United States Oral Hygiene Market Size, Share, Trends and Forecast by Product, Distribution Channel, Application, and Region, 2026-2034

United States Oral Hygiene Market Size, Share, Trends & Forecast (2026-2034)

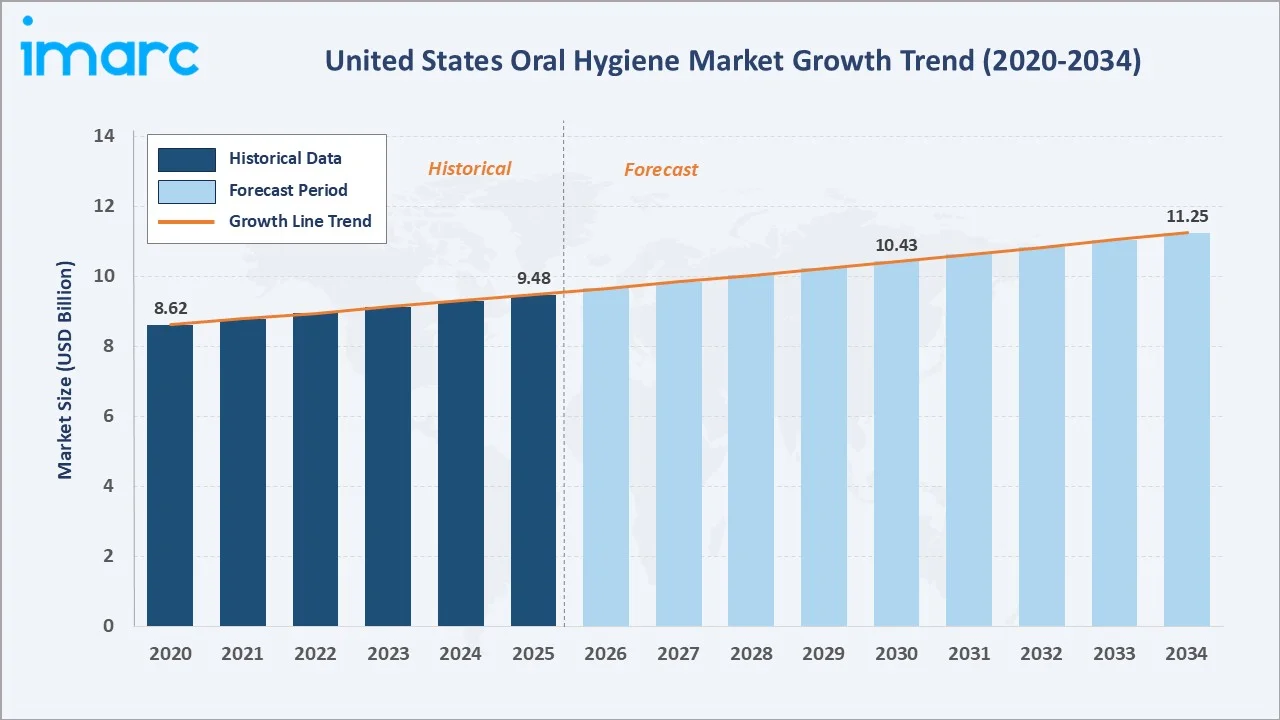

The United States oral hygiene market size reached USD 9.48 Billion in 2025 and is projected to reach USD 11.25 Billion by 2034, exhibiting a CAGR of 1.9% during 2026-2034. Rising dental disease prevalence, growing consumer health awareness, and premium product innovation are the primary forces driving market growth.

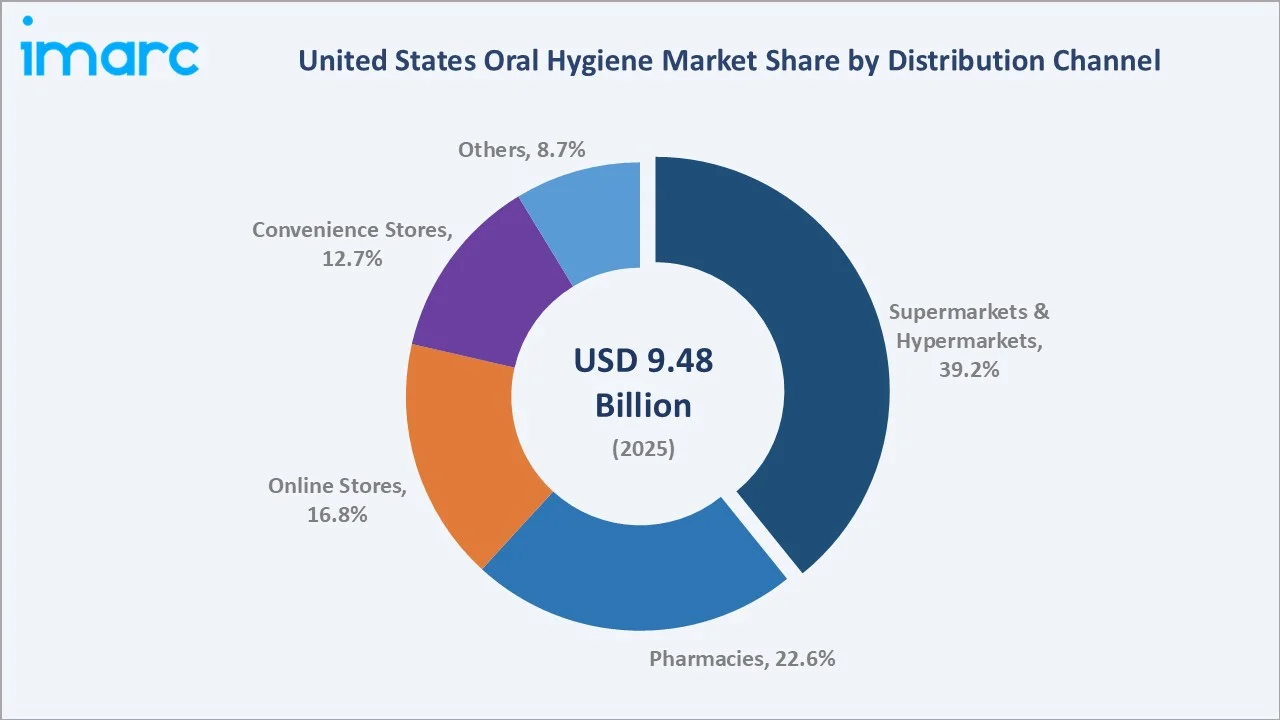

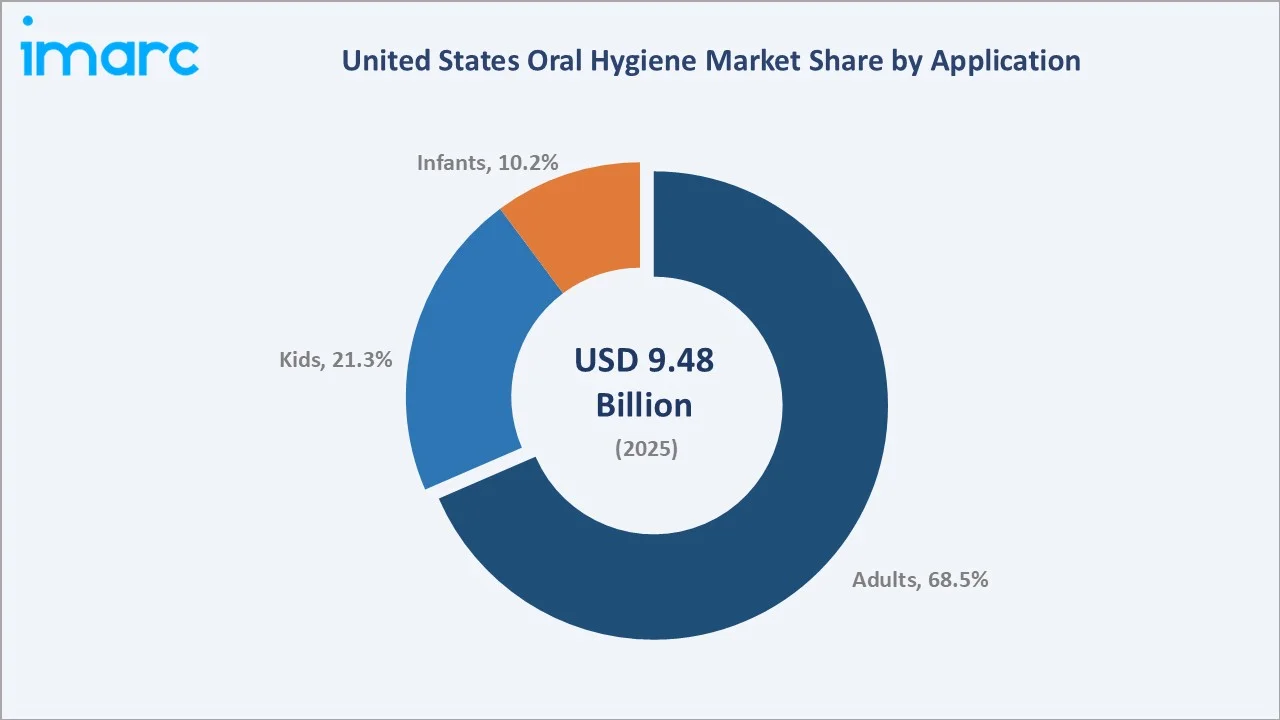

Supermarkets and hypermarkets dominate distribution at 39.2% in 2025, while Adults lead the application segment at 68.5%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.48 Billion |

|

Forecast Market Size (2034) |

USD 11.25 Billion |

|

CAGR (2026-2034) |

1.9% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Distribution Channel |

Supermarkets & Hypermarkets (39.2%, 2025) |

|

Leading Application |

Adults (68.5%, 2025) |

The United States oral hygiene market growth trajectory from 2020 through 2034, with historical expansion to USD 9.48 Billion in 2025, reflects sustained health-awareness-driven demand, while the forecast to USD 11.25 Billion captures accelerating e-commerce adoption, premium product uptake, and expanding dental care awareness.

To get more information on this market, Request Sample

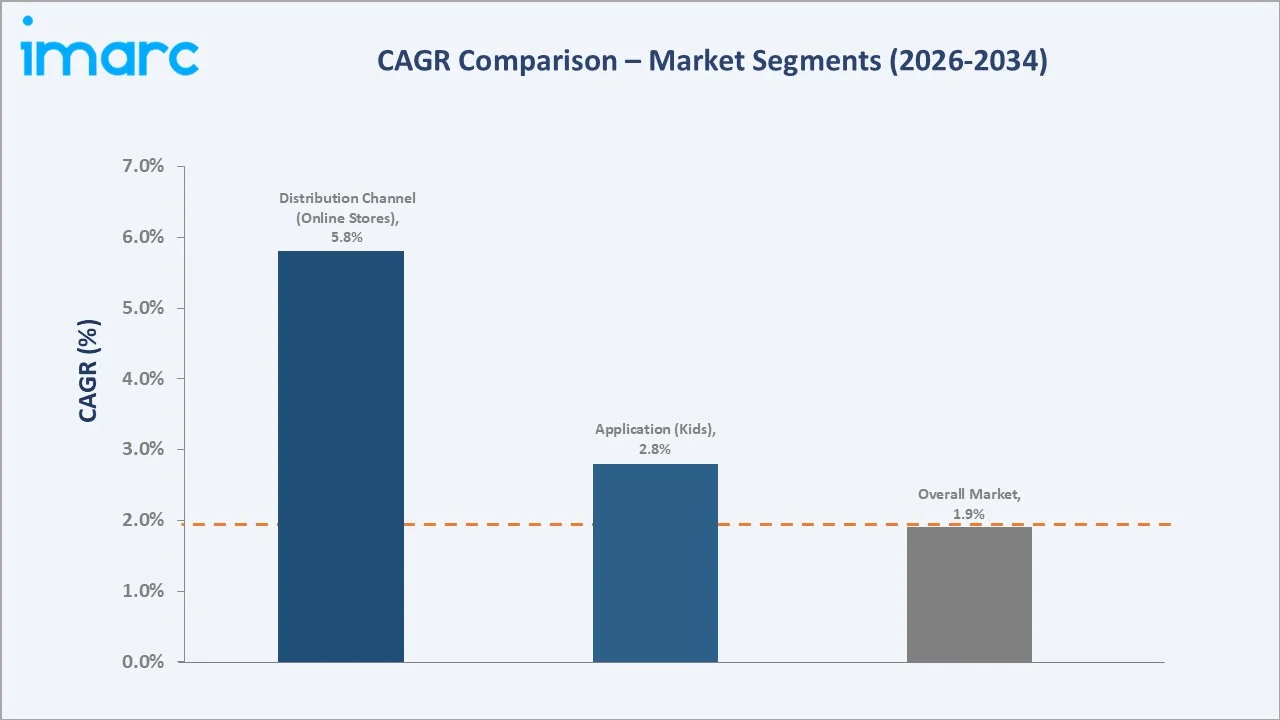

The CAGR trajectories across key distribution channel and application sub-segments, with online stores at ~5.8% CAGR and the kids application segment at ~2.8% CAGR, are the fastest-growing categories within the United States oral hygiene industry analysis through 2034.

Executive Summary

The United States oral hygiene market is on a sustained growth trajectory from USD 9.48 Billion in 2025 to USD 11.25 Billion by 2034. Oral hygiene products encompassing toothbrushes, toothpaste, mouthwash, dental floss, and whitening solutions benefit from daily essential usage, non-discretionary demand, and widening premium adoption across all demographics.

Supermarkets and hypermarkets dominate the distribution channel at 39.2% in 2025, reflecting mass retail's core role as the primary household oral care purchase point. Online stores at 16.8% are the fastest-growing channel at ~5.8% CAGR, driven by subscription replenishment models and DTC brand adoption across digital-native consumer cohorts.

Adults command 68.5% of the application segment in 2025, representing the largest purchasing demographic across toothpaste, mouthwash, whitening, and electric toothbrush categories. Kids (21.3%) and Infants (10.2%) are growing faster as parental investment in early childhood dental health expands age-appropriate product ranges.

Key Market Insights

|

Insight |

Data |

|

Largest Distribution Channel |

Supermarkets & Hypermarkets – 39.2% share (2025) |

|

Fastest-Growing Channel |

Online Stores – ~5.8% CAGR (2026-2034) |

|

Leading Application |

Adults – 68.5% share (2025) |

|

Fastest-Growing Application |

Kids – ~2.8% CAGR (2026-2034) |

|

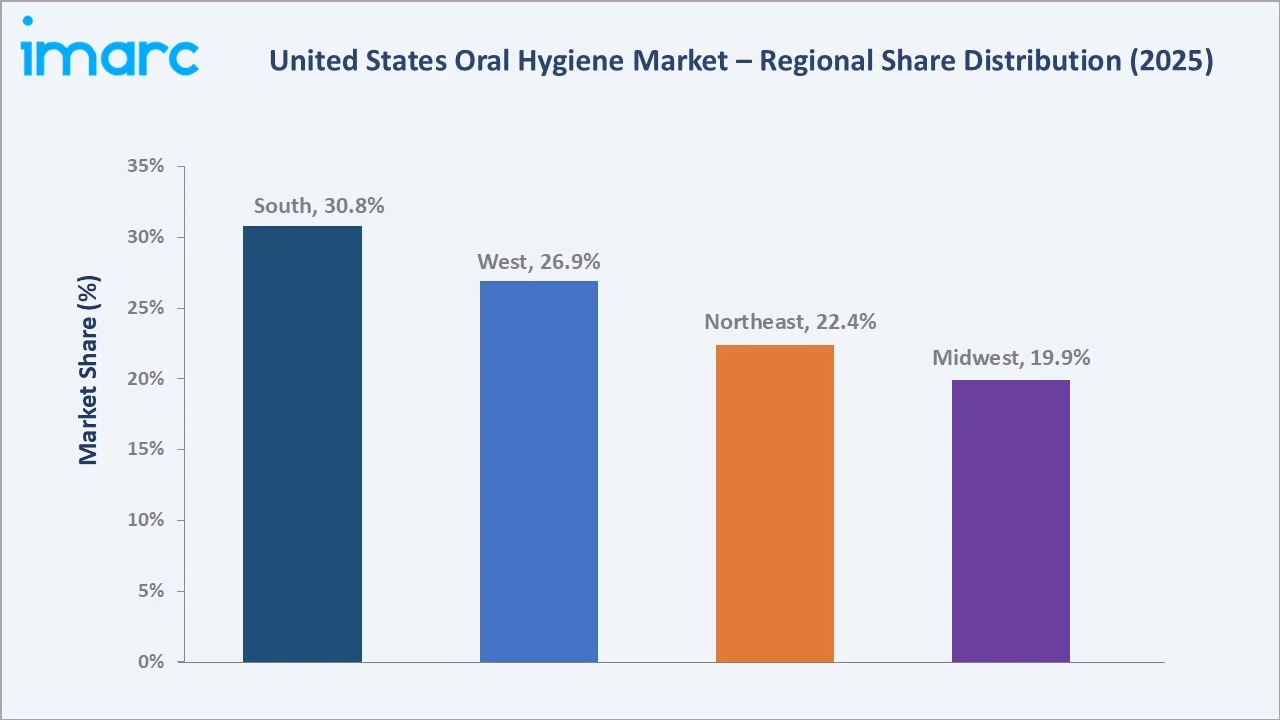

Dominant Region |

South – 30.8% share (2025) |

|

Top Companies |

Colgate-Palmolive Company, Procter & Gamble, Haleon Group of Companies, Church & Dwight Co., Inc., Koninklijke Philips N.V., Sunstar Suisse S.A. |

Key Analytical Observations Supporting the Above Data:

- Supermarkets and hypermarkets, with 39.2% in 2025, dominate oral hygiene distribution through consolidated household shopping, broad brand assortment, consistent promotional activity, and competitive pricing for everyday replenishment of toothpaste, toothbrushes, and mouthwash.

- Online stores at 16.8% in 2025 are the fastest-growing channel at ~5.8% CAGR through 2034, driven by subscription replenishment models, DTC brand emergence, and Amazon's oral care category capturing both price-conscious and premium-seeking consumer segments simultaneously.

- Adults at 68.5% in 2025 represent the dominant application segment spending across the full oral care product range, including premium electric toothbrushes, whitening toothpaste, therapeutic mouthwash, sensitivity formulations, and cosmetic dentistry adjuncts.

- The South region's 30.8% market share in 2025 reflects high population concentration across Texas, Florida, and the Southeast, above-national-average dental disease prevalence, and a robust supermarket and pharmacy retail infrastructure supporting consistent oral care demand.

United States Oral Hygiene Market Overview

Oral hygiene refers to the practices and products used to maintain the health of teeth, gums, and the oral cavity. Core product categories include toothpaste, manual and powered toothbrushes, mouthwash and rinses, dental floss and interdental cleaners, denture care products, and at-home whitening systems.

The US oral hygiene ecosystem integrates global multinational consumer goods companies, specialty oral health brands, retail pharmacy chains, mass market retailers, e-commerce platforms, dental professional networks, and regulatory bodies including the FDA and American Dental Association, creating a highly structured and competitive consumer health market.

Market Dynamics

To evaluate market opportunities, Request Sample

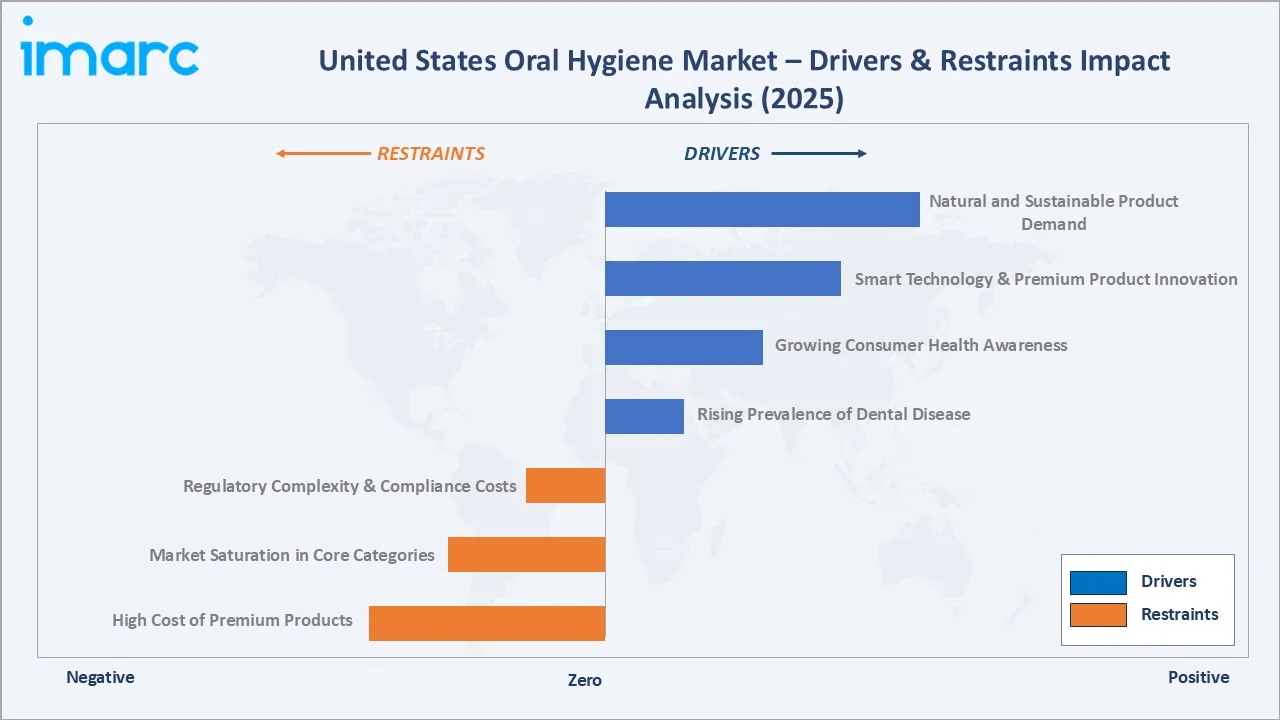

Market Drivers

- Rising Prevalence of Dental Disease: The CDC reports that 91% of US adults aged 20-64 have experienced dental caries. High disease burden creates non-discretionary, habitual demand for preventive and therapeutic oral hygiene products across all demographic segments.

- Growing Consumer Health Awareness: Federal public health campaigns, dental professional endorsements, and extensive media coverage linking oral health to systemic conditions including cardiovascular disease and diabetes are motivating increased consumer investment in premium oral care products and routine upgrades.

- Smart Technology and Premium Product Innovation: AI-powered electric toothbrushes with real-time coaching, sonic cleaning systems, clinically validated whitening platforms, and nano-hydroxyapatite remineralizing toothpastes are creating a fast-growing premium tier, expanding category average selling prices and revenue per household.

Market Restraints

- High Cost of Premium Products: Elevated price points for advanced oral care devices and specialized treatment solutions create affordability constraints for price-sensitive consumer segments, thereby limiting adoption rates and restricting penetration within high-value product categories. This pricing disparity widens the gap between mass-market and premium offerings, slowing overall category premiumization, while also requiring manufacturers to carefully balance innovation with cost efficiency to ensure broader accessibility without margin erosion.

- Market Saturation in Core Categories: Core segments such as toothpaste and manual toothbrushes demonstrate near-universal household penetration, resulting in limited scope for volume expansion; consequently, growth is increasingly dependent on premiumization and product innovation to drive consumer trade-up rather than new category adoption. This dynamic intensifies competitive pressures among established players, making differentiation critical, while also pushing brands to rely on value-added features, strong branding, and targeted marketing to stimulate replacement demand and incremental consumption.

Market Opportunities

- E-Commerce and Subscription Commerce: The U.S. oral care e-commerce segment, with steady mid-single-digit growth, represents a high-momentum channel driven by increasing digital adoption and shifting consumer purchasing behavior. Direct-to-consumer subscription models are enhancing revenue predictability while effectively engaging premium, younger consumer cohorts through convenience, personalization, and brand-led experiences.

- Natural and Sustainable Product Demand: Growing preference for fluoride-free, botanical-ingredient oral care and eco-packaged products is creating a premium niche. Bamboo toothbrushes, charcoal toothpaste, refillable tablet toothpaste systems, and zero-waste packaging attract environmentally conscious consumers willing to pay meaningful price premiums.

Market Challenges

- Regulatory Complexity and Compliance Costs: FDA over-the-counter drug monograph regulations governing fluoride-containing toothpaste and antimicrobial mouthwash impose significant compliance costs. New active ingredient efficacy claims require extensive clinical substantiation, lengthening time-to-market for differentiated therapeutic formulations.

- Shelf Space Competition and Private Label Pressure: Major retail chains including Walmart, Target, and CVS are aggressively expanding private label oral care lines at 30-40% price discounts to national brands, capturing price-sensitive consumer segments and compressing national brand shelf space allocation and retail margin structures.

Emerging Market Trends

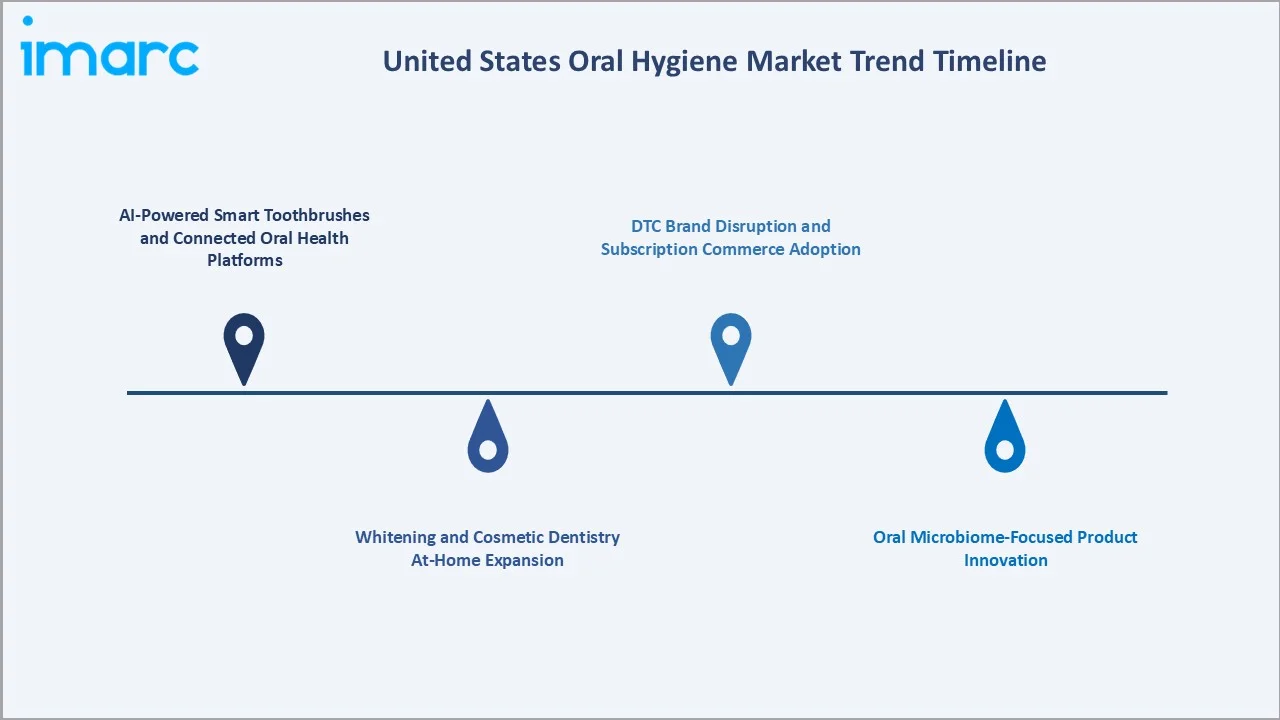

1. AI-Powered Smart Toothbrushes and Connected Oral Health Platforms

Philips Sonicare and Oral-B iO smart toothbrush lines incorporate pressure sensors, brushing position detection, and real-time coaching via companion smartphone apps. These devices are expanding the premium electric toothbrush market and creating sustained digital health engagement between brands and consumers beyond point-of-purchase.

2. Whitening and Cosmetic Dentistry At-Home Expansion

Consumer demand for professional-grade whitening without dental office costs is driving rapid expansion in LED whitening kit platforms, whitening pen systems, and enamel-safe peroxide strip formats. Colgate Optic White Professional and Crest 3D Whitestrips lines are extending into new sub-formats to capture this cosmetic oral care opportunity.

3. Oral Microbiome-Focused Product Innovation

Research linking oral microbiome balance to systemic health is driving innovation in probiotic toothpastes, microbiome-friendly mouthwash formulations without harsh antimicrobials, and enzyme-based plaque-control systems. Health-conscious consumers are increasingly seeking clinically substantiated products addressing root-cause oral biology.

4. DTC Brand Disruption and Subscription Commerce Adoption

Direct-to-consumer oral care brands including Quip, Burst Oral Care, and Hello Products leverage social media, influencer partnerships, and monthly subscription refill models to capture millennial and Gen Z consumers, generating design-led oral care products at accessible premium price points outside traditional retail channels.

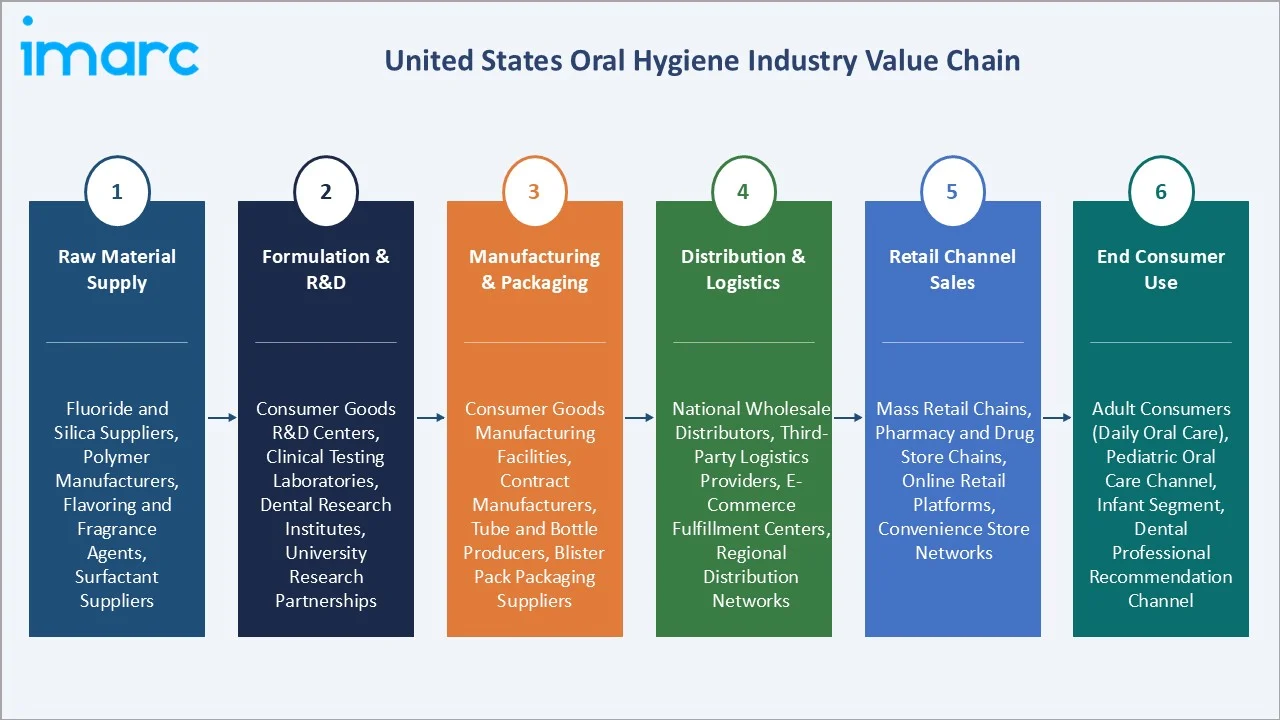

Industry Value Chain Analysis

The oral hygiene value chain spans six stages from raw material sourcing through consumer use. Formulation research, brand marketing, and retail channel management capture the highest value-add margins. Integrated manufacturers with captive raw material sourcing and proprietary active ingredient IP achieve superior cost structures versus asset-light brand operators.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Fluoride and silica suppliers, polymer manufacturers, flavoring and fragrance agents’ producers, surfactant suppliers |

|

Formulation & R&D |

Consumer goods R&D centers, clinical testing laboratories, dental research institutes, university research partnerships |

|

Manufacturing & Packaging |

Consumer goods manufacturing facilities, contract manufacturers, tube and bottle producers, blister pack packaging suppliers |

|

Distribution & Logistics |

National wholesale distributors, third-party logistics providers, e-commerce fulfillment centers, regional distribution networks |

|

Retail Channel Sales |

Mass retail chains, pharmacy and drug store chains, online retail platforms, convenience store networks |

|

End Consumer Use |

Adult consumers (daily oral care), pediatric oral care channel, infant segment, dental professional recommendation channel |

Overall, value creation is driven by brand equity, product innovation, and retail dominance, with increasing influence from e-commerce and direct-to-consumer channels shaping competitive dynamics.

Technology Landscape in the US Oral Hygiene Industry

Electric Toothbrush Technology: Sonic and AI-Powered Systems

Sonic toothbrush technology generates between 30,000 to 40,000 strokes per minute, delivering clinically superior plaque removal versus manual brushing. The latest Oral-B iO Series 9 and Philips Sonicare 9900 Prestige integrate AI pressure sensing, brushing position recognition, and personalized coaching delivered through Bluetooth smartphone connectivity, creating smart oral health systems.

Toothpaste Formulation Innovation: Nano-Hydroxyapatite and Bioactive Glass

Novel remineralizing agents including nano-hydroxyapatite are entering the US market as clinically validated fluoride alternatives and complements. Bioactive glass formulations used in Sensodyne Repair & Protect create mineral precipitation across exposed dentin tubules, providing sensitivity relief beyond conventional potassium nitrate. Activated charcoal and coconut oil-based formulations are expanding the natural toothpaste segment.

Digital Health Platforms and Teledentistry Integration

Teledentistry platforms including Aspen Dental Digital, Byte, and SmileDirectClub are creating digital dental care ecosystems that extend consumer brand engagement beyond product purchase. Philips entered a multi-year partnership with Aspen Dental in 2024, integrating Sonicare into over 1,100 dental offices, creating a hybrid device-service model connecting product use with professional dental care.

Sustainable Materials and Biodegradable Oral Care Technology

Growing regulatory and consumer pressure for sustainability is accelerating development of plant-based toothbrush handles, biodegradable floss from bamboo and corn fibers, and concentrated toothpaste tablets in aluminum packaging that eliminate single-use plastic tubes. Major brands including Colgate and Oral-B have committed to 100% recyclable packaging portfolios by 2025-2030, driving materials science investment in the category.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Toothpaste |

🔒 |

2025 |

|

Distribution Channel |

Supermarkets and Hypermarkets |

39.2% |

2025 |

|

Application |

Adults |

68.5% |

2025 |

|

Region |

South |

30.8% |

2025 |

By Distribution Channel

Supermarkets and hypermarkets command a 39.2% majority share in 2025 as the primary household consumer goods purchase point. Walmart, Kroger, Target, and Costco provide broad brand assortment, consistent in-store promotions, and private label competitive alternatives, making them the default oral care replenishment destination for most US households.

To access detailed market analysis, Request Sample

Pharmacies at 22.6% in 2025 benefit from oral care's positioning as a health and wellness category, with CVS Health, Walgreens, and Rite Aid providing healthcare-associated purchase environments reinforcing therapeutic product credibility. Online stores (16.8%) growing at ~5.8% CAGR through 2034 are the fastest-expanding channel.

By Application

Adults dominate the application segment with 68.5% in 2025, representing the broadest product consumption across all toothbrush types, specialty toothpastes for sensitivity, whitening and gum care, therapeutic mouthwash, and cosmetic dentistry adjuncts. Adults' disposable income and expanding cosmetic oral health awareness sustain premium product adoption and trade-up cycles.

Kids at 21.3% in 2025 represent a growing segment driven by parental investment in age-appropriate dental habits from early childhood. Character-branded toothbrushes, fluoride training toothpastes formulated for 6-12 age groups, low-foam rinses, and orthodontic flossers designed for children are expanding the specialized kids oral care product range.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

30.8% |

High population density; elevated dental disease; strong retail infrastructure |

|

West |

26.9% |

Health & wellness culture; premium adoption; large Hispanic demographic |

|

Northeast |

22.4% |

High disposable income; urban pharmacy density; professional dental network |

|

Midwest |

19.9% |

Stable consumer spending; supermarket channel strength; e-commerce growth |

The South region's 30.8% dominance in 2025 reflects high population concentration across Texas, Florida, Georgia, and the Southeast, combined with above-national-average dental caries rates. The region's strong big-box retail and pharmacy density, with Walmart and CVS having highest per-capita store counts, sustains consistent oral care product demand.

The West at 26.9% in 2025 is shaped by California's deeply embedded health and wellness consumer culture, strong premium product adoption, and the large Hispanic demographic creating bilingual oral care marketing requirements. The Northeast's 22.4% reflects high urban pharmacy concentration and above-average household oral care spending in metropolitan markets.

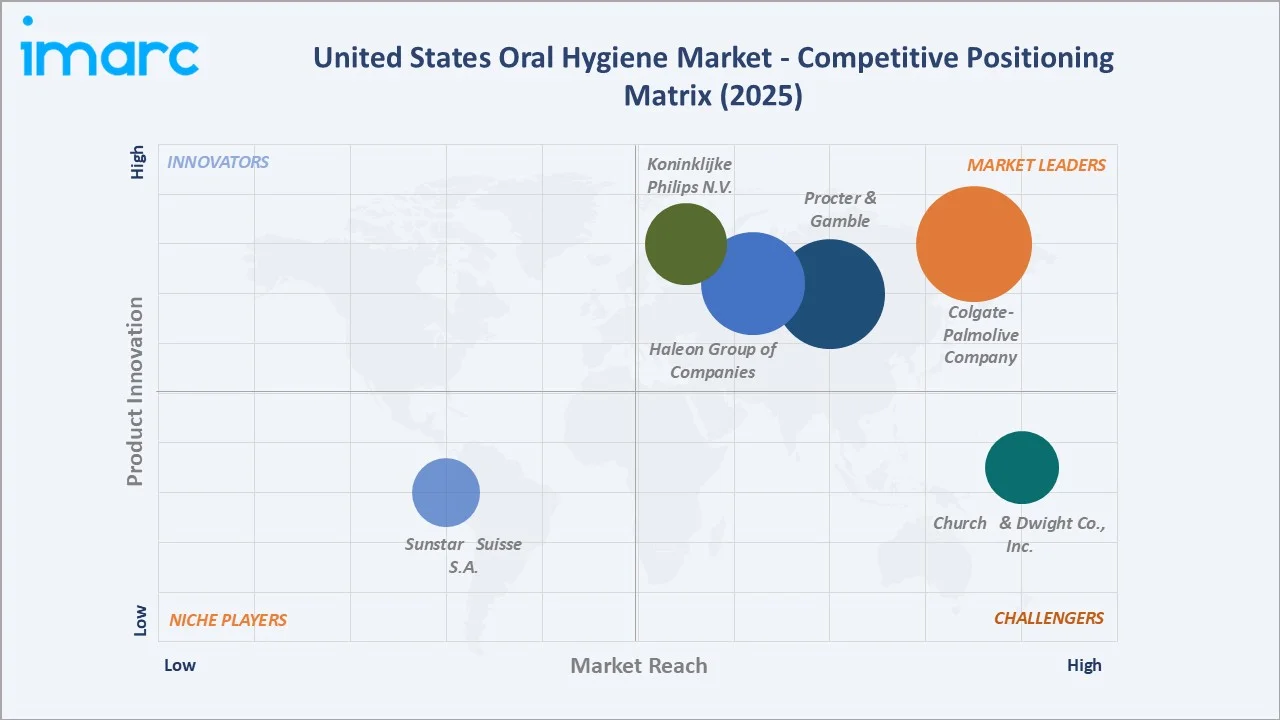

Competitive Landscape

The United States oral hygiene market is highly concentrated at the national brand level, with Colgate-Palmolive and Procter & Gamble collectively accounting for approximately 50% of total US market revenue. Haleon, Unilever, and Kenvue hold significant positions in therapeutic and mouthwash segments, while DTC and specialty brands are capturing incremental share.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Colgate-Palmolive Company |

Colgate, Tom’s of Maine, Hello |

Leader |

Innovation + sustainability + premiumization |

|

Procter & Gamble |

Crest, Fixodent, Oral-B |

Leader |

AI device + whitening category dominance |

|

Haleon Group of Companies |

Sensodyne, parodontax, Polident |

Leader |

Therapeutic oral health premiumization |

|

Church & Dwight Co., Inc. |

Arm & Hammer, TheraBreath |

Challenger |

Baking soda natural whitening positioning |

|

Koninklijke Philips N.V. |

Sonicare |

Leader |

Premium connected device market share |

|

Sunstar Suisse S.A. |

GUM, Butler, GelX, Periocline, GrindCare |

Niche |

Dental professional channel specialist |

Key players include Colgate-Palmolive Company, Procter & Gamble, Haleon Group of Companies, Church & Dwight Co., Inc., Koninklijke Philips N.V., Sunstar Suisse S.A., and others.

Key Company Profiles

Colgate-Palmolive Company

Colgate-Palmolive is the largest oral hygiene company globally and the category leader in US toothpaste, commanding over 35% market share through its Colgate Total, Colgate Optic White, and Colgate Sensitive lines. The company's innovation pipeline spans smart toothbrush development, whitening technology, and sustainable packaging.

- Product Portfolio: Colgate Total, Optic White Advanced, Colgate 360 toothbrush, and Colgate Peroxyl oral cleanser.

- Recent Developments: In January 2026, Colgate-Palmolive announced a multi-year global partnership with the WHO Foundation to support the World Health Organization’s efforts in advancing oral health worldwide. The collaboration includes a four-year funding commitment aimed at strengthening prevention, education, and system-level integration of oral healthcare.

- Strategic Focus: Colgate's strategy combines core category innovation with premiumization in whitening and electric toothbrush, sustainability through recyclable packaging commitments, and digital brand engagement through dental health apps and teledentistry partnerships.

Procter & Gamble

Procter & Gamble's Oral-B and Crest brands collectively represent the largest oral care portfolio in the US market. Oral-B dominates the US power toothbrush segment through continuous AI and connected technology investment, while Crest leads whitening toothpaste and whitening strip formats with Crest 3D Whitestrips.

- Product Portfolio: Oral-B iO Series 9 with AI brushing recognition, Crest 3D Whitestrips, Crest Pro Health Advanced, Crest Gum Detoxify, and Scope Mouthwash.

- Recent Developments: In December 2020, Procter & Gamble introduced recyclable high-density polyethylene (HDPE) toothpaste tubes across its key oral care brands, reinforcing its commitment to sustainable packaging innovation. The initiative, being implemented across North America and Europe, is designed to make toothpaste tubes compatible with existing recycling infrastructure, significantly improving ease of disposal for consumers.

- Strategic Focus: P&G's oral care strategy focuses on Oral-B connected device leadership through sustained R&D investment and Crest's whitening category dominance through product line extensions targeting sensitivity, enamel protection, and professional-grade efficacy.

Haleon Group of Companies

Haleon, holds a strong US market position through therapeutic oral health brands. Sensodyne is the world's leading sensitivity toothpaste brand and Parodontax leads the gum health sub-category, with both brands growing as consumers seek specialized therapeutic oral care solutions.

- Product Portfolio: Sensodyne Repair & Protect, Sensodyne Pronamel, Sensodyne Clinical White, Parodontax Complete Protection, Polident denture adhesive, and Biotene dry mouth relief products.

- Recent Developments: In October 2024, Haleon announced a £130 million investment to establish a Global Oral Health Innovation Centre in the UK, aimed at strengthening its research and development capabilities in oral care. The state-of-the-art facility is designed to serve as the central hub for scientific research, product innovation, and cross-functional collaboration across Haleon’s oral health portfolio, enhancing its ability to address evolving consumer needs.

- Strategic Focus: Haleon's strategy targets the therapeutic-premium overlap, expanding Sensodyne into whitening and daily enamel protection, and Parodontax into daily-use gum health prevention, supported by 2.7% of revenue dedicated to clinical R&D annually.

Market Concentration Analysis

The US oral hygiene market is highly concentrated at the national brand level, with the top five companies (Colgate-Palmolive, P&G, Haleon, Kenvue, and Unilever) collectively accounting for approximately 70% of total revenue. Category-level concentration is even higher in mouthwash (Listerine ~65%) and power toothbrush (Oral-B and Philips ~80% combined share).

Private label and DTC brands are collectively gaining approximately 0.5-1.0 percentage point of national brand share annually, representing the most significant structural competitive threat to incumbents. Amazon oral care, combining private label, DTC exclusives, and national brands, is increasingly the battleground for digital-native consumer acquisition and retention.

Investment & Growth Opportunities

Fastest-Growing Segments

Online stores at ~5.8% CAGR through 2034 represent the highest-growth distribution channel, driven by subscription commerce and DTC brand adoption. The kids application segment at ~2.8% CAGR reflects growing parental investment in early childhood oral health, expanding household total oral care wallet share beyond adult products alone.

Emerging Markets

The therapeutic oral health segment, encompassing sensitivity, gum disease prevention, and remineralization products, is growing faster than the overall market as consumers make evidence-based, dentist-recommended trade-ups. The natural and sustainable product niche, currently representing ~8-10% of the market, is projected to reach 15-18% of market share by 2034.

Venture & Investment Trends

Private equity investment in DTC oral care brands accelerated post-2020, with Quip raising USD 10+ Million rounds for subscription electric toothbrush models and Hello Products expanding natural oral care across mass retail. Smart device platform integration with teledentistry and systemic health monitoring represents the next investment frontier.

Future Market Outlook (2026-2034)

The US oral hygiene market is forecast to expand from USD 9.48 Billion in 2025 to USD 11.25 Billion by 2034 at a CAGR of 1.9%, adding USD 1.77 Billion in incremental annual market value. This steady growth reflects essential consumer goods demand characteristics combined with broadening premium adoption.

Three forces will shape the market through 2034. Personalized oral health supported by AI diagnostics and smart brush data analytics will drive premium product premiumization cycles. Sustainability requirements will accelerate recyclable and refillable packaging adoption across all major brands. E-commerce's continued share capture will restructure brand investment from in-store promotion to digital subscription and CRM platforms.

Research Methodology

Primary Research

Primary research encompassed structured interviews with US oral hygiene market stakeholders including senior brand managers at major CPG companies, retail category buyers at national pharmacy and grocery chains, dental hygienists, periodontists, and pediatric dentists. Primary data validated market sizing, segment shares, and channel growth trajectory estimates.

Secondary Research

Key secondary sources include CDC National Health and Nutrition Examination Survey oral health data, ADA Health Policy Institute consumer surveys, FDA OTC drug monograph publications, Nielsen/IRI US oral care scanner data reports, company annual reports, and trade publications including Drug Store News, Chain Store Age, and Progressive Grocer.

Forecasting Models

Market size estimations and growth projections were derived using bottom-up consumption models, top-down category growth rate analysis, Nielsen scanner data trend extrapolation, and macroeconomic overlays including US population growth, disposable income trends, and dental disease prevalence projections through 2034. Base, optimistic, and conservative scenarios were modeled.

United States Oral Hygiene Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Toothpaste, Toothbrushes & Accessories, Mouthwash/Rinses, Dental Accessories/Ancillaries, Denture Products, Dental Prosthesis Cleaning Solutions, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Pharmacies, Online Stores, Others |

| Applications Covered | Adults, Kids, Infants |

| Region Covered | Northeast, Midwest, South, West |

| Companies Covered | Colgate-Palmolive Company, Procter & Gamble, Haleon Group of Companies, Church & Dwight Co., Inc., Koninklijke Philips N.V., Sunstar Suisse S.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Oral Hygiene Market Report

The United States oral hygiene market reached USD 9.48 Billion in 2025, reflecting consistent demand from high dental disease prevalence, growing health awareness, and premium oral care product adoption across all US demographics.

The market is projected to reach USD 11.25 Billion by 2034, growing at a CAGR of 1.9% during 2026-2034, driven by e-commerce expansion, smart device adoption, and therapeutic and cosmetic oral care premiumization.

Supermarkets and hypermarkets lead with 39.2% channel share in 2025, valued for one-stop household shopping convenience, broad brand assortment, and competitive pricing for everyday oral care replenishment.

Online stores are the fastest-growing channel at ~5.8% CAGR through 2034, driven by DTC subscription replenishment models, Amazon's expanding oral care category, and digital-native consumer adoption of e-commerce purchasing.

Adults dominate with 68.5% of application share in 2025, representing the largest purchasing demographic with the broadest product range usage across basic and premium oral care categories.

The Kids segment at ~2.8% CAGR and Infants at ~2.4% CAGR are growing faster than Adults, driven by early childhood oral health awareness and expanding age-appropriate product ranges from Colgate, P&G, and specialized kid’s brands.

The South commands a 30.8% regional share in 2025, reflecting high population concentration across Texas, Florida, and the Southeast, above-average dental disease prevalence, and strong supermarket and pharmacy retail infrastructure.

Leading companies include Colgate-Palmolive Company, Procter & Gamble, Haleon Group of Companies, Church & Dwight Co., Inc., Koninklijke Philips N.V., Sunstar Suisse S.A., and others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)