United States Diabetes Market Size, Share, Trends and Forecast by Segment and Ditribution Channel, 2026-2034

United States Diabetes Market Size, Share, Trends & Forecast (2026-2034)

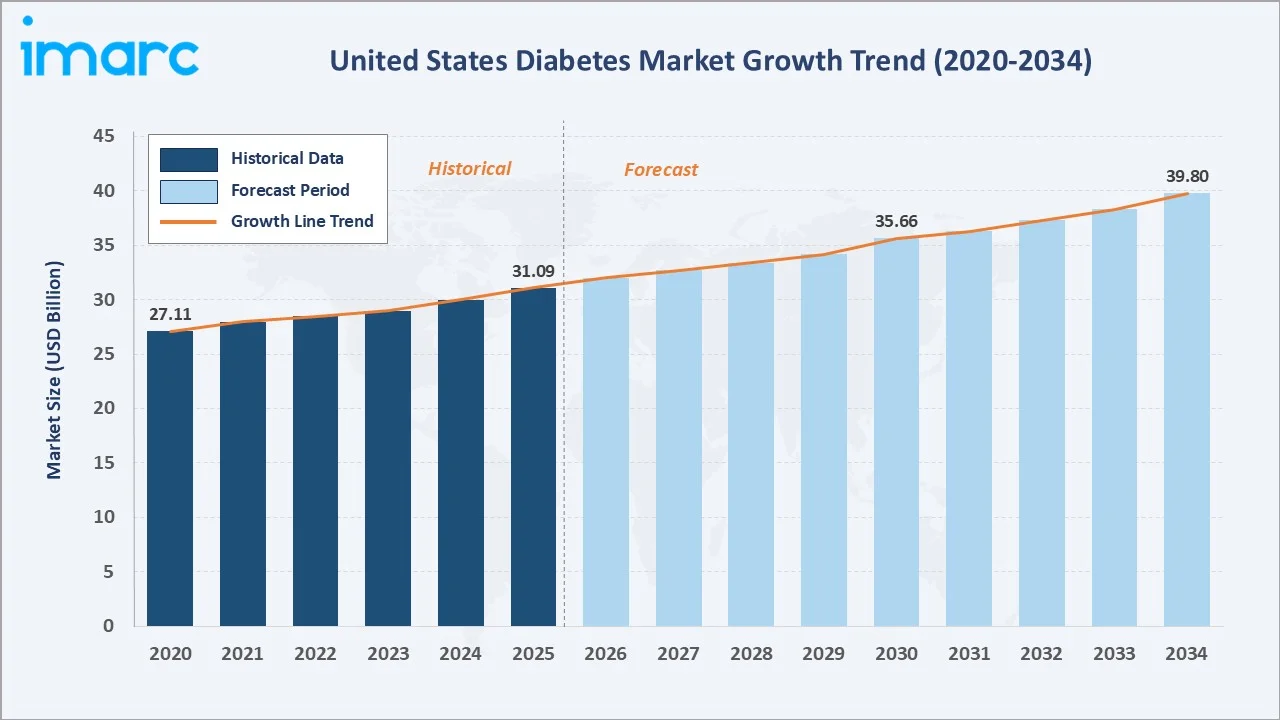

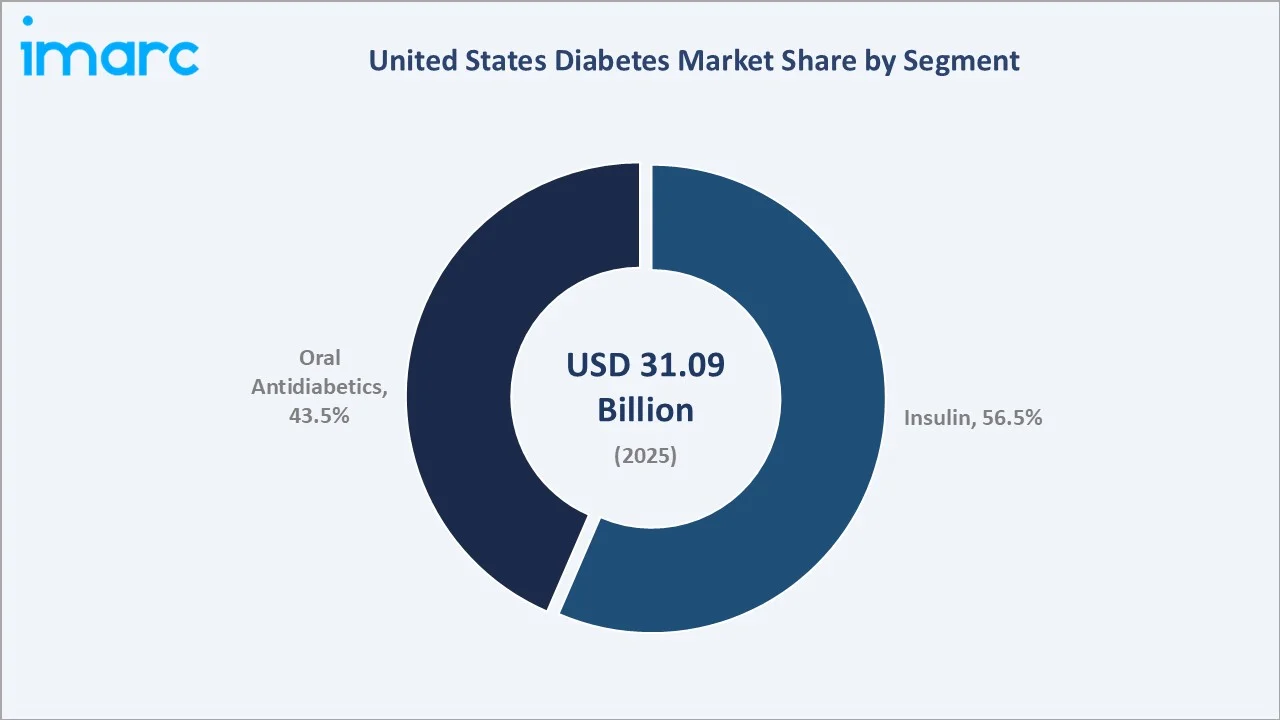

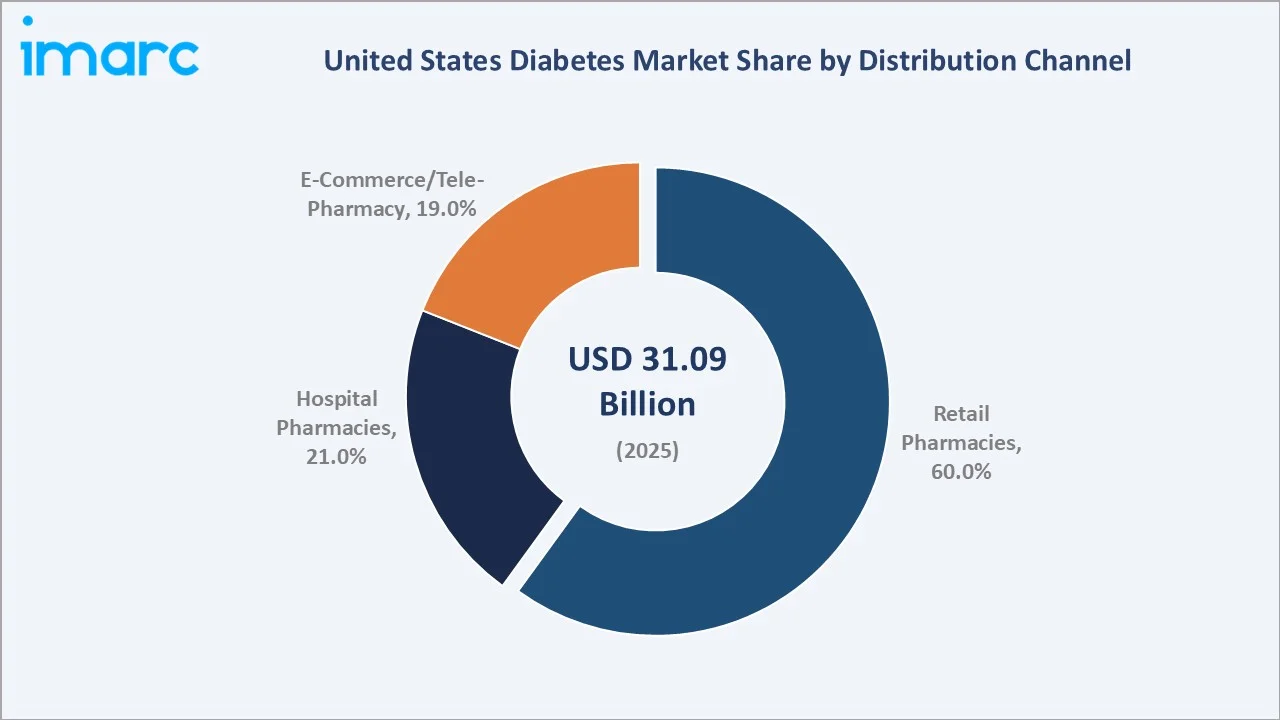

The United States diabetes market reached USD 31.09 Billion in 2025 and is projected to reach USD 39.80 Billion by 2034, growing at a CAGR of 2.78% during 2026-2034. The United States diabetes market is driven by the high prevalence of diabetes, rising obesity rates, growing adoption of advanced therapies and technologies, and increasing healthcare expenditure. More than 40 million Americans, or 12% of the population, are living with diabetes. Insulin dominates at 56.5% segment share, and retail pharmacies lead the distribution channel at 60.0%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 31.09 Billion |

|

Forecast Market Size (2034) |

USD 39.80 Billion |

|

CAGR (2026-2034) |

2.78% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Segment |

Insulin (56.5%, 2025) |

|

Largest Distribution Channel |

Retail Pharmacies (60.0%, 2025) |

The market expanded from USD 27.11 Billion in 2020 to USD 31.09 Billion in 2025, anchored at USD 35.66 Billion in 2030, and forecast to reach USD 39.80 Billion by 2034. The GLP-1 agonist class is the single most transformative pharmaceutical development in US diabetes care history, redirecting treatment paradigms, market share, and patient outcomes simultaneously.

To get more information on this market, Request Sample

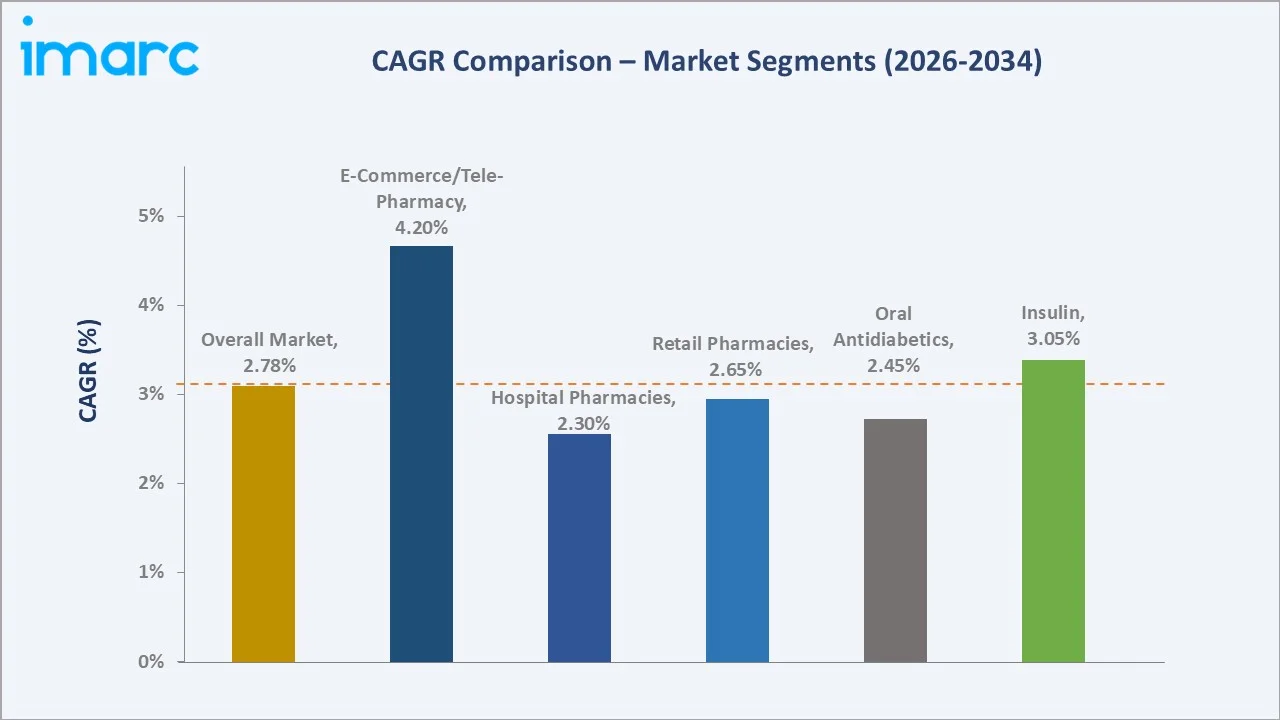

E-commerce/tele-pharmacy grows fastest at ~4.2% CAGR (2026-2034), driven by US retail expansion. Insulin grows at ~3.05% CAGR, outpacing oral antidiabetics at ~2.45%, as GLP-1 injectable agonists and biosimilar analogs together sustain premium revenue growth, offsetting brand insulin price compression from the IRA's negotiation framework.

Executive Summary

The United States diabetes market reached USD 31.09 Billion in 2025, the world's largest national diabetes pharmaceutical market by value. The US combines the highest absolute patient count among developed nations, premium branded insulin pricing, and the world's most advanced GLP-1 agonist commercial market. The market grows at 2.78% CAGR to USD 39.80 Billion by 2034, reflecting the interplay of premium GLP-1/GIP drug expansion against IRA drug price negotiation compression on established brands.

Insulin leads at 56.5% market share (2025), anchored by the premium basal analog franchise and the explosive GLP-1 injectable agonist category. Oral antidiabetics at 43.5% are led by the growth of SGLT-2 inhibitors, partly offsetting DPP-4 inhibitor revenue erosion from generic competition. Retail pharmacies dominate at 60.0% of distribution; E-commerce/tele-pharmacy at 19.0% is the fastest-growing channel.

Key Market Insights

|

Insight |

Data |

|

Largest Segment |

Insulin - 56.5% share (2025) |

|

Leading Distribution Channel |

Retail Pharmacies - 60.0% share (2025) |

Key Analytical Observations Supporting the Above Data:

- Insulin at 56.5% (2025), driven by GLP-1 injectable agonist explosive growth: The insulin segment encompasses GLP-1 receptor agonists alongside traditional basal and bolus insulins.

- Retail pharmacies at 60.0%: Retail pharmacies dominate the market by distribution channel due to their widespread accessibility, strong insurance network integration, and convenient access to prescription refills, over-the-counter products, and diabetes management services.

United States Diabetes Market Overview

The United States diabetes market encompasses all pharmaceutical treatments, insulin delivery systems, and monitoring solutions for type-1, type-2, and gestational diabetes patients. The ecosystem integrates biologic API manufacturers, branded and biosimilar pharmaceutical companies, wholesale distributors, and retail/hospital/e-pharmacy dispensing channels serving diagnosed patients.

The market operates under FDA regulation, and the insurance coverage is under Medicare and Medicaid. The macroeconomic factors include high healthcare spending, rising diabetes cases with rising urban lifestyles, rising insurance coverage, increasing disposable income, and an aging population contributing to greater demand for diabetes care.

Market Dynamics

To evaluate market opportunities, Request Sample

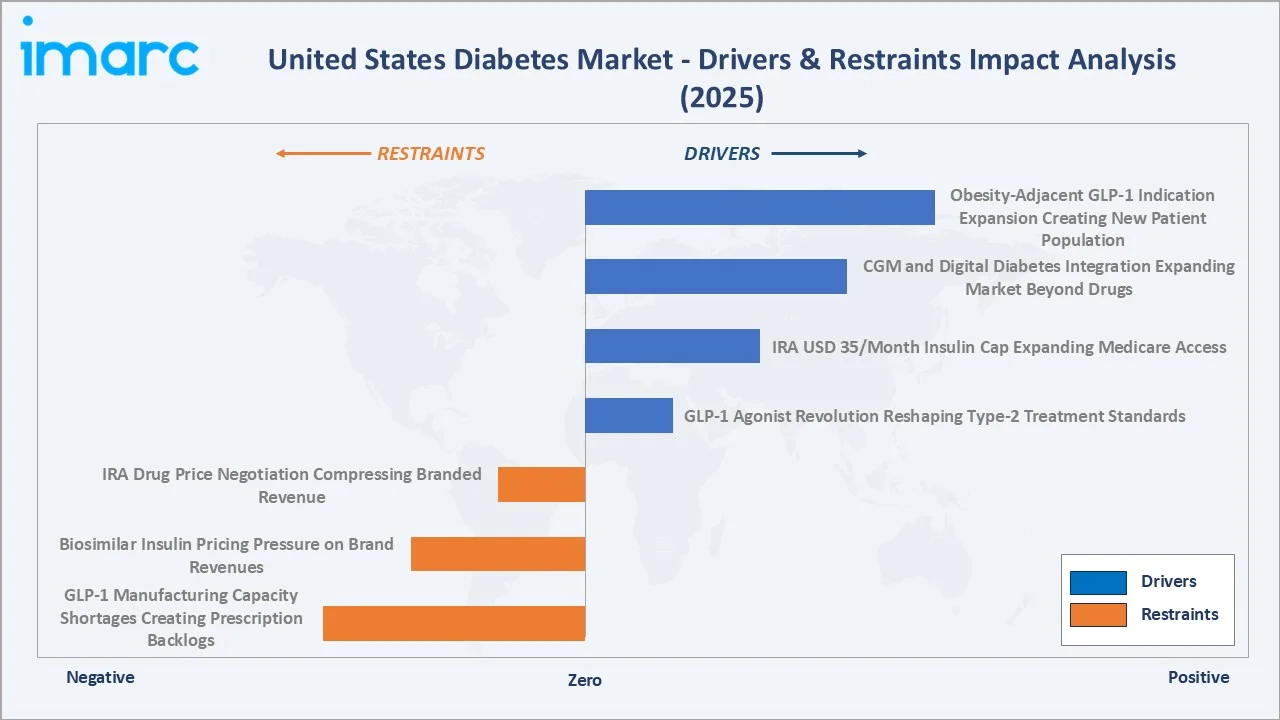

Market Drivers

- GLP-1 Agonist Revolution Reshaping Type-2 Treatment Standards: In December 2024, the U.S. FDA approved the first generic version of Victoza (18 mg/3 mL), a GLP-1 receptor agonist used to improve glycemic control in adults and children aged 10 and above with type 2 diabetes, alongside diet and exercise. The GLP-1 agonists are to be used as second-line therapy in all Type-2 patients with cardiovascular or kidney disease risk, expanding the FDA-approved prescribing population.

- IRA USD 35/Month Insulin Cap Expanding Medicare Access: The Inflation Reduction Act's insulin out-of-pocket cap for Medicare Part D beneficiaries, USD 35/month regardless of quantity, reduced cost barriers for insulin-dependent Medicare patients.

- CGM and Digital Diabetes Integration Expanding Market Beyond Drugs: Continuous glucose monitoring systems are expanding the US diabetes management market beyond pharmaceuticals.

Market Restraints

- IRA Drug Price Negotiation Compressing Branded Revenue: The IRA's Medicare Drug Price Negotiation Program (MPNP) selected 10 drugs for 2026 price negotiation. Negotiated prices effective January 2026 will reduce Medicare reimbursement for some drugs, compressing manufacturer revenues from the Medicare segment.

- Biosimilar Insulin Pricing Pressure on Brand Revenues: Biosimilar insulin intensifies price competition, reducing revenues and margins for branded drug manufacturers. This pricing pressure can limit profitability, constrain R&D investments, and slow innovation in the U.S. diabetes market.

Market Opportunities

- Obesity-Adjacent GLP-1 Indication Expansion Creating New Patient Population: Wegovy (semaglutide 2.4mg) and Zepbound (tirzepatide obesity indication) received FDA approvals for chronic weight management, creating an adjacent patient population of obese Americans potentially eligible for GLP-1 therapy.

- Once-Weekly Basal Insulin Products: In March 2026, Novo Nordisk received approval from the U.S. Food and Drug Administration for Awiqli (insulin icodec-abae) 700 units/mL, the first once-weekly long-acting basal insulin for improving glycemic control in adults with type 2 diabetes alongside diet and exercise. Once-weekly dosing addresses the primary adherence barrier in insulin therapy, potentially creating a market opportunity.

Market Challenges

- GLP-1 Manufacturing Capacity Shortages Creating Prescription Backlogs: GLP-1 manufacturing capacity shortages create supply constraints, leading to prescription delays and limited patient access to critical therapies. This disrupts treatment continuity and restricts market growth despite strong demand in the U.S. diabetes market.

- Medicare GLP-1 Coverage Gaps Limiting Access for 65+ Population: Despite Ozempic's clinical cardiovascular benefits (SELECT trial), Medicare Part D does not cover GLP-1 agonists prescribed exclusively for weight management, creating coverage gaps for obese Medicare patients with multiple cardiometabolic risk factors.

Emerging Market Trends

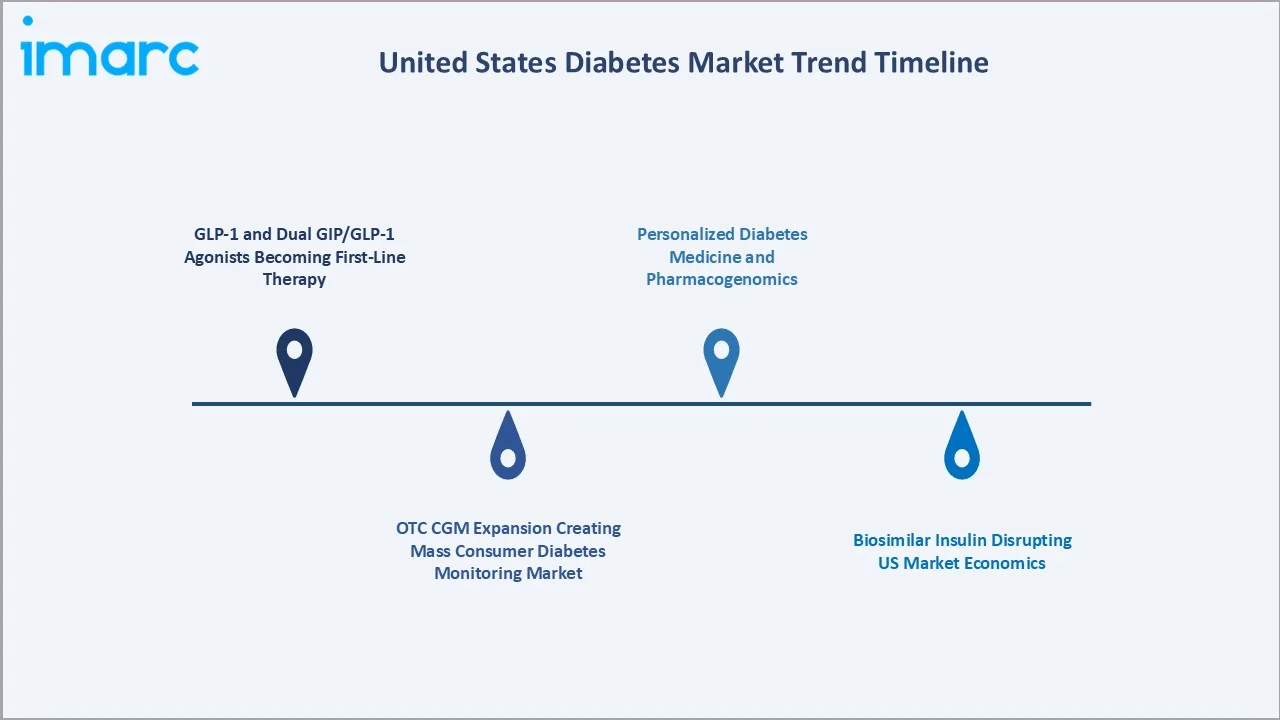

1. GLP-1 and Dual GIP/GLP-1 Agonists Becoming First-Line Therapy

The US diabetes treatment algorithm has undergone its most significant shift in two decades. GLP-1 and dual GIP/GLP-1 agonists are emerging as first-line therapy due to their superior glycemic control, weight loss benefits, and cardiovascular risk reduction, shifting treatment guidelines and physician preference away from traditional therapies toward advanced incretin-based options.

2. OTC CGM Expansion Creating Mass Consumer Diabetes Monitoring Market

OTC CGM expansion is emerging as a key trend in the U.S. diabetes market by enabling easier, prescription-free access to continuous glucose monitoring, driving adoption among prediabetic and wellness-focused consumers and expanding the market beyond traditional insulin-dependent patients.

3. Biosimilar Insulin Disrupting US Market Economics

Biosimilar insulin is intensifying price competition, lowering treatment costs, and improving patient access to insulin therapies. It is also reshaping payer strategies and accelerating the shift toward cost-efficient diabetes management solutions across healthcare systems.

4. Personalized Diabetes Medicine and Pharmacogenomics

Personalized diabetes medicine and pharmacogenomics are gaining traction by enabling treatment plans tailored to an individual’s genetic profile, improving drug efficacy and reducing adverse effects. This approach supports more precise therapy selection, enhances patient outcomes, and drives the shift toward data-driven, patient-centric diabetes care.

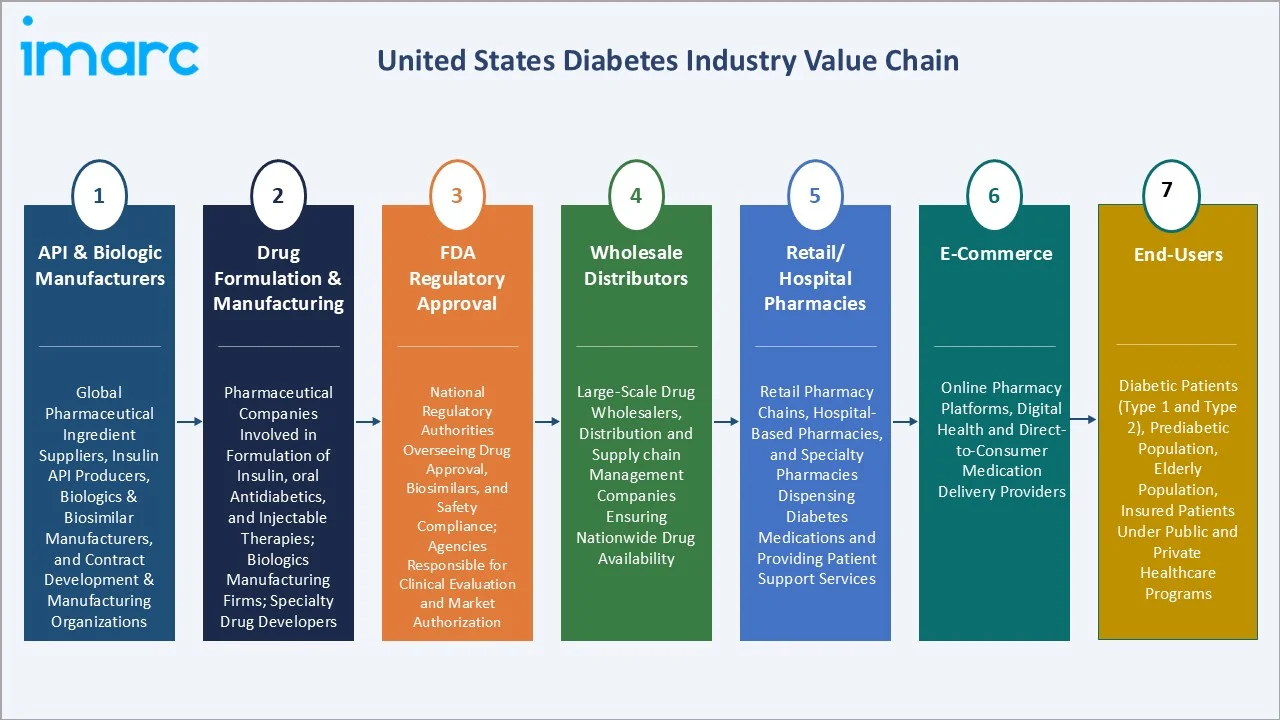

Industry Value Chain Analysis

The US diabetes market value chain integrates API biologic manufacturing through pharmaceutical production, FDA regulatory approval, wholesale distribution, and retail/hospital/e-pharmacy dispensing, serving diagnosed patients under Medicare, Medicaid, and commercial insurance coverage frameworks. PBMs control formulary access for 90%+ of insured Americans, making PBM relationships as critical as FDA approval for commercial market success.

|

Stage |

Key Participants |

|

API & Biologic Manufacturers |

Global pharmaceutical ingredient suppliers, insulin API producers, biologics and biosimilar manufacturers, and contract development and manufacturing organizations |

|

Drug Formulation & Manufacturing |

Pharmaceutical companies involved in the formulation of insulin, oral antidiabetics, and injectable therapies, biologics manufacturing firms, and specialty drug developers |

|

FDA Regulatory Approval |

National regulatory authorities overseeing drug approval, biosimilars, and safety compliance, and agencies responsible for clinical evaluation and market authorization |

|

Wholesale Distributors |

Large-scale drug wholesalers, distribution and supply chain management companies ensure nationwide drug availability |

|

Retail / Hospital Pharmacies |

Retail pharmacy chains, hospital-based pharmacies, and specialty pharmacies dispensing diabetes medications and providing patient support services |

|

E-Commerce |

Online pharmacy platforms, digital health and direct-to-consumer medication delivery providers |

|

End Users |

Diabetic patients (type 1 and type 2), prediabetic population, elderly population, insured patients under public and private healthcare programs |

US pharmaceutical manufacturers capture 50-65% gross margins on branded GLP-1 agonists and insulin analogs. Wholesale distributors operate on 1-2% margins. Retail pharmacies earn 3-5% dispensing margins.

Technology Landscape in the United States Diabetes Industry

GLP-1 and Dual GIP/GLP-1 Receptor Agonist Drug Platforms

GLP-1 and dual GIP/GLP-1 receptor agonist platforms represent a major shift in the US diabetes technology landscape, integrating advanced incretin biology with long-acting formulations to deliver superior glycemic control, weight loss, and cardiovascular benefits. Their rapid adoption is driving innovation in drug delivery systems (e.g., weekly dosing, injectables, and oral formats) and redefining treatment standards across the diabetes care continuum.

Continuous Glucose Monitoring (CGM) Technology

CGM technology has evolved from intermittent flash monitoring (FreeStyle Libre 2) to real-time continuous monitoring (Dexcom G7, Libre 3) to factory-calibrated systems requiring zero fingerstick calibrations.

Digital Health and Telehealth Integration

Digital health and telehealth integration are reshaping the diabetes technology landscape by enabling continuous remote monitoring, virtual consultations, and real-time data sharing between patients and providers. This ecosystem, powered by connected devices, mobile apps, and AI analytics, supports proactive disease management, improves adherence, and enhances clinical decision-making.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Segment | Insulin | 56.5% | 2025 |

| Distribution Channel | Retail Pharmacies | 60.0% | 2025 |

By Segment

Insulin leads at 56.5% market share (2025). The insulin segment encompasses traditional basal analogs, rapid-acting analogs, biosimilar insulins, premixed formulations, and GLP-1 receptor agonists. In February 2025, the FDA approved Merilog (insulin-aspart-szjj) as a biosimilar to Novolog (insulin aspart) for the improvement of glycemic control in adults and pediatric patients with diabetes mellitus.

To access detailed market analysis, Request Sample

Oral antidiabetics at 43.5% are anchored by SGLT-2 inhibitors, DPP-4 inhibitors, and metformin. The oral segment grows with SGLT-2 inhibitors' cardiorenal indication expansion, offsetting DPP-4 revenue erosion.

By Distribution Channel

Retail pharmacies lead at 60.0% market share (2025). Retail pharmacies lead the market due to their extensive nationwide presence, easy accessibility, and integration with insurance and PBM networks. They provide convenient access to medications, diabetes supplies, and patient support services, driving high prescription volumes.

Hospital pharmacies at 21.0% serve inpatient diabetes management for hospitalized patients. E-commerce/tele-pharmacy at 19.0% grows fastest at ~4.2% CAGR, driven by Amazon Pharmacy, Cost Plus Drugs, GoodRx, and PBM mail-order programs offering supply convenience.

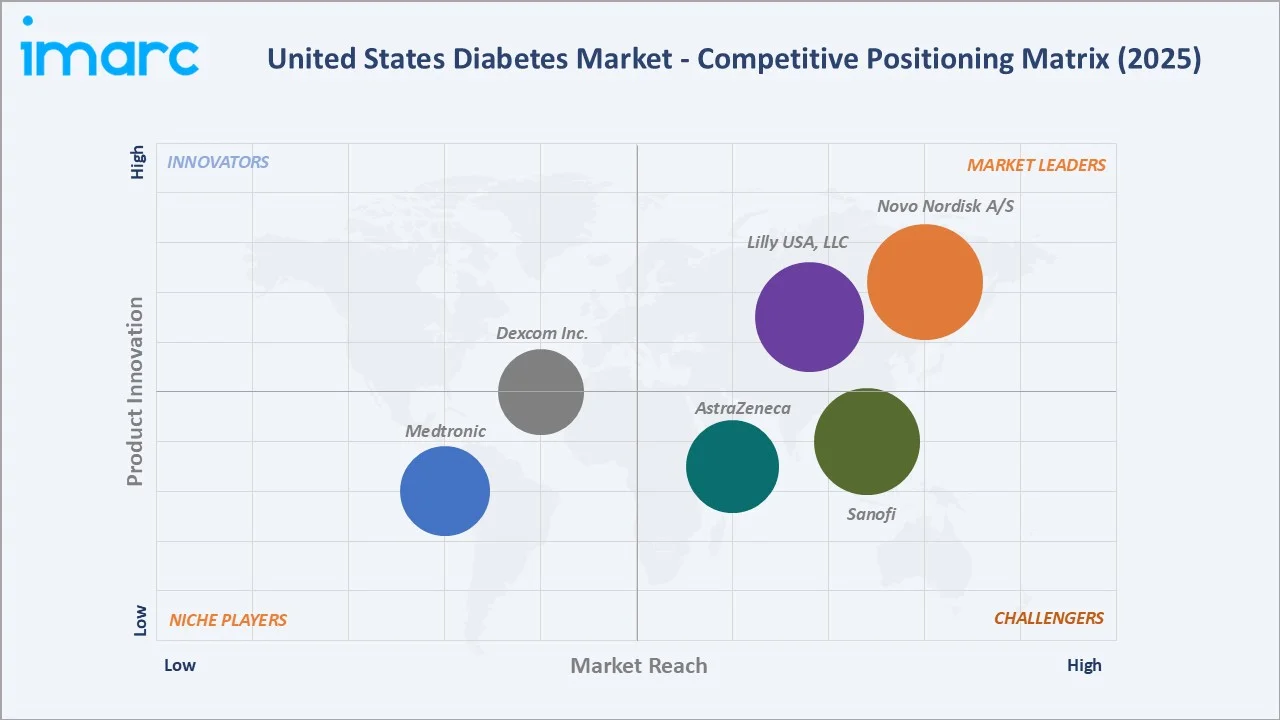

Competitive Landscape

The US diabetes pharmaceutical market is moderately concentrated at the branded drug level and highly fragmented in the generic oral antidiabetic segment. Novo Nordisk and Lilly USA together captured approximately 45-50% of US diabetes pharmaceutical revenues (2025), driven by their combined GLP-1 agonist franchise dominance.

|

Company Name |

Brand / Product |

Market Position |

Core Strength |

|

Novo Nordisk A/S |

Ozempic, Rybelsus, Victoza, Awiqli, Fiasp, Tresiba |

Market Leader |

One of the world's largest diabetes companies |

|

Lilly USA, LLC |

Basaglar, Glyxambi, Humalog, Humulin, Jardiance |

Market Leader |

Strong innovation in advanced diabetes therapies, supported by robust R&D capabilities and a well-established product portfolio |

|

Sanofi |

Toujeo, Lantus, Soliqua, Admelog, Amaryl |

Strong Challenger |

Strong presence in long-acting insulin therapies, supported by a broad diabetes portfolio and extensive global manufacturing and distribution capabilities. |

|

AstraZeneca |

Farxiga, Kombiglyze XR, Onglyza |

Strong Challenger |

Strong position in oral diabetes therapies |

|

Medtronic |

InPen Smart Insulin Pen, MiniMed 780G Insulin Pump, Smart MDI |

Niche Player |

Closed-loop insulin delivery pioneer; MiniMed 780G advanced hybrid closed-loop system |

|

Dexcom Inc. |

Dexcom G7, Stelo Glucose Biosensor |

Established Player |

Since 1999, Dexcom has been developing innovative technology that has transformed how people manage diabetes and track their glucose. |

The competitive landscape's center of gravity has permanently shifted from insulin analogs to GLP-1 agonists and next-generation cardiometabolic therapies. Biosimilar insulin manufacturers are disrupting traditional insulin revenue streams. CGM and digital health companies are capturing 8-10% of total US diabetes market revenues (2025), a share growing at 12-15% CAGR as monitoring technology becomes standard diabetes care infrastructure.

Key Company Profiles

Novo Nordisk A/S

Novo Nordisk is one of the world's most valuable pharmaceutical companies by market capitalization and the US diabetes market's undisputed revenue leader.

- Product Portfolio: Ozempic, Rybelsus, Victoza, Awiqli, Fiasp, Tresiba.

- Recent Developments: In March 2026, Novo Nordisk received US Food and Drug Administration (FDA) approval for Awiqli (insulin icodec-abae) injection 700 units/mL, the first and only once-weekly, long-acting basal insulin, indicated as an adjunct to diet and exercise to improve glycemic control (blood sugar) in adults living with type 2 diabetes.

- Strategic Focus: Focus on expanding leadership in advanced diabetes therapies, scaling manufacturing capacity, and strengthening access through pricing strategies and broad patient reach.

Lilly USA, LLC

Lilly USA, LLC achieved one of the fastest pharmaceutical commercial launches in US history with Mounjaro (tirzepatide).

- Product Portfolio: Basaglar, Glyxambi, Humalog, Humulin, Jardiance.

- Recent Developments: In February 2026, Eli Lilly and Company released detailed findings from the Phase 3 ACHIEVE-3 trial, comparing the safety and efficacy of orforglipron, an oral small-molecule GLP-1 therapy without food or water restrictions, against oral semaglutide in adults with type 2 diabetes inadequately managed on metformin.

- Strategic Focus: Focus on advancing innovative diabetes therapies, expanding manufacturing capacity, and strengthening market access to enhance patient reach and treatment outcomes in the market.

Market Concentration Analysis

The US diabetes market exhibits strong concentration at the branded GLP-1 agonist level and high fragmentation in oral antidiabetic generics. Novo Nordisk and Lilly USA together hold approximately 45-50% of total US diabetes pharmaceutical revenues (2025), a concentration unprecedented in the market's history.

The oral antidiabetic segment is highly fragmented, holding the remaining oral market share. No single oral antidiabetic drug exceeds 15% of the oral antidiabetic market. Consolidation trends include Novo Nordisk and Eli Lilly's manufacturing expansion, creating a health IT-pharmaceutical integration pathway. The biosimilar insulin entry is fragmenting the previously concentrated basal insulin market, representing a structural market share shift that will compound through 2034.

Investment & Growth Opportunities

Fastest Growing Segments

E-commerce/tele-pharmacy (~4.2% CAGR), OTC CGM market (~35-40% CAGR from small base), GLP-1 agonist class (~8-10% class CAGR within insulin segment), oral GLP-1 agonists (~25%+ CAGR), and closed-loop insulin delivery systems (~15% CAGR) represent the US diabetes market's highest-growth investment vectors through 2034. Oral GLP-1 agonists represent the single largest untapped pharmaceutical opportunity.

Emerging Market Opportunities

The US pre-diabetic population represents a pharmacological prevention opportunity; metformin's demonstrated high type-2 diabetes prevention in the DPP trial suggests a pre-diabetes pharmacotherapy market if guideline adoption accelerates. GLP-1 agonists' weight loss benefits in pre-diabetics could create a prevention indication, adding potential US GLP-1 patients beyond existing type-2 prescriptions.

Investment Themes

- OTC CGM consumer platform development: Companies building consumer digital health platforms integrating OTC CGM data with nutrition, exercise, and medication coaching are positioned for 30-40% CAGR growth.

- Oral GLP-1 agonist development: Oral GLP-1 agonist development represents the next wave of type-2 diabetes innovation. Oral GLP-1 agonists removing injection barriers for most of the type-2 patients refusing injectable therapy could increase the number of US GLP-1 users.

Future Market Outlook (2026-2034)

The United States diabetes market is projected to grow from USD 31.09 Billion in 2025 to USD 39.80 Billion by 2034 at a 2.78% CAGR, reflecting steady growth in the world's largest, most commercially complex national diabetes market. The market's USD 35.66 Billion anchor value in 2030 will be defined by the interplay of three countervailing forces: premium GLP-1/GIP agonist revenue expansion driving top-line growth; IRA drug price negotiation compressing established brand revenues in the Medicare channel; and biosimilar insulin commoditization converting premium insulin revenues to generic volume.

Three structural forces define the US diabetes market's trajectory with high visibility through 2034: the GLP-1/GIP agonist franchise of Novo Nordisk and Eli Lilly; the IRA's drug price negotiation framework creating systematic Medicare revenue compression for established brands; and the closed-loop CGM-insulin delivery ecosystem transitioning from specialty to standard Type-1 care.

Research Methodology

Primary Research

Primary research comprised structured interviews with 90+ industry stakeholders (2025), including endocrinologists from major US academic centers, pharmaceutical company US commercial leaders, PBM formulary and access specialists, retail pharmacy chain diabetes clinical leaders, and CMS Medicare Part D coverage policy analysts.

Secondary Research

Secondary research encompassed CDC National Diabetes Statistics Report 2024, ADA Standards of Medical Care in Diabetes 2024, CMS Medicare Part D drug spending data 2024, FDA drug approval database and biosimilar action plan reports, IRA drug price negotiation program documentation, IQVIA US pharmaceutical market data, the manufacturer earnings reports, ADA Scientific Sessions 2024 clinical trial data. Over 180 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using bottom-up prescription volume x net price per prescription models, segmented by segment (insulin including GLP-1 agonists, oral antidiabetics) and distribution channel. Key inputs include CDC diabetes prevalence trajectory, ADA guideline adoption rates for GLP-1 agonists, IRA negotiated price projections, biosimilar insulin substitution rates, OTC CGM adoption curves, GLP-1 manufacturing capacity expansion timelines, and US Census Bureau demographic aging projections for the 65+ Medicare population through 2034.

US Diabetes Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Segments Covered | Oral Antidiabetics, Insulin |

| Distribution Channels Covered | E-commerce and Tele-pharmacy, Hospital Pharmacies, Retail Pharmacies |

| Companies Covered | Novo Nordisk A/S, Lilly USA, LLC, Sanofi, AstraZeneca, Medtronic, Dexcom Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Diabetes Market Report

The US diabetes market reached USD 31.09 Billion in 2025, driven by 40 million patients with diabetes, GLP-1 agonist class revenues, and strong retail pharmacy distribution infrastructure.

The US diabetes market is projected to grow at 2.78% CAGR during 2026-2034, reaching USD 39.80 Billion by 2034, balancing premium GLP-1 agonist expansion against IRA drug price negotiation compression and biosimilar insulin adoption.

Insulin leads at 56.5% market share (2025), encompassing premium GLP-1 injectable agonists, traditional basal analogs, and biosimilar insulins.

Retail pharmacies hold 60.0% market share (2025), anchored by US outpatient diabetes prescriptions under PBM network agreements.

E-commerce/tele-pharmacy grows fastest at ~4.2% CAGR (2026-2034), driven by online pharmacies and PBM mail-order program enrollment incentives.

Leading companies include Novo Nordisk A/S, Lilly USA, LLC, Sanofi, AstraZeneca, Medtronic, and Dexcom Inc., among others.

The US diabetes market is projected to reach approximately USD 35.66 Billion by 2030, anchored by GLP-1 combined revenues, oral GLP-1 agonist entry, OTC CGM market growth, and biosimilar insulin high prescription share.

Oral antidiabetics hold 43.5% (2025), led by SGLT-2 inhibitors' growth, partly offsetting Januvia DPP-4 revenue erosion from generic competition and metformin's generic dominance.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)