United States Used Car Market Size, Share, Trends and Forecast by Vehicle Type, Vendor Type, Fuel Type, Sales Channel, and Region, 2026-2034

United States Used Car Market Size, Share, Trends & Forecast (2026-2034)

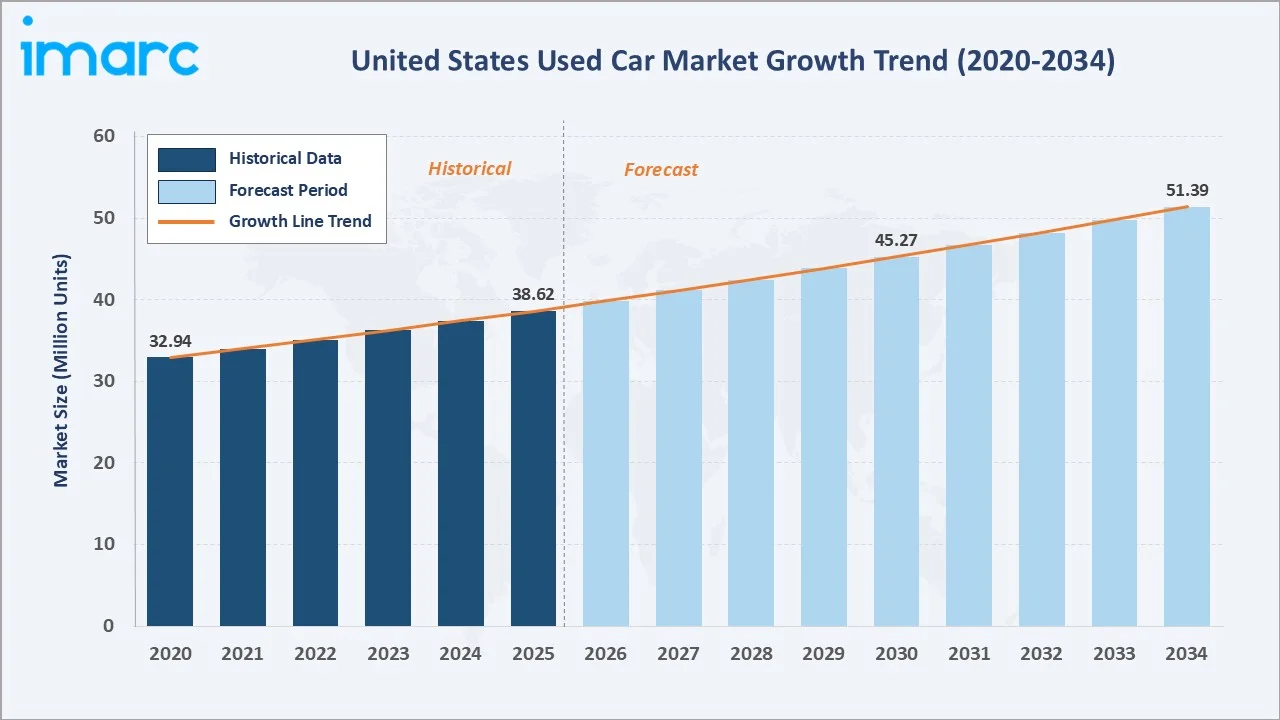

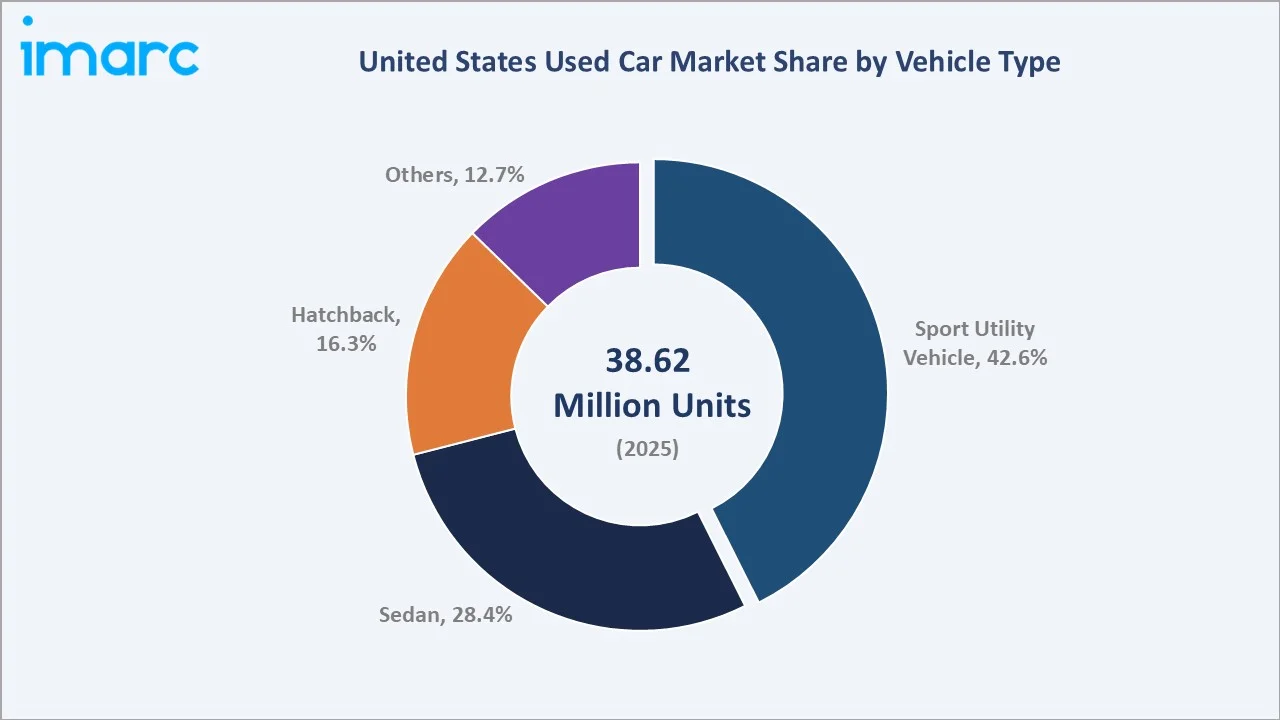

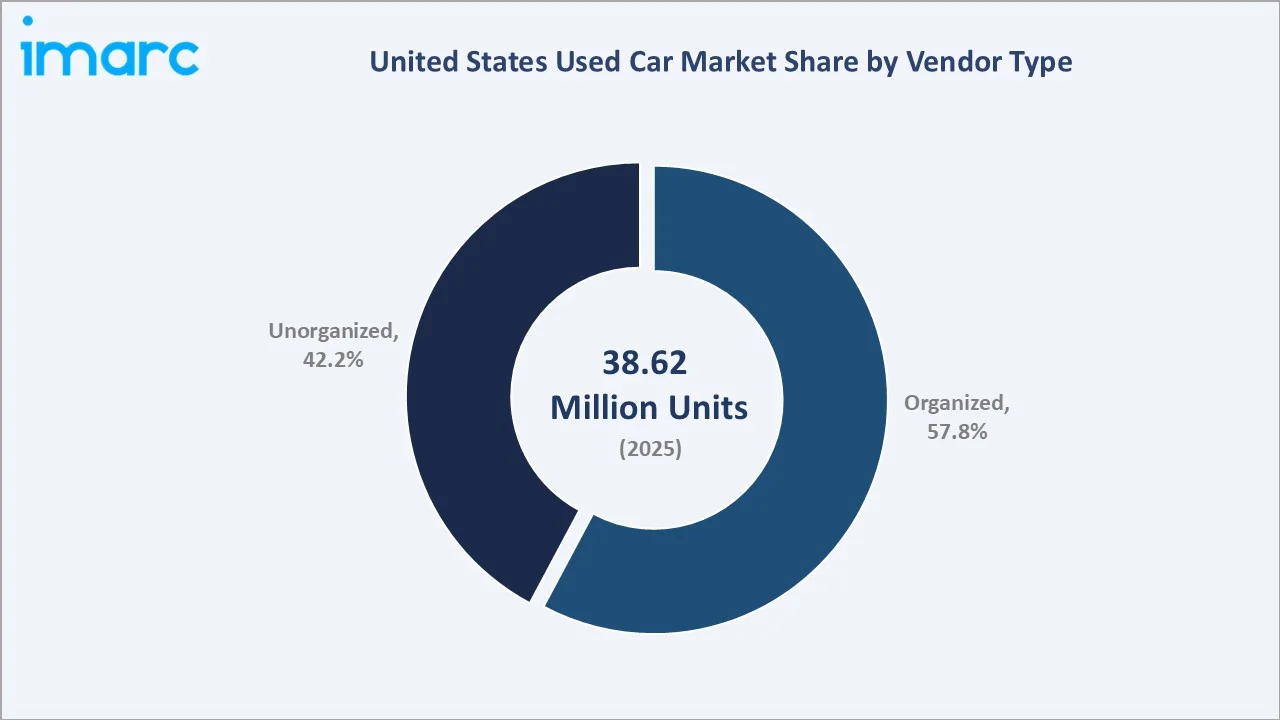

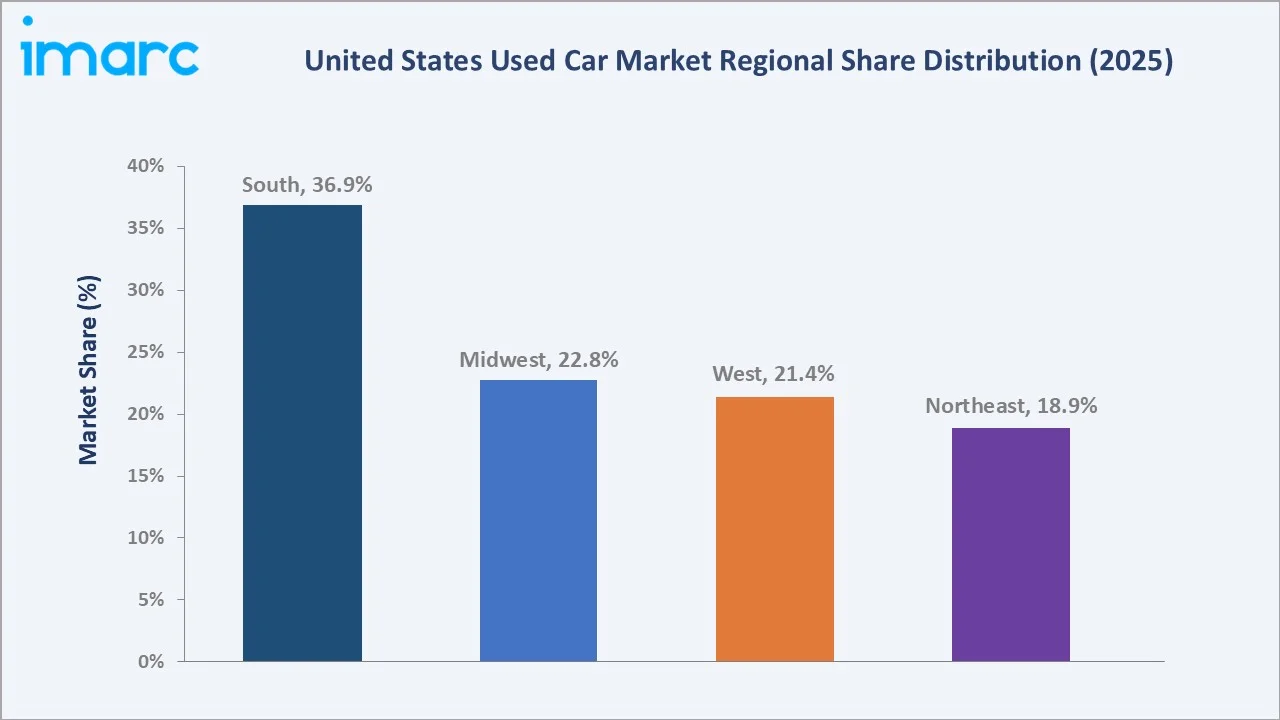

The United States used car market size was valued at 38.62 Million Units in 2025 and is projected to reach 51.39 Million Units by 2034, exhibiting a CAGR of 3.23% during the forecast period 2026-2034. Persistent new-vehicle affordability gaps, expanding online retail platforms, and recovering lease-return volumes are driving the US used car market growth. Sport utility vehicles lead at 42.6% share in 2025, while organized vendors account for 57.8% of total transactions. The South region dominates with 36.9% of national volume in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

38.62 Million Units |

|

Forecast Market Size (2034) |

51.39 Million Units |

|

CAGR (2026-2034) |

3.23% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South (36.9% share, 2025) |

|

Leading Vehicle Type |

Sport Utility Vehicle (42.6%, 2025) |

|

Leading Vendor Type |

Organized (57.8%, 2025) |

The United States used car market growth trajectory from 2020 through 2034 contrasts a steady historical expansion against a sustained forecast curve, supported by the new-vehicle affordability gap, growing online D2C retail, and the gradual normalization of lease-return inventory across the country.

To get more information on this market, Request Sample

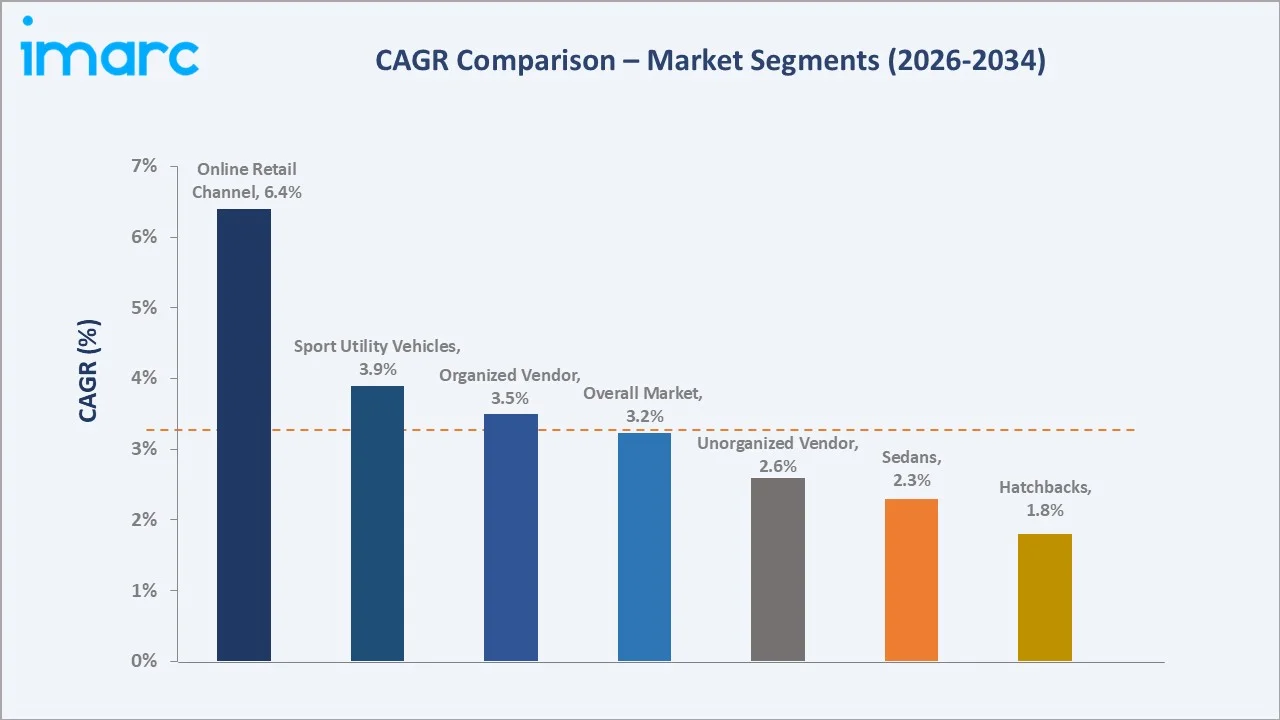

Segment-level CAGR comparisons highlight online retail and the SUV category as the fastest-growing sub-segments within the broader United States used car market forecast through 2034, while traditional sedan and hatchback formats grow at a more measured pace.

Executive Summary

The United States used car market is undergoing a meaningful structural shift. It is shaped by elevated new-car prices, the rapid rise of online used-vehicle retail, and the growing maturity of certified pre-owned (CPO) programmes. Valued at 38.62 Million Units in 2025, the market is projected to reach 51.39 Million Units by 2034 at a CAGR of 3.23%, expanding from 32.94 Million Units recorded in 2020.

Sport utility vehicles command 42.6% of unit volume in 2025, supported by sustained consumer preference for higher seating positions, AWD capability, and family-friendly cargo space. Sedans hold 28.4%, while hatchbacks contribute 16.3% on the back of urban demand and entry-level price points. Organized vendors dominate distribution at 57.8%, though unorganized dealers and private-party sales still represent a sizeable 42.2% of total transactions.

The South leads with a 36.9% volume share in 2025, followed by the Midwest at 22.8% and the West at 21.4%. The US used car market outlook remains constructive as digital retail expansion, used-EV adoption, and the multi-year recovery of late-model inventory converge across all four US census regions.

Key Market Insights

|

Insight |

Data |

|

Largest Vehicle Segment |

Sport Utility Vehicle – 42.6% share (2025) |

|

Second Vehicle Segment |

Sedan – 28.4% share (2025) |

|

Largest Vendor Type |

Organized – 57.8% share (2025) |

|

Fastest-Growing Channel |

Online Retail – ~6.4% CAGR (2026-2034) |

|

Leading Region |

South – 36.9% volume share (2025) |

|

Top Companies |

CarMax Enterprise Services, AutoNation Inc., Carvana Co., Lithia Motors Inc., Penske Automotive Group Inc. |

|

Forecast Market Size (2034) |

51.39 Million Units |

Key Analytical Observations Supporting the Above Data:

- SUVs' 42.6% dominance in 2025 reflects a multi-decade consumer migration away from sedans. Compact and mid-size used SUVs such as the Toyota RAV4, Honda CR-V, and Ford Escape consistently rank among the most-searched used models on major US auto-listing platforms.

- Sedans' 28.4% share is anchored by entry-level affordability, ride-hail driver demand, and strong residual values for nameplates such as the Toyota Camry, Honda Civic, and Honda Accord across the US used-vehicle market.

- Hatchbacks' 16.3% position is supported by urban commuters and first-time buyers in metropolitan markets. Models such as the Honda Fit, Hyundai Elantra GT, and Kia Forte5 continue to circulate strongly in the secondary market.

- Organized vendors' 57.8% lead reflects the scale of CarMax, AutoNation, Carvana, and franchise-dealer used-vehicle operations. Organized players differentiate through warranty bundles, financing integration, and 30-day return policies that build buyer trust.

- Unorganized vendors' 42.2% share captures independent used-car lots and private-party sales. Platforms such as Facebook Marketplace, Craigslist, and Autotrader continue to enable a large peer-to-peer transaction layer across the country.

- South's 36.9% regional dominance is underpinned by Texas, Florida, and Georgia. Population inflows, auto-dependent metros such as Houston, Dallas, Atlanta, and Miami, and a high household vehicle-ownership rate jointly support sustained used-car volume across the region.

United States Used Car Market Overview

The United States used car market includes the retail and wholesale sale of pre-owned passenger vehicles, spanning sport utility vehicles, sedans, hatchbacks, pickup trucks, vans, and other body styles. Inventory is sourced primarily through trade-ins, lease returns, fleet remarketing, rental-car de-fleeting, and private-party trades, then redistributed through wholesale auctions and retail channels.

The industry sits at the intersection of automotive manufacturing, consumer finance, digital retail, and logistics. Macroeconomic drivers include household disposable income, auto-loan interest rates, new-vehicle pricing, and used-vehicle wholesale benchmarks such as the Manheim Used Vehicle Value Index. The US used car industry analysis must also factor in the average age of vehicles on US roads, which reached approximately 12.6 years in 2024 according to S&P Global Mobility - a record level that supports sustained replacement demand.

Market Dynamics

To evaluate market opportunities, Request Sample

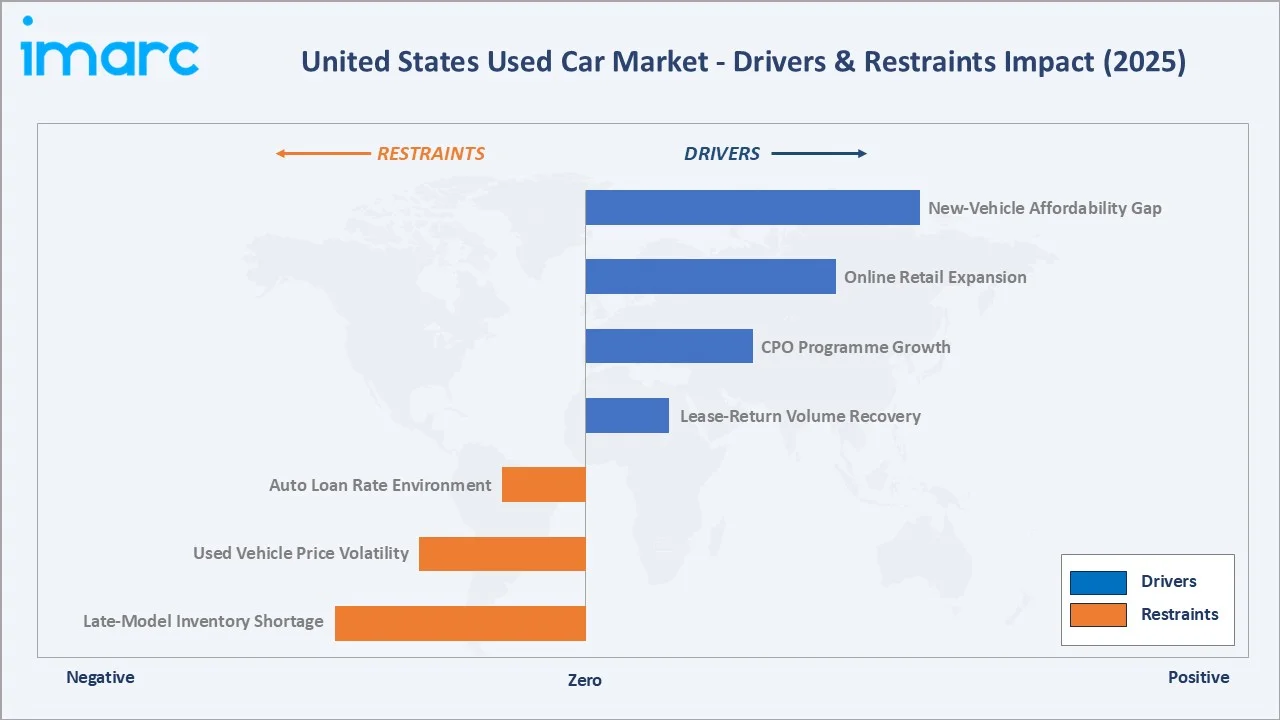

Market Drivers

- New-Vehicle Affordability Gap: Average transaction prices for new vehicles in the United States crossed over USD 48,000 in 2024 according to Kelley Blue Book, while comparable used vehicles transacted at roughly half that level. This widening gap continues to redirect price-sensitive buyers toward late-model used inventory.

- Online Retail Expansion: Carvana, CarMax's online platform, AutoNation USA, and Lithia's Driveway have collectively normalized end-to-end digital used-car purchasing. Touchless transactions, home delivery, and 7-day or 30-day return policies have meaningfully raised consumer confidence in online used-vehicle buying since 2021.

- CPO Programme Growth: Manufacturer-backed certified pre-owned programmes from Toyota, Honda, BMW, and others continue to expand. CPO units carry multi-point inspections, extended warranties, and special-rate financing - features that justify a premium and drive organized-channel share gains through 2034.

- Lease-Return Volume Recovery: After the 2022-2023 trough caused by depressed 2020-2021 leasing activity, the pipeline of three-year lease-return vehicles is expected to rebuild materially through 2026-2028, restoring late-model used-vehicle supply at retail auctions.

Market Restraints

- Late-Model Inventory Shortage: The 2020-2021 production cuts, chip shortage, and reduced fleet sales constrained the supply of 2-4 year old used vehicles entering the market in 2024-2025, pressuring CPO availability and lifting wholesale prices on the most-demanded segments.

- Used Vehicle Price Volatility: The Manheim Used Vehicle Value Index fluctuated sharply between 2021 and 2024, swinging dealer profitability and complicating retail pricing strategies for both organized and unorganized vendors across the United States.

- Auto Loan Rate Environment: Average used-vehicle auto-loan APRs remained near multi-year highs through 2024-2025, increasing total cost of ownership for consumers and partially offsetting the affordability advantage of used vehicles versus new ones.

Market Opportunities

- Used Electric Vehicle Market: As 2020-2022 model-year EVs rotate into the secondary market, used EV transactions are growing materially. Federal used-EV tax credits of up to USD 4,000 introduced under the Inflation Reduction Act continue to support adoption among value-conscious buyers.

- Subscription and Buy-Here-Pay-Here Innovation: Vehicle subscription pilots, refreshed buy-here-pay-here models with telematics-based default management, and rideshare-targeted leasing programmes are expanding the addressable market for organized used-car retailers through 2034.

Market Challenges

- Floor-Plan Financing Costs: Higher interest rates raise the cost of holding inventory on dealer lots, squeezing gross margins per unit and forcing faster turn rates across both organized and independent used-vehicle dealers.

- Title Fraud and Disclosure Compliance: Odometer rollback, flood- and salvage-title disclosure, and recall-compliance requirements vary by state. The patchwork landscape requires investment in vehicle-history data, technician training, and dealer-management systems for compliant operations.

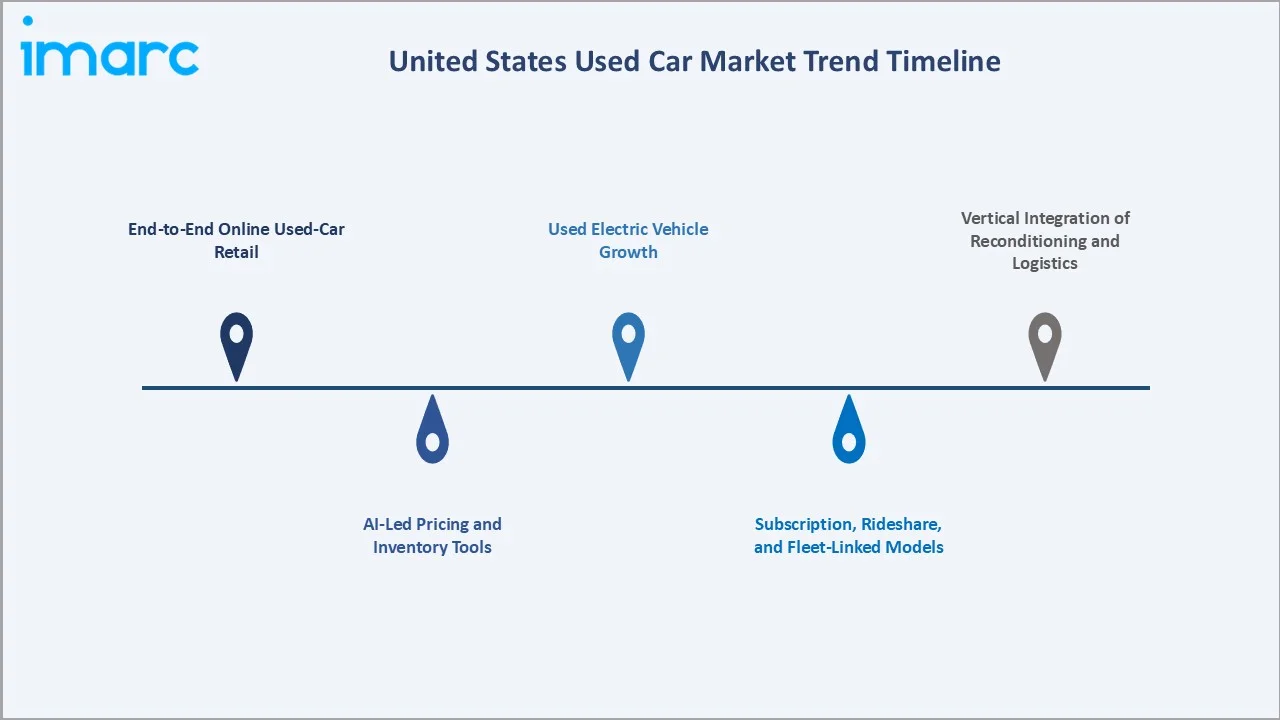

Emerging Market Trends

1. End-to-End Online Used-Car Retail

Online used-car retail is reshaping consumer behaviour. Carvana, CarMax, AutoNation USA, and Lithia's Driveway all offer fully digital purchase journeys with home delivery and multi-day return windows. Online transactions are projected to grow at roughly 6.4% CAGR through 2034, faster than any other US used-car sub-segment.

2. Used Electric Vehicle Growth

Used EV listings have expanded sharply since 2023 as 2020-2022 leases mature. Tesla Model 3 and Model Y dominate the early used-EV pool, while Chevrolet Bolt, Ford Mustang Mach-E, and Hyundai Ioniq 5 are gaining secondary-market traction. Federal used-EV tax credits are accelerating buyer interest through 2025-2027.

3. AI-Led Pricing and Inventory Tools

Vendors are deploying AI-driven pricing engines such as vAuto, Kelley Blue Book Instant Cash Offer, and proprietary tools at CarMax and Carvana. Real-time wholesale-market signals, demand-elasticity modelling, and image-recognition for condition grading are reducing average days-to-sale across organized retailers.

4. Vertical Integration of Reconditioning and Logistics

Leading retailers continue to invest in reconditioning megacentres, in-house transport networks, and integrated financing arms. CarMax's reconditioning hubs and Carvana's logistics fleet are illustrative examples that lower per-unit reconditioning costs while shortening time-to-retail through 2034.

5. Subscription, Rideshare, and Fleet-Linked Models

Hertz, Enterprise, and other rental operators have built dedicated used-car retail arms that monetize de-fleeted vehicles directly to consumers. Subscription and gig-economy-targeted leasing programmes are also extending the addressable buyer base across major US metros.

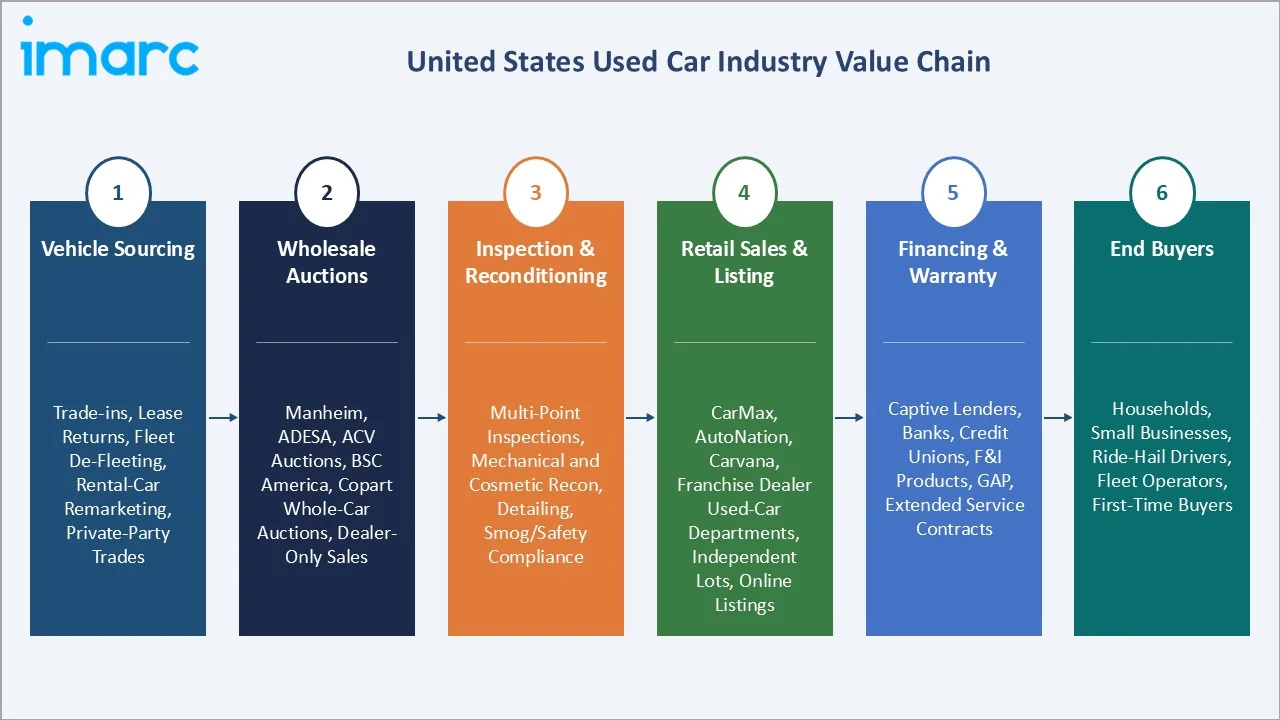

Industry Value Chain Analysis

The US used car industry value chain spans six integrated stages from vehicle sourcing through end-buyer purchase. Each stage shows distinct margin profiles and operating economics that shape the broader US used car market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Vehicle Sourcing |

Trade-ins, lease returns, fleet de-fleeting, rental-car remarketing, private-party trades |

|

Wholesale Auctions |

Manheim, ADESA, ACV Auctions, BSC America, Copart whole-car auctions, dealer-only sales |

|

Inspection & Reconditioning |

Multi-point inspections, mechanical and cosmetic recon, detailing, smog/safety compliance |

|

Retail Sales & Listing |

CarMax, AutoNation, Carvana, franchise dealer used-car departments, independent lots, online listings |

|

Financing & Warranty |

Captive lenders, banks, credit unions, F&I products, GAP, extended service contracts |

|

End Buyers |

Households, small businesses, ride-hail drivers, fleet operators, first-time buyers |

Organized retailers and large auction operators capture the highest strategic value by combining sourcing scale, reconditioning capability, and integrated financing. Online platforms continue to compress time-to-retail and increase price transparency, while franchise dealers leverage CPO programmes to defend and grow their used-vehicle margins.

Technology Landscape in the US Used Car Industry

Online Retail Platforms and D2C Apps

Direct-to-consumer apps and websites from Carvana, CarMax, AutoNation USA, and Lithia's Driveway support full-funnel digital buying, including pre-qualification, virtual walkarounds, e-signature paperwork, and home delivery. These platforms have fundamentally reset US consumer expectations around used-car purchase convenience since 2021.

Pricing Engines and Vehicle History Tools

vAuto, Kelley Blue Book, Black Book, J.D. Power Valuation Services, Carfax, and AutoCheck supply pricing intelligence and history data that underpin both wholesale and retail pricing decisions. Real-time data integration is now standard across organized US used-car retailers.

Telematics, Diagnostics, and Reconditioning Automation

OBD-II diagnostics, image-based dent detection, and AI-led condition grading are accelerating reconditioning workflows. Major reconditioning hubs use computer-vision quality inspection and standardized check-lists that reduce per-unit recon time and improve consistency across geographies.

EV Battery Health Assessment

As used EVs scale, battery state-of-health (SoH) verification has become a critical buyer-confidence factor. Recurrent, ChargerHelp, and proprietary OEM tools provide standardized battery-health certification, helping organized retailers price used EVs more accurately and reduce post-sale disputes.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the United States used car market, along with forecasts at the national and regional level from 2026 to 2034. The market has been categorized based on vehicle type and vendor type.

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Vehicle Type |

Sports Utility Vehicle |

42.6% |

2025 |

|

Vendor Type |

Organized |

57.8% |

2025 |

|

Fuel Type |

🔒 |

🔒 |

2025 |

|

Sales Channel |

🔒 |

🔒 |

2025 |

|

Region |

South |

36.9% |

2025 |

By Vehicle Type

Sport utility vehicles lead the US used car market with a 42.6% share in 2025. Demand reflects a multi-decade consumer migration away from sedans toward higher seating positions, all-wheel-drive capability, and family-friendly cargo space. Compact and mid-size models such as the Toyota RAV4, Honda CR-V, Ford Escape, Nissan Rogue, and Chevrolet Equinox consistently rank among the most-searched used models across major US listing platforms.

To access detailed market analysis, Request Sample

Sedans hold 28.4% of unit volume and remain a critical entry-level and ride-hail category. The Toyota Camry, Honda Civic, Honda Accord, and Toyota Corolla continue to anchor the segment with strong residual values, fuel economy, and reliability ratings. Hatchbacks contribute 16.3%, supported by urban commuters and first-time buyers, with models such as the Honda Fit and Hyundai Elantra GT circulating actively. The Others segment, at 12.7%, includes pickup trucks, vans, coupes, convertibles, and other body styles that round out the broader US used-vehicle pool.

By Vendor Type

Organized vendors are the dominant vendor type at 57.8% of US used car volume in 2025. This share reflects the scale and reach of CarMax, AutoNation, Carvana, Lithia / Driveway, Penske Automotive, Sonic / EchoPark, and the used-vehicle departments of franchise dealers across the country. Organized players differentiate through manufacturer-backed CPO programmes, multi-point inspections, integrated financing, extended warranties, and 7-day or 30-day return policies that strengthen consumer trust and support premium pricing.

Unorganized vendors account for 42.2% of US used car transactions in 2025. The category covers independent used-car lots, buy-here-pay-here operators, and private-party sales conducted through platforms such as Facebook Marketplace, Craigslist, and Autotrader. Unorganized channels typically lead on entry-level price points and serve a meaningful base of subprime and cash buyers, but they generally lack the warranty, financing, and reconditioning infrastructure that defines organized US used-car retail.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

36.9% |

Texas, Florida, Georgia population inflows; auto-dependent metros; high household vehicle ownership |

|

Midwest |

22.8% |

Auto-manufacturing belt, established franchise-dealer base, affordability-led demand |

|

West |

21.4% |

California ZEV programmes, used EV adoption, urban metros in CA, WA, OR; rideshare demand |

|

Northeast |

18.9% |

Dense metros (NYC, Boston, Philadelphia), CPO premium demand, suburban lease-return supply |

The South leads with a 36.9% volume share in 2025. Texas, Florida, and Georgia together account for the bulk of regional volume, supported by sustained population inflows, auto-dependent metros such as Houston, Dallas, Atlanta, Miami, and Tampa, and elevated household vehicle-ownership rates. The region also concentrates a deep base of franchise dealers, independent lots, and CarMax superstores that serve both retail and trade-in flows.

The Midwest holds 22.8% of national volume, anchored by the auto-manufacturing belt across Michigan, Ohio, Indiana, and Illinois. The region's deep franchise-dealer footprint, affordability-led buyer profile, and proximity to OEM remarketing flows underpin a steady pipeline of late-model used vehicles into both organized and unorganized retail channels.

The West contributes 21.4%, led by California, Washington, and Oregon. The region over-indexes on used EV demand, particularly in California where state ZEV mandates and HOV access incentives sustain electrified-vehicle adoption. Rideshare and gig-economy demand also support steady throughput of mid-mileage used sedans and crossovers in metros such as Los Angeles, San Francisco, Seattle, and Phoenix. The Northeast accounts for 18.9%, driven by densely populated metros across New York, Massachusetts, New Jersey, and Pennsylvania. CPO programmes are particularly strong in this region given the higher disposable-income base and the suburban lease-return supply that feeds franchise-dealer used-car departments.

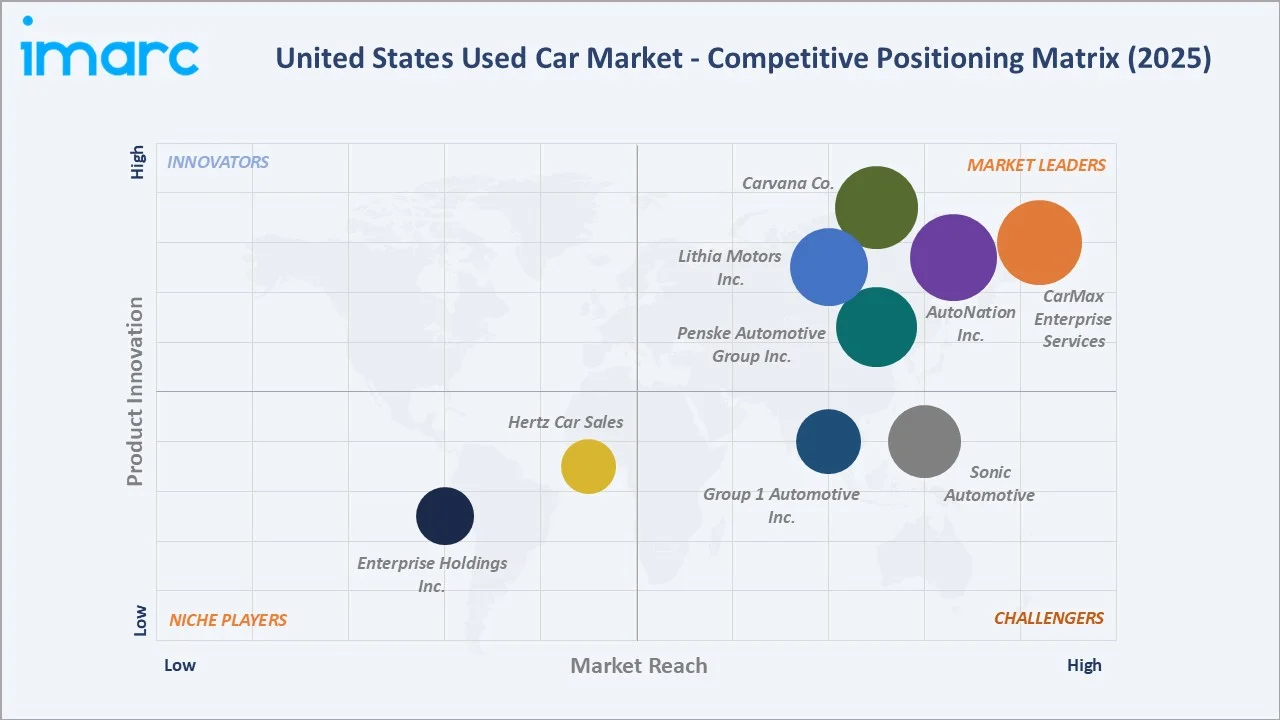

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

CarMax Enterprise Services |

CarMax |

Leader |

Largest US used-car retailer, omnichannel reach, instant cash offers |

|

AutoNation Inc. |

AutoNation |

Leader |

Nationwide used-car superstore network, brand scale, F&I depth |

|

Carvana Co. |

Carvana |

Leader |

Pure-play online retailer, end-to-end digital buying, home delivery |

|

Lithia Motors Inc. |

Lithia Motors |

Leader |

National rollup, omnichannel Driveway platform, dealer-network scale |

|

Penske Automotive Group Inc. |

Penske, CarShop |

Leader |

Premium franchise dealer, CarShop used-vehicle stores, fleet supply |

|

Sonic Automotive |

Sonic Automotive |

Challenger |

EchoPark pre-owned superstore network, strong Southeast presence |

|

Group 1 Automotive Inc. |

Group 1 |

Challenger |

Multi-state franchise dealer group, AcceleRide digital platform |

|

Hertz Car Sales |

Hertz Car Sales, Hertz Rent2buy |

Emerging |

Rental-fleet remarketing, no-haggle pricing, 7-day buy-back |

|

Enterprise Holdings Inc. |

Enterprise Car Sales |

Emerging |

Largest US rental remarketing, certified used vehicles, fleet supply |

The competitive landscape in the United States used car market is moderately fragmented. Large national retailers compete with online pure-plays, franchise dealer groups, and a long tail of independent lots. Players differentiate on inventory breadth, omnichannel reach, financing integration, reconditioning quality, and consumer-trust mechanisms such as no-haggle pricing and money-back guarantees. M&A and roll-up activity remains active - Lithia Motors continued its multi-year acquisition strategy through 2024, while CarMax and AutoNation expanded their omnichannel footprints with selective store openings and digital investments.

Key Company Profiles

CarMax Enterprise Services

CarMax Enterprise Services is the largest used-vehicle retailer in the United States, headquartered in Richmond, Virginia. Founded in 1993 as a spinoff of Circuit City, CarMax operates more than 240 superstores across the country and combines its physical footprint with a deeply integrated online buying platform.

- Product & Platform Portfolio: CarMax's offer spans the CarMax superstore network, CarMax.com online retail, instant online cash offers for trade-ins, in-house CarMax Auto Finance, MaxCare extended warranties, and a 30-day money-back guarantee paired with a 90-day or 4,000-mile limited warranty.

- Recent Developments: In 2024, CarMax continued advancing its omnichannel strategy by integrating online and in-store buying journeys, strengthening digital appraisal tools that deliver instant offers, and enhancing its financing capabilities through CarMax Auto Finance to support growth across customer segments in the United States.

- Strategic Focus: CarMax's strategy centres on omnichannel leadership, digital tooling enhancement, F&I monetization, and disciplined inventory turn through reconditioning hubs that maximize used-vehicle margin while preserving a no-haggle consumer experience nationwide.

AutoNation Inc.

AutoNation Inc. is one of the largest automotive retailers in the United States, headquartered in Fort Lauderdale, Florida. Established in 1996, AutoNation operates more than 350 new and used-vehicle franchises plus the AutoNation USA used-car superstore network across multiple US states.

- Product & Platform Portfolio: AutoNation's used-vehicle offering spans AutoNation USA standalone superstores, used-vehicle departments at franchise stores, AutoNation Express digital retail, AutoNation captive financing, and pre-owned certification programmes layered on top of OEM CPO offerings.

- Recent Developments: In 2026, AutoNation continued expanding its dealership footprint while accelerating its digital strategy, enhancing online sales capabilities and integrating omnichannel tools to improve customer experience, alongside capital allocation initiatives including a significant share buyback program.

- Strategic Focus: AutoNation's strategy focuses on scaling AutoNation USA superstores, deepening online retail integration, expanding captive finance, and using its dealer-network scale to source competitively-priced used inventory through trade-ins and remarketing channels.

Carvana Co.

Carvana Co. is a pure-play online used-vehicle retailer headquartered in Tempe, Arizona. Founded in 2012, Carvana built its brand around fully digital used-car purchasing, distinctive multi-storey car vending machines, and a nationwide home-delivery and 7-day return network.

- Product & Platform Portfolio: Carvana's offering covers the Carvana.com online retail platform, signature car-vending-machine pickup, in-house reconditioning megacentres, vertically integrated logistics, Carvana Financing, and a 7-day money-back guarantee that has become a category-defining consumer benefit.

- Recent Developments: In 2024-2025, Carvana stabilized its operating model after prior restructuring, returned to consistent unit-growth, integrated remaining ADESA US locations acquired earlier, and continued investing in AI-led pricing, inspection, and reconditioning tools.

- Strategic Focus: Carvana's strategic focus centres on scaling its omnichannel digital model, optimizing reconditioning and logistics throughput, deepening F&I attach rates, and leveraging integrated wholesale and retail capabilities to widen its used-vehicle competitive moat through 2034.

Market Concentration Analysis

The US used car market exhibits low to moderate concentration. The top five retail players - CarMax, AutoNation, Carvana, Lithia, and Penske Automotive - collectively account for an estimated 12-15% of US used-vehicle retail volume in 2025. The remaining share is distributed across thousands of franchise-dealer used-car departments, regional retailers such as Sonic / EchoPark and Group 1 Automotive, rental-fleet operators, and a long tail of independent used-car lots and private-party sellers nationwide.

The market is experiencing a steady consolidation dynamic. Organized vendors continue to gain share at the expense of independent lots, supported by online retail scale, captive financing, and CPO programmes. At the same time, dealer-group rollups and selective M&A activity by Lithia Motors and others are concentrating the franchise-dealer used-vehicle base. This bifurcated dynamic - online platforms versus franchise rollups - is intensifying competition through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Online used-car retail represents the highest-growth channel sub-segment at approximately 6.4% CAGR through 2034. Sport utility vehicles remain the largest absolute-volume growth category, while organized vendors continue to outpace unorganized channels in terms of market-share gains driven by trust, financing, and warranty bundling.

Emerging Sub-Markets

Used electric vehicles, certified pre-owned premium luxury, and ride-hail-targeted high-mileage sedans all represent above-trend growth pockets. Federal used-EV tax credits of up to USD 4,000, expanding 2020-2022 EV lease returns, and strong rideshare demand in major US metros support multi-year category expansion through the late 2020s and into 2034.

Venture and Strategic Investment Trends

Strategic acquisitions continue to reshape the competitive set. Lithia Motors completed multiple US dealership bolt-on deals, while Carvana's earlier acquisition of ADESA US locations strengthened its wholesale and reconditioning footprint. Venture and growth-equity capital is flowing into AI pricing platforms, EV battery-health analytics, online auction technology, and digital F&I tools across the US used-car ecosystem through 2034.

Future Market Outlook (2026-2034

The US used car market forecast projects steady volume expansion from 38.62 Million Units in 2025 to 51.39 Million Units by 2034 at a CAGR of 3.23%. The South is expected to retain regional leadership, while the West gains share on the back of used EV adoption. Sport utility vehicles, organized retailers, and online retail channels are forecast to outpace overall market growth.

Three structural shifts will shape the US used car market through 2034. First, online and omnichannel retail will become the dominant purchase pathway as consumer trust in digital used-car buying matures further. Second, used electric vehicles will move from niche to mainstream as 2020-2025 model-year EVs rotate into the secondary market in volume. Third, organized retailers will keep gaining share from independent lots through a combination of CPO programmes, financing integration, and standardized reconditioning that elevates the consumer experience nationwide.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024-2025 with US used-car stakeholders, including general managers at organized retailers, used-car directors at franchise dealer groups, wholesale-auction executives, F&I leaders, and digital-platform product managers. These interviews validated unit-volume sizing, segmentation estimates, and channel-growth assumptions.

Secondary Research

Secondary sources included Cox Automotive Manheim Used Vehicle Value Index publications, S&P Global Mobility vehicle-age data, Kelley Blue Book pricing reports, Edmunds market-insight notes, NADA and NIADA dealer-association data, US Bureau of Labor Statistics auto-loan rate releases, the Consumer Financial Protection Bureau auto-finance reports, and trade publications such as Automotive News, Used Car News, and WardsAuto.

Forecasting Models

Market size estimates and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating new-vehicle pricing trends, lease-return cycles, household disposable income, auto-loan rate paths, and historical category-evolution patterns. Scenario analysis was performed across base, optimistic, and conservative cases.

United States Used Car Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Units |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Hatchbacks, Sedan, Sports Utility Vehicle, Others |

| Vendor Types Covered | Organized, Unorganized |

| Fuel Types Covered | Gasoline, Diesel, Others |

| Sales Channels Covered | Online, Offline |

| Regions Covered | Northeast, Midwest, South, West |

| Comapnies Covered | CarMax Enterprise Services, AutoNation Inc., Carvana Co., Lithia Motors Inc., Penske Automotive Group Inc., Sonic Automotive, Group 1 Automotive Inc., Hertz Car Sales, Enterprise Holdings Inc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States used car market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the United States used car market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States used car industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Used Car Market Report

The United States used car market was valued at 38.62 Million Units in 2025, supported by elevated new-vehicle prices, online retail expansion, used EV demand, and consistent household replacement demand across all four US census regions.

The market is projected to reach 51.39 Million Units by 2034, growing at a CAGR of 3.23% during 2026-2034, supported by online retail growth, used EV adoption, and a multi-year recovery in lease-return inventory volumes nationwide.

Sport utility vehicles lead with a 42.6% share in 2025, driven by long-running consumer migration away from sedans, all-wheel-drive demand, and strong residual values for compact and mid-size used SUV nameplates across the United States.

Organized vendors dominate at 57.8% in 2025, supported by CarMax, AutoNation, Carvana, Lithia / Driveway, Penske, and franchise-dealer used-vehicle departments offering CPO programmes, integrated financing, and structured warranty packages nationwide.

Key trends include rising electric and hybrid vehicle demand, rapid online marketplace expansion, surge in certified pre-owned program uptake, and tech-enabled purchasing convenience.

Online retail is the fastest-growing channel, advancing at an estimated 6.4% CAGR through 2034, supported by Carvana, CarMax online, AutoNation USA, Lithia's Driveway, and broader consumer comfort with digital used-vehicle purchasing.

The South leads with a 36.9% share in 2025. Texas, Florida, and Georgia anchor the region with population inflows, auto-dependent metros, and elevated household vehicle-ownership rates that sustain steady used-vehicle volume.

Key drivers include the new-vehicle affordability gap, online retail expansion, certified pre-owned programme growth, lease-return volume recovery, used EV adoption, and the record 12.6-year average age of vehicles on US roads supporting replacement demand.

Major players include CarMax Enterprise Services, AutoNation Inc., Carvana Co., Lithia Motors Inc., Penske Automotive Group Inc., Sonic Automotive, Group 1 Automotive Inc., Hertz Car Sales, Enterprise Holdings Inc.

Late-model inventory shortages from earlier production cuts, used-vehicle wholesale price volatility, elevated auto-loan APRs, floor-plan financing costs, and state-level title and disclosure compliance burdens are the main near-term restraints facing the market.

The used electric vehicle segment is scaling rapidly as 2020-2022 lease vehicles rotate into the secondary market. Tesla Model 3 and Model Y dominate early volumes, supported by federal used-EV tax credits worth up to USD 4,000 for eligible buyers.

Online retail is reshaping consumer behaviour through Carvana, CarMax online, AutoNation USA, and Driveway. End-to-end digital purchasing, home delivery, multi-day return windows, and AI-led pricing have meaningfully expanded the addressable used-car buyer pool nationally.

Investment opportunities include online used-car platforms, AI pricing and inventory tools, EV battery-health analytics, digital F&I products, dealer-group roll-ups, and rental-fleet remarketing channels across the United States used-vehicle market through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade