US Generative AI Market Size, Share, Trends and Forecast by Offering Type, Technology Type, Application, and Region, 2026-2034

US Generative AI Market Size, Share, Trends & Forecast (2026-2034)

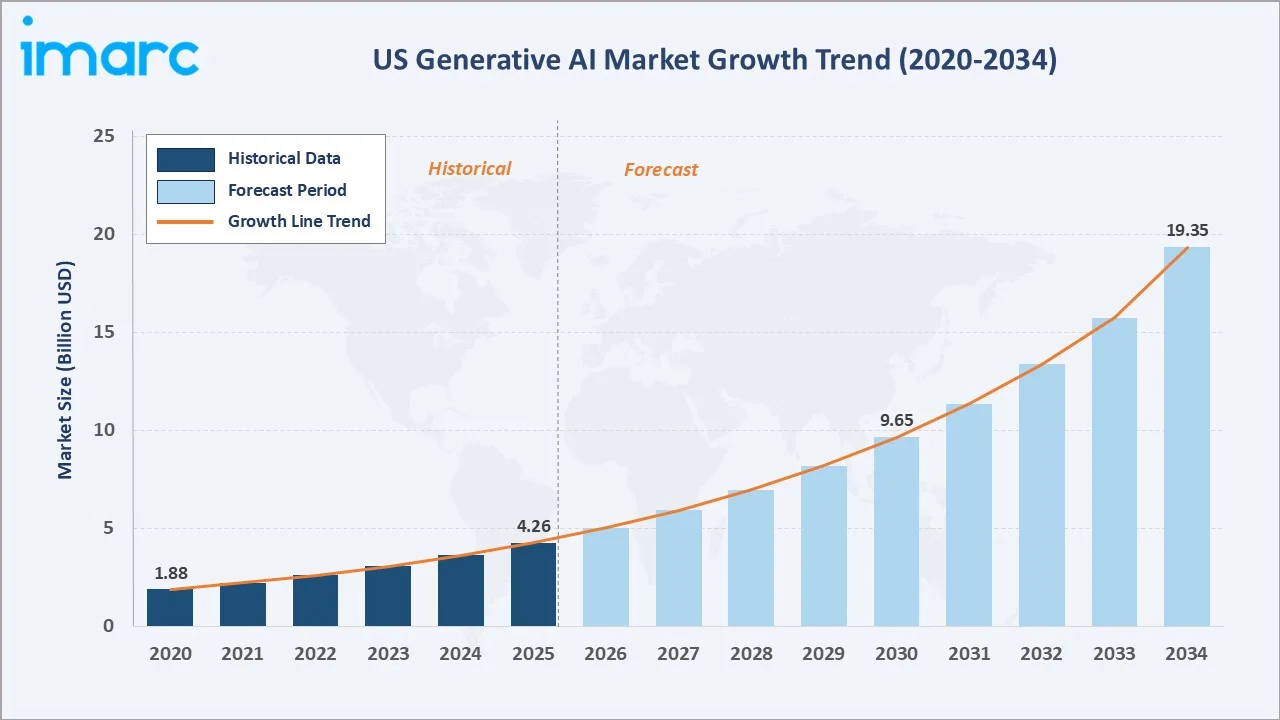

The US generative AI market reached USD 4.26 Billion in 2025 and is projected to reach USD 19.35 Billion by 2034, growing at a CAGR of 17.77% during 2026-2034. The US leads global generative AI development and deployment, owing to nearly 40% of U.S. adults aged 18–64 having adopted Gen AI, with about one-third using it daily or weekly to support work-related tasks.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.26 Billion |

|

Forecast Market Size (2034) |

USD 19.35 Billion |

|

CAGR (2026-2034) |

17.77% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

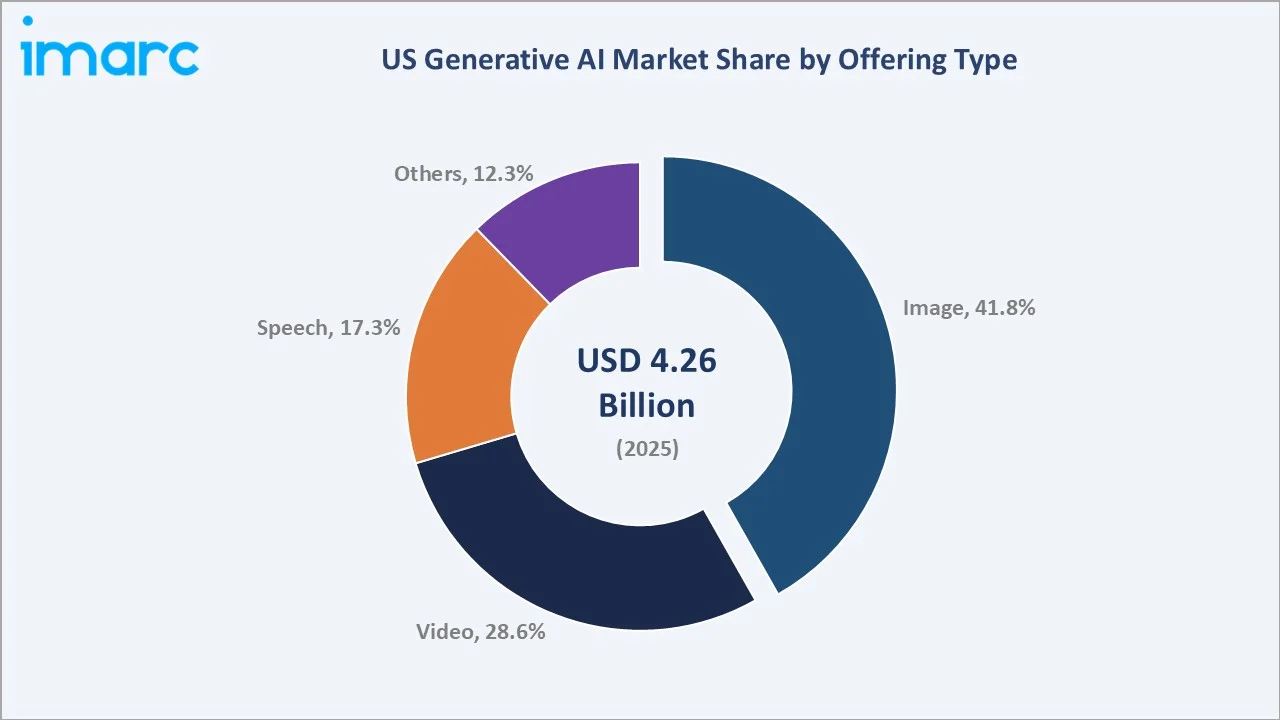

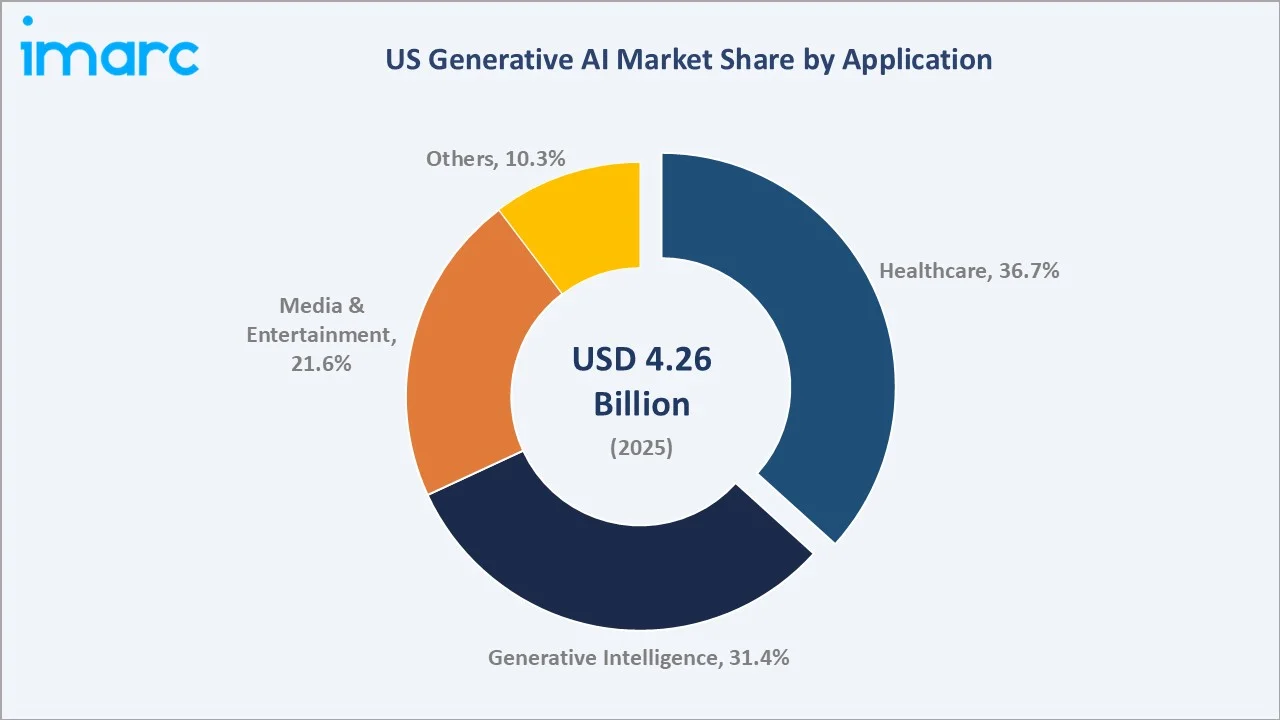

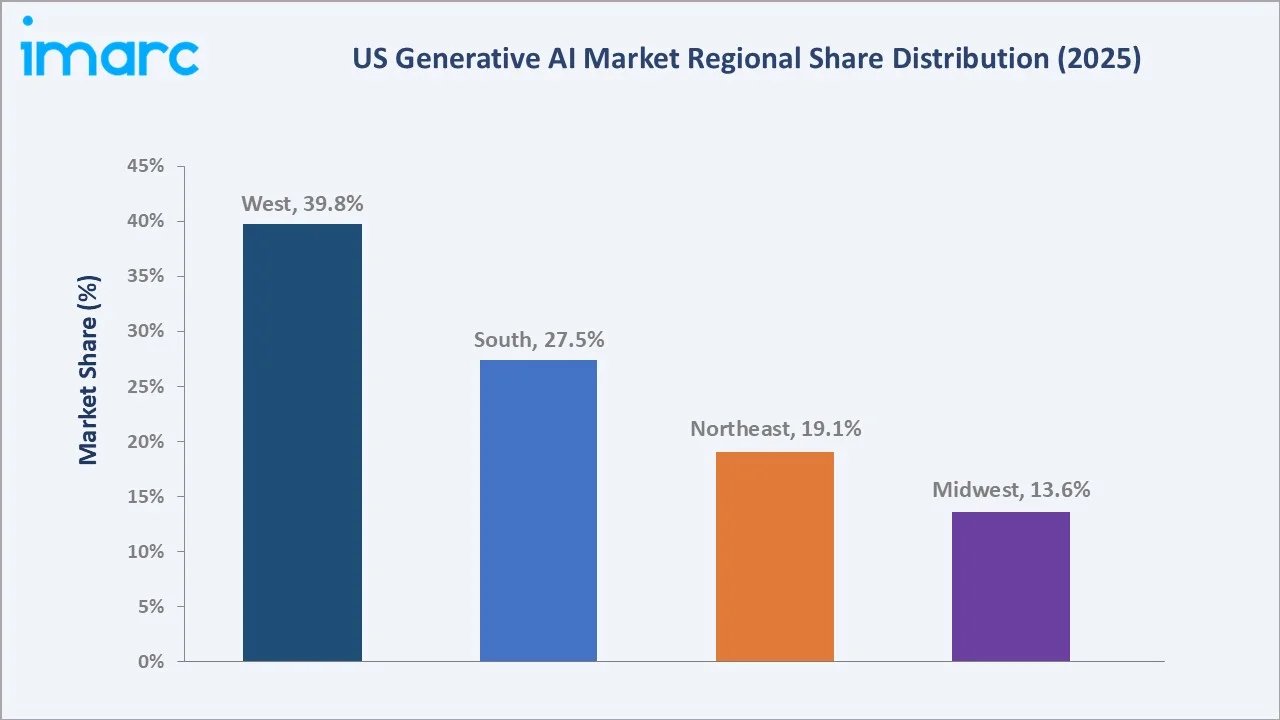

The West region leads with a 39.8% market share in 2025, anchored by Silicon Valley's concentration of foundation model developers, cloud infrastructure providers, and AI-native enterprise SaaS companies. Image dominates the offering type breakdown at 41.8%, while healthcare leads the application segment at 36.7%.

To get more information on this market, Request Sample

The US generative AI market is underpinned by three structural forces: the extraordinary foundation model capability progression that continuously expands commercially viable generative AI applications; the institutional capital commitment exemplified by Microsoft's USD 80 billion AI infrastructure investment through 2028 (FY 2025) that creates non-discretionary enterprise adoption pressure; and the US federal government's National AI Initiative Act funding and executive orders mandating AI integration across federal agencies.

Executive Summary

The US generative AI market is experiencing extraordinary expansion, driven by the transition from experimental generative AI pilots to large-scale enterprise deployment across all major industry verticals. The market reached USD 4.26 Billion in 2025 and is forecast to reach USD 19.35 Billion by 2034, growing at a CAGR of 17.77%. This growth is underpinned by OpenAI's ChatGPT achieving 900 million weekly active users in February 2025.

Image dominates the offering type segment with a 41.8% share in 2025, driven by Adobe Firefly's enterprise creative platform, Midjourney's 20 million user base, and the explosive growth of AI-generated marketing, advertising, and product imagery across US commercial sectors.

Healthcare leads the application segment at 36.7%, owing to US healthcare spending reaching USD 5.3 trillion in 2024, creating massive AI adoption budgets, regulatory clarity from the FDA's Digital Health Center of Excellence, and the clinical value demonstrated by AI diagnostic tools at major health systems.

The West region at 39.8% leads regionally, anchored by Silicon Valley's foundation model ecosystem and tech sector concentration. Leading vendors collectively represent the world's most concentrated generative AI competitive ecosystem, driving continuous capability advancement that sustains the market's above-average growth trajectory.

Key Market Insights

|

Insight |

Data |

|

Largest Offering Type |

Image – 41.8% share (2025) |

|

Fastest Growing Offering Type |

Video – ~22.4% CAGR (2026-2034) |

|

Largest Application |

Healthcare – 36.7% share (2025) |

|

Fastest Growing Application |

Healthcare – ~20.8% CAGR (2026-2034) |

|

Leading Region |

West – 39.8% share (2025) |

|

Top Companies |

Microsoft, Google LLC, OpenAI, NVIDIA Corporation, and Anthropic PBC |

Key Analytical Observations Supporting The Above Data:

- Image at 41.8% (2025) leads as visual content creation represents the generative AI use case with the broadest US market application footprint, from marketing agencies using Midjourney and Adobe Firefly for campaign creative, to e-commerce platforms generating product imagery, to media publishers creating editorial illustrations.

- Video at 28.6% share (2025) is growing fastest at ~22.4% CAGR as OpenAI's Sora, Runway ML's Gen-3 Alpha, and Adobe's Firefly Video enable AI-generated video content at production quality for the first time.

- Healthcare at 36.7% (2025) leads application segments owing to the US healthcare system, which deploys generative AI for clinical documentation, diagnostic imaging analysis, drug discovery acceleration, and synthetic clinical data generation that transforms the economics of AI model training in regulated healthcare environments.

- The West's 39.8% share (2025) reflects the geographic concentration of the US AI economy: San Francisco Bay Area alone hosts OpenAI, Anthropic, Google DeepMind, Meta AI Research, and NVIDIA AI, creating a talent, capital, and infrastructure density that sustains regional AI market leadership through the forecast period.

US Generative AI Market Overview

The US generative AI market encompasses the full ecosystem of AI systems capable of generating novel content in response to natural language prompts or structured inputs. The market spans foundation model development, inference infrastructure, API and SDK platforms, AI application development tools, and the enterprise SaaS applications built on generative AI capabilities across healthcare, media and entertainment, financial services, education, legal, and manufacturing verticals.

The market's structural foundation is the rapid capability progression of foundation models: from GPT-3's 175 billion parameters (2020) to GPT-4's multimodal capabilities (2023) to reasoning-specialized models like OpenAI o3 that demonstrate near-human performance on professional-grade reasoning benchmarks. Each capability improvement expands the commercially viable application surface, drawing new enterprise adopters and creating demand for the next generation of model capabilities in a virtuous growth cycle that sustains the market's compound growth trajectory.

Market Dynamics

To evaluate market opportunities, Request Sample

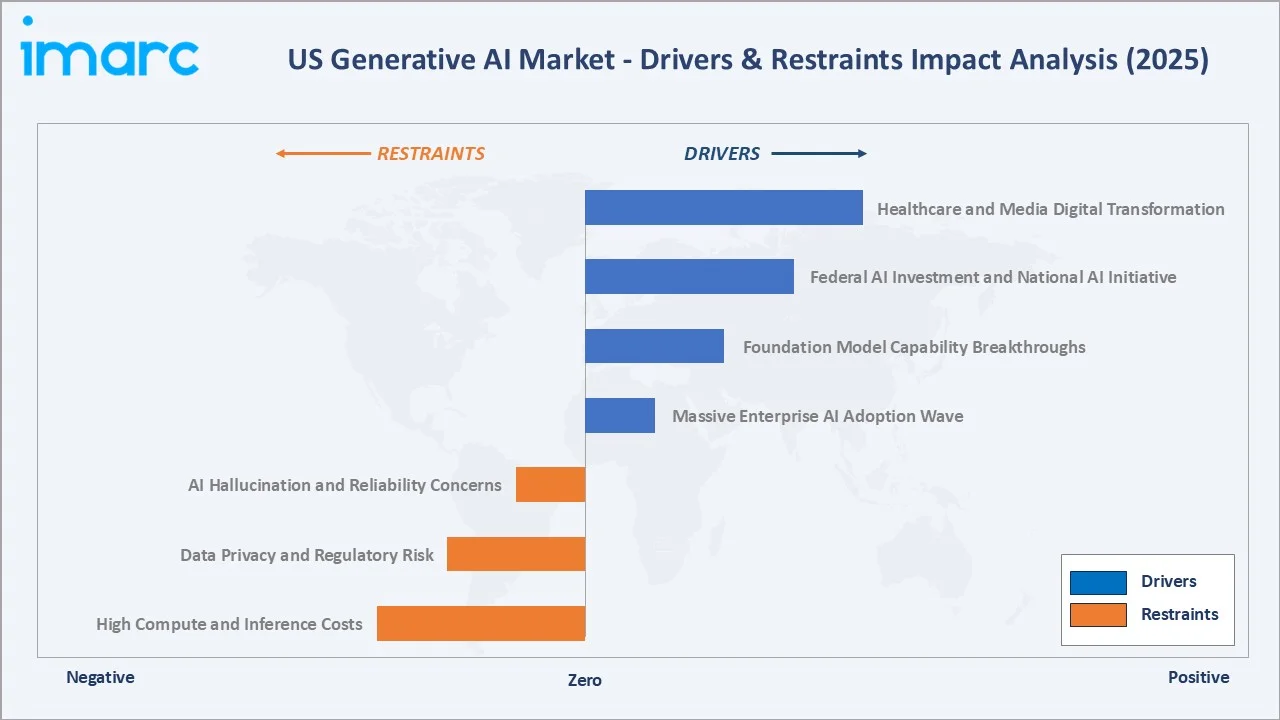

Market Drivers

- Massive Enterprise AI Adoption Wave: In December 2025, Microsoft reported that over 90% of Fortune 500 companies are now using Microsoft 365 Copilot. Additionally, in May 2026, ServiceNow surpassed USD 1 billion in AWS Marketplace transactions and expanded its AWS partnership with AI governance, agent integrations, and developer tools for enterprise AI adoption.

- Foundation Model Capability Breakthroughs: In April 2025, OpenAI released o3 and o4-mini, designed specifically for advanced mathematics, coding, and multimodal reasoning, demonstrating expert-level performance on AIME, GPQA, and professional coding benchmarks. Anthropic's Claude 3.7 Sonnet (February 2025) demonstrated hybrid reasoning that switches between standard and extended thinking modes, achieving breakthrough performance on software engineering benchmarks.

- Federal AI Investment and National AI Initiative: The US National Science Foundation's USD 140 million investment in seven new AI research institutes in May 2023, the National AI Initiative Act's interagency coordination, and the Executive Order on AI Safety (October 2023), creating sector-specific AI deployment frameworks, collectively represent the federal government's structural commitment to US AI leadership.

- Healthcare and Media Digital Transformation: The US healthcare system's adoption of AI clinical documentation tools is creating recurring SaaS revenue streams that anchor healthcare as the largest application segment.

Market Restraints

- AI Hallucination and Reliability Concerns: Large language model hallucination remains the primary technical barrier to generative AI deployment in high-stakes applications, including legal research, medical diagnosis, and financial analysis. A Stanford study published in 2025, based on tools tested in May 2024, reported hallucination rates of 17% for Lexis+ AI, 33% for Westlaw AI-Assisted Research, and 43% for GPT-4.

- Data Privacy and Regulatory Risk: Enterprise legal and compliance teams are imposing 6–18 month review cycles on new generative AI tool deployment, constraining the commercial velocity of AI adoption in regulated industries relative to the technology's capability advancement pace.

- High Compute and Inference Costs: Training frontier foundation models now costs USD 100 million to USD 500+ million per run, with GPT-4 estimated at USD 100 million. Inference costs remain significant for real-time enterprise applications at scale, as a Fortune 500 company processing 10 million customer queries monthly through an LLM API incurs USD 150,000–1.5 million monthly in inference costs.

Market Opportunities

- Agentic AI and Autonomous Workflow Systems: The transition from single-turn generative AI interactions to multi-step autonomous AI agents represents the next major commercial frontier. OpenAI's Operator agent, Anthropic's Computer Use, and Microsoft Copilot Agents are establishing the agentic AI commercial category.

- Domain-Specific Foundation Models for Healthcare: The FDA's evolving Digital Health Center of Excellence framework for AI/ML-based Software as a Medical Device (SaMD) is creating a regulatory pathway that enables specialized medical AI models to achieve FDA clearance and command healthcare-grade pricing premiums of 3–5x versus general-purpose AI.

Market Challenges

- Intellectual Property and Training Data Liability: Multiple pending US federal court cases are creating unresolved legal uncertainty around the copyright status of foundation model training data. A judicial ruling that model training on copyrighted data constitutes infringement would require major model providers to rebuild training datasets, potentially costing USD 1–10 billion per model in licensed data acquisition costs.

- Model Commoditization and Pricing Pressure: Meta's open-source Llama 3 release and Mistral AI's competitive open-weight models demonstrating competitive reasoning performance at substantially lower training costs are creating downward pricing pressure on commercial foundation model APIs.

Emerging Market Trends

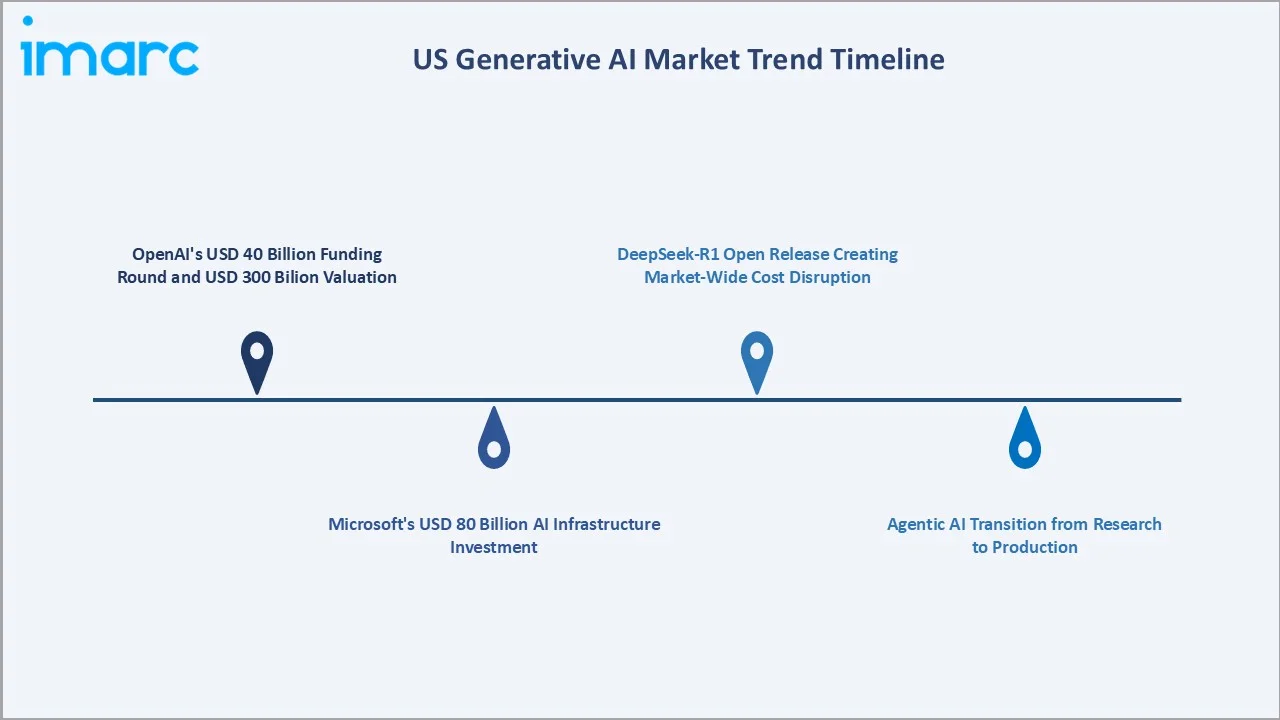

1. OpenAI's USD 40 Billion Funding Round and USD 300 Billion Valuation

As of March 2025, OpenAI closed a USD 40 billion funding round, bringing its valuation to USD 300 billion, led by SoftBank Group. This capital deployment reflects investor conviction that OpenAI's ChatGPT platform, API business serving 2+ million developers, and enterprise ChatGPT Team/Enterprise subscriptions constitute a durable foundation for a multi-hundred-billion-dollar AI technology company.

2. Microsoft's USD 80 Billion AI Infrastructure Investment

Microsoft's announcement in January 2025 of USD 80 billion in planned AI infrastructure investment, encompassing data center construction, NVIDIA GPU procurement, and Azure AI platform expansion, represents the single largest corporate AI infrastructure commitment in US history. This investment will expand Microsoft's Azure AI compute capacity, enabling the scaling of next-generation foundation models and supporting the deployment of Microsoft Copilot across its 300 million Office 365 enterprise user base.

3. Agentic AI transition from Research to Production

In January 2025, OpenAI launched Operator, its first commercially deployed autonomous AI agent capable of browsing the web, completing forms, and executing multi-step tasks on behalf of users without human intervention for each step. Microsoft's Copilot Agents, deployed across Teams and Dynamics 365, enable enterprise workflows where AI agents autonomously process invoice approvals, customer service tickets, and HR onboarding tasks.

4. DeepSeek-R1 Open Release Creating Market-Wide Cost Disruption

DeepSeek released its R1 reasoning large language model (LLM) in January 2025 with open weights, demonstrating performance competitive with OpenAI's o1 on reasoning benchmarks at substantially lower training costs. The release triggered a US stock market response reflecting investor concern about the capital intensity assumptions underlying US AI infrastructure investment.

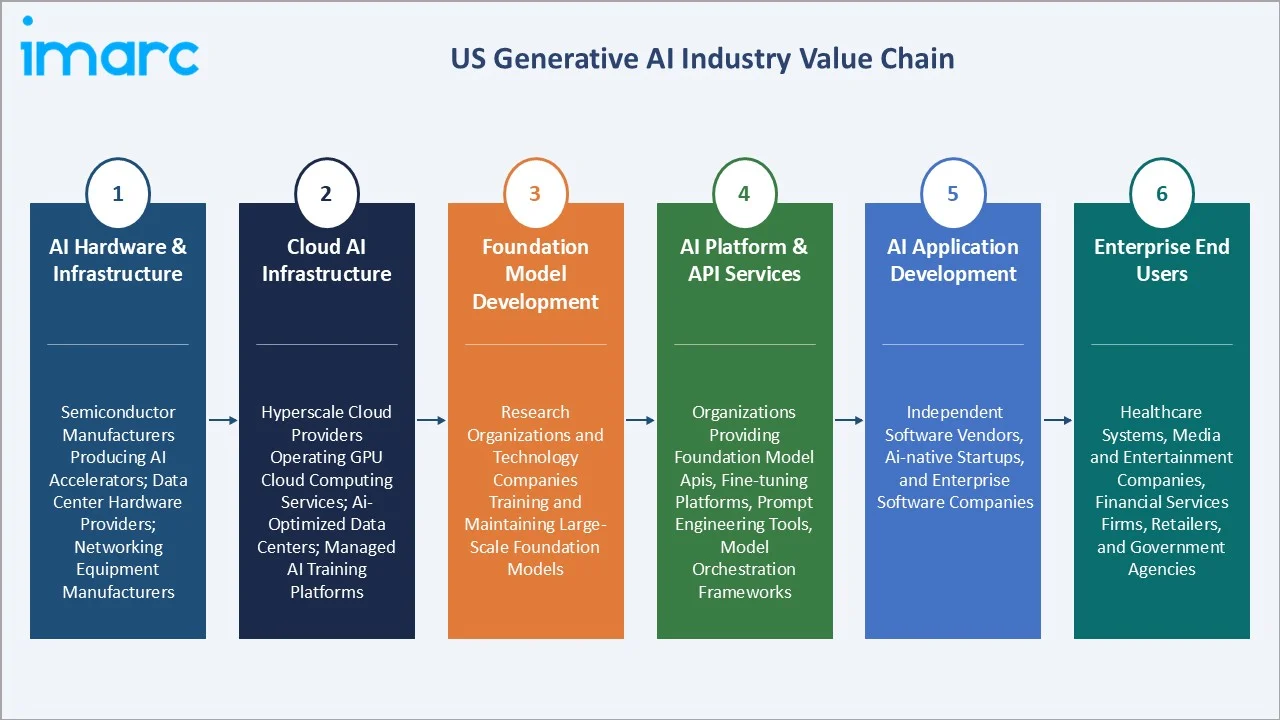

Industry Value Chain Analysis

The US generative AI value chain spans semiconductor and infrastructure provision through enterprise end-user application deployment, with each stage occupied by specialized companies whose performance determines model capability, deployment economics, and application utility.

|

Stage |

Key Players / Examples |

|

AI Hardware & Infrastructure |

Semiconductor manufacturers producing AI accelerators; data center hardware providers; networking equipment manufacturers |

|

Cloud AI Infrastructure |

Hyperscale cloud providers operating GPU cloud computing services; AI-optimized data centers; managed AI training platforms |

|

Foundation Model Development |

Research organizations and technology companies training and maintaining large-scale foundation models |

|

AI Platform & API Services |

Organizations providing foundation model APIs, fine-tuning platforms, prompt engineering tools, model orchestration frameworks |

|

AI Application Development |

Independent software vendors, AI-native startups, and enterprise software companies |

|

Enterprise End Users |

Healthcare systems, media and entertainment companies, financial services firms, retailers, and government agencies |

Technology Landscape in the US Generative AI Industry

Large Language Models and Text Generation

The US LLM market is dominated by GPT-4o (OpenAI), Claude Haiku 4.5 (Anthropic), Gemini 2.5 Pro (Google), and Grok-3 (xAI), collectively representing the frontier of commercial text generation capability. Enterprise LLM deployment is transitioning from general-purpose models toward fine-tuned vertical specialists, including Bloomberg GPT for financial analysis, Microsoft Azure Health Bot for clinical documentation, Harvey AI for legal research, and Salesforce Einstein GPT for CRM.

Image and Visual Generation Platforms

US image generation platforms serve distinct market segments from consumer creative to enterprise marketing production. Adobe Firefly's commercial safety model has established the enterprise-acceptable image generation standard, with 22 billion assets generated through Firefly tools by April 2025. The integration of AI image generation into existing enterprise creative workflows through Adobe Creative Cloud, Canva's AI suite, and Microsoft Designer is mainstreaming AI visual creation beyond specialist AI tool users.

Video Generation and Synthetic Media

AI video generation is being driven by OpenAI's Sora, Runway ML's Gen-3 Alpha, and Adobe Premiere Pro's Firefly Video. Adobe launched AI-powered upgrades for Premiere Pro in April 2025, including Generative Extend, which expands video/audio clips using the Firefly Video Model. The update also added Media Intelligence to search large footage libraries in seconds and Caption Translation for captions across 27 languages.

Speech Generation and Conversational AI

AI speech generation serves the US podcasting, customer service, education, and accessibility markets. ElevenLabs, LMNT, and OpenAI's TTS API represent the commercial speech generation market, while voice AI companies are deploying real-time conversational AI phone agents that handle 1 million+ customer service calls daily for US financial services, healthcare, and retail enterprises.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Offering Type |

Image |

41.8% |

2025 |

|

Application |

Healthcare |

36.7% |

2025 |

|

Technology Type |

🔒 |

🔒 |

2025 |

|

Region |

West |

39.8% |

2025 |

By Offering Type

The image segment dominates with a 41.8% share in 2025, reflecting the US creative and marketing industry's early and enthusiastic adoption of AI visual tools, including Adobe Firefly generating 22 billion assets, Midjourney serving 20 million users, and DALL-E 3 processing 5 million daily image requests, across advertising, e-commerce, media publishing, and enterprise marketing applications.

To access detailed market analysis, Request Sample

Video represents 28.6% share (2025) and is growing fastest (~22.4% CAGR) as AI video quality reaches production-usable standards and integration with professional editing tools begins. Speech at 17.3% serves the US voice AI, accessibility, and conversational AI markets, growing as voice AI agents replace human agents in customer service workflows.

By Application

Healthcare leads with a 36.7% share in 2025, owing to both the sector's enormous technology procurement budget and the high clinical value delivered. AI clinical documentation tools reduce physician documentation time by 30–50%, potentially recovering USD 50,000–100,000 annually in physician productivity value per clinician.

Generative intelligence at 31.4% encompasses enterprise productivity applications, including AI writing assistants, code generation tools, analytical AI, and autonomous AI agents deployed across general business workflows. Media and entertainment at 21.6% serves US studios, broadcasters, advertising agencies, and digital media publishers deploying AI for content creation, post-production, and audience personalization.

Regional Market Insights

The West region's dominant 39.8% market share in 2025 reflects Silicon Valley's unparalleled concentration of AI talent, capital, and enterprise adoption. The presence of leading technology firms, AI startups, venture capital networks, and cloud infrastructure providers continues to accelerate innovation and commercialization across the region.

The South at 27.5% is growing rapidly, driven by Texas's emergence as a major AI industry hub, supported by expanding data center investments, enterprise AI adoption, and a growing startup ecosystem. The region is also benefiting from favorable business policies, lower operating costs, and rising demand for Gen AI solutions across healthcare, finance, retail, and energy sectors.

|

Region |

Share (2025) |

Key Growth Drivers |

|

West |

39.8% |

Dominant venture capital deployment in AI startups; hyperscale cloud AI infrastructure concentration; leading AI talent university pipeline |

|

South |

27.5% |

Rapidly growing AI industry cluster in Texas; major hyperscale data center expansion; significant healthcare AI adoption across major South health systems |

|

Northeast |

19.1% |

Financial services AI adoption from Wall Street and major US banks; biotech and pharmaceutical AI research; major media and advertising AI adoption |

|

Midwest |

13.6% |

Manufacturing and industrial AI adoption across automotive and aerospace sectors; growing AI research ecosystem; significant healthcare AI adoption; expanding AI startup ecosystem |

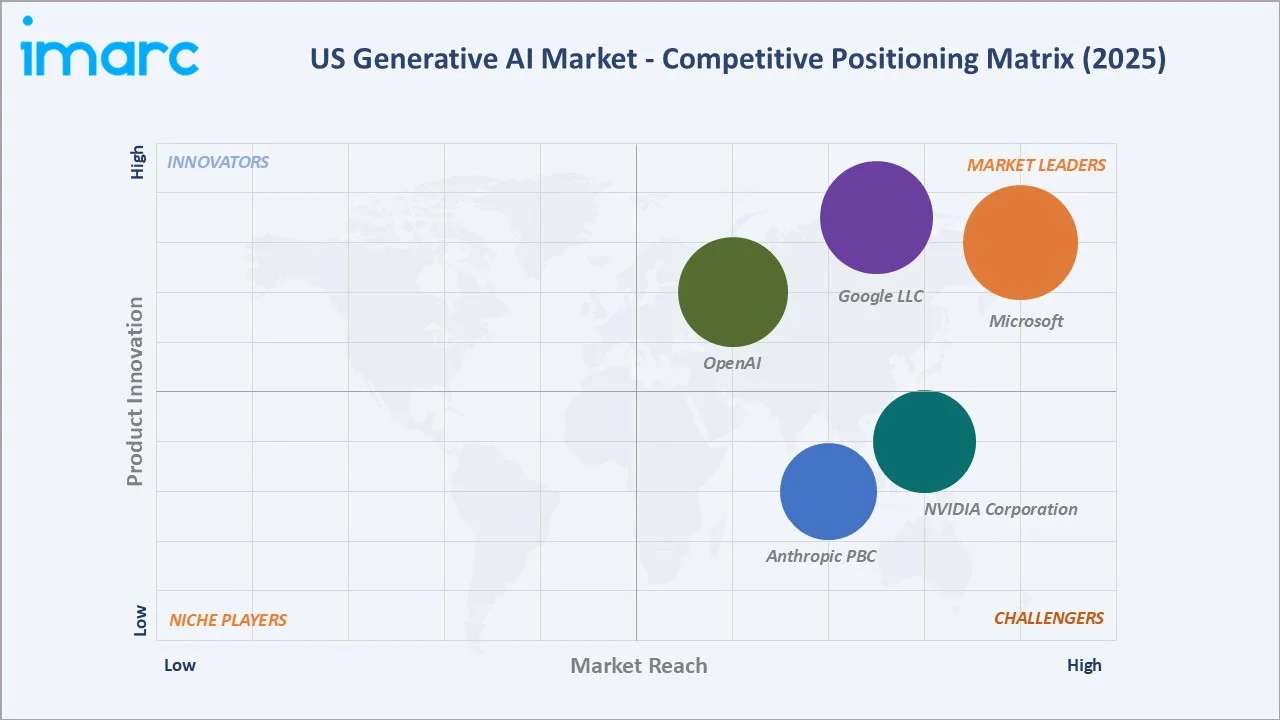

Competitive Landscape

The US generative AI market exhibits moderate concentration at the foundation model level, with Microsoft, Google, and OpenAI collectively dominating enterprise API revenue.

|

Company Name |

Product/Brand |

Market Position |

Core Strength |

|

Microsoft |

Microsoft 365 Copilot, Microsoft AI, Azure |

Market Leader |

Largest enterprise AI deployment via Copilot; Azure AI infrastructure; Office 365 enterprise user distribution advantage |

|

Google LLC |

Gemini, DeepMind, Google AI Studio |

Market Leader |

Gemini multimodal models; DeepMind research leadership; Google Cloud Vertex AI; large consumer product distribution |

|

OpenAI |

ChatGPT, ChatGPT Business, ChatGPT Enterprise, ChatGPT for Education, Codex |

Market Leader |

Large base of active users; GPT-4o and o3 frontier models; largest AI developer ecosystem |

|

NVIDIA Corporation |

NVIDIA NeMo, NVIDIA AI Foundry, NVIDIA NIM, NVIDIA Blueprints, NVIDIA AI Enterprise, AI-Q NVIDIA AI Blueprint |

Strong Challenger |

Highest data center GPU market share; CUDA software ecosystem; NIM inference microservices |

|

Anthropic PBC |

Claude, Claude Code, Claude Code for Enterprise, Claude Cowork, Claude Security, Claude for Chrome, Claude for Slack, Claude for Microsoft 365 |

Strong Challenger |

Claude constitutional AI safety leadership; Claude 3.7 frontier reasoning performance; AWS and Google Cloud strategic partnerships; enterprise trust positioning |

The application layer is highly fragmented across thousands of vertical-specific AI SaaS companies deploying specialized models for healthcare, legal, financial, and creative applications.

Key Company Profiles

Microsoft

Microsoft is one of the world's largest enterprise generative AI deployment companies. Microsoft Copilot represents the broadest enterprise AI product distribution in history, with 90% of Fortune 500 companies actively using Microsoft 365 Copilot as of December 2025.

- Product Portfolio: Microsoft 365 Copilot, GitHub Copilot, Azure OpenAI Service, Copilot Studio, Microsoft Designer, and Azure AI Foundry.

- Recent Developments: In June 2026, Microsoft unveiled 7 new in-house AI models, including MAI-Thinking-1, to reduce AI operating costs. The move strengthens Microsoft’s control over its AI stack while supporting cheaper, more customized AI tools across Copilot, Azure, GitHub, and Windows.

- Strategic Focus: Enterprise Copilot subscription revenue growth; Azure AI infrastructure leadership; agentic AI workflow automation across enterprise applications; AI safety compliance for regulated industry deployment.

Google LLC

Google LLC operates one of the world's most vertically integrated AI stacks, from custom TPU AI chips through the Gemini foundation model family to consumer AI products. Google's AI research leadership through DeepMind has produced foundational AI architecture breakthroughs.

- Product Portfolio: Gemini 2.0 Pro/Flash/Ultra foundation models, Google AI Studio, Gemini in Google Workspace, Imagen 3 text-to-image, Veo video generation, and NotebookLM AI research assistant.

- Recent Developments: In October 2025, Google LLC launched Gemini Enterprise as an AI platform that lets business users access company data, documents, and applications through conversational AI. The platform includes pre-built and custom AI agents for tasks such as research, data analysis, software development, and workflow automation, strengthening Google’s push into enterprise AI.

- Strategic Focus: Gemini multimodal model leadership; Google Cloud Vertex AI enterprise revenue growth; AI search transformation through Google AI Overviews; healthcare AI via Google Health and DeepMind AlphaFold 3 drug discovery platform.

OpenAI

OpenAI is one of the most influential AI research organizations in the US, having launched the generative AI era with GPT-3 (2020), initiated mass consumer AI adoption with ChatGPT (2022), and established the foundation model API business model that all commercial AI providers now emulate.

- Product Portfolio: ChatGPT, ChatGPT Business, ChatGPT Enterprise, ChatGPT for Education, and Codex.

- Recent Developments: In June 2026, OpenAI made its frontier models (GPT-5.5 and GPT-5.4) and Codex generally available on AWS, enabling enterprise customers to build with OpenAI inside their existing AWS security, governance, procurement, and billing workflows. The offering is available through Amazon Bedrock, including Codex for software engineering tasks, and is supported across AWS Commercial and GovCloud regions.

- Strategic Focus: Agentic AI platform commercialization; ChatGPT enterprise subscription revenue; safety-focused AGI development; API ecosystem expansion to 2M+ developers.

Market Concentration Analysis

The US generative AI market exhibits distinct concentration patterns across the value chain: the foundation model layer is highly concentrated, the infrastructure layer is oligopolistic, and the application layer is highly fragmented with thousands of vertical AI SaaS companies. This structural separation creates investment opportunities at each layer, independent of competition at adjacent layers.

Investment & Growth Opportunities

Fastest Growing Segments

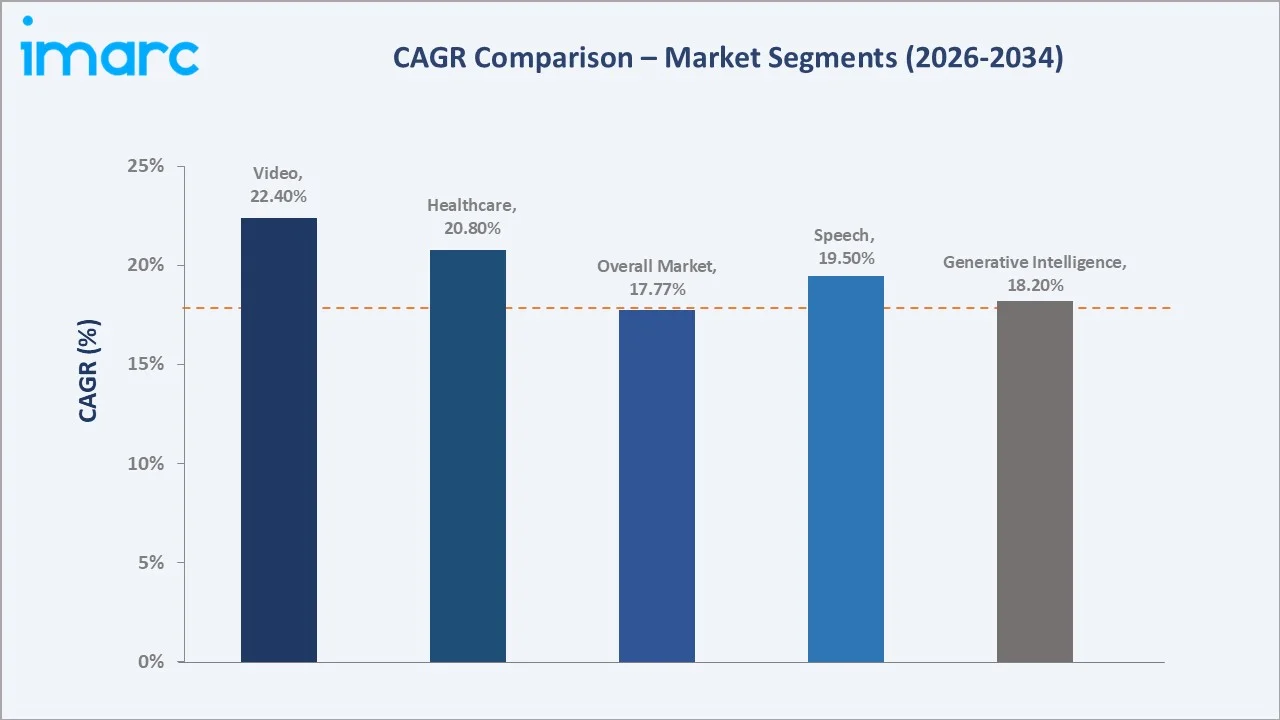

Video (~22.4% CAGR), healthcare AI applications (~20.8% CAGR), agentic AI workflow automation (~40% CAGR), and AI-powered enterprise SaaS (~25%+ CAGR) represent the highest-growth investment vectors through 2034. Together, these subcategories address a combined USD 15+ billion addressable incremental market opportunity within the US generative AI ecosystem by 2030.

Emerging Market Expansion

Key growth vectors include the accelerating adoption of AI agents and multi-model orchestration through Azure AI Foundry, the expansion of Microsoft 365 Copilot into SME and mid-market segments beyond large enterprises, and the deepening of vertical-specific GenAI solutions targeting regulated industries such as banking, healthcare, and government where data residency, compliance, and security requirements create structural barriers that favor Microsoft's integrated cloud-and-AI stack over standalone model providers.

Venture and Institutional Investment Trends

- Firms in the United States account for the largest share of global AI venture capital by a significant margin, representing approximately 75% of total AI VC deal value, equivalent to USD 194 billion.

- In November 2025, Cursor raised USD 2.3 billion in Series D financing at a USD 29.3 billion post-money valuation, backed by investors including Thrive, a16z, Accel, DST, Coatue, NVIDIA, and Google. The funding will support AI coding research, product development, frontier model training, and enterprise expansion, as Cursor surpassed USD 1 billion in annualized revenue.

Future Market Outlook (2026-2034)

The US generative AI market is positioned for sustained expansion through 2034. From a base of USD 4.26 Billion in 2025, the market is projected to reach USD 19.35 Billion by 2034, representing total incremental value creation of USD 15.09 billion at a CAGR of 17.77%. This growth is underpinned by the non-discretionary nature of enterprise AI adoption, combined with the relentless foundation model capability progression that continuously creates new commercially viable applications.

By 2034, agentic AI will supplant passive, single-turn AI assistants as the dominant deployment paradigm, with autonomous AI systems executing multi-day complex tasks across healthcare, legal, financial, and software development workflows. Image will retain 38–40% offering type share, while video is projected to grow to 32–35% as AI video quality reaches cinematic production standards. Healthcare will retain application leadership at 35%+, with generative intelligence growing to 33–35% as agentic AI tools create a new enterprise software category.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 100 industry participants in 2024–2025, including foundation model developers, enterprise AI deployment executives, venture capital investors, health system chief digital officers, media technology directors, and government AI program managers across California, New York, Texas, and Massachusetts.

Secondary Research

Secondary research encompassed company SEC filings and investor presentations, OpenAI partnership disclosures, Anthropic funding announcements, NVIDIA quarterly earnings reports, US National AI Initiative program documents, FDA Digital Health guidance, FTC AI reports, and industry publications (Bloomberg Intelligence AI Outlook, CB Insights State of AI).

Forecasting Models

Market size estimations incorporated US enterprise AI software spending forecasts, foundation model API pricing and volume trends, healthcare AI procurement data, media AI adoption surveys, and regional AI investment data. A base-case CAGR of 17.77% reflects consensus estimates validated against enterprise AI budget surveys, vendor revenue disclosures, and announced AI product commercialization timelines from FY2020 to FY2025.

US Generative AI Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Offering Types Covered | Image, Video, Speech, Others |

| Technology Types Covered | Autoencoders, Generative Adversarial Networks, Others |

| Applications Covered | Healthcare, Generative Intelligence, Media and Entertainment, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Microsoft, Google LLC, OpenAI, NVIDIA Corporation, Anthropic PBC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the US generative AI market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the US generative AI market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the US generative AI industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the US Generative AI Market Report

The US generative AI market reached USD 4.26 Billion in 2025 and is projected to reach USD 19.35 Billion by 2034.

The market is expected to grow at a CAGR of 17.77% during 2026-2034, driven by massive enterprise AI adoption, foundation model capability breakthroughs, and federal AI infrastructure investment.

The West region leads with a 39.8% share in 2025, anchored by Silicon Valley's concentration of foundation model developers, AI research labs, and the world's largest AI venture capital deployment.

Image dominates with a 41.8% share in 2025, driven by Adobe Firefly's enterprise creative platform, Midjourney's 20 million user base, and broad US commercial sector adoption of AI visual content creation.

Healthcare holds the largest share at 36.7%, driven by AI clinical documentation deployment at 700+ health systems, diagnostic AI, drug discovery, and synthetic medical data generation across the USD 4.5 trillion US healthcare system.

Some of the key players include Microsoft, Google LLC, OpenAI, NVIDIA Corporation, and Anthropic PBC.

Video is growing at ~22.4% CAGR as OpenAI's Sora, Runway ML's Gen-3, and Adobe Firefly Video achieve production-quality AI video, creating massive demand from the US media and entertainment industry for AI-generated content.

Key challenges include AI hallucination reliability concerns, data privacy and intellectual property regulatory risk, high inference costs constraining broad deployment, skilled AI talent shortage, and model commoditization pressure from open-source international models.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)