improvements aimed at delivering better riding capability and value, reinforcing the company’s focus on affordable, high-performance e-bikes.

- Strategic Focus: Cost leadership, direct-to-consumer sales, simplified product lineup, and targeting first-time e-bike buyers with accessible pricing.

Market Concentration Analysis

The U.S. e-bikes market is moderately fragmented at the brand and distribution level, with a mix of direct-to-consumer (D2C) brands, legacy bicycle manufacturers, and independent retailers operating across the value chain. A significant portion of sales is driven by regional bike shops and online-first brands, creating a competitive but decentralized market structure.

In mature urban markets such as California, New York, and Texas, market concentration is higher within premium and performance segments, where established players like Trek Bicycle Corporation and Specialized Bicycle Components command strong brand recognition and pricing power. These companies benefit from robust dealer networks, advanced product engineering, and strong after-sales support. In contrast, price-sensitive and entry-level segments remain highly fragmented, with numerous emerging D2C brands and imports competing aggressively on price.

Consolidation at the brand and distribution level is expected to accelerate through 2034, driven by increasing competition, margin pressures, and the need for scale in procurement and technology integration. Larger players are likely to acquire smaller brands or form strategic partnerships to expand market share, while retailers may consolidate to strengthen service networks and customer reach.

Investment & Growth Opportunities

Fastest Growing Segments

Cargo e-bikes, commuter e-bikes, and subscription-based ownership models represent the highest-growth segments through 2034. These categories are benefiting from rising urban congestion, increasing fuel costs, and growing adoption of sustainable mobility solutions. Cargo e-bikes, in particular, are gaining traction in last-mile delivery and commercial fleet applications, addressing a rapidly expanding urban logistics market.

Emerging Market Expansion

Urban and suburban regions across the U.S. present strong growth opportunities, particularly in cities investing in cycling infrastructure and sustainability initiatives. States such as California, Colorado, and New York are leading adoption due to supportive policies, incentives, and developed bike lane networks. Additionally, mid-sized cities are emerging as high-growth markets as consumers seek cost-effective and flexible transportation alternatives to cars.

Technology and Innovation Investment Trends

- Battery manufacturers and motor system providers such as Bosch eBike Systems and Shimano are witnessing strong demand as brands prioritize performance, range, and reliability improvements.

- Direct-to-consumer e-bike brands and subscription platforms are attracting investment by lowering entry barriers and offering flexible ownership models, expanding access to a broader consumer base.

- Digital platforms, including ride-tracking apps, fleet management systems, and connected mobility solutions, are becoming critical for both consumer engagement and commercial fleet optimization, driving increased investment in software and IoT integration.

Future Market Outlook (2026-2034)

The U.S. e-bikes market is expected to experience sustained, infrastructure-driven growth through 2034, supported by increasing urbanization, rising environmental awareness, and a shift toward alternative mobility solutions. Demand will continue to expand across commuter, recreational, and commercial use cases, particularly as cities invest in bike-friendly infrastructure and policies that support electrified transport.

Product innovation and technology integration will be the primary competitive differentiators. Companies that successfully balance performance, affordability, and smart connectivity features will capture the broadest consumer base. The evolution of e-bikes into connected, software-enabled mobility devices—featuring advanced battery systems, IoT integration, and subscription-based ownership—represents a key growth frontier.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 150 industry participants in 2024–2025, comprising bubble tea franchise operators, ingredient and equipment suppliers, retail buyers, food service distributors, and end consumers across Asia Pacific, North America, Europe, and the Middle East.

Secondary Research

Secondary research encompassed a comprehensive review of company press releases, franchise disclosure documents, trade publications (QSR Magazine, Food Business News, Nation's Restaurant News), industry databases (Euromonitor, Mintel), and publicly available market data including government trade statistics and tea industry association reports. Over 250 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of bottom-up outlet count and average revenue per outlet modeling, combined with top-down consumer expenditure analysis incorporating tea consumption data, café culture penetration rates, and social media trend analytics.

United States E-Bike Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Modes Covered | Throttle, Pedal Assist |

| Motor Types Covered | Hub Motor, Mid Drive, Others |

| Battery Types Covered | Lead Acid, Lithium Ion, Nickel-Metal Hydride (Nimh), Others |

| Classes Covered | Class I, Class II, Class III |

| Designs Covered | Foldable, Non-Foldable |

| Applications Covered | Mountain/Trekking Bikes, City/Urban, Cargo, Others |

| Key Companies | Trek Bicycle Corporation, Aventon Bikes, Lectric eBikes, Pedego Electric Bikes, Accell Group, Giant Bicycles, Specialized Bicycle Components, Cannondale, Segway-Ninebot |

| Regions Covered | Northeast, Midwest, South, West |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States e-bike market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the United States e-bike market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States e-bike industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States E-Bike Market Report

The United States e-bike market size was valued at USD 1,142.2 Million in 2025.

The market is expected to grow at a compound annual growth rate of 9.39% from 2026 to 2034, reaching USD 2,561.5 Million by 2034.

Throttle mode, holding the largest revenue share of 54.6% in 2025, is widely adopted for delivery and utility applications given its ease of use and accessible price points, and remains the dominant operating mode across the U.S. e-bike market.

Key drivers include rising environmental consciousness, escalating fuel costs, supportive government incentive programs, expanding cycling infrastructure, technological advancements in battery and motor systems, and growing commercial adoption in last-mile delivery logistics.

Major challenges include inconsistent cycling infrastructure across regions, high upfront acquisition costs limiting mass-market penetration, regulatory fragmentation across U.S. states regarding e-bike classification, and battery safety concerns attracting municipal regulatory scrutiny in major urban centers.

Key opportunities include the expansion of cargo e-bikes for last-mile delivery, growing demand for sustainable urban mobility solutions, increasing adoption in suburban commuting, and the rise of subscription and leasing models that lower upfront costs and expand consumer access.

Key limiting factors include high initial purchase costs, lack of standardized regulations across states, uneven cycling infrastructure in non-urban areas, and concerns around battery safety and theft, which continue to impact consumer confidence.

Some of the key players include Trek Bicycle Corporation, Aventon Bikes, Lectric eBikes, Pedego Electric Bikes, Accell Group, Giant Bicycles, Specialized Bicycle Components, Cannondale, and Segway-Ninebot.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)