US Hair Care Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

US Hair Care Market Size, Share, Trends & Forecast (2026-2034)

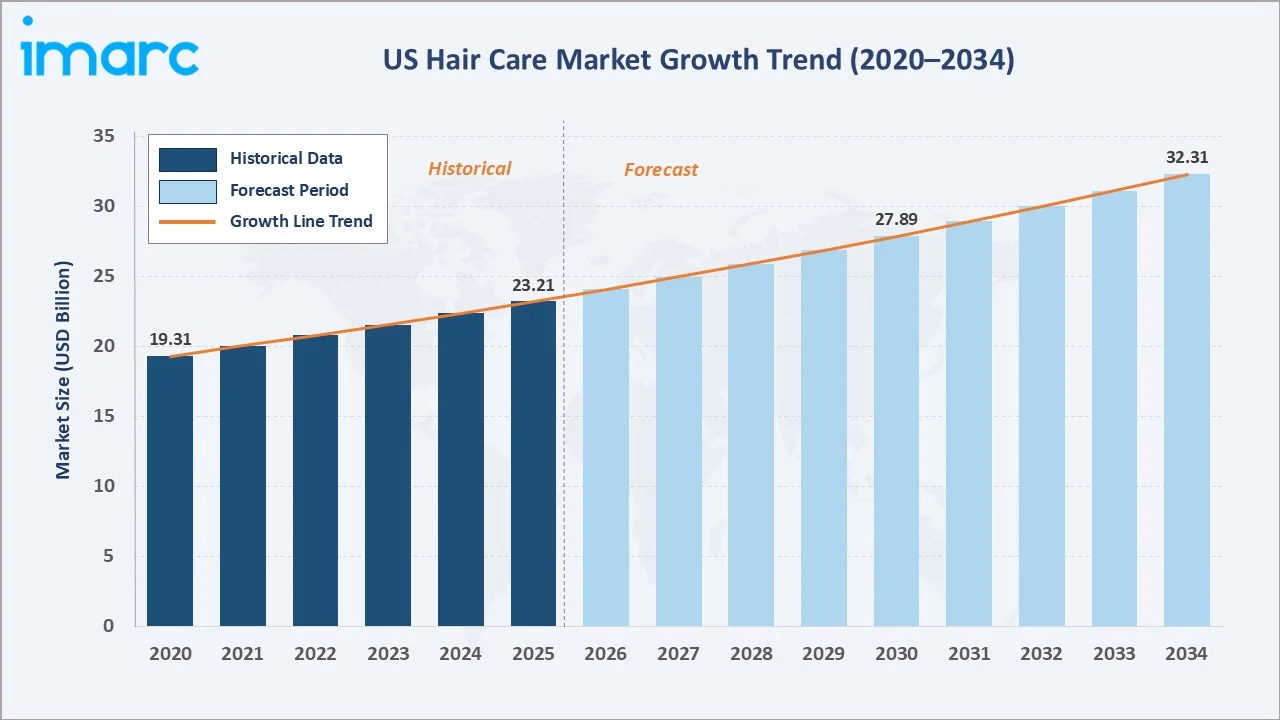

The US hair care market size was valued at USD 23.21 Billion in 2025 and is projected to reach USD 32.31 Billion by 2034, growing at a CAGR of 3.74% during 2026-2034. Evolving consumer preferences toward premium, natural, and specialized formulations, combined with rising scalp health awareness and expanding e-commerce infrastructure, underpin consistent market expansion across all demographic segments.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 23.21 Billion |

|

Forecast Market Size (2034) |

USD 32.31 Billion |

|

CAGR (2026-2034) |

3.74% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

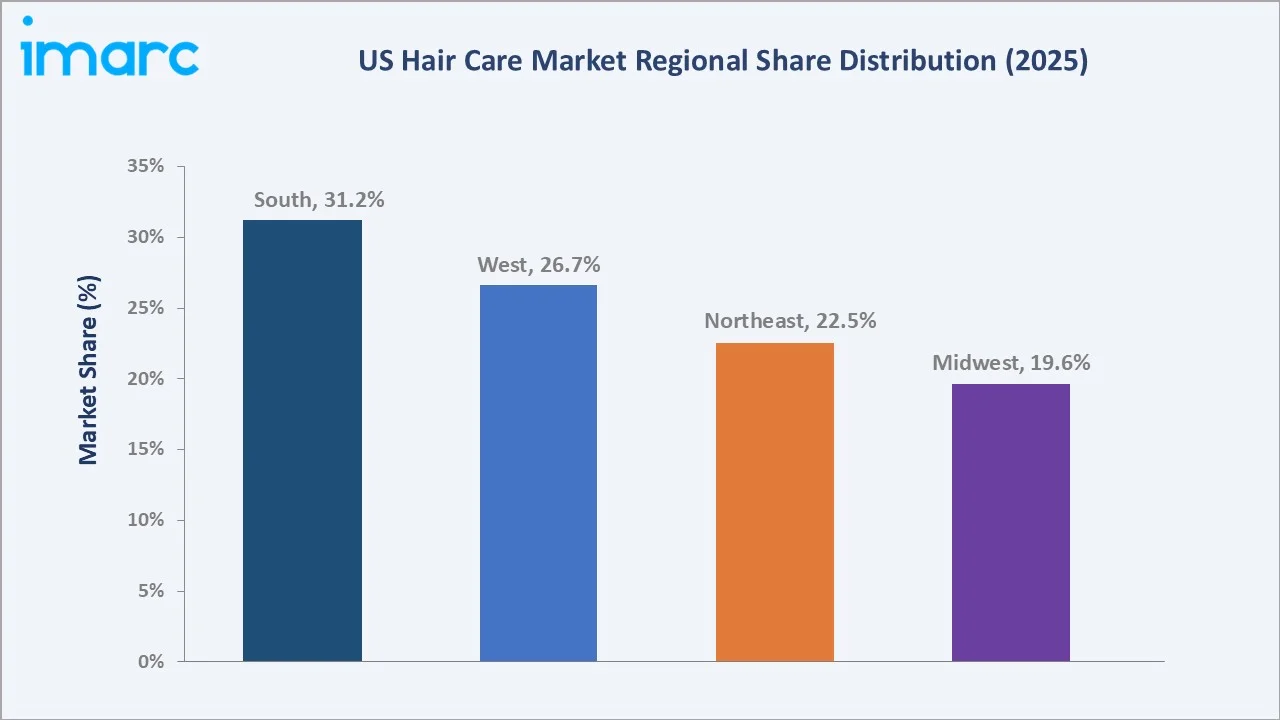

Largest Region |

South (31.2% share, 2025) |

|

Largest Product Segment |

Shampoo (45.0% share, 2025) |

|

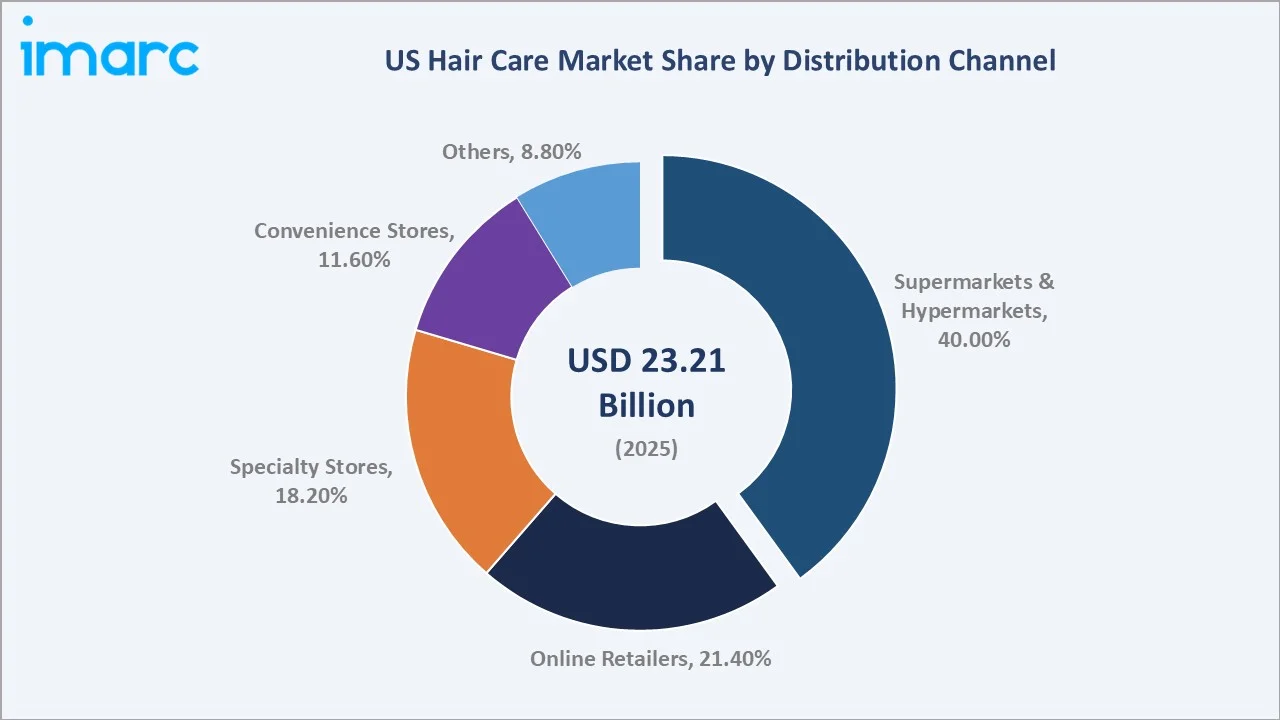

Leading Distribution Channel |

Supermarkets & Hypermarkets (40.0% share, 2025) |

The market encompasses a wide range of products, including shampoos, conditioners, hair oils, colorants, and styling solutions, catering to diverse hair types and preferences. Growth is driven by rising demand for clean-label, organic, and sulfate-free formulations, along with increasing adoption of personalized and salon-quality products at home.

To get more information on this market, Request Sample

The South dominates regionally with a 31.2% share in 2025. Shampoo leads product demand at 45.0%, while Supermarkets and hypermarkets command the largest distribution share at 40.0%. In February 2025, Cécred partnered with Ulta Beauty to launch its products across over 1,400 stores nationwide, signaling strong retailer confidence in the category's premiumization trajectory.

Executive Summary

The US hair care market represents a mature yet dynamically evolving industry characterized by accelerating premiumization, clean-label formulation trends, and the expansion of digital-first distribution channels. The market reached USD 23.21 Billion in 2025 and is forecast to surpass USD 32.31 Billion by 2034, representing a steady CAGR of 3.74% over the forecast period.

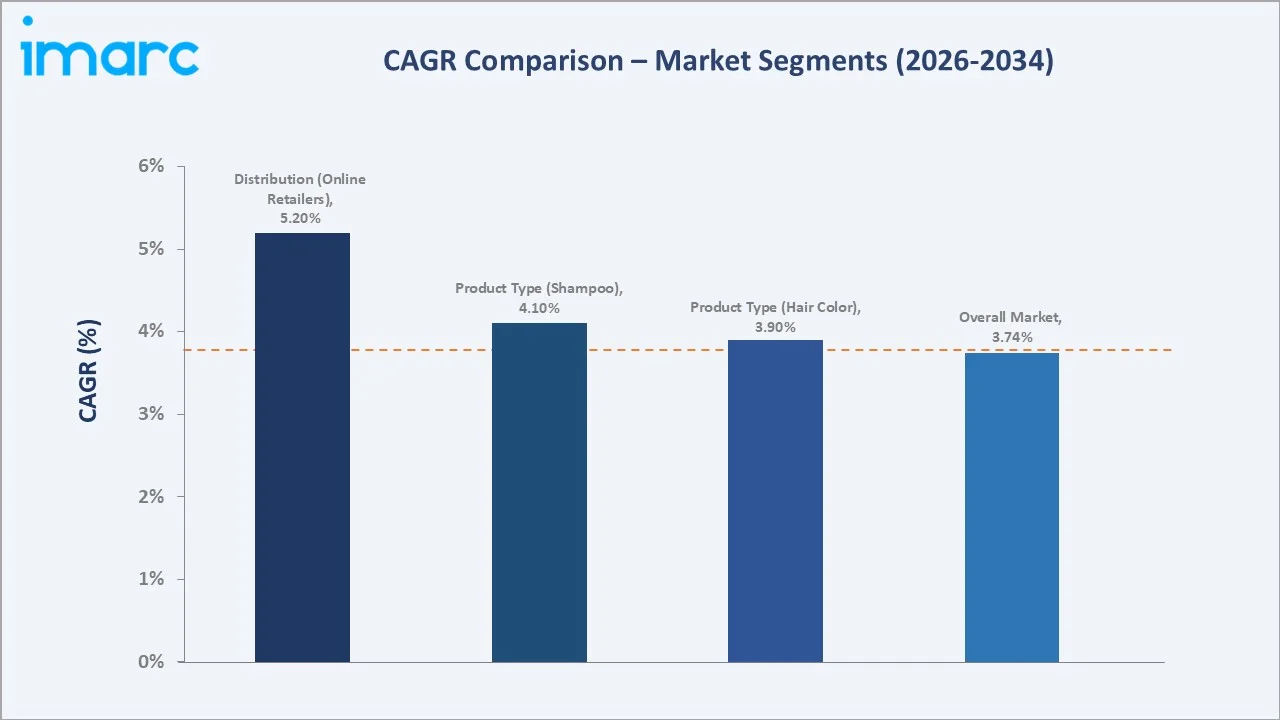

Shampoo dominates product demand at 45.0% in 2025, driven by daily consumer usage patterns and the proliferation of specialized variants addressing dandruff, volumizing, and damage repair. Supermarkets and hypermarkets remain the leading distribution channel at 40.0%, though online retailers are the fastest-growing channel at a 5.20% CAGR. The South holds the largest regional share at 31.2%, supported by high population density, warm climate driving year-round hair care product consumption, and strong retail infrastructure.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product Type) |

Shampoo – 45.0% share (2025) |

|

Second Largest Product Segment |

Hair Color – 17.6% share (2025) |

|

Leading Distribution Channel |

Supermarkets & Hypermarkets – 40.0% share (2025) |

|

Fastest Growing Channel |

Online Retailers – 21.4% share, 5.20% CAGR (2026-2034) |

|

Leading Region |

South – 31.2% share (2025) |

|

Top Companies |

L'Oréal S.A., Procter & Gamble, Unilever, Henkel AG & Co. KGaA, and Kao Corporation |

Key Analytical Observations Supporting the Above Data:

- Shampoo accounts for 45.0% of the US hair care market in 2025, sustained by daily usage frequency and continuous new variant launches. In April 2025, Prose launched a custom scalp serum, exemplifying the shift toward specialized scalp-centric shampoo and treatment hybrids.

- Hair Color (17.6%) is benefiting from the at-home coloring boom, inclusive shade range expansion, and the premiumization of salon-quality color kits available through retail. L'Oréal's acquisition of Color Wow in June 2025 strengthened its color-care portfolio in the U.S. and UK.

- Online Retailers (21.4%) represent the fastest-growing distribution channel at an estimated CAGR of 5.20%, propelled by subscription-based hair care models, personalized DTC brand experiences, and the growing influence of beauty influencers driving discovery and conversion on social commerce platforms.

- The South holds 31.2% of share in 2025. Warm climate conditions, high humidity, and a culturally diverse population with varied hair textures generate structurally elevated demand for specialized hair care formulations, particularly in the conditioner, styling, and treatment categories.

- More than 114 million people in the U.S. experience hair-related concerns, prompting Unilever to expand its Nutrafol portfolio with science-backed, dermatologist-recommended supplements and personalized hair health solutions.

US Hair Care Market Overview

The US hair care market encompasses a broad spectrum of products, including shampoos, conditioners, hair color formulations, styling products, treatments, and salon-professional offerings. The ecosystem spans raw material suppliers, formulation laboratories, contract manufacturers, brand owners, distributors, and diverse retail and e-commerce channels serving mass-market, premium, and professional consumer segments.

Structural demand is driven by rising consumer prioritization of hair and scalp wellness, increasing willingness to trade up to premium and specialized formulations, and the accelerating convergence of skincare science with hair care innovation. The US hair care market growth is further supported by demographic tailwinds, including a growing multicultural consumer base with diverse hair care needs, the aging population investing in hair health and loss prevention solutions, and Gen Z consumers driving demand for clean, sustainable, and ethically sourced products.

Market Dynamics

To evaluate market opportunities, Request Sample

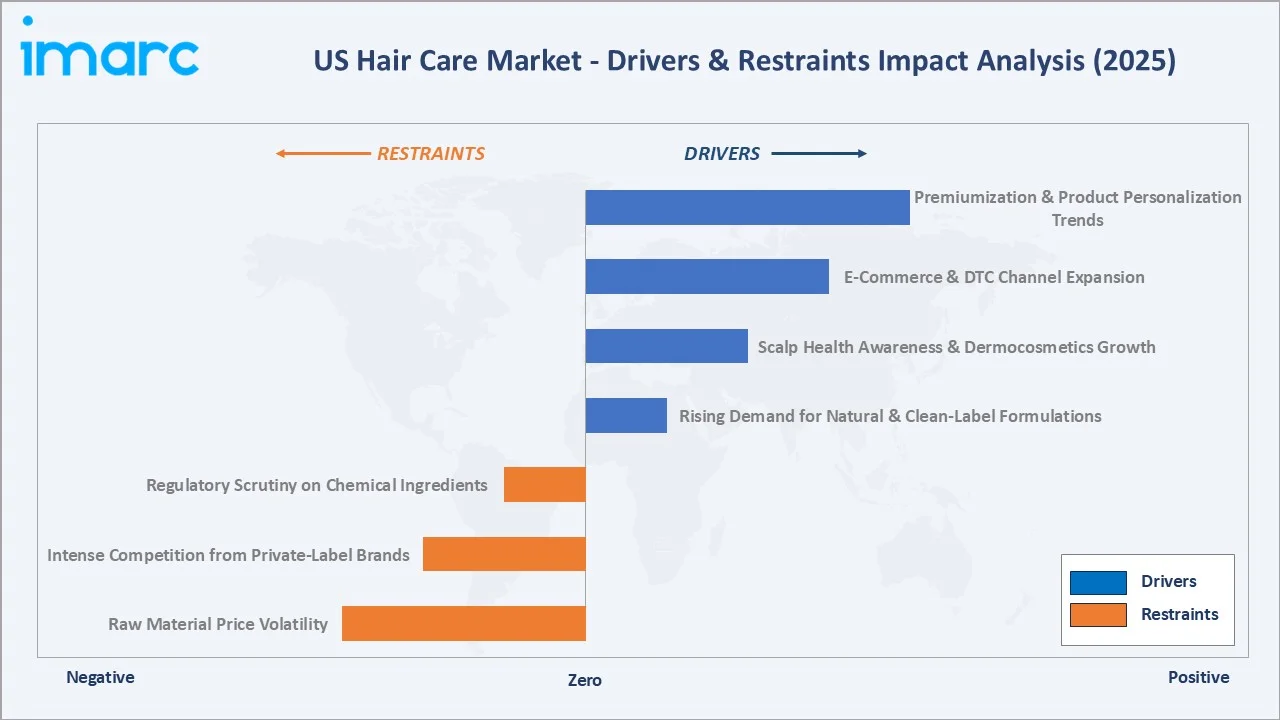

Market Drivers

- Rising Demand for Natural & Clean-Label Formulations: Consumer preference for products free from sulfates, parabens, silicones, and synthetic fragrances is reshaping brand portfolios across all tiers. A total of 74% of consumers regard organic ingredients as an important factor when choosing personal care products, creating structural demand for clean-formulated shampoos, conditioners, and treatments that deliver clinical efficacy alongside ingredient transparency.

- Scalp Health Awareness & Dermocosmetics Growth: Scalp care is transitioning from a niche concern to a mainstream wellness category. In May 2025, Prose launched a tailored scalp serum addressing individual scalp concerns through personalized diagnostics. The scalp health segment is growing at an estimated 7% CAGR through 2034, driven by the rising incidence of scalp conditions and the expansion of dermatology-aligned formulations into mass-market retail.

- E-Commerce & DTC Channel Expansion: Online retailers are the fastest-growing distribution channel for hair care in the U.S., growing at an estimated 5.20% CAGR through 2034. Subscription-based models, AI-powered hair diagnostic tools, and personalized recommendation engines offered by brands including Prose, Function of Beauty, and Curology deepen consumer engagement and enhance lifetime value.

- Premiumization & Product Personalization Trends: Consumers across income segments are trading up to premium hair care, with professional salon brands, including Kérastase, Redken, and Bumble and bumble, increasingly accessible through specialty retailers and e-commerce. Personalized formulations addressing individual hair texture, porosity, and scalp conditions command 2–3x price premiums over mass-market equivalents.

Market Restraints

- Raw Material Price Volatility: Hair care formulations incorporate specialty botanical extracts, silicones, keratin proteins, and proprietary delivery systems. Supply chain disruptions affecting key raw material sourcing regions, particularly for plant-derived actives from South America and Southeast Asia, periodically drive cost inflation that compresses manufacturer margins.

- Intense Competition from Private-Label Brands: Major retailers, including Target, Walmart, and Costco, have expanded private-label hair care ranges that offer comparable formulation performance at 30–50% price discounts versus branded equivalents. This intensifies pricing pressure on mid-tier branded hair care and limits revenue growth in mass-market shampoo and conditioner categories.

- Regulatory Scrutiny on Chemical Ingredients: The FDA's increased scrutiny of formaldehyde-releasing agents in hair straightening products and the California Safe Cosmetics Program's expanded disclosure requirements create compliance complexity and reformulation costs, particularly for hair color and chemical treatment categories.

Market Opportunities

- Scalp-Centric & Nutraceutical Hair Wellness: Unilever's acquisition of Nutrafol signals the convergence of ingestible hair wellness supplements with topical hair care. This USD 4.2 billion addressable segment by 2030 encompasses scalp serums, growth treatments, and hair-health nutraceuticals that position hair care within the broader wellness economy.

- Inclusive Hair Care for Multicultural Consumers: The U.S. multicultural consumer population, representing over 40% of the national population, has historically been underserved by mass-market hair care. Brands developing specialized formulations for textured, coily, and mixed hair types are capturing high-growth, high-loyalty consumer segments.

- Sustainable Packaging and Refillable Systems: Consumer demand for sustainable packaging, particularly refillable bottles, concentrated solid formats, and recycled-content packaging, is creating product differentiation opportunities. Brands successfully communicating sustainability credentials command premium positioning and access to sustainability-conscious retail shelf space in specialty and natural channels.

Market Challenges

- Brand Proliferation and Consumer Attention Fragmentation: The DTC boom has generated thousands of new hair care brands competing for digital shelf space and consumer attention. Established brands face escalating digital marketing costs, with U.S. beauty sector CPAs increasing 35% between 2022 and 2025, while new entrants struggle to achieve sustainable customer acquisition economics.

- Supply Chain Localization Pressure: Trade policy uncertainty and rising reshoring expectations are prompting multinational hair care manufacturers to evaluate localized production strategies for the U.S. market, adding capital investment requirements and operational complexity.

Emerging Market Trends

1. Rising Demand for Scalp-Centric Formulations

In May 2025, Prose launched a tailored scalp serum designed to address individual scalp concerns, reflecting the US hair care market trend toward diagnostic-driven, personalized treatment solutions. Platforms including Prose and Function of Beauty use AI-powered questionnaires to deliver customized scalp care regimens, achieving subscription retention rates significantly above industry average.

2. Premiumization and Celebrity-Driven Brand Launches

In February 2025, Cécred, the hair care brand founded by Beyoncé Knowles-Carter, expanded into retail through an exclusive partnership with Ulta Beauty, launching across more than 1,400 stores nationwide and online, marking the retailer’s largest hair care rollout. In June 2025, L'Oréal's acquisition of Color Wow illustrates how legacy multinationals are acquiring premium indie brands to access the fast-growing prestige hair care segment.

3. Clean-Label and Sustainability-Led Innovation

The US hair care market trend toward clean formulation is now extending beyond ingredient exclusions to encompass full lifecycle sustainability, from sustainably sourced botanical actives and biodegradable formulations to refillable packaging systems and waterless concentrate formats. Brands communicating credible sustainability stories achieve superior shelf placement in specialty natural channels and generate higher social media engagement metrics among Gen Z and millennial consumers.

4. Technology Integration in Personalized Hair Care

AI-powered hair and scalp diagnostic tools, accessible via mobile applications and in-store consultations, analyze hair texture, porosity, scalp condition, and environmental stress factors to generate bespoke product recommendations. Brands including Function of Beauty and Curology are commercializing clinical-grade personalization at accessible price points, achieving strong customer lifetime values.

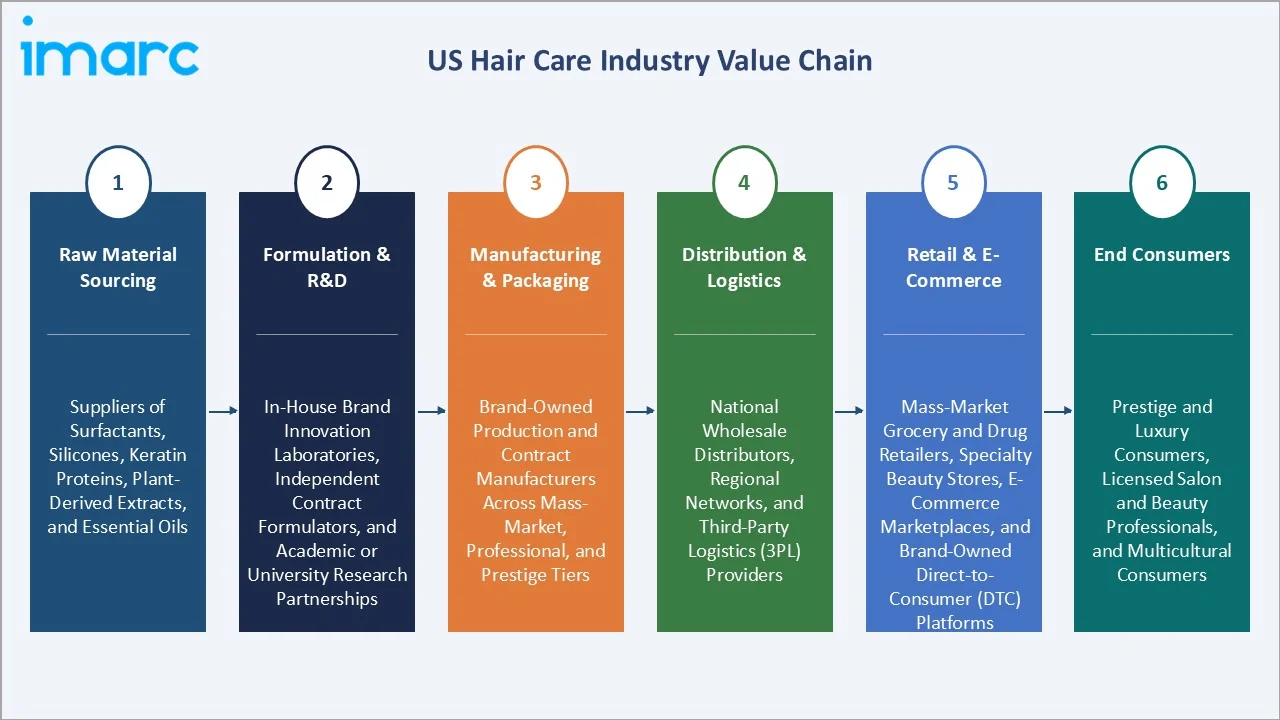

Industry Value Chain Analysis

The US hair care value chain encompasses raw material sourcing through end-consumer delivery, with each stage populated by specialized operators whose performance directly influences product quality, formulation efficacy, and retail competitiveness.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Suppliers of specialty chemical and botanical inputs, including surfactants, silicones, keratin proteins, plant-derived extracts, and essential oils |

|

Formulation & R&D |

In-house brand innovation laboratories, independent contract formulators, and academic or university research partnerships |

|

Manufacturing & Packaging |

Brand-owned production facilities and contract manufacturers that batch, fill, and package hair care products across mass-market, professional, and prestige tiers |

|

Distribution & Logistics |

National wholesale distributors, regional distribution networks, and third-party logistics (3PL) providers |

|

Retail & E-Commerce |

Mass-market grocery and drug retailers, specialty beauty stores, e-commerce marketplaces, and brand-owned direct-to-consumer (DTC) platforms |

|

End Consumers |

Prestige and luxury consumers, licensed salon and beauty professionals, and multicultural consumers |

Technology Landscape in the US Hair Care Industry

AI-Powered Personalization Platforms

L'Oréal's ModiFace technology, deployed across Redken, Kérastase, and Garnier digital touchpoints, enables consumers to virtually try hair colors and assess scalp conditions through smartphone cameras. Function of Beauty's AI questionnaire generates over 54 trillion possible product combinations, delivering genuinely personalized formulations at mass-market scale. These platforms achieve 40–60% repeat purchase rates versus 15–25% for traditional retail, demonstrating the commercial value of personalization infrastructure.

Biotech-Derived Active Ingredients

Probiotic-derived actives, biosynthetic keratin proteins, and fermented botanical extracts deliver clinical efficacy with improved sustainability profiles. Brands including Virtue Labs (alpha keratin 60ku protein) and Prose (microbiome-balancing prebiotic systems) are commercially demonstrating biotech-derived formulation advantages.

Sustainable Packaging Innovation

Unilever's Love Beauty and Planet brand offers refillable conditioner systems in Target stores, while Schwarzkopf Professional focuses on sustainability through circular packaging, aiming for 100% recyclable or reusable packaging and a 50% reduction in virgin plastic use, alongside increased adoption of recycled and bio-based materials.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Shampoo |

45.0% |

2025 |

|

Distribution Channel |

Supermarkets and Hypermarkets |

40.0% |

2025 |

|

Region |

South |

31.2% |

2025 |

By Product Type

Shampoo dominates the product type segment with a 45.0% share in 2025. Its dominance reflects universal daily usage patterns, the broadest demographic penetration of any hair care category, and sustained new variant introductions addressing specific hair and scalp conditions, from anti-dandruff to bond-repair and scalp microbiome-balancing formulations.

To access detailed market analysis, Request Sample

Hair Color holds 17.6% share, growing through expanded at-home coloring adoption and L'Oréal's June 2025 acquisition of Color Wow. Conditioner accounts for 15.8%, with growth driven by moisture-focused formulations targeting heat-damaged and chemically treated hair. Hair styling products represent 12.9%, evolving toward multi-benefit formulations that combine style with treatment.

By Distribution Channel

Supermarkets and hypermarkets command a 40.0% distribution share in 2025, maintaining dominance through comprehensive product assortments, competitive pricing facilitated by promotional cycles and loyalty programs, and widespread geographic presence enabling convenient access across urban and suburban markets nationwide.

Online Retailers represent 21.4% of the market, the fastest-growing channel at an estimated CAGR of 5.20% through 2034. Subscription-based hair care models, influencer-driven discovery, and algorithm-powered personalized recommendations are accelerating digital adoption. Specialty stores account for 18.2%, driven by Ulta Beauty and Sephora's expansion of professional and prestige hair care assortments.

Regional Market Insights

The South's market leadership (31.2%, 2025) reflects a combination of high population density, culturally diverse consumer demographics with varied hair care needs, warm and humid climate conditions that drive elevated product usage, and robust retail infrastructure across Texas, Florida, Georgia, and the Carolinas.

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

31.2% |

Multicultural demand, warm climate, strong retail coverage |

|

West |

26.7% |

Clean beauty adoption, premium DTC brands, coastal salon culture |

|

Northeast |

22.5% |

High-income urban consumers, salon professional demand, and professional product spend |

|

Midwest |

19.6% |

Mass-market value focus, supermarket-led distribution, growing natural channel |

The West is growing fastest among all regions, driven by California's progressive consumer base with high clean beauty adoption, the concentration of DTC and digitally-native hair care brands headquartered in Los Angeles, and the dense Ulta Beauty and Sephora store network enabling prestige hair care access across the region. Oregon and Washington contribute to a growing demand for natural and organic formulations through the well-developed Pacific Northwest natural retail ecosystem.

Competitive Landscape

The US hair care market exhibits high concentration at the top tier, with L'Oréal S.A., Procter & Gamble, and Unilever collectively commanding an estimated 45–55% of total U.S. hair care retail value in 2025. These multinationals leverage vast brand portfolios spanning mass-market, premium, and professional segments, and deep retailer relationships cultivated across decades of category management.

|

Company |

Brand Portfolio |

Market Position |

Core Strength |

| L'Oréal S.A. | L'Oréal Paris, Kérastase, Redken, Color Wow | Market Leader | World's #1 hair care; Color Wow acquisition Jun 2025; ModiFace AI; USD 14.5B hair revenue |

| Procter & Gamble | Pantene, Head & Shoulders, Herbal Essences | Market Leader | Mass-market dominance; P&G The Science Behind; head & shoulders global #1 anti-dandruff |

| Unilever | Dove, TRESemmé, K18, Nexxus, Nutrafol | Market Leader | Scalp wellness entry; TRESemmé strong mass-market share |

| Henkel AG & Co. KGaA |

Schwarzkopf, Authentic Beauty Concept, Bain de Terre, BC Bonacure, Schwarzkopf Gliss, Joico, among others |

Strong Challenger | Professional color leadership; Schwarzkopf salon brand; sustainability BOLD initiative |

| Kao Corporation | Essential, GUHL, JOHN FRIEDA, Liese, melt, among others | Challenger | John Frieda color brand strength, Goldwell professional salon leadership |

Strategic acquisitions, including L'Oréal's purchase of Color Wow in June 2025 and Unilever's acquisition of Nutrafol, continue to reshape market share dynamics in the fast-growing scalp health and prestige segments.

Key Company Profiles

L'Oréal S.A.

L'Oréal, headquartered in Clichy, France, with major U.S. operations across New York and New Jersey, is the world's largest beauty company and holds the leading position in the US hair care market through its Consumer, Professional, and Luxury divisions.

- Product Portfolio: L'Oréal Paris, Kérastase, Redken, and Color Wow, among others.

- Recent Developments: In June 2025, L’Oréal signed an agreement to acquire Color Wow. The acquisition strengthened L’Oréal’s Professional Products portfolio and supports its strategy to expand in high-growth premium haircare.

- Strategic Focus: AI-powered personalization via ModiFace; BeautyTech investment; sustainable formulation transition; premiumization of U.S. drug store and specialty channel assortments.

Procter & Gamble

Procter & Gamble, headquartered in Cincinnati, Ohio, is the leading U.S. hair care mass-market manufacturer, with Pantene and Head & Shoulders among the highest-revenue hair care brands in the U.S. market.

- Product Portfolio: Pantene, Head & Shoulders, and Herbal Essences, among others.

- Recent Developments: In January 2026, Head & Shoulders launched the BARE Itchy Scalp Relief Serum, a minimalist scalp treatment with just 9 ingredients designed to provide instant itch relief and maintain anti-dandruff protection between washes.

- Strategic Focus: Scalp health innovation; digital consumer engagement; sustainable packaging targets; emerging markets expansion leveraging U.S. brand equity.

Unilever

Unilever, headquartered in London and Rotterdam, operates a diversified U.S. hair care portfolio spanning mass-market, premium, and professional segments, with a strategic pivot toward scalp health and hair wellness through the Nutrafol acquisition.

- Product Portfolio: Dove, TRESemmé, Nexxus, K18, and Nutrafol, among others.

- Recent Developments: Unilever reported third-quarter 2025 underlying sales growth of 3.9% and strong momentum in its Beauty & Wellbeing division, which grew 5.1%, driven by premium hair care brands like Dove, K18, and Nutrafol.

- Strategic Focus: Hair wellness ecosystem development; sustainable packaging; multicultural hair care expansion; Nutrafol integration into hair health portfolio.

Market Concentration Analysis

The US hair care market exhibits high concentration at the manufacturing and brand tier, with the top three players, L'Oréal S.A., Procter & Gamble, and Unilever, collectively commanding an estimated 45–55% of U.S. retail value. However, the emergence of DTC brands, celebrity-backed lines, and indie clean beauty brands is creating meaningful fragmentation in the premium and specialty segments, disrupting established share dynamics.

Acquisition activity remains the primary strategic response to indie brand disruption. L'Oréal's Color Wow acquisition, Unilever's Nutrafol purchase, and Estée Lauder's long-term ownership of Aveda and Bumble and bumble demonstrate that multinationals are acquiring founder-led brands with strong consumer loyalty rather than attempting organic category entry.

Investment & Growth Opportunities

Fastest Growing Segments

Scalp health and nutraceutical hair wellness (estimated 7% CAGR through 2034), online retail and DTC subscription models (5.20% CAGR), and personalized hair care via AI diagnostics (8% CAGR) represent the three highest-growth investment vectors. Together, these opportunities address a combined addressable market of approximately USD 6.5 billion by 2030 within the U.S. hair care ecosystem.

Multicultural Hair Care Market

The multicultural hair care segment, serving African-American, Latina, Asian-American, and mixed-heritage consumers with textured, coily, and curly hair formulations, remains strategically underpenetrated by major multinationals. Brands successfully developing authentic, efficacious, and culturally resonant products for these segments command high consumer loyalty and premium pricing.

Venture and Private Equity Investment Trends

- Key investment themes include personalized hair care technology platforms, biotech-derived ingredient suppliers serving the clean formulation trend, scalp microbiome research-based product development, and waterless/solid format innovation reducing packaging and logistics costs.

- PE-backed roll-up strategies targeting prestige and professional hair care brands — particularly those with strong salon distribution networks and DTC digital channels — continue to attract significant capital in the U.S. beauty sector.

Future Market Outlook (2026-2034)

The US hair care market is positioned for steady, innovation-driven growth through 2034. From a base of USD 23.21 Billion in 2025, the market is projected to reach USD 32.31 Billion by 2034, representing total incremental value creation of USD 9.10 Billion over the forecast decade.

The market's growth trajectory will be shaped by three structural megatrends: the convergence of hair care with wellness and clinical dermatology, the accelerating shift to digital and DTC distribution, and the ongoing premiumization of the mass market. Brands that successfully navigate the clean-label imperative, invest in AI-personalization infrastructure, and develop authentic multicultural product offerings will capture a disproportionate share of the USD 32.31 Billion forecast market.

Long-term, the US hair care market demonstrates defensive demand characteristics; hair care remains a daily-use essential across economic cycles, combined with significant premiumization upside as scientific innovation and consumer education elevate category average selling prices. Regulatory evolution toward ingredient transparency and sustainability mandates will further differentiate brands investing in clean, biotech-derived, and sustainably packaged formulations from commodity private-label competitors.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 110 industry participants in 2024–2025, including hair care brand executives, retail category managers, salon professionals, independent beauty advisors, dermatologists specializing in scalp conditions, and a representative consumer panel of 2,200 U.S. hair care purchasers across the South, West, Northeast, and Midwest regions.

Secondary Research

Secondary research encompassed a systematic review of company earnings reports, SEC filings, Euromonitor International beauty market data, Mintel consumer research publications, trade publications (CEW, Beauty Packaging, Cosmetics & Toiletries), IQVIA retail scanner data, and U.S. Census Bureau consumer expenditure surveys. Over 190 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating U.S. Bureau of Economic Analysis personal consumption expenditure data for personal care products, retail sell-through scanner data, and brand-reported net sales growth. A base-case CAGR of 3.74% reflects consensus analyst estimates validated against reported manufacturer revenue growth rates and category-level scanner data trends.

US Hair Care Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Shampoo, Hair Color, Conditioner, Hair Styling Products, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Convenience Stores, Online Retailers, Others |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | L'Oréal S.A., Procter & Gamble, Unilever, Henkel AG & Co. KGaA, Kao Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the US Hair Care Market Report

The US hair care market reached USD 23.21 Billion in 2025 and is projected to reach USD 32.31 Billion by 2034.

The market is expected to grow at a CAGR of 3.74% during 2026-2034, supported by clean-label demand, scalp health awareness, e-commerce expansion, and product premiumization trends.

The South leads with a 31.2% share in 2025, driven by a large, culturally diverse population, warm climate conditions generating high product usage, and robust retail infrastructure across Texas, Florida, and Georgia.

The shampoo segment holds the largest product share at 45.0% in 2025 (approx. USD 10.44 Billion), sustained by daily consumer usage patterns and continuous new variant launches addressing specific hair and scalp concerns.

Supermarkets and hypermarkets lead with a 40.0% channel share in 2025, benefiting from comprehensive product assortments, competitive pricing, and widespread geographic access. Online Retailers are the fastest-growing channel at 5.20% CAGR through 2034.

Key players include L'Oréal S.A., Procter & Gamble, Unilever, Henkel AG & Co. KGaA, and Kao Corporation.

Key drivers include rising demand for natural and clean-label formulations, scalp health awareness and dermocosmetics growth, e-commerce and DTC channel expansion (Online Retailers CAGR: 5.20%), and premiumization and product personalization through AI diagnostic platforms.

High-growth opportunities include scalp health and nutraceutical hair wellness platforms (7% CAGR), AI-powered personalized hair care subscriptions, multicultural hair care for textured and coily hair segments (USD 2.8 Billion incremental opportunity by 2030), and sustainable packaging and waterless format innovation aligned with clean beauty consumer expectations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)