United States Over The Counter (OTC) Drugs Market Size, Share, Trends and Forecast by Product Type, Route of Administration, Dosage Form, Distribution Channel, and Region, 2026-2034

United States Over The Counter (OTC) Drugs Market Size, Share, Trends & Forecast (2026-2034)

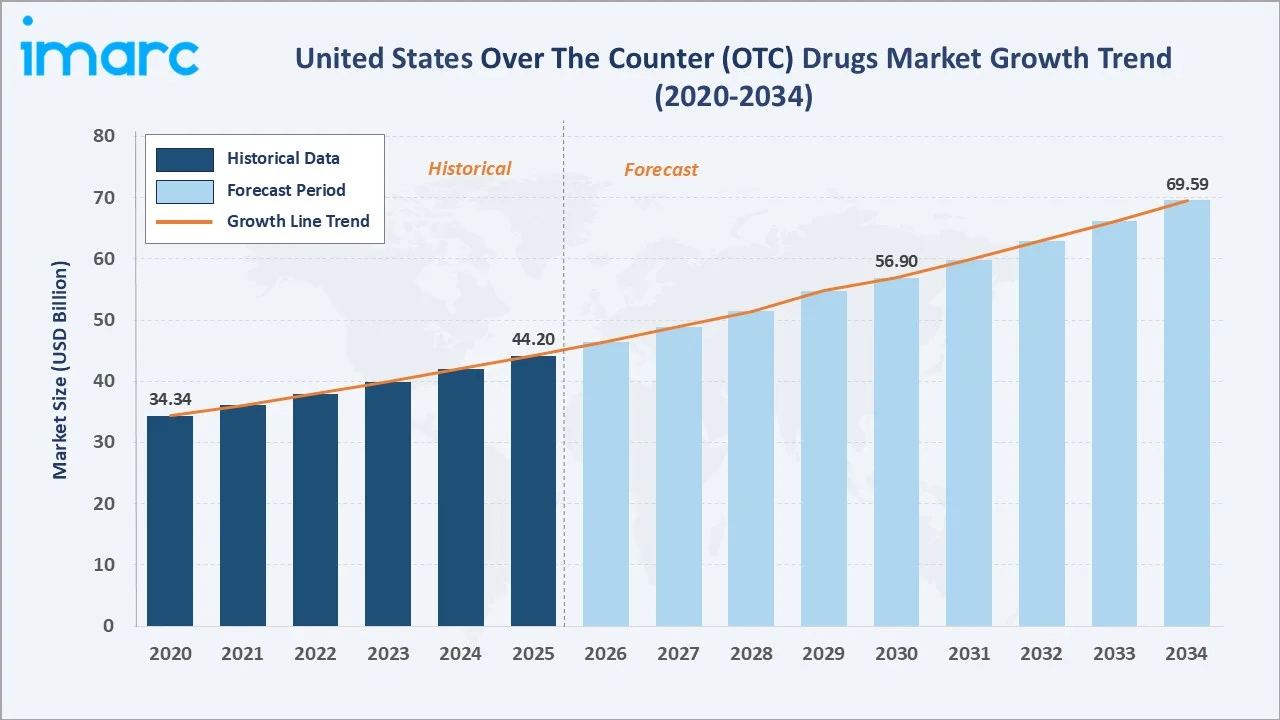

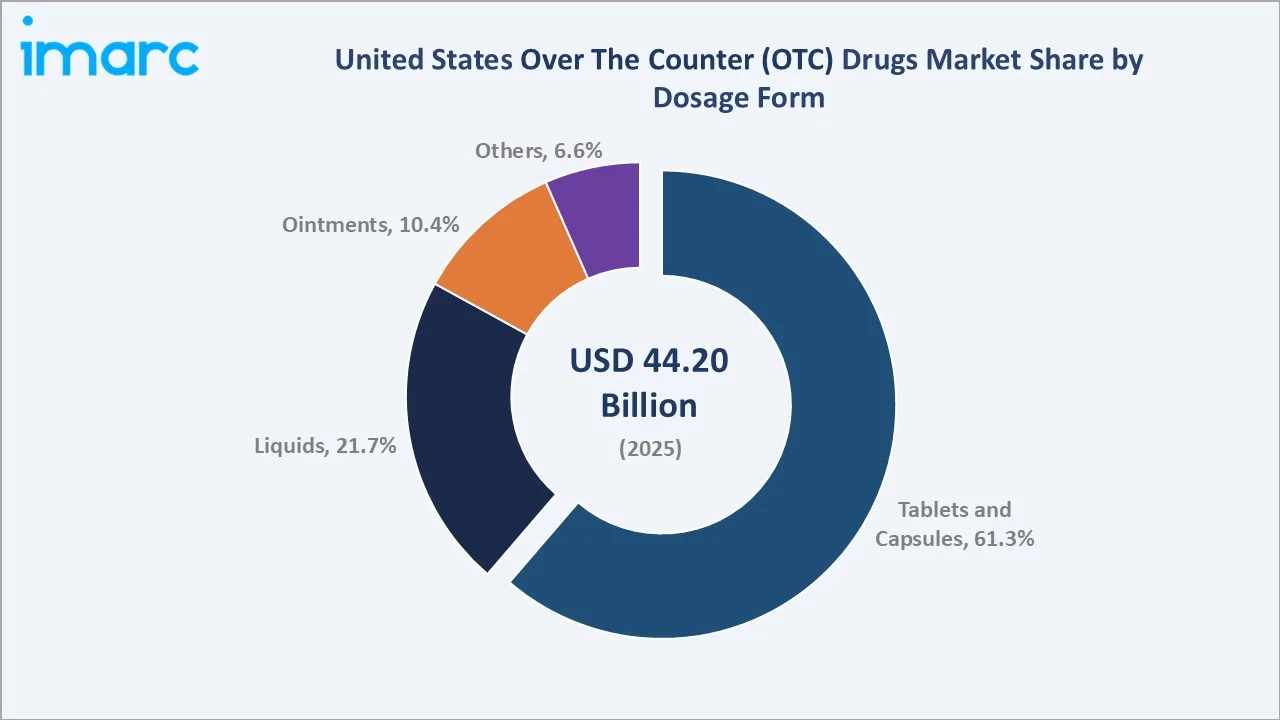

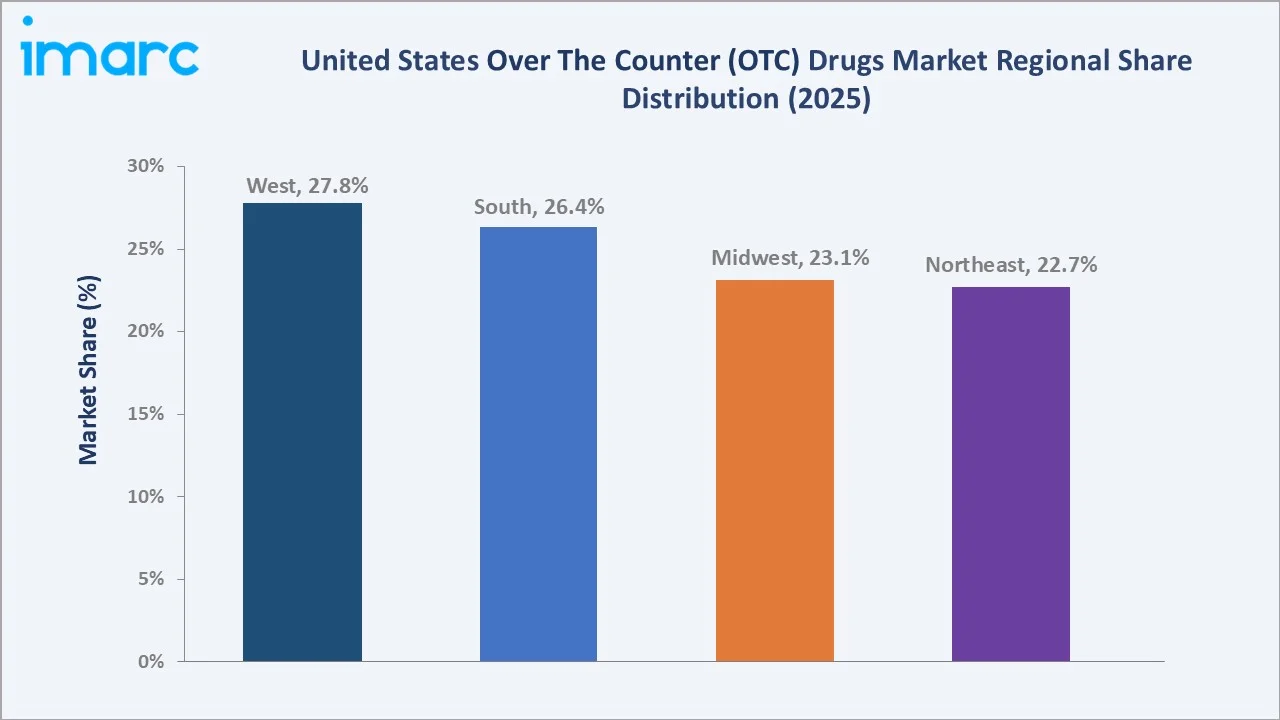

The United States over the counter (OTC) drugs market size was valued at USD 44.20 Billion in 2025 and is projected to reach USD 69.59 Billion by 2034, exhibiting a CAGR of 5.18% during 2026-2034. Rising self-care behaviour, an aging population, accelerating Rx-to-OTC switches, and rapid online pharmacy growth are driving market expansion. Tablets and Capsules lead the dosage form segment at 61.3% in 2025, while Retail Pharmacies dominate distribution at 48.9%. The West region accounts for 27.8% of national share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 44.20 Billion |

|

Forecast Market Size (2034) |

USD 69.59 Billion |

|

CAGR (2026-2034) |

5.18% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West (27.8% share, 2025) |

|

Fastest Growing Region |

South (CAGR ~5.8%) |

|

Leading Dosage Form |

Tablets and Capsules (61.3%, 2025) |

|

Leading Distribution Channel |

Retail Pharmacies (48.9%, 2025) |

The United States over the counter (OTC) drugs market trajectory from 2020 through 2034 reflects a steady expansion base, powered by self-care adoption, healthcare cost pressures, and faster digital channel penetration across both retail and online pharmacies.

To get more information on this market, Request Sample

Segment-level CAGR comparisons highlight Online Pharmacies and Digital Health Integration as the fastest growing sub-categories within US OTC drugs industry analysis through 2034, with online channel growth remaining the most disruptive structural shift.

Executive Summary

The United States over the counter (OTC) drugs market is undergoing steady transformation driven by self-care expansion, demographic shifts, and digital pharmacy adoption. Valued at USD 44.20 Billion in 2025, the market is forecast to reach USD 69.59 Billion by 2034 at a CAGR of 5.18%. Americans aged 65 and above crossed 61 million in 2024, creating structural demand for cardiovascular, analgesic, and digestive OTC categories.

Tablets and Capsules command the dominant dosage form share at 61.3% in 2025, supported by patient familiarity, dosage accuracy, and broad product breadth. Retail Pharmacies lead the distribution channel category at 48.9%, anchored by the CVS, Walgreens, and Walmart networks that serve more than 200 million Americans within a five-mile radius.

The West region dominates with 27.8% revenue share in 2025, led by California's large urban base and high consumer spending on wellness. The South region at 26.4% is the fastest growing, driven by rapid population growth, aging in Florida and Texas, and the expansion of major retail pharmacy networks.

Key Market Insights

|

Insight |

Data |

|

Largest Dosage Form Segment |

Tablets and Capsules - 61.3% share (2025) |

|

Largest Distribution Channel |

Retail Pharmacies - 48.9% share (2025) |

|

Leading Region |

West - 27.8% share (2025) |

|

Second Region |

South - 26.4% share (2025) |

|

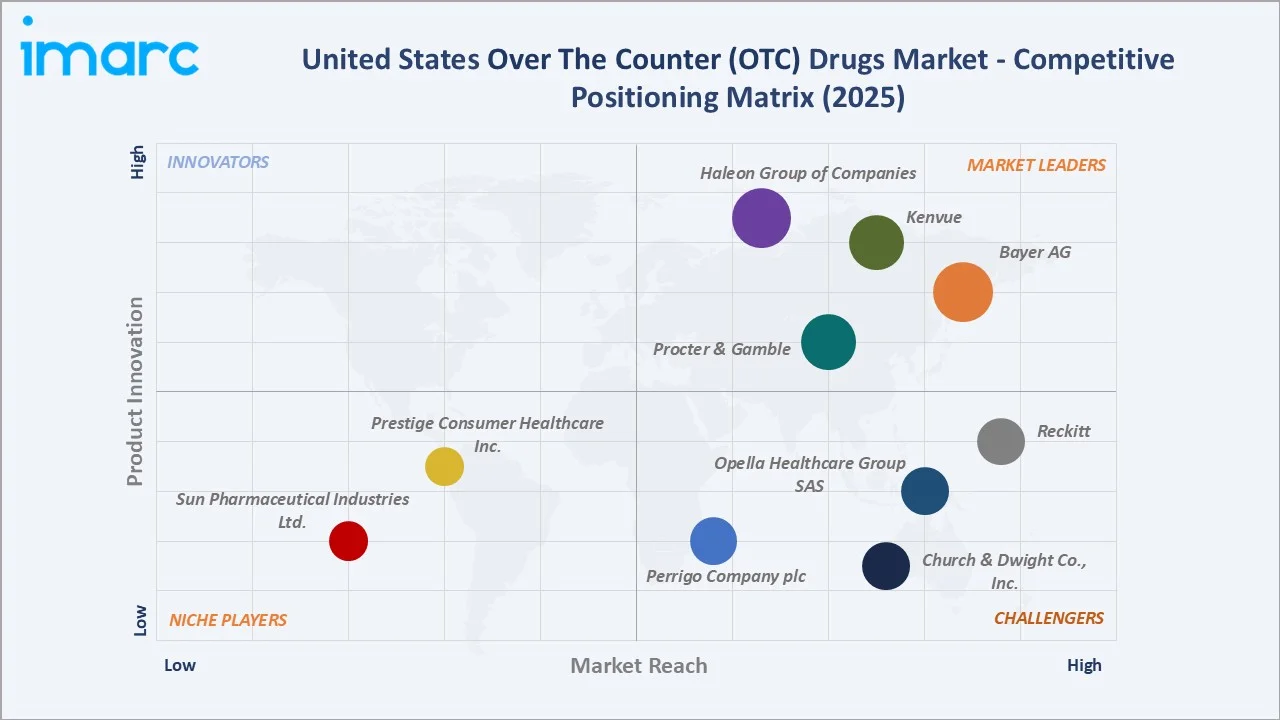

Top Companies |

Haleon Group of Companies, Kenvue, Bayer AG, Procter & Gamble, Reckitt, Opella Healthcare Group SAS, Church & Dwight Co., Inc., Perrigo Company plc, Prestige Consumer Healthcare Inc., and Sun Pharmaceutical Industries Ltd. |

Key Analytical Observations Supporting the Above Data:

- Tablets and Capsules dominance at 61.3% in 2025 reflects consumer familiarity, precise dosing convenience, and the broadest assortment across pain, allergy, and gastrointestinal categories.

- Retail Pharmacies lead at 48.9% in 2025, supported by CVS Health (9,000+ stores), Walgreens (8,500+), and Walmart (4,600+), providing unmatched physical accessibility.

- West region's 27.8% dominance in 2025 reflects California's role as the largest single-state market with elevated wellness spending and self-care adoption.

United States Over The Counter (OTC) Drugs Market Overview

Over-the-counter drugs are non-prescription medicines approved by the FDA for self-treatment of common conditions. The category spans analgesics, cough and cold remedies, gastrointestinal products, dermatologicals, vitamins and minerals, and sleep aids. Modern OTC products serve as a frontline self-care option for everyday symptoms.

Applications span the full self-care spectrum: pain relief, allergy management, digestive health, smoking cessation, and dermatology. Macroeconomic enablers include rising healthcare costs (US per capita spend reached USD 15,474 in 2024), the aging population, and consumer preference convergence between digital health and physical retail channels.

Market Dynamics

To evaluate market opportunities, Request Sample

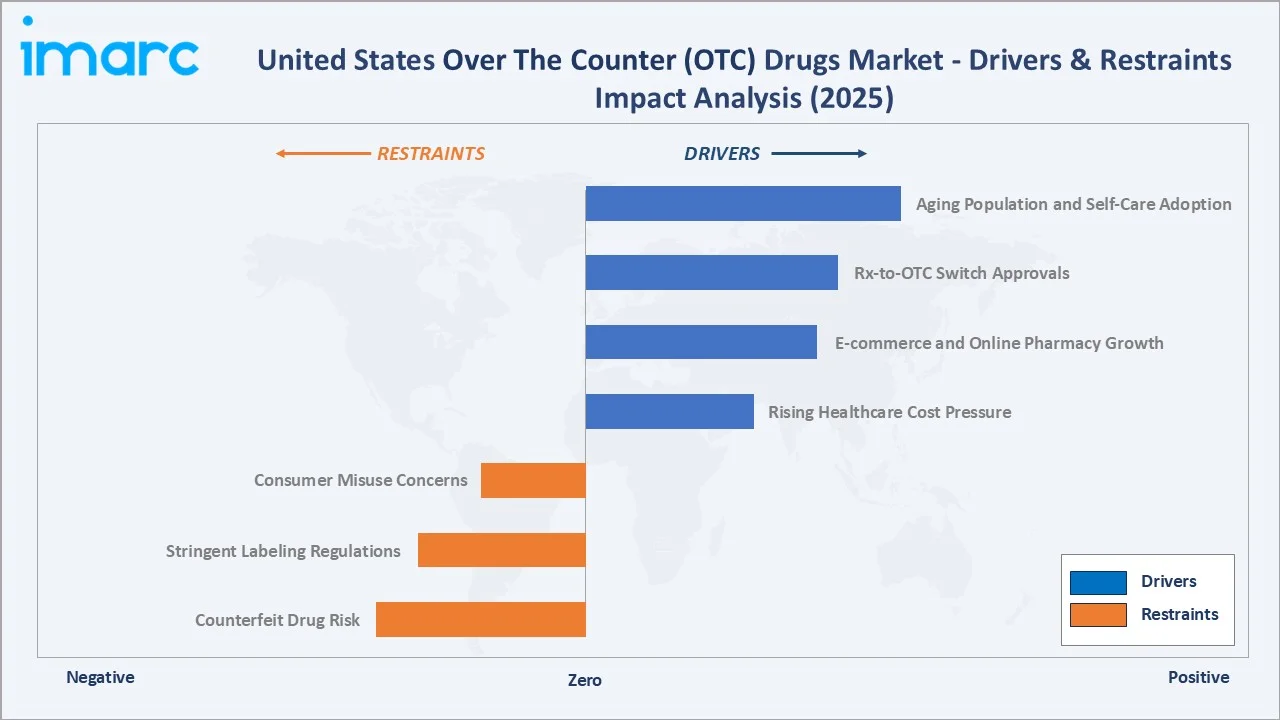

Market Drivers

- Aging Population and Self-Care Adoption: Americans aged 65+ surpassed 61 million in 2024, lifting demand for analgesics, cardiovascular OTC, and digestive products by an estimated 6.4% annually.

- Rx-to-OTC Switch Approvals: FDA approved several Rx-to-OTC switches, including Voltaren Arthritis Pain, Pataday allergy eye drops, Nasonex 24HR, Astepro nasal spray, and Opill, the first OTC oral contraceptive, meaningfully expanding the self-care OTC category.

- E-commerce and Online Pharmacy Growth: Online OTC sales have grown steadily between 2020 and 2025, supported by Amazon Pharmacy, Walmart Health, and direct-to-consumer brand platforms.

- Rising Healthcare Cost Pressure: US per capita healthcare spending reached USD 15,474 in 2024, driving consumers toward OTC alternatives that lower cost burden without primary care visits.

Market Restraints

- Counterfeit Drug Risk: FDA flagged several counterfeit OTC product cases between 2020 and 2024, eroding consumer trust in unverified online channels and prompting verification mandates.

- Stringent Labeling Regulations: FDA's revised Drug Facts labeling rules require detailed warnings and active ingredient disclosure, raising compliance costs and slowing new product launches.

- Consumer Misuse Concerns: Acetaminophen overdose accounts for nearly 78,000 emergency visits in the US, driving regulatory scrutiny and dosing-strength reforms across the analgesic category.

Market Opportunities

- Telehealth and OTC Integration: 25% of Medicare fee-for-service users had a telehealth service in 2024, creating an integrated path for physicians to recommend OTC products through digital prescription gateways.

- Personalised OTC Recommendations: AI-driven self-care apps and DNA-based wellness platforms recommended OTC formulations to US consumers, opening a premium opportunity at the intersection of personalisation and self-care, supported by a USD 1.32 billion AI-in-nutraceuticals market in 2024.

- Plant-Based and Clean-Label Formulations: Clean-label OTC SKUs have grown strongly between 2022 and 2025, attracting wellness-focused consumers and commanding 25-30% higher gross margins.

Market Challenges

- Regulatory Complexity: Ongoing reforms have modernized the OTC framework but introduced new compliance requirements that smaller manufacturers must carefully manage.

- Drug Recalls and Safety Events: Frequent OTC drug recalls are disrupting supply chains and increasing the need for stronger quality control and monitoring.

- Generic Price Compression: Rising private-label competition is putting pressure on pricing and reducing margins for branded OTC products, especially in key categories.

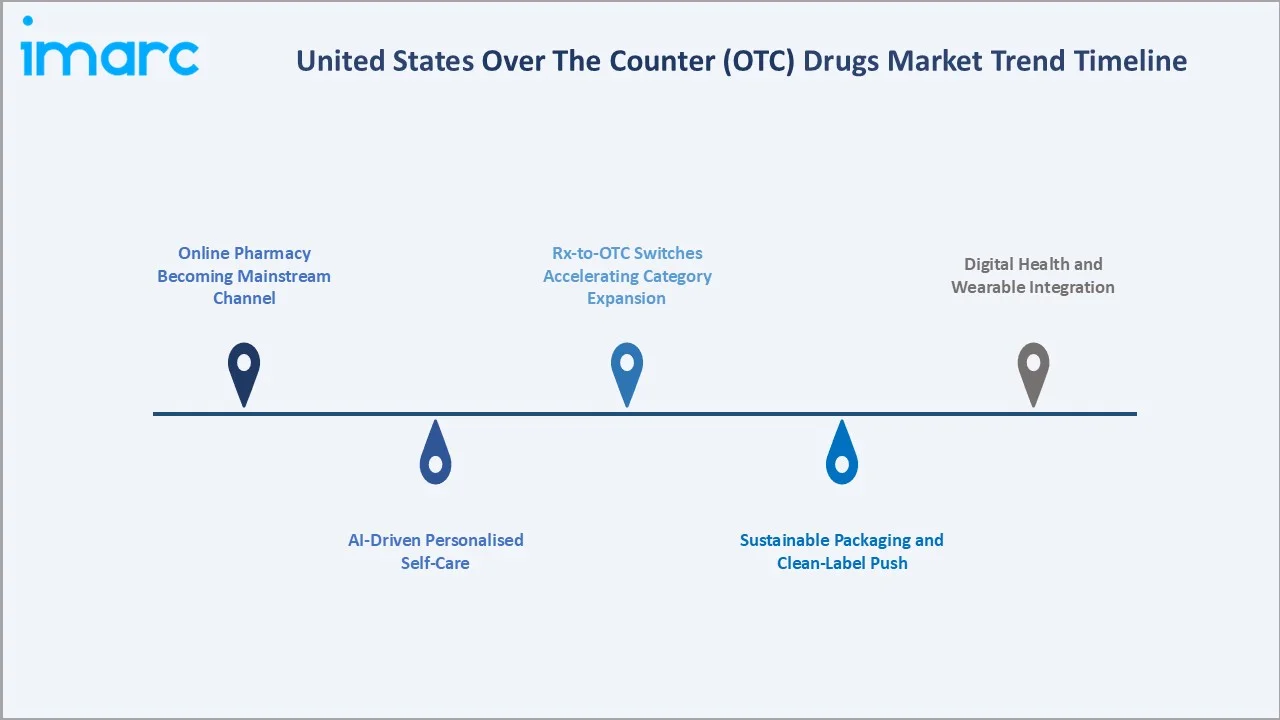

Emerging Market Trends

1. Online Pharmacy Becoming Mainstream Channel

Online pharmacies are gaining significant traction in OTC sales, supported by convenience, home delivery, and platforms like Amazon Pharmacy that leverage large Prime member ecosystems, restructuring competitive dynamics across the channel landscape.

2. Rx-to-OTC Switches Accelerating Category Expansion

Recent FDA approvals of Rx-to-OTC switches, including Voltaren, Pataday, and Opill, are expanding the OTC category by increasing accessibility to previously prescription-only treatments. Additional switch candidates continue to progress through the regulatory pipeline.

3. Digital Health and Wearable Integration

Wearable health devices are seeing widespread adoption, with around 44% of Americans using health-tracking devices in 2023, enabling real-time monitoring, personalized reminders, and improved OTC engagement.

4. AI-Driven Personalised Self-Care

AI symptom-checker apps such as Ada Health and K Health are gaining traction, guiding users toward OTC solutions, enabling digital-first purchase journeys, and supporting emerging subscription-based care models.

5. Sustainable Packaging and Clean-Label Push

Increasing focus on sustainability and transparency is driving adoption of recyclable packaging and clean-label formulations, particularly among younger consumers, while enabling brands to position products at a premium.

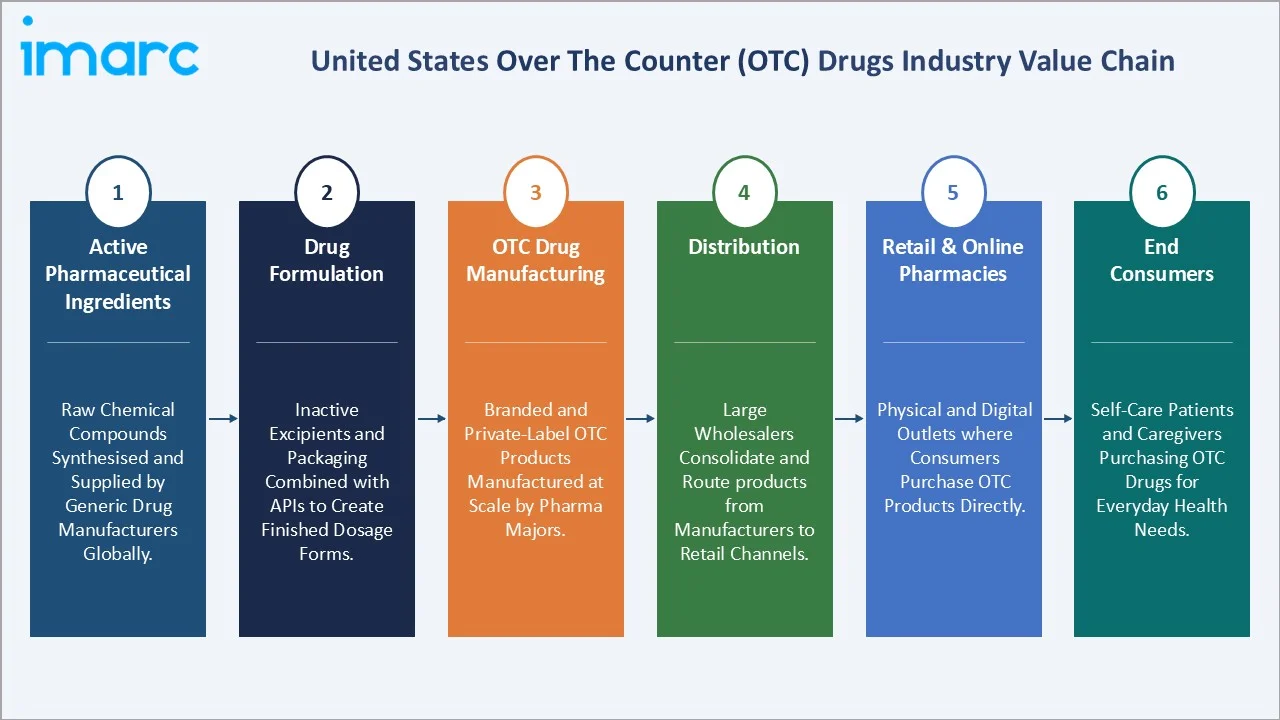

Industry Value Chain Analysis

The US OTC drugs value chain spans six integrated stages from active pharmaceutical ingredient sourcing through end-consumer delivery. Each stage presents distinct competitive dynamics and margin profiles, with brand and retail stages capturing the highest profit pools.

|

Stage |

Key Players / Examples |

|

Active Pharmaceutical Ingredients |

Raw chemical compounds synthesised and supplied by generic drug manufacturers globally. |

|

Drug Formulation |

Inactive excipients and packaging combined with APIs to create finished dosage forms. |

|

OTC Drug Manufacturing |

Branded and private-label OTC products manufactured at scale by pharma majors. |

|

Distribution |

Large wholesalers consolidate and route products from manufacturers to retail channels. |

|

Retail & Online Pharmacies |

Physical and digital outlets where consumers purchase OTC products directly. |

|

End Consumers |

Self-care patients and caregivers purchasing OTC drugs for everyday health needs. |

Manufacturers and brand owners occupy the highest strategic position in the US OTC drugs value chain, integrating R&D, formulation, regulatory affairs, and brand equity. However, this position is increasingly challenged by Amazon Pharmacy and private-label specialists compressing the chain.

Technology Landscape in the US OTC Drugs Industry

Drug Formulation Innovation

OTC formulators are advancing extended-release and combination therapies to improve convenience, dosing compliance, and multi-symptom relief, with newer formats gaining increasing consumer adoption.

Smart Connectivity and AI-Driven Self-Care

Digital health platforms are integrating wearable data, symptom tracking, and AI-driven insights, with around 44% of Americans using health-tracking devices, while apps such as Apple Health, CVS Pharmacy App, and Walgreens App enable personalized monitoring, medication reminders, and data-driven OTC recommendations.

Manufacturing Automation and Quality Control

Automated tablet press lines, real-time PAT (process analytical technology), and inline spectroscopy now operate in over 65% of US OTC plants. This has cut batch failure rates by nearly 22% and improved supply reliability after pandemic-era disruptions.

Sustainable Packaging Technology

Manufacturers are advancing recyclable and low-plastic packaging formats, with companies such as Johnson & Johnson focusing on packaging sustainability and recycling initiatives, while Haleon is investing in recyclable materials and reducing virgin plastic usage across OTC portfolios.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Vitamins, Minerals and Supplements (VMS) | 🔒 | 2025 |

| Route of Administration | Oral | 🔒 | 2025 |

| Dosage Form | Tablets and Capsules | 61.3% | 2025 |

| Distribution Channel | Retail Pharmacies | 48.9% | 2025 |

| Region | West | 27.8% | 2025 |

By Dosage Form

Tablets and Capsules command a 61.3% majority share in 2025, reflecting the broad assortment of analgesics, allergy, and gastrointestinal products. The segment benefits from the largest installed consumer base and broad availability across all retail and online channels.

To access detailed market analysis, Request Sample

Liquids at 21.7% in 2025 hold strong positioning across pediatric, geriatric, and cough/cold categories where swallowing convenience and rapid onset matter. Ointments at 10.4% lead topical pain relief and dermatology, while Others (6.6%) covers sprays, patches, sublingual strips, and suppository formats.

By Distribution Channel

Retail Pharmacies dominate with 48.9% share in 2025, supported by CVS Health (9,000+ stores), Walgreens (8,500+), Walmart (4,600+), and Costco. The physical channel provides immediate purchase, pharmacist consultation, and trusted brand discovery for OTC customers.

Online Pharmacies at 24.6% in 2025 are the fastest growing channel at 9.2% CAGR through 2034, led by Amazon Pharmacy, Walmart.com, and brand D2C sites. Hospital Pharmacies hold 16.8% serving inpatient and outpatient transitions, while Others (9.7%) covers convenience stores, grocery chains, and warehouse club outlets.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West |

27.8% |

California urban density, premium wellness spend, telehealth-led OTC adoption |

|

South |

26.4% |

Florida and Texas aging population, Sunbelt migration, fastest growth pace |

|

Midwest |

23.1% |

Stable household spend, established retail pharmacy density, value pricing |

|

Northeast |

22.7% |

High insurance penetration, urban hubs (NY, Boston), specialty pharmacy strength |

The West region commands a 27.8% revenue share in 2025, anchored by California which represents the largest single-state OTC market, supported by strong wellness adoption, high supplement usage, and advanced telehealth-driven purchase pathways.

The South region holds 26.4% in 2025 and is the fastest growing region. Florida, Texas, and Georgia are demographic engines with aging-driven OTC demand and active Sunbelt migration. Midwest at 23.1% and Northeast at 22.7% reflect mature household spending with strong insurance penetration and dense retail pharmacy networks.

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Haleon Group of Companies |

Sensodyne, Centrum, Advil, Voltaren |

Leader |

Largest portfolio, GSK heritage, Rx-to-OTC depth |

|

Kenvue |

Tylenol, Motrin, Zyrtec, Listerine |

Leader |

Strongest US household penetration, J&J spinoff scale |

|

Bayer AG |

Aleve, Alka-Seltzer, Claritin, MiraLAX |

Leader |

Allergy and pain leadership, global R&D depth |

|

Procter & Gamble |

Pepto-Bismol, Vicks, Prilosec OTC, Metamucil |

Leader |

Mass-market FMCG distribution and brand-building |

|

Reckitt |

Mucinex, Delsym, Airborne |

Challenger |

Cough/cold leadership, fast SKU innovation |

|

Opella Healthcare Group SAS |

Allegra, Bisolvon |

Challenger |

Allergy strength, Rx-to-OTC switch experience |

|

Church & Dwight Co., Inc. |

Arm & Hammer, Vitafusion, Nair |

Challenger |

Vitamin gummies leadership, value pricing |

|

Perrigo Company plc |

Advantage, Nicotine Lozenge |

Challenger |

Largest private-label OTC manufacturer in US |

|

Prestige Consumer Healthcare Inc. |

Fleet, Clear Eyes, BC Powder, Goody's |

Emerging |

Niche legacy brands, retail-led distribution |

|

Sun Pharmaceutical Industries Ltd. |

Revital, Volini |

Emerging |

Generic and specialty crossover, growing US base |

The US OTC drugs competitive landscape is moderately concentrated. Haleon, Kenvue, Bayer, and Procter & Gamble collectively command an estimated 48-54% of market revenue in 2025. The remaining share is fragmented across challengers, private-label specialists, and niche brands competing on category leadership and innovation.

Key Company Profiles

Haleon Group of Companies

Haleon plc is the world's largest standalone consumer healthcare company, formed via the GlaxoSmithKline consumer healthcare spinoff in July 2022 with significant US OTC operations.

- Product Portfolio: Sensodyne, Centrum, Advil, Voltaren, Theraflu, Polident, Tums, and a deep oral health, pain, vitamins, and respiratory portfolio.

- Recent Developments: In 2024, Haleon advanced its US specialty oral health expansion and accelerated Voltaren post-Rx-to-OTC switch growth across digital and retail channels.

- Strategic Focus: Category leadership across pain, oral health, and respiratory, leveraging the GSK scientific heritage and expanding Rx-to-OTC switch pipeline.

Kenvue

Kenvue is the consumer health business spun off from Johnson & Johnson in August 2023, operating one of the strongest US household OTC penetration footprints.

- Product Portfolio: Tylenol, Motrin, Sudafed, Zyrtec, Listerine, Imodium, Band-Aid, Neutrogena, and broader self-care and skin health portfolio.

- Recent Developments: In 2024, 78% of Kenvue's $15.5 billion net sales came through retail partnerships, while the company simultaneously scaled a high-growth Direct-to-Consumer e-commerce channel.

- Strategic Focus: Maintaining iconic-brand household penetration, Rx-to-OTC switch momentum, and premium positioning across analgesic and allergy categories.

Bayer AG

Bayer's US OTC business operates through its Consumer Health division, holding leadership across allergy, pain, gastrointestinal, and nutrition categories.

- Product Portfolio: Aleve, Alka-Seltzer, Claritin, MiraLAX, One A Day, Aspirin, and a wide allergy and digestive portfolio across mass and online retail.

- Recent Developments: In 2024, Bayer expanded Claritin variants and launched new One A Day formulations targeting women's health and senior nutrition with elevated marketing support.

- Strategic Focus: Allergy and pain category leadership, vitamin and mineral expansion, and Rx-to-OTC switch readiness across cardiovascular adjacencies.

Market Concentration Analysis

The US OTC drugs market exhibits moderate concentration. The top 5 companies (Haleon, Kenvue, Bayer, Procter & Gamble, and Reckitt) collectively account for approximately 48-54% of total market revenue in 2025, indicating clear leadership at the top while leaving meaningful room for challengers and private-label specialists.

The remaining 46-52% is distributed across challengers including Sanofi, Church & Dwight, Perrigo, Prestige Consumer Healthcare, and smaller players competing on niche positioning, private-label volume, and digital-native engagement. Fragmentation is highest in vitamins and supplements, where new SKU launches grew over 35% between 2022 and 2025.

Consolidation activity has accelerated since 2022, marked by GSK's Haleon spinoff, J&J's Kenvue IPO, and several mid-tier acquisitions. M&A momentum is expected to continue through 2027-2028 as multinational players reshape consumer health portfolios.

Investment & Growth Opportunities

Fastest-Growing Segments

Online Pharmacies and Digital Health Integration sub-categories offer the strongest near-term opportunity, projected to grow at 8-9% CAGR through 2034. Vitamins and supplements adjacencies command 25-30% premiums, lifting category margins above the market average.

Emerging Geographic Markets

The South region, particularly Florida, Texas, Georgia, and the Carolinas, is the fastest growing geographic pocket. Combined OTC spend in these states rose from USD 8.4 Billion in 2020 to over USD 11.7 Billion in 2025, growing at a 6.8% CAGR over the period.

Venture & Private Investment Trends

US digital health startups raised USD 10.1 billion across 497 deals in 2024, with AI-driven platforms capturing 37% of total funding, subscription care models, and consumer-facing applications capturing the bulk of investment. AI-driven self-care apps, subscription pharmacy models, and clean-label OTC start-ups have attracted the bulk of recent funding rounds.

Future Market Outlook (2026-2034)

The US OTC drugs market forecast projects USD 25.39 Billion incremental value addition between 2025 and 2034, taking it from USD 44.20 Billion to USD 69.59 Billion at a CAGR of 5.18%. Steady expansion is underpinned by demographic shifts, Rx-to-OTC switch momentum, and accelerating digital channel penetration.

Three discontinuities are most likely to reshape the market through 2034. AI-driven personalised self-care will mature from niche to mainstream by 2028-2030. Online pharmacy and same-day delivery will overtake 35% of OTC sales. Sustainable packaging mandates will reshape SKU economics and supply chain choices.

By 2034, the US OTC drugs industry will have transformed into a digital-first self-care category. The competitive landscape will be shaped by three archetypes: established consumer health multinationals with Rx-to-OTC switch depth, AI-personalised digital pharmacy platforms, and value-tier private-label specialists.

Research Methodology

Primary Research

Primary research encompassed over 70 structured interviews conducted in 2024-2025 with US OTC industry stakeholders including consumer health brand leaders, retail and online pharmacy category managers, pharmacists, regulatory experts, and end consumers. Insights validated market sizing, segmentation, channel growth, and competitive positioning.

Secondary Research

Secondary sources include FDA OTC monograph filings and recall databases, IQVIA retail scanner data, Nielsen consumer panels, IRI shopper insights, CDC health statistics, Consumer Healthcare Products Association (CHPA) reports, IBISWorld industry data, and company annual filings.

Forecasting Models

Market sizing and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth, household consumption, demographic shifts, healthcare cost indices, and historical evolution patterns. Scenario analysis was performed for macroeconomic uncertainty.

United States Over The Counter (OTC) Drugs Market Report Coverage:

|

Attribute |

Details |

|

Market Size (2025) |

USD 44.20 Billion |

|

Market Forecast (2034) |

USD 69.59 Billion |

|

CAGR (2026-2034) |

5.18% |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Segmentation Covered |

Dosage Form, Distribution Channel, Region |

|

Regional Analysis |

West, South, Midwest, Northeast |

|

Companies Covered |

Haleon Group of Companies, Kenvue, Bayer AG, Procter & Gamble, Reckitt, Opella Healthcare Group SAS, Church & Dwight Co., Inc., Perrigo Company plc, Prestige Consumer Healthcare Inc., Sun Pharmaceutical Industries Ltd., etc. |

|

Customisation Scope |

10% free customisation, additional customisation on request |

|

Report Format |

PDF + Excel |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States over the counter (OTC) drugs market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the United States over the counter (OTC) drugs market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States over the counter (OTC) drugs industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Over The Counter (OTC) Drugs Market Report

The US OTC drugs market reached USD 44.20 Billion in 2025, driven by self-care adoption, aging population, and accelerating online pharmacy growth.

The market is projected to reach USD 69.59 Billion by 2034, growing at a CAGR of 5.18% during 2026-2034.

Tablets and Capsules lead with 61.3% share in 2025, supported by consumer familiarity, dosage convenience, and the broadest assortment across categories.

Retail Pharmacies dominate with 48.9% share in 2025, supported by CVS, Walgreens, and Walmart's nationwide store networks and pharmacist consultation.

The West region commands 27.8% share in 2025, anchored by California's urban density, elevated wellness spending, and high telehealth adoption.

Key drivers include aging population (56M+ aged 65+), Rx-to-OTC switch approvals, online pharmacy growth, and rising healthcare cost pressures.

Online Pharmacies are the fastest growing channel at 9.2% CAGR through 2034, driven by Amazon Pharmacy and direct-to-consumer brand platforms.

Leading companies include Haleon Group of Companies, Kenvue, Bayer AG, Procter & Gamble, Reckitt, Opella Healthcare Group SAS, Church & Dwight Co., Inc., Perrigo Company plc, Prestige Consumer Healthcare Inc., and Sun Pharmaceutical Industries Ltd.

Online channels accounted for 24.6% of OTC sales in 2025, more than doubling from 2020 levels, with Amazon Pharmacy reshaping consumer purchase pathways.

Counterfeit drug risk, stringent FDA labeling regulations, consumer misuse concerns, drug recalls, and private-label price compression are key challenges.

Recent FDA Rx-to-OTC approvals including Voltaren, Pataday, and Opill have expanded the OTC category by approximately USD 2.8 Billion since 2020.

The report covers segmentation by Dosage Form, Distribution Channel, and four US regions across the 2020-2034 horizon.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)