United States Implantable Medical Devices Market Size, Share, Trends and Forecast by Product, Material, End User, and Region, 2026-2034

United States Implantable Medical Devices Market Size and Share:

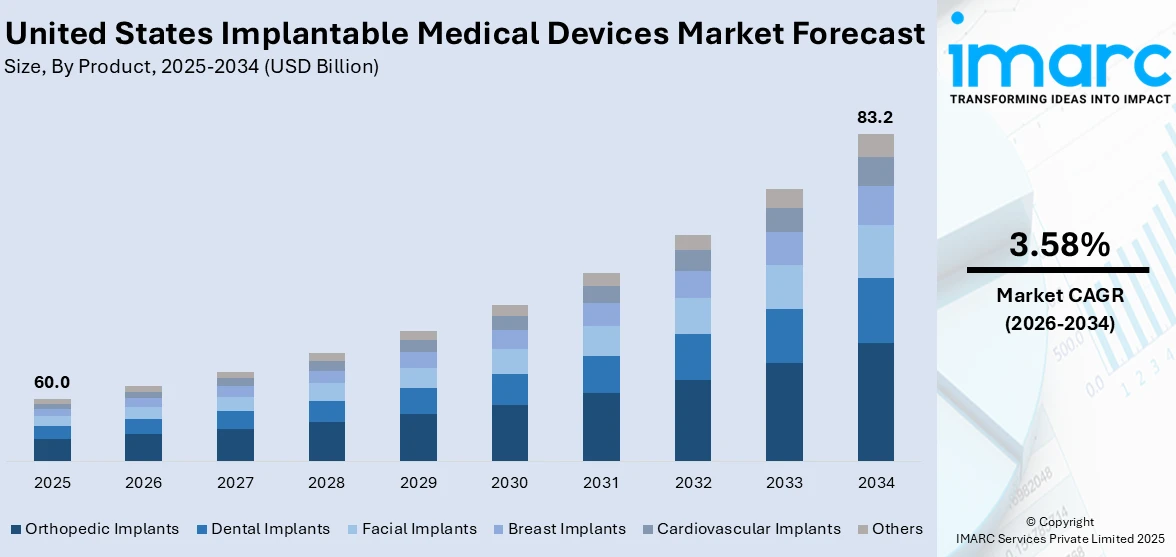

The United States implantable medical devices market size was valued at USD 60.0 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 83.2 Billion by 2034, exhibiting a CAGR of 3.58% from 2026-2034. Northeast currently dominates the market, holding a market share of 35.0% in 2025. The market is driven by an aging population, increasing prevalence of chronic conditions, and a growing preference for minimally invasive (MI) treatments. Advances in medical technology and supportive healthcare infrastructure continue to fuel innovation and adoption, making these devices essential in modern medical care further increasing the United States implantable medical devices market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 60.0 Billion |

|

Market Forecast in 2034

|

USD 83.2 Billion |

| Market Growth Rate (2026-2034) | 3.58% |

One of the key drivers of the U.S. implantable medical devices market is the growing elderly population, which is more prone to chronic conditions like cardiovascular diseases, arthritis, and neurological disorders. In 2022, around 58 million Americans aged 65 and older represented 17.3% of the population, and this is projected to rise to 22% by 2040. As people age, the need for devices such as pacemakers, joint implants, and neurostimulators increases. This demographic shift not only drives demand but also pressures healthcare systems to adopt long-term solutions. Implantable devices provide effective, life-enhancing treatments, making them an essential part of managing aging-related health issues in the U.S. healthcare system.

To get more information on this market Request Sample

The continuous evolution of medical technology significantly propels the U.S. implantable medical devices market. Innovations such as bioresorbable stents, smart implants with wireless monitoring, and three dimensional (3D)-printed devices are transforming patient care. These advancements improve the precision, safety, and longevity of implants, making them more appealing to both healthcare providers and patients. Additionally, integration of artificial intelligence (AI) and data analytics in some implantable systems allows for real-time health monitoring and predictive diagnostics. As technology becomes more sophisticated and accessible, it expands the scope and success rates of implant procedures, driving wider adoption and market growth across multiple medical fields.

United States Implantable Medical Devices Market Trends:

Integration of Smart Technologies and Wireless Connectivity

A major United States implantable medical devices market trends is the integration of smart technologies and wireless connectivity. Modern implantable devices, such as pacemakers and neurostimulators, now feature wireless capabilities, allowing real-time data transmission for continuous patient monitoring. This shift enables healthcare providers to track patient progress remotely and make timely adjustments to treatments. The use of artificial intelligence in these devices is also enhancing diagnostic precision and personalizing therapy, leading to better patient outcomes. As telemedicine and remote healthcare management become more prevalent, the demand for these advanced, connected implantable devices continues to rise.

Advancements in 3D Printing for Personalized Implants

3D printing is revolutionizing the production of implantable medical devices by enabling highly personalized solutions. According to the U.S. Food and Drug Administration (FDA), over 100 devices currently on the market were manufactured using 3D printing techniques. These include patient-matched implants, such as knee replacements and facial reconstruction devices, tailored to fit a patient's unique anatomy. This technology allows for the creation of custom-designed implants that improve the fit, function, and comfort, especially in areas like orthopedics and dental prosthetics, where precision is critical. The ability to print complex structures that were previously impossible to manufacture enhances the overall effectiveness of implants. With continued advancements in 3D printing materials, the trend is expected to expand, leading to more individualized treatment options and better clinical outcomes for patients, further transforming the landscape of medical care.

Emphasis on Minimally Invasive Procedures

Minimally invasive procedures are becoming increasingly popular in the U.S. implantable medical devices market due to their numerous advantages. These procedures offer faster recovery times, reduced risks of complications, and shorter hospital stays, improving patient outcomes and experiences. Healthcare providers are adopting devices that can be implanted through smaller incisions or via catheter-based techniques, which are especially common in cardiovascular treatments. Devices such as stents and heart valves are now often delivered using minimally invasive methods, reducing the need for traditional open surgeries. As patients seek less invasive treatment options, demand for these advanced devices continues to rise. This trend is driving innovation and the development of new implantable devices tailored for minimally invasive procedures, further shaping the United States implantable medical devices market growth.

United States Implantable Medical Devices Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the United States implantable medical devices market, along with forecast at the regional, and country levels from 2026-2034. The market has been categorized based on product, material, and end user.

Analysis by Product:

- Orthopedic Implants

- Dental Implants

- Facial Implants

- Breast Implants

- Cardiovascular Implants

- Others

Based on the United States implantable medical devices market forecast, the orthopedic implants hold the majority share of 46.0% driven by the rising prevalence of musculoskeletal disorders, including arthritis, osteoporosis, and sports-related injuries. As the aging population increases, the demand for joint replacements, spinal implants, and fracture fixation devices grows. Orthopedic implants are crucial in restoring mobility, improving quality of life, and enhancing patient outcomes. Advances in materials, such as bioactive ceramics and titanium alloys, have improved the durability and functionality of these implants, making them more reliable. Furthermore, the development of minimally invasive surgical techniques has made these procedures less risky and more accessible, further boosting their demand and market share. The rising focus on personalized care also plays a role in the growing use of customized orthopedic implants.

Analysis by Material:

- Polymers

- Metals

- Ceramics

- Biologics

Metals account for the majority share of 48.8% driven by their excellent strength, durability, and biocompatibility. Materials such as titanium, stainless steel, and cobalt-chromium alloys are commonly used in implants like orthopedic joints, dental implants, and cardiovascular devices due to their ability to withstand stress and corrosion within the human body. These metals are also highly favored for their resistance to wear and tear, making them ideal for long-term use. Additionally, advancements in metal alloy technology, including the development of lightweight, yet strong materials, have further enhanced their appeal in implantable devices. The increasing demand for durable and long-lasting implants in an aging population continues to drive the dominance of metals in the market.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

- Hospitals

- Ambulatory Surgery Centers (ASCs)

- Clinics

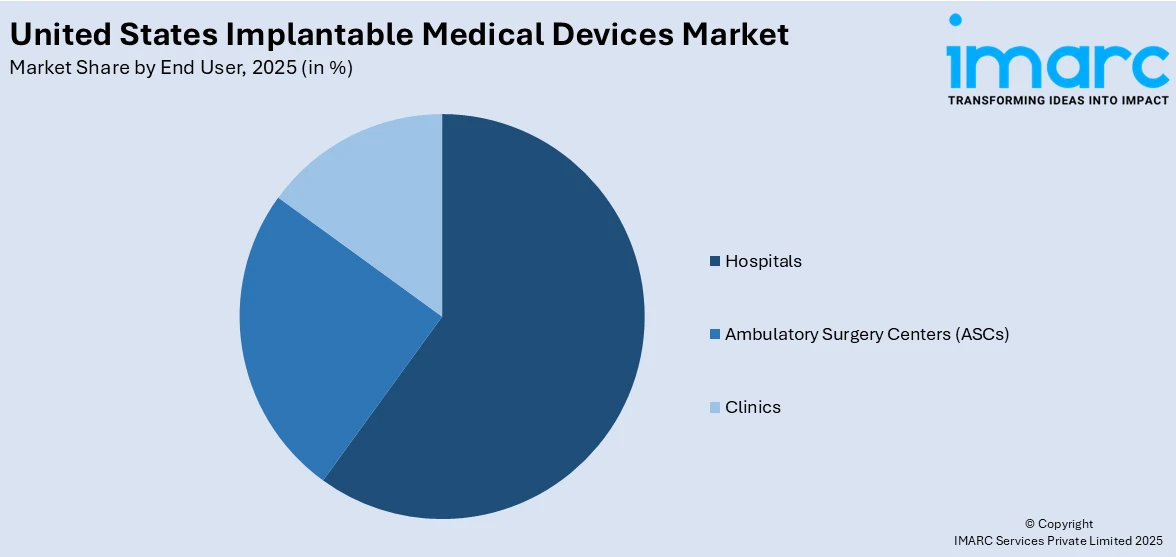

Hospitals dominate the U.S. implantable medical devices market, holding a 60.0% share, due to their central role in patient care and advanced surgical procedures. Hospitals are primary centers for implant surgeries, including joint replacements, cardiovascular surgeries, and spinal treatments, where a wide range of implantable devices are required. They have the necessary infrastructure, specialized healthcare professionals, and access to advanced technology to handle complex procedures. Moreover, hospitals tend to have higher patient volumes and specialized units dedicated to the treatment of chronic conditions, such as musculoskeletal disorders and heart diseases, further driving the demand for implantable devices. The increasing preference for treatments that require inpatient care, alongside advancements in medical technologies, strengthens hospitals' dominance in this sector.

Analysis by Region:

- Northeast

- Midwest

- South

- West

The Northeast region leads the U.S. implantable medical devices market, holding a 35.0% share, due to its concentration of world-class healthcare facilities, research institutions, and medical device manufacturers. Major cities in the Northeast, like Boston and New York, are hubs for medical innovation and home to leading hospitals and medical centers that specialize in advanced surgeries requiring implantable devices. The region’s strong healthcare infrastructure, coupled with high patient demand for treatments related to chronic diseases, orthopedic conditions, and cardiovascular issues, boosts market growth. Additionally, the presence of key players in the medical device industry accelerates technological advancements and manufacturing capabilities. The Northeast's demographic profile, with an aging population, also drives the demand for implantable devices, making it a dominant region in the United States implantable medical devices market outlook.

Competitive Landscape:

The competitive landscape in the U.S. implantable medical devices market is highly dynamic and fragmented, characterized by the presence of both established global players and emerging innovators. Companies are focused on research and development to create advanced, minimally invasive, and personalized solutions. Strategic collaborations, mergers, and acquisitions are common, as companies seek to expand their product portfolios and enter new markets. Additionally, the adoption of new technologies such as 3D printing, AI integration, and wireless connectivity is increasing competition. Regulatory compliance and reimbursement policies play a significant role in shaping market dynamics, with companies striving to meet stringent standards. Companies are also focusing on patient-centric approaches, improving device performance, and offering better clinical outcomes to stay competitive.

The report provides a comprehensive analysis of the competitive landscape in the United States implantable medical devices market with detailed profiles of all major companies.

Latest News and Developments:

- January 2025: Elutia fully launched EluPro, an FDA-cleared antibiotic-eluting biomatrix for pacemakers, defibrillators, and neurostimulators. Following strong pilot demand, EluPro gained approval in 136 hospitals and four GPOs. It combines rifampin and minocycline with regenerative biomatrix to reduce infection and improve surgical healing outcomes.

- January 2025: Aptyx obtained Medical Murray’s Charlotte, North Carolina facility to launch Aptyx Interventional Systems. The move strengthened its capabilities in catheter-based interventional and implantable products, including stents and delivery systems, while expanding ISO Class 7 manufacturing and biotextile expertise to serve high-growth structural heart and vascular markets.

- December 2024: Sequana Medical standard FDA approval for alfapump, an active implantable device for recurrent or refractory ascites owing to liver cirrhosis. The device significantly reduces the need for paracentesis and improves patient quality of life, with commercial launch planned for the second half of 2025.

- October 2024: Johnson & Johnson completed its acquisition of V-Wave Ltd., adding the Ventura® Interatrial Shunt to its MedTech portfolio. This implantable device targets heart failure with reduced ejection fraction.

- July 2024: Neuspera Medical raised USD 23 Million in Series D funding to support FDA premarket approval of its ultra-miniaturized, implantable Neuspera Sacral Neuromodulation System for urinary urge incontinence.

United States Implantable Medical Devices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Orthopedic Implants, Dental Implants, Facial Implants, Breast Implants, Cardiovascular Implants, Others |

| Materials Covered | Polymers, Metals, Ceramics, Biologics |

| End Users Covered | Hospitals, Ambulatory Surgery Centers (ASCs), Clinics |

| Regions Covered | Northeast, Midwest, South, West |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States implantable medical devices market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the United States implantable medical devices market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States implantable medical devices industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Implantable Medical Devices Market Report

The United States implantable medical devices market was valued at USD 60.0 Billion in 2025.

The United States implantable medical devices market is projected to exhibit a CAGR of 3.58% during 2026-2034, reaching a value of USD 83.2 Billion by 2034.

The U.S. implantable medical devices market is driven by several key factors. Foremost is the increasing prevalence of chronic diseases, such as cardiovascular disorders, diabetes, and orthopedic conditions, which necessitate long-term medical interventions. Advancements in medical technology, including the development of minimally invasive procedures and smart implants, have enhanced the efficacy and appeal of these devices

The Northeast region leads the U.S. implantable medical devices market, holding a 35.0% share, due to its advanced healthcare infrastructure, concentration of leading medical institutions, and robust research and development activities. This environment fosters innovation and adoption of cutting-edge implantable technologies, contributing to the region's market dominance.?

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)