United States Healthcare Big Data Analytics Market Size, Share, Trends and Forecast by Component, Analytics Type, Delivery Model, Application, End User, and Region, 2026-2034

United States Healthcare Big Data Analytics Market Size, Share, Trends & Forecast (2026-2034)

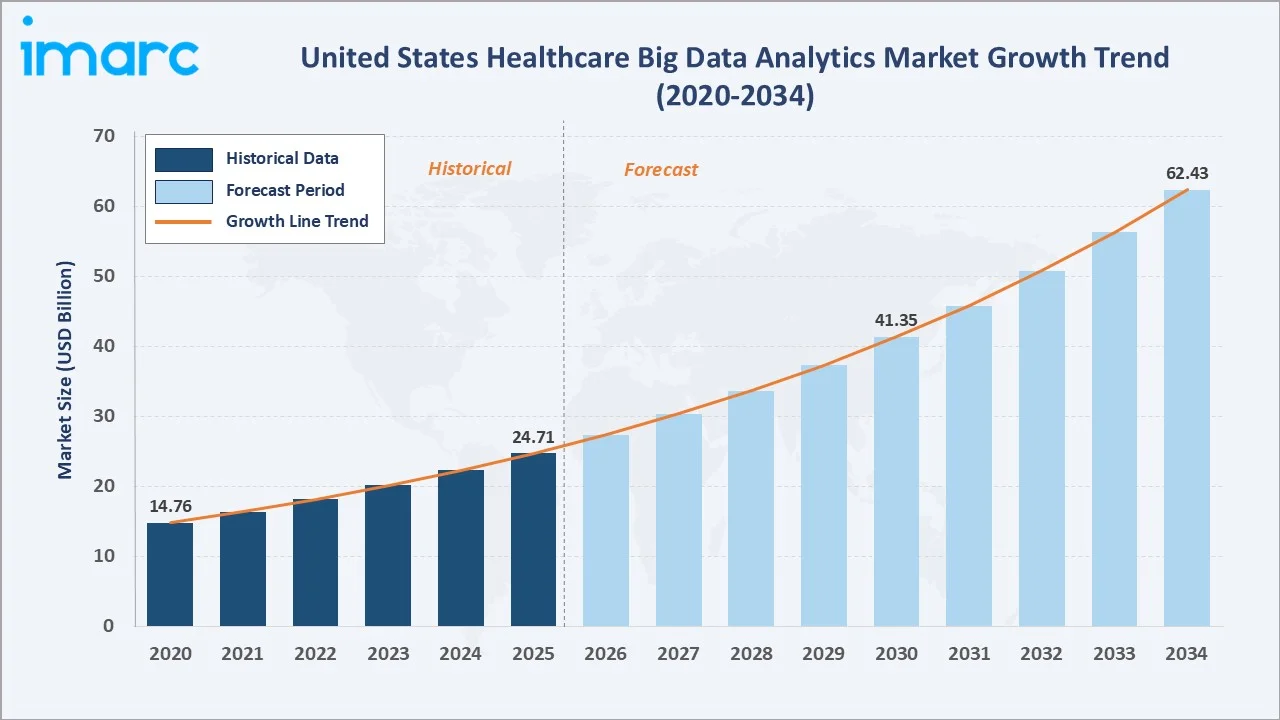

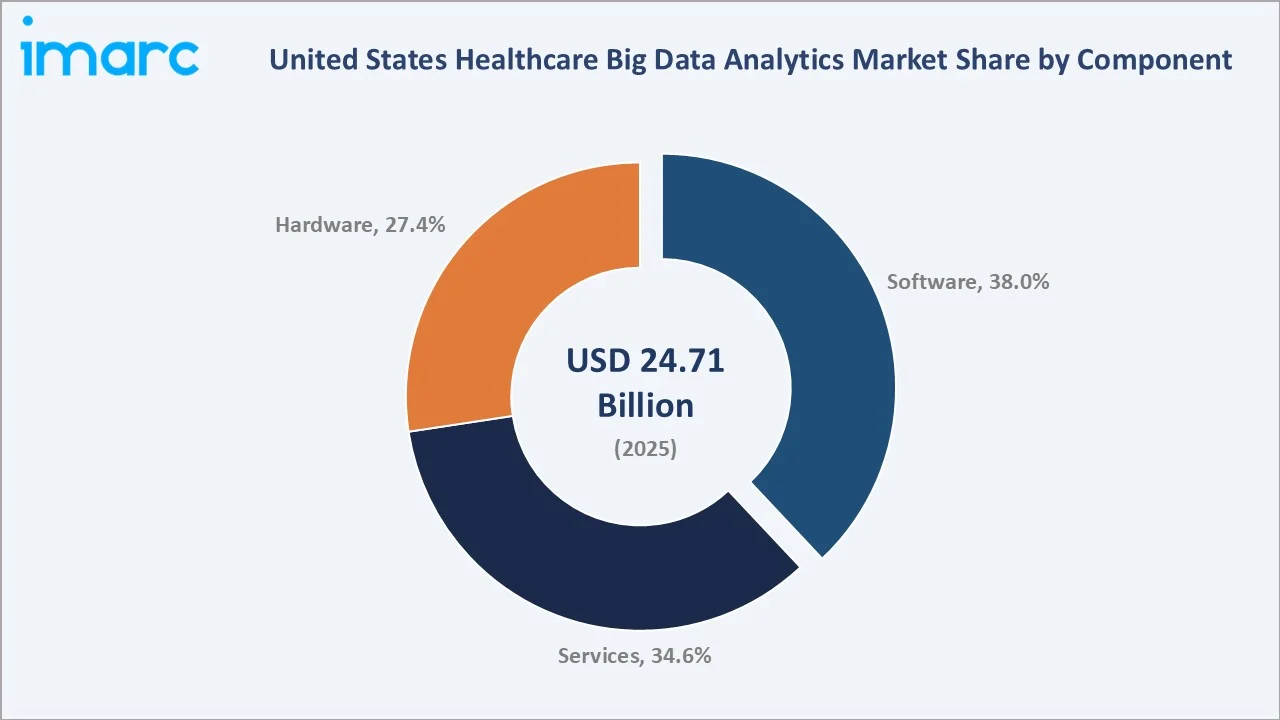

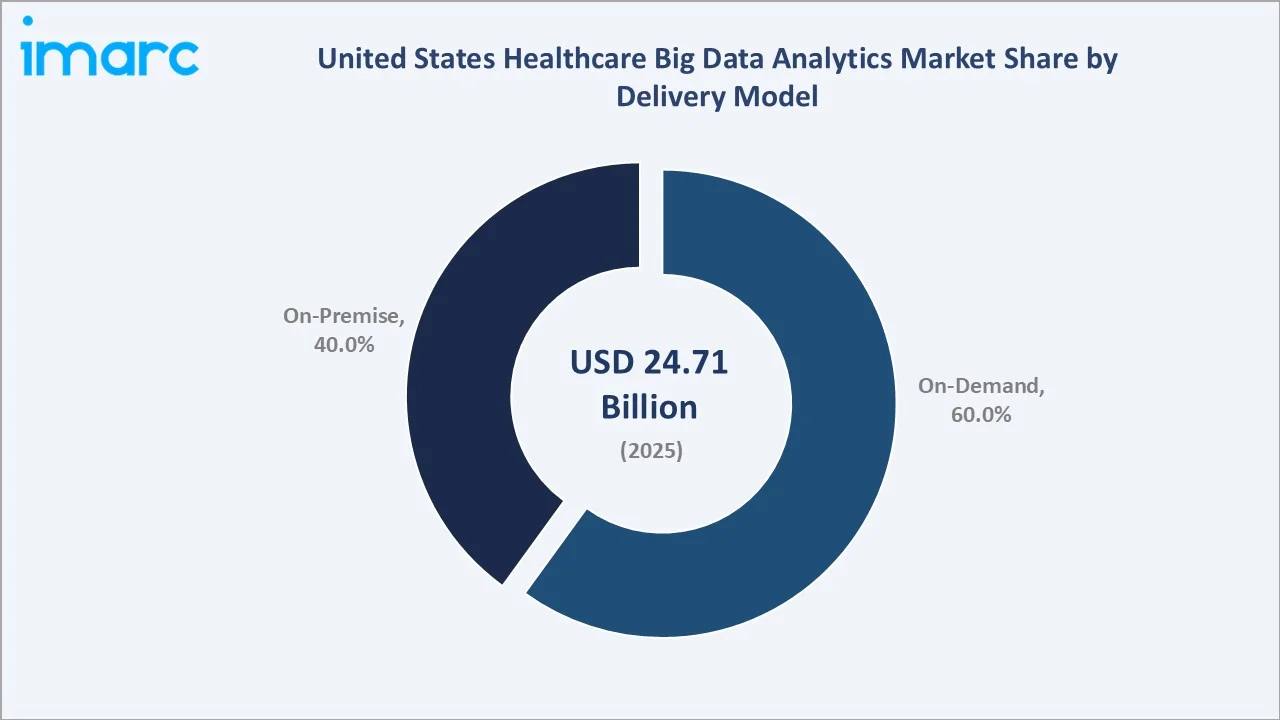

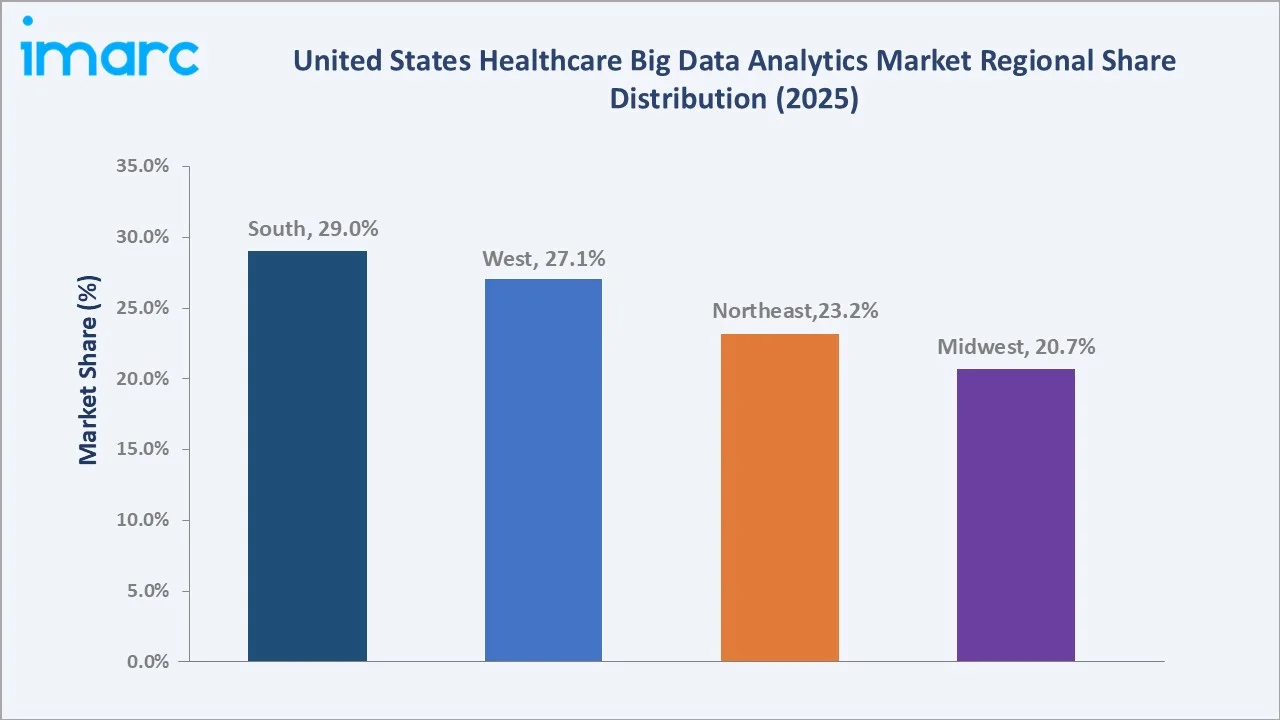

The United States healthcare big data analytics market size was valued at USD 24.71 Billion in 2025 and is projected to reach USD 62.43 Billion by 2034, exhibiting a CAGR of 10.9% during 2026-2034. Rising digitization of clinical workflows, accelerating cloud adoption across hospitals and health systems, expanding use of artificial intelligence in diagnostics, and policy-driven interoperability mandates are collectively fueling market growth. Software dominates with a 38.0% share in 2025, while the On-Demand delivery model accounts for 60.0% of revenue. The South region leads with a 29.0% share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 24.71 Billion |

|

Forecast Market Size (2034) |

USD 62.43 Billion |

|

CAGR (2026-2034) |

10.9% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South (29.0% share, 2025) |

|

Fastest Growing Region |

West |

|

Leading Component |

Software (38.0%, 2025) |

|

Leading Delivery Model |

On-Demand (60.0%, 2025) |

The chart below illustrates the U.S. healthcare big data analytics market trajectory from 2020 to 2034, reflecting steady historical growth driven by EHR adoption and a robust forecast supported by AI integration and cloud-based deployments.

To get more information on this market, Request Sample

CAGR analysis identifies On-Demand delivery and Software components as the fastest-expanding segments during the 2026-2034 forecast window, while overall market growth remains anchored at 10.9% CAGR.

Executive Summary

The U.S. healthcare big data analytics market is undergoing rapid transformation, fueled by widespread EHR adoption, value-based care reimbursement, and the integration of artificial intelligence into clinical decision support. Valued at USD 24.71 Billion in 2025, it is projected to reach USD 62.43 Billion by 2034 at a 10.9% CAGR. The historical period (2020-2025) saw revenue expand from USD 14.76 Billion.

Software components led the market with a 38.0% share in 2025, anchored by EHR analytics, predictive modeling platforms, and population health tools. Services accounted for 34.6%, while Hardware contributed 27.4%. The On-Demand delivery model commanded 60.0% of revenue. Around 71% of U.S. hospitals reported using predictive AI integrated with EHRs in 2024.

Regionally, the South leads with 29.0% share in 2025, anchored by Texas, Florida, and Georgia healthcare ecosystems. The West follows at 27.1%, the Northeast holds 23.2%, and the Midwest 20.7%. The convergence of generative AI, federated learning, and FHIR-based data exchange will redefine analytics use cases through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Component Segment |

Software — 38.0% share (2025) |

|

Second Component Segment |

Services — 34.6% share (2025) |

|

Leading Delivery Model |

On-Demand — 60.0% share (2025) |

|

Leading Region |

South — 29.0% (2025) |

|

Second Region |

West — 27.1% (2025) |

|

Top Companies |

Optum Inc., Oracle, Epic Systems Corporation, IQVIA, and Merative |

Key Analytical Observations Supporting The Above Data Points:

- Software's 38.0% dominance in 2025 is anchored by EHR-integrated analytics platforms; CDC data shows around 95% of U.S. office-based physicians have adopted EHR systems, creating a deep substrate for analytics deployment.

- Services at 34.6% in 2025 reflect strong demand for implementation, system integration, and managed analytics consulting, particularly among mid-sized hospital networks lacking in-house data science capabilities.

- On-Demand delivery at 60.0% in 2025 validates the structural pivot toward cloud-native architectures, with major systems migrating workloads to AWS, Azure, and Google Cloud platforms for scalability and cost efficiency.

- The South region's 29.0% lead in 2025 reflects dense healthcare infrastructure across Texas, Florida, Georgia, and North Carolina have large and growing Medicare beneficiary populations due to aging demographics and population size, driving population health analytics demand.

- The West region's 27.1% share is propelled by Silicon Valley's health-tech ecosystem, with California-based digital health startups and academic medical centers like Stanford and UCSF accelerating AI analytics adoption.

- Top competitors are investing heavily in AI; for example, Optum acquired MedInsight in late 2024 to strengthen value-based care analytics, while Truveta raised around USD 320 million in a Series C funding round in January 2025 to expand its platform.

U.S. Healthcare Big Data Analytics Market Overview

Healthcare big data analytics refers to the systematic processing of large, complex datasets generated across clinical, administrative, financial, and operational domains. Solutions span software platforms, professional services, and supporting hardware. Core applications include clinical decision support, population health, fraud detection, and precision medicine.

The ecosystem includes EHR vendors, cloud providers, AI software developers, system integrators, regulatory bodies (HHS, ONC, CMS), and end users such as hospitals, payers, and research organizations. Macro factors include rising national health expenditure (USD 5.3 Trillion in 2024), aging demographics, value-based reimbursement, and federal interoperability mandates including TEFCA and the HTI-1 rule.

Market Dynamics

To evaluate market opportunities, Request Sample

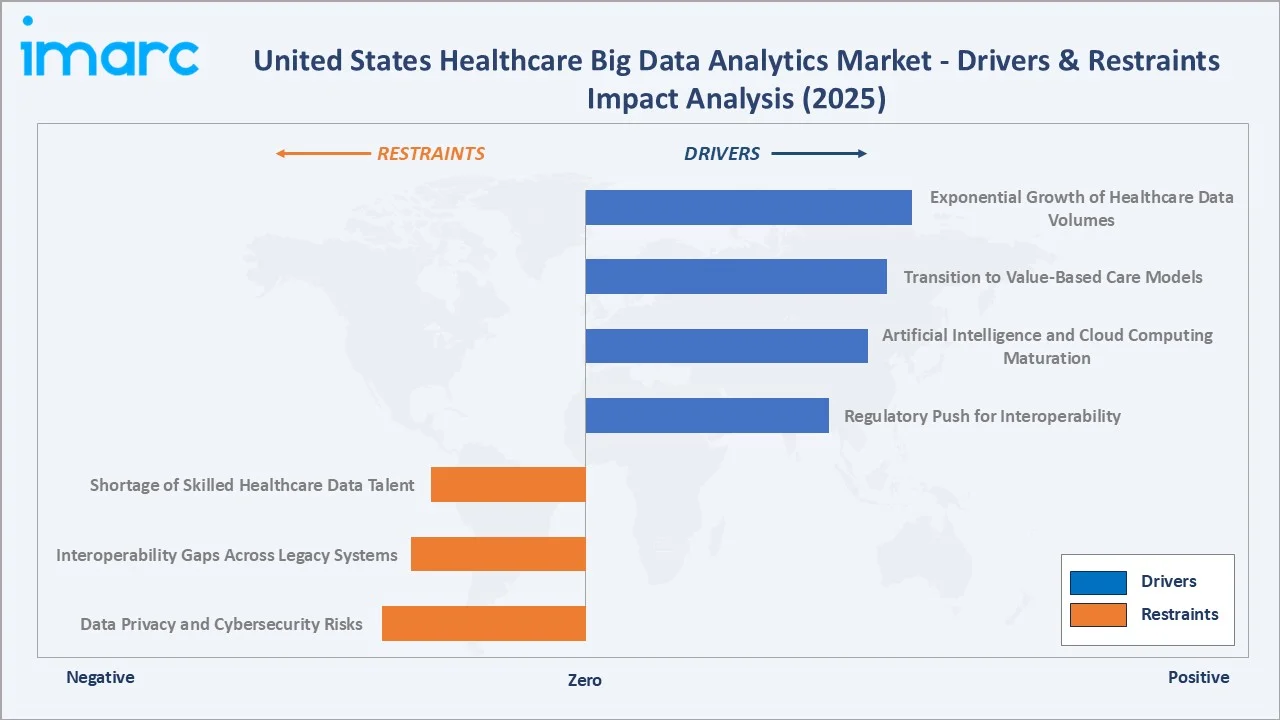

Market Drivers

- Exponential Growth of Healthcare Data Volumes: The U.S. healthcare system generates a disproportionately large share of global health data, driven by widespread EHR adoption, imaging, and connected devices, significantly increasing demand for advanced analytics platforms.

- Transition to Value-Based Care Models: Most Medicare payments are now tied to value-based care models, increasing the need for risk stratification, quality measurement, and population health analytics solutions.

- Artificial Intelligence and Cloud Computing Maturation: Around 71% of U.S. hospitals reported using predictive AI integrated with EHRs in 2024, while cloud platforms eliminate capital expenditure barriers for community hospitals.

- Regulatory Push for Interoperability: Policies such as TEFCA and FHIR standards are accelerating nationwide health data exchange, supported by over USD 1 billion in federal investment in public health data modernization since 2020.

Market Restraints

- Data Privacy and Cybersecurity Risks: Healthcare is the most targeted sector for cyberattacks, with incidents like the Change Healthcare cyberattack disrupting nationwide prescription processing, increasing compliance burdens under Health Insurance Portability and Accountability Act.

- Interoperability Gaps Across Legacy Systems: Despite progress under Trusted Exchange Framework and Common Agreement, fragmented EHR systems and inconsistent data standards continue to delay analytics deployment and increase integration complexity.

- Shortage of Skilled Healthcare Data Talent: The U.S. faces an estimated shortfall of over 250,000 data and AI specialists by 2030. Healthcare organizations compete with tech and finance sectors for the same talent pool, slowing analytics scaling.

Market Opportunities

- Generative AI in Clinical Documentation: AI-powered documentation tools like Microsoft Dragon Ambient eXperience (DAX) Copilot are being adopted by providers such as Tampa General Hospital to reduce clinician administrative burden and improve workflow efficiency.

- Population Health Management for Aging Demographics: Adults aged 65+ are projected to reach 80 Million by 2040 in the U.S. Predictive analytics for chronic-disease management, fall prevention, and Medicare Advantage risk adjustment represent high-margin growth pockets.

- Federated Learning and Privacy-Preserving Analytics: Emerging architectures allow multi-institutional research without raw data sharing, unlocking participation from privacy-conscious health systems and accelerating real-world evidence generation for life-sciences clients.

Market Challenges

- High Total Cost of Ownership for Enterprise Analytics: Enterprise healthcare analytics platforms require significant upfront and ongoing investment, including infrastructure, integration, and maintenance, which can limit adoption among smaller hospitals despite long-term ROI potential.

- Algorithmic Bias and Regulatory Scrutiny: The FDA and ONC are tightening oversight of clinical AI. Vendors must demonstrate demographic fairness and clinical validity, raising development costs and time-to-market for new analytical models.

- Data Quality and Standardization Issues: Inconsistent clinical data standards (ICD-10 (diagnoses), SNOMED CT (clinical terminology), and LOINC (laboratory data)), unstructured records, and incomplete datasets require extensive data preparation, slowing analytics implementation.

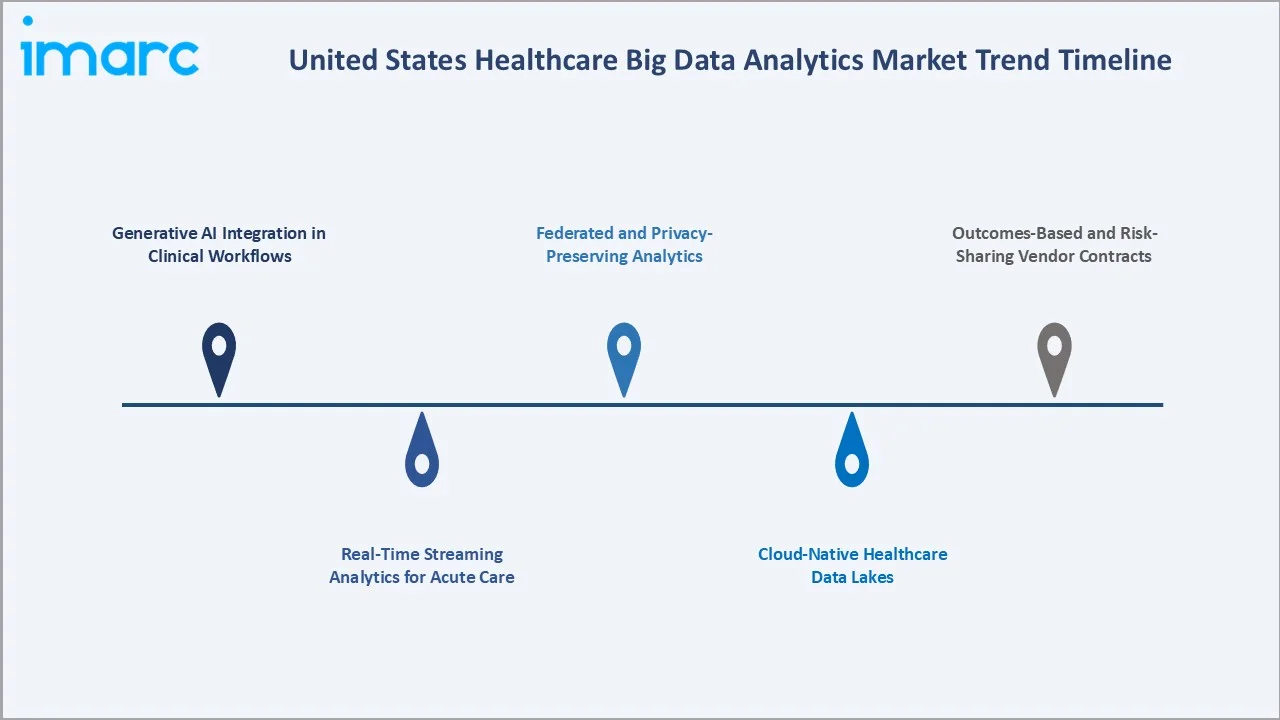

Emerging Market Trends

1. Generative AI Integration in Clinical Workflows

Healthcare organizations are deploying generative AI for ambient documentation, summarization, and clinical decision support. Tampa General Hospital reported measurable reductions in clinician burden after implementing ambient voice technology and DAX Copilot, validating ROI for AI-augmented analytics.

2. Real-Time Streaming Analytics for Acute Care

Real-time analytics from bedside monitors, lab systems, and EHRs enable sepsis prediction, deterioration alerts, and ICU optimization. Major academic centers are deploying streaming platforms that process millions of events per second to support time-critical clinical decisions.

3. Cloud-Native Healthcare Data Lakes

Hospitals increasingly consolidate disparate data into cloud-native lakehouses. Veradigm leverages AWS infrastructure (e.g., AWS HealthLake and AWS Marketplace) for scalable healthcare data solutions to enhance analytics offerings, reflecting an industry-wide shift toward elastic, vendor-neutral infrastructure.

4. Federated and Privacy-Preserving Analytics

Truveta raised around USD 320 million in a Series C funding round in January 2025, exemplifies federated analytics models that aggregate de-identified patient records across multiple health systems without transferring raw data, enabling large-scale real-world evidence research.

5. Outcomes-Based and Risk-Sharing Vendor Contracts

Payers and providers are tying analytics-vendor compensation to measurable clinical and financial outcomes such as readmission reduction and risk-adjustment lift. This shift rewards vendors who can demonstrate quantifiable impact on cost and quality KPIs.

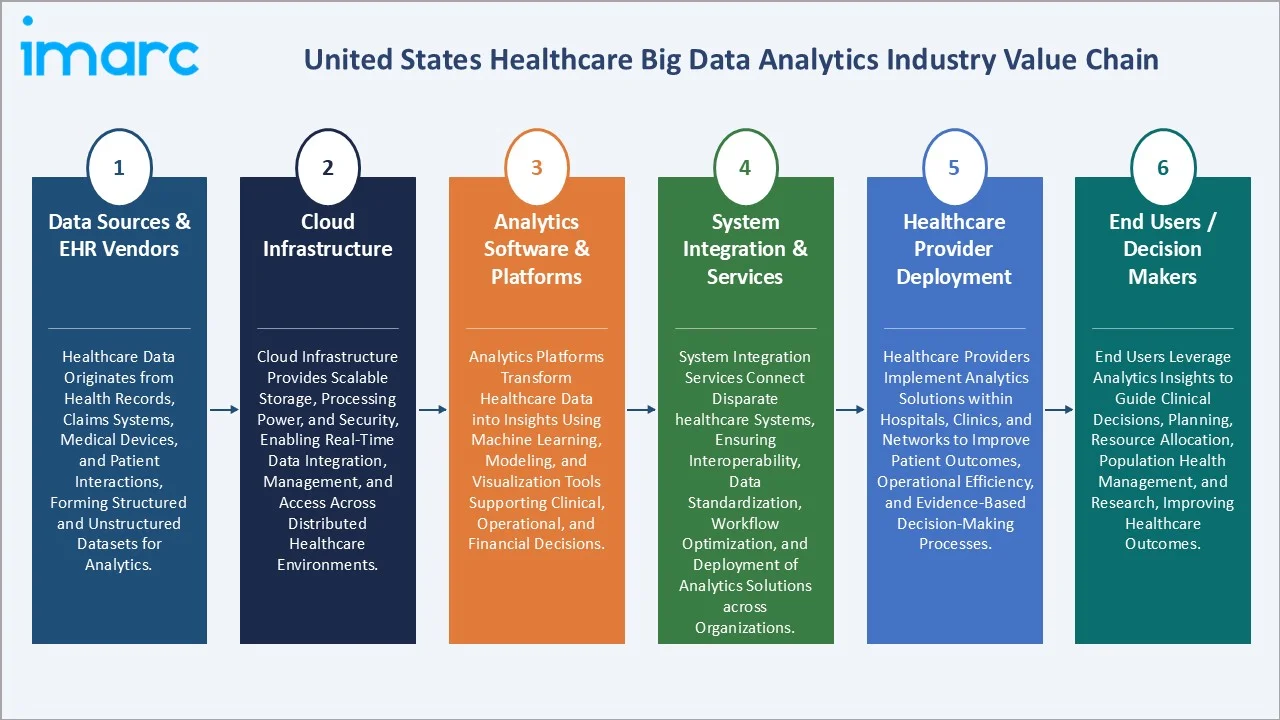

Industry Value Chain Analysis

The U.S. healthcare big data analytics value chain comprises six interconnected stages, each populated by specialized participants. The chain converts raw clinical and operational data into actionable insights consumed by clinicians, administrators, payers, and researchers.

|

Stage |

Description |

|

Data Sources & EHR Vendors |

Healthcare data originates from health records, claims systems, medical devices, and patient interactions, forming structured and unstructured datasets for analytics. |

|

Cloud Infrastructure |

Cloud infrastructure provides scalable storage, processing power, and security, enabling real-time data integration, management, and access across distributed healthcare environments. |

|

Analytics Software & Platforms |

Analytics platforms transform healthcare data into insights using machine learning, modeling, and visualization tools supporting clinical, operational, and financial decisions. |

|

System Integration & Services |

System integration services connect disparate healthcare systems, ensuring interoperability, data standardization, workflow optimization, and deployment of analytics solutions across organizations. |

|

Healthcare Provider Deployment |

Healthcare providers implement analytics solutions within hospitals, clinics, and networks to improve patient outcomes, operational efficiency, and evidence-based decision-making processes. |

|

End Users / Decision Makers |

End users leverage analytics insights to guide clinical decisions, planning, resource allocation, population health management, and research, improving healthcare outcomes. |

Tier-1 platform vendors capture the highest economic value by combining proprietary algorithms, scaled data assets, and direct enterprise relationships. Cloud hyperscalers extract recurring infrastructure margins, while integrators monetize implementation complexity.

Technology Landscape in the U.S. Healthcare Big Data Analytics Industry

Artificial Intelligence and Machine Learning

AI and ML form the technological backbone of modern healthcare analytics. Predictive models for sepsis, readmission, and no-show risk are now standard at Tier-1 health systems. Approximately 71% of U.S. hospitals reported deploying EHR-integrated predictive AI in 2024.

Cloud Computing and Data Lakehouses

Cloud adoption is accelerating across U.S. healthcare, replacing legacy on-premises systems with scalable architectures. Data lakehouse approaches unify structured and unstructured datasets, improving analytics efficiency and flexibility, though exact cost savings depend on implementation and are not uniformly standardized.

Natural Language Processing for Unstructured Data

NLP is increasingly applied to extract insights from unstructured clinical data such as physician notes and reports, which constitute a large share of healthcare information. It supports use cases in clinical decision-making, research, and real-world evidence generation.

Interoperability Standards and FHIR APIs

FHIR-based APIs, promoted under the 21st Century Cures Act, are advancing interoperability in U.S. healthcare. The HTI-1 final rule mandates standardized API access in certified health IT, improving data exchange and enabling broader analytics integration.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Component | Software | 38.0% | 2025 |

| Analytics Type | Descriptive Analytics | 35.0% | 2025 |

| Delivery Models | On-Demand Delivery Model | 60.0% | 2025 |

| Application | Clinical Analytics | 36.0% | 2025 |

| End User | Hospitals and Clinics | 50.0% | 2025 |

| Region | South | 29.0% | 2025 |

By Component

Software dominates with a 38.0% share in 2025, driven by EHR-integrated analytics platforms, AI-powered clinical decision support, and population health management suites. Vendors are embedding generative AI, real-time streaming, and predictive modeling into next-generation software.

To access detailed market analysis, Request Sample

Services account for 34.6% in 2025, supporting implementation, integration, training, and managed analytics. Hardware represents 27.4%, encompassing data storage, network infrastructure, firewalls, VPNs, and on-site servers required for hybrid deployments and HIPAA-compliant data residency.

By Delivery Model

On-Demand (cloud-based) delivery commands 60.0% of the market in 2025, driven by lower upfront costs, faster deployment cycles, and elastic scalability. Healthcare organizations increasingly favor subscription-based models that align expenditure with utilization.

On-Premise delivery retains 40.0% in 2025, anchored by large IDNs, government health systems, and providers in regulated jurisdictions requiring strict data residency, audit-trail control, and integration with legacy clinical infrastructure.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Companies |

|

South |

29.0% |

Dense healthcare networks across Texas, Florida, Georgia; aging Medicare population; HCA Healthcare and Tenet hubs |

Optum, Tempus, McKesson, Health Catalyst |

|

West |

27.1% |

California digital health ecosystem; Stanford and UCSF analytics innovation; cloud-tech convergence |

Oracle Health, Salesforce Health Cloud, Innovaccer |

|

Northeast |

23.2% |

Major academic medical centers (Mass General, Johns Hopkins); insurer headquarters; pharma R&D analytics demand |

IBM (Merative), IQVIA, Verisk Health, Arcadia |

|

Midwest |

20.7% |

Mayo Clinic and Cleveland Clinic anchor research analytics; large rural population health programs |

Epic Systems, Cerner (Oracle), Allscripts (Veradigm) |

The South leads with 29.0% share in 2025, supported by Texas (Houston Methodist, Tampa General investments), and Florida (Mayo Jacksonville). The region's aging population and high chronic-disease prevalence drive substantial demand for population health and predictive analytics.

The West (27.1%) is propelled by California's tech-healthcare convergence, with companies like Salesforce, Oracle, and Innovaccer headquartered or operating major R&D centers. The Northeast (23.2%) leverages dense academic medical centers and pharma analytics demand, while the Midwest (20.7%) benefits from Mayo Clinic and Cleveland Clinic, both pioneering AI-driven clinical analytics initiatives.

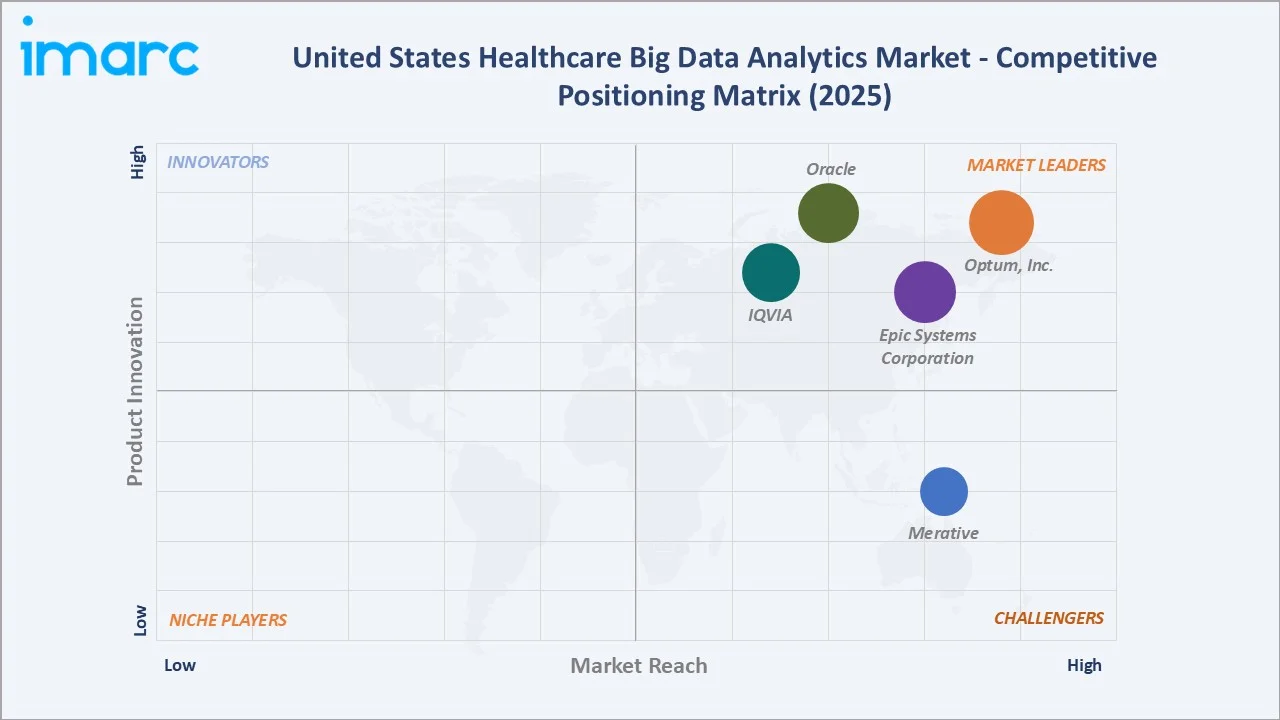

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Optum, Inc. |

Optum Health |

Leader |

Vertically integrated payer-provider analytics; population health |

|

Oracle |

Oracle Health |

Leader |

Acute care EHR + analytics suite; cloud-native architecture |

|

Epic Systems Corporation |

Epic |

Leader |

Largest installed EHR base; Cosmos research dataset |

|

IQVIA |

IQVIA Connected Intelligence |

Leader |

Real-world evidence; life-sciences analytics depth |

|

Merative |

Truven |

Challenger |

Imaging analytics; payer claims platforms |

The U.S. healthcare big data analytics market is moderately concentrated at the top, with players like Optum leveraging integration with UnitedHealth Group (~USD 400B revenue in 2024), while Epic Systems’ Cosmos database spans over 300M patient records, supporting large-scale research analytics.

Key Company Profiles

Optum, Inc.

Optum, based in Minnesota, is the health services division of UnitedHealth Group, generating over USD 250 billion revenue in 2024. Its Optum Insight unit provides analytics, technology, and consulting services, supporting healthcare providers, payers, and government programs nationwide.

- Product & Service Portfolio: Optum offers healthcare analytics, revenue cycle management, population health solutions, risk adjustment tools, pharmacy benefit analytics (OptumRx), and data-driven platforms through Optum Insight for providers, payers, and life sciences organizations.

- Recent Developments: In 2025 - 2026, Optum, Inc. announced the expansion of its healthcare analytics and care delivery capabilities as part of a strategic shift toward value-based care models. The company is enhancing operational efficiency and building high-performing provider networks to improve clinical outcomes and cost management across the U.S. healthcare ecosystem.

- Strategic Focus: Optum focuses on integrating data analytics, care delivery, and pharmacy services to advance value-based care, improve clinical outcomes, and enhance cost efficiency across payer-provider ecosystems.

Oracle

Oracle Health, formed after Oracle Corporation acquired Cerner Corporation for USD 28.3 billion in 2021, delivers cloud-based healthcare IT solutions, including EHR and analytics platforms, supporting hospitals and health systems across the United States.

- Product & Service Portfolio: Oracle Health offers electronic health record systems (Millennium), population health analytics (HealtheIntent), device connectivity (CareAware), and cloud-based data infrastructure through Oracle Cloud Infrastructure for healthcare providers and payers.

- Recent Developments: In 2024 - 2025, Oracle Corporation introduced a next-generation, cloud-based electronic health record (EHR) platform embedded with generative AI and voice-enabled capabilities. The solution integrates conversational search, clinical AI agents, and automated workflows to modernize legacy systems, reduce administrative burden, and enhance provider efficiency across U.S. healthcare organizations.

- Strategic Focus: Oracle Health focuses on cloud-native EHR modernization, voice-enabled clinical workflows, and integration with Oracle Cloud Infrastructure for analytics scalability.

Epic Systems Corporation

Epic Systems Corporation, based in Verona, Wisconsin, is a leading privately held EHR provider whose platforms support hundreds of millions of patient records globally, with strong U.S. hospital adoption and a growing analytics ecosystem including Cosmos for large-scale clinical research.

- Product & Service Portfolio: Epic offers integrated analytics and data platforms including Cosmos (research dataset), SlicerDicer (self-service analytics), Cogito (data warehouse), Caboodle (enterprise data platform), and Healthy Planet for population health management.

- Recent Developments: In 2025–2026, Epic Systems Corporation expanded generative AI capabilities across its EHR ecosystem, introducing tools such as AI-generated in-basket message drafting, ambient documentation (AI charting), and AI-assisted coding support to streamline clinical workflows and reduce administrative burden.

- Strategic Focus: Epic focuses on tightly integrated clinical and analytics platforms, expanding Cosmos for research collaboration, and embedding AI-driven capabilities directly within its native EHR workflows.

Market Concentration Analysis

The U.S. healthcare big data analytics market displays a moderately concentrated structure at the top, with Optum Inc., Oracle, Epic Systems Corporation, IQVIA collectively accounting for an estimated 35-40% of revenue in 2025. These leaders benefit from deep enterprise relationships, vast proprietary data assets, and substantial R&D investments running into hundreds of millions of dollars annually.

Mid-tier players, including Merative and Veradigm, contribute a significant share by focusing on specialized areas such as imaging, claims analytics, and oncology data, while the remaining market is fragmented among niche vendors and emerging firms like Innovaccer, Tempus, and Others

Consolidation activity remains brisk. Oracle's prior USD 28.3 Billion Cerner deal exemplify the strategic pursuit of data scale, AI talent, and enterprise distribution. Venture funding into specialized healthcare AI startups exceeded USD 11 Billion in 2024, signaling continued fragmentation pressure as new categories such as ambient AI and federated analytics emerge.

Investment & Growth Opportunities

Fastest-Growing Segments

Cognitive and predictive analytics are among the fastest-growing segments, driven by AI adoption and value-based care. Cloud-based (on-demand) delivery models are expanding rapidly due to scalability and cost-efficiency, steadily increasing their share of healthcare analytics deployments.

Emerging End-User Categories

Beyond hospitals, payers including finance and insurance entities are expanding analytics adoption for risk adjustment and fraud detection. Research organizations are also growing, supported by U.S. Food and Drug Administration real-world evidence initiatives and data-driven clinical development.

Venture & Strategic Investment Trends

Healthcare AI and analytics startups in the U.S. continue attracting strong venture funding. Companies like Truveta and Carta Healthcare raised significant capital, strategic acquirers including Optum and Oracle continue absorbing specialized vendors.

Future Market Outlook (2026-2034)

The U.S. healthcare big data analytics market is projected to expand from USD 24.71 Billion in 2025 to USD 62.43 Billion by 2034 — adding USD 37.72 Billion of incremental value at a 10.9% CAGR. Three forces will shape this trajectory: pervasive generative AI integration, federated data architectures, and outcomes-based commercial models that reward measurable clinical impact.

By 2030, the market is expected to reach USD 41.35 Billion, with cloud-based deployments crossing 70% of revenue. Generative AI applications are forecast to be embedded in over 80% of new analytics platform purchases, accelerating the transition from descriptive toward prescriptive and cognitive analytics across oncology, cardiology, and behavioral health.

By 2034, analytics will converge with broader workflow automation, blurring boundaries between EHR, analytics, and clinical AI. Vendors investing in proprietary datasets, validated clinical AI, and scaled cloud infrastructure are best positioned to capture disproportionate value as U.S. healthcare continues its data-driven transformation.

Research Methodology

Primary Research

Primary research conducted in 2024-2025 included structured interviews with chief information officers, chief analytics officers, and clinical informaticists at 60+ U.S. hospitals and IDNs, alongside senior executives at major analytics vendors and payers.

Secondary Research

Secondary sources include vendor financial filings (UnitedHealth, Oracle, IQVIA), CMS National Health Expenditure Data, ONC Health IT statistics, peer-reviewed journals, and industry reports from KLAS, Black Book, and HIMSS Analytics.

Forecasting Models

Market sizing combines top-down (national health expenditure × analytics spend ratio) and bottom-up (segment revenue aggregation) approaches, incorporating macroeconomic indicators, federal IT spending, and scenario analysis.

United States Healthcare Big Data Analytics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Services, Software (Electronic Health Record Software, Practice Management, Workforce Management), Hardware (Data Storage, Routers, Firewalls, Virtual Private Networks, E-Mail Servers, Others) |

| Analytics Types Covered | Descriptive Analytics, Predictive Analytics, Prescriptive Analytics, Cognitive Analytics |

| Delivery Models Covered | On-Premise Delivery Model, On-Demand Delivery Model |

| Applications Covered | Financial Analytics, Clinical Analytics, Operational Analytics, Others |

| End Users Covered | Hospitals and Clinics, Finance and Insurance Agencies, Research Organizations |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Optum, Inc., Oracle, Epic Systems Corporation, IQVIA, Merative, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Healthcare Big Data Analytics Market Report

The U.S. healthcare big data analytics market was valued at USD 24.71 Billion in 2025, driven by EHR adoption, AI integration, and value-based care.

The market is projected to reach USD 62.43 Billion by 2034, growing at a 10.9% CAGR during 2026-2034, supported by AI maturation and rising population health analytics demand.

Software leads with a 38.0% share in 2025, anchored by EHR-integrated analytics, AI-powered clinical decision tools, and population health software.

On-Demand (cloud-based) delivery commands 60.0% share in 2025, reflecting the shift toward scalable, subscription-based analytics platforms.

The South leads with 29.0% share in 2025, driven by dense healthcare ecosystems in Texas, Florida, and Georgia and substantial Medicare populations.

Key drivers include rising healthcare data volumes, value-based care transition, AI and cloud advancements, federal interoperability mandates, and chronic-disease analytics demand.

Major challenges include data privacy and cybersecurity threats, interoperability gaps, healthcare data talent shortage, high implementation costs, and algorithmic bias scrutiny.

Leading companies include Optum Inc., Oracle, Epic Systems Corporation, IQVIA, and Merative.

Services account for 34.6% in 2025, supporting implementation, integration, training, and managed analytics across hospitals, payers, and research organizations.

AI enables predictive risk stratification, ambient documentation, and real-time decision support. About 71% of U.S. hospitals deployed EHR-integrated predictive AI in 2024.

Cloud platforms reduce upfront infrastructure costs, accelerate deployment, enable elastic scalability, and support advanced AI workloads behind the 60.0% On-Demand market share.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)