United States Online Gambling Market Size, Share, Trends and Forecast by Game Type, Device, and Region, 2026-2034

United States Online Gambling Market Size, Share, Trends & Forecast (2026-2034)

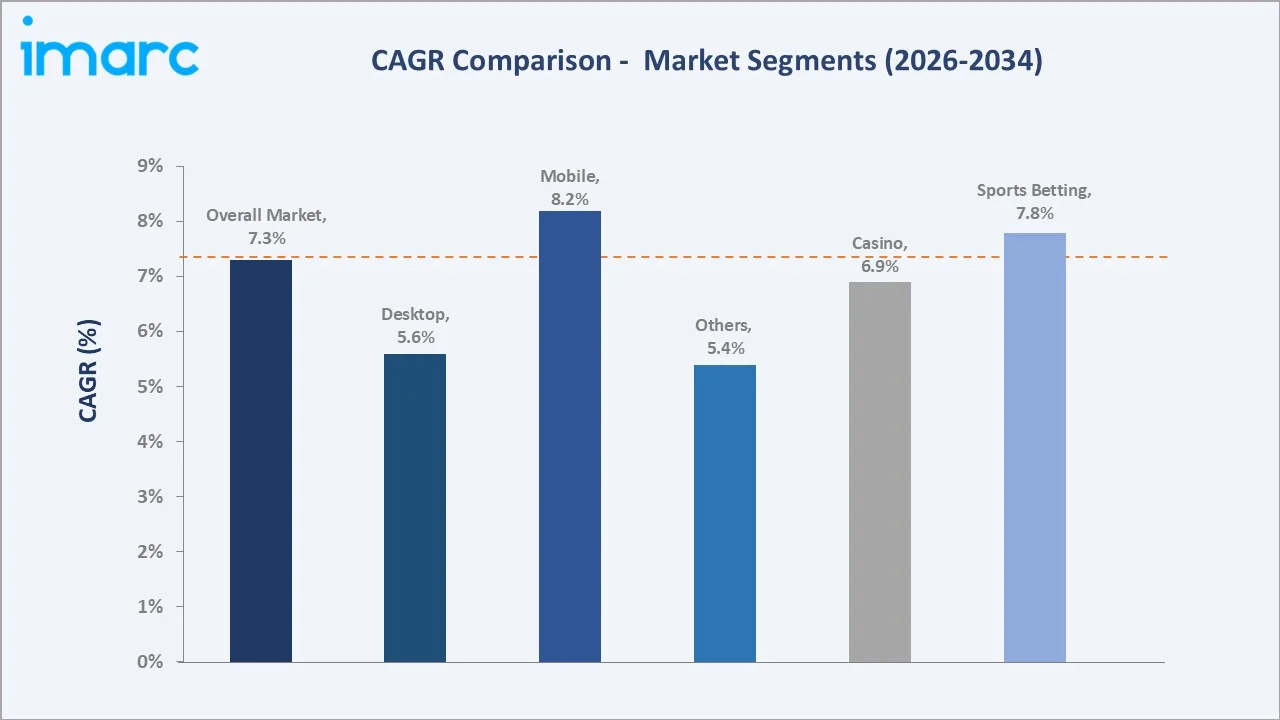

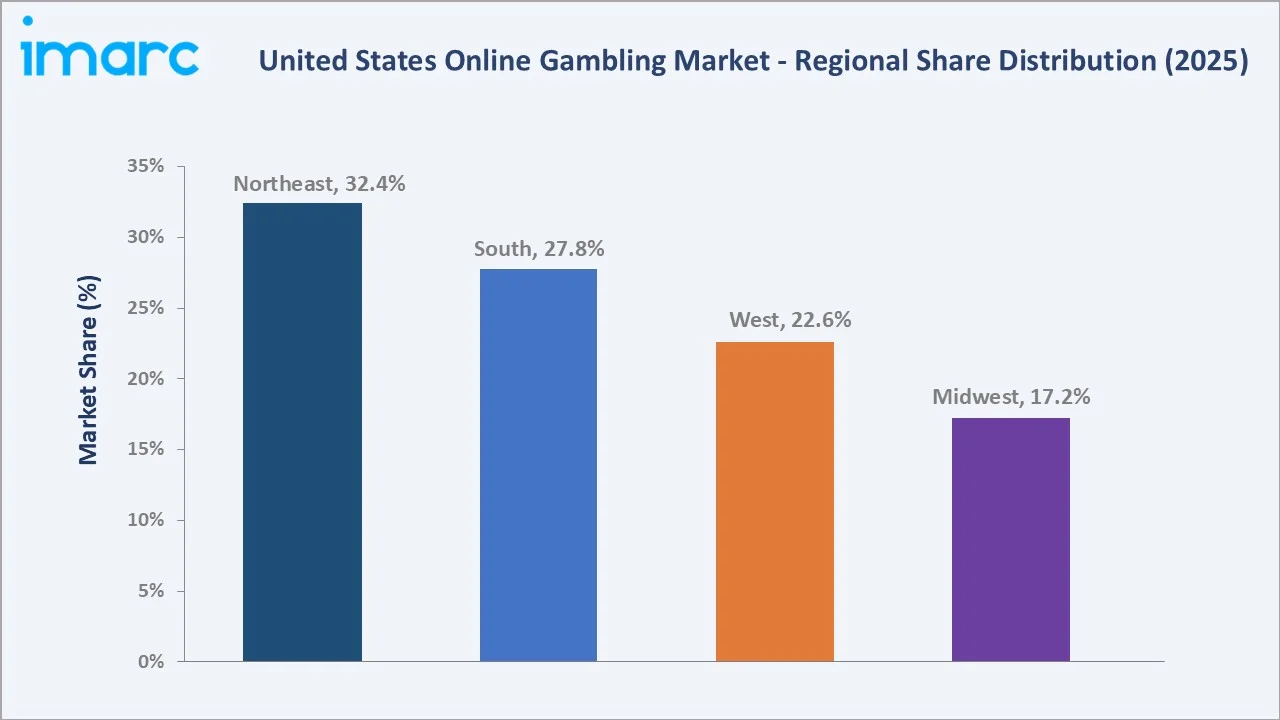

The United States online gambling market size increased from USD 11.80 Billion in 2025 to USD 12.70 Billion in 2026 and is projected to reach USD 22.8 Billion by 2034, growing at a CAGR of 7.33% during 2026-2034. The market is driven by increasing state-level legalization, rising smartphone and internet penetration, with nearly all Americans (98%) now owning some type of cell phone, with approximately 91% (9 in 10) using a smartphone, and growing consumer demand for convenient digital gaming platforms. Sports betting leads at 49.3% game type share, and mobile dominates device access at 68.7%. The Northeast region commands 32.4% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 11.80 Billion |

|

Market Size (2026) |

USD 12.70 Billion |

|

Forecast Market Size (2034) |

USD 22.8 Billion |

|

CAGR (2026-2034) |

7.33% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Game Type |

Sports Betting (49.3%, 2025) |

|

Dominant Device |

Mobile (68.7%, 2025) |

|

Leading Region |

Northeast (32.4%, 2025) |

The market increased from USD 8.3 Billion in 2020 to USD 11.80 Billion in 2025, and is estimated to reach USD 12.70 Billion in 2026. The market is further expected to grow to USD 16.9 Billion in 2030, and forecast to reach USD 22.8 Billion by 2034. Mobile sportsbook apps normalizing betting behavior, combined with iGaming expansion, drives the high 7.33% CAGR through 2034.

To get more information on this market, Request Sample

Mobile device grows fastest at ~8.2% CAGR (2026-2034), reinforced by US smartphone penetration and operators investing in mobile app development. Sports betting grows at ~7.80% CAGR.

Executive Summary

The US online gambling market expanded from USD 11.80 Billion in 2025, to an estimated USD 12.70 Billion in 2026. driven by the world's most dynamic regulated sports betting expansion. With US states having legalized some form of online sports betting, the US is now one of the world's largest regulated online gambling markets by gross gaming revenue. The market is projected to reach USD 22.8 Billion by 2034 at 7.33% CAGR, reflecting the compounding effects of new state market openings.

Sports betting commands 49.3% market share (2025). Casino games at 42.6% are driven by legal availability in only 8 states, limiting their addressable market relative to sports betting's state coverage. Mobile at 68.7% continues to dominate and grow, reinforcing the market's mobile-first architecture through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Game Type |

Sports Betting - 49.3% share (2025) |

|

Leading Device |

Mobile - 68.7% share (2025) |

|

Leading Region |

Northeast - 32.4% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Sports Betting at 49.3% (2025): Sports betting drives the market through high user engagement, real-time wagering, and strong integration with mobile platforms. Its widespread legalization across states and partnerships with sports leagues further accelerate user acquisition and revenue growth.

- Mobile at 68.7% driven by operator mobile-first investment and app quality: Mobile betting apps offer live in-game wagering with sub-second odds updates, parlay builders, and personalized promotional offers that desktop cannot replicate.

- Northeast at 32.4% - the most mature and highest-revenue US gambling region: New Jersey pioneered US online gambling post-PASPA with the nation's first legal online sportsbook launch.

United States Online Gambling Market Overview

The US online gambling market encompasses all forms of internet-based wagering, including sports betting, online casino games, daily fantasy sports, and poker. The market operates within a state-regulated framework, with each of the 50 states independently deciding whether and how to legalize online gambling within its jurisdiction.

The ecosystem integrates technology platform providers, gambling operators, state gaming regulators, payment processors, and media and affiliate marketing networks. Macroeconomic drivers include US smartphone penetration, 5G network coverage expanding real-time betting infrastructure, US sports fans, and state governments' fiscal incentive to legalize and tax online gambling revenues, projected to generate high annual state tax receipts from jurisdictions.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

- 38+ States Legalized Sports Betting Creating Vast Addressable Market: As of 2025, 38 states and the District of Columbia have legalized sports betting in some form. Each new state opening creates an immediate surge in operator customer acquisition.

- Smartphone Penetration Enabling Mobile-First Betting Normalization: Nearly all Americans (98%) now own some type of cellular device, with 9 in 10 people (91%) using a smartphone, combined with 5G network coverage, creates optimal infrastructure for mobile betting as a normalized consumer entertainment behavior.

- State Tax Revenue Incentives Accelerating Legalization Momentum: US states with legal online sports betting generated high tax revenues, representing a compelling fiscal argument for non-legalized states.

Market Restraints

- Patchwork State-by-State Regulatory Complexity: Unlike European markets with national licensing frameworks, US operators must obtain individual state licenses. Compliance costs for a multi-state operator may be very high across legal, compliance, and technology localization requirements. This regulatory fragmentation creates barriers for smaller operators and increases operating costs for all market participants.

- Problem Gambling and Responsible Gaming Regulatory Pressure: US state gaming regulators are intensifying responsible gaming requirements, including mandatory self-exclusion programs, deposit limits, cooling-off periods, and marketing restrictions.

Market Opportunities

- California and Texas Legalization Creating Combined Market Opportunity: California and Texas together represent the largest unlegalized US sports betting markets.

- iGaming Expansion: Online casino games are available in only 8 states as of April 2026, despite online sports betting being legal in US states. Each new iGaming state legalization adds high value to the national market within 24 months.

Market Challenges

- Operator Profitability Pressure from High Marketing and Promotional Costs: US online gambling operators should spend heavily on marketing and promotional bonuses, reflecting the intense customer acquisition competition in the market.

- NFL and Major Sports League Scheduling Concentration Creating Revenue Seasonality: US online gambling revenues are heavily concentrated in September-February (NFL regular season and playoffs), creating significant seasonality risk.

Emerging Market Trends

1. In-Game Live Betting Reshaping Sports Wagering Revenue Mix

In-game live betting is transforming the U.S. online gambling market by increasing user engagement through real-time wagering opportunities during events. It is shifting revenue mix toward higher-frequency bets, boosting operator margins and enhancing overall platform monetization.

2. AI-Powered Personalization and Responsible Gaming Platforms

AI-powered personalization and responsible gaming platforms are transforming the market by delivering tailored user experiences, targeted promotions, and real-time recommendations that boost engagement and retention. At the same time, advanced analytics enable early detection of risky behavior, supporting compliance and strengthening player protection frameworks.

3. iGaming Expansion Driving the Second US Online Gambling Growth Wave

iGaming expansion is driving the next growth wave in the market by diversifying beyond sports betting into online casino games, increasing revenue streams and user engagement. It also supports higher margins and recurring play, strengthening long-term market growth potential.

4. Daily Fantasy Sports Evolution into Skill-Based Gaming Adjacent Market

Daily fantasy sports are evolving into a broader skill-based gaming segment, attracting users seeking strategy-driven and interactive experiences beyond traditional betting. This shift is expanding the addressable audience, increasing engagement, and creating new monetization opportunities in the U.S. online gambling market.

Industry Value Chain Analysis

The US online gambling value chain spans platform software development through operator brand building, state regulatory licensing, payment processing, affiliate marketing, and end-user acquisition serving American adults who have placed a legal sports bet. Operators capture 40-60% gross margins on gaming revenues; platform providers earn 5-10% of GGR on technology licensing; payment processors earn 1-3% on transactions.

|

Stage |

Key Participants |

|

Software & Platform Developers |

Providers of gaming platforms, sportsbook engines, casino software, live dealer technology, and user interface solutions; cloud and backend technology providers |

|

Gambling Operators & Brands |

Online sportsbook operators, iGaming platforms, fantasy sports providers, and casino brands offering betting and gaming services to consumers |

|

State Regulatory Licensing |

State-level gaming authorities and regulatory bodies are responsible for licensing, compliance, taxation, and operational oversight of online gambling activities |

|

Payment Processors & Digital Wallets |

Payment gateways, digital wallet providers, card networks, and alternative payment solutions enable secure deposits and withdrawals |

|

Affiliate & Media Marketing Partners |

Media networks, sports broadcasters, affiliate marketing platforms, comparison websites, and digital advertising channels are driving user acquisition |

|

End Users (Bettors & Players) |

Adult population in legalized states, sports bettors, online casino users, mobile-first consumers, and younger demographics engaging in digital gaming platforms |

The US online gambling ecosystem's most distinctive characteristic versus other markets is the state-by-state regulatory structure requiring operators to obtain individual licenses, establish technology integrations with state-mandated gaming systems, and comply with distinct responsible gaming requirements in each jurisdiction. This creates a high-barrier-to-entry value chain where scale advantages generate compounding operational efficiency advantages unavailable to smaller operators.

Technology Landscape in the United States Online Gambling Industry

Mobile App Development and Real-Time Betting Technology

Mobile app development and real-time betting technology are central to the U.S. online gambling technology landscape, enabling seamless, on-the-go betting with instant access to live odds, in-play wagering, and interactive features. These platforms leverage real-time data processing, AI, and cloud infrastructure to deliver low-latency experiences, personalized interfaces, and continuous user engagement.

AI and Machine Learning for Personalization and Odds Setting

AI and machine learning are a core part of the U.S. online gambling technology landscape, enabling platforms to deliver hyper-personalized user experiences and highly dynamic odds setting. Advanced algorithms analyze vast datasets, including player behavior, betting history, and real-time game data, to generate tailored recommendations and continuously adjust odds with high accuracy. These technologies also enhance risk management, fraud detection, and predictive analytics, creating a data-driven ecosystem where personalization, real-time decision-making, and automated pricing models define modern sportsbook and iGaming platforms.

Payment Technology and Financial Compliance Infrastructure

Payment technology and financial compliance infrastructure are a critical part of the U.S. online gambling technology landscape, ensuring secure, real-time transactions while meeting strict regulatory requirements. Platforms integrate advanced payment gateways, digital wallets, and multi-currency systems with encryption, fraud detection, and seamless mobile checkout to support high transaction volumes.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Device | Sports Betting | 49.3% | 2025 |

| Equipment | Mobile | 68.7% | 2025 |

| Region | Northeast | 32.4% | 2025 |

By Game Type

Sports betting leads at 49.3% market share (2025). NFL wagering alone generates a high demand for total US sports betting handle. The sports betting segment grows at ~7.80% CAGR (2026-2034), driven by new state openings, in-game live betting adoption reaching handle, and international and same-game parlay wagering expanding handle per bettor.

To access detailed market analysis, Request Sample

Casino at 42.6% is geographically restricted to 8 states but generates the highest revenue-per-active-user of any segment. Online slots represent 60%+ of iGaming revenues; live dealer games are the fastest-growing iGaming sub-category at 25%+ CAGR. Others at 8.1% encompasses DFS, poker, and prediction markets growing at ~5.4% CAGR.

By Device

Mobile leads at 68.7% market share (2025). The US mobile betting experience has normalized betting as smartphone entertainment. 91% smartphone usage further expands the market growth. Mobile's ~8.2% CAGR (2026-2034) is driven by 5G enabling seamless live streaming + in-game betting combinations, wearable device betting experiments, and younger demographic (18-30) user concentration on mobile-exclusive platforms.

Desktop at 24.5% serves serious bettors and iGaming players who prefer larger screens for multi-tabling poker, complex parlay building, or live dealer casino games. Desktop grows at ~5.6% CAGR, limited by mobile's share gains. Others at 6.8% includes Smart TV apps, in-arena betting kiosks, and tablet devices growing with venue-integrated wagering programs.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

Northeast |

32.4% |

Early legalization of online gambling, strong regulatory frameworks, high population density, mature iGaming and sports betting markets, and high revenue contribution from established states |

|

South |

27.8% |

Growing legalization momentum, strong sports culture driving betting demand, mobile-first adoption, increasing state-level regulatory developments, and a rising user base |

|

West |

22.6% |

Large population base, high digital adoption, expansion potential in key states, and increasing interest in mobile betting |

|

Midwest |

17.2% |

Rapid market growth with new state entries, increasing adoption of mobile sportsbooks, and strong engagement in sports betting |

The Northeast's 32.4% dominance reflects market maturity, with New Jersey launched the US's first legal online sportsbook in June 2018, providing the longest track record of consumer normalization. New York's mobile sports betting launch at a high tax rate was the single largest US market opening event.

The South's 27.8% reflects regions successful mobile-only model, online-only sports betting. The Midwest's 17.2% features Michigan as its highest-value state, increasing adoption of mobile sportsbooks, and strong engagement in sports betting.

Competitive Landscape

The US online gambling market is highly concentrated in sports betting – Flutter and BetMGM collectively control 60-65% of the US sports betting market share (2025), representing a duopoly structure unusual in scale among major US consumer industries.

|

Company Name |

Brand / Platform |

Market Position |

Core Strength |

|

Flutter Entertainment |

FanDuel |

Market Leader |

Strong market leadership driven by a diversified sportsbook and iGaming portfolio, supported by advanced technology and high user engagement. |

|

BetMGM |

BetMGM, Borgata Online, PartyCasino, PartyPoker, Wheel of Fortune Casino |

Strong Challenger |

Strong position through a leading iGaming and sportsbook platform. |

|

PENN Entertainment, Inc. |

theScore BET |

Strong Challenger |

The company developed apps for fun anytime with online gaming and sports betting |

|

Rush Street Interactive |

Rush Street Interactive, BetRivers Poker, PlaySugarHouse |

Established Player |

Rush Street Interactive's ambition is to create the most fun, friendly, and fair online gaming platform in the Americas. |

|

Hard Rock Bet |

Hard Rock Bet |

Established Player |

Hard Rock Bet has remixed the online sportsbook and casino experience to deliver legendary Hard Rock entertainment |

The top 5 operators collectively account for approximately 85-90% of US online gambling revenues. The competitive dynamic is shifting from customer acquisition to customer retention and monetization.

Key Company Profiles

Flutter Entertainment

Flutter Entertainment is one of the world's largest online gambling companies. Flutter Entertainment's global scale provides technology leverage, capital access, and talent depth beyond any US-only operator.

- Product Portfolio: FanDuel

- Recent Developments: In December 2025, FanDuel, part of Flutter Entertainment and CME Group, launched prediction markets through the new FanDuel Predicts app that will expand access to financial markets for millions of customers in the United States.

- Strategic Focus: Maintain sports betting market share leadership through product quality; iGaming expansion as primary addressable market opportunity.

BetMGM

BetMGM is the US online gambling industry's operator, uniquely positioned as the digital extension. The company has a strong position through a leading iGaming and sportsbook platform.

- Product Portfolio: BetMGM, Borgata Online, PartyCasino, PartyPoker, Wheel of Fortune Casino.

- Recent Developments: In July 2024, BetMGM expanded its mobile sports betting services across Washington, D.C. Previously limited to a two-block area around the sportsbook at Nationals Park, sports fans throughout the district can now enjoy the BetMGM sports wagering experience, with rewards linked to both MGM Resorts and Marriott Bonvoy destinations.

- Strategic Focus: Expanding its market presence through mobile sports betting, enhancing user engagement with a broad portfolio of iGaming offerings, and leveraging partnerships to integrate loyalty rewards across major hospitality brands.

Market Concentration Analysis

The US online gambling market is among the most concentrated consumer technology markets in the US. Flutter and BetMGM’s combined 60-65% sports betting market share creates a structural duopoly that has intensified, when 10+ operators competed for a similar share. The top 5 operators collectively capture 85-90% of US online gambling revenues (2025), with Tier-2 operators competing primarily for the remaining 10-15% of market share rather than meaningfully challenging the duopoly.

iGaming market concentration is modestly lower, reflecting the importance of existing online casino technology and premium game content selection that differentiates from sports betting market share positions. Evolution Gaming's virtual monopoly on US live dealer casino content represents a value chain concentration point that few recognize as structurally important.

Investment & Growth Opportunities

Fastest Growing Segments

Mobile device (~8.2% CAGR), sports betting (~7.80% CAGR), iGaming online casino expansion across new states (~25%+ CAGR per new state), in-game live betting (~15% CAGR within sports betting), and AI-personalization-driven promotional efficiency improvement represent the market's highest-growth investment vectors. California legalization is the single event that would most materially accelerate the 2026-2034 forecast trajectory.

Emerging Market Opportunities

The US prediction markets segment, regulated differently from gambling as financial contracts, represents an emerging opportunity to operate prediction markets on sports outcomes under CFTC oversight. This regulatory arbitrage allows prediction markets to operate in states where sports betting remains illegal, potentially capturing an annual wagering volume by 2028. E-sports betting, growing at 15%+ CAGR globally, is underdeveloped in the US market, with only 10% of operators offering comprehensive e-sports wagering products.

Investment Themes

iGaming state legalization plays: Each new iGaming state legalization creates an addressable market. Operators with existing sports betting licenses in target states have structural first-mover advantages in the licensing queue, making state-by-state iGaming expansion rights a high-value strategic asset.

Future Market Outlook (2026-2034)

The US online gambling market is projected to grow from USD 11.80 Billion in 2025 to USD 12.70 Billion in 2026, reaching USD 22.8 Billion by 2034, delivering a 7.33% CAGR and near-doubling the market over the forecast period. The market's anchor value of USD 16.9 Billion in 2030 reflects a fundamentally transformed competitive and regulatory landscape versus 2025, with iGaming available in more states (versus 8 in 2026), mobile betting normalized in 40+ states, and the companies' duopoly either reinforced by failed challenge or beginning to fracture as media-operator integration models mature.

Three structural forces define the US online gambling market's growth trajectory with high predictability: state-level legalization expansion creating new addressable markets at an estimated 3-4 new states annually through 2028; iGaming legalization wave expanding per-capita revenue well beyond sports-betting-only states' performance; and AI personalization transforming the better lifetime value economics by improving retention, reducing churn, and increasing average bets per active user - the three metrics that determine operator profitability in mature market phases.

Research Methodology

Primary Research

Primary research comprised structured interviews with 70+ industry stakeholders (2025), including CEO and C-suite executives; state gaming regulators from New Jersey DGE, Michigan MGCB, and Pennsylvania PGCB; sports league betting partnership officers; technology platform providers; affiliate marketing network operators; and responsible gaming program directors from the National Council on Problem Gambling.

Secondary Research

Secondary research encompassed American Gaming Association (AGA) State of the States 2025 Report, AGA Commercial Gaming Revenue data through Q4 2024, individual state gaming commission monthly revenue reports (New Jersey, Michigan, Pennsylvania, New York, Ohio), company investor presentations and earnings calls, Nielsen Sports Betting consumer research 2024, and Eilers & Krejcik Gaming market analysis reports. Over 120 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts used bottom-up state-by-state gross gaming revenue models incorporating licensed state count projections, per-active-bettor revenue assumptions calibrated against mature state benchmarks, new state opening timelines based on legislative tracking data, iGaming expansion probability scenarios by state, and mobile versus desktop revenue split trends. Key inputs include US Census Bureau state population data, AGA legalization tracking, smartphone penetration rates, NFL and NBA viewership trends, and operator guidance from public company earnings disclosures.

United States Online Gambling Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Game Types Covered |

|

| Devices Covered | Desktop, Mobile, Others |

| Region Covered | Northeast, Midwest, South, West |

| Companies Covered | Flutter Entertainment, BetMGM, PENN Entertainment, Inc., Rush Street Interactive, Hard Rock Bet, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Online Gambling Market Report

The US online gambling market reached USD 12.70 Billion in 2026, driven by 38+ legalized states, companies' combined market share, record NFL wagering volumes, and iGaming expansion in 8 states.

The market is projected to grow at 7.33% CAGR during 2026-2034, reaching USD 22.8 Billion by 2034, driven by new state legalizations, iGaming expansion from 7 to 15-18 states, mobile penetration, and AI personalization.

Sports betting leads at 49.3% (2025), anchored by NFL wagering generating 35%+ of total handle, in-game live betting reaching 35%+ of sports betting revenue, and 38+ state legal coverage versus Casino's 8-state iGaming limitation.

Mobile leads at 68.7% (2025), with DraftKings and FanDuel 4.8/5.0-rated apps processing 78% of active bettor wagers via smartphone, driven by 95%+ US smartphone penetration and 5G enabling seamless live in-game betting.

The Northeast leads at 32.4% (2025), anchored by New Jersey's online gambling revenue, New York's mobile sports betting, and the highest concentration of early-legalizing states with 7+ years of market maturity.

Leading companies include Flutter Entertainment, BetMGM, PENN Entertainment, Inc., Rush Street Interactive, and Hard Rock Bet, among others.

The US online gambling market is projected to reach approximately USD 16.9 Billion by 2030, driven by iGaming expansion, mobile crossing 75% of total betting handle, and in-game live betting exceeding 50% of sports wagering.

Casino holds 42.6% (2025), from 8 legal iGaming states. Michigan demonstrates per-state potential; each new iGaming state legalization adds a high-demand opportunity within 24 months of launch.

AI powers personalized betting recommendations, promotional targeting efficiency, real-time in-game odds setting, and problem gambling behavioral monitoring mandated by regulators.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade