US Pet Food Market Size, Share, Trends and Forecast by Pet Type, Product Type, Pricing Type, Ingredient Type, and Distribution Channel, 2026-2034

US Pet Food Market Size, Share, Trends & Forecast (2026-2034)

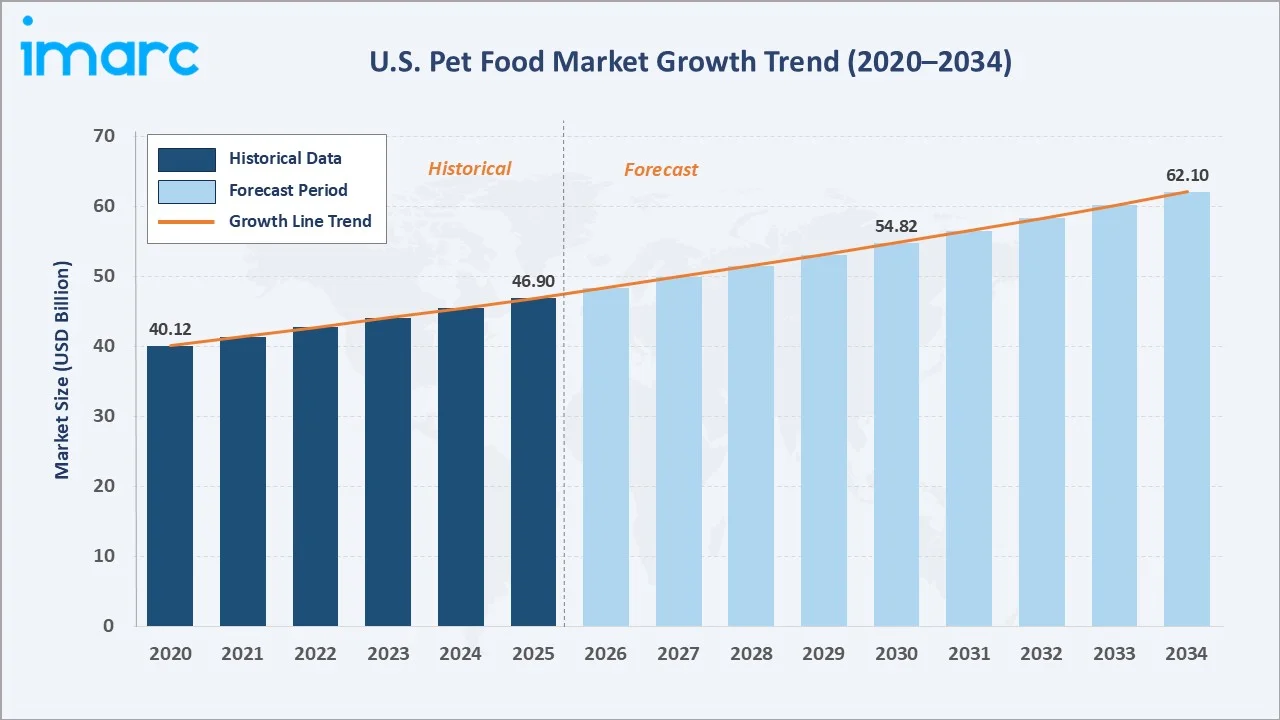

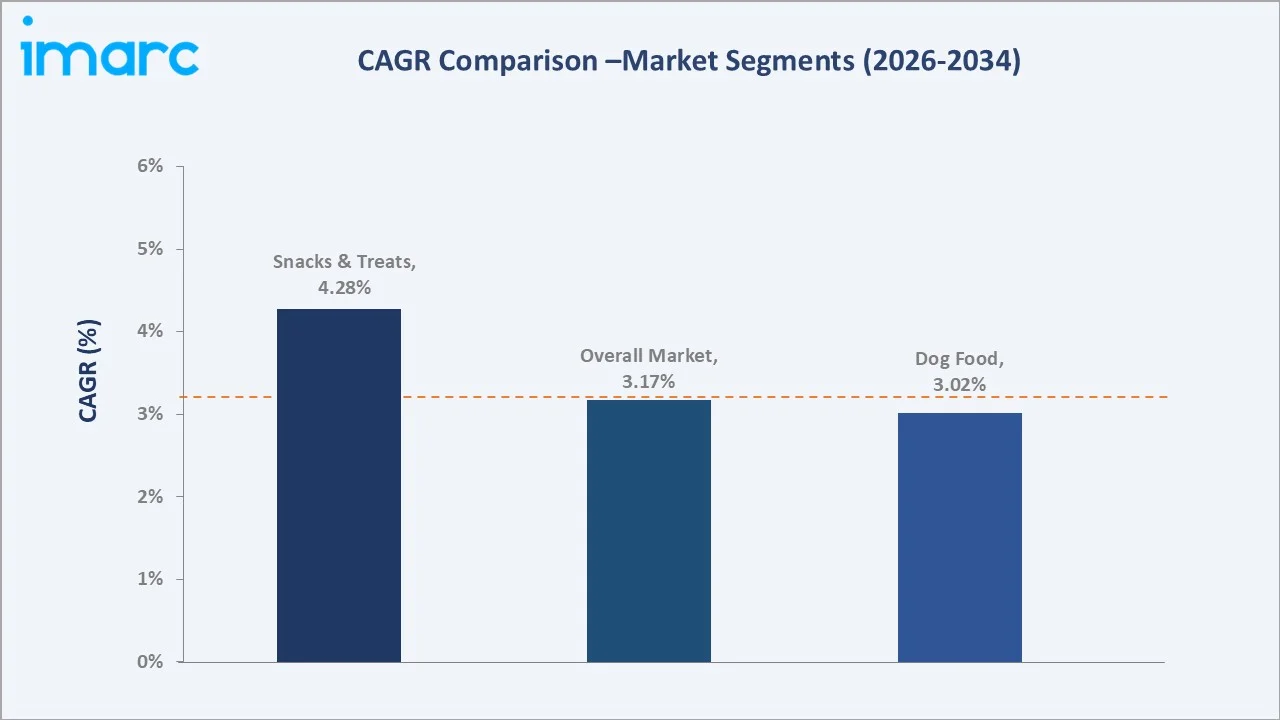

The US pet food market reached USD 46.90 Billion in 2025 and is projected to reach USD 62.10 Billion by 2034, growing at a CAGR of 3.17% during 2026-2034. Rapid growth in pet ownership, the humanization of pets, and rising demand for premium, functional, and grain-free formulations are key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 46.90 Billion |

|

Forecast Market Size (2034) |

USD 62.10 Billion |

|

CAGR (2026-2034) |

3.17% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South |

|

Fastest Growing Region |

West Coast |

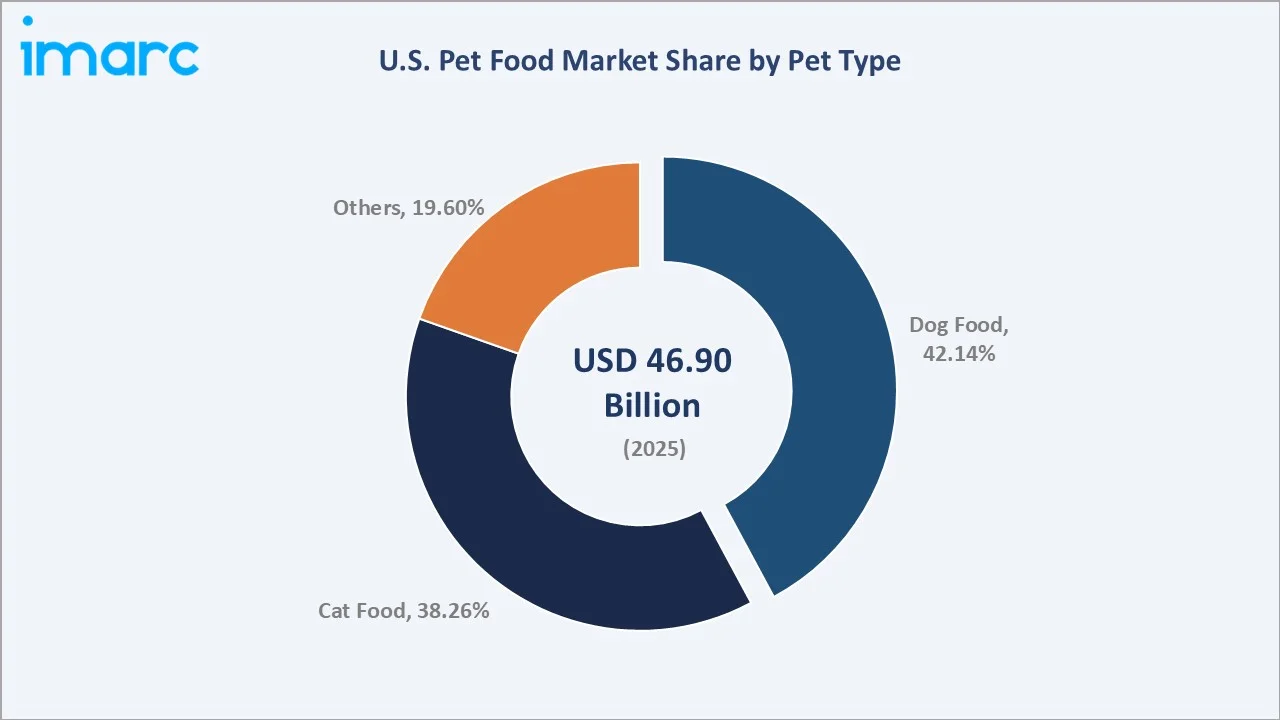

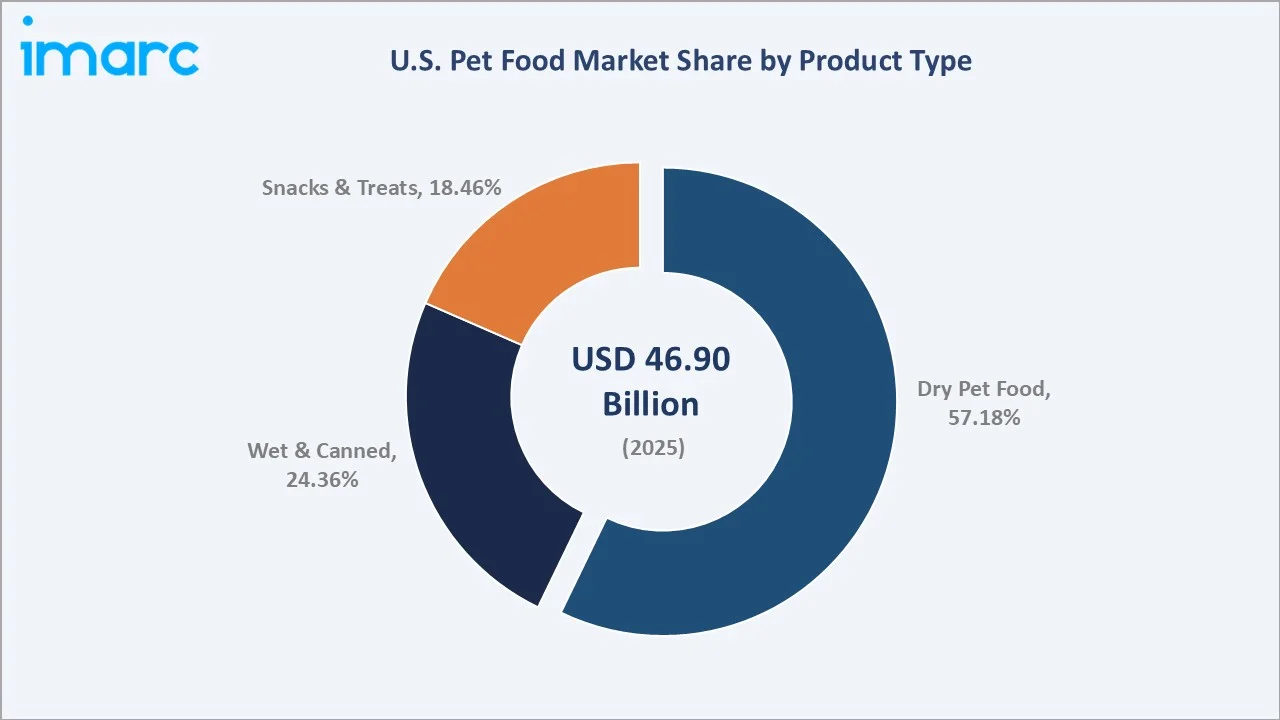

Dog food leads by pet type with a 42.14% market share, while dry pet food dominates product formats at 57.18%, supported by strong retail shelf presence and consumer familiarity. Dog food and dry pet food collectively account for the dominant share across segments, underscoring the breadth of the US pet food market growth opportunity.

To get more information on this market, Request Sample

The US pet food market forecast reflects a stable and sustained growth trajectory. Innovations in ingredients, including insect-based proteins, human-grade formulations, and nutraceutical-enriched recipes, are reshaping consumer preferences and creating new revenue pockets across mainstream and specialty channels.

Executive Summary

The US pet food market is on a sustained growth path, underpinned by rising pet ownership, premiumization, and a fundamental shift in how Americans perceive animal companions. The market reached USD 46.90 Billion in 2025 and is forecast to surpass USD 62.10 Billion by 2034, driven by a CAGR of 3.17%. This trajectory reflects robust consumer spending on pet wellness, nutrition, and specialized dietary solutions across all demographic segments.

The South leads domestically in 2025, supported by high pet ownership density and expanding specialty retail footprints across Texas, Florida, and Georgia. Dog food commands a 42.14% share of the market by pet type, while dry pet food leads product formats at 57.18%, driven by its convenience, long shelf life, and broad price accessibility.

Leading players, including Nestlé, Mars, Incorporated, Colgate-Palmolive Company, SCHELL & KAMPETER, INC., and General Mills Inc., continue to invest in clean-label formulations, sustainable packaging, and direct-to-consumer digital channels to align with evolving pet owner expectations. The US pet food market outlook remains highly attractive, presenting strong investment opportunities across premium and functional nutrition segments.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Pet Type) |

Dog Food – 42.14% share (2025) |

|

Largest Segment (Product Type) |

Dry Pet Food – 57.18% share (2025) |

|

Fastest Growing Region |

West Coast (premiumization + e-commerce) |

|

Top Companies |

Nestlé, Mars, Incorporated, Colgate-Palmolive Company, SCHELL & KAMPETER, INC., and General Mills Inc. |

Key Analytical Observations Supporting the Above Data:

- Dog food accounts for 42.14% of the US pet food market in 2025, driven by the highest pet ownership share. According to APPA’s annual survey, the share of U.S. households owning dogs rose from 51% in 2024 to 53% in 2025, reaching a total of 71 million households.

- Dry pet food leads product formats at 57.18% (2025), with dominance rooted in consumer convenience, cost-effectiveness, and wide retail availability. Prescription and veterinarian-recommended dry formulations are also expanding market penetration within this segment.

- The West Coast is the fastest-growing regional segment, fueled by higher-income demographics, a well-established organic and natural food culture, and accelerating adoption of subscription-based pet food delivery models among urban millennials.

- Functional pet nutrition, including joint health, gut microbiome, dental, and cognitive support formulations, represents the market's highest-growth innovation vector, with an estimated USD 8.5 Billion total addressable segment value projected by 2034.

US Pet Food Market Overview

Pet food encompasses all nutritionally formulated food products designed for domestic animals, including dogs, cats, birds, fish, small mammals, and reptiles. The industry spans a complex ecosystem from raw commodity ingredients, including meat meals, grains, vitamins, and mineral premixes, through manufacturing, packaging, distribution, and retail or direct-to-consumer delivery.

Macroeconomic factors, including rising disposable income, growth in single-person households with companion animals, and the cultural phenomenon of "pet parenting", serve as primary growth catalysts. Pet food in the US has progressively evolved from basic commodity nutrition to a sophisticated functional food sector, paralleling trends observed in human health and wellness markets.

Market Dynamics

To evaluate market opportunities, Request Sample

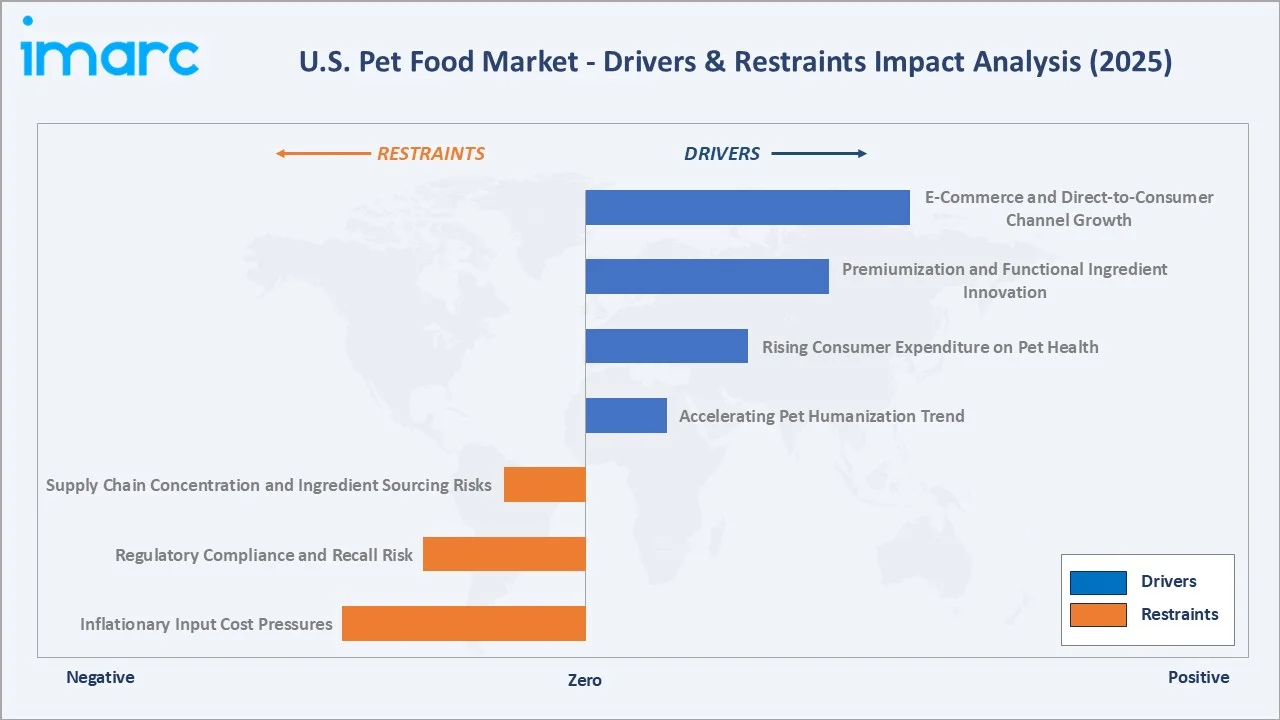

Market Drivers

- Accelerating Pet Humanization Trend: The 2025 National Pet Owners Survey, referenced in APPA’s 2026 State of the Industry Report, indicates that 95 million U.S. households own a pet. An increasing proportion of these owners regard pets as family members, directly driving demand for human-grade ingredients, specialized dietary formulations, and veterinary-developed nutrition plans that command significantly higher price points.

- Rising Consumer Expenditure on Pet Health: US pet industry spending totaled USD 152 billion in 2024, with pet food representing the single largest category. As preventive pet healthcare gains mainstream traction, demand for nutraceutical-enriched, breed-specific, and life-stage-optimized pet food formulations is expanding consistently across income segments.

- Premiumization and Functional Ingredient Innovation: Consumer migration from value-tier to premium and super-premium pet food products is a structural tailwind. Ingredients such as real meat proteins, probiotics, omega-3 fatty acids, and botanical adaptogens are being integrated to support gut health, coat quality, joint mobility, and cognitive function.

- E-Commerce and Direct-to-Consumer Channel Growth: Online pet food sales in the US have grown dramatically, with Chewy reporting net sales of approximately USD 12.60 billion in fiscal year 2025. Subscription auto-ship models provide predictable revenue streams for brands while offering consumers the convenience of doorstep delivery and personalized product recommendations.

Market Restraints

- Inflationary Input Cost Pressures: Protein commodity inflation, freight cost volatility, and elevated packaging material costs have compressed manufacturer margins. Between 2021 and 2023, several leading pet food producers implemented multiple rounds of price increases, risking volume attrition among price-sensitive consumer segments.

- Regulatory Compliance and Recall Risk: The US FDA and AAFCO impose stringent nutritional standards and ingredient labeling requirements. Product recalls, driven by contamination events or formulation non-compliance, can permanently damage brand equity and erode consumer trust in affected product lines.

- Supply Chain Concentration and Ingredient Sourcing Risks: Geographic concentration of key ingredient suppliers, particularly for novel proteins, specialty grains, and functional additives, exposes manufacturers to single-source disruption risk, as evidenced during the COVID-19 pandemic supply chain disruptions of 2020–2021.

Market Opportunities

- Personalized and Precision Pet Nutrition: AI-powered platforms are enabling customized pet food formulations based on breed, age, health history, and activity levels. Subscription-based fresh meal plan brands demonstrate superior customer lifetime value and retention metrics versus conventional retail channels.

- Alternative Proteins and Sustainability Innovation: Insect-based proteins, cultivated meat ingredients, and plant-derived protein alternatives represent a nascent but fast-growing opportunity. The sustainable pet food segment is estimated to achieve a CAGR exceeding 8% through 2034, as environmentally conscious millennial and Gen Z pet owners prioritize eco-aligned purchasing decisions.

Market Challenges

- Consumer Trust and Transparency Demands: Increasing scrutiny of pet food ingredient sourcing, manufacturing practices, and nutritional claims requires brands to invest heavily in traceability systems and transparent communication strategies. A single product recall can have outsized reputational consequences in a category where brand trust is a primary purchase driver.

- Shelf Space Competition and Retailer Power Dynamics: In April 2026, Dr. Pol launched a veterinarian-formulated clinical nutrition dog food line exclusively through Walmart, making the products available nationwide in stores and on Walmart.com. Such exclusive partnerships highlight how large retailers control product visibility, pricing, and distribution, often prioritizing select brands while limiting access for smaller or emerging players.

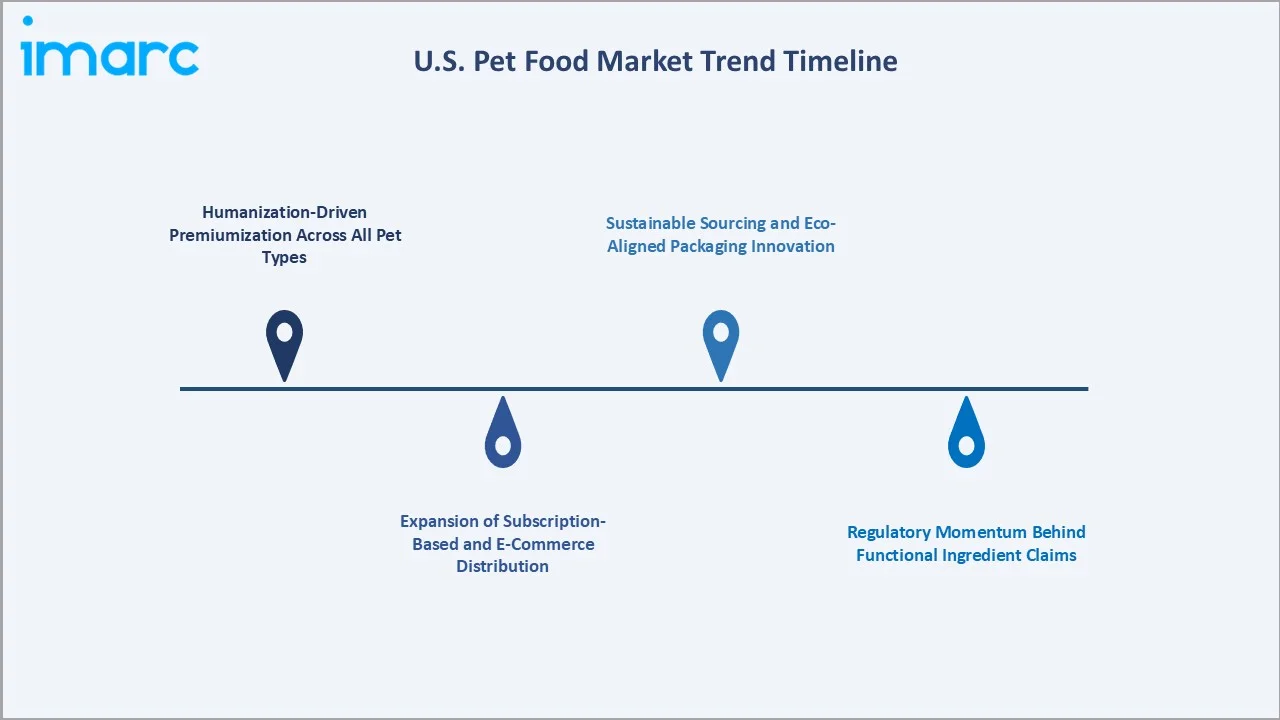

Emerging Market Trends

1. Humanization-Driven Premiumization Across All Pet Types

According to the APPA, pet food industry expenditures in the US grew to USD 65.8 billion in 2024, up 2.8% from 2023, reflecting consistent wallet-share expansion even amid broader consumer inflation. Super-premium and holistic pet food brands have achieved double-digit revenue growth through 2023–2025, as mainstream consumers trade up in pursuit of perceived health benefits for their companion animals.

2. Expansion of Subscription-Based and E-Commerce Pet Food Distribution

Chewy's auto-ship subscription platform accounted for 83.3% of fiscal 2025 net sales. A January 2025 survey by Packaged Facts found that 39% of pet product shoppers use the internet for at least one type of pet product subscription, with pet food being the most common at 20%. This structural channel shift enables brands to capture first-party consumer data, enabling more targeted marketing and personalization.

3. Regulatory Momentum Behind Functional Ingredient Claims

Brands are now investing in clinical nutrition research partnerships with veterinary schools to substantiate structure-function claims for ingredients such as prebiotics, omega fatty acid complexes, and joint-support nutraceuticals. The US pet food market trends indicate that clinically validated functional nutrition is becoming a critical differentiator; the prescription pet food segment commands a 35–50% price premium and is growing at an estimated CAGR of 5.8% through 2034.

4. Sustainable Sourcing and Eco-Aligned Packaging Innovation

A survey of 945 pet owners across Canada, France, the U.K., and the U.S., conducted by Yummypets and Pets International magazine, highlighted growing interest in sustainable pet food packaging. About 55% of respondents said they actively seek sustainable packaging, while 46% reported purchasing pet food in sustainable or recyclable packaging.

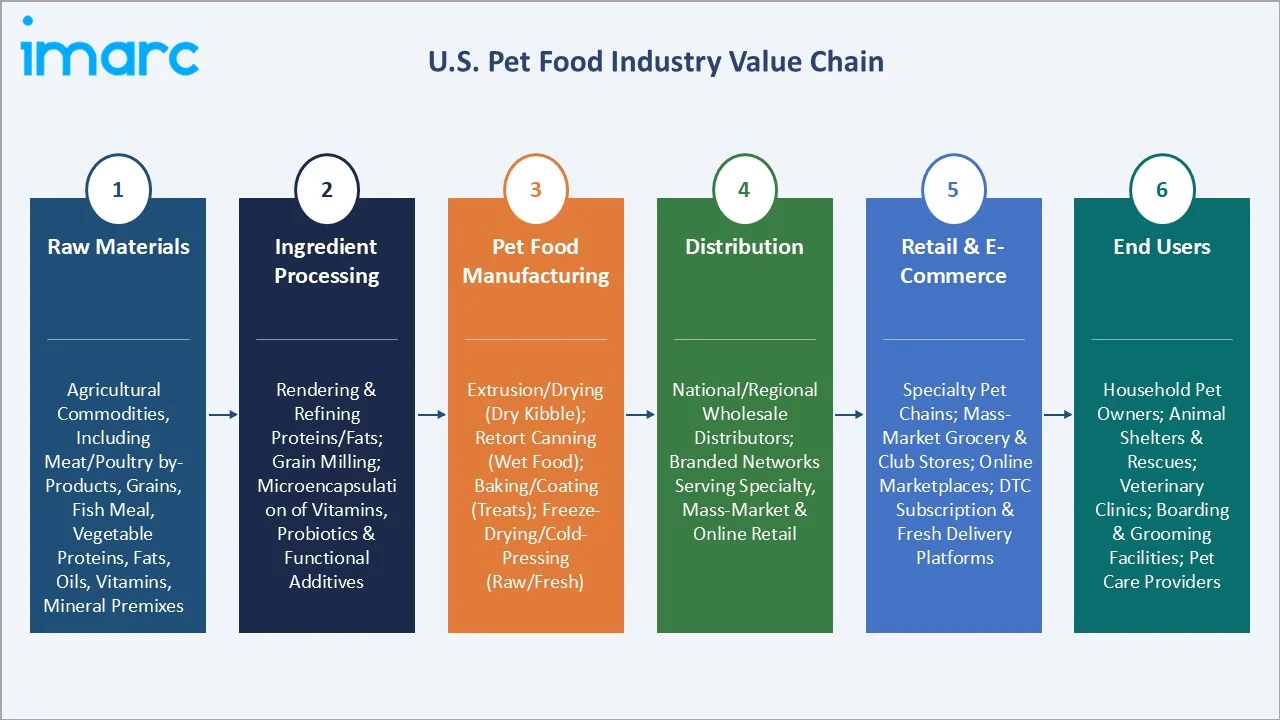

Industry Value Chain Analysis

The US pet food value chain extends from agricultural commodity sourcing through sophisticated manufacturing, multi-channel distribution, and final delivery to pet-owning households. Each stage is populated by specialized operators whose operational efficiency and quality standards directly influence product safety, nutritional integrity, and shelf-competitive pricing.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Agricultural commodities, including meat/poultry by-products, grains, fish meal, vegetable proteins, fats, oils, vitamins, mineral premixes |

|

Ingredient Processing |

Rendering & refining proteins/fats; grain milling; microencapsulation of vitamins, probiotics & functional additives |

|

Pet Food Manufacturing |

Extrusion/drying (dry kibble); retort canning (wet food); baking/coating (treats); freeze-drying/cold-pressing (raw/fresh) |

|

Distribution |

National/regional wholesale distributors; branded networks serving specialty, mass-market & online retail |

|

Retail & E-Commerce |

Specialty pet chains; mass-market grocery & club stores; online marketplaces; DTC subscription & fresh delivery platforms |

|

End Users |

Household pet owners; animal shelters & rescues; veterinary clinics; boarding & grooming facilities; pet care providers |

Technology Landscape in the US Pet Food Industry

AI-Driven Personalized Nutrition Platforms

In October 2024, Ollie acquired AI-powered diagnostic company DIG Labs to integrate real-time, image-based pet health screenings covering digestion, weight, skin, dental, and overall wellness, while bringing co-founder Tara Zedayko on board as Chief Scientific Officer to lead innovation. The company also launched Foodback Loop, a proprietary data-driven system aimed at improving product development and optimizing feeding algorithms for better canine health.

Advanced Extrusion and High-Pressure Processing Technology

Modern co-extrusion and twin-screw extrusion technologies allow manufacturers to precisely control kibble density, texture, and nutrient retention across diverse formulation matrices. High-Pressure Processing (HPP) has been adopted by fresh and raw pet food manufacturers as a non-thermal pasteurization alternative, preserving bioactive nutrients and enzymes while meeting US FDA food safety standards.

Blockchain-Based Ingredient Traceability

Leading manufacturers are implementing distributed ledger technology to provide verifiable, end-to-end supply chain transparency. In a market where a single contamination event can trigger nationwide recalls and lasting brand damage, real-time traceability from farm or fishery to finished product is becoming a critical risk management and marketing investment.

Alternative Protein Processing Innovation

Insect protein fractionation, single-cell protein fermentation, and precision fermentation technologies are enabling the production of novel, sustainable protein concentrates. These processing technologies are at various stages of commercial scale-up, with insect-protein ingredients receiving AAFCO regulatory recognition, a critical milestone expected to accelerate adoption across mainstream pet food formulations from 2025 onward.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Pet Type |

Dog Food |

42.14% |

2025 |

|

Product Type |

Dry Pet Food |

57.18% |

2025 |

|

Pricing Types |

Mass Products |

70.08% |

2025 |

|

Ingredient Types |

Animal Derived |

65.1% |

2025 |

|

Distribution Channel |

Supermarkets and Hypermarkets |

62.76% |

2025 |

By Pet Type

Dog food dominates the US pet food market by pet type with a 42.14% share in 2025. Its dominance reflects the highest pet ownership share as an estimated 71 million US households own a dog, combined with the widest range of price tiers, formulation types, and distribution channels serving diverse owner demographics.

To access detailed market analysis, Request Sample

Cat food holds a 38.26% share, growing as cat adoption continues to rise among urban, younger demographics who prefer cats for their lower maintenance requirements. Wet and canned formulations hold particular importance within cat food, as cats' obligate carnivore physiology and preference for high-moisture diets drive strong demand for pate, shredded, and broth-based product formats.

By Product Type

Dry pet food leads product format demand at 57.18% in 2025, driven by its superior shelf life, lower per-serving cost, and broad distribution footprint across both mass-market and specialty retail channels. Kibble products benefit from strong brand loyalty, with established platforms such as Purina Pro Plan and Hill's Science Diet commanding significant share within the veterinarian-recommended prescription dry food segment.

Wet and canned pet food accounts for 24.36%, with its share particularly strong in the cat food sub-segment due to cats' preference for moisture-rich diets. Snacks and treats represent 18.46% and are the fastest-growing product format by CAGR at 4.28%, fueled by the "treat humanization" trend and growing use of functional treats for dental care, anxiety relief, joint support, and reward-based training programs.

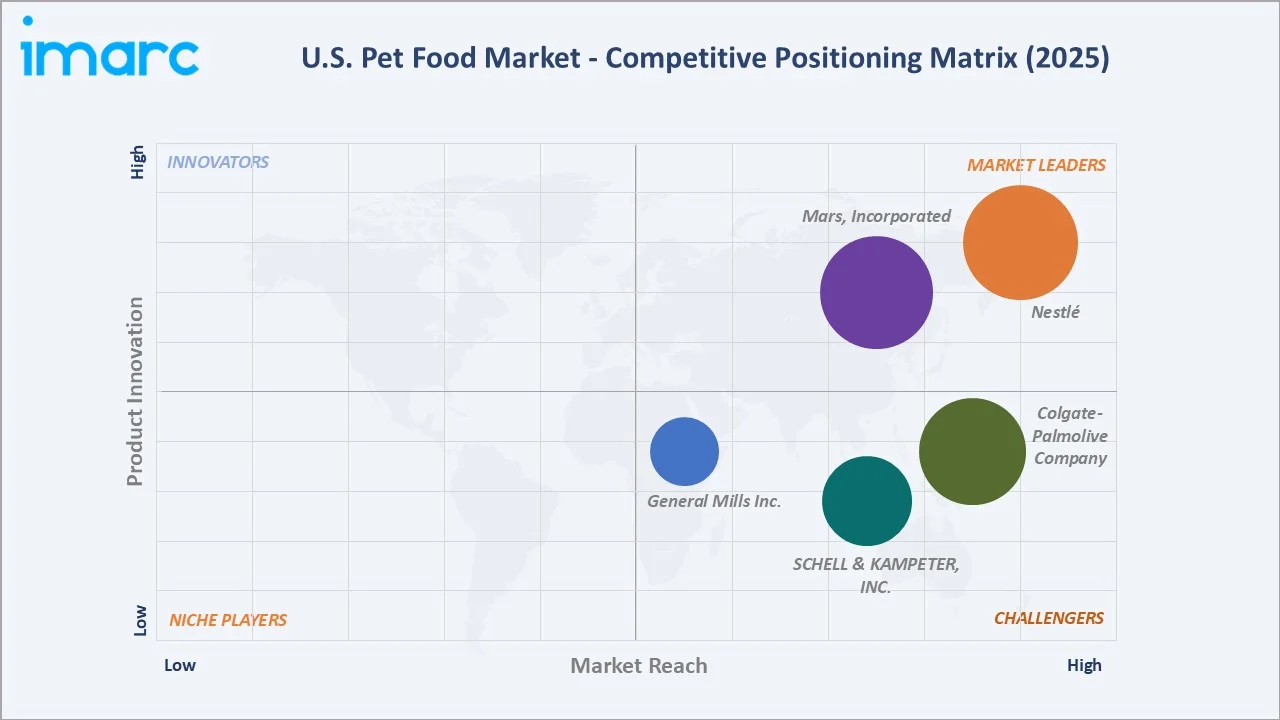

Competitive Landscape

The US pet food market exhibits a moderately concentrated structure. The top five manufacturers, Nestlé, Mars, Incorporated, Colgate-Palmolive Company, SCHELL & KAMPETER, INC., and General Mills Inc., collectively hold approximately 58–63% of the US market revenue in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Nestlé |

Purina ONE, Purina Pro Plan, Purina Pro Plan Veterinary Diets, Friskies, among others |

Market Leader |

Largest US pet food manufacturer; strong vet channel; innovation pipeline |

|

Mars, Incorporated |

Pedigree, Whiskas, IAMS, Royal Canin, CESAR, SHEBA, among others |

Market Leader |

Global breadth; veterinary/prescription strength via Royal Canin |

|

Colgate-Palmolive Company |

Hill’s Pet Nutrition |

Strong Challenger |

Dominant veterinary recommendation channel; therapeutic diet authority |

|

SCHELL & KAMPETER, INC. |

Diamond, Diamond Naturals, Diamond PRO89, Diamond CARE, Diamond CARE Rx, Diamond Naturals Grain-free |

Challenger |

Value-premium grain-free leadership; independent channel strength |

|

General Mills Inc. |

Blue Buffalo |

Challenger |

Natural/holistic positioning; strong digital marketing; major retail presence |

Regional and specialty manufacturers, along with an expanding cohort of direct-to-consumer fresh pet food startups, account for the remaining share. Competitive intensity is high, with leading players competing across price, product innovation, veterinary endorsement, retail shelf presence, and digital channel investment.

Key Company Profiles

Nestlé

Nestlé, headquartered in Vevey, Switzerland, is one of the largest pet food companies in the United States by revenue. The US pet food operating subsidiary is Nestlé Purina PetCare Company, headquartered in St. Louis, Missouri, which commands extensive retail penetration from mass-market to specialty channels.

- Product Portfolio: Purina ONE, Purina Pro Plan, Purina Pro Plan Veterinary Diets, Friskies, Dog Chow, Cat Chow, Fancy Feast, and DentaLife.

- Recent Developments: In May 2025, Nestlé Purina expanded its pet nutrition strategy by investing in advanced R&D and shifting toward therapeutic and functional pet foods designed to address specific health conditions. The company aimed to strengthen its growth by combining science-backed nutrition with veterinary-focused solutions.

- Strategic Focus: Expansion of veterinary nutrition platform; investment in digital direct-to-consumer capabilities; sustainability commitments under Nestlé's Net Zero roadmap.

Mars, Incorporated

Mars, Incorporated is also one of the dominant players with significant US market share across mass-market, premium, and veterinary-prescription pet food segments. Its Royal Canin brand serves as the global leader in breed-specific and veterinary therapeutic nutrition.

- Product Portfolio: Pedigree, Whiskas, IAMS, Royal Canin, CESAR, SHEBA, Temptations, Greenies, Nutro, Eukanuba, and Crave.

- Recent Developments: In July 2025, Mars, Incorporated committed to investing USD 2 billion in U.S. manufacturing through 2026 to expand production capacity, strengthen supply chains, and support innovation across its pet food portfolio.

- Strategic Focus: Veterinary channel deepening through Royal Canin; precision nutrition platform investment; digital ecosystem expansion via Whistle smart collar pet health integration.

SCHELL & KAMPETER, INC.

SCHELL & KAMPETER, INC., headquartered in Meta, Missouri, is a privately held US pet food manufacturer operating multiple manufacturing plants. It is best known for producing independent-channel and specialty retail brands, including Diamond Naturals.

- Product Portfolio: Diamond, Diamond Naturals, Diamond PRO89, Diamond CARE, Diamond CARE Rx, and Diamond Naturals Grain-free.

- Recent Developments: In September 2022, SCHELL & KAMPETER, INC. invested USD 259 million in a new 700,000-square-foot manufacturing and distribution facility in Rushville, Indiana, aimed at expanding production capacity to meet rising U.S. pet food demand.

- Strategic Focus: Private-label manufacturing scale; independent pet specialty channel leadership; value-premium grain-free positioning at accessible price points.

Market Concentration Analysis

The US pet food market exhibits moderate-to-high concentration at the national brand manufacturing level. The top five players, Nestlé, Mars, Incorporated, Colgate-Palmolive Company, SCHELL & KAMPETER, INC., and General Mills Inc., collectively account for approximately 58–63% of the US market revenue in 2025. However, a large and expanding cohort of independent natural pet food brands, private-label manufacturers, and direct-to-consumer startups ensures meaningful fragmentation in premium and specialty sub-segments.

Consolidation activity has been elevated, driven by major consumer goods companies seeking exposure to the high-growth pet nutrition sector. Strategic acquisitions include General Mills' purchase of Blue Buffalo (2018) and multiple private equity-backed roll-ups of regional natural pet food manufacturers. The US pet food market forecast anticipates continued M&A activity as large multinationals seek to fill portfolio gaps in fresh, functional, and sustainable nutrition categories.

Investment & Growth Opportunities

Fastest Growing Segments

Functional pet treats and supplements (estimated CAGR 5.8%), fresh and refrigerated pet food meal subscriptions (CAGR 9.2%), and personalized AI-driven nutrition platforms (CAGR 12%+) represent the three highest-growth investment vectors through 2034. Collectively, these niches address a total addressable market of approximately USD 8.5 Billion by 2034.

E-Commerce and DTC Platform Investment

Direct-to-consumer pet food platforms have attracted significant venture and growth capital, with fresh meal delivery brands including The Farmer's Dog and Ollie collectively raising over USD 500 million in institutional funding through 2024. These platforms demonstrate superior customer lifetime value and retention metrics versus conventional retail channels.

Venture and Institutional Investment Trends

- High-growth investment themes include functional ingredient platforms (probiotics, adaptogens, omega complexes), sustainable packaging innovation, and precision fermentation-derived alternative proteins.

- Private equity firms are increasingly targeting vertical integration plays—consolidating ingredient sourcing, manufacturing, and DTC distribution into single-platform pet food companies to capture full value chain margin.

- Retail channel development across underserved US markets—including rural independent pet specialty and US military commissary channels—represents an opportunity for value and mainstream pet food brands.

Future Market Outlook (2026-2034)

The US pet food market is positioned for sustained, broad-based growth through 2034. From a base of USD 46.90 Billion in 2025, the market is projected to reach USD 62.10 Billion by 2034, representing total incremental value creation of approximately USD 15.20 Billion over the forecast decade. The US pet food market forecast reflects the structural permanence of pet humanization as a consumer megatrend, the continued premiumization of product portfolios, and the accelerating role of e-commerce as the channel of choice for pet food purchasing.

Regulatory evolution, particularly FDA dietary guidelines for pet food health claims, AAFCO nutritional adequacy standard updates, and state-level labeling mandates on ingredient transparency, will drive product reformulation investment and elevate barriers to entry for undercapitalized new entrants. The US pet food market outlook is underpinned by three durable structural themes: demographic tailwinds, technological enablement, and health convergence.

Research Methodology

Primary Research

Primary research comprised structured interviews and surveys with over 120 industry participants in 2024–2025, including pet food manufacturers, contract manufacturers, ingredient suppliers, veterinary nutritionists, retail buyers, and end consumers across major US geographic markets. Proprietary IMARC Group consumer surveys captured purchasing patterns, ingredient preference, and price sensitivity across key demographic segments.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, FDA regulatory filings, AAFCO publications, APPA industry expenditure surveys, industry databases (Euromonitor, IRI/Circana, Nielsen), trade publications (Pet Business Magazine, Pet Age, Pet Product News), and publicly available financial disclosures.

Forecasting Models

Market size estimations were derived using a combination of top-down and bottom-up forecasting approaches, incorporating macroeconomic indicators, channel sell-through data, manufacturer-reported revenue figures, and proprietary demand modeling. A base-case CAGR of 3.17% reflects consensus analyst estimates validated against reported manufacturer growth rates and retail scanner data trends.

US Pet Food Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons, Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Pet Types Covered | Dog Food, Cat Food, Others |

| Product Types Covered | Dry Pet Food, Wet and Canned Pet Food, Snacks and Treats |

| Pricing Types Covered | Mass Products, Premium Products |

| Ingredient Types Covered | Animal Derived, Plant Derived |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Online, Others |

| Companies Covered | Nestlé, Mars, Incorporated, Colgate-Palmolive Company, SCHELL & KAMPETER, INC., General Mills Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the U.S. Pet Food Market Report

The US pet food market reached USD 46.90 Billion in 2025. It is projected to reach USD 62.10 Billion by 2034.

The US pet food market is expected to grow at a CAGR of 3.17% during the forecast period 2026-2034, supported by consistent demand driven by pet humanization, premiumization, and growing e-commerce channel adoption across all major US regions.

Dog food dominates the pet type segment with a 42.14% share in 2025. Its dominance is driven by approximately 71 million dog-owning US households and the widest range of formulations across the category, including breed-specific, life-stage, and prescription diets.

Dry pet food leads the product type segment with a 57.18% share in 2025, driven by its superior shelf life, lower per-serving cost, and extensive distribution across mass-market, club, and specialty retail channels.

Key drivers include the humanization of pets, rising consumer expenditure on pet health and wellness, premiumization toward functional and natural formulations, and the rapid growth of e-commerce and subscription-based pet food distribution channels.

Major trends include premiumization and humanization of pet diets, expansion of subscription-based DTC e-commerce channels, growing demand for functional and clinically validated nutrition, sustainable ingredient sourcing and eco-aligned packaging innovation, and the rise of AI-driven personalized pet nutrition platforms.

Key players in the US pet food market include Nestlé, Mars, Incorporated, Colgate-Palmolive Company, SCHELL & KAMPETER, INC., and General Mills Inc. The top five collectively hold approximately 58–63% of the US market revenue in 2025.

High-growth investment opportunities include functional pet treat and supplement formulations, fresh and refrigerated meal subscription platforms. AI-driven personalized nutrition services, alternative protein development, and sustainable packaging innovation targeting eco-conscious millennial and Gen Z pet owners.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)