US Generic Drug Market Size, Share, Trends and Forecast by Segment, Therapy Area, Drug Delivery, and Distribution Channel, 2026-2034

US Generic Drug Market Size, Share, Trends & Forecast (2026-2034)

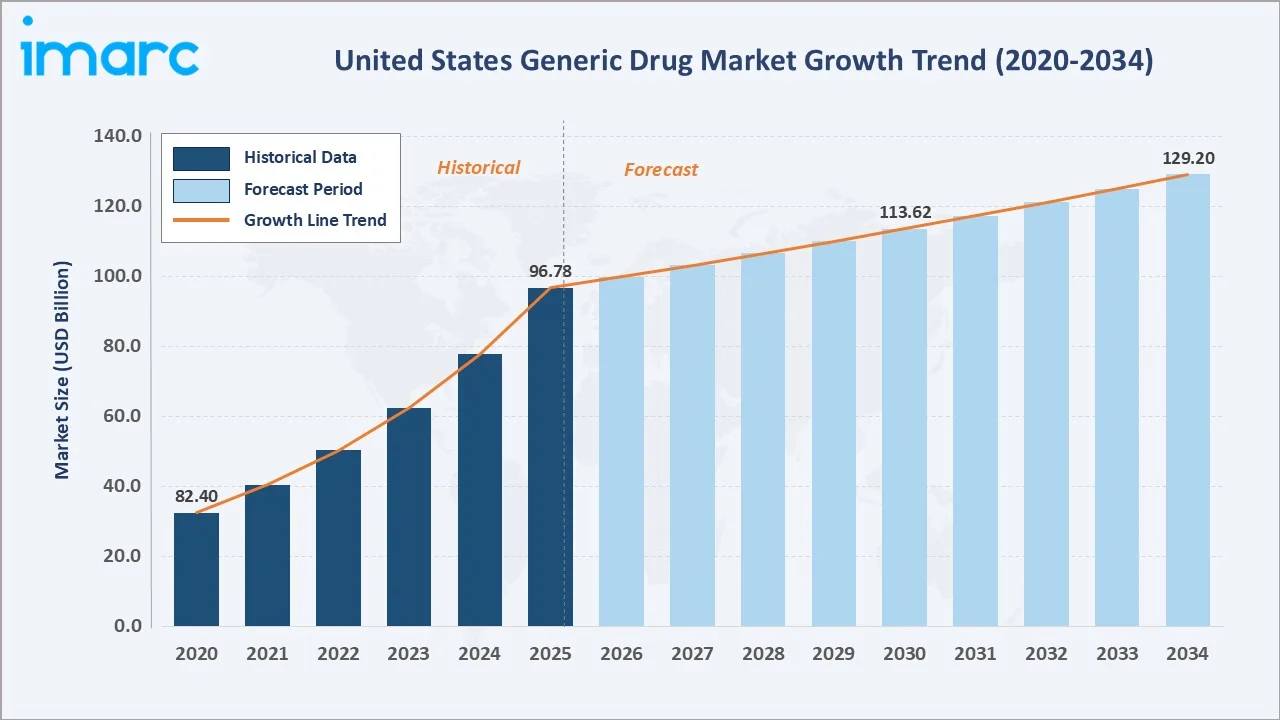

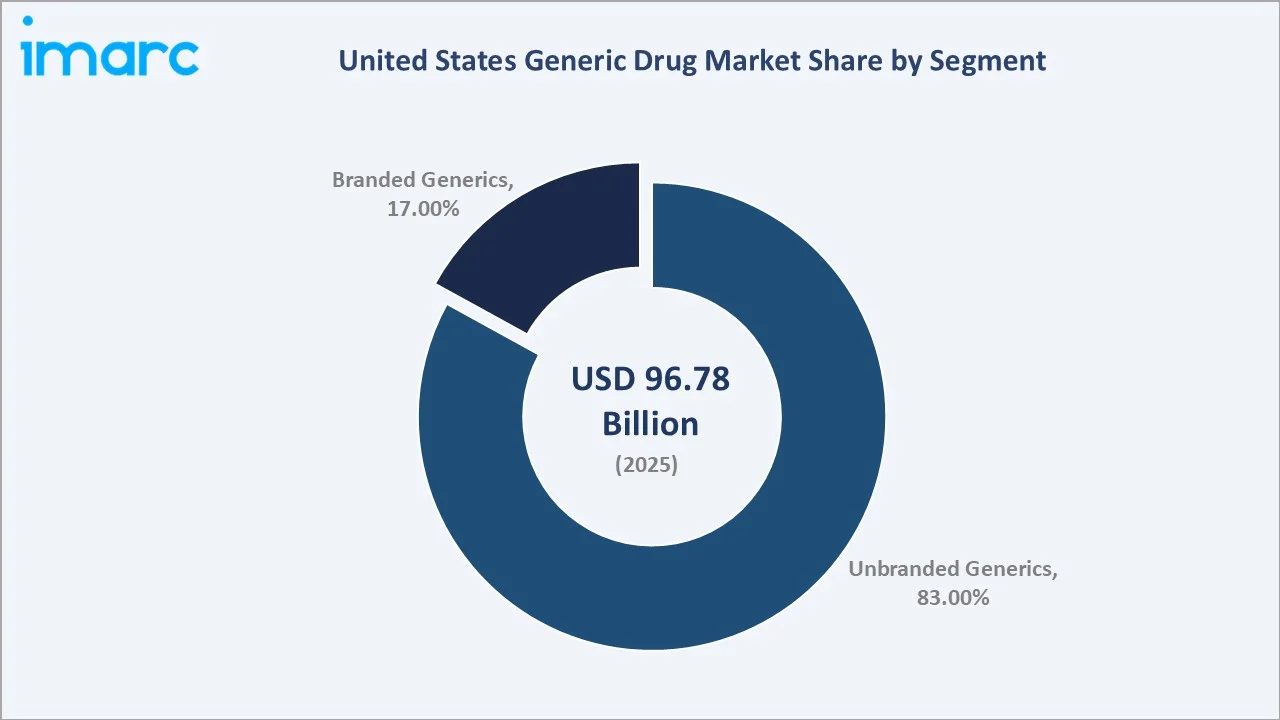

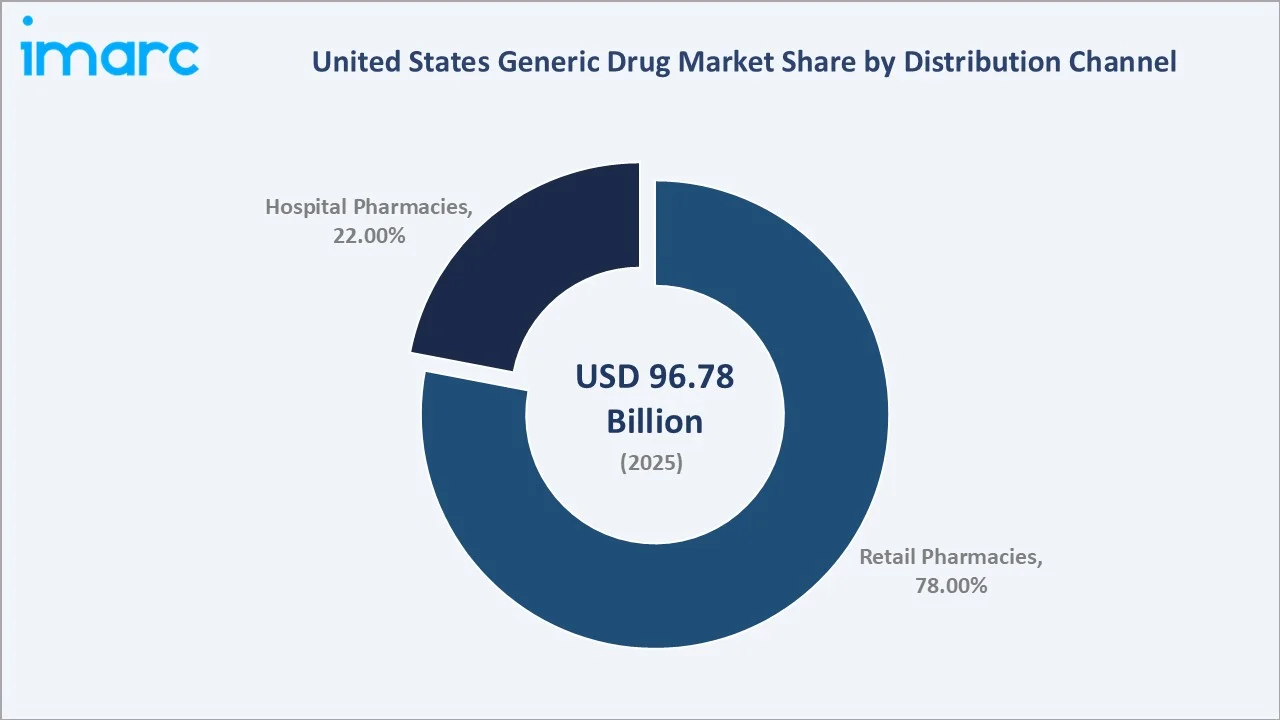

The US generic drug market reached USD 96.78 Billion in 2025 and is projected to reach USD 129.20 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 3.3% during the forecast period 2026-2034. The market growth is driven by accelerating patent expirations on blockbuster branded drugs, rising prevalence of chronic diseases, growing geriatric population, supportive FDA Drug Competition Action Plan, and sustained payer demand for cost-effective prescription alternatives.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 96.78 Billion |

|

Forecast Market Size (2034) |

USD 129.20 Billion |

|

CAGR (2026-2034) |

3.3% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Segment (2025) |

Unbranded Generics (83.0%) |

|

Leading Distribution Channel (2025) |

Retail Pharmacies (78.0%) |

To get more information on this market, Request Sample

Generic drugs are pharmaceutical products that are bioequivalent to their brand-name counterparts in terms of active ingredients, dosage form, strength, route of administration, quality, and safety profile. They are approved through the FDA's Abbreviated New Drug Application (ANDA) pathway, following the expiration of brand-name patents, and deliver the same therapeutic outcomes at significantly lower costs, typically 80–85% below the branded equivalent. Generic medicines now account for more than 90% of all US prescriptions while absorbing only approximately 18% of total drug expenditure, underscoring their critical role in managing national healthcare costs.

Strong regulatory support from the U.S. Food and Drug Administration, including streamlined approval pathways, further accelerates market entry. Additionally, rising healthcare cost pressures and payer preference for cost-effective treatments are increasing generic drug adoption across healthcare systems.

Executive Summary

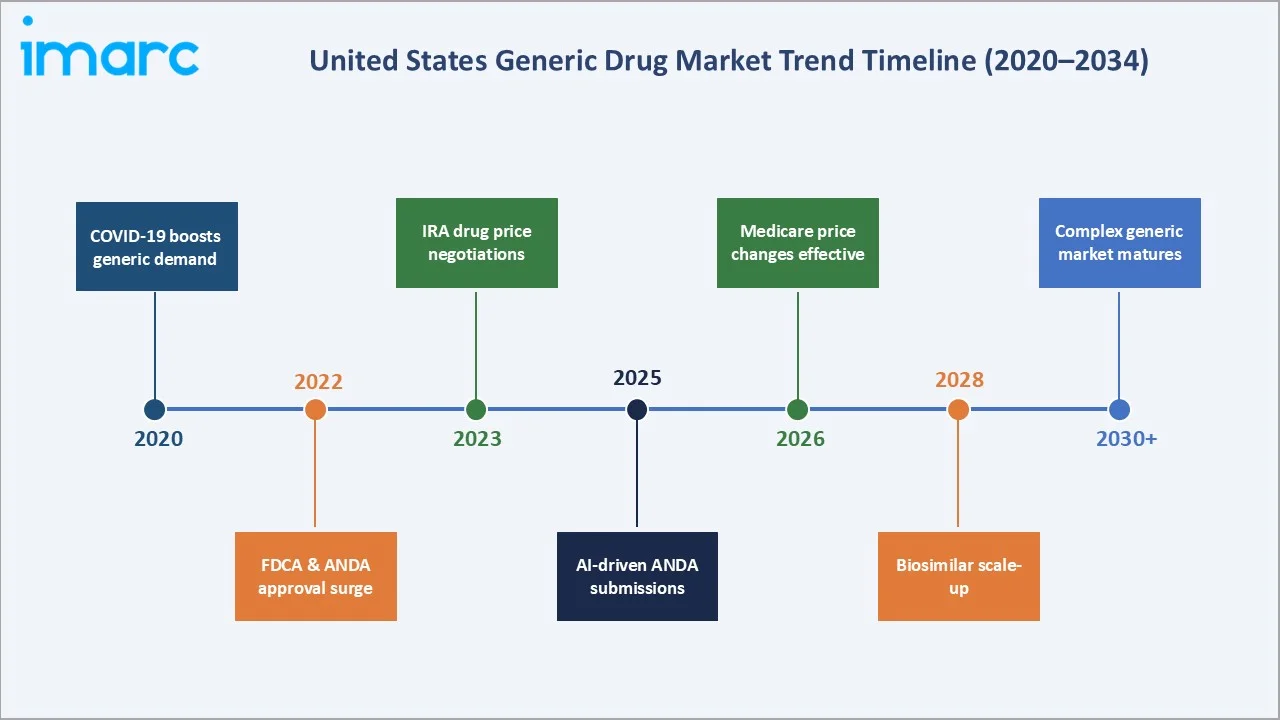

The US generic drug market continues to demonstrate resilient, structurally underpinned growth, reaching USD 96.78 Billion in 2025 and projected to attain USD 129.20 Billion by 2034 at a CAGR of 3.3%. Growth is anchored by one of the most consequential patent expiry cycles in pharmaceutical history, between 2025 and 2030, nearly 200 blockbuster drugs will lose patent protection, unlocking expansive ANDA opportunities for generic manufacturers.

In December 2024, the FDA approved the first generic daily GLP-1 injection for type 2 diabetes — a watershed event signalling the opening of the complex injectable generics segment. Additionally, in October 2025, the FDA launched a domestic manufacturing pilot program offering expedited ANDA approvals for drugs manufactured entirely in the United States, reinforcing supply chain resilience objectives.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Unbranded Generics — 83.0% share (2025) |

|

Largest Distribution Channel |

Retail Pharmacies — 78.0% share (2025) |

|

CAGR (2026-2034) |

3.3% |

|

Historical Period |

2020-2025 |

|

Market Size (2025) |

USD 96.78 Billion |

|

Forecast Market Size (2034) |

USD 129.20 Billion |

|

Top Companies |

Teva Pharmaceutical, Viatris Inc., Sun Pharmaceutical, Dr. Reddy's Laboratories, Lupin Pharmaceuticals, Par Health, Inc. |

Key Analytical Observations:

- Unbranded generics dominate at 83.0% share (2025), owing to widespread acceptance of non-proprietary substitution, aggressive pricing by PBMs favouring cost-effective dispensing, and FDA-approved therapeutic equivalence ratings (AB-rated). Unbranded products typically enter the market at 80–85% below branded prices, immediately capturing prescription volume after patent expiry.

- Retail pharmacies lead distribution at 78.0% (2025), reflecting the dominance of community pharmacy networks, PBM-directed prescription flow, and the rapid growth of mail-order and specialty pharmacy channels. CVS Caremark, Express Scripts (Cigna), and OptumRx collectively manage around 79% of US PBM volume, directly steering generic dispensing rates.

- FDA pipeline activity remains robust: as of late Q3 2025, at least 63 first generics had been approved year-to-date, with biosimilar approvals on track to surpass 2024's record. The December 2024 approval of the first generic GLP-1 daily injection marks the opening of the mass-market GLP-1 generic segment, a multi-billion-dollar opportunity.

US Generic Drug Market Overview

Generic drugs are the backbone of the US prescription drug system. Defined as pharmaceutical products that are bioequivalent to a reference listed drug (RLD) in terms of active ingredient, dosage form, strength, route of administration, and labeling, generics are approved by the FDA via the ANDA pathway without requiring repetitive clinical safety and efficacy trials. This streamlined regulatory mechanism was established under the Drug Price Competition and Patent Term Restoration Act of 1984 (Hatch-Waxman Act), which remains the foundational legislative framework governing generic market entry in the US.

The competitive landscape is characterised by moderate concentration among large multi-national generic manufacturers, including Teva, Viatris, and Sandoz, with a significant long tail of mid-tier and specialty generic companies. Looking ahead to 2034, the market will be defined by the expansion into complex generics and biosimilars, the integration of artificial intelligence in drug development and ANDA submissions, and the evolution of domestic manufacturing policy under evolving supply chain resilience priorities.

Market Dynamics

To evaluate market opportunities, Request Sample

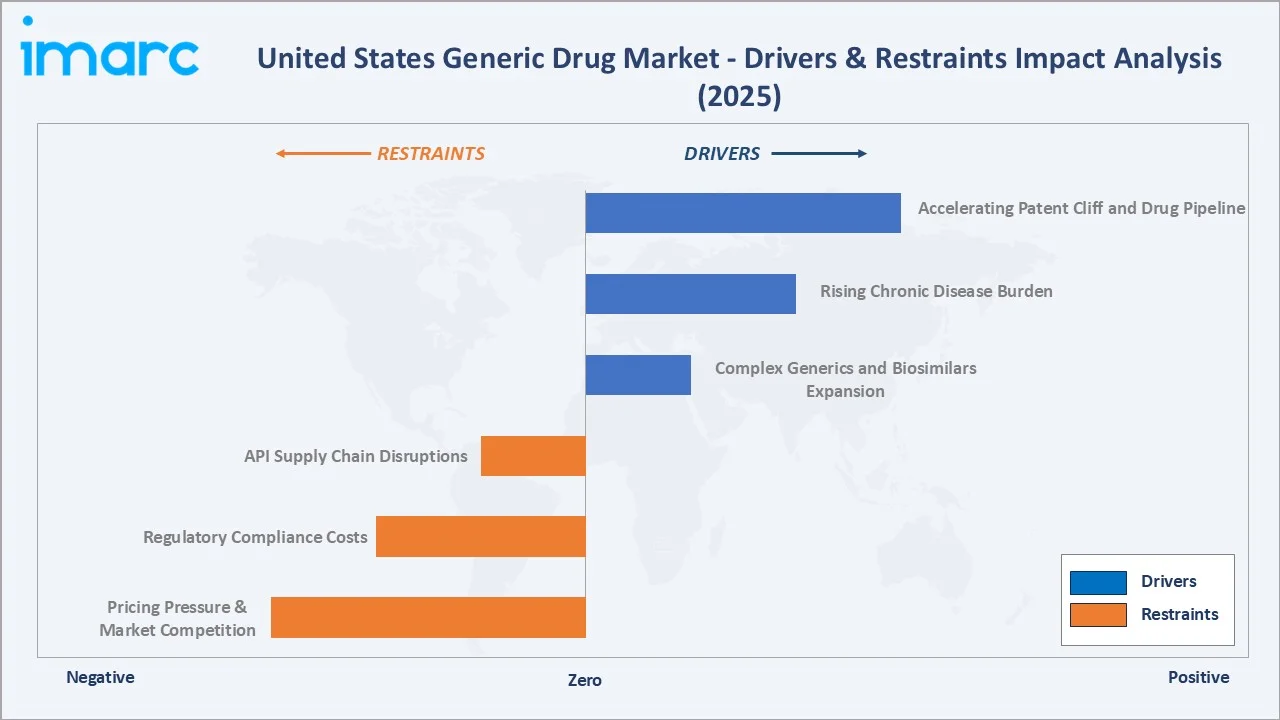

Market Drivers

- Accelerating Patent Cliff and Drug Pipeline: The single most powerful growth driver is the large-scale expiration of brand-name drug patents. High-profile expirations include oncology biologics , GLP-1 receptor agonists, and cardiovascular agents, collectively representing a multi-billion-dollar generic opportunity across small-molecule and complex formulations.

- Rising Chronic Disease Burden and Geriatric Population: The US faces a compounding chronic disease burden, over 37 million Americans live with diabetes, more than 122 million with cardiovascular disease. These conditions require long-term pharmaceutical therapy, directly driving prescription volume for generics.

- FDA Drug Competition Action Plan and GDUFA Reforms: In FY-2025, around 689 generic drugs were approved by the FDA, including 92 first-time generics. In October 2025, the FDA launched a new pilot to fast-track ANDAs for domestically manufactured drugs, further boosting approval velocity.

Market Restraints

- Intense Price Competition and Margin Compression: The rapid entry of multiple generic competitors following patent expiry creates immediate and severe pricing pressure. Research indicates that the entry of the first three generic competitors typically reduces branded drug prices by 40–80% within 12 months. While beneficial for payers and patients, these dynamic compresses manufacturer margins, challenging profitability for companies reliant on commodity generics.

- Regulatory Compliance Costs and Manufacturing Standards: Meeting FDA current Good Manufacturing Practice (cGMP) requirements imposes significant capital costs and compliance burdens. The FDA issued over 105 warning letters in 2024, and plant inspections at API manufacturing sites in India and China, which supply over 80% of US generic APIs, have resulted in import alerts and supply disruptions. Compliance investment is a high operational cost for generic manufacturers.

Market Opportunities

- Complex Generics and Biosimilars Expansion: The shift to complex generics, inhalation products, transdermal patches, modified-release formulations, ophthalmic drugs, and sterile injectables offers significantly higher margins and limited competition compared to standard oral solid generics.

- Domestic Manufacturing Investment and Policy Tailwinds: The October 2025 FDA domestic manufacturing pilot program, combined with Inflation Reduction Act provisions and the BIOSECURE Act restricting foreign API sourcing, is incentivising US-based API and dosage form manufacturing.

- AI-Driven ANDA Development and Quality Assurance: In early 2025, the FDA issued its first-ever guidance on AI in drug development, catalyzing adoption across the generic industry. AI and machine learning are being applied to accelerate bioequivalence studies, automate regulatory submission preparation, and implement real-time quality assurance on manufacturing lines, reducing development costs and cycle times significantly.

Market Challenges

- Drug Shortages and Supply Chain Fragility: The persistent gap between ANDA approval and market launch, IQVIA estimates 37% of approved generics between 2013 and Q1 2024 had not launched, undermining the competitive potential of generic approvals. Injectables are the most shortage-prone category, with 75% of shortages involving unlaunched generics.

- Pharmacy Benefit Manager Consolidation and Pricing Power: The consolidation of PBMs into three dominant players gives these entities extraordinary leverage over generic dispensing and pricing. PBMs' use of proprietary formularies, preferred networks, and rebate arrangements can disadvantage smaller generic manufacturers and distort competitive market dynamics.

Emerging US Generic Drug Market Trends

1. Expansion into Complex Generics and Biosimilars

The US generic market is undergoing a structural transformation from standard oral solid dose products toward complex generics requiring advanced formulation expertise and sterile manufacturing capabilities. In April 2025, Biocon Pharma Limited, a wholly owned subsidiary of Biocon, has obtained approval from the U.S. Food and Drug Administration (FDA) for its Abbreviated New Drug Application (ANDA) for Everolimus tablets. The approved strengths include 0.25 mg, 0.5 mg, 0.75 mg, and 1 mg. Everolimus is prescribed to help prevent organ rejection in adult patients undergoing kidney or liver transplantation. This approval enhances Biocon’s portfolio of complex, vertically integrated pharmaceutical products.

2. AI Integration in ANDA Submissions and Manufacturing Quality

In 2025, the FDA released its first regulatory guidance on the use of artificial intelligence in drug development, signalling institutional endorsement of AI-assisted ANDA submissions. Leading generic companies, including Teva and Viatris, have deployed AI-driven quality assurance systems that reduce manufacturing variability and improve bioequivalence testing consistency.

3. Medicare Drug Price Negotiations and IRA Impact on Generic Demand

The Inflation Reduction Act's Medicare drug price negotiation provisions, effective January 1, 2026 for the first 10 negotiated drugs, are reshaping the branded-to-generic conversion dynamic. Government-negotiated prices for the first cohort are estimated to save USD 1.5 billion in annual out-of-pocket costs for beneficiaries. As negotiated branded prices approach generic levels in select categories, generic manufacturers are recalibrating their entry strategies toward the next wave of patent expirations in oncology and immunology with higher commercial upside.

4. Domestic Manufacturing Drive and Onshoring of API Production

The October 2025 FDA domestic manufacturing pilot program offers expedited ANDA approvals for drugs manufactured entirely in the United States. This initiative, aligned with broader legislative efforts including the BIOSECURE Act restricting reliance on Chinese and Indian API suppliers for federally purchased drugs, is catalysing capital investment in US-based pharmaceutical manufacturing.

5. Transparent Pricing Models and Direct-to-Consumer Generic Access

The emergence of transparent, direct-to-consumer generic pricing platforms, led by Cost Plus Drug Company, is disrupting the traditional opaque PBM-driven supply chain. By publishing actual manufacturing costs plus a fixed markup, these platforms have forced established generic distributors to reassess pricing strategies.

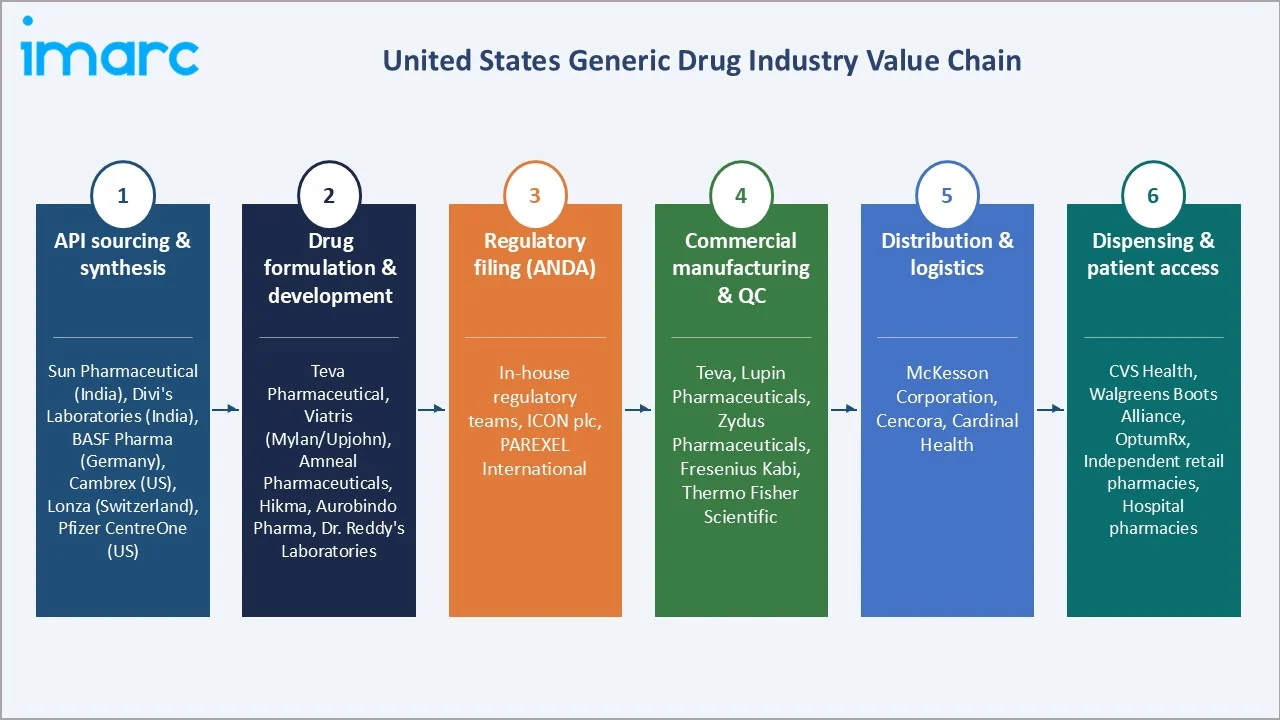

Industry Value Chain Analysis

The US generic drugs value chain spans six stages from active pharmaceutical ingredient (API) synthesis through patient dispensing. Formulation science and GMP-compliant manufacturing capture the highest value-add margins, while regulatory filing and distribution generate substantial working capital requirements that structurally favor large, vertically integrated generics manufacturers with dedicated regulatory affairs infrastructure.

|

Stage |

Key Players / Examples |

|

API sourcing & synthesis |

Sun Pharmaceutical (India), Divi's Laboratories (India), BASF Pharma (Germany), Cambrex (US), Lonza (Switzerland), Pfizer CentreOne (US) |

|

Drug formulation & development |

Teva Pharmaceutical, Viatris Inc., Amneal Pharmaceuticals, Hikma, Aurobindo Pharma, Dr. Reddy's Laboratories |

|

Regulatory filing (ANDA) |

In-house regulatory affairs teams at major generics manufacturers; CRO support via ICON plc and PAREXEL International |

|

Commercial manufacturing & QC |

Teva, Lupin Pharmaceuticals, Zydus Pharmaceuticals, Fresenius Kabi (injectables), Thermo Fisher Scientific |

|

Distribution & logistics |

McKesson Corporation, Cencora, Cardinal Health — the "Big Three" wholesale distributors controlling ~92% of US pharmaceutical distribution |

|

Dispensing & patient access |

CVS Health, Walgreens Boots Alliance, OptumRx (UHG), independent retail pharmacies, hospital pharmacies |

Vertically integrated generics manufacturers with captive API sourcing arrangements and in-house finished dose manufacturing — such as Teva's global API division supplying a significant share of its own finished drug production — achieve structurally lower cost-of-goods than pure-play formulators relying entirely on third-party API spot markets.

Technology Landscape in the United States Generic Drugs Industry

Synthesis & API Manufacturing Technology: Continuous Flow Chemistry and Process Intensification

Traditional batch API synthesis is being progressively supplemented by continuous flow chemistry platforms, which offer tighter control over reaction parameters (temperature, residence time, mixing) and reduce intermediate isolation steps. Continuous manufacturing applied to small-molecule API synthesis can reduce solvent consumption by 30–50% and cut cycle times by 60–70% versus equivalent batch routes.

Formulation Science: Oral Solid Dosage and Complex Drug Delivery

The dominant formulation technology for generic drugs remains immediate-release oral solid dosage (OSD), tablets and capsules, manufactured via wet granulation, dry granulation (roller compaction), and direct compression. For complex generics, formulation challenges are significant: extended-release polymer matrix systems using hydroxypropyl methylcellulose (HPMC) and ethylcellulose, abuse-deterrent formulations incorporating physical barriers and antagonist layering, and bioequivalence-sensitive narrow therapeutic index (NTI) drugs require extensive pharmacokinetic profiling.

Regulatory Technology: Electronic Common Technical Document (eCTD) and AI-Assisted ANDA Preparation

Regulatory technology (RegTech) platforms, including AI-assisted gap analysis tools from companies such as Veeva Systems and specialized ANDA assembly software, are reducing submission error rates and accelerating first-cycle approval probabilities.

Manufacturing Technology: Continuous Manufacturing and Process Analytical Technology (PAT)

The FDA actively promotes continuous manufacturing (CM) for finished dose forms as an alternative to batch manufacturing, citing real-time quality assurance advantages. CM platforms integrate feeding, blending, granulation, and tablet compression into an uninterrupted process, enabling real-time release testing (RTRt) in place of traditional end-product testing.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Segment |

Unbranded Generics |

83% |

2025 |

|

Therapy Area |

CNS |

16% |

2025 |

|

Drug Delivery |

Oral |

72% |

2025 |

|

Distribution Channel |

Retail Pharmacies |

78% |

2025 |

By Segment

To access detailed market analysis, Request Sample

Unbranded generics dominate the US generic drug market with an 83.0% share in 2025. Unbranded generics, also referred to as pure generics or non-proprietary generics, are dispensed under their International Nonproprietary Name (INN) and are identified solely by their active pharmaceutical ingredient.

Branded generics represent 17.0% of the 2025 market, marketed under proprietary trade names despite containing off-patent active ingredients. These products trade on brand equity, physician familiarity, and patient habit persistence to command price premiums above commodity unbranded equivalents.

By Distribution Channel

Retail pharmacies account for the highest share of the US generic drug market at 78.0% in 2025. Retail pharmacies, encompassing community chain pharmacies (CVS Pharmacy, Walgreens, Rite Aid), independent pharmacies, mail-order pharmacy services, and specialty pharmacy operators, dominate generic drug distribution.

Hospital pharmacies, representing 22.0% of the distribution channel, are the primary dispensing point for intravenous generics, oncology injectables, and hospital-administered acute care medications. Hospital formulary committees, operating under Value Analysis Committee (VAC) frameworks, systematically evaluate and substitute branded products with generic equivalents to reduce institutional drug expenditure.

Competitive Landscape

The US generic drug market is moderately consolidated at the top tier, with Teva Pharmaceutical, Viatris, and Sandoz (Novartis's generic division, listed independently in 2023) collectively commanding approximately 30–35% of the generic prescription volume market. The August 2025 merger of Mallinckrodt plc and Endo, Inc. created a new diversified therapeutics entity with a broad generic and branded portfolio, signalling continued consolidation pressure in the sector.

|

Company Name |

Key Product |

Market Position |

Core Strength |

|

Teva Pharmaceutical Industries |

Broad Generic Portfolio (Oral Solids, Injectables, Respiratory, CNS) |

Market Leader (~20–22%) |

One of the world's largest generic drug maker; vast API self-sufficiency; US generics anchor despite branded Copaxone decline |

|

Viatris Inc. |

Generic Injectables, Complex Generics, EpiPen (Branded) |

Market Leader (~10–12%) |

Complex generics pipeline; strong biosimilar entry strategy; global distribution scale |

|

Sandoz Group AG |

Broad Generics & Biosimilars (Zarxio, Hyrimoz) |

Strong Challenger (~8–10%) |

Spun off as independent entity; global biosimilars pioneer |

|

Sun Pharma |

Specialty Generics (Dermatology, Psychiatry, Ophthalmology) |

Strong Challenger (~5–7%) |

Ranbaxy integration; dermatology-led differentiation; growing branded-generic hybrid strategy |

|

Par Health Inc. |

Generic Oral Solids, Injectables, Controlled Substances |

Mid-Tier Challenger (~3–5%) |

Injectable and controlled-substance generics strength; assets reorganized under new ownership |

|

Lupin Pharmaceuticals |

Cardiovascular, CNS, Anti-Infective, Respiratory Generics |

Emerging Challenger (~3–4%) |

India-based; strong ANDA pipeline in the US; oral contraceptives and inhalation generics focus |

|

Dr. Reddy's Laboratories |

Oncology, Cardiovascular, Dermatology Generics |

Emerging Challenger (~3–4%) |

Vertically integrated API-to-formulation model; proprietary branded-generic play |

|

Pfizer |

Injectable Generics, Biosimilars (Inflectra, Retacrit) |

Injectable Specialist (~4–5%) |

Dominant injectable generics franchise; Pfizer's biosimilar commercialization engine |

Key companies include Teva Pharmaceutical Industries, Viatris Inc., Sandoz Group AG, Sun Pharmaceutical Industries, Par Health, Inc., Lupin Pharmaceuticals, Dr. Reddy's Laboratories, and Pfizer, among others.

Key Company Profiles

Teva Pharmaceutical Industries Ltd.

- Headquarters: Tel Aviv, Israel

- Market Position: Largest generic drug manufacturer globally; leading US generic market share by prescription volume

- Product Portfolio: Over 3,600 generic product registrations globally; US generics spanning oral solids, injectables, inhalation, dermatologicals, and biosimilars

- Recent Developments: In December 2025, Teva Pharmaceuticals has submitted a New Drug Application (NDA) to the U.S. Food and Drug Administration (FDA) for its olanzapine extended-release injectable suspension (TEV-749), intended for the once-monthly treatment of adults with schizophrenia. The formulation is designed as a long-acting subcutaneous injection that delivers olanzapine steadily over time, potentially improving patient adherence and treatment stability.

- Strategic Focus: Operational de-leveraging, complex generics (inhalation, CNS), biosimilars, and US domestic manufacturing investment

Viatris Inc.

- Headquarters: Canonsburg, Pennsylvania, USA

- Market Position: Top 3 US generic market share; extensive global generics footprint across 165+ countries

- Product Portfolio: Generics, branded generics, and branded specialty including EpiPen and Lyrica; biosimilars through Biocon Biologics partnership

- Recent Developments: In August 2025, Viatris received approval from the U.S. Food and Drug Administration for its iron sucrose injection, marking the first generic version of the branded therapy Venofer in the U.S. The product, used to treat iron deficiency anemia in patients with chronic kidney disease, will be available in multiple dosage strengths and is expected to launch shortly.

- Strategic Focus: Portfolio rationalisation, complex generics, biosimilar commercialisation, and new product launches in specialty injectables.

Sandoz Group AG

- Headquarters: Basel, Switzerland

- Market Position: Global generics and biosimilar leader; independently listed since October 2023 following Novartis spin-off

- Product Portfolio: Broad oral generic portfolio; world's largest biosimilar pipeline including Zarxio, Hyrimoz, and Cimerli; specialty injectables and ophthalmics

- Recent Developments: Post-separation from Novartis, Sandoz has accelerated its US biosimilar strategy, particularly in immunology and oncology supportive care, benefiting from the FDA's 2025 Phase III waiver policy for monoclonal antibody biosimilars.

- Strategic Focus: Biosimilar leadership, complex generics, institutional/hospital market penetration, and European and US market share consolidation.

Sun Pharmaceutical Industries Ltd.

- Headquarters: Mumbai, India

- Market Position: Fifth-largest global generic drug company; leading US specialty and generic market participant

- Strategic Focus: Specialty generics, dermatology, oncology injectables, and branded specialty pharmaceuticals

Market Concentration Analysis

The US generic drugs market exhibits moderate-to-high production-side concentration, with the top five generic pharmaceutical manufacturers collectively accounting for approximately 55–65% of total US generic drug revenues by volume and value. Teva Pharmaceuticals alone commands approximately 20–22% of the US generics market, with Viatris, Sandoz (Novartis), Hospira (Pfizer), and Sun Pharma forming the next tier at 5–12% each.

Investment & Growth Opportunities

Fastest-Growing Segments

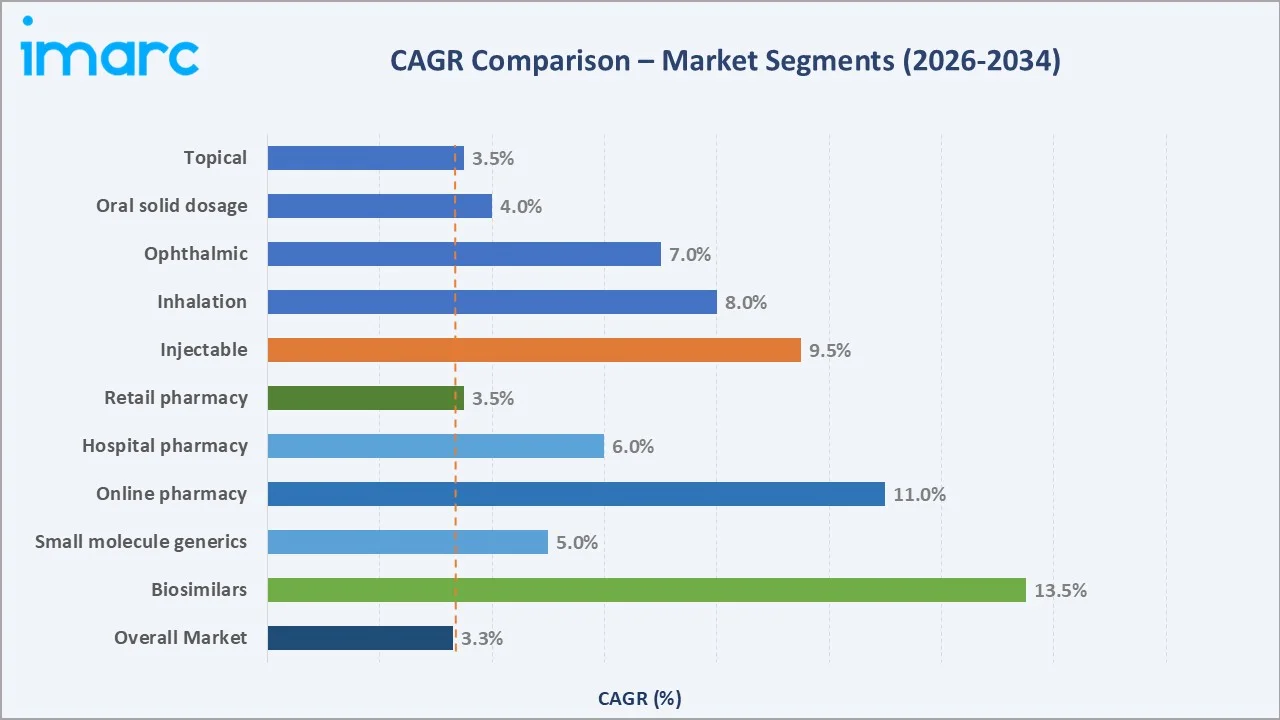

Biosimilars lead growth, driven by patent cliffs on blockbuster biologics like adalimumab and pembrolizumab. Specialty generics (~8.2% CAGR) and generic oncology (~7.6% CAGR) follow, fueled by IRA reforms and hospital formulary substitution pressure.

Emerging Markets

Medicaid/LIS channels and mail-order pharmacy platforms (~9.1% CAGR) are the fastest-expanding distribution segments, accelerated by PBM vertical integration and Part D restructuring. Rural and FQHC procurement remains underpenetrated and high potential.

Venture & Investment Trends

Private equity firms are consolidating specialty generic and injectable platforms at 8–12× EBITDA multiples. Domestic manufacturing reshoring is attracting federal procurement preference and HHS/DOD co-investment under BIOSECURE Act momentum. AI-driven ANDA acceleration tools are drawing active Series A–C rounds targeting first-to-file exclusivity capture.

Future US Generic Drug Market Outlook (2026-2034)

The US generic drug market is positioned for consistent, policy-supported expansion from USD 96.78 Billion (2025) to USD 129.20 Billion by 2034, representing incremental revenue of approximately USD 32 Billion over the forecast decade, driven by a CAGR of 3.3%. Growth will be predominantly driven by the complex generics and biosimilar sub-segments, which are expected to outpace the overall market rate as major biologic patents expire between 2025 and 2030.

The transition from traditional small-molecule oral solid generics to complex formulations, inhalation drugs, sterile injectables, transdermal delivery systems, modified-release formulations, and biosimilars, will define competitive differentiation and margin profiles over the forecast horizon.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 150 industry participants in 2024–2025, comprising bubble tea franchise operators, ingredient and equipment suppliers, retail buyers, food service distributors, and end consumers across Asia Pacific, North America, Europe, and the Middle East.

Secondary Research

Secondary research encompassed a comprehensive review of company press releases, franchise disclosure documents, trade publications (QSR Magazine, Food Business News, Nation's Restaurant News), industry databases (Euromonitor, Mintel), and publicly available market data including government trade statistics and tea industry association reports. Over 250 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of bottom-up outlet count and average revenue per outlet modeling, combined with top-down consumer expenditure analysis incorporating tea consumption data, café culture penetration rates, and social media trend analytics.

US Generic Drug Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Segments Covered | Unbranded, Branded |

| Therapy Areas Covered | CNS, Cardiovascular, Dermatology, Genitourinary/Hormonal, Respiratory, Rheumatology, Diabetes, Oncology, Others |

| Drug Deliveries Covered | Oral, Injectables, Dermal/Topical, Inhalers |

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies |

| Companies Covered | Teva Pharmaceutical Industries, Viatris Inc., Sandoz Group AG, Sun Pharma, Par Health Inc., Lupin Pharmaceuticals, Dr. Reddy's Laboratories, Pfizer, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the US Generic Drug Market Report

The US generic drug market reached USD 96.78 Billion in 2025 and is projected to reach USD 129.20 Billion by 2034.

The market is expected to expand at a compound annual growth rate (CAGR) of 3.3% during 2026-2034, driven by patent expirations, rising chronic disease prevalence, FDA ANDA acceleration, and payer demand for cost-effective prescriptions.

Unbranded generics hold the dominant share at 83.0% in 2025, reflecting widespread physician prescribing by INN, mandatory generic substitution laws in all 50 US states, and PBM formulary structures that prioritise the lowest-cost generic equivalent.

Retail pharmacies account for 78.0% of generic drug distribution in 2025, driven by community chain pharmacies, mail-order prescription services, and PBM-directed prescription flow.

Primary drivers include the large-scale patent expiry cycle, rising chronic disease burden, FDA Drug Competition Action Plan and GDUFA III reforms accelerating ANDA approvals, Medicare price negotiation under the Inflation Reduction Act driving generic adoption, and AI-enabled drug development and manufacturing quality improvements.

The FDA's domestic manufacturing pilot program offers expedited ANDA reviews for drugs manufactured entirely in the US, incentivising onshoring of API and dosage form production. This initiative supports supply chain resilience, reduces shortage risk, and provides participating companies with a regulatory time-to-market advantage.

Leading companies include Teva Pharmaceutical Industries, Viatris Inc., Sandoz Group AG, Sun Pharmaceutical Industries, Par Health, Inc., Lupin Pharmaceuticals, Dr. Reddy's Laboratories, and Pfizer, among others.

Key challenges include severe margin compression from multi-competitor entry following patent expiry, API supply chain dependency on India and China exposing the market to geopolitical and regulatory risks, persistent drug shortage dynamics, PBM consolidation reducing manufacturer pricing power, and escalating regulatory compliance costs under FDA cGMP standards.

Biosimilars represent the highest-growth sub-segment of the broader US generic market. With FDA Phase III waiver policies for monoclonal antibody biosimilars now in effect, and major biologic drugs including ustekinumab and vedolizumab entering generic competition by 2025–2027.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)