United States Handicrafts Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, End Use, and Region, 2026-2034

United States Handicrafts Market Size, Share, Trends & Forecast (2026-2034)

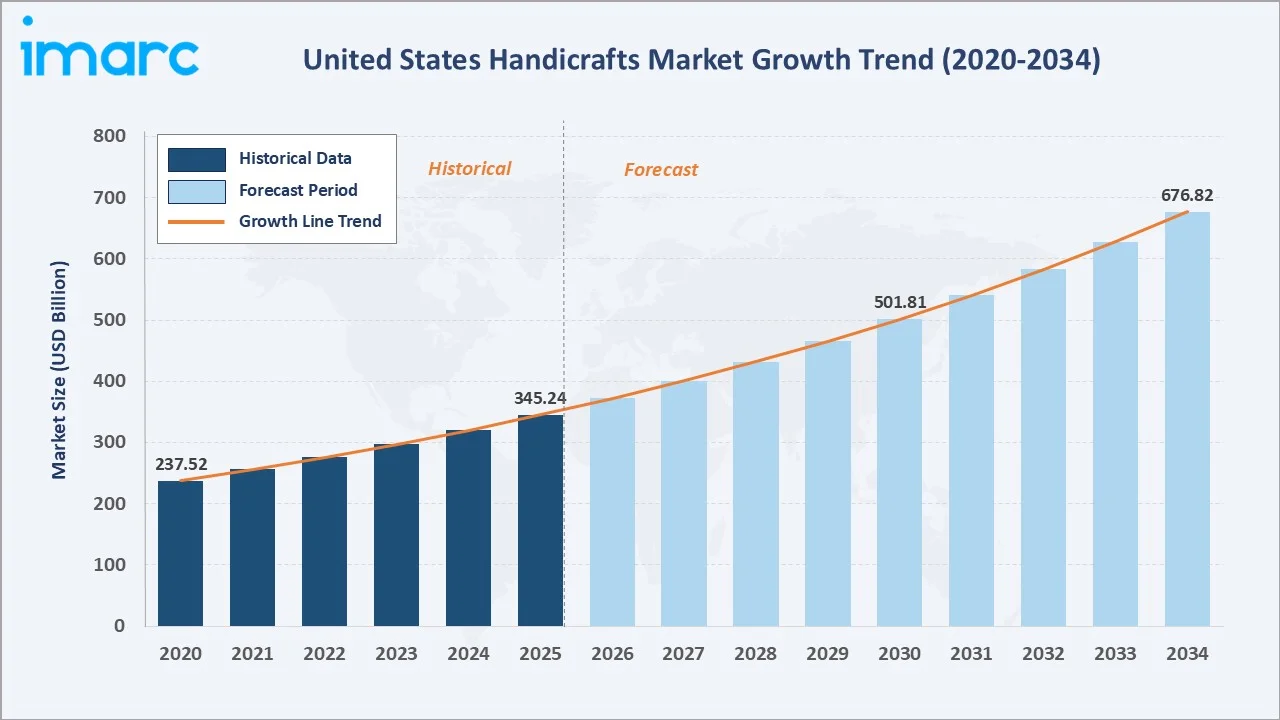

The United States handicrafts market reached USD 345.24 Billion in 2025 and is projected to reach USD 676.82 Billion by 2034, growing at a CAGR of 7.77% during 2026-2034. A resurgent DIY culture, surging e-commerce adoption, and growing consumer preference for unique, handmade, and artisan products are the primary growth engines.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 345.24 Billion |

|

Forecast Market Size (2034) |

USD 676.82 Billion |

|

CAGR (2026-2034) |

7.77% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South (31.0% share, 2025) |

|

Fastest Growing Region |

Online/West (digital + demographic growth) |

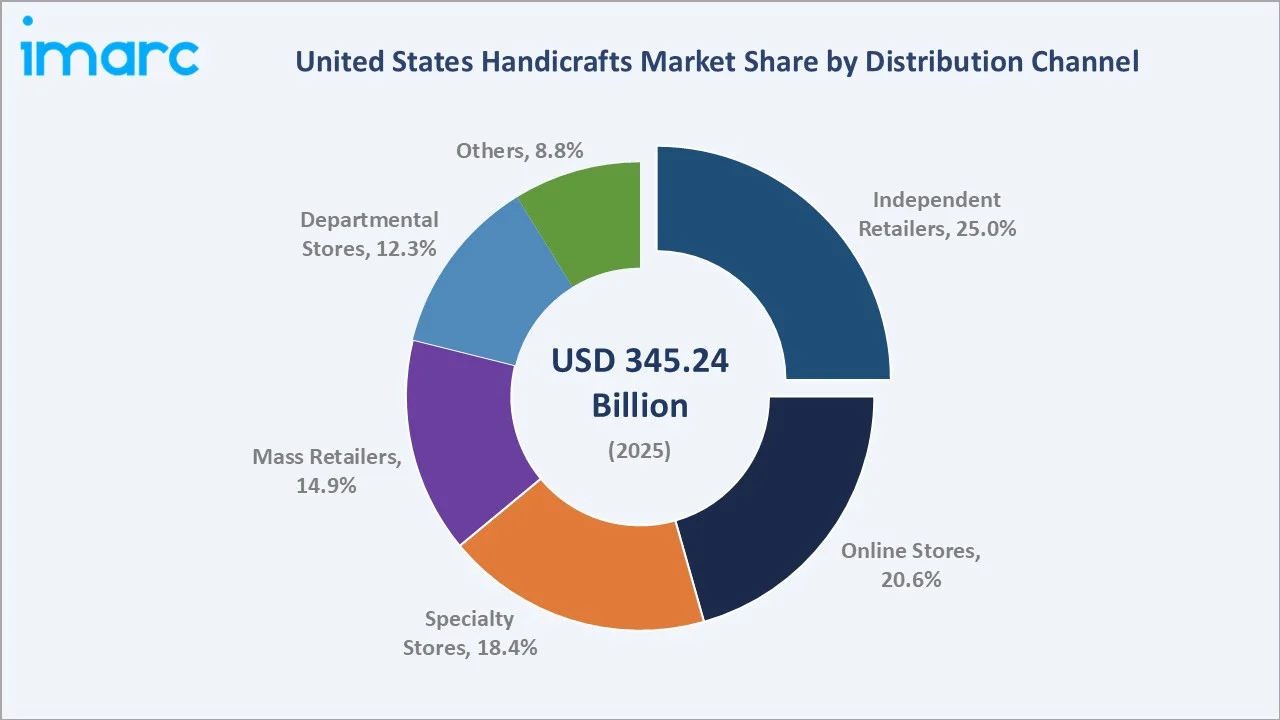

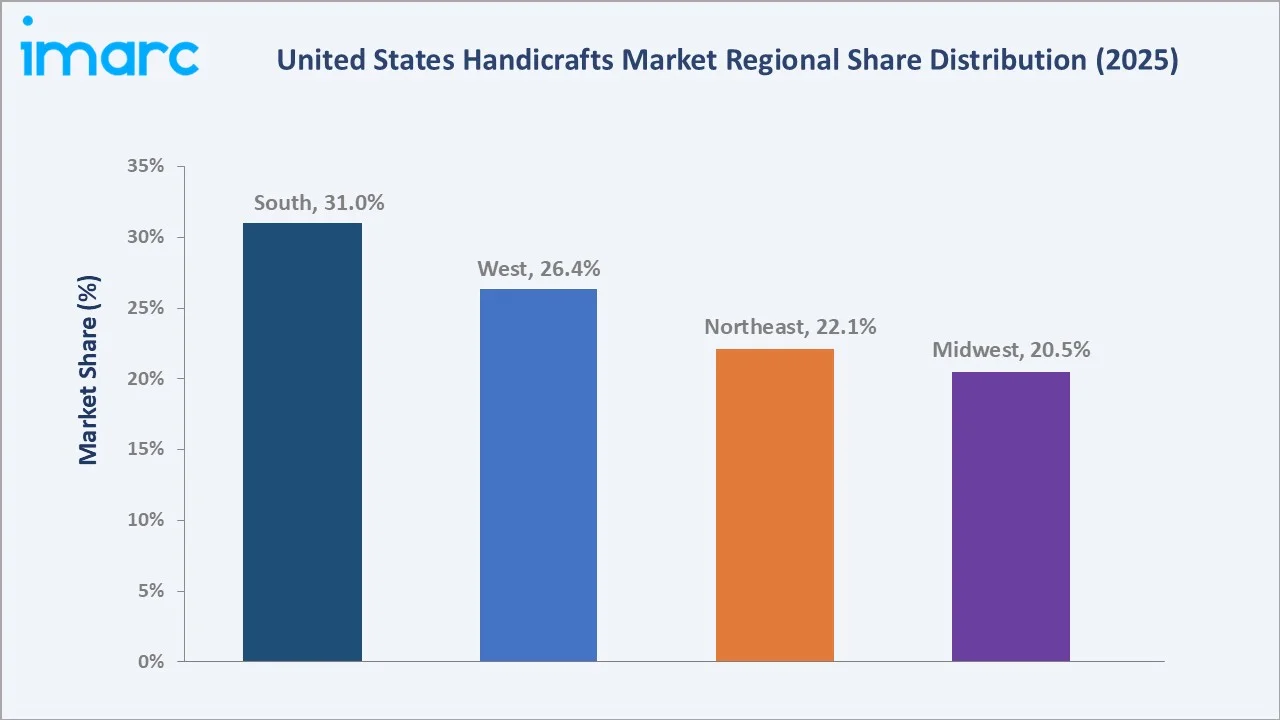

The South dominates, holding a 31.0% market share in 2025, while the residential end-use segment leads demand at 70.0%, reflecting the deep personal and home-décor nature of handicraft consumption across the country. Independent retailers lead distribution with a 25.0% channel share in 2025.

To get more information on this market, Request Sample

With applications spanning home décor, fashion accessories, seasonal gifts, cultural artefacts, and commercial venue decoration, the U.S. handicrafts market is set to expand broadly, supported by rising artisan entrepreneurship, influencer-driven craft trends, and growing institutional recognition of the economic and cultural value of handmade goods.

Executive Summary

The U.S. handicrafts market is experiencing sustained, broad-based growth, anchored by structural shifts in consumer values toward authenticity, sustainability, and personalization. The market reached USD 345.24 Billion in 2025 and is forecast to exceed USD 676.82 Billion by 2034, at a CAGR of 7.77% - substantially outpacing the broader U.S. retail market's average growth rate.

The South leads nationally with a 31.0% share, supported by states such as Texas, Tennessee, and North Carolina, where craft fairs, artisan tourism, and Southern heritage gifting traditions sustain year-round demand. The West commands 26.4%, energized by California's design-conscious consumer base and sustainability-led artisan communities in cities like Portland, Seattle, and Los Angeles.

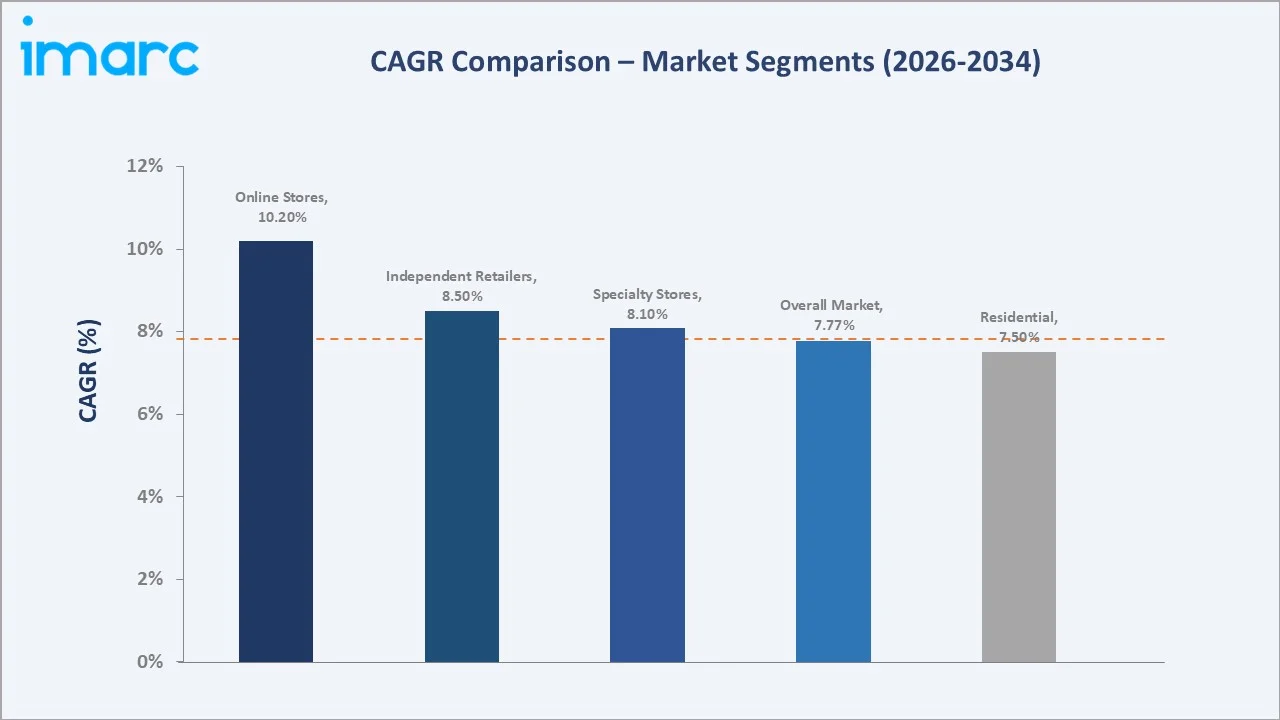

Residential demand accounts for 70.0% of the market, reflecting the central role of handicrafts in home decoration, seasonal celebrations, and personal gifting. Online stores are the fastest-growing channel at an estimated CAGR of 10.20%, as social media platforms including Pinterest, TikTok, and Instagram continuously drive discovery and direct-to-consumer purchasing of handmade products, compressing the traditional wholesale-to-retail value chain.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Distribution) |

Independent Retailers – 25.0% (2025) |

|

Largest Segment (End Use) |

Residential – 70.0% (2025) |

|

Largest Region |

South – 31.0% share (2025) |

|

Fastest Growing Channel |

Online Stores (est. CAGR 10.20%) |

|

Top Companies |

Hobby Lobby, Michaels Stores, Etsy, Inc., Crate & Barrel, and Ten Thousand Villages |

Key Analytical Observations Supporting the Above Data:

- Independent retailers command the largest distribution channel share at 25.0% in 2025, reflecting the deeply personal nature of handicraft retail where store owner curation, local artisan relationships, and community trust drive consumer preference over mass-market alternatives.

- Online stores are the fastest-growing channel at an estimated CAGR of 10.20%, as for its fiscal Q4 ending on December 31, Etsy, Inc. reported gross merchandise sales (GMS) on its primary marketplace of USD 3.29 billion, reflecting a 0.1% year-over-year increase.

- The South holds 31.0% of the U.S. handicrafts market in 2025, led by Texas, Tennessee, Georgia, and North Carolina, where craft tourism, artisan festivals (Kentucky Craft Fair, Tennessee Handmade), and strong gifting traditions generate disproportionate per-capita handicraft spend.

- Residential end-use dominates at 70.0% as consumers increasingly personalize living spaces with handcrafted home accents, wall art, ceramics, and textiles, a trend accelerated by the post-pandemic home improvement surge that added approximately USD 420 billion to U.S. home décor spending between 2020 and 2024.

- The sustainable and ethically sourced handicraft sub-segment is growing at an estimated 12-14% annually, driven by Gen Z and Millennial consumers, representing the majority of U.S. handicraft purchasers, who actively seek fair-trade certified, locally made, and eco-conscious handcrafted products.

United States Handicrafts Market Overview

The U.S. handicrafts market encompasses a broad spectrum of handmade products, including textile arts, woodworking, ceramics and pottery, jewelry, metalwork, glasswork, papercraft, and decorative accessories produced through skilled manual techniques. The sector spans from individual artisan makers and small craft cooperatives to large specialty retail chains and online marketplace platforms that aggregate millions of individual sellers.

The U.S. handicrafts ecosystem is uniquely characterized by its dual nature, a professional retail layer anchored by major chains (Hobby Lobby, Michaels, JOANN), and a vast informal artisan economy operating through Etsy, local craft fairs, farmers' markets, and consignment galleries. Macroeconomic factors, including post-pandemic home investment, social media-driven craft culture, and growing consumer premiumization of artisan goods, are primary structural growth drivers.

Market Dynamics

To evaluate market opportunities, Request Sample

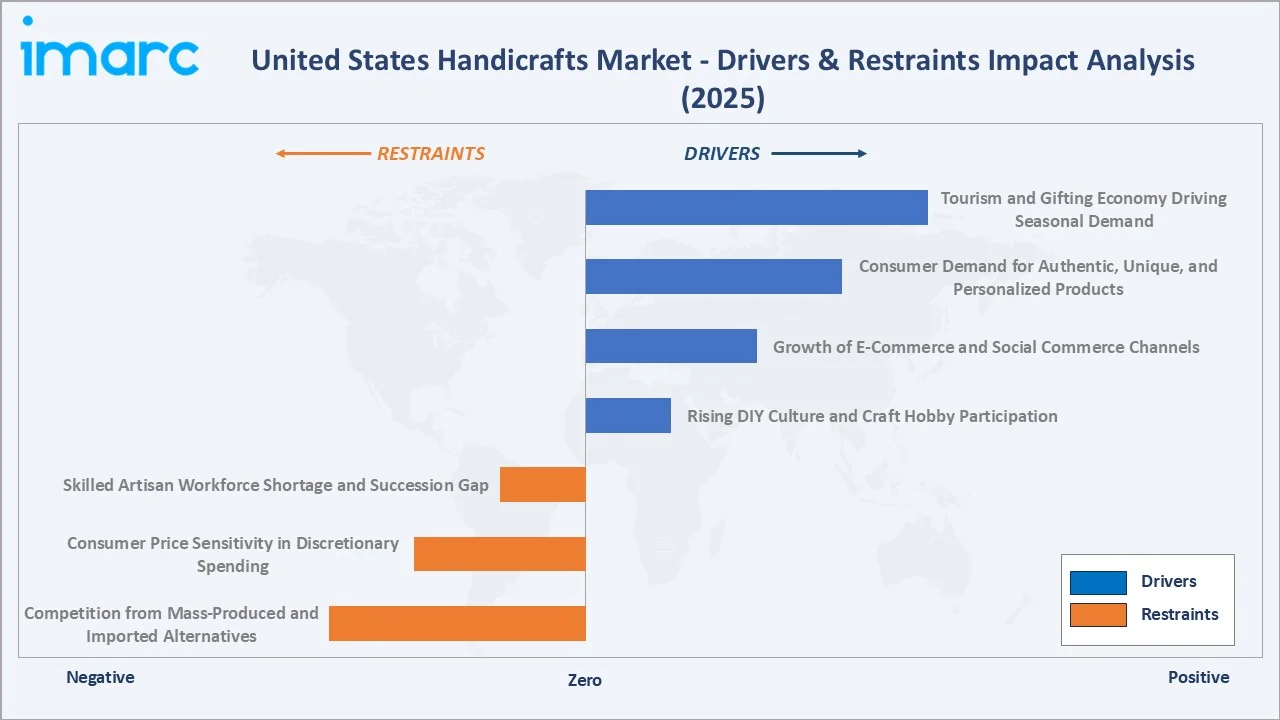

Market Drivers

- Rising DIY Culture and Craft Hobby Participation: A 1,000 American adults surveyed on the AYTM platform, and 67% of respondents reported having multiple hobbies, while 18% stated they have just one hobby they practice or participate in regularly.

- Growth of E-Commerce and Social Commerce Channels: According to an analysis by Digital Commerce 360, U.S. e-commerce sales reached approximately USD 1.234 trillion in 2025, with handmade and artisan goods representing one of the fastest-growing sub-categories. Pinterest's shopping features drive approximately 1.5 billion monthly visual searches for craft and handmade product ideas.

- Consumer Demand for Authentic, Unique, and Personalized Products: McKinsey's 2024 consumer survey found that Almost 20% of U.S. consumers and 33% of U.S. millennials prefer personalized products and services. The premiumization of gift-giving occasions is driving average spend per handcrafted gift unit upward.

- Tourism and Gifting Economy Driving Seasonal Demand: The U.S. travel & tourism sector generated USD 1.54 trillion in domestic travel spending in 2025, with local handicrafts and artisan souvenirs representing a major discretionary purchase category across heritage tourism destinations, including Santa Fe, Asheville, Savannah, and the entire American Southwest.

Market Restraints

- Competition from Mass-Produced and Imported Alternatives: Low-cost mass-produced home décor and giftware imported primarily from China, India, and Vietnam undercut artisan-priced U.S. handcrafted goods by 60-80% on unit price.

- Consumer Price Sensitivity in Discretionary Spending: The Federal Reserve's 2023-2024 rate tightening cycle increased consumer debt service costs, reducing disposable income available for non-essential purchases and moderating growth in the premium artisan segment during this period.

- Skilled Artisan Workforce Shortage and Succession Gap: The Bureau of Labor Statistics reports that the average age of U.S. manufacturing workers is 44 years, with insufficient apprenticeship and vocational training programs to replace retiring artisans at scale.

Market Opportunities

- Sustainable, Ethical, and Upcycled Handicraft Segment: The sustainable gifting market in the U.S. is estimated at USD 22 billion in 2025, with handcrafted sustainable products capturing an increasingly large share. Brands like Ten Thousand Villages (fair trade imports) and numerous Etsy sellers with eco-certification are growing 2-3x faster than the overall handicraft market.

- Corporate and Institutional Gifting Market Expansion: The U.S. corporate gifting market was valued at approximately USD 242 billion in 2024, with handcrafted and artisan goods increasingly preferred for premium client gifting, employee recognition, and branded merchandise programs.

- Digital Craft Education and Content Monetization: Online craft education platforms, including Skillshare and Craftsy offer subscription-based craft instruction that simultaneously drives supply and demand. YouTube craft channels with 1M+ subscribers generate significant affiliate and direct product sales, creating a virtuous content-commerce cycle that is expanding the total handicraft addressable market.

Market Challenges

- Counterfeiting and Handmade Authentication: Etsy, Inc. acknowledged in 2023 that a significant proportion of listings claiming to be handmade involved mass-produced imports relabeled as artisan goods, prompting a platform-wide seller authenticity enforcement program.

- Supply Chain Fragmentation and Scalability Limitations: The highly fragmented nature of the artisan supply chain, characterized by thousands of small producers with limited standardized practices, creates quality consistency challenges, unreliable fulfilment timelines, and scalability constraints.

Emerging Market Trends

1. DIY Boom and Pandemic-Era Craft Renaissance

The COVID-19 pandemic triggered an unprecedented surge in craft and DIY participation across the U.S. Etsy, Inc.'s gross merchandise sales grew 106% year-on-year in 2020. Crucially, this craft engagement has remained structurally elevated post-pandemic. A large number of Americans who took up craft hobbies during 2020-2021 continued to practice them, with one survey showing that 51% of Americans started a creative hobby, and nearly 98% of them maintained these activities throughout the lockdown.

2. Social Commerce Transforming Handicraft Discovery and Sales

TikTok Shop's U.S. launch facilitated direct in-video purchasing of handcrafted items, with creator-artisans reporting 400-1,000% revenue increases from viral content. Instagram Shopping and Pinterest Lens visual search are similarly transforming the discovery-to-purchase funnel for handcrafted goods, reducing the traditional role of craft fairs and specialty stores as primary discovery venues.

3. Sustainability and Fair-Trade Certification as Competitive Differentiators

Certified B Corp handicraft brands are outperforming the broader market, as environmentally and socially conscious consumption becomes a core purchase criterion for the under-45 demographic. As of 2023, 3 billion pounds of Fair Trade Certified produce have been sold, resulting in a cumulative $94 million in additional income for workers and their communities through the Fair Trade Premium. Fair Trade USA currently collaborates with 156 Certificate Holders across 14 countries.

4. AI-Assisted Design Personalization

Generative AI tools are creating a new paradigm in the handicraft market by enabling consumers to co-design personalized handcrafted products through AI-assisted platforms. Etsy, Inc.'s integration with AI design tools allows buyers to specify exact design parameters, colors, dimensions, and motifs, which are then interpreted and executed by artisan sellers.

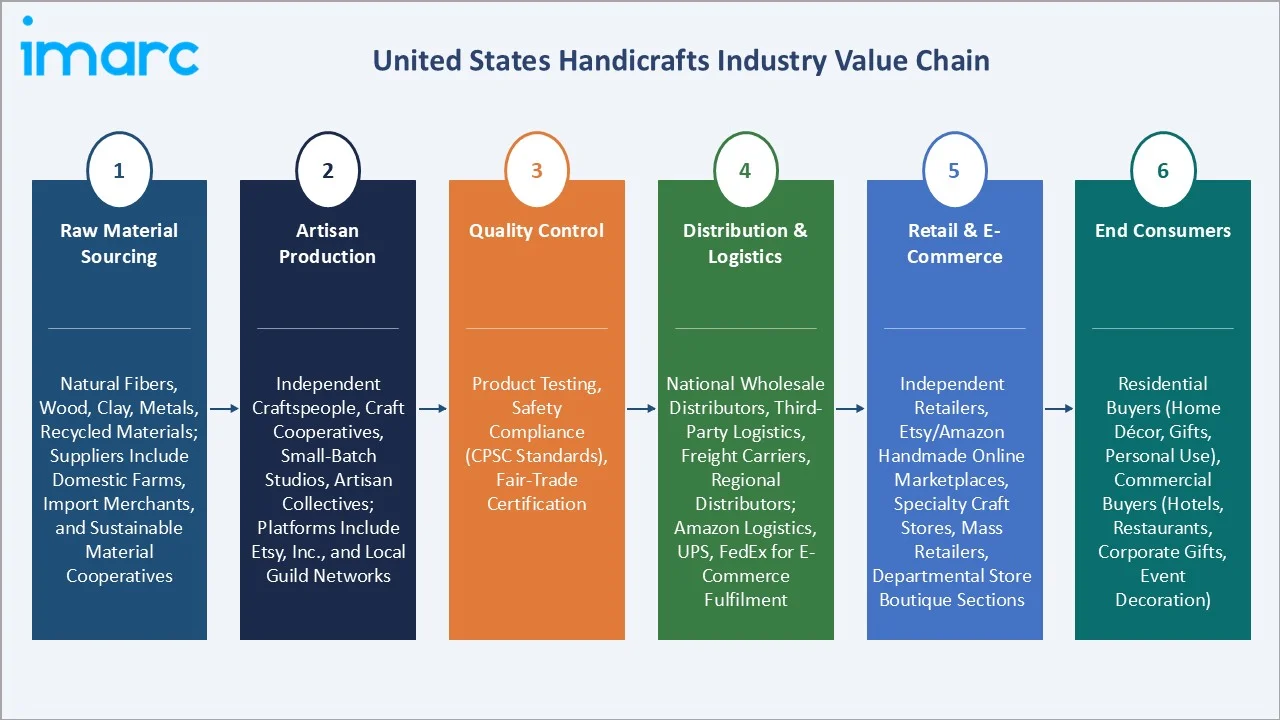

Industry Value Chain Analysis

The U.S. handicrafts value chain is characterized by significant fragmentation at the production stage - where millions of individual makers operate independently - and consolidation at the retail and distribution stages, where large specialty retailers and e-commerce platforms aggregate and distribute artisan output to the mass market.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Natural fibers, wood, clay, metals, recycled materials; suppliers include domestic farms, import merchants, and sustainable material cooperatives |

|

Artisan Production |

Independent craftspeople, craft cooperatives, small-batch studios, artisan collectives; platforms include Etsy, Inc., and local guild networks |

|

Quality Control |

Product testing, safety compliance (CPSC standards), fair-trade certification |

|

Distribution & Logistics |

National wholesale distributors, third-party logistics, freight carriers, regional distributors; Amazon Logistics, UPS, FedEx for e-commerce fulfilment |

|

Retail & E-Commerce |

Independent retailers, Etsy/Amazon Handmade online marketplaces, specialty craft stores, mass retailers, departmental store boutique sections |

|

End Consumers |

Residential buyers (home décor, gifts, personal use), commercial buyers (hotels, restaurants, corporate gifts, event decoration) |

Technology Landscape in the U.S. Handicrafts Industry

E-Commerce Marketplace Technology

Etsy's proprietary marketplace platform powers USD 13+ billion in annual gross merchandise sales with sophisticated seller analytics, personalized recommendation algorithms, and integrated shipping label printing. Michaels' MakerPlace online marketplace, launched in 2023, replicates the Etsy model with the added credibility of the Michaels brand and its 15 million active loyalty program members as a built-in buyer base for handmade goods.

Digital Design and Fabrication Tools

Cricut's cutting machine ecosystem (5.9 million active users in 2024) represents the intersection of technology and handicraft, enabling home crafters to produce professional-quality vinyl decals, fabric patterns, and paper crafts. Cricut's connected platform generates recurring revenue through design file subscriptions and proprietary material sales, creating a technology-driven craft ecosystem valued at approximately USD 1.8 billion.

Augmented Reality for Product Visualization

Retailers, including Wayfair, Etsy, Inc., and Crate & Barrel, have deployed AR visualization tools enabling consumers to preview handcrafted home décor items in their actual living spaces before purchase. AR feature users convert at 2.7x the rate of non-AR browser sessions for handicraft home décor, and return rates for AR-previewed products are 35% lower than equivalent non-AR purchases, improving unit economics significantly for premium handcrafted décor categories.

Blockchain and Provenance Authentication

Emerging blockchain-based provenance systems are being piloted to certify the authenticity and origin of handcrafted goods, addressing the critical counterfeiting challenge. Arweave-based craft certification pilots by American Craft Council members create immutable digital provenance records for each handcrafted piece, enabling premium pricing for verified artisan goods and protecting consumer trust in the rapidly growing online artisan commerce market.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Woodware | 24.0% | 2025 |

| Distribution Channel | Independent Retailers | 25.0% | 2025 |

| End Use | Residential | 70.0% | 2025 |

| Regions | South | 31.0% | 2025 |

By Distribution Channel

Independent retailers command the largest distribution channel share at 25.0% in 2025. Their dominance reflects the intrinsic nature of handicraft retail, curated product selection, personal artisan relationships, and community store identity, creating consumer experiences that large-format mass retailers cannot replicate.

To access detailed market analysis, Request Sample

Online stores hold a 20.6% share and are the fastest-growing channel at an estimated CAGR of 10.20%. Etsy, Inc., Amazon Handmade, and individual artisan websites powered by Shopify collectively drive this digital segment. Specialty stores account for 18.4%, including Hobby Lobby, Michaels, and JOANN, followed by mass retailers (14.9%) and departmental stores (12.3%).

By End Use

The residential end-use segment dominates the U.S. handicrafts market with a 70.0% share in 2025, driven by consumer demand for unique home décor, personalized gifts, seasonal decorations, and fashion accessories. Post-pandemic home investment, with U.S. households spending a median of USD 18,000 on home improvement and décor, has created a structurally elevated baseline of residential handicraft consumption.

The commercial end-use segment holds a 30.0% share, encompassing hospitality venues (hotels, restaurants, spas), corporate gifting programs, event and wedding decoration, retail display design, and institutional procurement by museums, galleries, and cultural centers.

Regional Market Insights

The South's market leadership (31.0%, 2025) is grounded in one of the country's richest craft heritage traditions. Appalachian craft traditions spanning North Carolina, Tennessee, and Kentucky represent centuries-old woodworking, quilting, and pottery practices with strong tourist and collector demand.

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

31.0% |

Strong craft heritage, major tourism, robust gifting economy |

|

West |

26.4% |

Tech-savvy consumers, a sustainability focus, and high disposable income |

|

Northeast |

22.1% |

High-income urban buyers, strong artisan culture, and interior design demand |

|

Midwest |

20.5% |

Strong DIY tradition, manufacturing base, value-conscious consumers |

The West (26.4%) is the second-largest and fastest-growing major region, driven by California's design-conscious consumer base and the Pacific Northwest's strong sustainability ethos. The Santa Fe arts market in New Mexico generates approximately USD 800 million annually, making it one of the largest arts and crafts markets in North America.

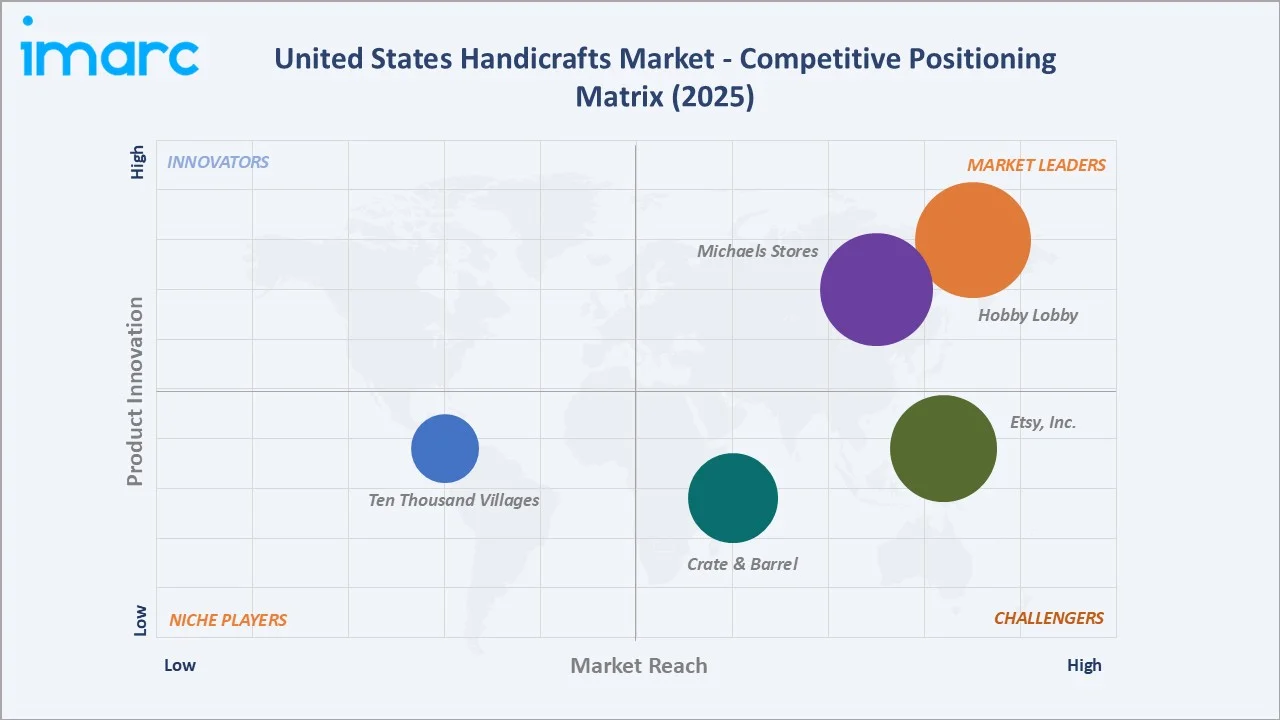

Competitive Landscape

The U.S. handicrafts market exhibits a layered competitive structure. At the specialty retail level, Hobby Lobby and Michaels Stores dominate brick-and-mortar craft retail with approximately 2,800 combined store locations, commanding an estimated 12-15% of total retail-side market revenue.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Hobby Lobby |

Yarn Bee, Woodpile Fun, The Paper Studio, Master’s Touch |

Market Leader |

Nation's one of the largest arts & crafts retailers |

|

Michaels Stores |

Make Market, Ashland, Loops & Threads, Artist's Loft, Recollections |

Market Leader |

Broadest SKU range; MakerPlace online marketplace |

|

Etsy, Inc. |

Etsy |

Strong Challenger |

Global artisan marketplace; 86.5M+ active buyers |

|

Crate & Barrel |

Crate & Kids/ CB2 |

Challenger |

Premium home décor; curated artisan collection partnerships |

|

Ten Thousand Villages |

Ten Thousand Villages |

Niche Player |

Fair trade pioneer; exclusively handmade artisan imports from 30+ countries |

In the marketplace layer, Etsy Inc. holds a dominant position in the online artisan marketplace with 5.6 million active sellers and 86.5 million active buyers as of February 2026.

Key Company Profiles

Hobby Lobby

Hobby Lobby is a privately held arts and crafts retail chain headquartered in Oklahoma City, Oklahoma. Founded in 1972, it operates 1,000+ stores across 48 states and is America's largest arts and crafts retailer, offering 80,000+ product SKUs across craft supplies, home décor, seasonal items, and finished handcrafted goods.

- Product Portfolio: Yarn Bee, Woodpile Fun, The Paper Studio, and Master’s Touch.

- Recent Developments: In May 2025, Hobby Lobby announced the opening of a new store in Honesdale, Pennsylvania, expanding its footprint in the region. The new location features the retailer’s full range of arts, crafts, and home decor products and will serve local hobbyists and DIY shoppers.

- Strategic Focus: Store expansion in Southeast and Midwest markets; private label home décor product development; increased artisan vendor partnerships.

Michaels Stores

Michaels Stores is the largest specialty arts and crafts retailer in North America by store count, operating approximately 1,300+ Michaels stores. Headquartered in Irving, Texas, directly competes with Etsy in the artisan e-commerce space.

- Product Portfolio: Make Market, Ashland, Loops & Threads, Artist's Loft, and Recollections.

- Recent Developments: In March 2026, Michaels lowered prices across its stores to counter ongoing consumer uncertainty. This discount strategy aims to make arts and crafts products more affordable and attract cautious shoppers, helping the chain maintain sales momentum.

- Strategic Focus: Omnichannel craft community platform; custom framing revenue growth; MakerPlace artisan seller recruitment.

Etsy, Inc

Etsy, Inc. is a global e-commerce marketplace headquartered in Brooklyn, New York, specializing exclusively in handmade, vintage, and craft supply goods. Etsy operates with a managed marketplace model, providing discovery, payments, and seller analytics tools to its 5.6 million active global sellers.

- Product Portfolio: Etsy marketplace

- Recent Developments: In January 2026, Etsy, Inc. announced a partnership with Google to integrate AI‑powered shopping features, making it easier for buyers to discover products through intelligent search and recommendations.

- Strategic Focus: Deepening U.S. buyer-seller relationships; international marketplace expansion; AI-driven personalized shopping experiences.

Market Concentration Analysis

The U.S. handicrafts market is structurally fragmented, reflecting its deep roots in individual artisan production and small business retail. The top players, Hobby Lobby, Michaels Stores, Etsy, Inc., and Crate & Barrel, collectively account for an estimated 15-18% of total market revenue in 2025, leaving the remaining 82-85% distributed across tens of thousands of independent retailers, regional craft chains, craft fair vendors, and direct artisan sellers.

The market's fragmentation is a structural feature as the inherent characteristics of handmade goods limit the dominance of any single player. However, consolidation is occurring within the specialty retail sub-segment, where JOANN Inc. filed for bankruptcy for the second time in January 2025, and subsequent restructuring reflects the challenging economics of large-format craft retail facing intense competition from online channels.

Investment & Growth Opportunities

Fastest Growing Segments

Online artisan marketplace platforms (estimated CAGR 10.20%), sustainable and fair-trade certified handicrafts (12-14% CAGR), and personalized/custom order handicrafts (9.5% CAGR) represent the three highest-growth investment vectors through 2034. Together, these emerging segments address a total addressable market of approximately USD 140 billion within the broader U.S. handicrafts space by 2030.

Emerging Market Expansion

The commercial and hospitality gifting sector represents an underpenetrated opportunity for U.S. artisan producers. The USD 242 billion corporate gifting market allocates an estimated 8-12% to artisan and handcrafted items currently - a share expected to grow to 18-22% by 2034 as ESG procurement guidelines and employee experience investments drive demand for premium, ethically sourced artisan gifts.

Venture and Institutional Investment Trends

- Key investment themes include AI-powered artisan marketplace platforms, craft education technology (EdTech-CraftTech convergence), sustainable material innovation for craft supplies, and social commerce tools for artisan sellers.

- Family offices and PE firms are increasingly targeting specialty craft retail consolidation plays, seeking to build regional or national craft retail platforms from independent retailer aggregation.

Future Market Outlook (2026-2034)

The U.S. handicrafts market is positioned for broad-based, sustained growth through 2034. From a base of USD 345.24 Billion in 2025, the market is projected to reach USD 676.82 Billion by 2034, with a total incremental value creation of approximately USD 331.6 Billion over the forecast decade. At a CAGR of 7.77%, this represents one of the most consistent long-cycle growth stories in the U.S. consumer goods landscape.

The structural macro-themes will define the market's trajectory. First, the long-term shift toward value-based consumption - where consumers increasingly prioritize authenticity, craftsmanship, and artisan provenance over price - will continue elevating the premium handicraft segment. Second, the maturation of the artisan platform economy, led by Etsy's model, will lower barriers to market entry for new artisan sellers while expanding consumer access globally.

The sustainability imperative, with B Corp and fair-trade certified handicraft brands growing 2-3x the market rate, represents a durable competitive advantage for producers who invest in ethical sourcing, circular economy design, and transparent supply chains. Brands that embed sustainability credentials will be positioned to capture the estimated USD 85 billion in sustainably sourced handicraft spending projected by 2034.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 140 industry participants in 2024–2025, including independent craft retailers, online artisan sellers, specialty craft store managers, wholesale distributors, corporate gifting procurement officers, and consumer focus group participants across all four U.S. census regions.

Secondary Research

Secondary research encompassed company annual reports, U.S. Census Bureau retail trade statistics, Bureau of Labor Statistics occupational data, American Craft Council membership and market surveys, Etsy annual reports and seller data, Craft Industry Alliance annual craft business survey data, trade publications (Handmade Business, Gifts & Decorative Accessories), and retailer financial disclosures.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting methodologies, incorporating U.S. consumer expenditure survey data, e-commerce penetration trend modelling, artisan marketplace volume data, and historical market evolution across comparable craft and home décor categories. A base-case CAGR of 7.77% reflects consensus projections validated against reported retailer same-store sales, Etsy GMV growth trends, and National Retail Federation handicraft category data.

United States Handicrafts Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Woodware, Artmetal Ware, Handprinted Textiles and Scarves, Embroidered and Crocheted Goods, Zari and Zari Goods, Imitation Jewelry, Sculptures, Pottery and Glass Wares, Attars and Agarbattis, Others |

| Distribution Channels Covered | Mass Retailers, Departmental Stores, Independent Retailers, Specialty Stores, Online Stores, Others |

| End Uses Covered | Residential, Commercial |

| Regions Covered | Northeast, Midwest, South, West |

| companies Covered | Hobby Lobby, Michaels Stores, Etsy, Inc., Crate & Barrel, Ten Thousand Villages, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Handicrafts Market Report

The U.S. handicrafts market reached USD 345.24 Billion in 2025 and is forecast to reach USD 676.82 Billion by 2034 at a CAGR of 7.77%.

The market is projected to grow at a CAGR of 7.77% during the forecast period 2026-2034, reflecting sustained consumer demand for authentic, personalized, and artisan-crafted goods.

The South leads with a 31.0% share in 2025, driven by Appalachian craft heritage, strong gifting traditions, and craft tourism across Texas, Tennessee, North Carolina, and Georgia.

Independent retailers dominate with a 25.0% channel share in 2025, while online stores are the fastest-growing channel at an estimated CAGR of 10.20%.

Key players include Hobby Lobby, Michaels Stores, Etsy, Inc., Crate & Barrel, and Ten Thousand Villages.

The residential segment dominates with a 70.0% market share in 2025, driven by home décor purchases, seasonal decoration, and personal gifting.

Online platforms like Etsy (USD 13B+ GMV), Amazon Handmade, and TikTok Shop are the fastest-growing channels, enabling artisans to reach national and global audiences cost-effectively.

Fair-trade certified, eco-friendly, and sustainably sourced handicrafts are growing 12-14% annually. The sustainable handicraft segment is projected to reach USD 85 billion by 2034.

Key challenges include competition from low-cost mass-produced imports, consumer price sensitivity, skilled artisan workforce shortages, and counterfeit "handmade" listings on online platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)