United States Veterinary Software Market Size, Share, Trends and Forecast by Product, Delivery Mode, Practice Type, End Use, and Region, 2026-2034

United States Veterinary Software Market Size and Share:

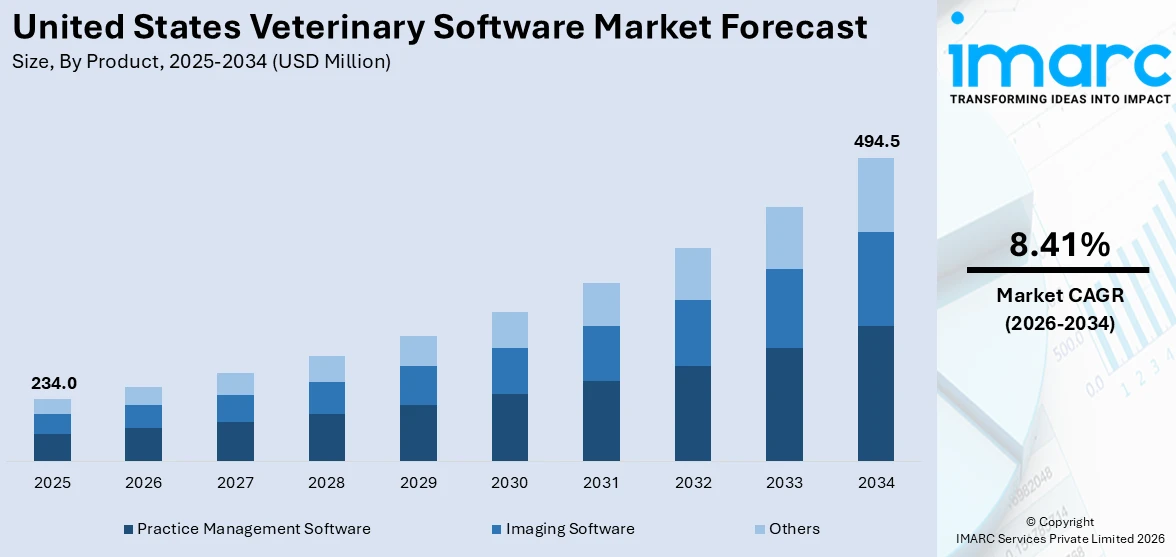

The United States veterinary software market size was valued at USD 234.0 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 494.5 Million by 2034, exhibiting a CAGR of 8.41% during 2026-2034. The market is driven by rising pet ownership, growing demand for efficient clinic management, increased adoption of telehealth, and advancements in cloud-based and AI-powered solutions. Additionally, the need for integrated healthcare systems and improved patient care is accelerating the adoption of innovative veterinary software across various regions, contributing to the expansion of the United States veterinary software market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 234.0 Million |

| Market Forecast in 2034 | USD 494.5 Million |

| Market Growth Rate 2026-2034 | 8.41% |

The market is experiencing robust growth, fueled by a combination of rising pet ownership, increasing demand for high-quality animal care, and the growing need for efficient clinical operations. With rising number of pet ownership in U.S. households, there is a heightened focus on delivering comprehensive healthcare services, which in turn drives the adoption of veterinary software. These solutions streamline appointment scheduling, billing, patient records, and inventory management, allowing clinics to improve workflow and enhance the overall client experience. Additionally, the increasing awareness of preventive care, wellness plans, and chronic disease management in animals has compelled veterinary practices to adopt software tools that facilitate consistent and efficient treatment planning. As veterinary service providers face mounting pressure to manage larger caseloads with limited resources, user-friendly, integrated software platforms are becoming essential to improve practice efficiency and support evidence-based care delivery across small and large veterinary establishments.

To get more information on this market Request Sample

Technological advancements and evolving client expectations are further propelling the United States veterinary market growth. The integration of telehealth features and remote monitoring tools into veterinary platforms is transforming how care is delivered, enabling virtual consultations, real-time updates, and better communication with pet owners. For instance, in January 2025, Covetrus unveiled its innovative Covetrus Platform™ at the VMX 2025 Conference, combining advanced technology with the powerful VetSuite network to enhance veterinary practices across the U.S. This comprehensive platform streamlines workflows, boosts productivity, and improves financial outcomes for clinics, helping them manage rising costs and competition. Key benefits include cost savings on medications, better pricing, and increased revenue through digital prescriptions. The VetSuite network empowers independent veterinarians by offering integrated solutions, lower costs, and exclusive community access, significantly improving clinic operations. The shift toward digital transformation in healthcare is boosting the adoption of cloud-based veterinary software due to its flexibility, accessibility, automatic updates, and strong data security. These systems suit both independent and multi-location practices. Their interoperability with diagnostic tools enhances collaboration and speeds up decision-making. Growing investments in pet insurance, veterinary infrastructure, and supportive welfare initiatives further drive market growth. Additionally, as demand for data-driven strategies rises, veterinary clinics increasingly use analytics tools to track clinical outcomes, financial health, and client engagement.

United States Veterinary Software Market Trends:

Rising Pet Ownership Driving Demand for Efficient Veterinary Services

The increasing number of pet-owning households in the United States is a key driver of the veterinary software market. As per the 2024 APPA National Pet Owners Survey, around 82 million U.S. households now own a pet, signaling a growing demand for veterinary services nationwide. This surge in pet ownership places significant pressure on veterinary clinics to manage more appointments, maintain accurate health records, and provide timely communication with pet owners. As a result, veterinary practices are increasingly turning to advanced software solutions that automate administrative tasks, streamline clinical workflows, and enhance patient management. These tools support functions such as electronic medical records (EMRs), automated reminders, integrated billing systems, and data analytics to improve service quality and clinic efficiency. In a competitive landscape, clinics that adopt such solutions are better equipped to manage increasing patient loads, offer personalized care, and maintain long-term client relationships, thus driving adding to a positive United States veterinary software market outlook.

Expanding Veterinary Healthcare Sector Boosting Technology Adoption

The U.S. veterinary healthcare sector is undergoing rapid transformation, with market projections indicating a compound annual growth rate (CAGR) of 5.30% from 2024 to 2032. This consistent growth highlights a rising investment in veterinary services, equipment, and technological infrastructure across the country. As clinics expand their service offerings, there is a growing need for sophisticated software solutions that can support modern clinical practices, including telemedicine, remote diagnostics, and real-time patient monitoring. Cloud-based veterinary software, in particular, is gaining popularity due to its flexibility, scalability, and ability to facilitate secure data sharing. Furthermore, the demand for interoperability, seamless integration with other healthcare systems, is becoming critical, enabling veterinarians to collaborate more effectively and make data-driven decisions. As the veterinary sector embraces innovation to meet rising client expectations and regulatory demands, the adoption of intelligent, integrated software platforms will be essential. This trend is positioning technology as a central pillar of future-ready veterinary care in the U.S.

United States Veterinary Software Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the United States veterinary software market, along with forecast at the country and regional levels from 2026-2034. The market has been categorized based on product, delivery mode, practice type, and end use.

Analysis by Product:

- Practice Management Software

- Imaging Software

- Others

As per the United States veterinary software market forecast, practice management software plays a significant role due to its comprehensive functionality, enabling clinics to streamline operations, manage appointments, maintain electronic health records, automate billing, and enhance client communication. Its growing adoption is driven by the need for operational efficiency and improved patient care, especially amid rising pet ownership. Imaging software is gaining prominence with the increasing reliance on diagnostic imaging in veterinary practices, supporting accurate diagnosis and treatment planning. Advancements in digital radiography and integration with other systems are further boosting its demand. The "Others" segment, which includes telehealth, inventory management, and lab integration tools, is expanding rapidly due to the shift toward virtual consultations, data-driven care, and the need for seamless interoperability. These segments collectively reflect the industry's pivot toward technology-enabled, efficient, and scalable solutions to meet the evolving demands of modern veterinary practice in the U.S.

Analysis by Delivery Mode:

- On-premises

- Cloud/Web-Based

In the United States veterinary software market, on-premises solutions have traditionally played a key role, particularly among larger or legacy practices valuing direct control over data security and infrastructure. These systems are preferred where internet reliability is a concern or for clinics with customized workflows requiring robust in-house capabilities. However, cloud/web-based solutions are rapidly gaining prominence, driven by their scalability, ease of access, and lower upfront costs. The shift toward remote work, telehealth, and mobile access to patient data has accelerated adoption of cloud-based platforms, especially among small to mid-sized clinics. Additionally, the ability to integrate seamlessly with other healthcare systems, ensure real-time updates, and support multi-location management is making cloud software increasingly essential. This transition reflects a broader trend in veterinary care toward flexible, tech-forward solutions that enhance collaboration, patient outcomes, and practice efficiency across the evolving digital healthcare landscape.

Analysis by Practice Type:

- Small Animals

- Mixed Animals

- Equine

- Food-producing Animals

- Others

In the United States veterinary software market, small animals represent the most dominant segment due to the high number of household pets and increasing spending on pet healthcare. With over 82 million U.S. households owning pets, there is strong demand for software that supports diagnostics, treatment plans, and client communication for companion animals. The mixed animals segment is also growing, driven by veterinary practices serving both small and large animals, requiring versatile software capable of handling varied medical records and billing needs. The equine segment benefits from rising interest in sports and recreational riding, prompting demand for specialized equine health tracking and mobile-compatible solutions. Food-producing animals drive software use in agricultural settings, focusing on herd health, productivity, and regulatory compliance. Other segments, including exotic and zoo animals, although smaller, contribute to niche software innovations. Overall, the growth is supported by increasing digitalization and demand for specialized care across all animal types.

Analysis by End Use:

Access the comprehensive market breakdown Request Sample

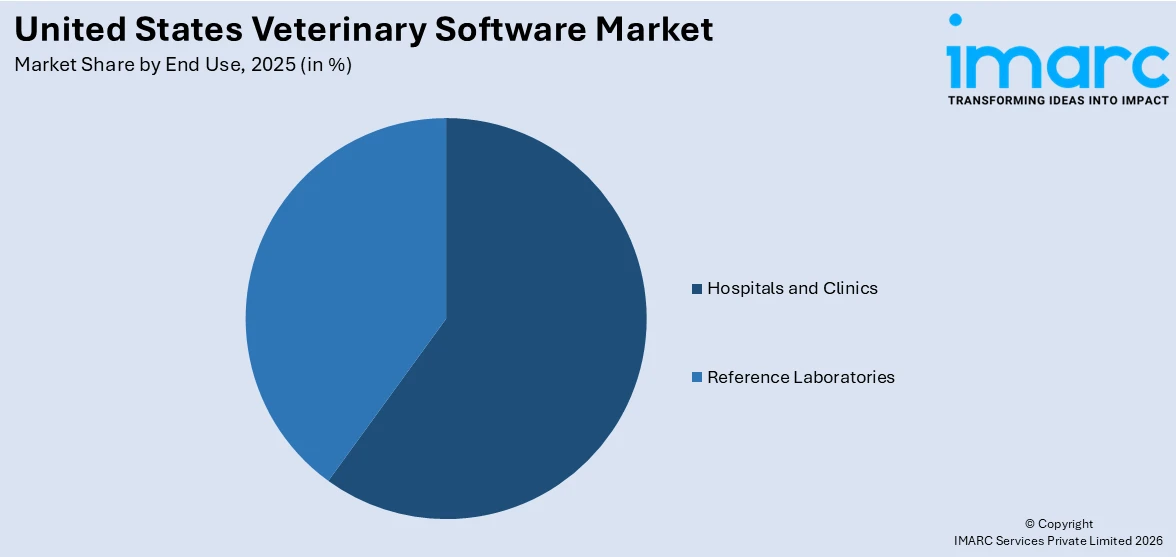

- Hospitals and Clinics

- Reference Laboratories

Hospitals and clinics hold a dominant position in the United States veterinary software market, as they are the primary points of care for both companion and livestock animals. The increasing need for efficient patient management, electronic health records, appointment scheduling, and billing solutions is driving the adoption of advanced veterinary software in these settings. With growing pet ownership and the rising demand for quality animal healthcare, veterinary hospitals and clinics are investing in digital tools to improve workflow, diagnosis, and treatment planning. On the other hand, reference laboratories are gaining prominence due to the increasing reliance on diagnostic testing and specialized services. These labs benefit from software that supports high-volume sample tracking, data analysis, and integration with clinic systems. The expansion of diagnostic capabilities and the need for real-time communication between clinics and labs are key drivers accelerating software uptake across both segments in the evolving veterinary care landscape.

Regional Analysis:

- Northeast

- Midwest

- South

- West

The United States veterinary software market is geographically diverse, with each region contributing uniquely to its growth. The Northeast region, with its high concentration of veterinary institutions and technologically advanced clinics, leads in adopting innovative software solutions to improve operational efficiency and patient care. The Midwest, home to numerous agricultural states, sees steady growth driven by mixed and food-producing animal practices requiring integrated software for herd health and compliance. In the South, the market is expanding rapidly due to a large pet-owning population and increasing demand for affordable veterinary care, pushing clinics to adopt cost-effective and scalable cloud-based systems. Meanwhile, the West benefits from a strong tech ecosystem and a high rate of pet ownership, encouraging early adoption of AI-enabled, cloud-based, and telehealth-friendly platforms. Across all regions, the drive to streamline veterinary operations, enhance patient outcomes, and integrate telemedicine continues to support robust software market growth.

Competitive Landscape:

The competitive landscape of the U.S. veterinary software market is characterized by the presence of both established and emerging players offering a range of solutions tailored to different veterinary needs. For instance, in May 2024, Evette, a leader in veterinary relief staffing, partnered with Shepherd Veterinary Software to address the veterinary industry's workforce shortage and burnout issues. This collaboration allows Shepherd clinics nationwide to easily access Evette’s relief staffing services, streamlining the process of securing temporary veterinary staff. With the veterinary industry facing high turnover and burnout, this innovative solution aims to improve staffing efficiency and reduce costs associated with turnover. The collaboration benefits over 600 clinics, providing better access to relief services for both practitioners and clinics, addressing the ongoing staffing crisis in animal healthcare. Companies compete primarily on technological innovation, user interface design, integration capabilities, and customer support services. Cloud-based platforms and AI-powered tools are gaining traction, and providers are focusing on adding advanced features like telemedicine, mobile access, and real-time analytics. Market players also differentiate themselves by targeting specific practice sizes—from small independent clinics to large hospitals and offering flexible pricing models. Strategic partnerships, product upgrades, and acquisitions are common as firms aim to expand market share and improve interoperability with laboratory systems, imaging tools, and third-party health platforms.

The report provides a comprehensive analysis of the competitive landscape in the United States veterinary software market with detailed profiles of all major companies.

Latest News and Developments:

- April 2025: Veterinary tech platform Otto launched automatic write-back for its AI-powered Recap feature, enabling seamless integration of AI-generated SOAP notes with major practice management systems. This update reduces manual admin work and is available free for Otto Flow subscribers. Vello reduces no-shows by 19%, streamlining client communication with automated reminders, online scheduling, two-way texting, and mobile access to pet records.

- December 2024: Provet Cloud launched a pilot program with a major U.S. veterinary group operating over 200 locations, expanding its North American presence. Already supporting 150 U.S. clinics, this marks its first corporate partnership in the region. The cloud-based platform aims to streamline operations and enhance patient care for large-scale veterinary groups.

- May 2024: Bionet America, Inc. launched the Brio XVet series, a next-gen multiparameter veterinary monitor line designed for surgical efficiency and safety. Featuring BT Link Next software, these monitors automatically capture vital signs, allowing vets to focus on patient care. The Brio X7Vet boasts a 15.6" touchscreen, the largest in its class, ensuring enhanced visibility. Now available across North America.

- August 2024: Inspire Veterinary Partners announced a non-binding acquisition proposal for Vetsie.ai, an AI-driven veterinary platform. If completed, this equity-only acquisition would integrate AI tools into IVP’s clinics, enhancing pet healthcare efficiency. Vetsie.ai, backed by Leap Venture Studio, Mars Petcare, and others, aims to revolutionize veterinary workflows with AI.

United States Veterinary Software Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Practice Management Software, Imaging Software, Others |

| Delivery Modes Covered | On-premises, Cloud/Web-Based |

| Practice Types Covered | Small Animals, Mixed Animals, Equine, Food-producing Animals, Others |

| End Uses Covered | Hospitals and Clinics, Reference Laboratories |

| Regions Covered | Northeast, Midwest, South, West |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States veterinary software market from 2020-2034.

- The United States veterinary software market research report provides the latest information on the market drivers, challenges, and opportunities in the regional market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within the region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States veterinary software industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Veterinary Software Market Report

The United States veterinary software market was valued at USD 234.0 Million in 2025.

The United States veterinary software market is projected to exhibit a CAGR of 8.41% during 2026-2034, reaching a value of USD 494.5 Million by 2034.

Key factors driving the United States veterinary software market include the increasing demand for efficient practice management, the growing adoption of telemedicine and remote monitoring, advancements in cloud-based solutions, enhanced data security, the need for seamless integration with other healthcare systems, and the rising investment in veterinary services and technology.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)