United States Online Food Delivery Market Size, Share, Trends and Forecast by Platform Type, Business Model, Payment Method, and Region, 2026-2034

United States Online Food Delivery Market Size, Share, Trends & Forecast (2026-2034)

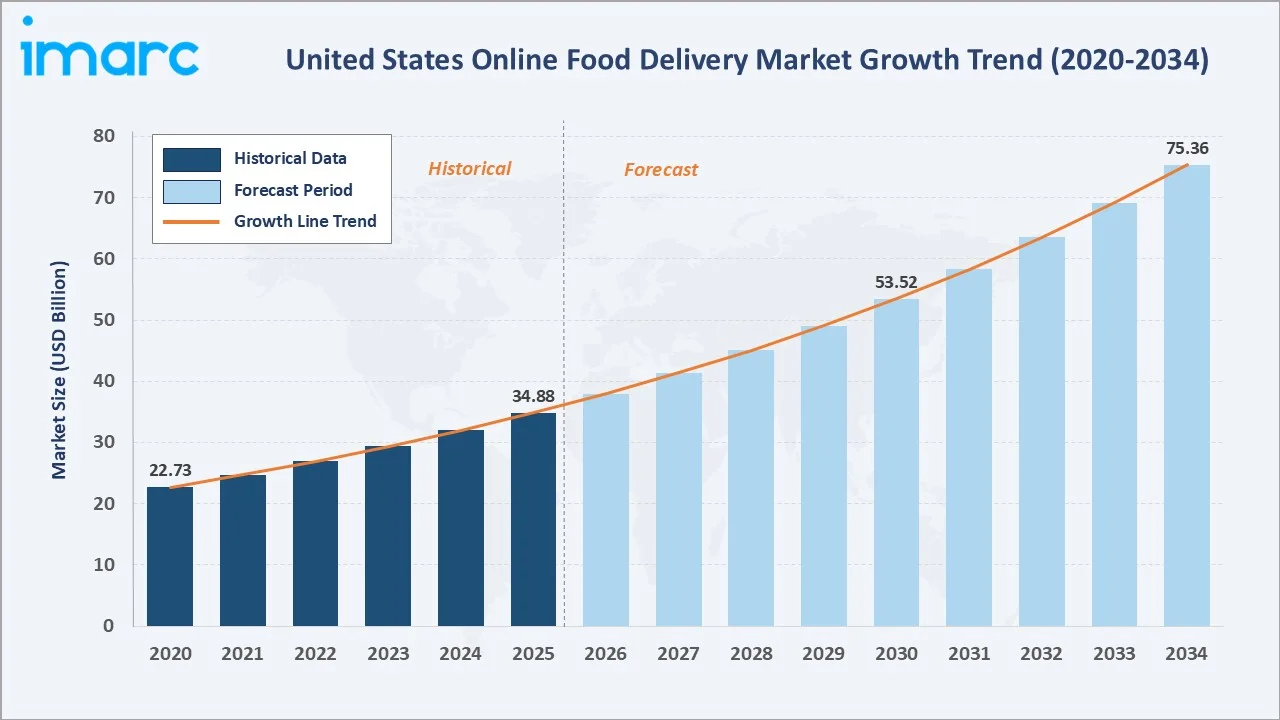

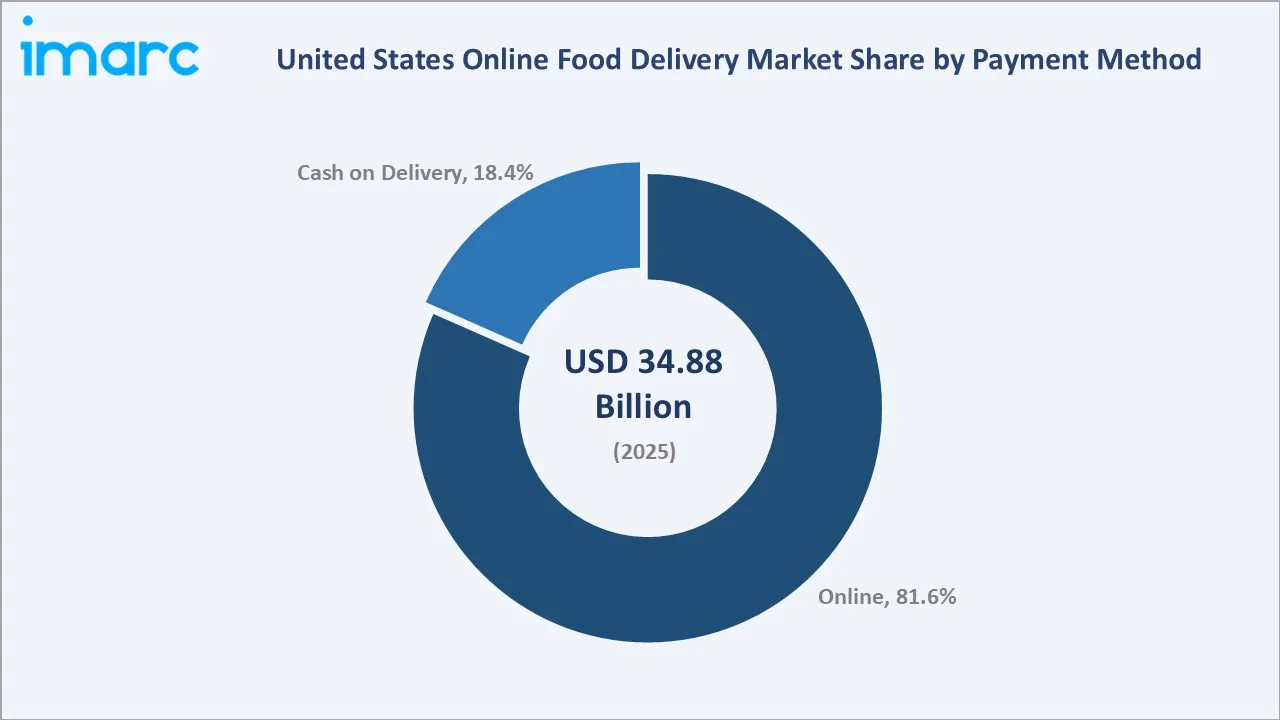

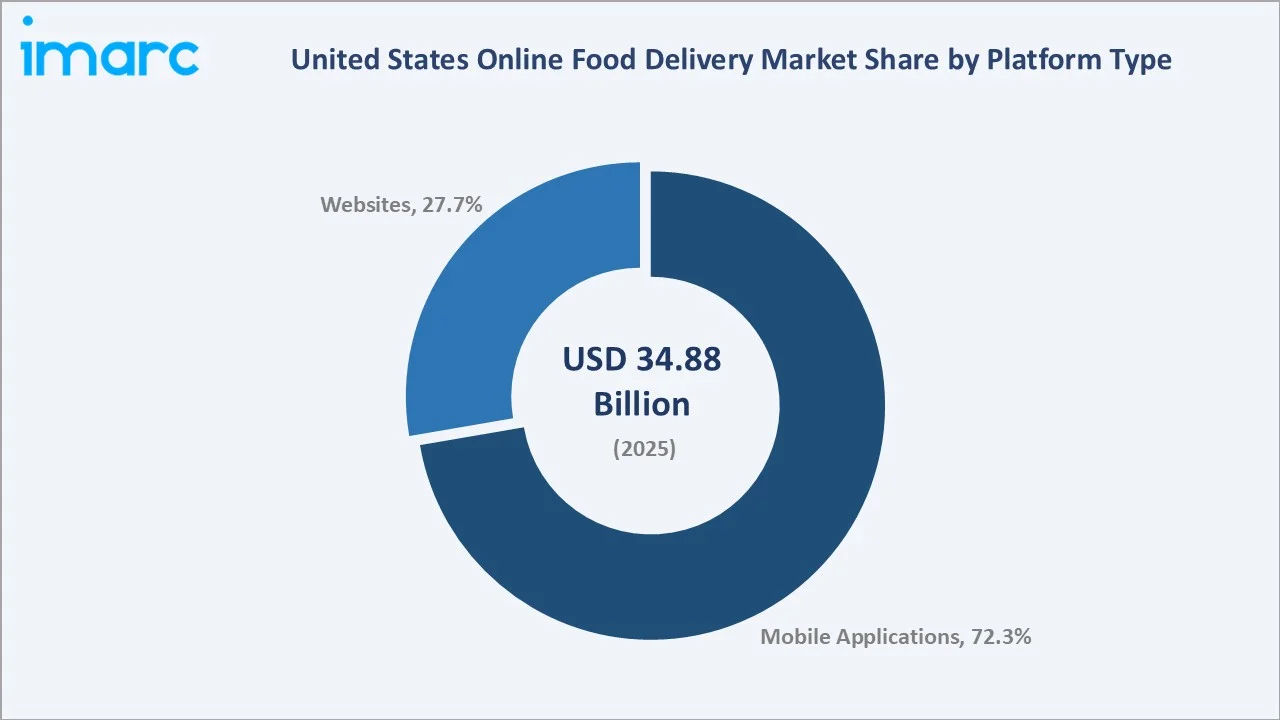

The United States online food delivery market size reached USD 34.88 Billion in 2025 and is projected to reach USD 75.36 Billion by 2034, exhibiting a CAGR of 8.94% during 2026-2034. Rising smartphone penetration, evolving consumer lifestyles, and expanding digital payment infrastructure are primary growth drivers.

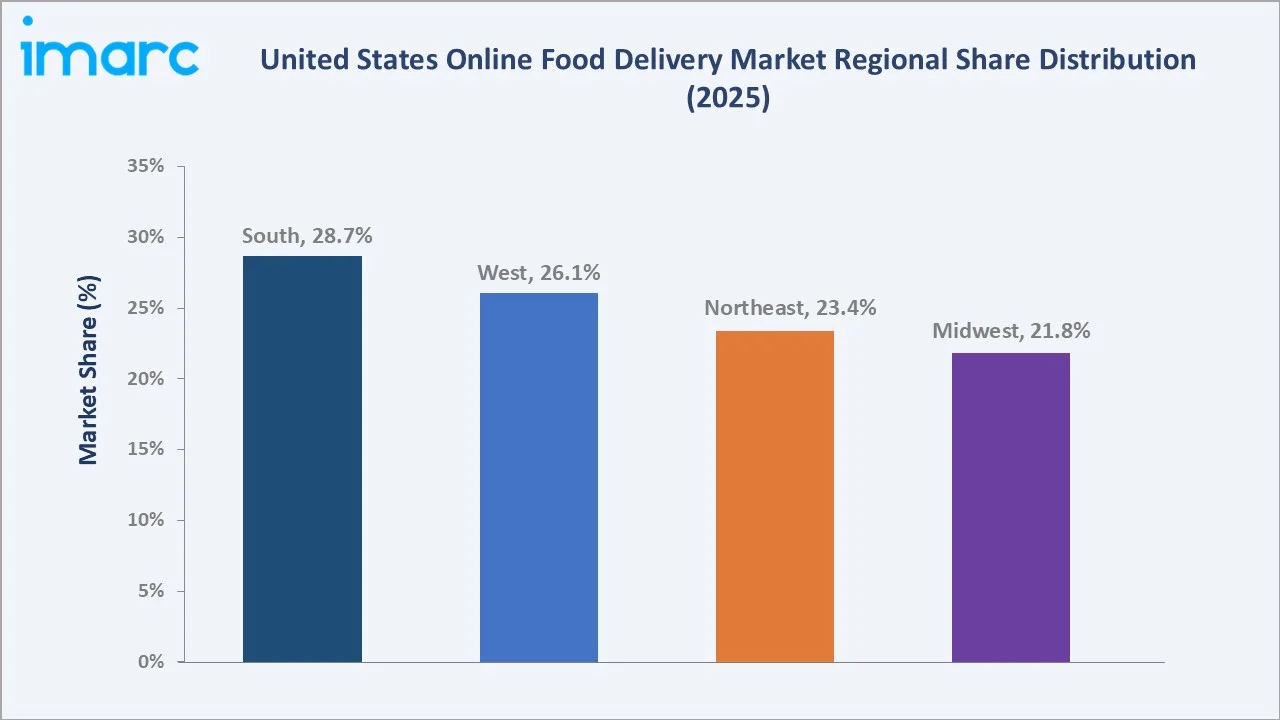

Online payment leads at 81.6% in 2025, while mobile applications dominate platform type at 72.3%. The South region holds the largest share at 28.7%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 34.88 Billion |

|

Forecast Market Size (2034) |

USD 75.36 Billion |

|

CAGR (2026-2034) |

8.94% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

| Leading Payment Method | Online (81.6% share, 2025) |

| Second Payment Method |

Cash on Delivery (18.4% share, 2025) |

| Leading Platform Type |

Mobile Applications (72.3%, 2025) |

|

Largest Region |

South (28.7% share, 2025) |

The market growth trajectory from 2020 through 2034, with historical expansion to USD 34.88 Billion in 2025, reflects consistent digitization-driven demand, while the forecast to USD 75.36 Billion captures accelerating mobile adoption, subscription model growth, and post-pandemic behavioral permanence.

To get more information on this market, Request Sample

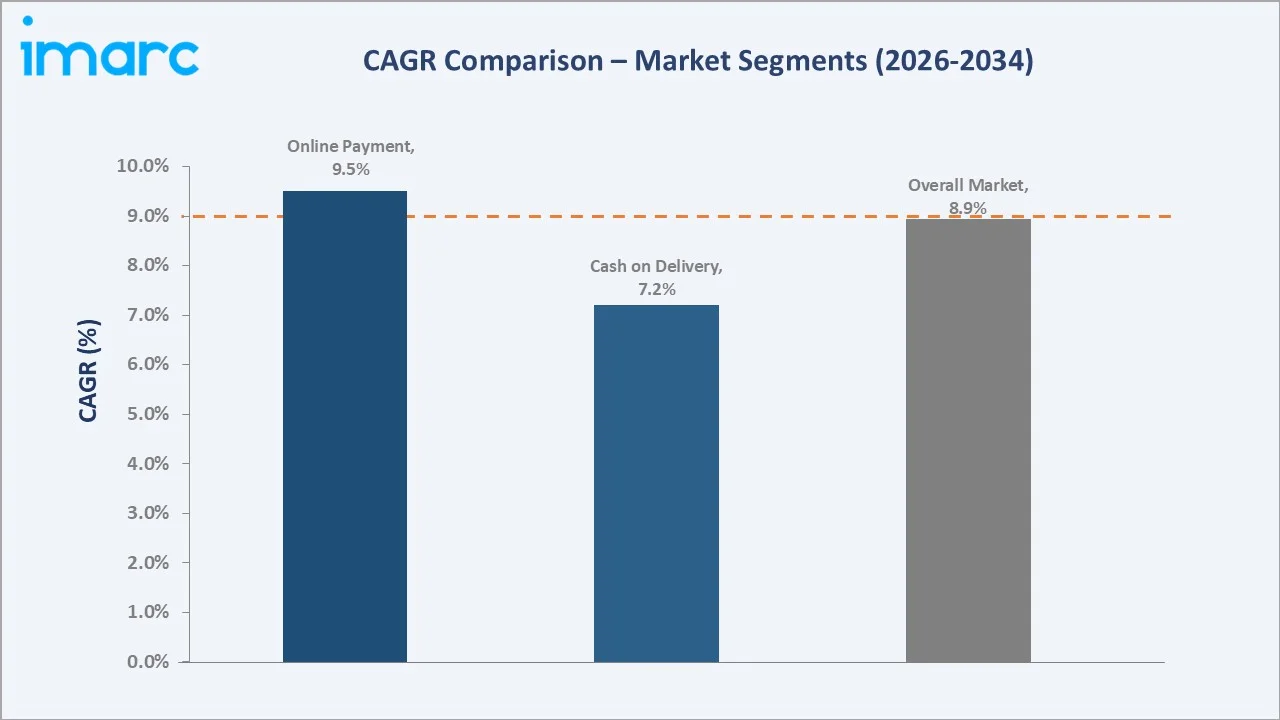

The CAGR trajectories across key platform, payment, and regional sub-segments, with mobile applications at ~10.2% CAGR and the South region at ~9.8% CAGR, are the fastest-growing categories within the United States online food delivery industry analysis through 2034.

Executive Summary

The US online food delivery market is on a sustained growth trajectory from USD 34.88 Billion in 2025 to USD 75.36 Billion by 2034. Online food delivery benefits from deeply embedded consumer convenience preferences formed during and after the COVID-19 pandemic, driving structural permanence.

Online payment dominates at 81.6% in 2025, driven by seamless in-app checkout, digital wallets, and one-tap reordering features. Cash on delivery retains an 18.4% share, primarily in lower-income demographics and suburban markets where digital payment adoption lags.

Mobile applications lead platform type at 72.3% in 2025, reflecting app-first consumer behavior, push notification-driven re-engagement, and loyalty program integrations unavailable on web platforms. Website ordering accounts for the remaining 27.7%.

The South (28.7%) leads regional demand, followed by the West (26.1%), Northeast (23.4%), and Midwest (21.8%). Sunbelt population growth, dense urban restaurant supply in Texas and Florida, and high platform penetration underpin Southern dominance.

Key Market Insights

|

Insight |

Data |

| Leading Payment Method |

Online – 81.6% share (2025) |

| Second Payment Method |

Cash on Delivery – 18.4% share (2025) |

| Leading Platform Type |

Mobile Applications – 72.3% share (2025) |

| Second Platform Type |

Websites – 27.7% share (2025) |

| Leading Region |

South – 28.7% (2025) |

| Second Largest Region |

West – 26.1% (2025) |

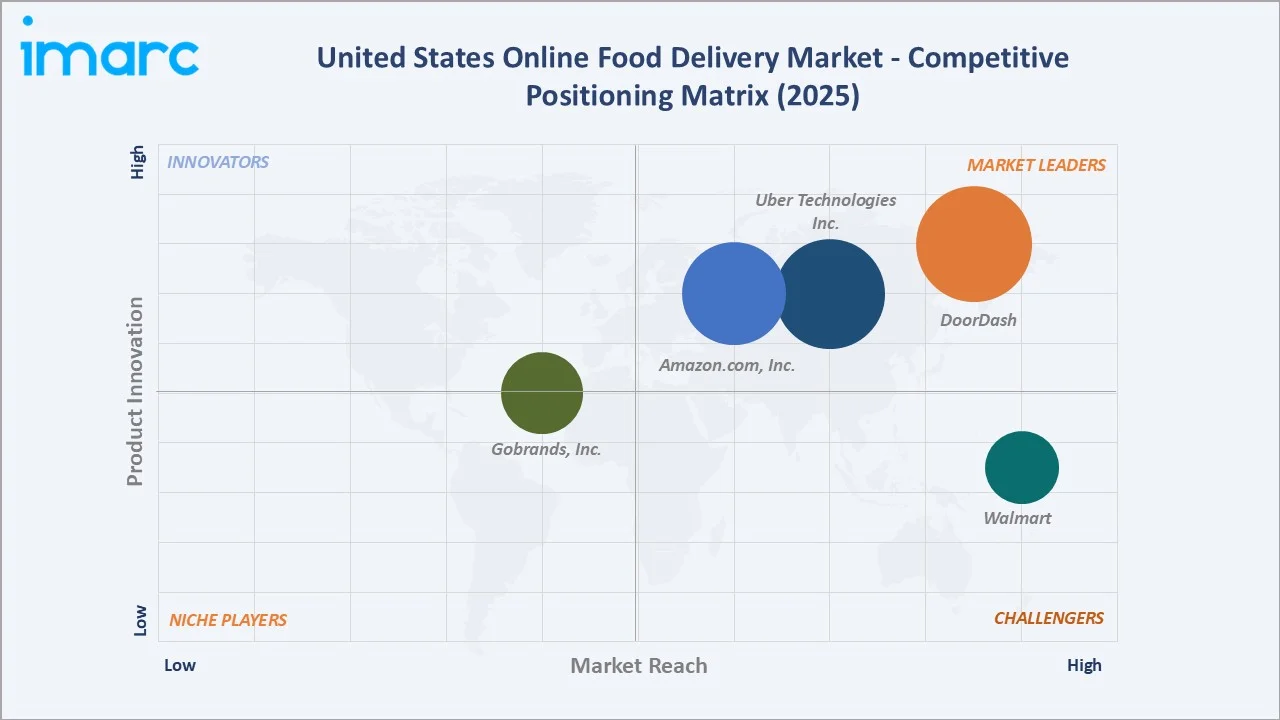

| Top Companies |

DoorDash, Uber Technologies Inc., Amazon.com, Inc., Walmart, Gobrands, Inc. |

Key Analytical Observations Supporting the Above Data:

- Online payment at 81.6% in 2025 dominates because integrated digital wallets, one-click reordering, and stored card profiles have eliminated checkout friction, particularly among urban millennials and Gen Z consumers aged 18-34.

- Mobile applications at 72.3% in 2025 lead because app-native features including real-time delivery tracking, geolocation-based restaurant discovery, push notification promotions, and gamified loyalty rewards create engagement loops that web browsers cannot structurally replicate.

- The South region's 28.7% dominance reflects demographic tailwinds. Texas, Florida, and Georgia represent the three fastest-growing state economies by population, with dense restaurant ecosystems and strong platform penetration across major metro areas.

- Cash on delivery at 18.4% remains meaningful in lower-income zip codes and among older demographics aged 55+ years. Platforms retaining COD capture incremental orders from households without primary debit/credit cards or those concerned about digital transaction security.

United States Online Food Delivery Market Overview

Online food delivery encompasses technology-enabled platforms connecting consumers to restaurants and grocery providers for home or office delivery. The ecosystem integrates platform operators, restaurant partners, third-party logistics networks, digital payment processors, cloud kitchen operators, and quick-commerce grocery services into a seamless consumer experience.

The US market operates through two primary business models: marketplace delivery, where platforms manage logistics using gig-economy couriers, and restaurant-to-consumer delivery, where established chains manage proprietary last-mile delivery operations independently of third-party platforms.

Market Dynamics

.webp)

To evaluate market opportunities, Request Sample

Market Drivers

- Smartphone Penetration and Mobile Commerce Growth: US smartphone penetration exceeded 80% of adults in 2025, with mobile commerce accounting for 62% of all e-commerce transactions, creating a structurally favorable environment for app-first food delivery platforms.

- Shifting Consumer Lifestyle and Time Scarcity: Dual-income households represent 61% of US families. Time-constrained consumers increasingly substitute home cooking with restaurant meal delivery, driving order frequency from 2.1x/month in 2020 to 3.8x/month in 2025 among active users.

- Expanding Restaurant Partner Network: Online food delivery platforms are continuously broadening their merchant partnerships, giving consumers access to a wide variety of local eateries, regional favorites, and national chains within a single app. This expanded selection enhances platform convenience and value, encouraging higher user engagement and more frequent ordering.

Market Restraints

- Delivery Fee Sensitivity and Platform Profitability Pressure: Consumer resistance to delivery fees averaging USD 5-8 per order, plus service fees of 15-20%, creates churn risk. Platforms subsidizing delivery to maintain order volume face sustained margin compression in a competitive landscape.

- Gig Economy Labor Regulation: California's AB5 and similar legislation in multiple states threaten to reclassify gig delivery workers as employees, potentially increasing platform labor costs by 25-40% and disrupting the asset-light delivery model underlying current valuations.

Market Opportunities

- Grocery and Quick Commerce Expansion: Food delivery platforms are increasingly moving beyond restaurant meals into grocery and rapid delivery services, targeting high-frequency use cases and larger basket sizes. This shift is intensifying competition as players invest in logistics, dark stores, and fulfillment capabilities to capture a greater share of everyday consumer spending.

- AI-Driven Personalization and Predictive Ordering: Platforms are leveraging advanced analytics and machine learning to better understand user behavior and deliver personalized recommendations based on factors such as past orders, location, and timing. These capabilities help improve user experience, drive higher engagement, and increase order value through more relevant and timely suggestions.

Market Challenges

- Autonomous Delivery Regulatory Uncertainty: Drone and robot delivery deployment faces inconsistent municipal regulation, FAA airspace restrictions, and public liability frameworks that vary by city, slowing commercial rollout of cost-reducing autonomous last-mile delivery technologies.

- Food Safety and Quality Control at Scale: Maintaining meal quality and food safety compliance across millions of daily deliveries, with average delivery windows of 28-35 minutes, creates persistent consumer satisfaction challenges that drive negative reviews and platform switching behavior.

Emerging Market Trends

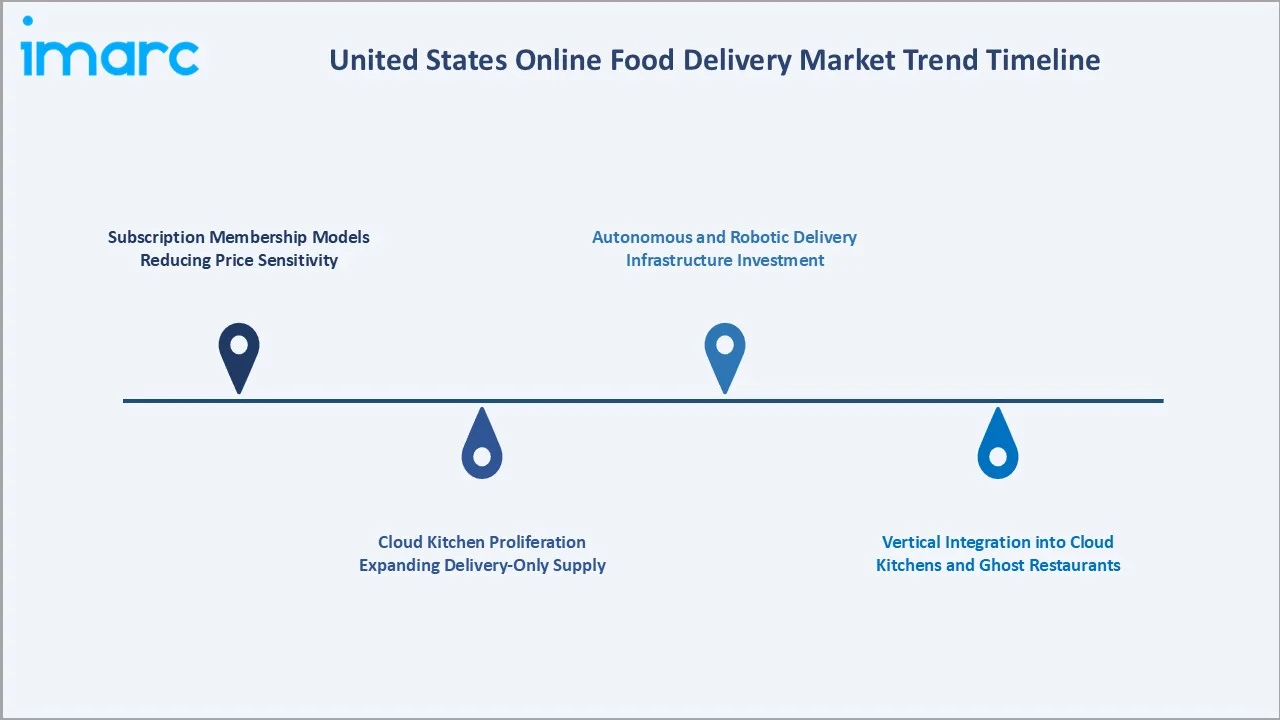

1. Subscription Membership Models Reducing Price Sensitivity

DashPass and Uber One memberships, priced at USD 9.99-USD 19.99/month, convert price-sensitive occasional users into high-frequency subscribers averaging 4-6x monthly orders.

2. Cloud Kitchen Proliferation Expanding Delivery-Only Supply

Cloud kitchens have grown from approximately 1,500 US locations in 2020 to over 10,000 in 2025. Their delivery-optimized menus, lower overhead, and faster preparation times improve delivery profitability for both operators and platform partners across all major metro markets.

3. Autonomous and Robotic Delivery Infrastructure Investment

Major platforms and logistics startups are piloting autonomous sidewalk robots and drone delivery in suburban markets. Commercial-scale deployment by 2027-2028 could reduce last-mile delivery costs by 35-50% in suitable markets, significantly improving platform unit economics.

4. Vertical Integration into Cloud Kitchens and Ghost Restaurants

Platform operators are vertically integrating into food production, capturing higher gross margins from delivery-only brands while providing restaurant partners access to demand-tested menus without capital-intensive brick-and-mortar risk in high-rent urban markets.

Industry Value Chain Analysis

The online food delivery value chain spans five stages from food preparation through last-mile delivery. Platform technology and logistics coordination capture the highest value-add margins, while payment processing and restaurant partnerships generate significant network effects.

|

Stage |

Key Players / Examples |

| Restaurant / Food Providers |

Integrated food brands, independent restaurants, cloud kitchens, ghost restaurant operators |

| Platform Technology |

Online marketplace platforms managing order routing, demand forecasting, and pricing |

| Payment Processing |

Digital payment networks, mobile wallet providers, card processors, and COD management |

| Delivery Logistics |

Gig-economy courier networks, micro-mobility operators, and emerging autonomous delivery providers |

| End Consumer |

Residential households, office workers, college students, and enterprise meal program users |

Technology Landscape in the Online Food Delivery Industry

AI-Powered Dispatch and Route Optimization

Food delivery platforms are increasingly leveraging machine learning algorithms to optimize courier assignment and order batching in real time, improving coordination between supply and demand. These systems enhance delivery efficiency by factoring in variables such as location, traffic conditions, and order density, enabling faster fulfillment and better resource utilization. As a result, platforms can reduce delivery times, improve customer satisfaction, and achieve greater operational scalability compared to traditional rule-based systems.

Real-Time Order Tracking and Consumer Communication

GPS-integrated real-time delivery tracking with live courier location maps, ETA countdowns, and automated push notifications has become table-stakes consumer expectation. Platforms investing in sub-minute location update frequencies achieve measurably higher post-delivery satisfaction scores.

Digital Payment Security and Fraud Prevention

Online food delivery platforms are strengthening transaction security through technologies such as tokenization, multi-factor authentication, and advanced fraud detection systems. Machine learning models are increasingly used to identify suspicious activity in real time, enhancing trust and reducing financial risk. The integration of biometric authentication with digital wallets further improves security and user convenience, helping lower fraud incidents and chargebacks compared to traditional verification methods.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Platform Type | Mobile Applications | 72.3% | 2025 |

| Business Model | Order Focused Food Delivery System | 55.8% | 2025 |

| Payment Method | Online | 81.6% | 2025 |

| Region | South | 28.7% | 2025 |

By Payment Method

Online payment commands an 81.6% majority share in 2025 owing to seamless app-integrated digital wallets, saved card profiles enabling one-tap checkout, and platform-native payment incentives such as cashback rewards and instant discount coupons, reflecting a structural shift in US consumer payment behavior accelerated by the pandemic.

To access detailed market analysis, Request Sample

Cash on delivery at 18.4% in 2025 serves unbanked or underbanked households, older demographics preferring physical currency, and consumers in lower-density markets with limited digital payment infrastructure. Platforms maintaining COD capture incremental orders unavailable to digital-only competitors.

By Platform Type

Mobile applications dominate platform type at 72.3% in 2025, representing the primary ordering interface for the majority of food delivery consumers. App-native features including GPS restaurant discovery, real-time delivery tracking, push notification promotions, and integrated loyalty reward programs drive structurally higher order frequency versus web users.

Website ordering at 27.7% in 2025 serves desktop users, enterprise lunch ordering accounts, and restaurant direct ordering platforms. Web share is declining at approximately 1.5 percentage points annually as mobile-first consumer behavior intensifies across all demographic cohorts.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

28.7% |

Population growth; Texas/Florida restaurant density; strong platform penetration |

|

West |

26.1% |

Tech-savvy consumers; CA/WA urban density; high average order values |

|

Northeast |

23.4% |

NYC/Boston urban markets; commuter demand; premium restaurant base |

|

Midwest |

21.8% |

Growing suburban adoption; college town demand; competitive pricing |

The South's 28.7% dominance in 2025 is driven by the fastest-growing US population centers. Texas added 562,000 residents in 2023-2024, the highest state net migration figure nationally, while Florida's Miami-Dade and Broward counties represent two of the three highest per-capita food delivery spend metros in the United States.

The West, with 26.1% in 2025, benefits from the highest concentration of technology-forward consumers in California, Washington, and Oregon. Silicon Valley and Seattle metro areas exhibit the highest household income levels correlated with premium restaurant delivery spend.

Competitive Landscape

The US online food delivery market is highly concentrated, with DoorDash commanding approximately 67% platform market share, Uber Eats at 23%, and Grubhub at approximately 6%. This three-player oligopoly contrasts with moderate fragmentation in grocery and quick-commerce delivery segments.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

| DoorDash | DoorDash app, DashMart, DashPass |

Leader |

US market leader; autonomous delivery; subscription growth |

| Uber Technologies Inc. | Uber Eats, Uber One |

Leader |

Global platform; ride-hailing integration; enterprise accounts |

| Amazon.com, Inc. | Amazon Fresh, Whole Foods Delivery | Leader |

Prime ecosystem; logistics advantage; broad product range |

| Walmart | Walmart Delivery, Spark |

Challenger |

Nationwide footprint; grocery strength; everyday pricing |

| Gobrands, Inc. | Gopuff app | Emerging |

Micro-fulfillment; 15-min delivery; convenience focus |

Key players include DoorDash, Uber Technologies Inc., Amazon.com, Inc., Walmart, Gobrands, Inc., and others.

Key Company Profiles

DoorDash

DoorDash is the largest online food delivery platform in the United States, headquartered in San Francisco. DoorDash operates the most extensive merchant and courier network, across restaurants, grocery, convenience, and alcohol delivery verticals.

- Product Portfolio: DoorDash app, DashPass subscription, DashMart convenience delivery, DoorDash for Business enterprise platform

- Recent Developments: In April 2026, DoorDash expanded its partnership with Wing to introduce drone-based food delivery in the Atlanta metropolitan area, offering customers a faster and more efficient delivery option. The service enables eligible users to order from select local and national restaurants and receive their meals via drone within a short timeframe.

- Strategic Focus: DoorDash's strategy leverages its dominant merchant and consumer network to expand into adjacent quick-commerce categories while investing in autonomous delivery to reduce last-mile costs and defend market share against Uber Eats' global scale advantages.

Uber Technologies Inc.

Uber Eats operates as the food delivery division of Uber Technologies, integrating with the Uber ride-hailing app and Uber One membership to create a multi-service consumer platform. With approximately 23% US platform share in 2025, Uber Eats benefits from Uber's existing driver network reducing incremental courier acquisition costs significantly.

- Product Portfolio: Uber Eats app, Uber One membership (USD 9.99/month bundling food delivery and rides), Uber Eats for Business, robotic delivery partnerships

- Recent Developments: In April 2026, Uber Technologies, Inc. and Block, Inc. expanded their global partnership to enhance restaurant operations and improve payment flexibility across Uber’s ecosystem. The collaboration extends the integration of Square’s point-of-sale system with Uber Eats into multiple international markets, enabling restaurants to manage orders, menus, and inventory more efficiently through a unified platform.

- Strategic Focus: Uber Eats differentiates through multi-service bundling via Uber One, leveraging ride-hailing customer acquisition costs to reduce food delivery CAC, while pursuing international scale advantages unavailable to DoorDash's predominantly US-focused operation.

Walmart

Walmart Delivery operates as the grocery and general merchandise delivery division of Walmart Inc., integrating with the Walmart+ membership program and its nationwide store network to create a unified omnichannel retail platform.

- Product Portfolio: Walmart+ membership, Walmart Delivery Now, Spark Driver network, InHome Delivery

- Strategic Focus: Walmart differentiates through everyday low pricing enabled by its direct supplier relationships and private label scale, leveraging its existing store network as micro-fulfillment nodes to undercut third-party delivery platforms on both speed and cost, while using Walmart+ membership to build recurring revenue and customer loyalty across grocery, general merchandise, and media.

Market Concentration Analysis

The US online food delivery market is highly concentrated at the platform level, with DoorDash (~67%), Uber Eats (~23%), and Grubhub (~6%) collectively controlling approximately 96% of the meal delivery segment. Grocery delivery is more fragmented, with Instacart, Amazon, Walmart, and regional players competing across a more heterogeneous consumer base.

Consolidation continues to intensify. DoorDash's acquisition of Wolt and Grubhub's acquisition by Wonder Group in 2024 demonstrate ongoing M&A-driven restructuring. The three-player meal delivery oligopoly is structurally durable given the network effects required to maintain both merchant supply density and courier availability simultaneously in each metro market.

Investment & Growth Opportunities

Fastest-Growing Segments

Mobile applications at ~10.2% CAGR through 2034 represent the highest-growth platform segment, driven by super-app convergence and expanding mobile commerce share. Online payment at ~9.5% CAGR through 2034 reflects increasing digital wallet adoption and declining COD preference.

Emerging Markets

The South region at ~9.8% CAGR is the fastest-growing US regional market through 2034, driven by population migration from high-cost coastal metros and expanding restaurant supply in mid-tier Sunbelt cities. Austin, Nashville, and Charlotte represent particularly high-growth opportunity markets.

Venture & Investment Trends

Autonomous delivery startups attracted USD 2.8 Billion in venture investment in 2023-2024. Private equity interest in cloud kitchen roll-ups is increasing, with platforms pursuing owned food supply as a gross margin improvement strategy. Retail media advertising on food delivery platforms represents a high-margin revenue growth opportunity as CPG brands increase delivery app ad spend.

Future Market Outlook (2026-2034)

The US online food delivery market is forecast to expand from USD 34.88 Billion in 2025 to USD 75.36 Billion by 2034 at a CAGR of 8.94%, adding USD 40.48 Billion in incremental annual market value over the forecast period. This sustained growth reflects embedded consumer behavioral permanence and expanding addressable use cases beyond restaurant meals.

Three technological forces will most significantly shape the landscape through 2034: autonomous delivery reducing last-mile costs by 35-50%, AI personalization increasing average order values by 15-20%, and quick-commerce grocery delivery expanding total addressable market into a USD 15+ Billion daily essentials category.

The South's demographic tailwinds and mobile-first consumer base position it as the dominant growth region through 2034. Platform consolidation will continue, with leading platforms capturing disproportionate share through superior logistics networks and subscription ecosystem advantages.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews with US online food delivery industry stakeholders, including platform operations executives, restaurant partner managers, digital payment specialists, gig-economy workforce representatives, and consumer behavior researchers. Primary data validated market sizing, segment shares, and technology adoption timelines.

Secondary Research

Key secondary sources include US Census Bureau consumer expenditure surveys, Bureau of Labor Statistics employment data, Second Measure transaction panel data, Statista food delivery platform tracking, SEC filings of DoorDash and Uber Technologies, and trade publications including Restaurant Business Online and Nation's Restaurant News.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting models incorporating demographic growth rates, smartphone penetration curves, disposable income projections, and restaurant industry revenue data. Scenario analysis across base, optimistic, and conservative cases accounts for gig economy regulatory and autonomous delivery commercialization risk.

United States Online Food Delivery Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Platform Types Covered | Mobile Applications, Websites |

| Business Models Covered | Order Focused Food Delivery System, Logistics Based Food Delivery System, Full Service Food Delivery System |

| Payment Methods Covered | Online, Cash on Delivery |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | DoorDash, Uber Technologies Inc., Amazon.com, Inc., Walmart, Gobrands, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States online food delivery market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the United States online food delivery market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States online food delivery industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Online Food Delivery Market Report

The market size reached USD 34.88 Billion in 2025 and is projected to reach USD 75.36 Billion by 2034.

The market is expected to exhibit a CAGR of 8.94% during 2026-2034.

Online payment leads with an 81.6% share in 2025, driven by digital wallet adoption and app-integrated checkout.

Mobile applications dominate with a 72.3% share in 2025, reflecting app-first consumer behavior.

The South region leads with a 28.7% share in 2025, followed by the West (26.1%), Northeast (23.4%), and Midwest (21.8%).

Key players include DoorDash, Uber Technologies Inc., Amazon.com, Inc., Walmart, Gobrands, Inc., and others.

The United States online food delivery market faces intense competition and price sensitivity, which compress margins due to heavy discounting and high customer acquisition costs. Operational challenges such as logistics complexity, last-mile delivery inefficiencies, and reliance on gig workers further impact service consistency and profitability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)