United States Running Gear Market Size, Share, Trends and Forecast by Product, Gender, Distribution Channel, and Region, 2026-2034

United States Running Gear Market Size, Share, Trends & Forecast (2026-2034)

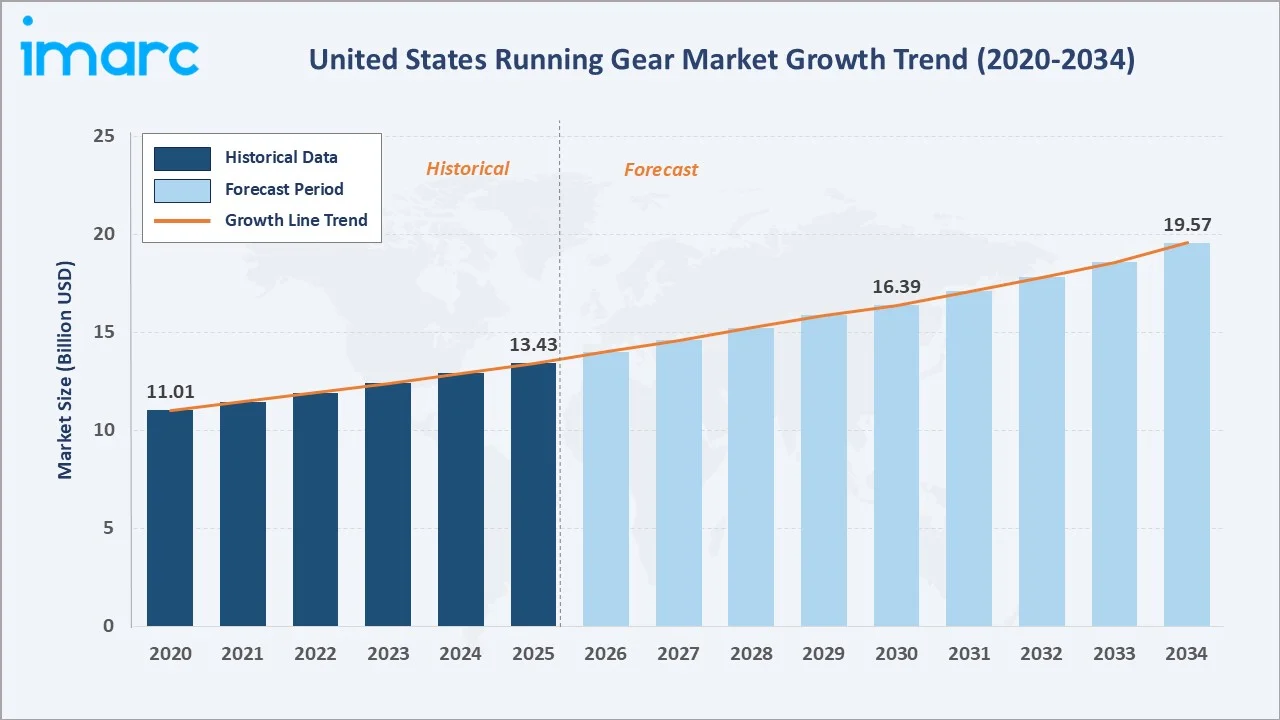

The United States running gear market reached USD 13.43 Billion in 2025 and is projected to reach USD 19.57 Billion by 2034, growing at a CAGR of 4.06% during 2026-2034. Rising health and fitness awareness, sustained growth in road race and marathon participation, rapid e-commerce channel expansion enabling direct-to-consumer brand sales, and the integration of technology into running footwear, apparel, and accessories are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 13.43 Billion |

|

Forecast Market Size (2034) |

USD 19.57 Billion |

|

CAGR (2026-2034) |

4.06% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

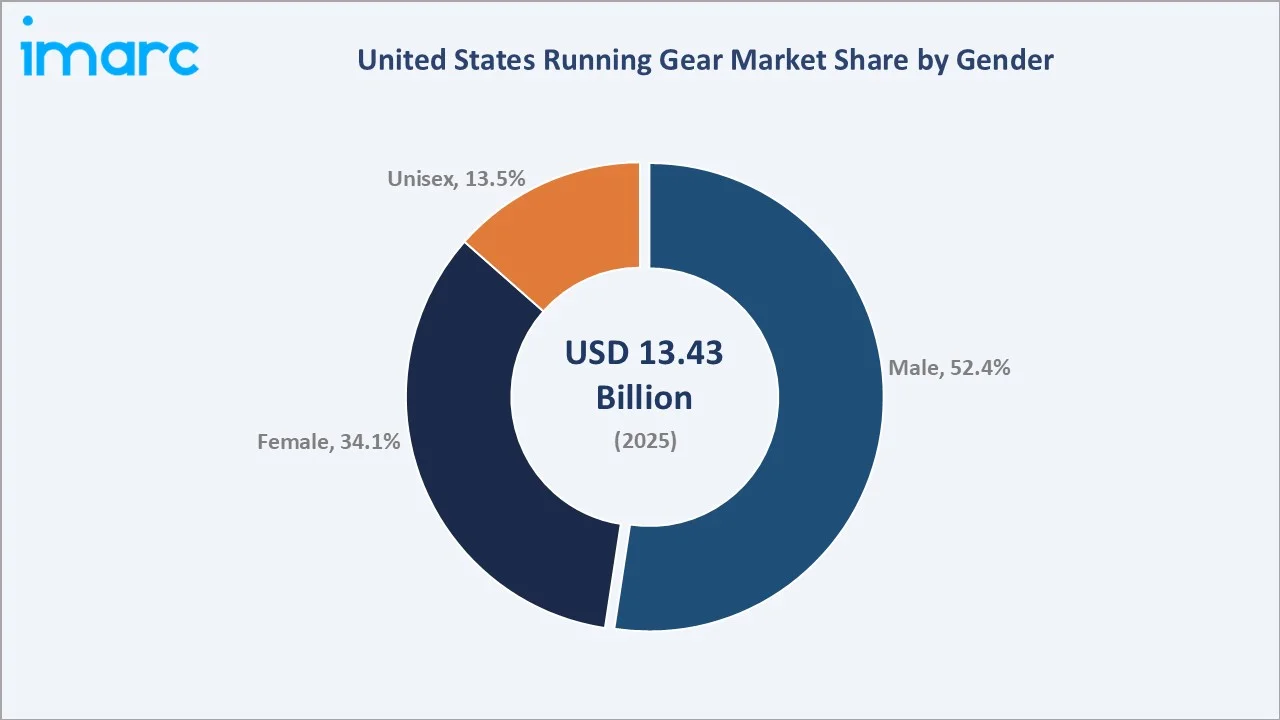

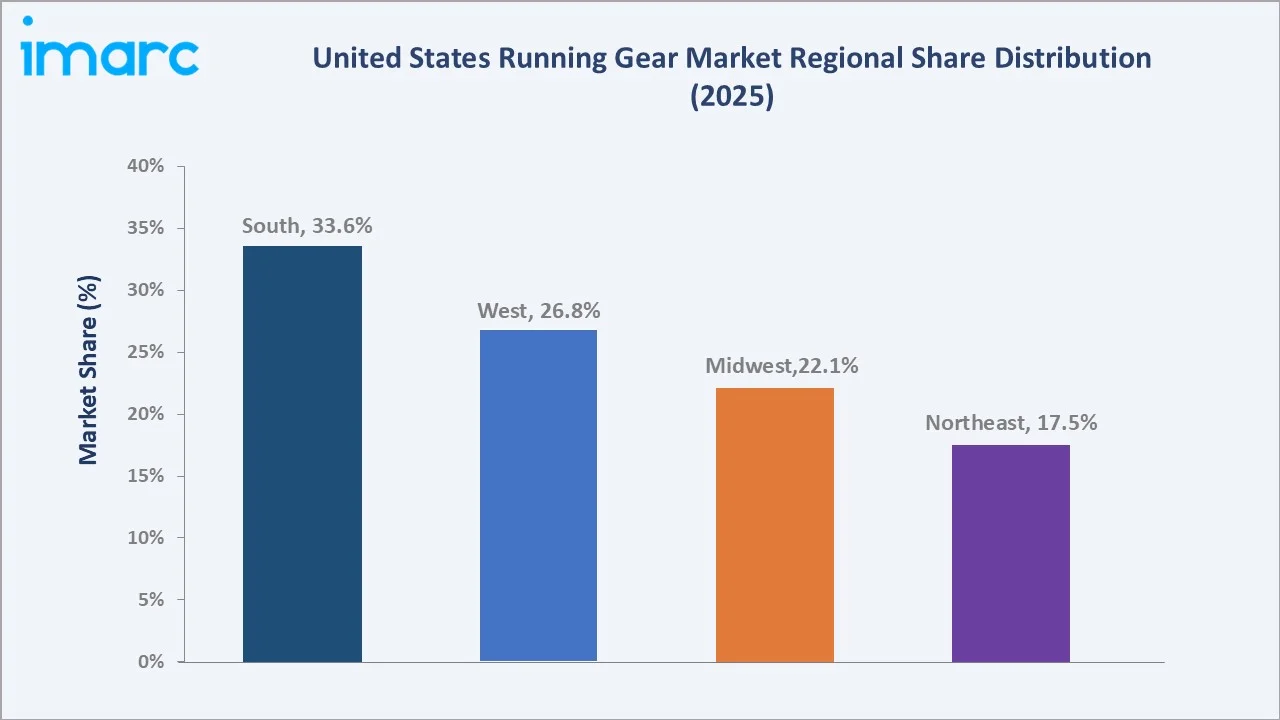

The South leads regionally with a 33.6% market share in 2025, driven by the region’s large population base, year-round mild climate enabling outdoor running, high road race participation density, and a large specialty sports retail footprint across Texas, Florida, Georgia, and North Carolina. The male segment commands a 52.4% gender share, reflecting their historically higher participation in competitive running events and higher average spend per running gear purchase.

To get more information on this market, Request Sample

The US running gear market is driven by three structural demand forces: the post-COVID health and fitness megatrend that has sustainably elevated participation in running as a primary physical activity across all demographic segments; the progressive technology integration of running gear creating premium product categories including carbon fiber plate racing shoes, GPS-enabled smart watches, and biometric tracking apparel that drive revenue growth above volume growth; and the e-commerce channel’s ongoing share gains enabling brands to develop direct-to-consumer relationships and capture the full margin on premium product sales.

Executive Summary

The United States running gear market is experiencing sustained growth, driven by the convergence of rising participation in recreational and competitive running, ongoing innovation in performance running technology, and the structural shift toward health and wellness spending that accelerated through the COVID-19 pandemic and has been sustained by demographic trends, including the continued fitness consciousness of Millennial and Generation Z consumers. The market was valued at USD 13.43 Billion in 2025 and is forecast to reach USD 19.57 Billion by 2034, growing at a CAGR of 4.06%.

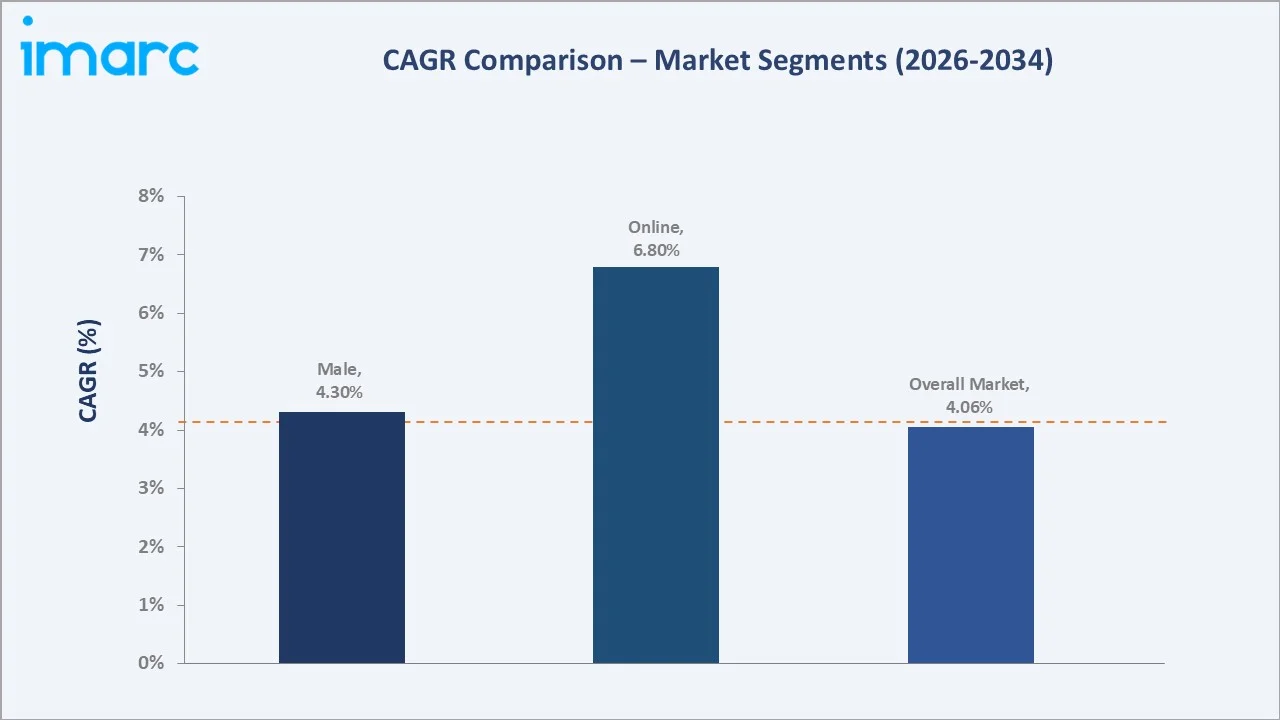

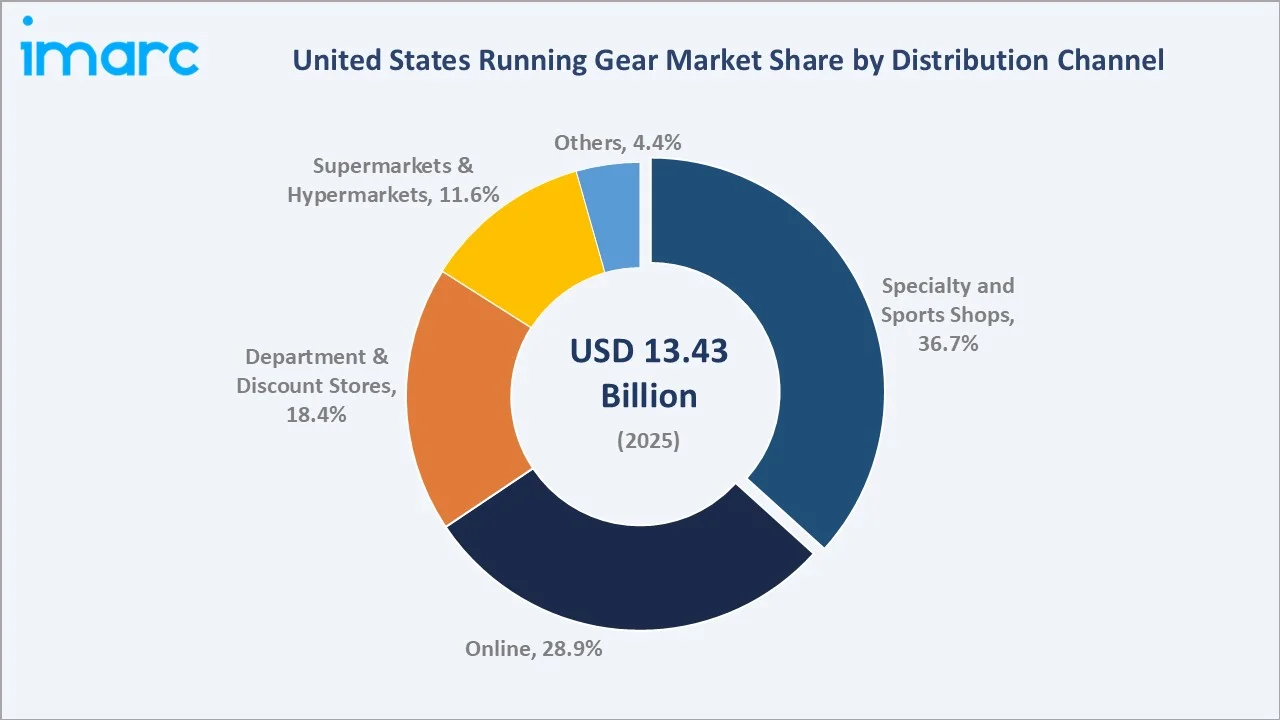

Male consumers account for 52.4% of the gender segment in 2025, reflecting historically higher participation rates in competitive running events and higher average transaction values in performance footwear categories. Specialty and sports shops at 36.7% lead the distribution channel segment, anchored by the irreplaceable role of expert staff, gait analysis, and try-on experience in performance running footwear purchase decisions, while online at 28.9% is the fastest-growing channel.

The South leads regionally at 33.6%, driven by its large population, year-round outdoor running conditions, and strong road race culture. Key players compete across innovation, brand positioning, channel strategy, and technology integration.

Key Market Insights

|

Insight |

Data |

|

Largest Gender |

Male – 52.4% share (2025) |

|

Second Largest Gender |

Female – 34.1% share (2025) |

|

Largest Distribution Channel |

Specialty and Sports Shops – 36.7% share (2025) |

|

Fastest Growing Distribution Channel |

Online – ~6.8% CAGR (2026-2034) |

|

Leading Region |

South – 33.6% share (2025) |

|

Top Companies |

Nike, Inc., adidas AG, New Balance, ASICS Corporation, and Under Armour, Inc. |

Key Analytical Observations Supporting the Above Data:

- Male at 52.4% (2025) leads the gender segment due to historically higher competitive running participation rates and higher average spending per transaction on performance footwear and GPS tracking devices. Male-targeted categories, including racing shoes, GPS running watches, and technical performance apparel, generate higher revenue per unit than women’s equivalents in the mid-performance tier, sustaining the segment’s revenue leadership despite smaller participation growth rates.

- Specialty and sports shops at 36.7% (2025) maintain their dominant position as the purchase decision for performance running footwear, particularly stability and motion control shoes requiring gait analysis, cannot be adequately served by non-expert retail formats. Running specialty retailers provide the biomechanical assessment, fit consultation, and trial experience that justify premium price points and reduce return rates.

- Online at 28.9% share (2025) is projected to grow fastest at approximately 6.8% CAGR through 2034. Nike’s direct digital revenue share, Brooks’ DTC online growth, and the proliferation of premium running e-tailers are collectively driving online channel share gains. Subscription boxes, augmented reality fitting tools, and AI-powered shoe recommendation engines are reducing online footwear purchase hesitation.

- The South’s 33.6% share (2025) reflects the region’s combination of the largest US population by region, year-round mild climate enabling outdoor running throughout all twelve months, and a strong road race culture anchored by the Houston, Atlanta, New Orleans, and Miami marathon markets.

United States Running Gear Market Overview

Running gear encompasses the full range of products worn, carried, or used by runners during training and racing activities, including running footwear (road shoes, trail shoes, track spikes, racing flats, and stability shoes), running apparel (shorts, tights, singlets, jackets, and base layers), and running accessories (GPS watches, hydration vests, belts, socks, compression sleeves, headlamps, and sunglasses).

Macroeconomic drivers include RunSignup’s RaceTrends report, which showed race participation increased by an average of 8% in 2024 compared with the previous year, the US fitness industry sustaining above-GDP revenue growth, and the athleisure trend sustaining double-digit growth in performance-positioned apparel purchases for non-athletic daily use. The premium running shoe segment is growing at above-market rates as the success of HOKA, On Running, and Salomon in the US market demonstrates the addressable market for premium performance footwear beyond the established Nike and adidas mainstream price points.

Market Dynamics

To evaluate market opportunities, Request Sample

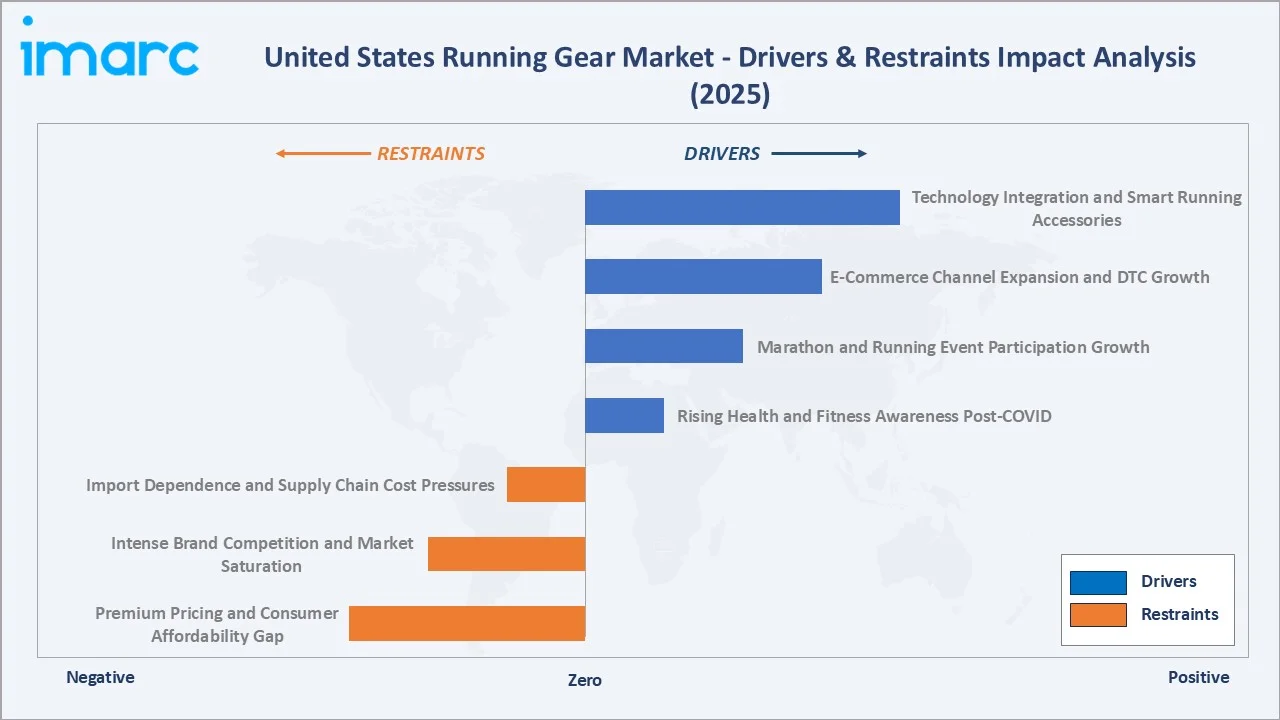

Market Drivers

- Rising Health and Fitness Awareness Post-COVID: The COVID-19 pandemic created a structural step-change in US health and fitness awareness and participation that has proven durable beyond the pandemic period. Running’s unique combination of zero gym fee requirement, social distance-compatible practice, and measurable performance progression resonated strongly with the pandemic-era fitness consumer.

- Marathon and Running Event Participation Growth: The Six Star World Marathon Majors generates hundreds of thousands of race finishers annually, whose participation drives premium gear purchases, including carbon fiber plate racing shoes, GPS performance watches, and technical race-day apparel. The growth of virtual racing events, trail running events, and obstacle course races is expanding the gear requirement ecosystem beyond traditional road running equipment.

- E-Commerce Channel Expansion and DTC Growth: Nike’s digital sales, Brooks’ sustained DTC channel investment, and the proliferation of specialist running e-tailers are accelerating the digital channel’s share of running gear sales. DTC channels enable brands to maintain full retail margin on premium products, invest in personalization technology, and build direct loyalty relationships with runners.

- Technology Integration and Smart Running Accessories: Carbon fiber plate midsole has democratized to sub-USD-200 price points across multiple brands, creating mass-market demand for technology-differentiated running footwear. GPS running watches, smart running insoles, biomechanical analysis apps, and biometric compression garments are collectively expanding the running accessories market at above-market growth rates.

Market Restraints

- Premium Pricing and Consumer Affordability Gap: The running gear market’s premiumization trend has created a widening price gap between entry-level and performance running gear, with top-tier running shoes at USD 250–350 and GPS watches at USD 300–600 representing significant discretionary spend. Inflation-driven consumer affordability pressure is creating resistance to premium price points in the mass market segment, limiting premium gear’s addressable market to higher-income consumer segments.

- Intense Brand Competition and Market Saturation: The US running footwear market’s attractiveness has drawn a large number of premium brands, creating intense competition for shelf space and consumer attention. This competitive density is driving marketing cost escalation and compressing brand margins, with smaller brands facing particular challenges in competing for specialty retail floor space against established category leaders.

- Import Dependence and Supply Chain Cost Pressures: The US running gear market is predominantly supplied by imports manufactured in Vietnam, Indonesia, and China, creating exposure to trade tariff risk, ocean freight cost volatility, and supply chain lead time uncertainty. The Trump administration’s tariff announcements on Southeast Asian manufactured goods in 2025 created significant cost uncertainty for running shoe brands dependent on Vietnamese manufacturing.

Market Opportunities

- Women’s Running Category Growth: Women’s running participation is growing at above-market rates, with women accounting for 45–50% of marathon finishers in the country. Brands that invest in women-specific biomechanical research, femtech-integrated performance tracking, and female community building through running groups and events are positioned to capture above-average revenue growth as the women’s running market approaches parity with the male segment in total revenue by 2034.

- Trail Running and Adventure Race Market Expansion: The trail running market is growing at above-road-running rates in the US, driven by the increased interest in nature-based outdoor recreation that accelerated during the COVID-19 pandemic. Trail-specific running shoes, trail hydration vests, trekking poles, and trail navigation accessories represent a growing premium product category with higher average selling prices than road running equivalents.

Market Challenges

- Counterfeit Product Infiltration in Online Channels: The growth of e-commerce in running gear has increased exposure to counterfeit Nike, adidas, and ASICS products sold through third-party marketplace listings. Counterfeit running shoes, which cannot provide the performance or safety characteristics of genuine products, damage brand reputation and divert revenue from legitimate sales channels.

- Tariff Impact on Vietnam and Southeast Asian Manufacturing: US tariff policy changes affecting Vietnam and other Southeast Asian countries, where the majority of US running shoe brands manufacture their products, represent the most significant near-term cost risk. Brands have limited ability to rapidly relocate manufacturing, creating exposure to significant retail price increases if tariff rates are implemented at levels that cannot be absorbed in brand margins.

Emerging Market Trends

1. Carbon Fiber Plate Racing Shoe Mass Market Adoption

Carbon fiber plate running shoes, which use a rigid carbon plate in the midsole to increase propulsive energy return and improve running economy by 3–4%, have transitioned from elite racing-only products to mainstream consumer items. Nike’s Vaporfly and Alphafly series, adidas’ Adizero Adios Pro Evo 2, Brooks’ Hyperion Elite, and ASICS’ MetaSpeed Sky are each recording strong consumer sales at USD 200–350 price points among recreational runners motivated by personal best improvement. This technology democratization has driven above-market revenue growth in the premium running footwear category.

2. Direct-to-Consumer Digital Channel Transformation

Nike’s strategy of reducing wholesale distribution in favor of DTC channel growth through Nike.com and Nike Apps is transforming the running gear retail landscape. In the third quarter of fiscal 2025, NIKE Digital sales declined 15% year-on-year. Despite this drop, digital remains a significant part of NIKE’s DTC business, which contributes around 40% of the company’s global revenue. Brooks, New Balance, and ASICS are each investing in DTC e-commerce capability, direct loyalty programs, and connected app ecosystems that create data-driven relationships with runners, enabling personalized product recommendations and retention marketing.

3. Running Watch and GPS Wearable Market Expansion

Garmin’s Forerunner and Fenix series, Apple Watch’s running tracking features, and the Coros running watch ecosystem are collectively driving a premium running accessory market growing at above-running-apparel rates. GPS watches with advanced biometric tracking, including running power, ground contact time, vertical oscillation, and AI-generated training load recommendations, are becoming standard equipment for dedicated recreational runners investing USD 300–600 in performance optimization tools. This category represents the highest average selling price segment in running accessories.

4. Sustainability and Circular Economy Initiatives

The US consumer’s growing environmental consciousness is driving demand for sustainable running gear that performs at competitive standards while reducing environmental impact. Nike’s Move to Zero program, adidas’ partnership with Parley for the Oceans, and On Running’s Cyclon subscription-based recyclable shoe program represent the leading commercial implementations of circular economy principles in running gear. These initiatives are commanding price premiums of 10–20% versus conventional equivalents among environmentally conscious consumers.

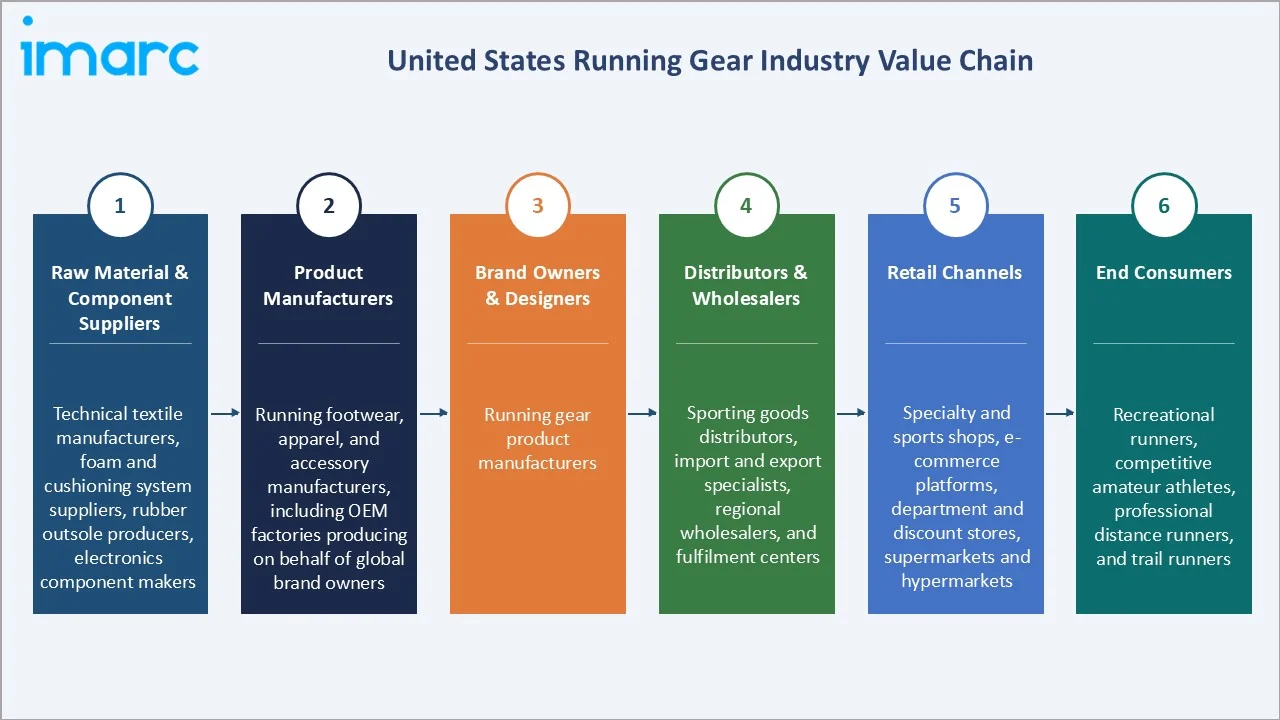

Industry Value Chain Analysis

The US running gear value chain spans from technical material and component manufacturing through product development, brand building, distribution, and consumer engagement across multiple retail formats and direct digital channels. The brand owner tier captures the majority of market value through design, technology development, and brand equity investment, while physical manufacturing is predominantly outsourced to specialist Asian factories.

|

Stage |

Key Players / Examples |

|

Raw Material & Component Suppliers |

Technical textile manufacturers, foam and cushioning system suppliers, rubber outsole producers, electronics component makers |

|

Product Manufacturers |

Running footwear, apparel, and accessory manufacturers, including OEM factories producing on behalf of global brand owners |

|

Brand Owners & Designers |

Running gear product manufacturers |

|

Distributors & Wholesalers |

Sporting goods distributors, import and export specialists, regional wholesalers, and fulfilment centers |

|

Retail Channels |

Specialty and sports shops, e-commerce platforms, department and discount stores, supermarkets and hypermarkets |

|

End Consumers |

Recreational runners, competitive amateur athletes, professional distance runners, and trail runners |

Technology Landscape in the United States Running Gear Industry

Advanced Midsole Cushioning Technology

The running footwear industry’s primary technology competition centers on midsole cushioning systems that balance energy return, cushioning protection, and weight reduction. Nike’s ZoomX foam, adidas’ BOOST foam, and New Balance’s FuelCell PEBA foam each represent proprietary approaches to maximizing cushioning performance. The addition of carbon fiber plates to enhance energy return and stiffness-optimized propulsion represents the most significant footwear technology innovation of the 2020s decade, enabling both elite performance improvement and recreational runner experience enhancement.

Performance Apparel Fabric Technology

Running apparel technology focuses on moisture management, temperature regulation, aerodynamic drag reduction, and integrated biometric sensing capability. Nike’s Dri-FIT and Dri-FIT ADV technologies, adidas' AEROREADY and COLD.RDY fabrics, and Brooks' DriLayer moisture management system represent the primary proprietary fabric technology platforms. Smart textile integration is the frontier technology development area, with mass-market adoption anticipated through 2028–2034.

GPS and Biometric Running Technology

GPS running watches have evolved from basic pace and distance tracking to comprehensive physiological monitoring platforms providing VO2 max estimation, training effect scoring, recovery time recommendations, and route navigation. Garmin’s Running Dynamics Pod, Coros’ Air Pack power meter, and Apple Watch’s running stride metrics exemplify the expansion of running data beyond pace and distance to biomechanical efficiency optimization. AI-powered training plan generation, personalized pacing recommendations, and injury risk prediction algorithms represent the next generation of GPS running technology entering mainstream adoption.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Gender |

Male |

52.4% |

2025 |

|

Distribution Channel |

Specialty and Sports Shops |

36.7% |

2025 |

|

Product |

🔒 |

🔒 |

2025 |

|

Region |

South |

33.6% |

2025 |

By Gender

Male consumers lead with a 52.4% share of the market in 2025, reflecting male runners’ historically higher participation in competitive road racing and higher average transaction values across all running gear categories. Nike’s male-targeted Vaporfly and Pegasus lines, adidas’ Adizero Boston and SL series, and Garmin’s Forerunner professional series are among the highest-revenue running gear products in the US male consumer segment.

To access detailed market analysis, Request Sample

Female at 34.1% share (2025) is one of the fastest-growing gender segments, driven by women’s road race participation growth outpacing men’s in RunningUSA’s annual survey, the athleisure trend driving women’s running apparel purchases for non-athletic daily use, and brands’ investment in female-specific performance research and product development. Unisex at 13.5% encompasses running accessories, including GPS watches, hydration systems, and compression sleeves that serve both male and female runners from shared product lines.

By Distribution Channel

Specialty and sports shops lead with a 36.7% share in 2025, reflecting the essential role of expert staff guidance, gait analysis, fit consultation, and try-on experience in the running footwear purchase journey. Running specialty retailers provide biomechanical assessment services that justify premium pricing and reduce return rates, creating customer outcomes impossible to replicate in mass retail or pure online channels.

Online at 28.9% share (2025) is the fastest-growing channel at approximately 6.8% CAGR through 2034, driven by Nike DTC digital, brand e-commerce platforms, Amazon's sporting goods expansion, and specialist running e-tailers. Department and discount stores at 18.4% serve the entry-level and value price tier, with Foot Locker, Dick’s Sporting Goods, and TJ Maxx serving price-sensitive running consumers.

Regional Market Insights

The South’s dominant position (33.6%, 2025) reflects the region’s position as the largest US population region, with year-round mild climate enabling outdoor running throughout all twelve calendar months, creating the highest annual running gear purchase frequency of any US region. Texas alone hosts over 500 registered road races annually, generating sustained gear demand across performance footwear, apparel, and accessories categories.

The West at 26.8% is driven by California’s combination of the largest state population, premium health and fitness consumer culture, and strong trail and mountain running market in Northern California and Colorado. The Midwest at 22.1% benefits from a strong mid-distance racing culture anchored by the Chicago Marathon and its supporting road race calendar.

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

33.6% |

Largest US regional population base, strong outdoor running and fitness culture year-round due to mild climate, high participation in road races and marathons, and large specialty sports retail footprint |

|

West |

26.8% |

High health and fitness consciousness in California, Colorado, and Oregon, strong trail and mountain running culture, premium running gear adoption, and significant technology-driven running wearable penetration |

|

Midwest |

22.1% |

Growing running event participation, established specialty running store network, strong collegiate and amateur running communities across Chicago, Minneapolis, and Columbus metropolitan areas, and rising e-commerce running gear adoption |

|

Northeast |

17.5% |

Concentration of competitive runners and triathlon participants, premium performance gear demand, strong urban running culture in New York and Boston, and the highest-income demographic driving above-average running gear spend per capita |

Competitive Landscape

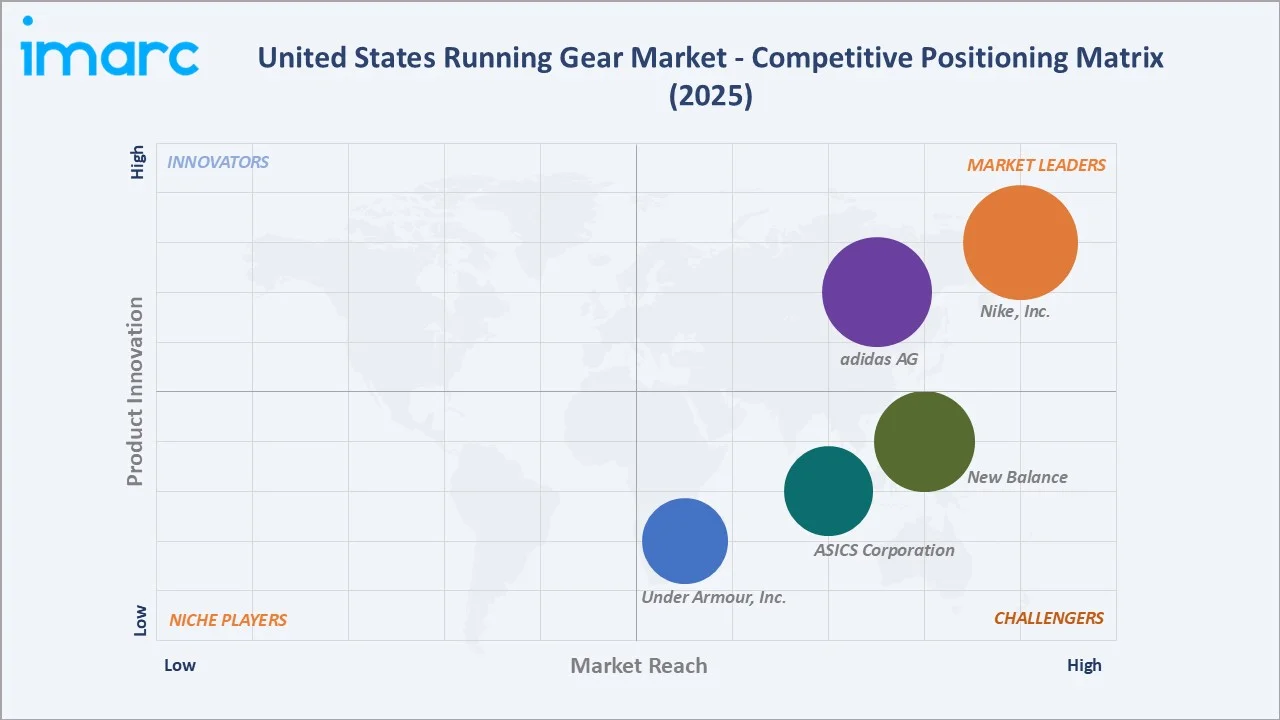

The United States running gear market is highly competitive, with global sporting goods conglomerates competing against pure-play running specialists, emerging performance brands, and technology companies. The market’s competitive intensity is highest in the USD 100–250 performance running shoe segment, where every major brand competes for specialty retailer shelf space and consumer trial.

|

Company Name |

Key Products/Brands |

Market Position |

Core Strength |

|

Nike, Inc. |

Vaporfly, Alphafly, Pegasus, Vomero, Invincible, Air Zoom |

Market Leader |

One of the largest running footwear revenue shares, deep athlete endorsement portfolio, and AI-integrated running app ecosystem |

|

adidas AG |

Adizero, Hyperboost Edge, Runfalcon, Galaxy 7, Ultraboost, adidas Running |

Market Leader |

BOOST technology platform leadership, strong sustainability credentials, global reach, and competitive marathon racing shoe portfolio |

|

New Balance |

AC Runner, Ellipse, Fresh Foam, FuelCell, Tektrel, 1080, among others |

Strong Challenger |

US-domestic manufacturing positioning, strong Fresh Foam technology franchise, premium price point differentiation, and growing trail running portfolio |

|

ASICS Corporation |

Gel-Kayano, Gel-Nimbus, MetaSpeed, Novablast, among others |

Challenger |

GEL cushioning technology heritage, strong biomechanics research foundation, competitive position in stability running shoes, and a loyal runner customer base |

|

Under Armour, Inc. |

UA Velociti Elite, UA Launch, UA Charged, UA Velociti Pro, UA Fly-By |

Challenger |

Performance technology integration with UA MapMyRun app ecosystem, competitive mid-price footwear positioning, and growing direct-to-consumer channel strength |

The competitive dynamics of the US running gear market are characterized by rapid innovation cycles combined with an intense battle for specialty retailer relationships that serve as the primary validation channel for running shoe credibility.

Key Company Profiles

Nike, Inc.

Nike, Inc. is one of the world’s largest athletic footwear and apparel companies and the dominant brand in the US running gear market. Its running category represents one of the highest-revenue running footwear franchises in the US market.

- Product Portfolio: Pegasus 41 (everyday trainer), Nike Zoom Vomero 18(maximum cushion), Invincible 3 (plush cushion), Vaporfly 3 (carbon plate racer), Alphafly 3 (elite marathon), Dri-FIT running apparel, Nike Running Club app.

- Recent Developments: In October 2025, Nike unveiled Project Amplify, the world’s first powered footwear system for running and walking, developed with robotics partner Dephy. The motor-assisted system is designed to help everyday users move faster and farther with less effort by augmenting natural ankle and lower-leg movement.

- Strategic Focus: DTC digital revenue maximization; Nike Run Club app ecosystem deepening; elite marathon performance leadership through Vaporfly and Alphafly platforms; women’s running category growth investment.

New Balance

New Balance is one of the largest privately held athletic footwear and apparel companies distinguished by its US and UK domestic manufacturing capability, a unique competitive positioning in a market dominated by Asian-manufactured goods. Its Fresh Foam and FuelCell technology platforms compete across the full price range from everyday training to carbon plate racing.

- Product Portfolio: Fresh Foam X 1080v14 (premium daily trainer), FuelCell SuperComp Elite v4 (carbon plate racer), More v4 (maximum cushion), 860v14 (stability), Lifestyle running-inspired 990 series, NB running apparel.

- Recent Developments: In February 2026, New Balance reported 2025 global sales of USD 9.2 billion, up 19%, marking its fifth consecutive year of double-digit growth. The company saw strong regional growth, with North America rising over 20%, while apparel and owned retail each crossed USD 1 billion.

- Strategic Focus: US domestic manufacturing as brand differentiator; FuelCell platform expansion into racing shoe competition with Nike and adidas carbon plate series; lifestyle and fashion running crossover with heritage silhouettes.

Market Concentration Analysis

The US running gear market exhibits moderate-to-high concentration at the footwear segment, with Nike, Inc. and adidas AG, collectively accounting for approximately 40–45% of total US running shoe revenues. The remaining 55–60% is distributed among specialist brands at the premium performance tier. The market’s concentration is moderating as premium challenger brands have achieved significant US market share gains through distinctive cushioning technology positioning and premium brand narratives that have captured consumer segments previously served by established leaders.

Investment & Growth Opportunities

Fastest Growing Segments

Online DTC channel growth (~6.8% CAGR), women’s running gear (~5.5% CAGR), carbon plate performance footwear (~8% annual growth), and GPS running watches and connected accessories represent the highest-growth investment vectors within the US running gear market through 2034. Trail running as a sub-category is growing at approximately twice the road running CAGR, creating above-market demand for trail-specific footwear, hydration, and navigation accessories.

Emerging Trends

The United States running gear market is witnessing several high-growth emerging trends through 2034. Carbon fiber plate midsole technology, originally an elite marathon racing innovation, has democratized to sub-USD 200 price points across multiple brands, creating mass-market demand for technology-differentiated running footwear. AI-powered personalization platforms are reducing return rates and improving fit satisfaction in both DTC and specialty retail channels.

Technology Investment Trends

- Advanced midsole foam technology R&D is the primary product innovation investment priority for major running shoe brands, with PEBA (polyether block amide) foam formulation optimization, nitrogen-infused foam processes, and responsive gel matrix technologies each receiving significant R&D budgets targeting the next generation of energy return and comfort performance.

- Sustainable material development investment is growing as brands respond to consumer demand and regulatory requirements for reduced environmental impact, with bio-based nylon, recycled Pebax, ocean plastic fiber textiles, and bio-based rubber outsoles each in commercial development across multiple brands.

Future Market Outlook (2026-2034)

The United States running gear market is positioned for sustained growth through 2034. From USD 13.43 Billion in 2025, the market is projected to reach USD 19.57 Billion by 2034, representing total incremental value creation of USD 6.14 Billion at a CAGR of 4.06%.

This growth is underpinned by the durable post-COVID shift toward active lifestyles, the ongoing premiumization of running footwear driven by performance technology innovation, the sustained growth in women’s running participation, and the e-commerce channel’s continued share gain, enabling direct brand-consumer relationships that support higher average transaction values.

The market’s competitive landscape will continue to evolve as premium challenger brands, compelling established leaders Nike and adidas to accelerate innovation cycles and deepen specialty retailer relationships to defend share. The tariff landscape affecting Asian manufacturing represents the most significant structural uncertainty for the 2026–2028 period, with brands that successfully diversify manufacturing toward non-tariff-affected geographies or build domestic manufacturing capability best positioned to manage cost risk without passing retail price increases that would compress demand.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 70 industry participants in 2024–2025, including running gear brand executives, specialty running retailer owners and buyers, US road race directors, running gear distributors, athletic footwear product developers, and running community coaches and athletes. Expert input validated market sizing, segment growth rates, and regional demand estimates.

Secondary Research

Secondary research encompassed running gear brand annual reports and investor presentations, RunningUSA State of the Sport annual surveys, Sports & Fitness Industry Association (SFIA) participation reports, US Census retail trade survey data, NPD Group athletic footwear data, SportsOneSource market share intelligence, and industry publications including Running Insight, Footwear News, and Sports Business Journal.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating US running participation trend data, athletic footwear and apparel retail sales data from industry associations, brand revenue growth disclosures, distribution channel share evolution modelling, and demographic trend analysis for gender and age cohort participation rates.

United States Running Gear Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

|

Scope of the Report

|

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Running Footwear, Running Apparel, Running Accessories, Fitness Trackers |

| Genders Covered | Male, Female, Unisex |

| Distribution Channels Covered | Specialty and Sports Shops, Supermarkets and Hypermarkets, Department and Discount Stores, Online, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Nike, Inc., adidas AG, New Balance, ASICS Corporation, Under Armour, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Running Gear Market Report

The United States running gear market reached USD 13.43 Billion in 2025 and is projected to reach USD 19.57 Billion by 2034.

The market is expected to grow at a CAGR of 4.06% during 2026-2034, driven by rising health and fitness awareness, marathon participation growth, e-commerce channel expansion, and performance technology integration in running footwear and accessories.

The South leads with a 33.6% share in 2025, driven by the region’s large population base, year-round outdoor running conditions, high road race participation, and large specialty sports retail infrastructure across Texas, Florida, and Georgia.

The male segment leads with a 52.4% share in 2025, reflecting historically higher participation rates in competitive running events and higher average transaction values in performance footwear and GPS watch categories.

Specialty and sports shops lead with a 36.7% share in 2025, reflecting the essential role of expert staff guidance, gait analysis, and fit consultation in performance running footwear purchase decisions. Online is the fastest-growing channel at approximately 6.8% CAGR.

Some of the key players include Nike, Inc., adidas AG, New Balance, ASICS Corporation, and Under Armour, Inc.

Key drivers include rising post-COVID health and fitness awareness that has sustained elevated running participation; marathon and road race participation growth driving performance gear demand; e-commerce and DTC channel expansion, and technology integration, including carbon fiber plate footwear, GPS watches, and smart running apparel.

Key opportunities include women’s running category growth investment, online DTC channel development, carbon plate performance footwear technology platforms, trail running gear market expansion, sustainable and recycled material running gear, and GPS running watch and smart accessories market growth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)