US Cement Market Size, Share, Trends and Forecast by Type, End-Use, and Region, 2026-2034

US Cement Market Size, Share, Trends & Forecast (2026-2034)

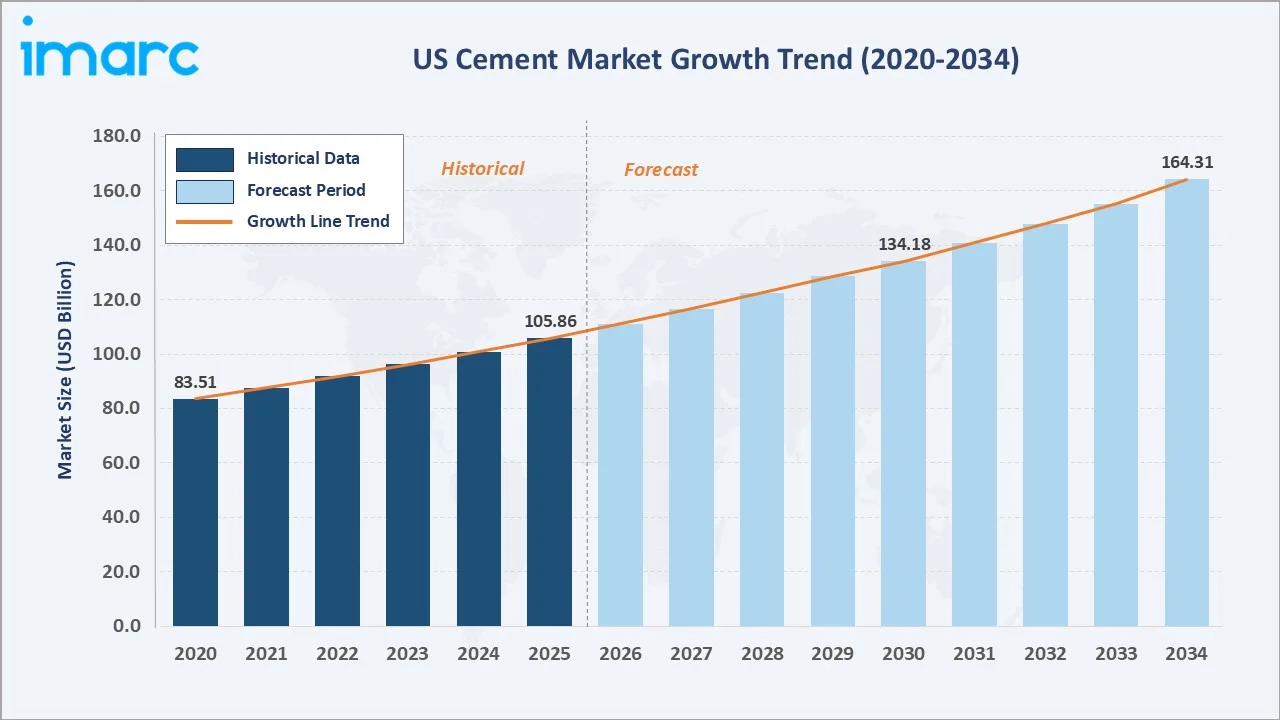

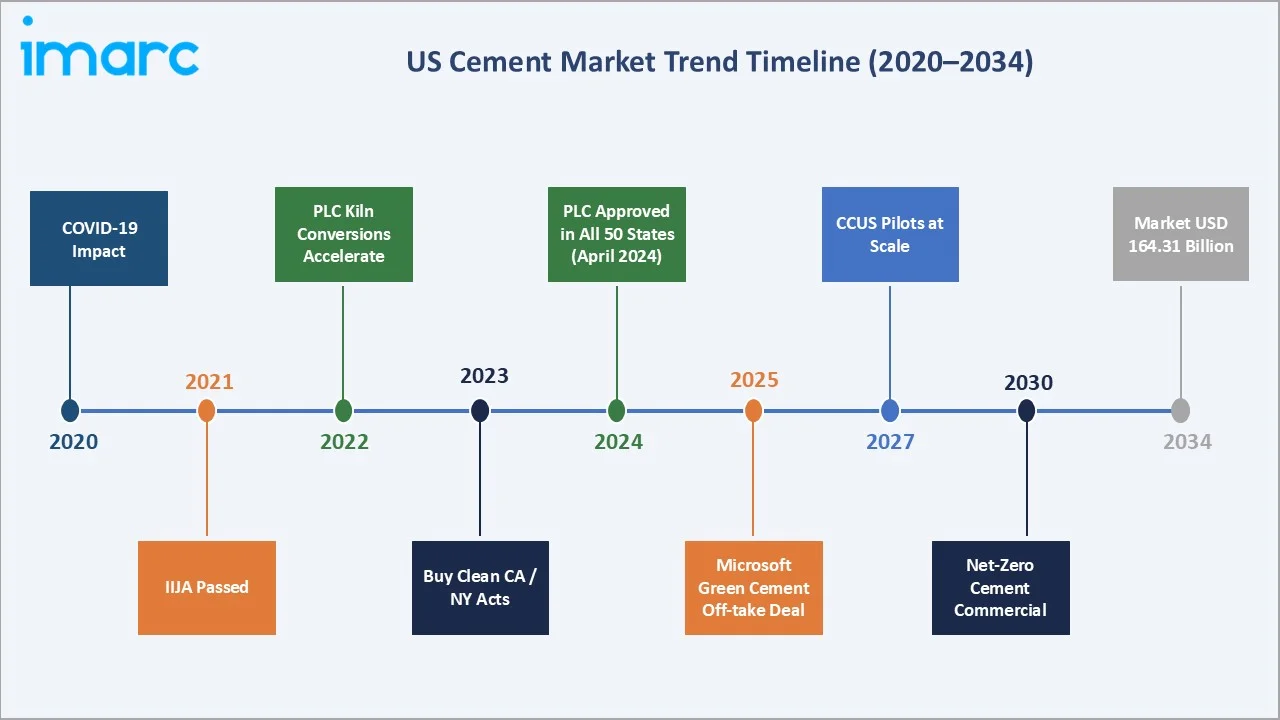

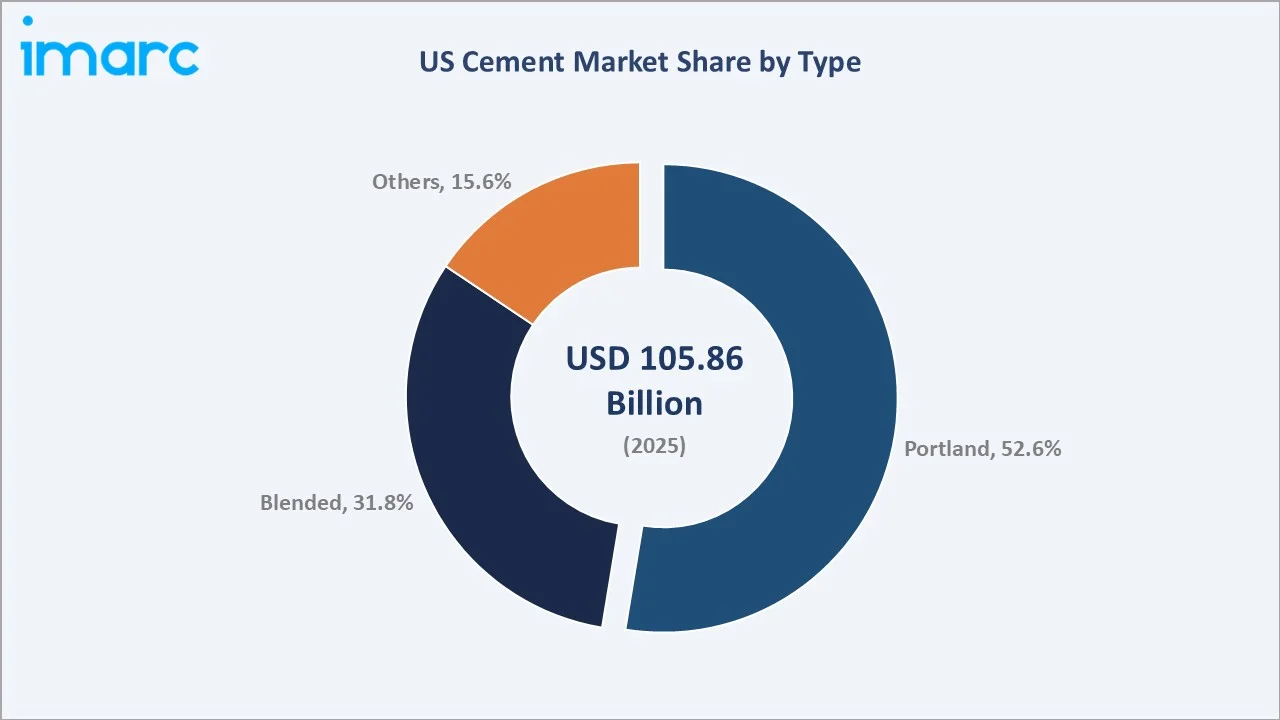

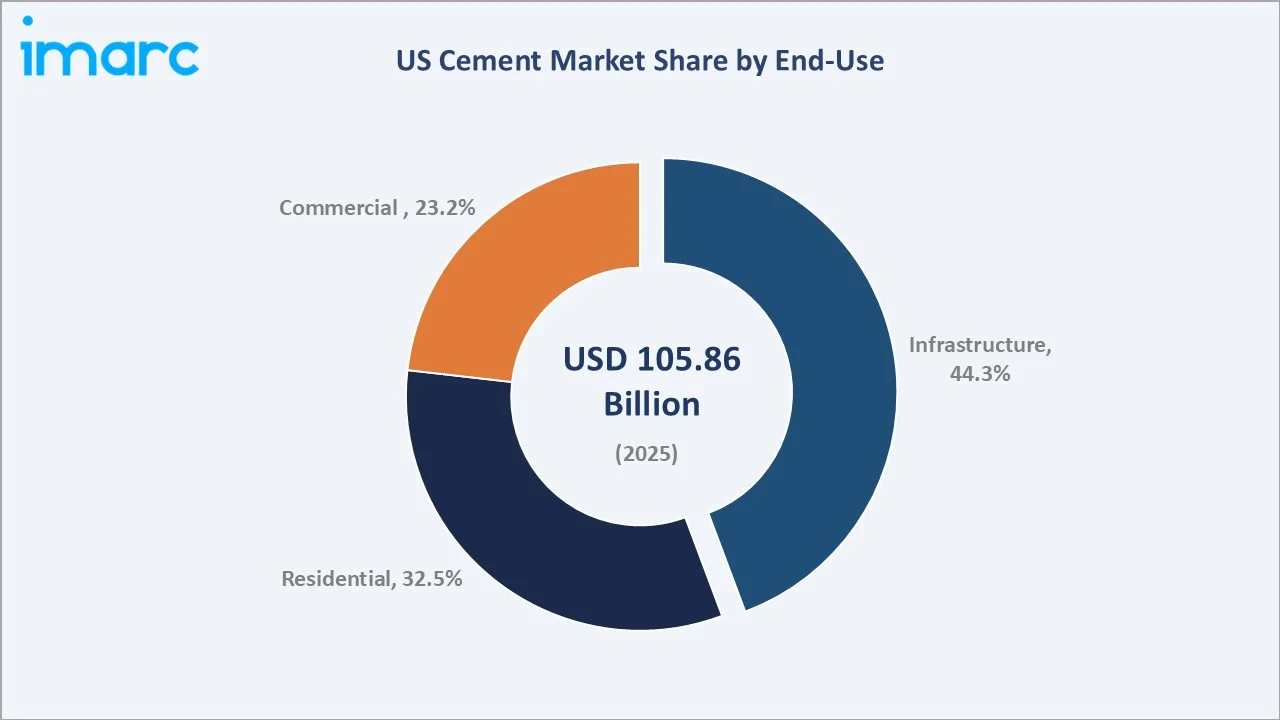

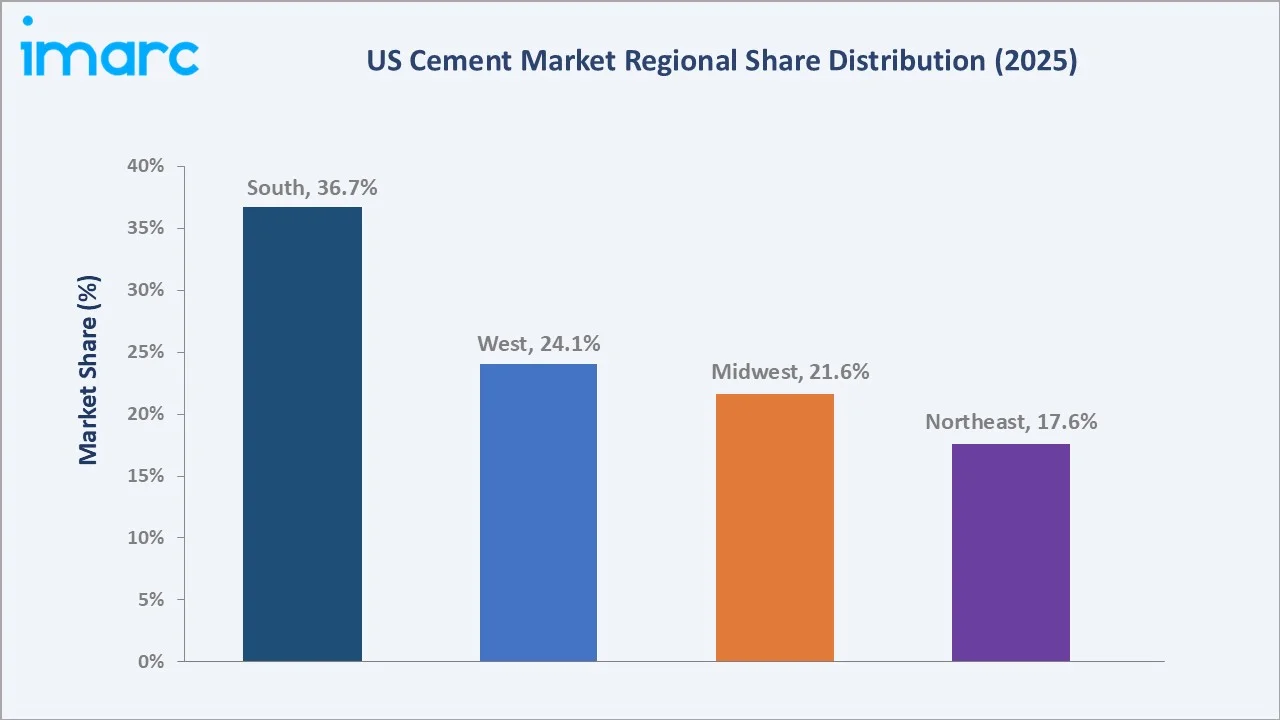

The US cement market size was valued at USD 105.86 Billion in 2025 and is projected to reach USD 164.31 Billion by 2034, exhibiting a CAGR of 4.86% during the forecast period 2026-2034. Historic federal infrastructure allocations under the Infrastructure Investment and Jobs Act (IIJA), a structural US housing deficit, rapid commercial and industrial construction, including data centers and semiconductor fabrication plants, and the accelerating adoption of Portland-limestone cement (PLC), now approved in all 50 US states, are driving the US cement market growth. Portland leads type-level demand at 52.6% in 2025, while the infrastructure end-use segment accounts for 44.3% of total consumption. The South dominates regionally with a 36.7% share, driven by year-round construction activity across Texas, Florida, and Georgia.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 105.86 Billion |

|

Forecast Market Size (2034) |

USD 164.31 Billion |

|

CAGR (2026-2034) |

4.86% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South (36.7% share, 2025) |

|

Fastest Growing Region |

South (∼5.1% CAGR) |

|

Leading Type |

Portland (52.6%, 2025) |

|

Leading End-Use |

Infrastructure (44.3%, 2025) |

To get more information on this market, Request Sample

The US cement market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by IIJA infrastructure disbursements, resilient residential construction, and accelerating Portland-limestone cement adoption across all 50 states.

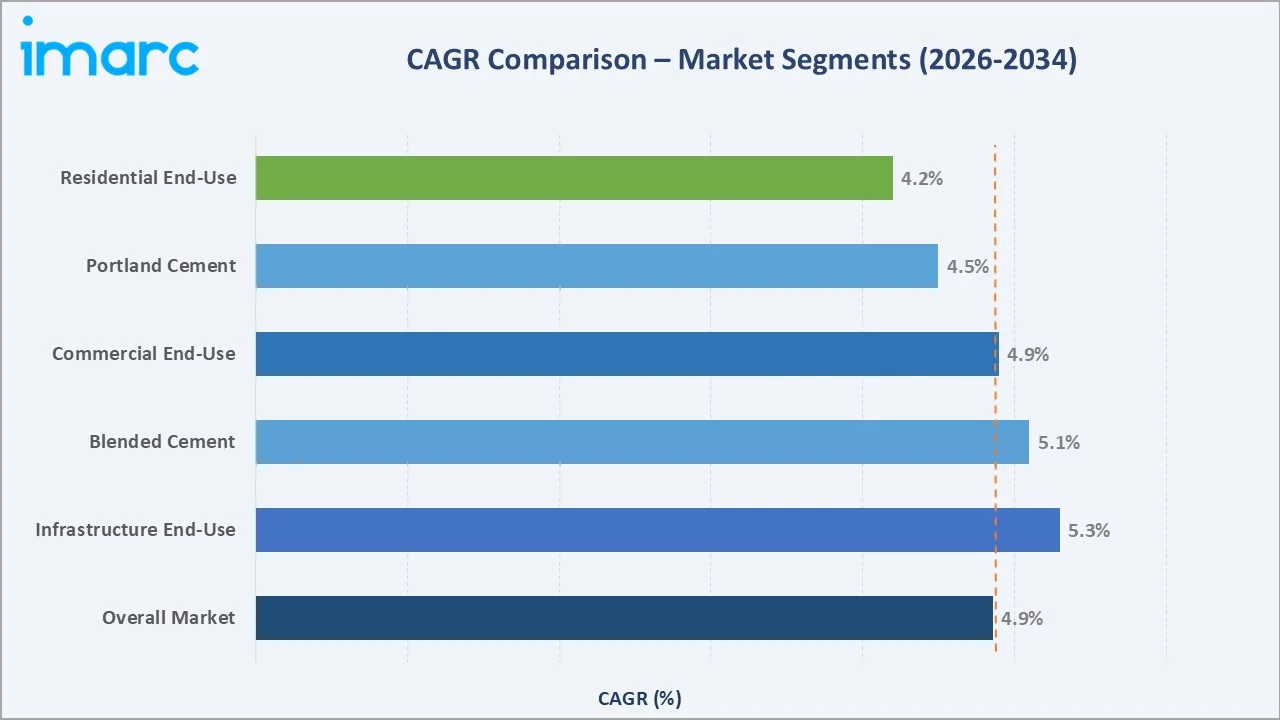

Segment-level CAGR comparisons highlighting blended and infrastructure end-use as the two fastest-growing sub-categories within the US cement market analysis through 2034, both exceeding the overall market CAGR of 4.86%.

Executive Summary

The US cement market is undergoing a structural demand expansion driven by the convergence of historic federal infrastructure investment, a population-driven housing shortfall, and accelerating diversification into sustainable low-carbon cement formulations. Valued at USD 105.86 Billion in 2025, the market is forecast to reach USD 164.31 Billion by 2034 at a CAGR of 4.86%. The Infrastructure Investment and Jobs Act (IIJA) provides USD 1.2 trillion in total appropriations, with approximately USD 500 billion allocated for roads, bridges, ports, and water systems—with only 40% disbursed as of September 2025, ensuring multi-year cement demand visibility.

Portland commands the dominant type-level share at 52.6% in 2025, reflecting its universal specification under ASTM C150 and ACI 318 standards. Blended at 31.8% is the fastest-growing type, driven by green public procurement mandates under the Federal Buy Clean Initiative, state-level EPD certification requirements in California and New York, and the capacity-expansion benefit of 10–15% additional output at PLC-converting plants without new kiln investment. Infrastructure accounts for 44.3% of total end-use demand, followed by residential at 32.5% and commercial at 23.2%.

The South leads regional consumption at 36.7%, anchored by Texas, the nation’s single largest cement-consuming state. Net imports accounted for 23% of US cement shipments in 2024, underscoring persistent domestic capacity constraints. The competitive landscape is moderately consolidated, led by Amrize Ltd, Heidelberg Materials AG, CEMEX, S.A.B. de C.V., CRH plc, and Buzzi Unicem S.p.A., with M&A activity accelerating as decarbonization priorities and digital logistics drive strategic realignment.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Portland – 52.6% share (2025) |

|

Fastest Growing Type |

Blended – ∼5.1% CAGR (2026-2034) |

|

Largest End-Use Segment |

Infrastructure – 44.3% share (2025) |

|

Leading Region |

South – 36.7% revenue share (2025) |

|

Second Largest Region |

West – 24.1% revenue share (2025) |

|

Top Companies |

Amrize, Heidelberg Materials, CEMEX USA, CRH (Ash Grove), Buzzi Unicem USA, Eagle Materials, GCC |

Key Analytical Observations Supporting The Above Data:

- Portland with 52.6% dominance in 2025 reflects universal ASTM C150 specification across structural concrete, highways, and bridge decks, with production clusters in Texas, Missouri, California, and Florida accounting for 43% of national output.

- Blended with 5.1% CAGR, the fastest-growing type is propelled by universal PLC adoption across all 50 states, Federal Buy Clean mandates, and state-level EPD procurement requirements, making lower-carbon cement a public project prerequisite.

- Infrastructure’s 44.3% end-use share reflects the structural impact of IIJA-funded highway, bridge, port, and water system projects.

- The South’s 36.7% regional dominance is underpinned by year-round construction activity, high population inflows to Texas, Florida, and Georgia, and key players’ US capacity expansion commitment for 2025.

- Net imports at 23% of 2024 shipments highlight persistent domestic capacity gaps, making import terminal access and port-side distribution a strategic competitive advantage for major producers serving coastal markets.

US Cement Market Overview

Cement is a hydraulic binding material produced by heating limestone and clay to form clinker, which is then ground with gypsum. It is the core input for concrete, mortar, and related construction materials, hardening through a chemical reaction with water to provide structural strength. In the U.S., key product types include ordinary Portland cement (OPC), Portland-limestone cement (PLC), blended cement with supplementary materials like fly ash and slag, and specialty variants for niche applications.

Cement demand spans all construction segments, including residential, commercial, infrastructure, and industrial projects, with the ready-mix concrete sector accounting for the majority of consumption. The U.S. production base is regionally concentrated, while domestic supply gaps sustain a structural reliance on imports, influencing pricing and supply chain strategies.

Market growth is supported by long-term infrastructure funding, persistent housing demand, and ongoing urban development in high-growth regions, creating a stable and diversified demand outlook for cement across end-use sectors.

Market Dynamics

To evaluate market opportunities, Request Sample

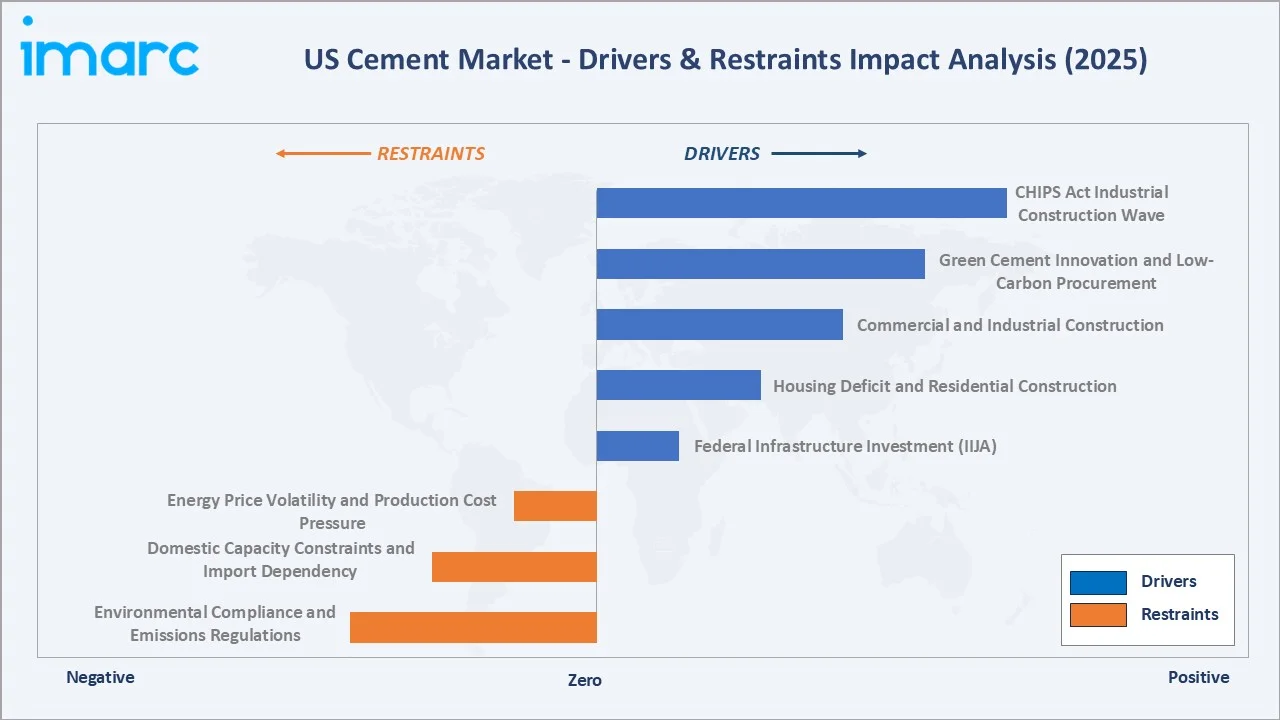

Market Drivers

- Federal Infrastructure Investment (IIJA): The Infrastructure Investment and Jobs Act (IIJA) provides a long-term, policy-backed demand pipeline for cement, supported by significant funding for transport and public infrastructure and a large backlog of upgrades.

- Housing Deficit and Residential Construction: A persistent housing shortage continues to support residential construction, sustaining steady cement consumption across single-family and multi-family projects.

- Commercial and Industrial Construction: Semiconductor fabs, data centers, and logistics hubs are creating a new, high-intensity demand segment, diversifying cement consumption beyond traditional cycles.

Market Restraints

- Environmental Compliance and Emissions Regulations: Stricter emissions standards are increasing compliance costs and extending timelines for plant upgrades and capacity expansion.

- Domestic Capacity Constraints and Import Dependency: Domestic production limitations and ongoing plant upgrades are sustaining reliance on imports, affecting supply stability.

Market Opportunities

- Green Cement Innovation and Low-Carbon Procurement: Green procurement mandates and corporate off-take agreements are accelerating demand for sustainable cement, creating premium growth opportunities.

- CHIPS Act Industrial Construction Wave: Semiconductor manufacturing investments are generating concentrated, long-term cement demand in key regions.

- Digital Supply Chain and Logistics Optimization: Adoption of digital supply chain platforms—such as those by Buzzi Unicem—is improving efficiency, reducing costs, and enhancing customer service.

Market Challenges

- Energy Price Volatility and Production Cost Pressure: High dependence on fuel makes cement production sensitive to energy price fluctuations, impacting margins.

- Import Competition and Pricing Pressure: Continued inflow of lower-cost cement from international markets creates pricing pressure, particularly in coastal regions.

Emerging Market Trends

1. Universal Adoption of Portland-Limestone Cement Redefining the Product Standard

Portland-limestone cement (PLC) is now the default cement type across the U.S., driven by nationwide regulatory approval, lower emissions, and the ability to increase plant capacity without major capital investment.

2. IIJA Multi-Year Disbursement Pipeline Creating Structural Demand Visibility

The Infrastructure Investment and Jobs Act is creating a stable, multi-year demand pipeline, enabling producers to align capacity expansion with sustained infrastructure spending.

3. Decarbonization and Green Procurement Mandates Reshaping Market Access

Green procurement regulations are making low-carbon cement a requirement for public projects, pushing companies toward acquisitions and partnerships to secure sustainable material supply chains.

4. M&A Consolidation Reshaping Industry Structure

M&A activity—led by players like CRH plc and Heidelberg Materials—is accelerating as scale, capital, and technology become critical for competitiveness.

5. Digital Supply Chain Integration Becoming a Competitive Imperative

Digital logistics and real-time tracking are becoming standard across the industry, with companies like Buzzi Unicem setting benchmarks for efficiency, cost optimization, and compliance.

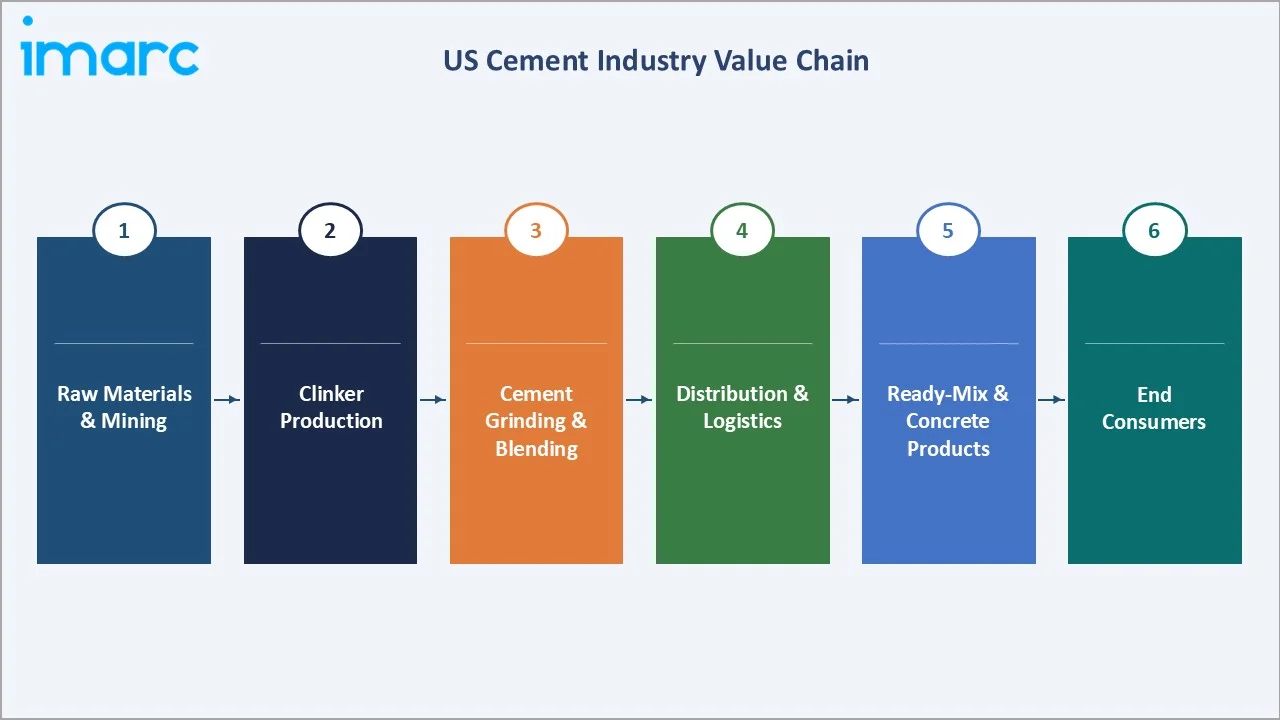

Industry Value Chain Analysis

The US cement industry value chain spans six integrated stages from raw material extraction through end-consumer project delivery. Each stage presents distinct competitive dynamics, margin profiles, and strategic investment requirements that shape the competitive positions of producers, distributors, and downstream concrete manufacturers.

|

Stage |

Key Players / Examples |

|

Raw Materials & Mining |

Limestone quarries, clay and shale mines, gypsum producers; key deposits in Texas, Missouri, California, Pennsylvania, and Alabama |

|

Clinker Production |

Amrize Ltd, Heidelberg Materials AG, CEMEX, S.A.B. de C.V., CRH plc, Buzzi Unicem S.p.A., Eagle Materials Inc., GCC, S.A.B. de C.V. |

|

Cement Grinding & Blending |

Integrated producers + independent grinding terminals; SCM suppliers (Eco Material Technologies, fly ash processors, slag cement from Nucor/US Steel) |

|

Distribution & Logistics |

Rail terminals, import terminals (Port of Houston, Port of Tampa, Port of Baltimore), bulk cement trucks, and regional distribution centers |

|

Ready-Mix & Concrete Products |

CRH Americas, Buzzi Unicem USA, regional ready-mix producers; precast, concrete block, pipe, and masonry product manufacturers |

|

End Consumers |

State DOTs, federal contractors (highway, bridge, dam), residential homebuilders, commercial developers, semiconductor and data center project owners |

Cement producers hold the highest strategic value in the U.S. value chain through vertically integrated operations spanning production, blending, and distribution. Control of import terminals is a key advantage in supply-constrained regions, while ongoing consolidation—highlighted by CRH plc’s acquisition of Eco Material Technologies—underscores the growing importance of owning low-carbon material supply chains as EPD requirements expand.

Technology Landscape in the US Cement Industry

Portland-Limestone Cement and Blended Formulation Technology

PLC (Type IL) is the most significant product shift in the U.S. cement market, enabling lower CO₂ emissions by incorporating limestone into clinker while maintaining structural performance standards. Its adoption is accelerating due to easy integration into existing grinding systems and the ability to boost plant capacity. Advanced blending with supplementary cementitious materials (SCMs) is further enhancing strength and durability, expanding use across applications.

Carbon Capture, Utilization, and Storage (CCUS)

Carbon capture is becoming essential for long-term decarbonization, as a large share of emissions comes from the calcination process. Government-backed pilot projects and private innovation are advancing deployment. Technologies like Fortera’s ReCarb and commercial agreements involving Sublime Systems highlight growing viability and demand for low-carbon cement solutions.

Digital Kiln Operations and Energy Efficiency Technology

AI-driven kiln optimization, advanced process controls, and digital twin models are improving energy efficiency and operational stability. At the same time, digital logistics platforms—such as those deployed by Buzzi Unicem—are enhancing supply chain visibility, reducing costs and emissions, and supporting compliance with increasingly stringent environmental product declaration (EPD) requirements.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Portland |

52.6% |

2025 |

|

End-Use |

Infrastructure |

44.3% |

2025 |

|

Region |

South |

36.7% |

2025 |

By Type

Portland commands a 52.6% majority share in 2025, reflecting its universal specification under ASTM C150 and ACI 318 standards across structural concrete, road, and bridge applications.

To access detailed market analysis, Request Sample

Blended at 31.8% in 2025 is the fastest-growing type segment, propelled by universal PLC adoption, green public procurement mandates, and corporate sustainability commitments. Others at 15.6% include specialty formulations: oil well cement for energy sector applications, masonry cement, rapid-hardening cement for cold-weather construction, and white cement for architectural and decorative applications.

By End-Use

Infrastructure dominates end-use demand at 44.3% in 2025, driven by IIJA-funded transportation projects, water system upgrades, and energy infrastructure. Infrastructure cement demand exhibits low cyclicality because government capital programs are multi-year appropriated commitments.

Residential construction holds a 32.5% share, sustained by the 4.7 million-unit housing deficit and single-family completions running at an annualized rate of 1,027,000 units in 2025. Each new single-family home requires approximately 20 tons of cement, providing a direct volume bridge between housing starts and cement shipments. Commercial construction at 23.2% is increasingly driven by data center development, semiconductor fabs, logistics hubs, and mixed-use urban infill projects, with industrial construction providing a growing structural demand layer independent of the residential cycle.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

36.7% |

Texas energy & residential boom, Florida/Georgia population inflows, IIJA highway allocations, Heidelberg EUR 1B expansion |

|

West |

24.1% |

California Buy Clean mandates, Arizona/Nevada semiconductor fabs, data center construction, green procurement leadership |

|

Midwest |

21.6% |

Ohio/Illinois industrial base, EV manufacturing retrofits, bridge rehabilitation under IIJA, and Missouri production proximity |

|

Northeast |

17.6% |

NY Low Embodied Carbon Act, urban infill & institutional construction, Heidelberg Giant Cement acquisition (New England) |

The South commands a 36.7% share, the largest regional market in the US, driven by year-round construction activity and the highest concentration of cement-intensive projects nationally. Texas is the single largest cement-consuming state, supported by energy sector infrastructure, industrial facility construction, and rapid population-driven residential development.

The West accounts for 24.1% of US cement consumption, with California’s Buy Clean California Act making the region the most advanced in green cement procurement. The Midwest (21.6%) is anchored by Ohio, Illinois, and Michigan’s industrial base, with EV manufacturing retrofits, bridge rehabilitation under IIJA, and Missouri’s cement production proximity reducing logistics costs for regional projects. The Northeast (17.6%) serves as the nation’s regulatory bellwether: New York’s Low Embodied Carbon Concrete Leadership Act and Connecticut’s PLC approval are setting procurement precedents diffusing westward.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Amrize Ltd |

ECOPlanet / PLC Portfolio |

Leader |

Spun off from Holcim (Jun 2025); largest North American building solutions company; 1,000+ sites |

|

Heidelberg Materials AG |

Green Cement / Giant Cement |

Leader |

US subsidiary of Heidelberg Materials AG (Germany) |

|

CEMEX, S.A.B. de C.V. |

CEMEX USA |

Leader |

6 US cement plants; developed-market strategic focus; sustainability portfolio |

|

CRH plc |

Ash Grove / Eco Material |

Leader |

Eco Material Technologies acquisition (Jul 2025) |

|

Buzzi Unicem S.p.A. |

Buzzi Unicem USA |

Challenger |

8 US cement plants; digital logistics platform launched Nov 2024; regional distribution strength |

|

Eagle Materials Inc. |

Eagle Materials |

Emerging |

specialty cement and wallboard products; regional market focus |

|

GCC, S.A.B. de C.V. |

GCC America |

Emerging |

Focused Mountain/West Texas markets |

The US cement competitive landscape is characterized by a small number of large integrated producers controlling the majority of domestic production capacity, distribution terminals, and key import gateway positions at Gulf Coast and Atlantic ports. M&A activity has intensified significantly in 2024–2025. GCC S.A.B. de C.V. invested USD 750 million to commission a new 3,000 t/day clinker line at its Odessa, Texas, plant in late 2025, significantly expanding its West Texas footprint. The competitive environment is increasingly shaped by EPD certification, green procurement compliance, and CCUS investment capability as prerequisites for federal and state project access.

Key Company Profiles

Amrize Ltd

Amrize Ltd operates over 1,000 sites with 19,000 employees across every US state and Canadian province. It is a separate, independent publicly traded company from its former parent, Holcim Ltd, which now focuses on Europe, Latin America, Australia, and North Africa.

- Product & Platform Portfolio: ECOPlanet low-carbon cement, Portland-limestone cement (PLC), Hydromedia permeable concrete, standard OPC and blended cement formulations, roofing and insulation systems, and building envelope solutions across North America.

- Recent Developments: In June 2025, Amrize debuted as an independent publicly traded company following the 100% spin-off from Holcim, with shares distributed one-for-one to Holcim shareholders.

- Strategic Focus: Focuses on North American growth by targeting infrastructure development, manufacturing onshoring, and housing demand, leveraging its wide network and low-carbon cement solutions to serve diverse construction segments.

Heidelberg Materials AG

Heidelberg Materials AG is a building materials producer, established in 1874 and headquartered in Heidelberg, Germany, with extensive US operations spanning cement production, aggregates, and ready-mix concrete across the Southeast, Midwest, and New England.

- Product & Platform Portfolio: Standard Portland cement, Portland-limestone cement, blended cements, masonry cement; operations across multiple US plants and distribution terminals, including newly acquired Giant Cement assets in the Southeast and New England.

- Recent Developments: In November 2024, Heidelberg Materials North America signed a definitive agreement to acquire Giant Cement Holding Inc. for USD 600 million, adding a cement plant, import terminals, distribution points, and an alternative fuel recycling business.

- Strategic Focus: Prioritizes expansion in high-growth U.S. regions, strengthening domestic production capacity, and advancing low-carbon cement offerings aligned with global sustainability frameworks.

CRH plc

CRH plc is a building materials group headquartered in Dublin, Ireland, and one of the most acquisitive players in the US cement and building materials market. Its US operations through Ash Grove Cement and Americas Materials span cement, aggregates, asphalt, and construction services across multiple regions.

- Product & Platform Portfolio: Ash Grove cement brands, near-zero-carbon cementitious materials via Eco Material Technologies (acquired July 2025), ready-mix concrete, aggregates, asphalt, and construction services.

- Recent Developments: In July 2025, CRH announced the acquisition of Eco Material Technologies to scale near-zero-carbon cementitious materials, providing a substantial supply of fly ash and other SCMs essential for lower-carbon blended cement production.

- Strategic Focus: Drives growth through acquisitions to build integrated materials platforms in the U.S., while advancing sustainability through low-carbon materials and alignment with green construction standards.

Market Concentration Analysis

The US cement market exhibits moderate-to-high concentration among top integrated producers. Amrize Ltd, Heidelberg Materials AG, CEMEX, S.A.B. de C.V., and CRH plc collectively control the substantial majority of domestic production capacity, distribution terminals, and key import gateway positions. This consolidation is driven by the capital intensity of kiln construction, the long asset life of cement plants (30–50 years), and the logistics advantages of owning both production and distribution infrastructure at scale.

The market is evolving into a bifurcated structure, with consolidation accelerating at the premium end as stringent sustainability requirements—such as carbon capture, certifications, and low-carbon material sourcing—demand significant capital and R&D, limiting participation to large players. At the same time, the import segment remains fragmented, with multiple international suppliers competing in supply-constrained regions, where competitive advantage is increasingly defined by digital supply chain capabilities and green certification rather than traditional scale and logistics alone.

Investment & Growth Opportunities

Fastest-Growing Segments

Blended cement, especially PLC (Type IL), is the fastest-growing segment, driven by regulatory acceptance, green procurement mandates, and its ability to increase output without major capital investment. Low-carbon cement within this category is gaining traction, supported by corporate off-take agreements that de-risk investment in green production.

Emerging Market Expansion

Semiconductor manufacturing and hyperscale data centers are creating new, high-intensity cement demand streams in key U.S. regions, reducing reliance on traditional residential and infrastructure cycles. Meanwhile, CCUS-enabled cement is emerging as a premium segment, supported by policy incentives and long-term procurement commitments.

Venture & Strategic Investment Trends

The sector is witnessing strong consolidation and sustainability-led investments, with major acquisitions by CRH plc and Heidelberg Materials, alongside growing funding for low-carbon technologies. Startups like Sublime Systems, Fortera, and Brimstone are attracting capital, highlighting increasing focus on next-generation green cement solutions.

Future Market Outlook (2026-2034)

The US cement market forecast projects steady value expansion from USD 105.86 Billion in 2025 to USD 164.31 Billion by 2034 at a CAGR of 4.86%, representing approximately 55% cumulative market value growth over the forecast horizon. This expansion is supported by sustained infrastructure spending, housing demand, and expanding commercial construction from semiconductor and data center projects.

Three structural shifts will reshape the market. First, decarbonization will divide producers, with EPD-certified, low-carbon players gaining access to government-funded projects under tightening green procurement rules. Second, import reliance may decline as domestic producers improve cost and carbon competitiveness through technologies like CCUS. Third, digital supply chain capabilities will become essential, with real-time tracking and digital certification emerging as standard requirements.

By 2034, the industry is expected to transition toward blended and low-carbon cement as the dominant product mix, with a competitive advantage defined by integrated capabilities across carbon reduction, material sourcing, certification, and digital logistics.

Research Methodology

Primary Research

Primary research included structured interviews with key U.S. cement stakeholders—plant operators, DOT officials, ready-mix buyers, contractors, sustainability experts, and investors—used to validate market size, segment shares, regional demand trends, technology adoption, and competitive positioning.

Secondary Research

Secondary sources include the US Geological Survey Mineral Commodity Summaries (January 2025), Portland Cement Association (PCA) forecasts and shipment data, US International Trade Commission import/export data, US Department of Transportation infrastructure spending data, American Society of Civil Engineers 2025 Report Card, National Ready Mixed Concrete Association market data, Zillow housing deficit analysis (July 2025), National Association of Homebuilders housing data, EPA and DOE regulatory publications, IIJA disbursement tracking data, and trade publications including Engineering News-Record, Concrete International, and PCA Market Intelligence reports.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, construction spending indices, population and urbanization data, infrastructure investment disbursement schedules, housing starts and completions data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty, regulatory change, energy price volatility, and import competition dynamics.

US Cement Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Blended, Portland, Others |

| End-Uses Covered | Residential, Commercial, Infrastructure |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Amrize Ltd, Heidelberg Materials AG, CEMEX, S.A.B. de C.V., CRH plc, Buzzi Unicem S.p.A., Eagle Materials Inc., GCC, S.A.B. de C.V., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the US cement market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the US cement market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the US cement industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the US Cement Market Report

The US cement market was valued at USD 105.86 Billion in 2025, supported by strong infrastructure investment under the IIJA, resilient residential construction driven by a 4.7 million-unit housing deficit, and growing commercial and industrial construction demand.

The market is projected to reach USD 164.31 Billion by 2034, growing at a CAGR of 4.86% during 2026-2034, driven by IIJA infrastructure disbursements, housing deficit recovery, and industrial construction from CHIPS Act-funded semiconductor fabs and data center development.

Portland leads with a 52.6% share in 2025, driven by its universal specification under ASTM C150 and ACI 318 standards for structural concrete, roads, and bridges across all US construction sectors.

Infrastructure dominates with a 44.3% share in 2025, reflecting IIJA-funded highway, bridge, port, and water system projects.

The South currently dominates the US cement market with a 36.7% share in 2025.

Key drivers include the CHIPS Act-funded semiconductor fab construction, data center development, and accelerating universal adoption of Portland-limestone cement, now approved across all 50 states.

Blended is the fastest-growing type segment, projected at approximately 5.1% CAGR through 2034, driven by universal PLC adoption, Federal Buy Clean mandates, and state-level EPD procurement requirements in California and New York.

Leading companies include Amrize Ltd, Heidelberg Materials AG, CEMEX, S.A.B. de C.V., CRH plc, Buzzi Unicem S.p.A., Eagle Materials Inc., and GCC, S.A.B. de C.V.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)