US Healthcare Advertising Market Size, Share, Trends and Forecast by Product Type, 2026-2034

US Healthcare Advertising Market Size, Share, Trends & Forecast (2026-2034)

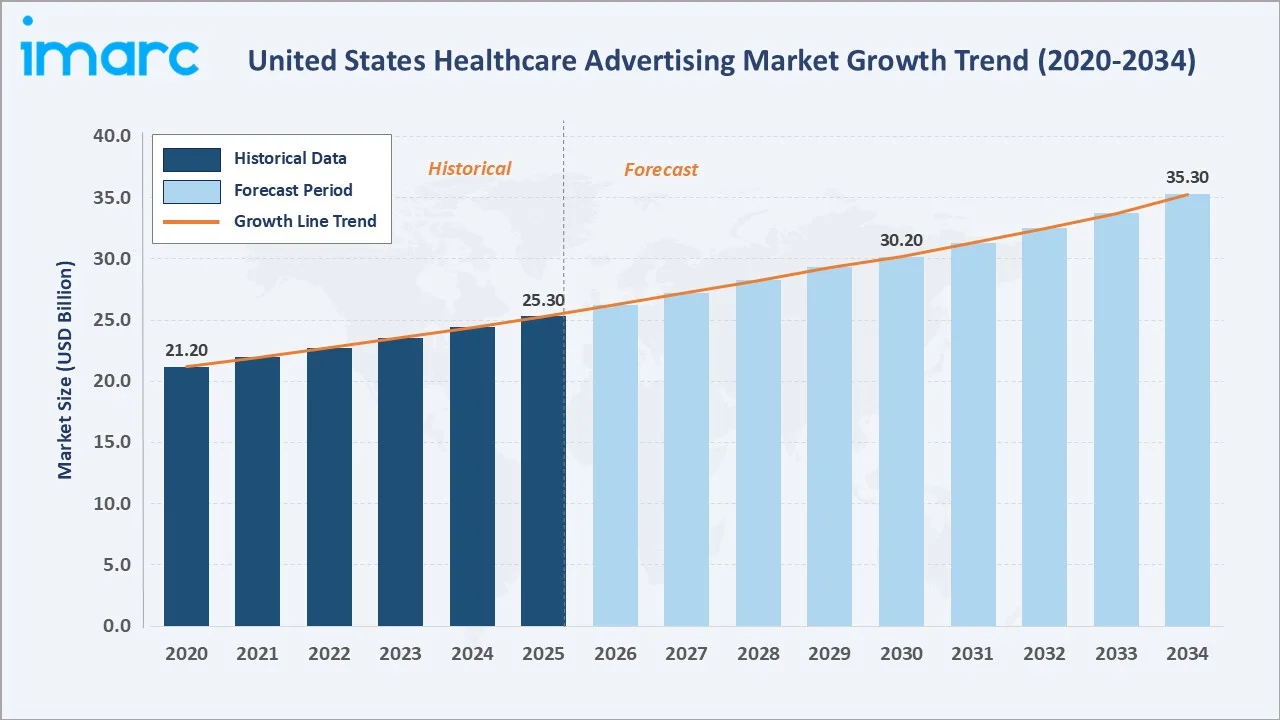

The US healthcare advertising market size increased from USD 25.3 Billion in 2025 to USD 26.2 Billion in 2026 and is projected to reach USD 35.3 Billion by 2034, expanding at a CAGR of 3.6% during the forecast period 2026-2034. Growth is driven by the rapid shift to digital advertising, rising direct-to-consumer pharmaceutical spend, and growing health awareness campaigns.

Market Snapshot

|

Metric |

Value |

|

Base Year Market Size (2025) |

USD 25.3 Billion |

| Market Size (2026) | USD 26.2 Billion |

|

Forecast Market Size (2034) |

USD 35.3 Billion |

|

CAGR (2026-2034) |

3.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2020-2025 |

|

Largest Segment (Product Type) |

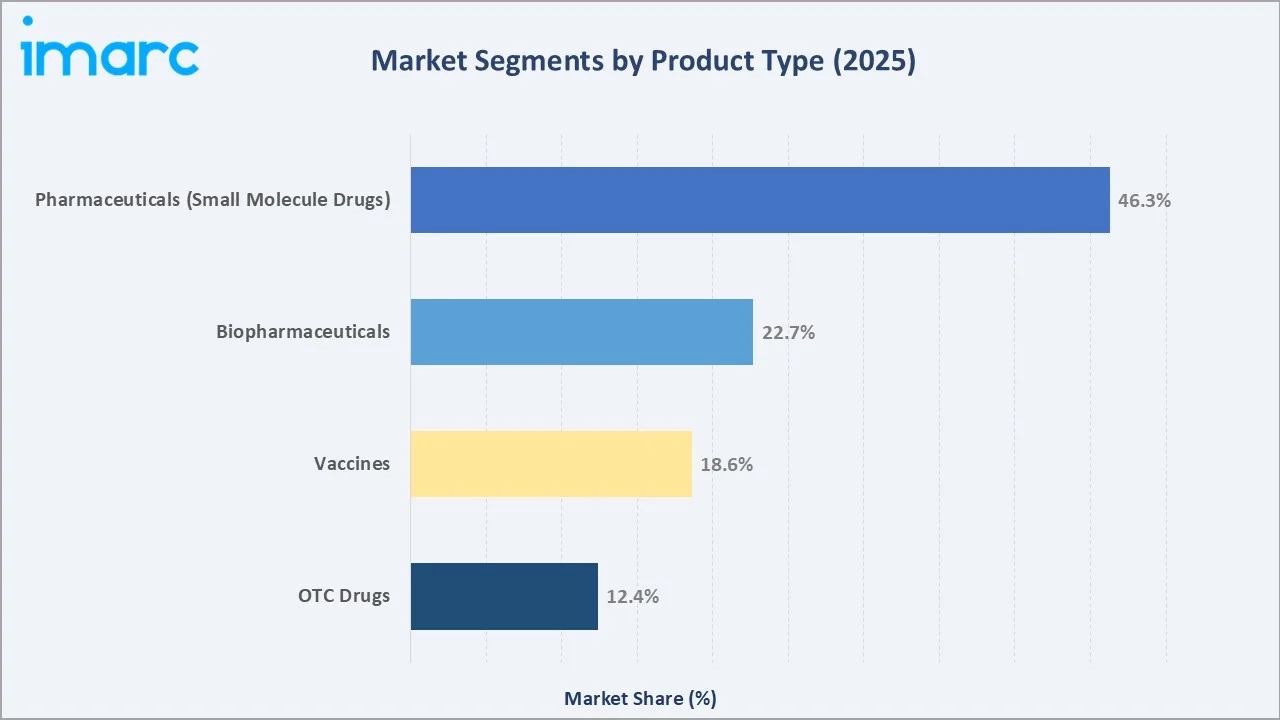

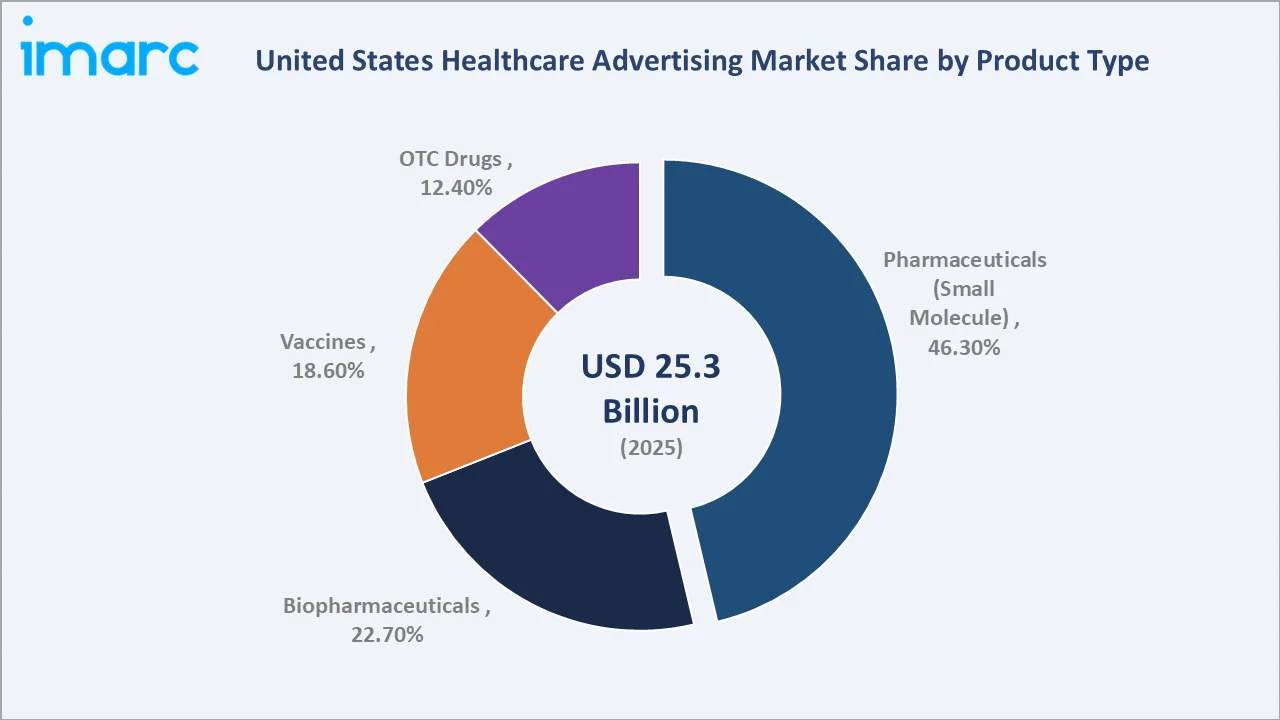

Pharmaceuticals (Small Molecule Drugs) – 46.3% (2025) |

Pharmaceuticals (small molecule drugs) lead all product segments with a 46.3% market share in 2025. WebFX reports that the average cost per lead in healthcare typically ranges from USD 200 to USD 500, with most providers falling closer to the midpoint of this range.

To get more information on this market, Request Sample

With healthcare spending continuing to rise, companies are investing heavily in advertising to capture the attention of consumers, healthcare professionals, and patients. The market is shaped by a blend of traditional advertising methods, including TV and print, alongside the increasing dominance of digital platforms such as social media and search engines.

Executive Summary

The US healthcare advertising market continues to exhibit steady expansion, driven by the rapid digitalization of media consumption, a growing pharmaceutical innovation pipeline, and the increasing empowerment of patients as active healthcare decision-makers. The market grew from USD 25.3 Billion in 2025 to USD 26.2 Billion in 2026, and is projected to reach USD 35.3 Billion by 2034.

Pharmaceuticals (Small Molecule Drugs) dominate product-type spending at 46.3% of market share in 2025, fueled by extensive branded prescription DTC campaigns. Biopharmaceuticals follow at 22.7%, propelled by high-value biologics launches for oncology, immunology, and rare diseases. In 2025, healthcare and pharma digital advertising spending is estimated at USD 24.8 Billion, a year-on-year increase of more than 13.3%, with social media overtaking linear TV as a primary channel for the first time.

The Northeast and West Coast regions represent the largest US advertising hubs, hosting the highest concentration of pharmaceutical headquarters and academic medical centers. Regulatory dynamics, including the FDA's evolving DTC oversight and FTC scrutiny of health claims, continue to shape campaign strategies. Looking ahead, AI-powered precision targeting, real-world data analytics, and expanded telemedicine advertising are set to redefine the competitive landscape for both established pharmaceutical advertisers and emerging digital health platforms.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product Type) |

Pharmaceuticals (Small Molecule Drugs) -46.3% share (2025) |

|

Fastest Growing Segment |

Biopharmaceuticals - driven by biologics DTC & precision targeting |

|

Top Companies |

Johnson & Johnson Services, Inc., Pfizer Inc., Eli Lilly and Company, Merck & Co., Inc, and AstraZeneca plc |

|

Market Opportunity |

AI-driven programmatic healthcare advertising projected at USD 8B+ by 2034 |

Key Analytical Observations Supporting the Above Data:

- Pharmaceuticals (Small Molecule Drugs) dominate at 46.3% (2025), fueled by massive, branded prescription DTC campaigns across television, digital video, and search. The US and New Zealand are the only countries permitting DTC prescription drug advertising, creating a structurally unique market.

- Biopharmaceuticals at 22.7% (2025) reflect strong DTC investment in biologics for oncology, autoimmune disorders, and rare diseases, with leading companies deploying AI-powered audience segmentation to engage both patients and physicians.

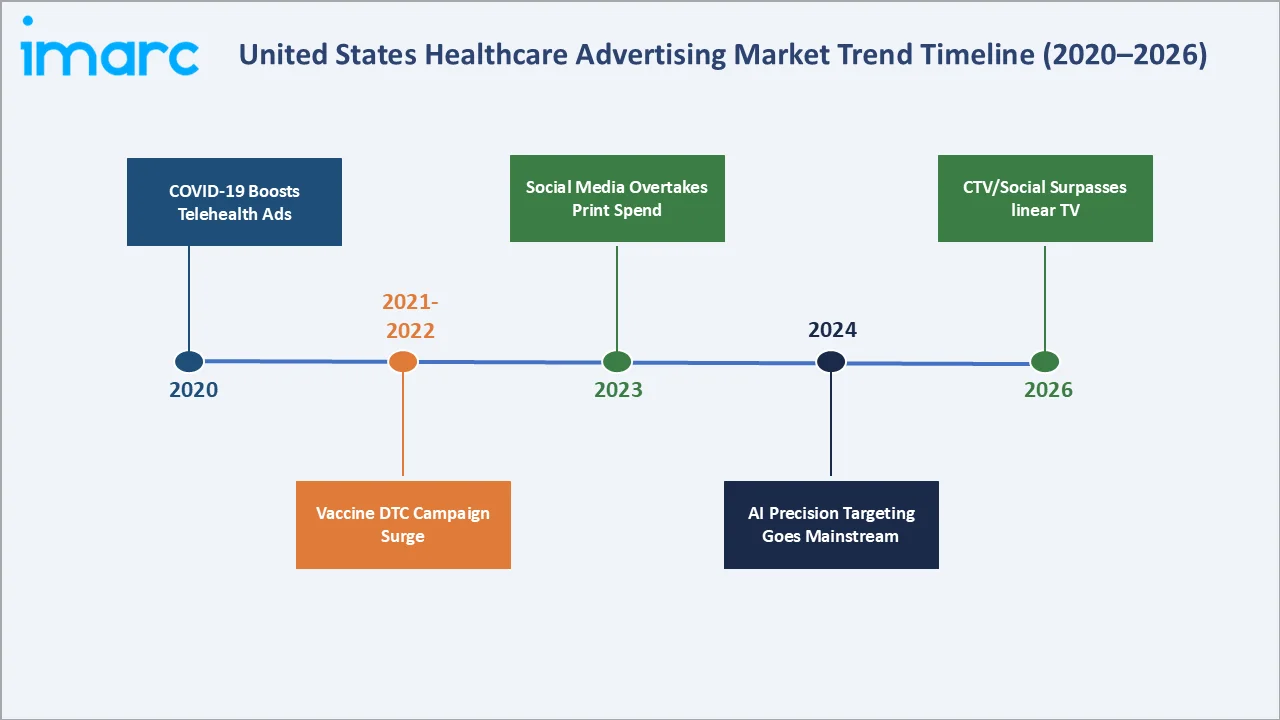

- Vaccines account for 18.6% (2025), supported by public health immunization campaigns and heightened consumer vaccination awareness following COVID-19. A 2024 study found 63% of patients discovered new medicines through pharma ads.

- Digital ad revenues are projected to see double-digit growth for the 16th consecutive year in 2025, with social media overtaking linear TV as the primary healthcare advertising channel for the first time, reflecting a structural shift in industry media allocation.

- AI and real-world data (RWD) adoption is accelerating campaign precision, enabling pharma brands to target patients by diagnosis code, treatment history, and behavioral health signals in HIPAA-compliant environments.

US Healthcare Advertising Market Overview

The US market is uniquely positioned as one of only two countries globally, alongside New Zealand, where direct-to-consumer prescription drug advertising is legally permitted. This creates an exceptionally large and commercially sophisticated advertising ecosystem spanning broadcast television, digital video, programmatic display, social media, search, connected television, and professional medical journals.

The broader ecosystem is supported by specialized healthcare advertising agencies, data and analytics providers, regulatory consultants, and media buying platforms, all operating under dual oversight of the FDA and FTC. Macroeconomic factors, including the aging US population, with adults 65 and older projected to comprise 23% of the total US population by 2050, rising insurance coverage rates, and growing chronic disease prevalence, collectively sustain high long-term advertising investment levels.

By 2034, the US healthcare advertising market is expected to benefit from the convergence of precision medicine advances, AI-driven media buying, and expanded telemedicine infrastructure. These forces will transform how pharmaceutical brands build awareness, drive patient-physician conversations, and measure campaign return on investment, with digital channels projected to account for the majority of total healthcare advertising spending by 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

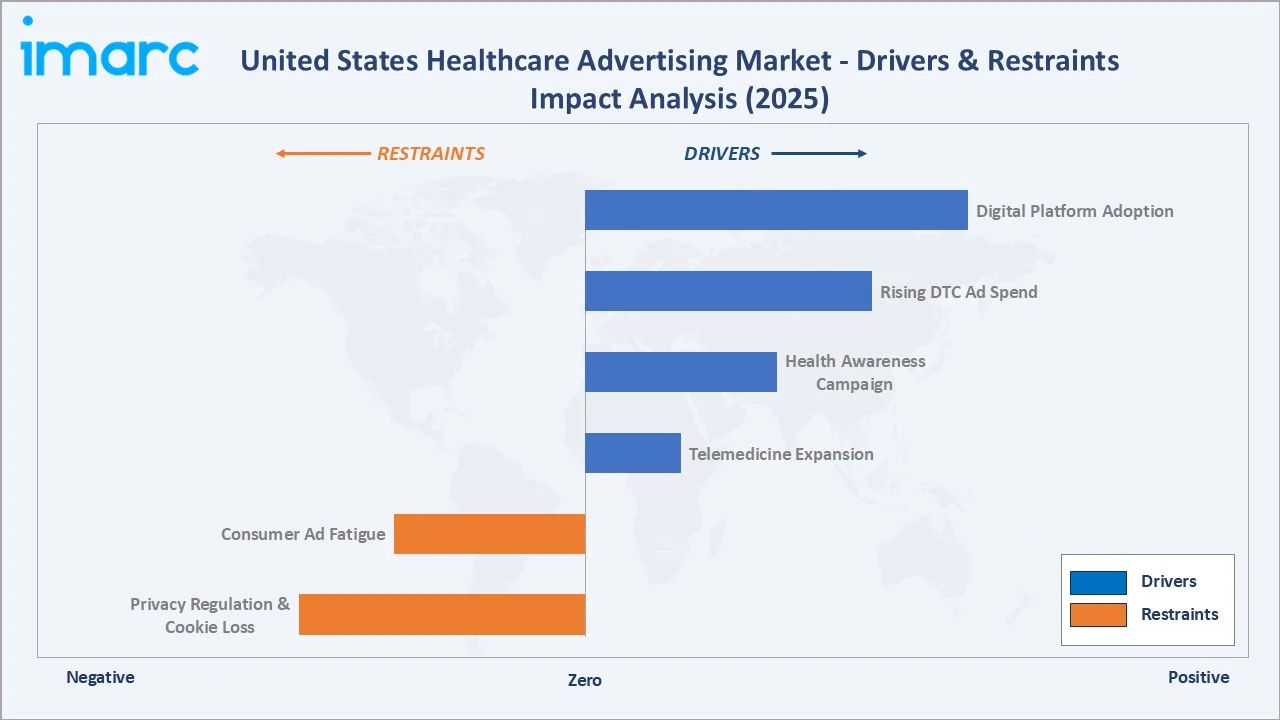

Market Drivers

- Rapid Shift to Digital and Programmatic Advertising: Healthcare and pharma digital ad spend reached USD 24.8 Billion in 2025, while traditional ad spending was USD 7.9 Billion, as brands migrate budgets from linear TV to CTV, social media, and programmatic channels for superior targeting and attribution capabilities.

- Rising Direct-to-Consumer Pharmaceutical Spend: Total US DTC prescription drug advertising surpassed USD 10.1 Billion in 2024. According to iSpot.TV data, pharma advertisers are projected to spend $5.96 billion on national TV drug ads in 2025, reflecting a sustained commitment to mass-market patient awareness campaigns for branded therapies.

- Growing Health Awareness and Chronic Disease Burden: With 3 in 4 American adults managing at least one chronic condition (2025), demand for disease awareness, treatment option education, and medication adherence campaigns is structurally elevated and growing.

- Expansion of Telemedicine and Digital Health Platforms: Telemedicine adoption reached 37% of US adults as of 2021 and continued expanding post-pandemic, creating new high-intent digital advertising surfaces for healthcare providers and pharmaceutical brands.

These drivers collectively reinforce an advertising investment cycle - digital platform growth enables better patient targeting, which improves campaign ROI, which in turn attracts greater advertising budgets from pharmaceutical and healthcare organizations throughout the forecast period.

Market Restraints

- Stringent FDA and FTC Regulatory Oversight: The FDA's Office of Prescription Drug Promotion (OPDP) increased enforcement actions in 2025, targeting misleading efficacy claims in DTC television advertisements, raising compliance costs and constraining creative messaging flexibility.

- Consumer Ad Fatigue and Trust Deficit: A 2025 SiriusXM Media survey found nearly 80% of respondents believe there are too many pharma ads on TV, with 48% characterizing drug ad visuals as misleading, constraining broadcast advertising effectiveness.

- Data Privacy Regulations and Cookie Deprecation: Evolving HIPAA interpretations, state-level consumer privacy laws, and the decline of third-party cookies are limiting digital healthcare audience targeting, requiring costly investment in first-party data infrastructure.

Market Opportunities

- AI-Powered Precision Targeting and Personalization: Machine learning algorithms enabling patient identification via symptom-search patterns, EHR-integrated advertising, and real-world data-driven audience segmentation represent a USD 8 Billion+ opportunity by 2034.

- Biopharmaceutical DTC Platform Expansion: Leading biopharma companies, including Eli Lilly, Dexcom, and Abbott, are establishing direct-to-consumer digital platforms for high-value therapies, bypassing traditional media for targeted patient engagement and direct dispensing.

- Connected TV and Audio Advertising Growth: Healthcare ad spend on CTV is projected to exceed USD 10 Billion by 2026 as streaming platforms offer pharmaceutical brands precise demographic targeting with reduced creative restrictions versus broadcast TV.

Market Challenges

- Rising Complexity of Omnichannel Campaign Coordination: Orchestrating consistent messaging across broadcast TV, CTV, programmatic display, search, social media, and EHR-integrated platforms requires significant operational investment and specialized healthcare marketing expertise.

- Potential Policy Restrictions on DTC Advertising: Proposals to limit direct-to-consumer prescription drug advertising, including mandatory cost-disclosure requirements, introduce regulatory uncertainty for established pharmaceutical campaign models.

- Measurement and Attribution Gaps: Linking digital healthcare ad exposure to prescription lift or patient initiation remains technically challenging, limiting advertiser confidence in fully committing to digital-first budget allocations.

Emerging Market Trends

1. Digital Channels Surpassing Traditional TV in Healthcare Advertising

By 2027, digital is projected to account for 82% of all healthcare and pharma ad spending, steadily increasing from its current 76% share. CTV and streaming platforms are absorbing the largest share of redirected traditional TV budgets, reflecting both audience migration and the superior targeting capabilities of digital environments.

2. AI-Driven Personalization and Real-World Data Adoption

Machine learning models identify high-intent patient cohorts via search behavior, insurance claims, and electronic health records. Physicians spend approximately 16 minutes per patient encounter in EHR systems (2024), creating a prime digital advertising surface. RWD-enabled targeting is replacing broad demographic campaigns with condition-specific, outcome-linked engagement strategies.

3. Rise of Patient-Centered and Testimonial-Driven Campaigns

A survey by IPG Mediabrands' MAGNA and DeepIntent (October 2024) found 63% of patients learned about new drugs through pharma advertisements, and 54% reported ads helped them better manage existing health conditions. Advertisers are responding by shifting from product-feature-centric messaging to authentic patient story formats, particularly across social media and digital video, where emotional resonance drives stronger physician discussion intent among target audiences.

4. Biopharmaceutical Direct-to-Consumer Platform Expansion

Pfizer launched PfizerForAll in August 2024 - a digital health management platform connecting patients to services and setting a new industry benchmark for DTC engagement. Eli Lilly expanded its LillyDirect DTC platform for GLP-1 medications in 2024, while Dexcom launched an OTC glucose biosensor DTC, collectively redefining biopharma's direct relationship with end consumers.

5. Integration of Market Access and Marketing Functions

For high-cost therapies, commercial success increasingly depends on advertising that educates patients on insurance navigation and access pathways, not just treatment awareness. Leading pharma companies are merging market access communications with consumer advertising, producing integrated campaigns that simultaneously build awareness, drive prescriptions, and guide patients.

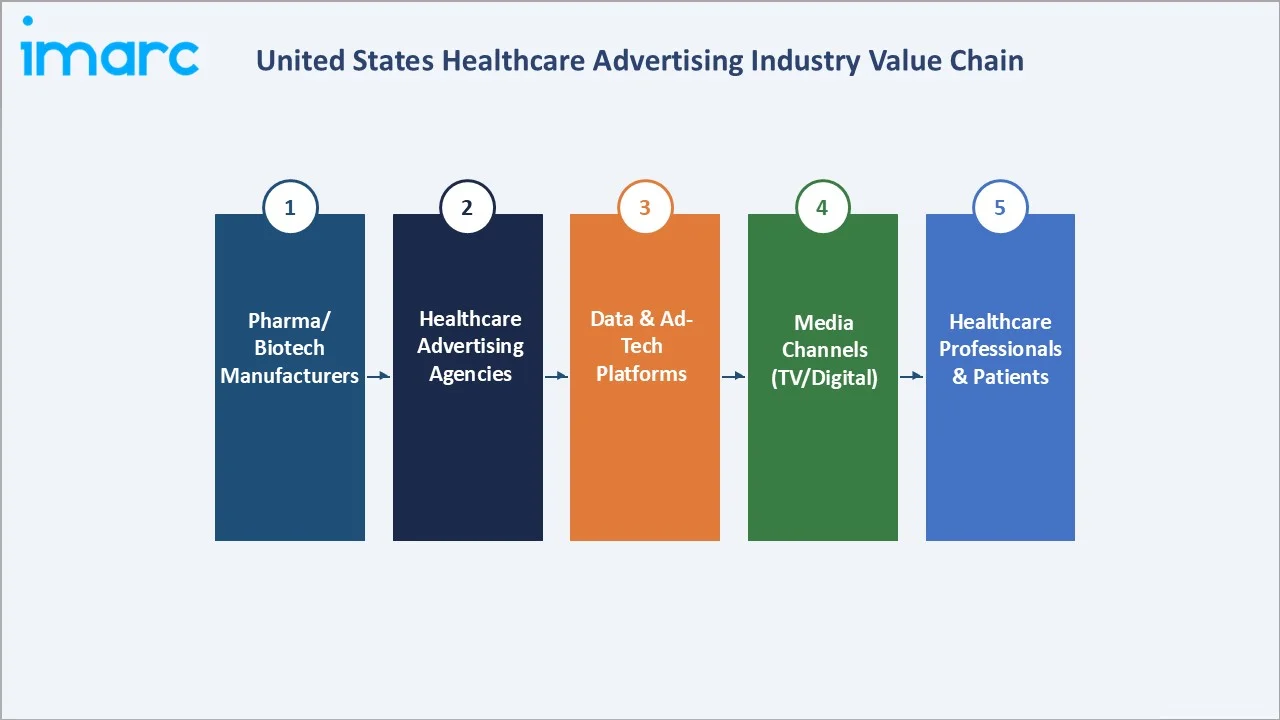

Industry Value Chain Analysis

The US healthcare advertising value chain spans from upstream pharmaceutical and device manufacturers through to downstream patient and healthcare professional audiences. Each stage involves specialized intermediaries whose collective performance shapes advertising effectiveness, regulatory compliance, and the ultimate commercial impact of healthcare communication campaigns.

|

Stage |

Key Players / Examples |

|

Drug & Device Manufacturers |

Johnson & Johnson Services, Inc., Pfizer Inc., Eli Lilly and Company, Merck & Co., Inc, AstraZeneca plc, Novartis (advertising budget owners) |

|

Healthcare Advertising Agencies |

TBWA\Health, McCann Health, Inizio Evoke, Ogilvy Health, FCB Health, CDM New York |

|

Data & Analytics Providers |

IQVIA, Komodo Health, PurpleLab, Veradigm, DeepIntent (RWD & audience targeting) |

|

Media Buying & Ad Tech Platforms |

Google, Meta, The Trade Desk, Doceree, PatientPoint (programmatic & EHR-integrated) |

|

Regulatory Review |

FDA OPDP, FTC, MLR review teams, medical-legal-regulatory consultants, and compliance specialists |

|

Distribution Channels |

TV networks, CTV (Hulu, Peacock, Amazon), social media (Meta, TikTok), search (Google), audio (Spotify) |

|

End Audiences |

US patients, caregivers, physicians, pharmacists, nurses, health insurance payers, and wellness consumers |

Technology Landscape in the Healthcare Advertising Industry

AI-Driven Healthcare Marketing Cloud for Precision Targeting

In March 2026, DeepIntent introduced Helix, a new purpose‑built healthcare marketing cloud designed to help brands and agencies plan, activate, and optimize campaigns with precision using healthcare‑specific data and analytics. The platform is available to marketers aiming to improve audience targeting and performance outcomes in regulated healthcare advertising.

Real-World Data and Precision Audience Segmentation

IQVIA’s Orchestrated Customer Engagement (OCE) solution was adopted by more than 30 life sciences companies, including top‑20 global pharmaceutical firms like Novo Nordisk and Roche, to harmonize customer interaction workflows and transform commercial engagement models across sales, marketing, and digital touchpoints.

Connected TV and Streaming Health Advertising

CTV platforms now offer pharmaceutical-grade audience targeting combined with broadcast-quality creative, enabling brands to reach specific patient demographics without broad demographic waste. WARC Media’s Global Ad Trends report projects CTV's share of pharma digital spend to exceed 40% by 2030, as streaming platforms including Hulu, Peacock, and Amazon develop HIPAA-compliant data partnerships with pharmaceutical advertisers.

Digital Patient Engagement Platforms

Pharmaceutical companies are investing in proprietary digital health platforms that serve as always-on advertising and patient support ecosystems. Pfizer's PfizerForAll (launched August 2024) exemplifies this trend - combining medication management, health content, and third-party service connections into a branded patient experience that transcends conventional advertising.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Pharmaceuticals (Small Molecule Drugs) |

46.3% |

2025 |

By Product Type

Pharmaceuticals (Small Molecule Drugs) dominate the US healthcare advertising market with a 46.3% share in 2025, owing to the US’s unmatched DTC advertising framework for branded prescription medications. Biopharmaceuticals follow at 22.7%, Vaccines at 18.6%, and OTC Drugs at 12.4%, reflecting the varying advertising intensity, regulatory frameworks, and patient engagement strategies.

To access detailed market analysis, Request Sample

Biopharmaceuticals represent the fastest-growing product category (2025), driven by the surge in high-value biologics launches, including monoclonal antibodies, GLP-1 receptor agonists, and immunotherapies, each requiring substantial market education investment. The vaccines reflect the amplified public health communication infrastructure built during COVID-19, repurposed for ongoing immunization campaigns for RSV, influenza, and HPV vaccines.

Competitive Landscape

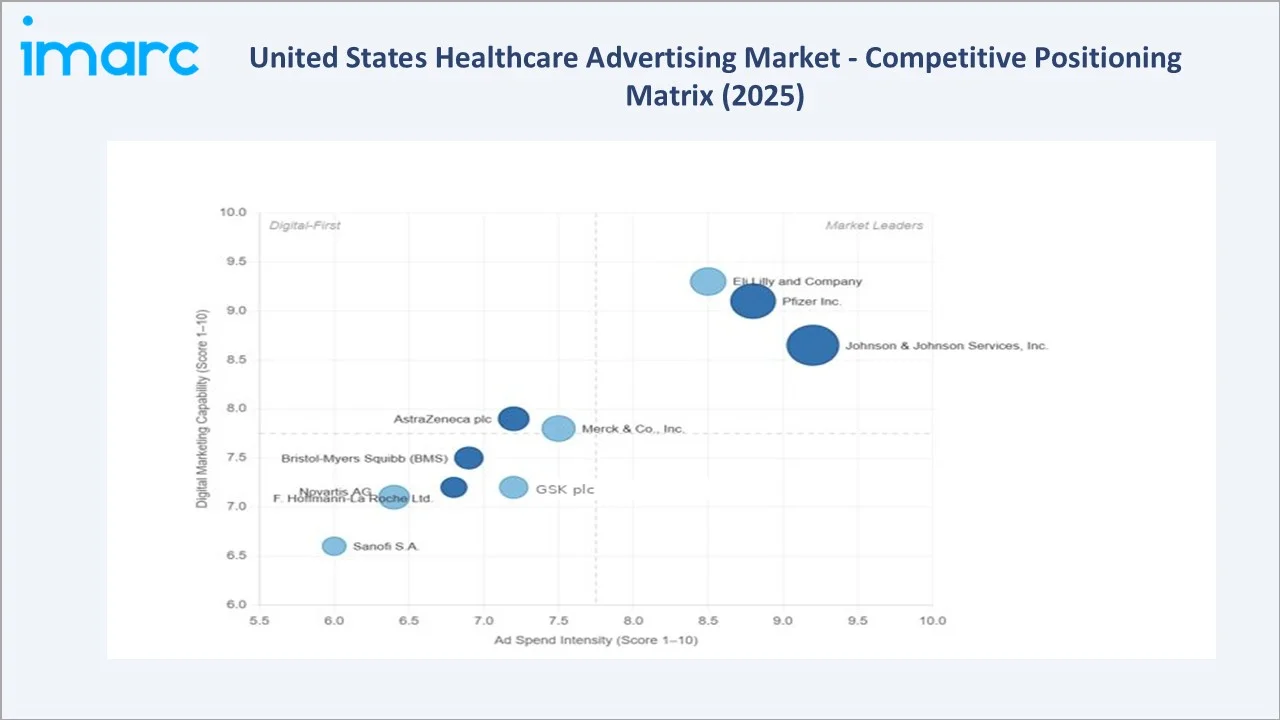

The US healthcare advertising market is dominated by major pharmaceutical and biopharmaceutical corporations that collectively invest tens of billions of dollars annually in patient and physician-directed campaigns. The top five advertisers, Johnson & Johnson Services, Inc., Pfizer Inc., Eli Lilly and Company, Merck & Co., Inc, and AstraZeneca plc, account for an estimated 55-60% of total industry advertising spend (2025).

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Johnson & Johnson Services Inc. |

Janssen |

Market Leader |

Broadest pharma & consumer healthcare advertising portfolio |

|

Pfizer Inc. |

Comirnaty/Paxlovid/Abrysvo |

Market Leader |

PfizerForAll™ DTC platform; dominant vaccine & Rx ad spend |

|

Merck & Co. Inc. |

Keytruda/Gardasil 9/Januvia |

Strong Challenger |

Oncology and vaccine advertising; high DTC investment |

|

GSK plc |

Shingrix/Trelegy/Advair |

Strong Challenger |

Respiratory and vaccine multichannel advertising leader |

|

Eli Lilly and Company |

Mounjaro/Zepbound/Trulicity |

Fast Riser |

GLP-1 DTC surge; LillyDirect consumer health platform |

|

Novartis AG |

Cosentyx/Kisqali/Kymriah |

Challenger |

AI-precision specialty drug and social media campaigns |

|

Sanofi S.A. |

Dupixent/Lantus/Beyfortus |

Challenger |

Immunology and rare disease DTC advertising growth |

|

AstraZeneca plc |

Tagrisso/Farxiga/Breztri |

Challenger |

Oncology advertising; strong HCP digital engagement |

|

F. Hoffmann-La Roche Ltd. |

Tecentriq/Hemlibra/Ocrevus |

Specialist |

Personalized medicine and diagnostics-linked advertising |

|

Bristol-Myers Squibb (BMS) |

Opdivo/Eliquis/Revlimid |

Challenger |

Oncology & cardiology patient-centric DTC messaging |

The competitive landscape is shifting from share-of-voice competition on traditional TV toward first-party data quality, omnichannel integration depth, and AI-powered optimization as the primary battleground.

Key Company Profiles

Johnson & Johnson Services Inc.

Johnson & Johnson is one of the largest healthcare companies by revenue in the US, with a comprehensive advertising portfolio spanning Janssen Pharmaceuticals, consumer health, and medical devices. Annual US pharmaceutical advertising investment exceeds USD 2 Billion (2024).

- Product Portfolio: Oncology, immunology, and neuroscience Rx drugs (Janssen); consumer OTC health and beauty products; surgical robotics and medical device solutions.

- Recent Developments: Launched integrated patient support and digital engagement campaigns for Carvykti (CAR-T therapy) in 2025, expanded AI-driven HCP targeting across oncology specialty segments.

- Strategic Focus: Omnichannel patient engagement, first-party data platform development, and DTC expansion for high-value specialty biologics and rare disease therapies.

Pfizer Inc.

Pfizer ranks among the top US pharmaceutical advertisers, with advertising spend exceeding USD 1.8 Billion annually (2024). The company launched PfizerForAll™ in August 2024, establishing a new benchmark for pharmaceutical DTC digital engagement and direct patient access.

- Product Portfolio: COVID-19 antivirals and vaccines, oncology, rare disease, women's health, and consumer health divisions spanning over 350 branded products.

- Recent Developments: PfizerForAll™ digital platform launched August 2024, connecting patients to health services; major DTC investment in RSV vaccine (Abrysvo) awareness campaigns nationally.

- Strategic Focus: Digital patient platform ecosystem, vaccine market maintenance, and precision oncology advertising through AI-powered patient segmentation and CTV channel expansion.

Eli Lilly and Company

Eli Lilly has emerged as one of the fastest-growing pharmaceutical advertisers in the US, driven by the enormous commercial opportunity in GLP-1 receptor agonists for diabetes and obesity, among the most heavily advertised drug classes of 2024-2025.

- Product Portfolio: Mounjaro (tirzepatide), Zepbound, Trulicity, Verzenio (oncology), Jardiance (diabetes/cardiovascular), and Emgality (migraine).

- Recent Developments: LillyDirect DTC platform expanded in 2024 for direct GLP-1 prescription and delivery; extensive CTV and digital video campaigns targeting obesity and diabetes patient populations.

- Strategic Focus: DTC platform direct-to-patient sales, integrated digital health advertising, and market education campaigns for GLP-1 therapy insurance access and patient adherence improvement.

Merck & Co. Inc.

Merck is a leading US healthcare advertiser, particularly in oncology (Keytruda immunotherapy) and vaccines (Gardasil HPV vaccine), with combined DTC advertising investment among the highest in the pharmaceutical industry.

- Product Portfolio: Keytruda (pembrolizumab, oncology), Gardasil 9 (HPV vaccine), Januvia (diabetes), Lagevrio (COVID-19 antiviral), Pneumovax 23 (pneumococcal disease).

- Recent Developments: Expanded Keytruda DTC patient awareness campaigns in 2024 across 40+ approved cancer indications; launched digital-first Gardasil HPV vaccination campaign targeting adolescent parents.

- Strategic Focus: Oncology patient empowerment advertising, vaccine-preventable disease awareness, and HCP digital engagement for complex therapy education at point-of-prescribing.

Market Concentration Analysis

The US healthcare advertising market exhibits a moderately concentrated structure at the top end. The ten largest pharmaceutical advertisers, led by Johnson & Johnson Services, Inc., Pfizer Inc., Eli Lilly and Company, Merck & Co., Inc, and AstraZeneca plc, collectively account for an estimated 55-60% of total industry advertising spend (2025).

Concentration is highest in the DTC television segment, where production costs and network CPMs favor large pharmaceutical companies with established brand portfolios. M&A activity among healthcare advertising agencies is reshaping the concentration of service providers. Newsweek's acquisition of Adprime (June 2025) and Inizio Evoke's launch of Flex Marketing (February 2025) signal growing specialization in the US healthcare advertising services market.

Consolidation at the pharma advertiser level is also accelerating, as large companies acquire DTC-experienced biotech brands to expand their consumer advertising capabilities. The market is expected to see continued growth in specialized health-focused independent agencies gaining market share versus generalist holding company networks, driven by the technical complexity of HIPAA-compliant digital healthcare advertising through 2034.

Investment & Growth Opportunities

Fastest Growing Segments

Biopharmaceutical advertising spending is growing at an estimated 7-9% annually, driven by GLP-1 obesity therapies, immunotherapies, and gene therapy launches that each require extensive patient and physician education campaigns. AI-powered healthcare advertising technology platforms are attracting venture capital investment exceeding USD 1.5 billion annually as of 2025, as pharma brands increasingly demand measurable, outcomes-linked advertising ROI.

Emerging Advertising Technology Investment

Key investment themes include EHR-integrated physician advertising networks, real-world data-powered patient audience platforms, AI-generated personalized health content systems, and HIPAA-compliant CTV targeting infrastructure. Companies including DeepIntent, Doceree, PatientPoint, and IQVIA's marketing technology division are attracting significant private equity and strategic investment as pharma brands seek measurable, physician-level campaign attribution.

Direct-to-Consumer Platform Development

The emergence of pharmaceutical company-owned direct-to-consumer digital platforms represents a structural advertising investment opportunity beyond traditional paid media. These owned platforms replace media-bought impressions with proprietary patient relationships, delivering superior engagement metrics, first-party data accumulation, and long-term customer lifetime value.

- AI-powered personalization tools for patient engagement: projected investment pool of USD 3-4 billion by 2030.

- HIPAA-compliant first-party data infrastructure: critical for post-cookie digital health advertising targeting across pharma brands.

- CTV health advertising inventory partnerships: Hulu, Peacock, and Amazon Prime Video are actively developing pharmaceutical-grade healthcare advertising category programs.

Future Market Outlook (2026-2034)

The US healthcare advertising market is positioned for steady, structurally supported growth through 2034, anchored by irreversible demographic trends, continuous pharmaceutical innovation, and accelerating digital media transformation. From a base of USD 25.3 Billion in 2025 to USD 26.2 Billion in 2026, the market is forecast to reach USD 35.3 Billion by 2034 at a CAGR of 3.60%, representing approximately USD 10 Billion in incremental advertising investment over the forecast period.

Technological disruptions, including generative AI-produced personalized health content, conversational AI patient engagement tools, and blockchain-enabled transparent drug pricing communications, are expected to materially reshape how pharmaceutical brands communicate with patients and physicians through 2034.

The Biopharmaceuticals and AI-enhanced digital advertising segments are projected to outpace the overall market growth rate, while traditional broadcast TV healthcare advertising spending is expected to continue declining as a share of total investment. Potential legislative changes may selectively constrain traditional TV spending while accelerating the migration to digital-first healthcare advertising models through the forecast period.

Research Methodology

Primary Research

Primary research for this report included in-depth structured interviews and executive surveys conducted with over 150 industry stakeholders during 2024-2025, comprising pharmaceutical marketing executives, healthcare advertising agency leaders, digital health platform operators, and regulatory affairs specialists across the United States.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, SEC filings, FDA OPDP enforcement records, eMarketer digital advertising databases, IQVIA pharmaceutical spending reports, trade publications (Fierce Pharma Marketing, MM+M), and publicly available advertising expenditure datasets.

Forecasting Models

Market size estimations and growth projections were developed using a combination of bottom-up channel-level spend modeling and top-down macro pharmaceutical revenue trend analysis. Scenario analysis incorporating base, optimistic (regulatory tailwind), and conservative (DTC restriction) cases was performed to bound the 3.60% CAGR central estimate through 2034.

US Healthcare Advertising Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Pharmaceuticals (Small Molecule Drugs), Biopharmaceuticals, Vaccines and Over-The-Counter Drugs |

| Companies Covered | Johnson & Johnson Services Inc., Pfizer Inc., Merck & Co. Inc., GSK plc, Eli Lilly and Company, Novartis AG, Sanofi S.A., AstraZeneca plc, F. Hoffmann-La Roche Ltd., Bristol-Myers Squibb (BMS), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the US healthcare advertising market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the US healthcare advertising market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the US healthcare advertising industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the US Healthcare Advertising Market Report

The US healthcare advertising market size is estimated to USD 26.2 Billion in 2026 and is projected to reach USD 35.3 Billion by 2034, growing at a CAGR of 3.6% during 2026-2034.

The market is expected to grow at a CAGR of 3.60% during the forecast period 2026-2034, supported by rising digital advertising investment and sustained pharmaceutical DTC campaign spend.

Pharmaceuticals (small molecule drugs) lead with a 46.3% market share in 2025, driven by extensive branded prescription DTC campaigns across digital, broadcast, and programmatic channels.

Growth is driven by GLP-1 obesity drug launches, oncology immunotherapy campaigns, and biopharma DTC platform expansion. The segment is growing faster than the overall market average.

AI enables precision patient targeting via real-world data, EHR-integrated physician advertising, programmatic audience segmentation, and personalized health content generation at a measurable campaign scale.

The Northeast accounts for approximately 32.5% of US healthcare advertising spend in 2025, driven by pharmaceutical HQ concentration in New Jersey and New York's media agency ecosystem.

Key players include Johnson & Johnson Services Inc., Pfizer Inc., Merck & Co. Inc., GSK plc, Eli Lilly and Company, Novartis AG, Sanofi S.A., AstraZeneca plc, F. Hoffmann-La Roche Ltd., and Bristol-Myers Squibb (BMS).

DTC advertising involves pharmaceutical companies promoting prescription drugs directly to consumers via TV, digital, and social media. It is legally permitted in the US and New Zealand only.

Telemedicine creates new high-intent digital advertising surfaces. With 37% of US adults using telehealth as of 2021 and adoption continuing to grow, the channel is rapidly expanding as an advertising destination.

The FDA's Office of Prescription Drug Promotion (OPDP) regulates prescription drug advertising, while the Federal Trade Commission (FTC) oversees OTC drug and general consumer health advertising.

Key opportunities include AI-powered programmatic health platforms, proprietary biopharma DTC digital platforms, CTV health advertising inventory, and HIPAA-compliant first-party data infrastructure.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade