United States Olive Oil Market Size, Share, Trends and Forecast by Type, Distribution Channel, Application, and Region 2026-2034

United States Olive Oil Market Size, Share, Trends & Forecast (2026-2034)

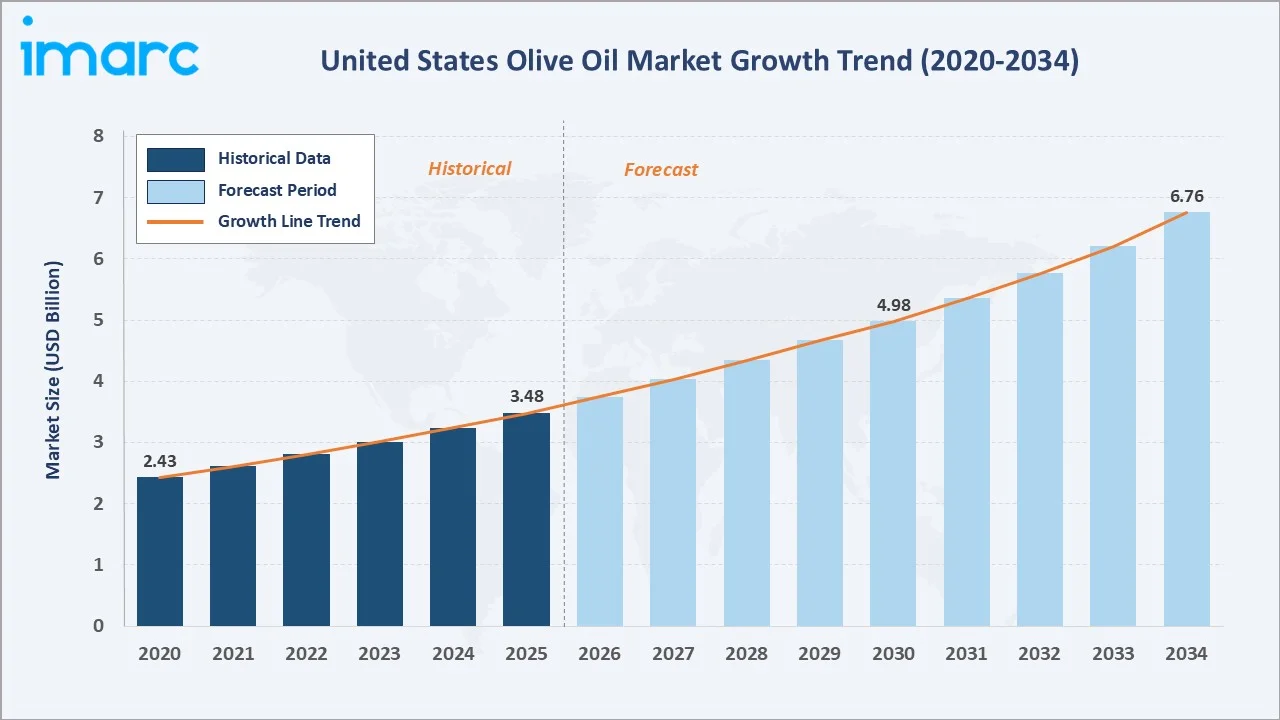

The United States olive oil market reached USD 3.48 Billion in 2025 and is projected to reach USD 6.76 Billion by 2034, growing at a CAGR of 7.42% during 2026-2034. Rising health consciousness among consumers, the surging popularity of the Mediterranean diet, and expanding applications of olive oil across food, cosmetics, and pharmaceutical sectors are key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.48 Billion |

|

Forecast Market Size (2034) |

USD 6.76 Billion |

|

CAGR (2026-2034) |

7.42% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

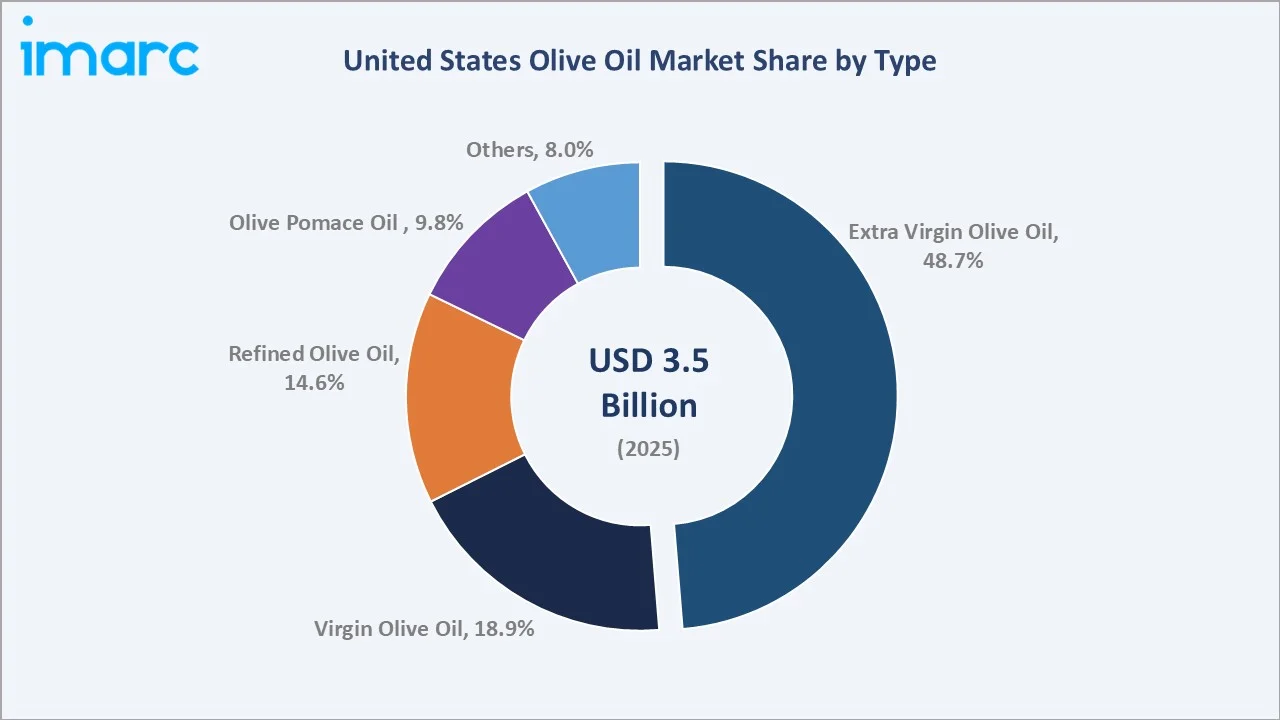

Largest Segment (Type) |

Extra Virgin Olive Oil – 48.7% share (2025) |

|

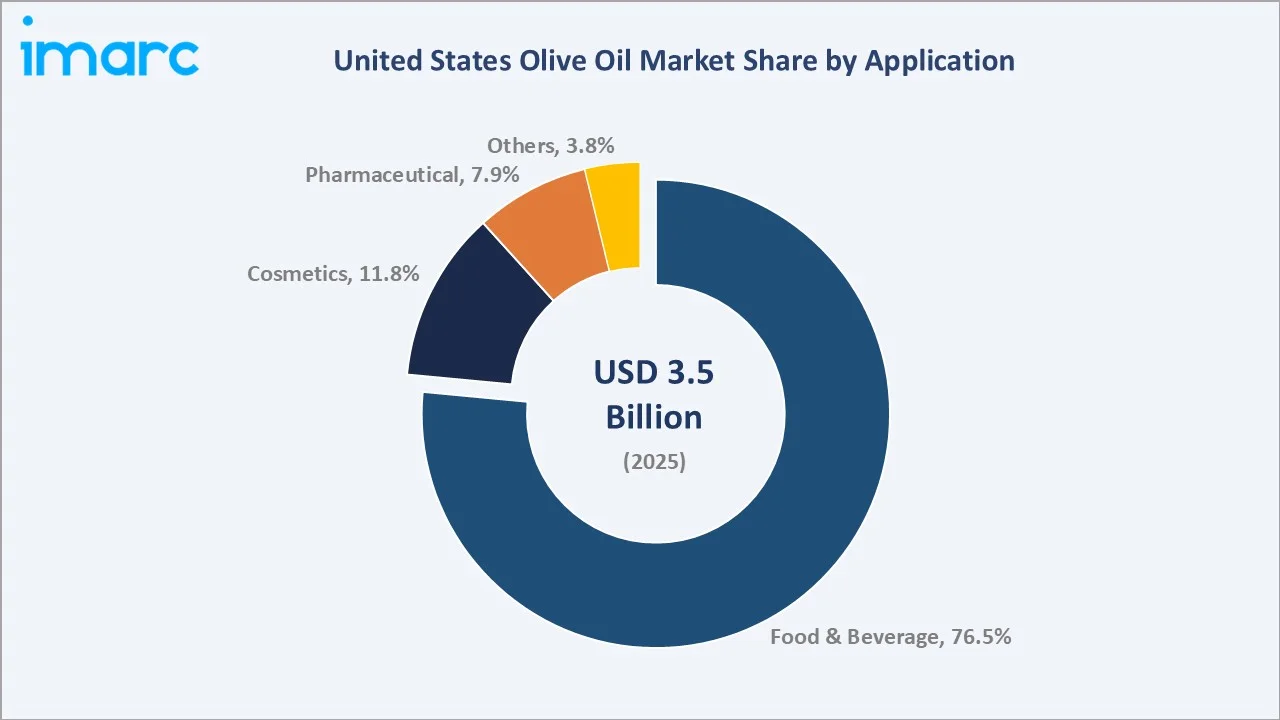

Largest Segment (Application) |

Food and Beverage – 76.5% share (2025) |

|

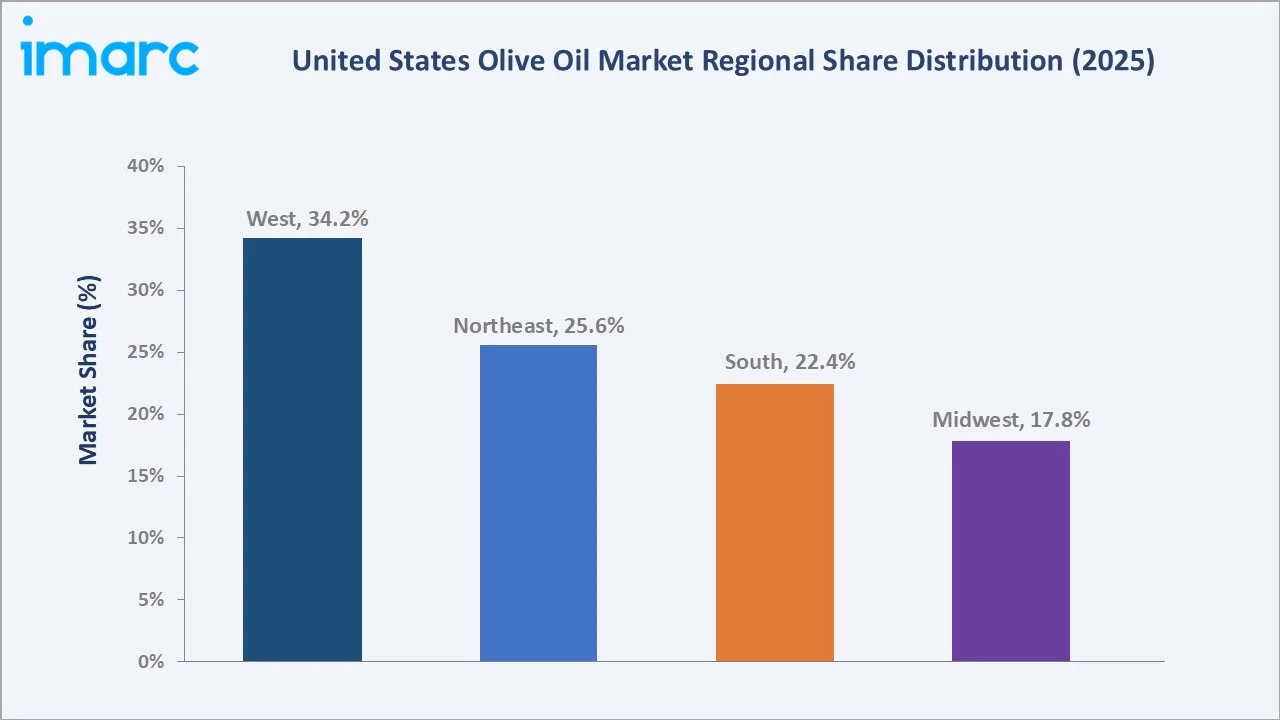

Largest Region |

West – 34.2% share (2025) |

To get more information on this market, Request Sample

The West region dominates, holding a 34.2% market share in 2025, while extra virgin olive oil leads type demand at 48.7%. The food and beverage segment remains the dominant application with a 76.5% share. The United States, which has emerged as the world's second-largest consumer of olive oil, is witnessing growing premiumization driven by increasing demand for authentic Mediterranean products and single-origin extra virgin olive oil varieties.

With applications spanning food and beverage manufacturing, cosmetic formulation, and pharmaceutical production, the market is expected to continue expanding, supported by increasing domestic production in California and a record-high USDA-forecast consumption of 478,000 metric tons in 2024/25.

Executive Summary

The United States olive oil market is on a sustained growth path, underpinned by increasing health consciousness, the widespread adoption of the Mediterranean diet, and the expanding use of olive oil across culinary, cosmetic, and pharmaceutical applications. The market reached USD 3.48 Billion in 2025 and is forecast to surpass USD 6.76 Billion by 2034. This trajectory reflects a healthy CAGR of 7.42% over the forecast period.

The West region leads with a 34.2% revenue share in 2025, driven by California's growing domestic olive oil production, health-conscious consumer demographics, and a thriving foodservice sector with high per-capita olive oil consumption. The Northeast follows at 25.6%, anchored by urban gourmet food cultures and strong specialty retail channels.

Extra virgin olive oil dominates the type segment at 48.7%, reflecting an accelerating premiumization trend, while food and beverage applications account for 76.5% of total market demand, encompassing retail cooking oils, restaurant use, food manufacturing, and salad dressings. Leading players, including Deoleo, Gallo Worldwide, Cargill, Incorporated, Ybarra, SOVENA, and California Olive Ranch, Inc., continue to invest in quality and digital retail channels to align with evolving consumer preferences.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Extra Virgin Olive Oil – 48.7% share (2025) |

|

Largest Segment (Application) |

Food and Beverage – 76.5% share (2025) |

|

Leading Region |

West – 34.2% revenue share (2025) |

|

Fastest Growing Segment |

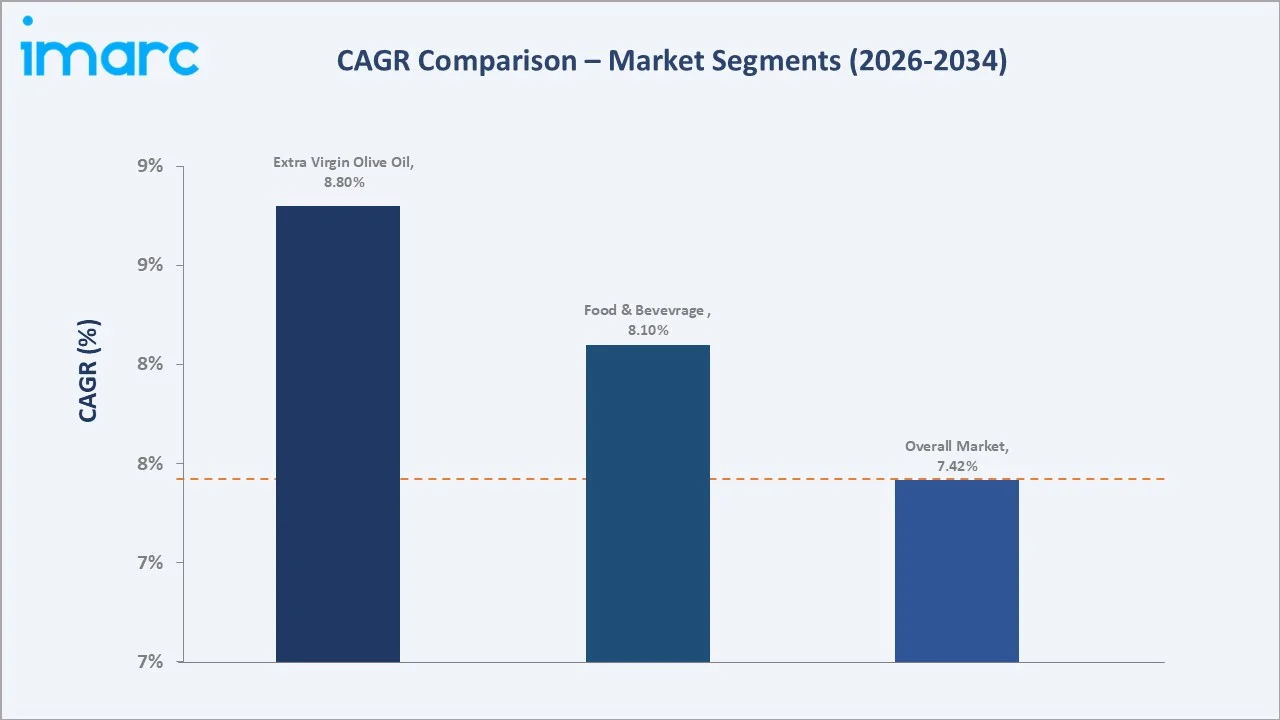

Extra Virgin Olive Oil (8.8% CAGR) |

|

Top Companies |

Deoleo, Gallo Worldwide, Cargill, Incorporated, Ybarra, SOVENA, and California Olive Ranch, Inc. |

|

Market Opportunity |

Organic and single-origin EVOO premium segment; pharmaceutical applications |

Key Analytical Observations Supporting the Above Data:

- Extra virgin olive oil accounts for 48.7% of the US olive oil market in 2025, preferred by health-conscious consumers and food service operators for its superior nutritional profile, unrefined quality, and rich flavor characteristics aligned with Mediterranean dietary patterns.

- Food and beverage represents the dominant application at 76.5% (2025), encompassing retail cooking oil, food manufacturing, restaurant kitchens, and salad dressing production, all benefiting from rising consumer demand for healthier cooking fats.

- The West region holds 34.2% of the US market in 2025, underpinned by California's growing domestic olive oil industry, high health consciousness among West Coast consumers, and a dense restaurant and foodservice ecosystem incorporating Mediterranean cuisine.

- The USDA has forecast US olive oil consumption to reach a record 478,000 metric tons in 2025/26, representing the third consecutive year of consumption growth, driven by the continued rise of health-oriented dietary choices nationally.

- Premiumization is reshaping the competitive landscape, with organic and single-origin extra virgin olive oil segments growing 22% year-over-year in 2025, driven by consumer demand for authenticity, traceability, and provenance verification.

United States Olive Oil Market Overview

Olive oil is a premium edible oil extracted from fresh olives, predominantly imported from Mediterranean countries including Spain, Italy, Greece, and Tunisia, with at least 97% of the US supply derived from imports. The market ecosystem encompasses producers and exporters in Mediterranean growing regions, import distributors, domestic California producers, food manufacturers, retail and foodservice channels, and end consumers across household, commercial, cosmetic, and pharmaceutical applications.

Macroeconomic factors, including rising per-capita health expenditure, growing awareness of cardiovascular disease prevention, and the mainstreaming of the Mediterranean dietary pattern, are primary growth catalysts. The US has overtaken Spain to become the world's second-largest olive oil consumer for the first time in 2023, and this position is expected to strengthen as health-driven food choices continue to displace conventional cooking oils such as vegetable and soybean oil in American kitchens.

Market Dynamics

To evaluate market opportunities, Request Sample

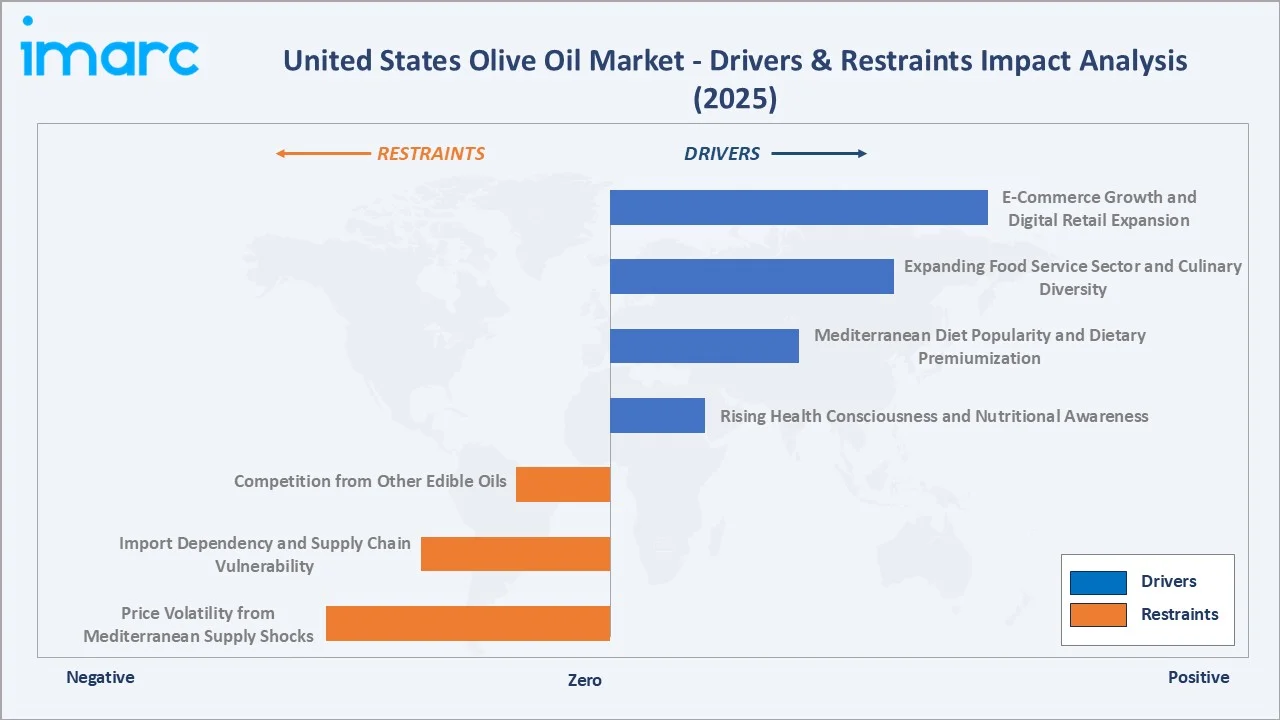

Market Drivers

- Rising Health Consciousness and Nutritional Awareness: Olive oil's documented cardiovascular benefits are driving consistent consumer trading-up from conventional cooking oils. In fact, 93% of Americans anticipate cooking as much or more in the next 12 months compared to the previous year, creating durable retail demand for premium olive oil varieties.

- Mediterranean Diet Popularity and Dietary Premiumization: The Mediterranean diet, endorsed by leading nutrition organizations and consistently ranked among the healthiest dietary patterns globally, positions olive oil as a daily essential. Growing adoption among health professionals has elevated olive oil from a specialty product to a household staple across all US income brackets.

- Expanding Food Service Sector and Culinary Diversity: Foodservice and restaurant channels account for approximately 40% of bulk olive oil purchases in the US, with major restaurant chains reformulating menus to feature olive oil as a core cooking ingredient.

- E-Commerce Growth and Digital Retail Expansion: Online retail platforms are experiencing rapid growth as a distribution channel for premium olive oil, with consumers able to access specialty, organic, and single-origin varieties not typically stocked by conventional supermarkets.

These drivers reinforce a self-sustaining premiumization cycle, health awareness elevates consumer willingness to pay for quality, which incentivizes producers to invest in certified organic and single-origin production, which in turn generates media attention and further consumer education about olive oil's health benefits.

Market Restraints

- Price Volatility from Mediterranean Supply Shocks: Severe droughts in Spain, which produce nearly half the world's olive oil, caused olive oil prices to surge over 175% in some markets between 2021 and 2024.

- Import Dependency and Supply Chain Vulnerability: At least 97% of the US olive oil supply is imported, exposing the market to geopolitical trade disruptions, shipping cost fluctuations, and import tariff changes.

- Competition from Other Edible Oils: Avocado oil, coconut oil, and domestic-origin seed oils compete for the premium cooking oil segment, particularly among younger consumers who are also responsive to social media food trends.

Market Opportunities

- Organic and PDO/PGI Certified Premium Segment Growth: Single-origin extra virgin olive oils with Protected Designation of Origin (PDO) or Protected Geographical Indication (PGI) certification command significant price premiums and are experiencing 22% year-over-year volume growth in specialty retail channels.

- Pharmaceutical and Nutraceutical Application Expansion: Olive oil's antioxidant, anti-inflammatory, and antimicrobial properties are driving increasing adoption in pharmaceutical formulations. The pharmaceutical application segment is projected to grow at 7.4% CAGR through 2030, representing a high-value diversification opportunity for premium olive oil producers and distributors.

- California Domestic Production Scale-Up: California's domestic olive oil industry is gaining market share through sustainable production methods, high polyphenol content, and fresh-harvest positioning. Domestic production reduces supply chain risk and tariff exposure while appealing to consumers prioritizing locally sourced premium food products.

Market Challenges

- Olive Oil Adulteration and Consumer Trust Issues: Adulteration of olive oil with lower-quality oils has historically undermined consumer confidence. Growing regulatory scrutiny and the adoption of DNA-sensor-based authentication technologies are addressing this issue, but reputational damage from past fraud cases continues to challenge the premium segment.

- Climate Change Impacts on Global Olive Production: Increasingly frequent and severe droughts, wildfires, and temperature extremes across Mediterranean olive-growing regions are structurally threatening long-term supply stability. As the primary production base for US imports, climate-related supply disruptions in Spain, Italy, and Greece create persistent market risk that cannot be fully mitigated by domestic production expansion.

Emerging Market Trends

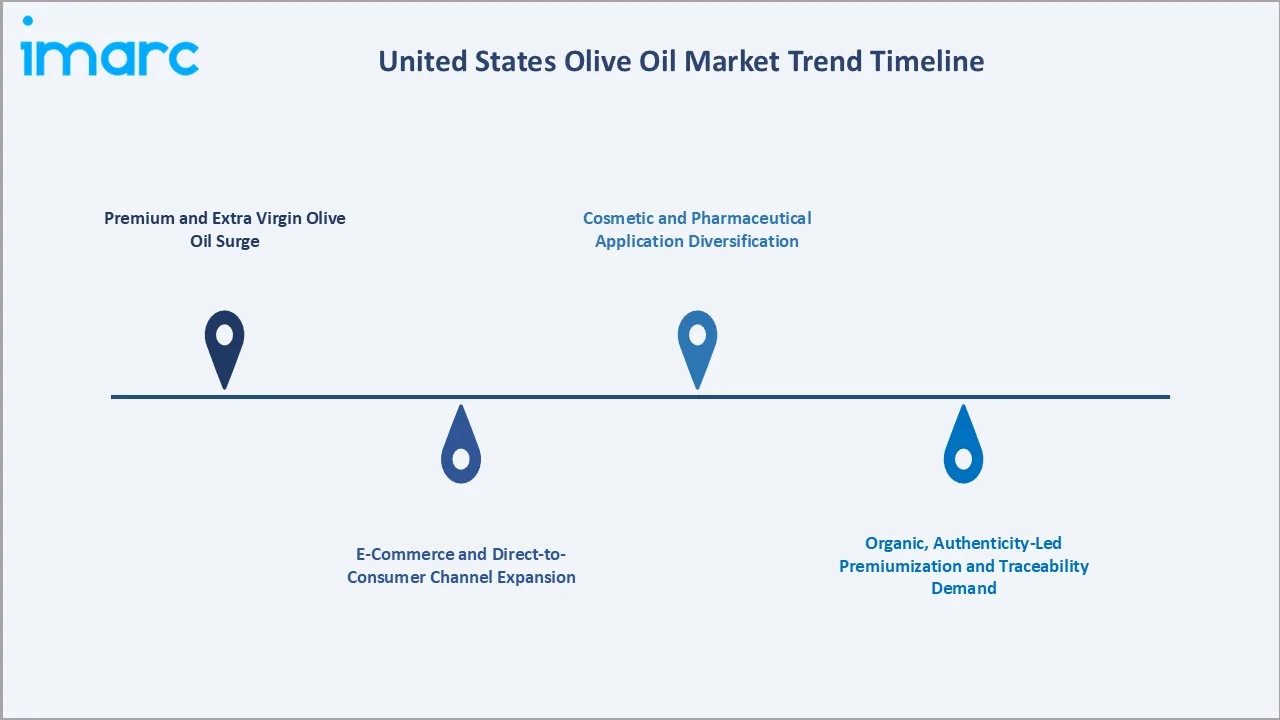

1. Premium and Extra Virgin Olive Oil Surge

The United States olive oil market is experiencing a pronounced premiumization wave, with extra virgin olive oil accounting for 48.7% of total market share in 2025 and advancing at an 8.8% CAGR through 2034. On 19 March 2026, Pompeian announced a nearly USD 10 million investment in its Baltimore headquarters, including a new high‑speed production line featuring Pompeian’s olive oil, specifically its range of high‑quality olive oils (including extra virgin olive oil).

2. E-Commerce and Direct-to-Consumer Channel Expansion

Online and direct-to-consumer (DTC) olive oil sales channels are growing rapidly, mirroring broader e-commerce trends in the premium food category. Specialty, organic, and single-origin extra virgin olive oil varieties are reaching health-conscious urban consumers through curated digital retail platforms, subscription models, and artisan food marketplaces. Domestic California producers are particularly benefiting from DTC e-commerce, enabling them to communicate freshness, harvest dates, and provenance directly to consumers without the margin compression of traditional retail distribution.

3. Organic, Authenticity-Led Premiumization and Traceability Demand

Protected Designation of Origin (PDO) and Protected Geographical Indication (PGI) certified oils are gaining mainstream retail presence, while QR-code-enabled packaging allowing consumers to trace oil provenance from specific groves to bottling facilities is becoming a key differentiator. In September 2024, research from ACS journals highlighted innovative authentication technologies, including DNA sensors capable of detecting olive oil adulteration, addressing a long-standing consumer trust challenge.

4. Cosmetic and Pharmaceutical Application Diversification

The cosmetics application segment holds an 11.8% market share in 2025 and is growing in tandem with the clean beauty and natural ingredients movement. In pharmaceutical applications, olive oil serves as a carrier oil and active ingredient in supplement formulations, topical ointments, and anti-inflammatory therapeutic products, with the pharmaceutical segment advancing at 7.4% CAGR.

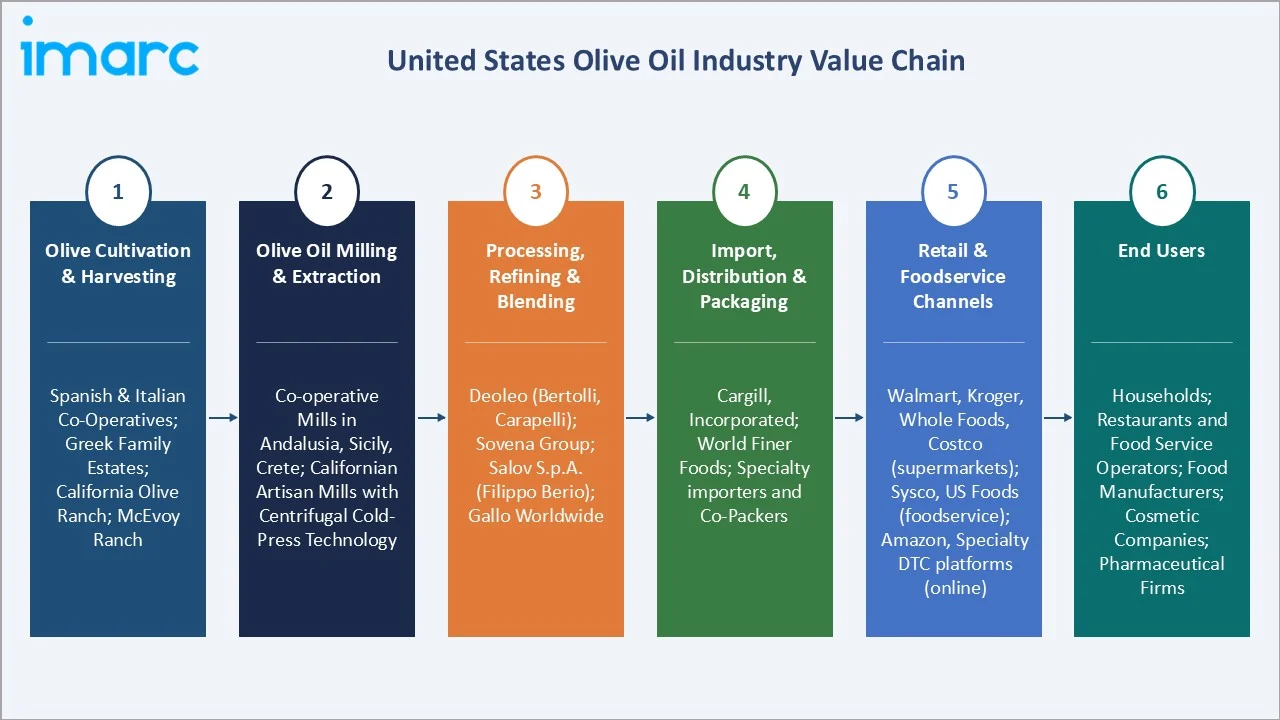

Industry Value Chain Analysis

The United States olive oil value chain spans Mediterranean olive cultivation through domestic retail and foodservice consumption, with each stage populated by specialized operators whose performance directly influences product quality, authenticity, pricing, and supply security. Import distributors and domestic packagers occupy the central commercial node of this chain, bridging Mediterranean and Californian production with diverse US retail, foodservice, and industrial end-user markets.

|

Stage |

Key Players / Examples |

|

Olive Cultivation & Harvesting |

Spanish and Italian co-operatives; Greek family estates; California Olive Ranch; McEvoy Ranch |

|

Olive Oil Milling & Extraction |

Co-operative mills in Andalusia, Sicily, Crete; Californian artisan mills with centrifugal cold-press technology |

|

Processing, Refining & Blending |

Deoleo (Bertolli, Carapelli, Carbonell); Sovena Group; Salov S.p.A. (Filippo Berio); Gallo Worldwide |

|

Import, Distribution & Packaging |

Cargill, Incorporated; World Finer Foods; specialty importers and co-packers |

|

Retail & Foodservice Channels |

Walmart, Kroger, Whole Foods, Costco (supermarkets); Sysco, US Foods (foodservice); Amazon, specialty DTC platforms (online) |

|

End Users |

Households; restaurants and food service operators; food manufacturers; cosmetic companies; pharmaceutical firms |

Technology Landscape in the United States Olive Oil Industry

Precision Olive Cultivation and Harvest Technology

California's domestic olive oil industry is deploying precision agriculture technologies to optimize olive grove management and harvest timing. High-density mechanical harvesting systems, capable of processing entire rows of olive trees without manual labor, are significantly reducing production costs and enabling California producers to achieve extraction quality standards competitive with traditional Mediterranean hand-harvested premium oils.

Cold-Press Extraction and Quality Preservation Technology

Advances in centrifugal cold-press extraction technology are enabling olive oil producers to achieve superior polyphenol preservation, lower peroxide values, and enhanced flavor profile consistency compared to traditional decanting methods. Controlled-atmosphere storage using inert gas blanketing of storage tanks significantly extends oxidation stability, preserving extra virgin quality standards over longer distribution cycles.

Authentication and Anti-Adulteration Technology

In September 2024, ACS journals highlighted DNA sensor technology capable of detecting olive oil species and geographic origin adulteration with high precision. Blockchain-enabled provenance tracking systems are being deployed by leading Mediterranean producers and importers to provide immutable supply chain records from grove to bottle, accessible to US consumers via QR codes on packaging.

Sustainable Packaging and Eco-Friendly Production

Consumer preference for sustainable packaging is driving the adoption of dark glass bottles and tins that preserve olive oil quality by blocking UV light degradation, while simultaneously satisfying eco-conscious consumer preferences. Post-consumer recycled (PCR) content labels, biodegradable secondary packaging, and reduced-weight glass formulations are being adopted by both domestic California producers and leading Mediterranean exporters to reduce carbon footprints across the US olive oil supply chain.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Type | Extra Virgin Olive Oil | 48.7% |

2025 |

| Distribution Channel | 🔒 | 🔒 |

2025 |

| Application | Food and Beverage | 76.5% |

2025 |

| Region | West | 34.2% |

2025 |

By Type

To access detailed market analysis, Request Sample

Extra virgin olive oil represents the largest segment, accounting for 48.7% of the United States olive oil market in 2025. Its dominance reflects the premium-quality positioning of the segment, driven by superior nutritional composition, richer polyphenol content, and authentic flavor characteristics preferred by health-conscious American consumers and premium foodservice operators.

Virgin olive oil holds an 18.9% share and is valued for its purity and cold-press processing without chemical refinement, making it a popular choice for moderate-temperature cooking and finishing dishes. Refined olive oil accounts for 14.6%, primarily serving the food manufacturing and commercial foodservice sector, where a neutral flavor profile and higher smoke point are operationally preferred.

By Application

The food and beverage segment accounts for the dominant share at 76.5% of the United States olive oil market in 2025. Its dominance encompasses household retail cooking oil, food service and restaurant use, food manufacturing for dressings and marinades, and snack food production, all underpinned by the growing adoption of olive oil as a health-promoting kitchen staple.

Cosmetics account for 11.8% of market demand, reflecting olive oil's growing adoption in premium skincare, hair care, and beauty formulations where its emollient, antioxidant, and moisturizing properties command clean-beauty brand positioning. The pharmaceutical application segment holds a 7.9% share, growing as olive oil is increasingly incorporated into supplement formulations, topical therapeutic products, and pharmaceutical-grade excipients.

Regional Market Insights

The West region's market leadership (34.2%, 2025) reflects a convergence of California's domestic olive oil production growth, a high concentration of health-conscious consumer demographics across California, Oregon, and Washington, and a thriving foodservice ecosystem with extensive Mediterranean cuisine representation.

|

Region |

Share (2025) |

Key Growth Drivers |

Key Characteristics |

|

West |

34.2% |

California domestic production; health-conscious demographics; premium foodservice |

Highest per-capita olive oil consumption; strong organic and specialty retail |

|

Northeast |

25.6% |

Urban gourmet food culture; specialty retail density; high-income demographics |

Strong premium and EVOO segment; dense specialty store network; Mediterranean restaurant clusters |

|

South |

22.4% |

Growing health awareness; expanding Mediterranean cuisine footprint; foodservice growth |

Rising retail adoption, strong import distribution network through Gulf ports, and emerging premium demand |

|

Midwest |

17.8% |

Mainstream retail channel penetration, value-premium olive oil adoption, and growing health trends |

Fastest-growing region by CAGR; supermarket-led distribution; increasing private-label adoption |

The Northeast accounts for 25.6% of the US olive oil market, anchored by high-income urban consumers in New York, Boston, and Philadelphia who demonstrate strong preferences for premium, imported, and certified EVOO varieties. The South at 22.4% is experiencing the strongest absolute consumption growth, driven by population expansion in Texas and Florida, rising health awareness, and an expanding Mediterranean and Italian restaurant sector.

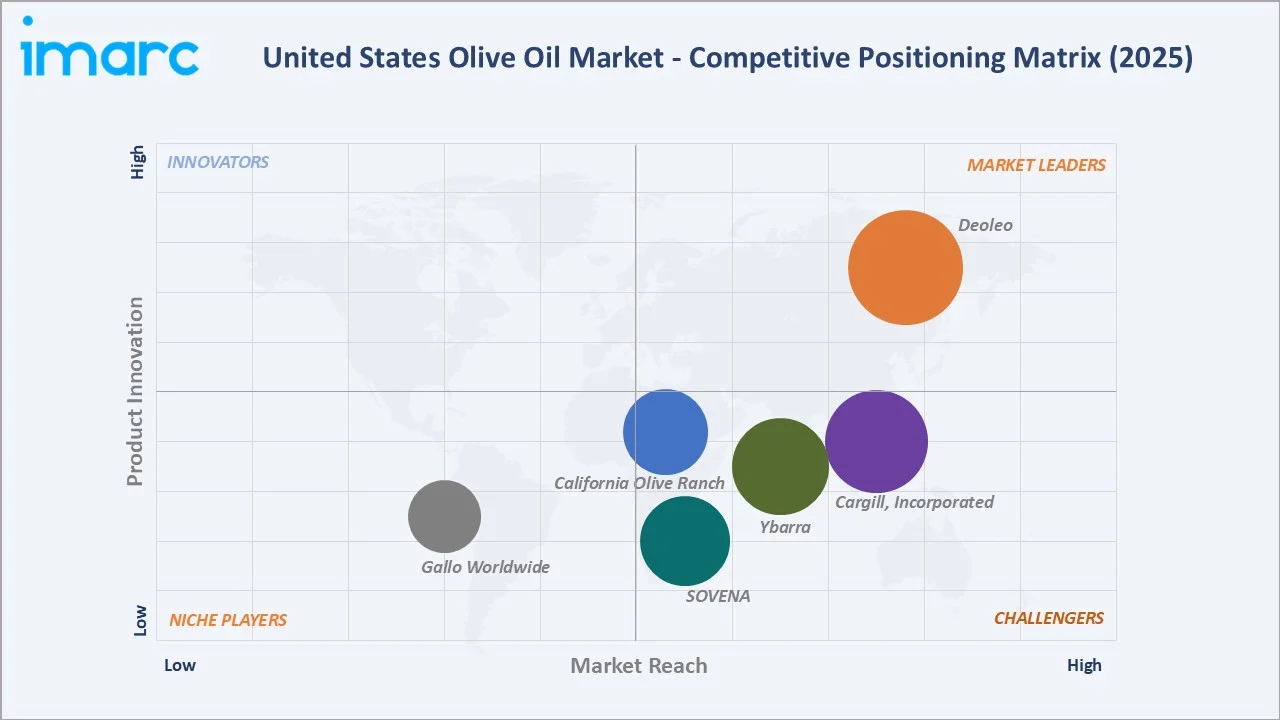

Competitive Landscape

The United States olive oil market exhibits a moderately fragmented structure, with the top five players, Deoleo, Gallo Worldwide, Cargill, Incorporated, Ybarra, SOVENA, and California Olive Ranch, Inc., collectively holding approximately 40–50% of total market revenue in 2025.

|

Company Name |

Key Brands |

Market Position |

Core Strength |

|

Deoleo |

Bertolli, Carbonell, Carapelli |

Market Leader |

Global olive oil brand portfolio; Mediterranean sourcing network |

|

Gallo Worldwide |

Victor Guedes |

Niche Player |

Premium EVOO positioning |

|

Cargill, Incorporated |

Refined and bulk olive oil products |

Strong Challenger |

Agricultural commodity scale; broad distribution network |

|

Ybarra |

Ybarra |

Strong Challenger |

Spanish heritage brand; premium quality positioning |

|

SOVENA |

Olivari |

Challenger |

Vertically integrated Mediterranean production; cost efficiency |

|

California Olive Ranch, Inc. |

California Olive Ranch, Destination Series |

Challenger |

Domestic California production; freshness and traceability positioning |

A diverse mix of Mediterranean export brands, California domestic producers, specialty importers, and private-label retailers accounts for the remaining market share, ensuring a competitive landscape that rewards both scale and quality differentiation.

Key Company Profiles

Deoleo

Deoleo, headquartered in Rivas-Vaciamadrid (Madrid), is the world's largest olive oil company by volume, with its Bertolli, Carbonell, and Carapelli brands holding significant shelf presence across US retail channels. The company operates extensive olive oil processing and bottling facilities in Spain and Italy, supplying the US market through its established import and distribution network.

- Product Portfolio: Bertolli extra virgin, pure, and light olive oil lines; Carbonell premium EVOO; Carapelli artisan and organic EVOO varieties.

- Recent Developments: In the February 2025 report, Deoleo said it achieved double‑digit sales growth to EUR 996 million and EUR 33 million in EBITDA in 2024, noting that the company maintained a steady 13.6 % market share in the United States.

- Strategic Focus: Mass-market and premium retail olive oil positioning; Mediterranean supply chain integration; US retail market share consolidation.

Gallo Worldwide

Gallo Worldwide, headquartered in Portugal, is a leading premium olive oil brand in Europe, available on Amazon and specialty importers in the US market, particularly in the extra virgin and organic segments. Gallo is a joint venture between Unilever and Sociedade Francisco Manuel dos Santos (Jerónimo Martins group).

- Product Portfolio: Gallo Clássico, Gallo Bio, Gallo Reserva, Gallo Grande Escolha, Gallo Ancestral.

- Strategic Focus: Premium and organic EVOO positioning; US retail and gourmet foodservice penetration; sustainability and provenance marketing.

Cargill, Incorporated

Cargill, Incorporated, headquartered in Wayzata, is a global agribusiness and food ingredient leader with extensive operations in edible oils, including olive oil. The company leverages its global agricultural commodity sourcing infrastructure and extensive US distribution network to supply refined and bulk olive oil products to food manufacturers, foodservice operators, and industrial customers.

- Product Portfolio: Refined olive oil, bulk olive oil for food manufacturing; blended edible oil products for commercial foodservice.

- Strategic Focus: Bulk and institutional olive oil supply; food manufacturing ingredient sourcing; sustainable agricultural supply chain management.

Market Concentration Analysis

The United States olive oil market exhibits moderate concentration at the distribution and brand level, with the top five players holding approximately 40–50% of total retail market revenue in 2025. However, a diverse ecosystem of specialty importers, regional distributors, California domestic producers, and private-label retailers ensures substantial competitive dynamism below the top tier, particularly in the growing premium and organic sub-segments.

Consolidation activity is accelerating in the import distribution segment, driven by the scale advantages required to manage complex Mediterranean supply chains, US regulatory compliance, and multi-channel distribution infrastructure. Private equity interest is growing in premium California olive oil producers and specialty import distributors that have demonstrated premiumization and DTC e-commerce capabilities.

Investment & Growth Opportunities

Fastest Growing Segments

Extra virgin olive oil (advancing at 8.8% CAGR), organic and PDO-certified premium variants (growing 22% year-over-year), and pharmaceutical applications (7.4% CAGR) represent the three highest-growth investment vectors through 2034. Together, these niches address a total addressable premium market of approximately USD 2.5–3.0 Billion by 2030, underpinned by structural consumer shifts toward health, authenticity, and natural product ingredients across food, health, and beauty categories.

Emerging Market Expansion

The South and Midwest regions represent the most significant incremental growth opportunities through 2034, driven by population expansion, rising health consciousness in previously mainstream-oil-dominated markets, and improving supermarket distribution infrastructure for premium olive oil products. California domestic production also represents a compelling investment opportunity, with growing consumer preference for locally sourced, traceable premium food products creating a structural tailwind for domestic EVOO producers seeking to reduce import dependency.

Venture and Institutional Investment Trends

- Key investment themes include DTC premium EVOO platforms, high-polyphenol functional olive oil brands targeting the health supplement channel, organic California grove development, and authentication technology companies addressing adulteration concerns in the premium segment.

- Family offices and PE firms are increasingly targeting vertically integrated California olive oil producers and premium Mediterranean import brands with established US retail presence, strong e-commerce capabilities, and certified organic or PDO product portfolios.

Future Market Outlook (2026-2034)

The United States olive oil market is positioned for sustained, above-average growth through 2034. From a base of USD 3.48 Billion in 2025, the market is projected to reach USD 6.76 Billion by 2034, representing total incremental value creation of USD 3.28 Billion over the forecast decade at a CAGR of 7.42%.

Supply-side developments, particularly improving Mediterranean harvest conditions following the severe drought-induced shortages of 2021–2024, and scaling California domestic production, are expected to improve price stability and support broader consumer adoption beyond the premium segment. Regulatory developments, including stricter USDA and IOC grade standards enforcement and expanded authentication technology requirements, will further reinforce consumer trust and segment integrity.

Long-term, the market's trajectory is tied to three structural macro-themes: the health and wellness revolution (which positions olive oil's documented cardiovascular and anti-inflammatory benefits at the centre of American dietary evolution), the premiumization of everyday food products (driving sustained trading-up from commodity cooking oils), and the diversification of olive oil into high-growth adjacent categories including cosmetics, pharmaceuticals, and nutraceuticals.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 100 industry participants in 2025–2026, including olive oil importers and distributors, foodservice procurement managers, retail category buyers, premium brand executives, California olive growers, and health and nutrition professionals across the United States.

Secondary Research

Secondary research encompassed a systematic review of USDA olive oil consumption data, IOC trade statistics, company annual reports, regulatory filings, FDA and USDA quality standard documentation, industry databases (SPINS, IRI/Circana), trade publications (Olive Oil Times, Gourmet Retailer), and publicly available financial data. Over 200 secondary sources were reviewed and triangulated to validate market estimates and trend insights.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating US olive oil import volume data, domestic production trends, per-capita consumption metrics, health and wellness spending indices, and historical market evolution across all four US regions. A base-case CAGR of 7.42% reflects consensus analyst estimates validated against reported brand revenue growth rates for 2023–2025.

United States Olive Oil Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Virgin Olive Oil, Refined Olive Oil, Extra Virgin Olive Oil, Olive Pomace Oil, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Others |

| Applications Covered | Food and Beverage, Pharmaceuticals, Cosmetics, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Deoleo, Gallo Worldwide, Cargill, Incorporated, Ybarra, SOVENA, California Olive Ranch, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States olive oil market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States olive oil market.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States olive oil industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Olive Oil Market Report

The United States olive oil market reached USD 3.48 Billion in 2025. It is projected to reach USD 6.76 Billion by 2034.

The United States olive oil market is expected to grow at a CAGR of 7.42% during the forecast period from 2026 to 2034, supported by consistent demand driven by health consciousness, Mediterranean diet adoption, and premium product category expansion.

The West region leads the market with a 34.2% revenue share in 2025, driven by California's growing domestic olive oil production, high health-conscious consumer demographics, and a thriving premium foodservice sector across California, Oregon, and Washington.

Extra virgin olive oil dominates with a 48.7% share in 2025, valued at approximately USD 1.69 Billion. Its dominance is driven by superior nutritional composition, high polyphenol content, and authentic flavour characteristics preferred by health-conscious American consumers.

The food and beverage segment holds the largest application share at 76.5% in 2025 (approx. USD 2.66 Billion), encompassing household retail cooking, restaurant and foodservice use, food manufacturing for dressings and marinades, and packaged food production across the United States.

Key players include Deoleo, Gallo Worldwide, Cargill, Incorporated, Ybarra, SOVENA, and California Olive Ranch, Inc., among other regional and specialty players.

The Mediterranean diet's growing adoption among American consumers, endorsed by leading health organisations and consistently ranked among the world's healthiest dietary patterns, is positioning olive oil as a daily dietary essential rather than a specialty product, driving sustained volume growth across all price tiers and retail channels.

Key challenges include price volatility from Mediterranean harvest disruptions and drought conditions, near-total US import dependency exposing the market to trade policy and supply chain risks, and ongoing consumer trust concerns related to olive oil adulteration in the premium segment.

Significant growth opportunities exist in the premium extra virgin and organic segments, growing at 8.8% CAGR and 22% year-over-year, respectively, pharmaceutical and cosmetic application diversification, California domestic EVOO production scale-up, and DTC e-commerce platforms targeting health-conscious premium consumers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)