United States Stainless Steel Market Size, Share, Trends and Forecast by Product, Grade, Application, and Region, 2026-2034

United States Stainless Steel Market Size, Share, Trends & Forecast (2026-2034)

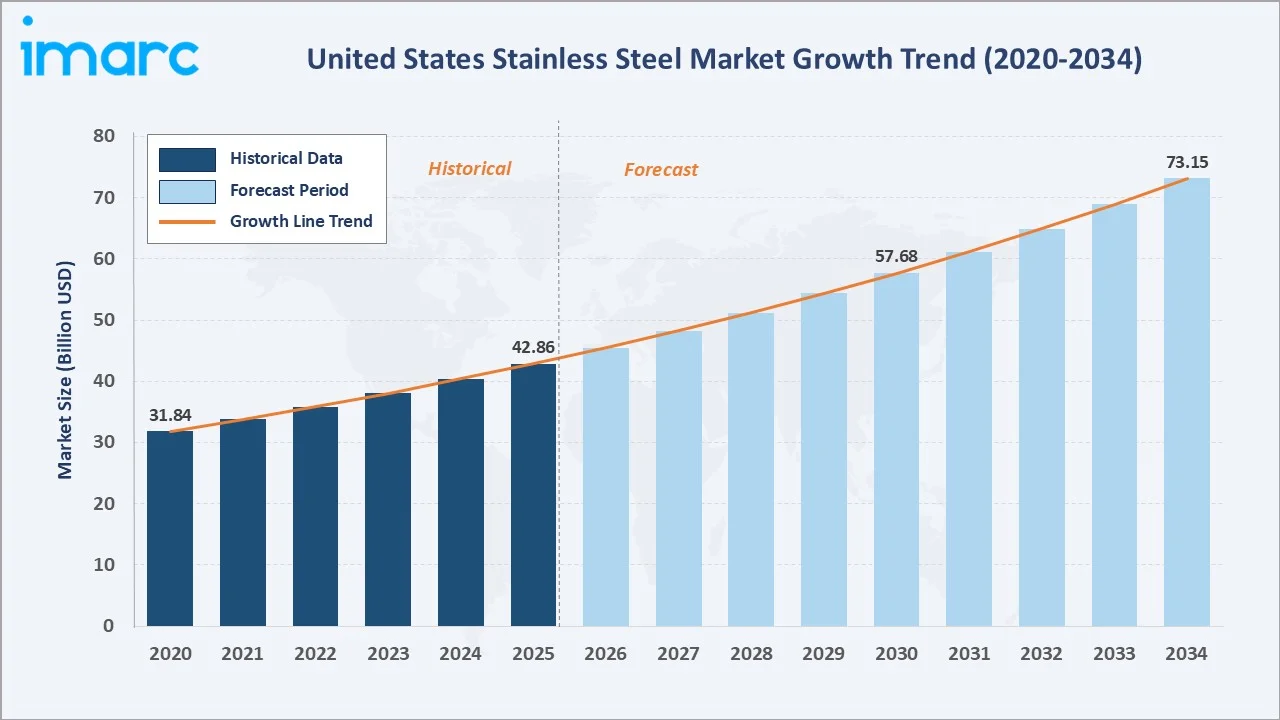

The United States stainless steel market reached USD 42.86 Billion in 2025 and is projected to reach USD 73.15 Billion by 2034, growing at a CAGR of 6.12% during 2026-2034. The market is driven by the Infrastructure Investment and Jobs Act, automotive lightweighting trends, expanding food processing sectors, and growing renewable energy installations.

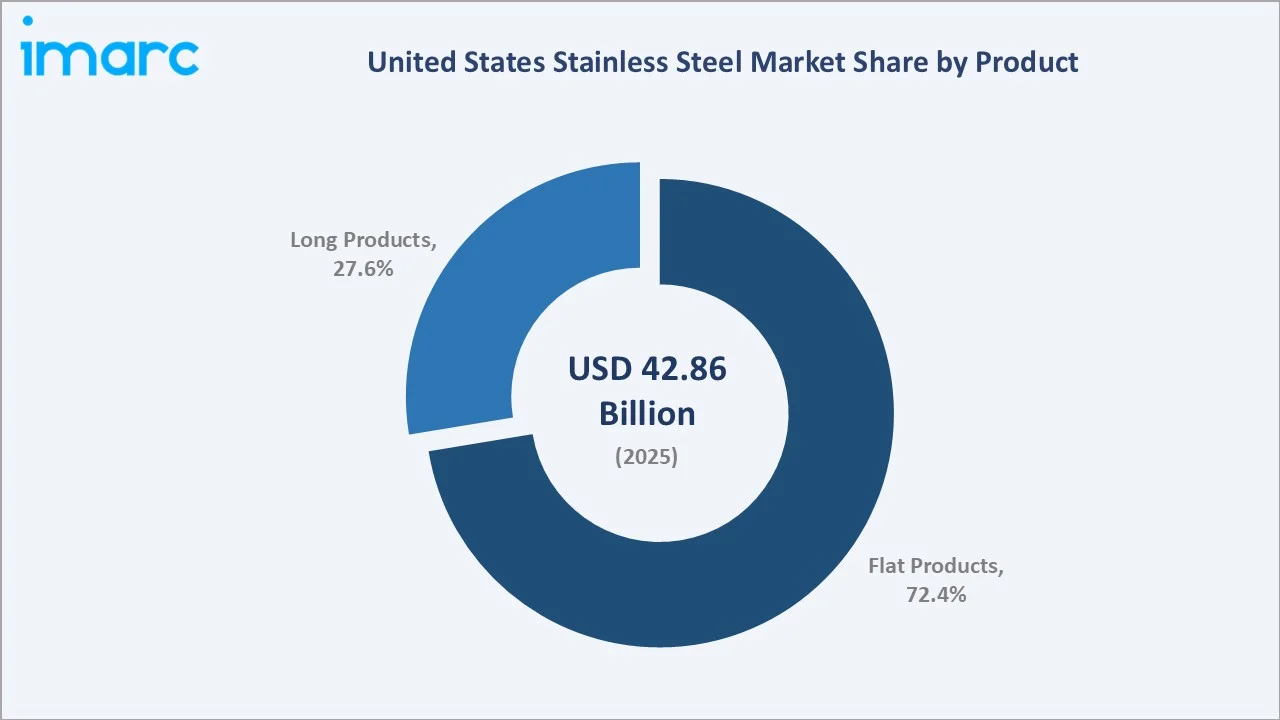

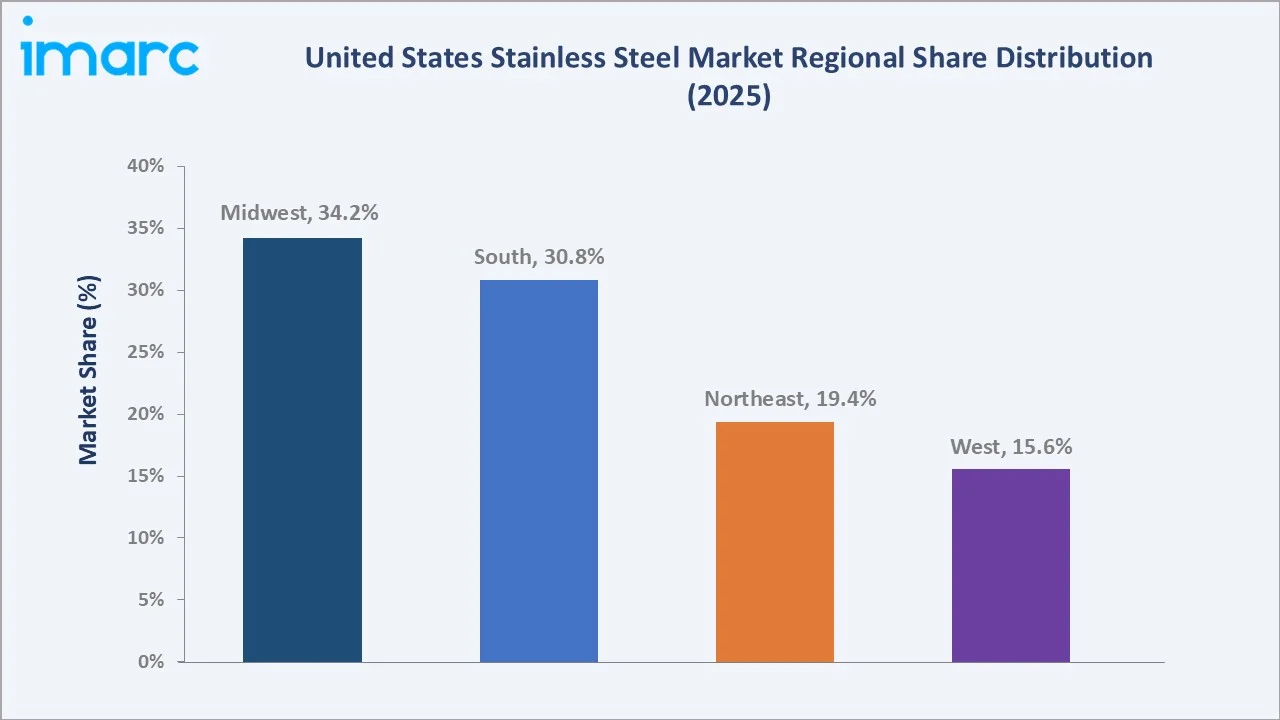

Flat products dominate at 72.4%, with the 300 Series leading grades at 54.8%. The Midwest commands 34.2% of the US market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 42.86 Billion |

|

Forecast Market Size (2034) |

USD 73.15 Billion |

|

CAGR (2026-2034) |

6.12% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product |

Flat (72.4%, 2025) |

|

Dominant Grade |

300 Series (54.8%, 2025) |

|

Leading Region |

Midwest (34.2%, 2025) |

The market expanded from USD 31.84 Billion in 2020 to USD 42.86 Billion in 2025, growing at a steady pace over five years, anchored at USD 57.68 Billion in 2030, and forecast to reach USD 73.15 Billion by 2034. Federal infrastructure investment, automotive demand recovery, and growing stainless adoption in renewable energy sustained the structural demand trajectory through the historical period.

To get more information on this market, Request Sample

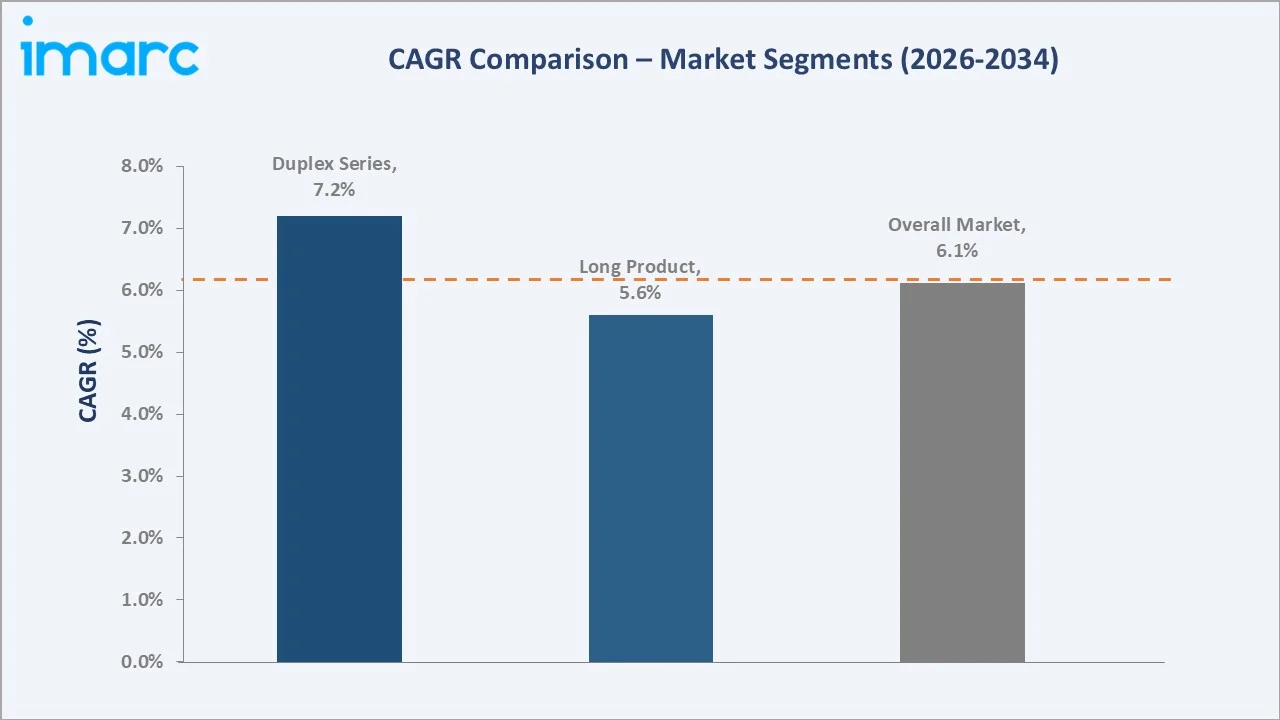

Flat products sustain their dominant share at 72.4% through automotive and construction applications. The 300 Series continues as the largest grade category, driven by its corrosion resistance critical across food processing, chemical, and architectural end-uses. The Duplex Series at 11.6% is the fastest-growing grade, gaining traction in oil & gas and desalination applications.

Executive Summary

The United States stainless steel market reached USD 42.86 Billion in 2025 and is projected to reach USD 73.15 Billion by 2034, driven by federal infrastructure investment, industrial reshoring, and growing specialty grade adoption. Flat products lead at 72.4%, and the 300 Series dominates at 54.8% in 2025.

The Midwest leads regionally at 34.2%, anchored by automotive and heavy manufacturing demand. The South at 30.8% is supported by petrochemical and construction growth. Duplex Series, at 11.6%, is the fastest-growing grade, gaining traction in oil & gas and desalination.

Key Market Insights

|

Insight |

Data |

|

Dominant Product |

Flat – 72.4% share (2025) |

|

Dominant Grade |

300 Series – 54.8% market share (2025) |

|

Leading Region |

Midwest – 34.2% market share (2025) |

|

Market Opportunity |

Duplex grades in oil & gas; green/low-carbon steel; near-shoring demand |

Key Analytical Observations Supporting the Above Data:

- Flat Products at 72.4%: Flat products dominate due to their extensive use in automotive body panels, food processing equipment, architectural cladding, and kitchen appliance manufacturing, where sheet and coil formats are the standard supply specification.

- 300 Series at 54.8%: The 300 Series leads as it offers the highest corrosion resistance and formability, making it the preferred choice for food & beverage processing, chemical handling, pharmaceutical equipment, and marine architecture across US industries.

- Midwest at 34.2%: The Midwest leads through its dense concentration of automotive OEMs, steel service centers in Chicago, and heavy industrial fabrication in Ohio, Michigan, and Indiana, creating a structurally high stainless steel demand base.

United States Stainless Steel Market Overview

The United States stainless steel market encompasses the production, processing, and distribution of iron-chromium alloy steel products containing a minimum of 10.5% chromium content, offering superior corrosion resistance across flat and long product formats.

The ecosystem integrates iron ore and ferrochrome raw material suppliers, domestic steel mills, service centers, fabricators, and end-use industries. Macroeconomic factors include federal infrastructure spending, reshoring of manufacturing, construction sector activity, and nickel and chromium commodity price dynamics.

Market Dynamics

To evaluate market opportunities, Request Sample

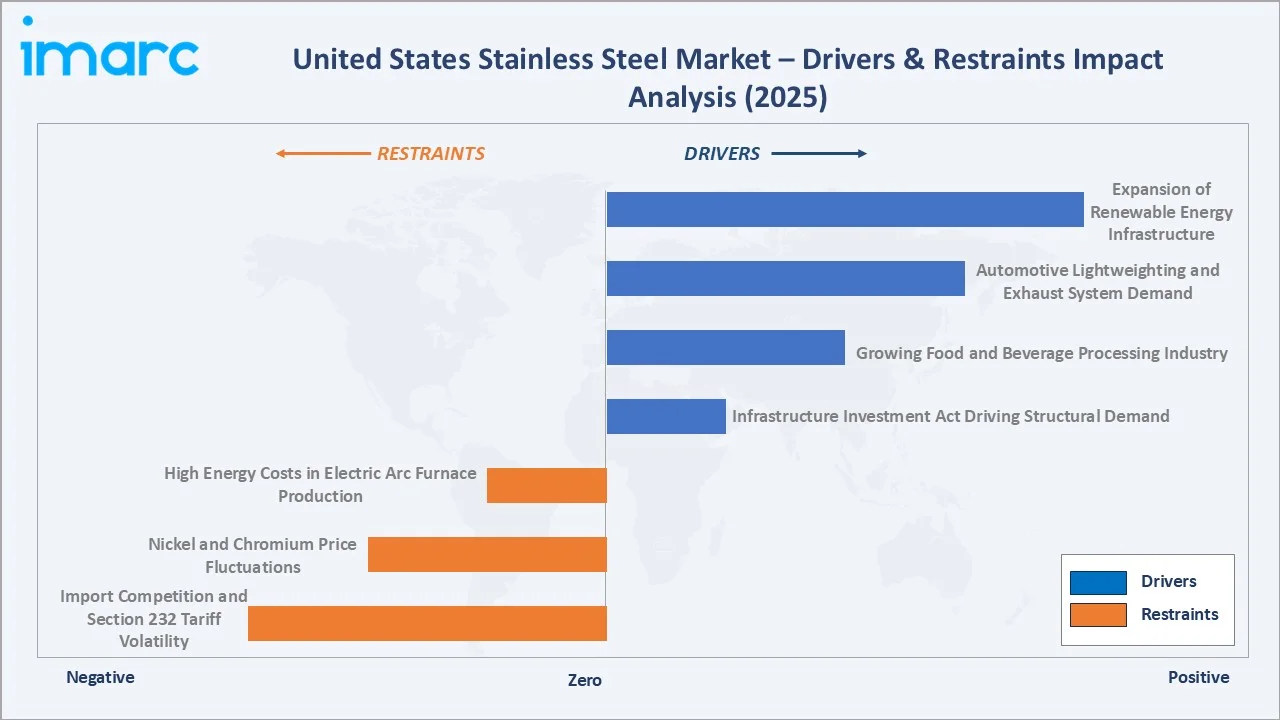

Market Drivers

- Infrastructure Investment Act Driving Structural Stainless-Steel Demand: The Infrastructure Investment and Jobs Act continue generating sustained procurement demand for stainless steel across water treatment facilities, bridges, tunnels, and public transit systems. Grade 316 stainless is heavily specified for water infrastructure piping and coastal construction, creating a multi-year government-funded demand pipeline across all US regions.

- Growing Food and Beverage Processing Industry: The US food and beverage processing industry is a leading stainless steel end-use sector, requiring 304 and 316 grade stainless for processing equipment, tanks, conveyors, and piping systems. Increasing food safety regulations and plant modernization programs are driving above-market demand growth in this segment through the forecast period.

- Automotive Lightweighting and Exhaust System Demand: Automotive manufacturers are increasing stainless steel use in exhaust systems, fuel cells, and structural components as lightweighting, and emissions reduction imperatives intensify. The shift toward fuel cell electric vehicles creates new demand for stainless bipolar plates as hydrogen vehicle production scales in the US through 2034.

- Expansion of Renewable Energy Infrastructure: Solar thermal, offshore wind, and geothermal energy projects are generating growing stainless-steel demand for heat exchangers, turbine components, desalination plants, and piping systems. The US Inflation Reduction Act investment in clean energy is creating a new structural demand pool for duplex and 300 Series grades in renewable energy applications.

Market Restraints

- Import Competition and Section 232 Tariff Volatility: Import competition from low-cost Asian producers and tariff policy uncertainty under Section 232 create pricing volatility and supply chain disruption risks for domestic US stainless steel producers and service centers. Tariff fluctuations can rapidly shift import volumes, creating demand-supply imbalances affecting pricing and margins.

- Nickel and Chromium Price Fluctuations: Nickel and chromium are the primary alloying elements in stainless steel production. Significant price volatility in LME nickel creates raw material cost uncertainty that compresses mill margins and increases stainless steel transaction price volatility, affecting buyer procurement strategies across the supply chain.

- High Energy Costs in Electric Arc Furnace Production: US stainless steel production via electric arc furnace is highly energy intensive. Rising electricity costs and grid reliability constraints increase operational costs for domestic producers, limiting their ability to compete on price against imported products in non-specialty commodity stainless grades.

Market Opportunities

- Near-Shoring and Domestic Manufacturing Investment: The structural trend toward domestic supply chain resilience is creating growing demand for US-manufactured stainless steel in semiconductor fabrication facilities, pharmaceutical clean rooms, and defense manufacturing, applications demanding domestic sourcing compliance and specialty grade availability.

- Duplex Grade Adoption in Oil and Gas and Desalination: Duplex stainless-steel grades are gaining traction in offshore oil platforms, subsea pipelines, chemical processing, and desalination plants. Their superior strength and chloride corrosion resistance versus 300 Series offers lifecycle cost advantages, creating a growing premium-grade substitution opportunity across the Gulf Coast industrial corridor.

Market Challenges

- Skilled Workforce Shortage in Specialty Steel Processing: The US stainless steel service center and fabrication industry faces a skilled workforce shortage in precision cutting, welding, and surface finishing. Workforce constraints limit throughput capacity, increase lead times, and raise processing costs, particularly for specialty duplex and high-alloy grade processing.

- Competition from Aluminum and Engineered Polymer Substitution: In select applications including automotive body panels, lightweight packaging, and consumer electronics, aluminum and high-performance polymers are competitive substitutes for stainless steel. Material substitution reduces addressable stainless-steel demand in specific end-use niches, requiring producers to differentiate on performance and lifecycle economics.

Emerging Market Trends

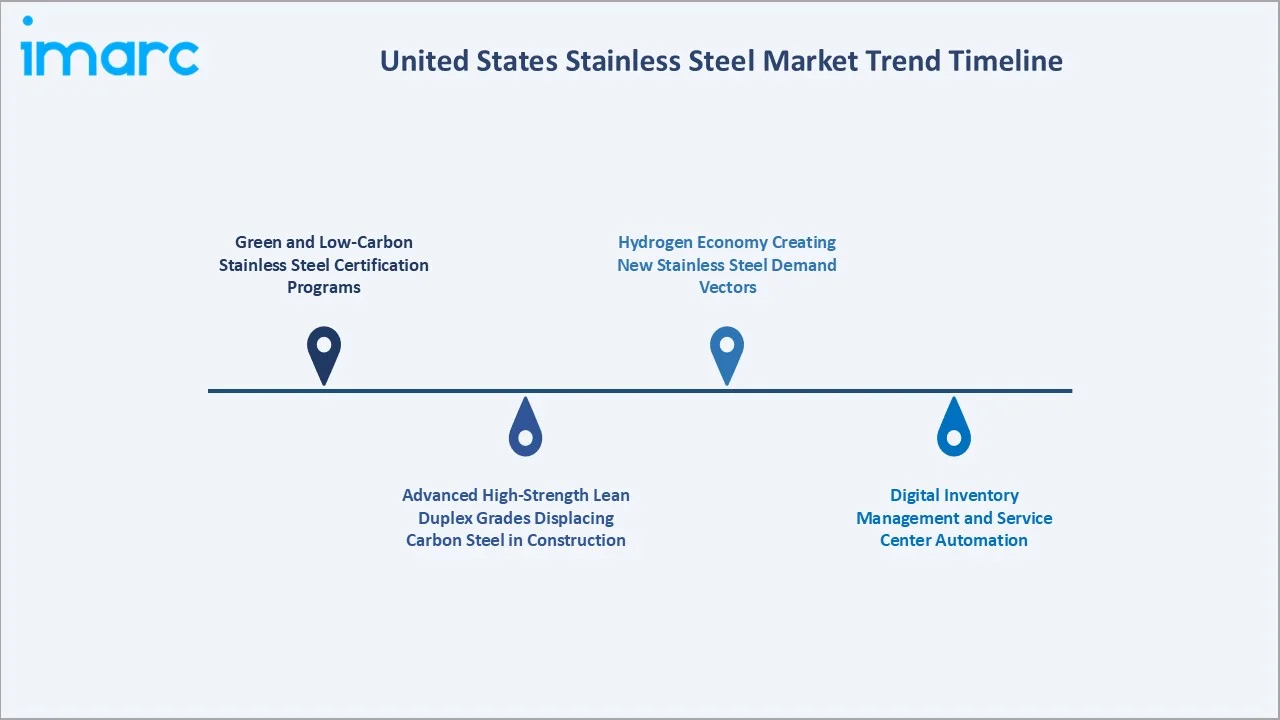

1. Green and Low-Carbon Stainless Steel Certification Programs

US industrial buyers are increasingly specifying low-carbon stainless steel with certified environmental product declarations for LEED-certified construction, federal procurement contracts, and ESG-aligned supply chains. Outokumpu's Circle Green and Acerinox's Ecostainless programs are gaining market traction in the US as sustainability credentials become a procurement differentiator.

2. Advanced High-Strength Lean Duplex Grades Displacing Carbon Steel in Construction

Lean duplex grades are increasingly displacing carbon steel in structural applications where corrosion resistance previously mandated carbon steel with protective coatings. This substitution trend in bridge girders, storage tanks, and coastal construction is expanding stainless steel's addressable construction market in the US through the forecast period.

3. Digital Inventory Management and Service Center Automation

US stainless steel service centers are investing in automated slitting, laser cutting, and real-time inventory management platforms to reduce lead times and processing costs. Digital transformation is enabling smaller minimum order quantities and faster custom processing turnaround, improving service center competitiveness against mill-direct supply channels.

4. Hydrogen Economy Creating New Stainless Steel Demand Vectors

The US hydrogen economy buildout, green hydrogen electrolyzers, hydrogen storage vessels, fuel cell stack components, and hydrogen distribution piping, is creating new stainless steel demand for 316L and duplex grades. The Department of Energy's hydrogen hub program creates a structural long-term demand pool for specialty stainless grades through 2034.

Industry Value Chain Analysis

The US stainless steel value chain integrates raw material procurement, domestic and import steelmaking, hot and cold rolling, service center processing, fabrication, and end-market consumption across automotive, construction, food processing, oil & gas, medical, and aerospace sectors.

|

Stage |

Key Participants |

|

Raw Material & Sourcing |

Iron ore, chromium, nickel, molybdenum, ferrochrome, and recycled scrap procurement |

|

Steelmaking & Alloying |

Electric arc furnace (EAF) and argon oxygen decarburization (AOD) refining process |

|

Hot & Cold Rolling |

Rolling, annealing, pickling, and finishing of flat and long stainless-steel products |

|

Distribution & Service Centers |

Metals USA, Ryerson, Service Center Institute members – slitting, shearing, processing |

|

End-Use Fabrication |

OEM manufacturers in automotive, food & beverage, construction, and oil & gas sectors |

|

End-Market Consumption |

Final consumption in infrastructure, consumer goods, industrial equipment, and aerospace |

The raw material and steelmaking tier is the most cost-sensitive stage, driven by LME nickel and ferrochrome spot prices. The service center tier, representing approximately 60-65% of US stainless steel distribution, is the most commercially critical intermediary stage between mill production and end-use fabrication.

Technology Landscape in the United States Stainless Steel Industry

Argon Oxygen Decarburization (AOD) Refining Technology

AOD technology remains the primary refining process for stainless steel production in the US, enabling precise control of carbon, nitrogen, and sulfur content. Modern AOD converters with computerized process control are improving yield, reducing raw material consumption, and enabling production of tighter-tolerance specialty stainless grades demanded by medical and semiconductor applications.

Powder Metallurgy and Additive Manufacturing Stainless Grades

Powder metallurgy stainless steel and metal additive manufacturing are creating new demand for specialty stainless powders in aerospace, medical implants, and defense components. Desktop Metal expanded its US stainless steel powder production for binder jetting additive manufacturing of 316L and 17-4 PH components to address growing domestic demand.

Surface Finishing and Functional Coating Technology

Advanced electropolishing, PVD coating, and nano-surface treatment technologies are enabling stainless steel service centers to supply higher-value, functional-surface products for pharmaceutical clean rooms, semiconductor equipment, and food contact applications — creating premiumization opportunities within the US stainless steel value chain.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Flat |

72.4% |

2025 |

|

Grade |

300 Series |

54.8% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

Midwest |

34.2% |

2025 |

By Product

Flat products dominate at 72.4% in 2025, encompassing hot-rolled and cold-rolled coils, sheets, and plates, the primary supply format for automotive, appliance, food processing, and architectural construction applications, where sheet and coil formats dominate procurement specifications.

To access detailed market analysis, Request Sample

Long products at 27.6% include bars, rods, wire, and structural sections serving oil & gas, construction, and mechanical engineering applications. Long products are experiencing above-average growth in the oil & gas sector, driven by subsea pipeline and offshore platform demand in the Gulf of Mexico.

By Grade

The 300 Series leads at 54.8% in 2025 through its dominant use in food & beverage processing, pharmaceutical, chemical, and architectural applications where austenitic stainless steel's corrosion resistance and formability are the primary selection criteria across US industries.

The 400 Series at 21.3% captures automotive exhaust, appliance, and industrial applications where ferritic grades offer cost efficiency and adequate corrosion resistance. Duplex Series at 11.6% is the fastest-growing grade category, driven by chemical processing, desalination, and offshore infrastructure demand. The 200 Series at 7.9% serves cost-sensitive consumer goods.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

Midwest |

34.2% |

Anchored by the Chicago steel service center hub, automotive supply chains, and heavy industrial fabrication demand across Ohio, Michigan, and Indiana. |

|

South |

30.8% |

Driven by petrochemical complexes in Texas and Louisiana, construction growth in Florida, and the expanding food processing industry demand. |

|

Northeast |

19.4% |

Supported by pharmaceutical manufacturing, food & beverage processing, high-value architectural applications, and dense industrial infrastructure. |

|

West |

15.6% |

Emerging aerospace, semiconductor fabrication, and technology infrastructure build-out is driving specialized stainless-steel demand in California and the Pacific Northwest. |

The Midwest, at 34.2%, leads the US stainless steel market through Chicago's steel service center hub, the automotive manufacturing corridor, and heavy industrial fabrication in the Great Lakes states. The South, at 30.8%, is driven by petrochemical complexes, construction growth in Texas and Florida, and food processing cluster demand.

The Northeast, at 19.4%, reflects dense pharmaceutical, biotech, and food & beverage processing industry demand. The West, at 15.6%, is experiencing emerging growth driven by semiconductor fab construction, renewable energy installations, and technology infrastructure development in California and the Pacific Northwest.

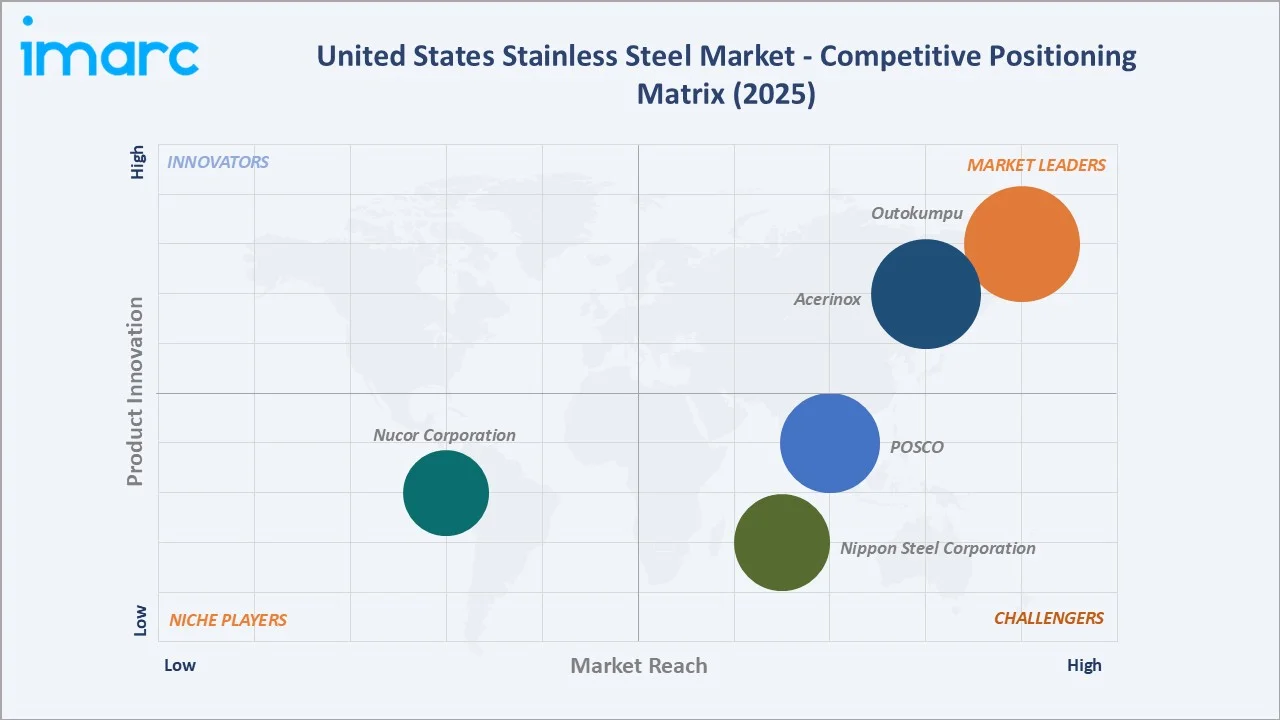

Competitive Landscape

The United States stainless steel market competitive landscape is moderately concentrated, with global integrated mills operating domestic facilities, import-focused distributors, and domestic EAF-based producers competing across flat and long product segments.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Outokumpu |

Moda, Core, Supra, Forta, Ultra, Dura, Therma, Prodec, Deco |

Market Leader |

Outokumpu Oyj leads in sustainable, low-carbon stainless steel production with strong US distribution through its Calvert, AL facility. |

|

Acerinox |

Austenitic, Ferritic, Martensitic, Duplex |

Market Leader |

Acerinox S.A. operates NAS in Ghent, KY — one of the largest integrated stainless facilities in the Americas. |

|

POSCO |

Austenitic, Ferritic, Martensitic, Duplex |

Strong Challenger |

POSCO supplies premium duplex and austenitic grades to North American automotive and petrochemical industries. |

|

Nippon Steel Corporation |

Austenitic stainless series, Ferritic stainless series, Austenitic-ferritic duplex stainless series, NS coat series, Colxam, Stainless Alsheet |

Strong Challenger |

Nippon Steel Corporation provides advanced stainless solutions for automotive and electronics applications in the US market. |

|

Nucor Corporation |

Stainless Steel Rebar (Grade 304, Grade 316), Carbon and Alloy Steel Sheet, Hot-Rolled Bar and Plate, Cold-Finished Bar |

Niche Player |

Nucor Corporation, a domestic US steel leader, is expanding its stainless capacity through electric arc furnace technology. |

Key players include Outokumpu, Acerinox, POSCO, Nippon Steel Corporation, Nucor Corporation, and others.

Key Company Profiles

Outokumpu

Outokumpu is a Finland-based global stainless-steel manufacturer with a significant US market presence through its Calvert, Alabama facility, one of North America's largest cold-rolling and finishing operations for stainless steel coil production.

- Key Products: Moda, Core, Supra, Forta, Ultra, Dura, Therma, Prodec, Deco

- Strategic Focus: Expanding certified low-carbon stainless steel production, growing Circle Green brand penetration in the US green construction and renewable energy sectors, and optimizing Calvert facility throughput for North American flat product supply.

Acerinox

Acerinox is a Spain-based global stainless steel producer operating North American Stainless (NAS) in Ghent, Kentucky, the largest integrated stainless steel production facility in the Americas, with hot-rolling, cold-rolling, and annealing-pickling capabilities.

- Key Products: Austenitic, Ferritic, Martensitic, Duplex

- Strategic Focus: Maximizing NAS facility utilization for domestic US flat product supply, expanding service center distribution agreements, and growing premium grade 316L and duplex production capacity at the Ghent facility.

Market Concentration Analysis

The US stainless steel market is moderately concentrated at the production level, with the top 3 key players collectively accounting for approximately 45-55% of domestic flat stainless production capacity. Import volumes from European and Asian producers account for 35-45% of total US stainless steel consumption.

Service center fragmentation is high, with hundreds of independent stainless-steel distributors and processors. Market concentration at the distribution tier is declining as digital platforms enable smaller distributors to compete with large service centers. Domestic production capacity is expected to increase modestly through 2034 as Nucor and other EAF producers invest in stainless steel expansion programs.

Investment & Growth Opportunities

Highest Growth Segments

Duplex Series grade adoption (~7.2% CAGR), renewable energy stainless applications (~8-10% CAGR), semiconductor and clean room stainless (~9% CAGR from smaller base), hydrogen economy stainless demand (~12% CAGR from emerging base), and green-certified low-carbon stainless (~10% CAGR premium segment) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Domestic stainless steel service center modernization represents the most actionable near-term investment opportunity, as aging processing equipment constraints create throughput bottlenecks across the Midwest and South distribution networks. Service centers investing in automated laser cutting, coil processing, and digital order management systems are capturing margin premium over commodity distribution competitors.

Investment Themes

- Green steel premium capture: US industrial buyers are demonstrating willingness to pay 3-8% premium for certified low-carbon stainless steel in LEED construction, federal procurement, and ESG supply chain compliance programs. Investment in green stainless certification infrastructure and carbon accounting systems creates a defensible price premium moat.

- Specialty grade vertical integration: The convergence of domestic semiconductor fab construction and hydrogen hub development creates a structural demand pool for 316L, duplex, and ultra-clean stainless grades with certified domestic sourcing. Vertical integration from specialty melt to precision fabrication targeting these sectors generates above-market margin opportunity through 2034.

Future Market Outlook (2026-2034)

The United States stainless steel market is projected to grow from USD 42.86 Billion in 2025 to USD 57.68 Billion by 2030, and USD 73.15 Billion by 2034, delivering a 6.12% CAGR over the forecast period. Three structural forces define US stainless steel market growth through 2034 with high confidence.

Federal infrastructure investment through the IIJA and IRA creates a decade-long government-funded stainless steel demand pipeline in water infrastructure, energy transition, and transportation construction. Industrial reshoring and near-shoring accelerates domestic stainless-steel procurement as semiconductor, pharmaceutical, and defense supply chains mandate domestic material sourcing.

The green economy transition — renewable energy installations, hydrogen infrastructure, and low-carbon building construction — creates new premium-grade stainless steel demand vectors with above-market growth rates, shifting the US market's demand mix toward higher-value specialty grades through 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025-2026), including stainless steel mill procurement directors, service center operations managers, automotive OEM materials engineers, food processing plant engineers, and construction materials specifiers.

Secondary Research

Secondary research encompassed AISI steel industry reports, US Census Bureau manufacturing statistics, USITC trade data for stainless steel imports and exports, company annual reports, EPA environmental permit filings, DOE hydrogen hub program documentation, and Infrastructure Investment Act procurement data. Over 60 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using end-use demand bottom-up model: (i) stainless steel consumption forecast by end-use industry; (ii) grade and product mix by end-use; (iii) average transaction price by grade and product format; (iv) import-domestic supply balance adjustment for Section 232 tariff scenario modeling across the forecast period.

United States Stainless Steel Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Flat, Long |

| Grades Covered | 200 Series, 300 Series, 400 Series, Duplex Series, Others |

| Applications Covered | Automotive and Transportation, Building and Construction, Consumer Goods, Mechanical Engineering and Heavy Industries, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Outokumpu, Acerinox, POSCO, Nippon Steel Corporation, Nucor Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States stainless steel market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the United States stainless steel market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States stainless steel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market

Frequently Asked Questions About the United States Stainless Steel Market Report

The US stainless steel market reached USD 42.86 Billion in 2025, up from USD 31.84 Billion in 2020, driven by Flat products at 72.4%, 300 Series at 54.8%, and Midwest regional demand at 34.2%. The market is supported by infrastructure investment, automotive demand, and growing food processing industry stainless steel consumption.

The US stainless steel market grows at 6.12% CAGR during 2026-2034, reaching USD 57.68 Billion by 2030 and USD 73.15 Billion by 2034. This growth reflects IIJA infrastructure demand, renewable energy stainless applications, industrial reshoring, and duplex grade substitution across oil & gas and chemical processing.

Flat products lead at 72.4% in 2025, capturing the largest end-use share through automotive, construction, food & beverage, and architectural applications where sheet, coil, and plate supply formats dominate procurement specifications.

The 300 Series leads at 54.8% through its widespread use in food & beverage, pharmaceutical, chemical, and construction applications. The Duplex Series at 11.6% is the fastest-growing grade, driven by oil & gas and desalination demand, growing at approximately 7.2% CAGR through the forecast period.

The Midwest leads at 34.2% through its dense automotive manufacturing, steel service center hub in Chicago, and heavy industrial fabrication base. The South at 30.8% is driven by petrochemical, oil & gas, and construction demand, with the Northeast and West at 19.4% and 15.6% respectively.

Leading companies include Outokumpu, Acerinox, POSCO, Nippon Steel Corporation, Nucor Corporation, and others.

The US stainless steel market is projected to reach USD 57.68 Billion by 2030, with Duplex Series growth, hydrogen economy demand, renewable energy stainless applications, and green certified low-carbon stainless steel becoming established premium market segments, contributing to sustained growth.

Three priority investment opportunities: green/low-carbon stainless steel certification for ESG-driven procurement premium capture, specialty stainless for hydrogen economy and semiconductor fab applications with domestic sourcing mandates, and US service center modernization through automation and digital processing platforms for margin improvement.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)