U.S. Two Wheeler Market Size, Share, Trends and Forecast by Type, Technology, Transmission, Engine Capacity, Fuel Type, End User, Distribution Channel, and Region 2026-2034

U.S. Two Wheeler Market Size, Share, Trends & Forecast (2026-2034)

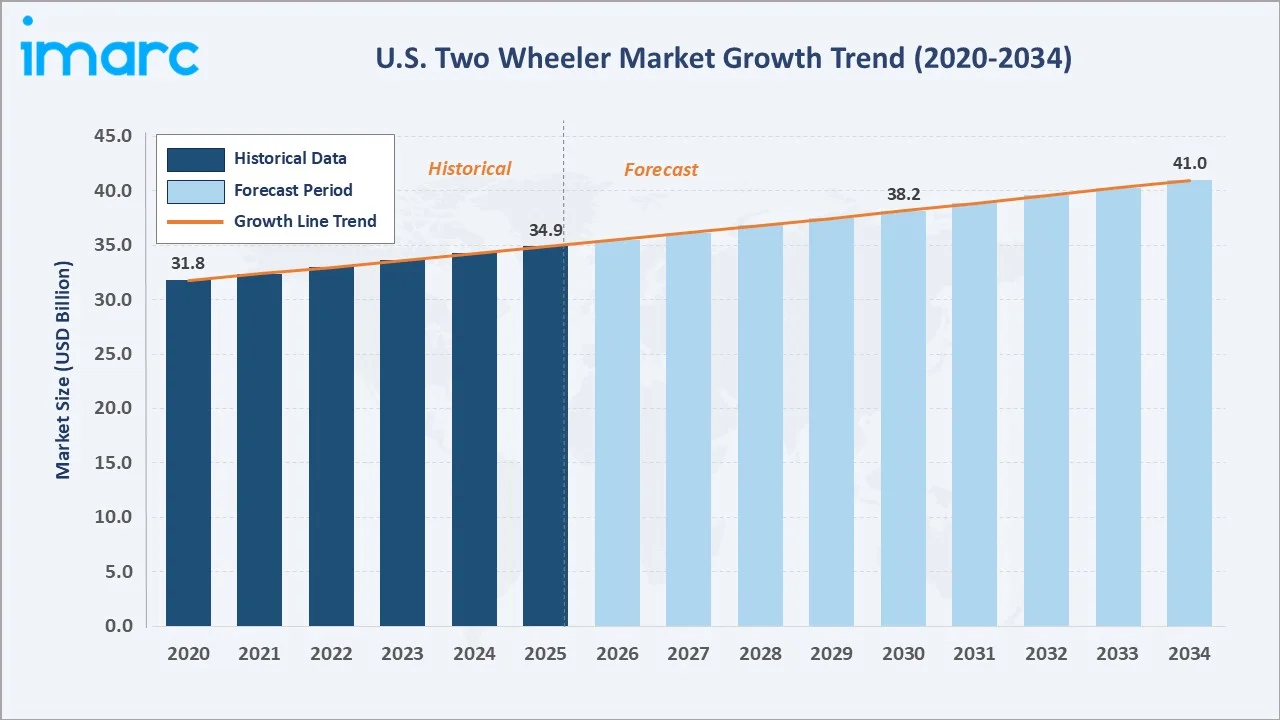

The U.S. Two Wheeler Market size reached USD 34.9 Billion in 2025 and is projected to reach USD 41.0 Billion by 2034, exhibiting a CAGR of 1.8% during 2026-2034. Growth is driven by rising urban mobility needs, increasing fuel efficiency awareness, growing interest in electric two-wheelers, and expanding recreational and leisure riding trends.

Market Snapshot

|

Report Attribute |

Key Statistics |

|

Market Size in 2025 |

USD 34.9 Billion |

|

Market Size in 2030 |

USD 38.2 Billion |

|

Market Forecast in 2034 |

USD 41.0 Billion |

|

Base Year |

2025 |

|

Forecast Years |

2026-2034 |

|

Market Growth Rate (2026-2034) |

1.8% CAGR |

|

Largest Region (2025) |

South – 36.8% |

|

Fastest Growing Segment (Type) |

Electric Two-Wheeler |

To get more information on this market, Request Sample

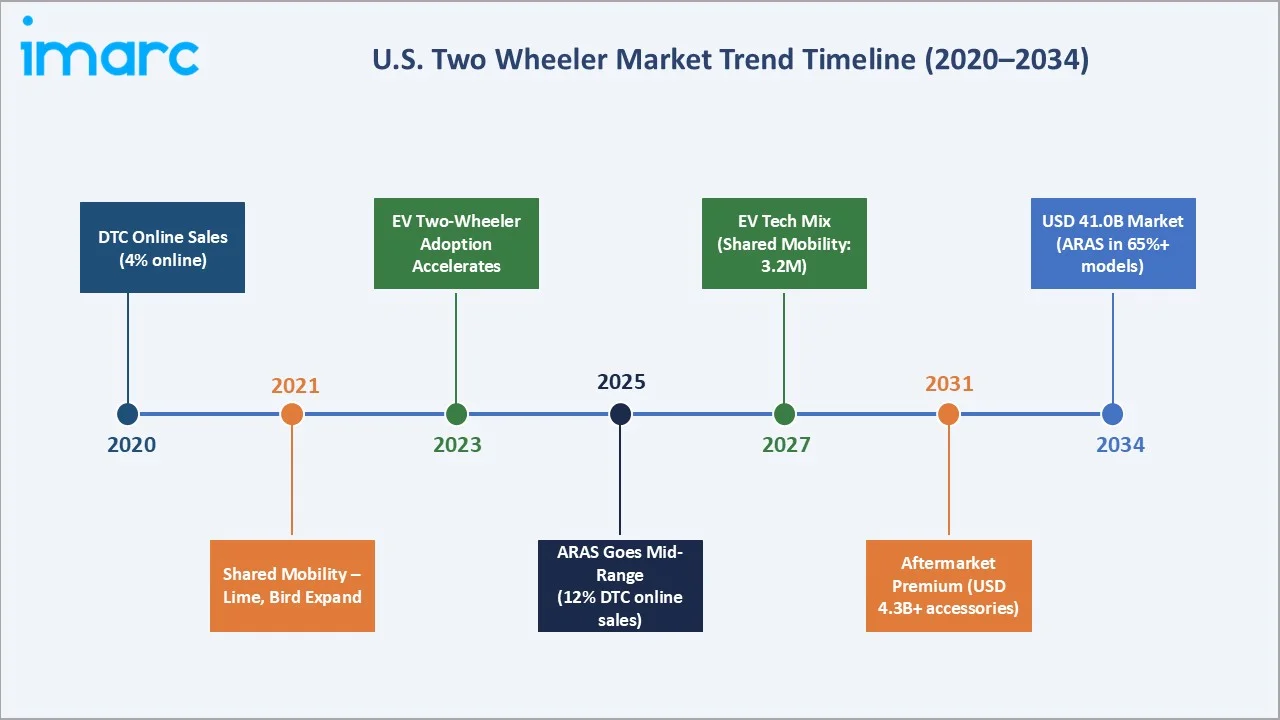

The market expanded steadily from USD 31.8 Billion in 2020, supported by pandemic-era mobility shifts, increased preference for personal transport, heightened outdoor recreational activity, and growing environmental awareness encouraging adoption of efficient, low-emission two-wheelers.

By 2025, the market has transitioned into a stable, measured growth trajectory, with electrification emerging as the primary incremental demand catalyst, supported by policy incentives, innovation, and expanding consumer acceptance through 2034.

Executive Summary

The U.S. Two Wheeler Market demonstrates steady, long-term growth momentum backed by structural lifestyle trends, transportation diversification, and rapid technology adoption. Valued at USD 34.9 Billion in 2025, the market is forecast to reach USD 41.0 Billion by 2034 at a CAGR of 1.8%.

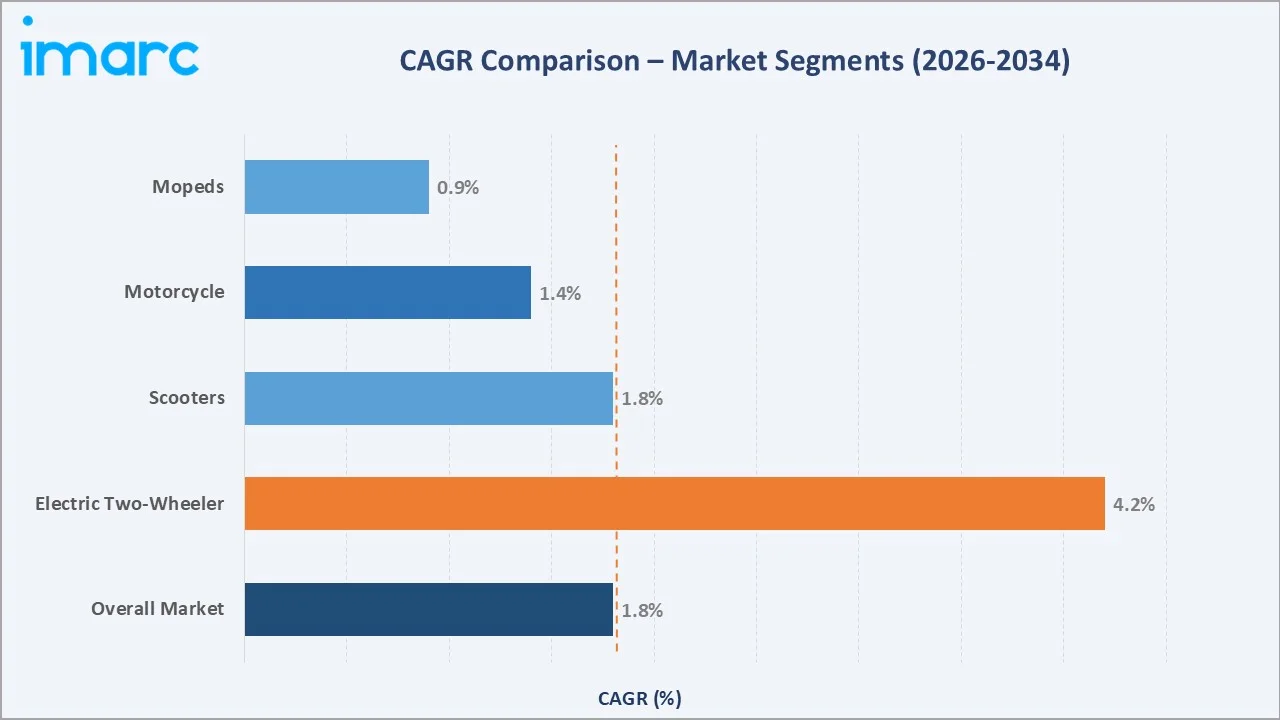

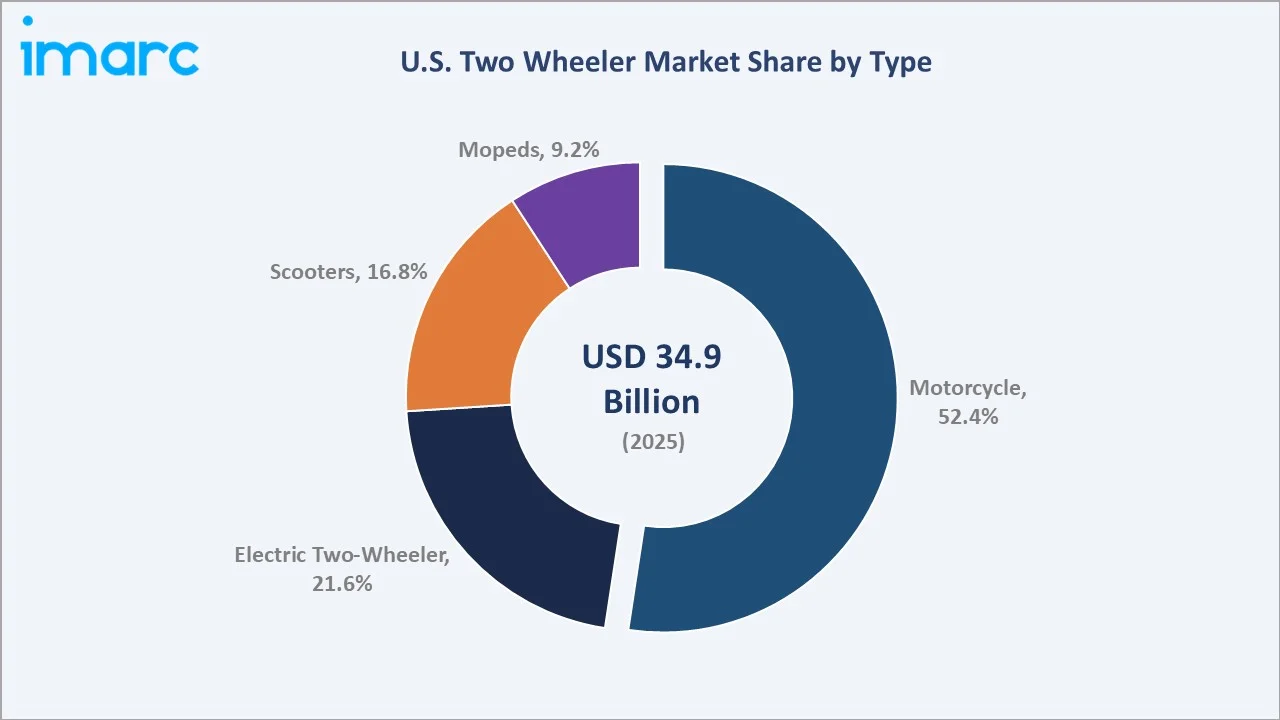

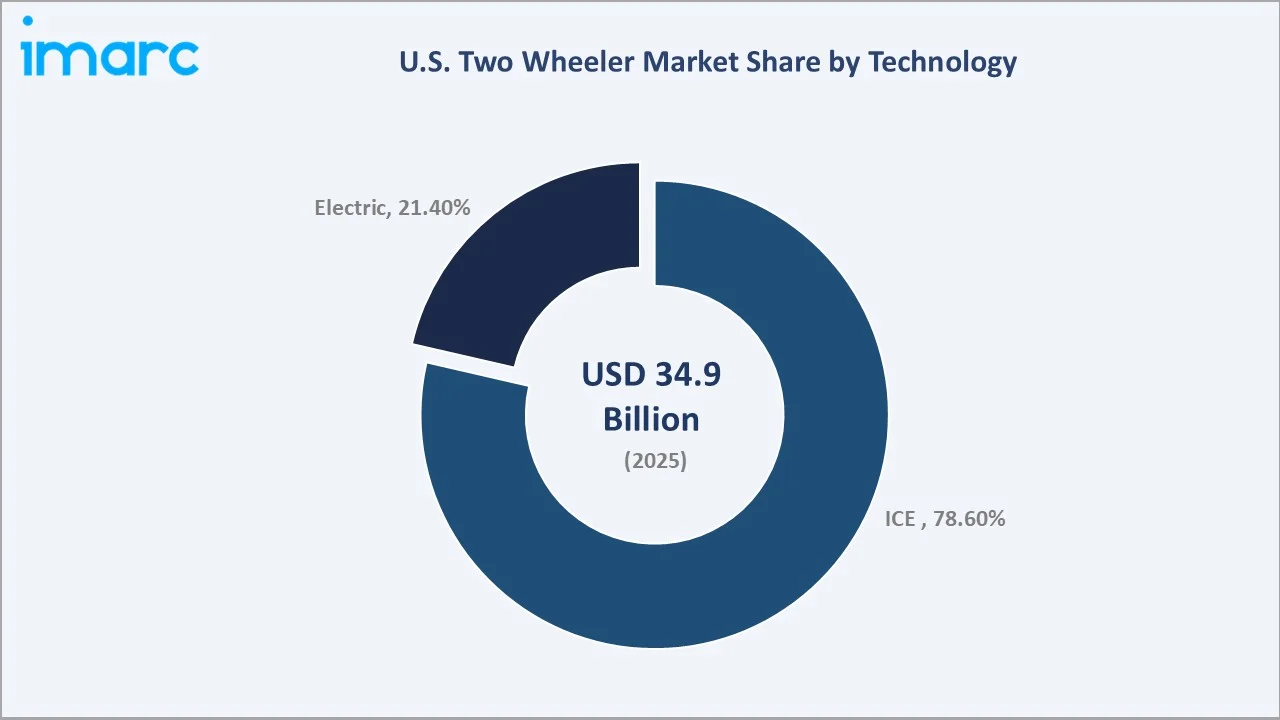

Motorcycles remain the largest segment at 52.4% of the 2025 type mix, reflecting their dominance in recreational and touring use. Electric two-wheelers, representing 21.6% of type share and 21.4% of the technology mix, are the fastest-growing sub-segment, driven by urban commuter adoption and federal EV incentives.

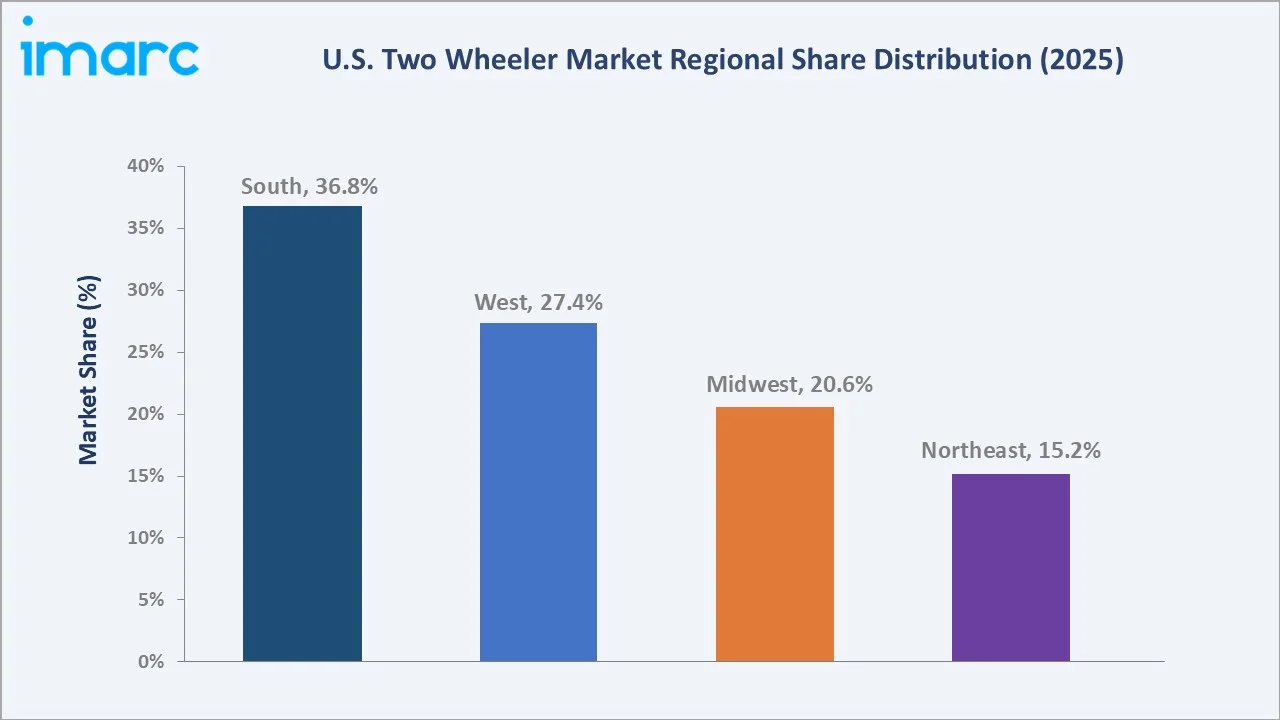

The South region commands a leading 36.8% revenue share in 2025, benefiting from favorable riding climates, lower vehicle taxation, and strong motorcycle culture. The West follows at 27.4%, buoyed by California's EV-forward policy environment, while the Midwest (20.6%) and Northeast (15.2%) contribute through recreational and commuter demand cycles respectively.

Key growth drivers include evolving commuter infrastructure, growing last-mile delivery fleet electrification, and expanding consumer credit availability for two-wheeler purchases. Overall, the market outlook through 2034 is constructive, with electrification, connectivity, and premiumization defining the next decade's competitive dynamics.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Motorcycle – 52.4% share (2025) |

|

Fastest Growing Segment (Type) |

Electric Two-Wheeler – ~4.2% CAGR (2026-2034) |

|

Largest Segment (Technology) |

ICE – 78.6% share (2025) |

|

Fastest Growing Segment (Tech) |

Electric – CAGR ~6.5% (2026-2034) |

|

Leading Region |

South – 36.8% revenue share (2025) |

|

Market Opportunity |

Electric Two-Wheeler fleet electrification |

Key Analytical Observations Supporting the Above Data:

- Motorcycles command 52.4% type share in 2025. They span recreational touring, commuter, and performance sub-categories, making them the most versatile and widely purchased two-wheeler format across all US regions.

- Electric two-wheelers represent 21.6% of type share and are growing at an estimated CAGR of 4.2% through 2034. Federal IRA tax credits of up to USD 1,500 per unit and state-level rebate programs in California, New York, and Colorado are materially accelerating adoption.

- The South's 36.8% dominance reflects year-round riding conditions, lower insurance premiums, and strong motorcycle culture across Texas, Florida, and the Carolinas, sustaining both recreational and commuter demand.

- Scooters at 16.8% and mopeds at 9.2% of type share serve the urban utility commuter and last-mile delivery segments, both of which are subject to strong electrification tailwinds through 2034.

- The West region’s 27.4% share is concentrated in California, which accounts for a significant portion of US electric two-wheeler registrations in 2025, underpinning the region’s above-average growth rate.

U.S. Two Wheeler Market Overview

The U.S. two wheeler industry encompasses the design, manufacturing, distribution, and retail sale of motorcycles, electric two-wheelers, scooters, and mopeds for personal and commercial use. The sector interfaces with automotive supply chains, battery and powertrain technology, insurance, and aftermarket service ecosystems.

Consumer segments span recreational touring enthusiasts, urban commuters, food-delivery operators, and fleet logistics businesses. Macroeconomic influences include consumer confidence indices, personal disposable income trends, fuel price movements, and federal transportation and clean energy policy.

Market Dynamics

To evaluate market opportunities, Request Sample

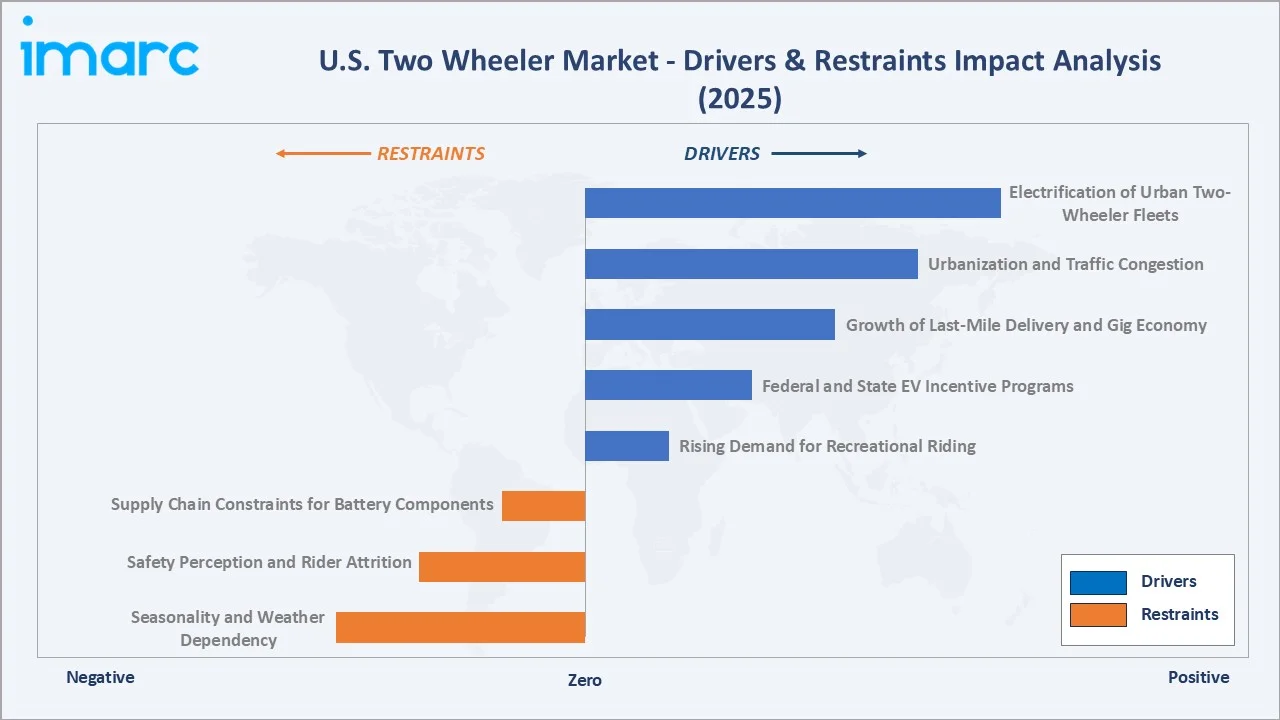

Market Drivers

- Rising Demand for Recreational Riding: US motorcycle registration volumes reflect durable leisure demand, reaching about 8.8 million registered motorcycles in 2023. Post-pandemic outdoor recreation trends have reinforced two-wheeler ownership as an accessible, personally fulfilling hobby across demographic cohorts.

- Federal and State EV Incentive Programs: The Inflation Reduction Act (IRA, 2022) and state-level zero-emission vehicle rebates have materially lowered the effective purchase price of electric two-wheelers. The USD 1,500 federal credit and California's Clean Vehicle Rebate Project (CVRP) subsidies are directly stimulating the electric two-wheeler sub-segment.

- Growth of Last-Mile Delivery and Gig Economy: The expansion of on-demand food and package delivery platforms including DoorDash, Uber Eats, and Amazon Flex has generated durable commercial fleet demand for electric scooters and mopeds. Urban fleet operators prioritize the lower fuel and maintenance costs of electric models, supporting steady growth in the commercial end-user segment through 2034.

- Urbanization and Traffic Congestion: US Census Bureau data projects continued urban population growth through 2034, intensifying congestion in major metros. Two-wheelers offer significant commuter time savings versus passenger cars in peak-hour conditions, driving practical ownership beyond purely recreational motivations.

Market Restraints

- Seasonality and Weather Dependency: Two-wheeler usage and, consequently, retail demand are heavily concentrated in Q2–Q3 in the Midwest and Northeast, where cold winters constrain the effective riding season to approximately 5–6 months. This creates pronounced revenue cyclicality and inventory management challenges for dealerships in these regions.

- Safety Perception and Rider Attrition: NHTSA data indicates motorcyclists account for a disproportionately high fatality rate per mile travelled versus passenger cars, sustaining negative consumer perception among potential new entrants. Safety concerns represent a structural constraint on market penetration beyond the existing rider base.

Market Opportunities

- Electrification of Urban Two-Wheeler Fleets: The commercial delivery fleet segment represents one of the most addressable near-term electrification opportunities in the US two-wheeler market. Fleet operators' sensitivity to total cost of ownership creates a compelling ROI case for electric models, with payback periods estimated at 18–24 months versus comparable ICE scooters at current energy and fuel prices.

- Connected and Smart Two-Wheeler Platforms: OEM integration of telematics, over-the-air (OTA) firmware updates, anti-lock braking systems (ABS), and traction control on mid-range platforms is expanding the addressable market for technology-forward buyers.

- Premiumization and Touring Segment Growth: Premium motorcycle models priced above USD 20,000 including touring, sport, adventure, and cruiser categories are growing faster than the mass market, supported by the aging Baby Boomer rider cohort's rising disposable income. Harley-Davidson's CVO touring lineup and Indian Motorcycle's Pursuit Elite reflect this premiumization opportunity.

Market Challenges

- Supply Chain Constraints for Battery Components: Electric two-wheeler manufacturers face persistent supply chain risks related to lithium-ion cell availability, semiconductor shortages, and rare-earth magnet supply. The industry's dependence on Asian battery supply chains particularly Chinese cell manufacturers introduces geopolitical and tariff risk exposure.

- Dealer Network Modernization: Traditional franchise dealerships, which account for a dominant share of US two-wheeler retail, face rising technology and capital investment needs to effectively serve electric vehicle buyers, including charging infrastructure, battery diagnostics, and technician training, with under-investment creating customer experience gaps.

Emerging Market Trends

1. Rapid Electric Two-Wheeler Adoption in Urban Corridors

Electric two-wheelers are transitioning from niche to mainstream in US urban commuter markets, with an estimated 21.4% of the 2025 technology mix now composed of electric powertrains. OEMs including Zero Motorcycles, and Harley-Davidson's LiveWire brand, and new market entrants are expanding model lineups.

2. Integration of Advanced Rider Assistance Systems (ARAS)

Adaptive cruise control, collision warning, cornering ABS, and lean-angle-sensitive traction control are steadily moving from premium to mid-range two-wheeler segments. By 2034, a majority of higher-priced motorcycles are expected to incorporate multiple ARAS features, reflecting a structural technology shift aligned with National Highway Traffic Safety Administration safety initiatives.

3. Subscription and Shared Mobility Models

Urban two-wheeler sharing programs including electric scooter fleets operated by Lime, Bird, and Super pedestrian are expanding beyond initial coastal markets. Monthly motorcycle subscription services offered by companies such as Riders Share and Indian Motorcycle's own rental program provide flexible access without long-term ownership commitment.

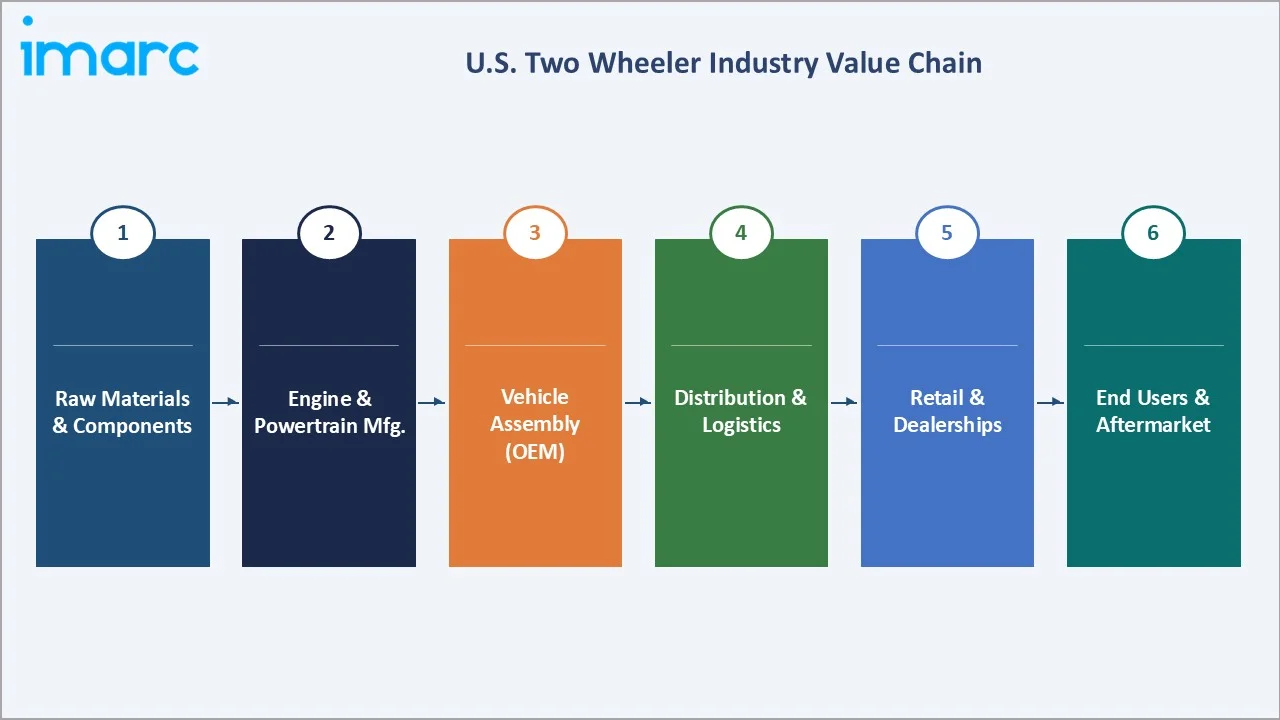

Industry Value Chain Analysis

The U.S. two wheeler value chain spans six interconnected stages from raw material supply and component manufacturing through OEM assembly, distribution, retail, and end-consumer ownership. Each stage presents distinct competitive dynamics and margin structures.

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Steel mills (Nucor), aluminum suppliers (Novelis), battery cell manufacturers (Panasonic, CATL, Samsung SDI), rubber and plastics producers |

|

Engine & Powertrain Manufacture |

In-house OEM divisions (Honda, Yamaha); specialized ICE engine suppliers; e-motor and power electronics specialists (Bosch, Continental) |

|

Vehicle Assembly (OEM) |

Harley-Davidson (Milwaukee, WI), Honda Manufacturing of Alabama, Kawasaki (Lincoln, NE), Zero Motorcycles (Scotts Valley, CA) |

|

Distribution & Logistics |

OEM regional distribution centers; third-party automotive logistics (RCX Motorcycles Transport, Intercity Lines); import brokers for Asian-sourced models |

|

Retail & Dealerships |

Franchised OEM dealerships (~5,400 US locations in 2025); independent multi-brand dealers; online retail platforms (RevZilla, Cycle Gear, Amazon) |

|

End Users & Aftermarket |

Individual recreational and commuter owners; commercial delivery fleets; rental and subscription operators; independent service and customization shops |

Component localization is a growing strategic priority, with US-based OEMs facing Section 301 tariffs on Chinese-sourced battery cells and electronic components. Honda and Harley-Davidson have each announced supply chain diversification initiatives through 2026–2027 to reduce single-source dependency and improve domestic content ratios.

Technology Landscape in the U.S. two wheeler Industry

Electric Powertrain and Battery Technology

Lithium-ion battery packs using NMC and LFP chemistries dominate the electric two-wheeler segment. Leading models offer strong urban range capabilities, while declining battery costs are supporting wider adoption and enabling price competitiveness with ICE models, particularly in high-volume scooter segments.

Internal Combustion Engine Efficiency

Modern ICE platforms incorporate advanced technologies such as variable valve timing, ride-by-wire throttle systems, and engine idle stop-start to meet stringent emission standards. Fuel-injected engines have fully replaced carbureted systems across major OEMs. Models like Harley-Davidson’s Revolution Max and Honda’s Africa Twin exemplify improved efficiency and performance in current-generation engines.

Connected Motorcycle Platforms

Over-the-air (OTA) firmware capability enabling remote diagnostics, navigation updates, and performance tuning. Harley-Davidson's H-D Connect (powered by Twilio IoT), Ducati's Connectivity Box, and BMW Motorrad's Connected Ride system represent the current OEM-led connectivity ecosystem. Third-party telematics providers (Zubie, GEICO's DriveEasy Moto) are expanding aftermarket connectivity solutions for existing fleet operators.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Motorcycle |

52.4% |

2025 |

|

Technology |

ICE |

78.6% |

2025 |

|

Transmission |

🔒 |

🔒 |

2025 |

|

Engine Capacity |

🔒 |

🔒 |

2025 |

|

Fuel Type |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

South |

36.8% |

2025 |

By Type

To access detailed market analysis, Request Sample

Motorcycles lead the U.S. two wheeler type segmentation with a 52.4% market share in 2025, a reflection of the US market's distinctively recreation-oriented two-wheeler culture compared to Asian markets. The category spans cruiser, touring, sport, adventure-touring, and naked/standard sub-segments, with touring and cruiser models representing the majority of unit revenue given their premium average selling prices.

By Technology

ICE technology retains a commanding 78.6% of the U.S. two wheeler technology mix in 2025. This reflects the dominance of recreational motorcycle categories where range, fueling convenience, and the established performance and sound character of internal combustion engines remain core purchase drivers.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Companies |

|

South |

36.8% |

Year-round riding climate; motorcycle culture in TX, FL, NC; strong dealership density; high recreational demand |

Harley-Davidson, Indian Motorcycle, Honda, Kawasaki |

|

West |

27.4% |

California EV policy leadership; urban commuter adoption; Silicon Valley tech-forward rider base; CARB zero-emission standards |

Zero Motorcycles, LiveWire, Yamaha, Honda, KTM |

|

Midwest |

20.6% |

Seasonal but loyal recreational rider base; touring and adventure segment strength; strong regional dealer networks |

Harley-Davidson, Indian Motorcycle, BMW Motorrad, Triumph |

|

Northeast |

15.2% |

Urban commuter demand in NYC, Boston, DC; growing electric scooter fleet operations; higher income demographics |

Zero Motorcycles, Ryvid, Honda, Vespa (Piaggio) |

The South's 36.8% market share reflects its status as the heartland of US motorcycle culture. Texas, Florida, and the Carolinas each support active motorcycle communities, extensive dealership infrastructure, and favorable regulatory environments.

Competitive Landscape

The U.S. Two Wheeler Market is moderately concentrated at the OEM level, with Harley-Davidson, Inc., American Honda Motor Co., Kawasaki Motors Corp., U.S.A., Yamaha Motor Corporation, U.S.A. collectively accounting for an estimated 55–60% of total market revenues in 2025.

|

Company Name |

Key Brand(s) |

Market Position |

Core Strength |

|

Harley-Davidson, Inc. |

LiveWire Group, Inc |

Market Leader |

Dominant brand equity in cruiser/touring; LiveWire EV brand expansion; extensive US dealer network (~1,400 locations) |

|

American Honda Motor Co. |

Honda |

Volume Leader |

Broadest model lineup across all type categories; strong value-for-money positioning; global R&D scale |

|

Kawasaki Motors Corp., U.S.A. |

Kawasaki, Ninja |

Strong Challenger |

Sport motorcycle leadership; performance engineering heritage; growing adventure-touring portfolio |

|

Yamaha Motor Corporation, U.S.A. |

Yamaha, MT, YZF-R |

Strong Challenger |

Crossover sport/adventure strength; connected bike platform investment; growing scooter presence |

|

Indian Motorcycle Company |

Indian |

Premium Challenger |

Direct Harley-Davidson competitor; premium touring and cruiser positioning; growing brand loyalty base |

|

Zero Motorcycles, Inc. |

Zero |

EV Innovation Leader |

Pure-play US EV-native motorcycle OEM; strongest electric range and performance credentials in class |

|

BMW Motorrad (BMW AG) |

BMW Motorrad |

Premium Specialist |

Premium adventure and touring leadership; ARAS technology pioneer; high average selling price discipline |

The electric sub-segment introduces a more fragmented competitive structure, with Zero Motorcycles (dominant US-based EV-native OEM), LiveWire (Harley's EV spin-off), and multiple Asian and domestic startups competing for early adopter share.

Key Company Profiles

Harley-Davidson Inc.

Harley-Davidson is the dominant force in US two-wheeler market. Founded in Milwaukee, Wisconsin in 1903, the company is the defining brand in American recreational motorcycling..

- Product Portfolio: Touring (Road Glide, Street Glide), Softail (Fat Boy, Heritage Classic), Pan America (adventure), Nightster (Sportster series), LiveWire One and S2 Del Mar (electric).

- Recent Developments: In 2026, Harley-Davidson is set to launch a new affordable entry-level bike featuring a 750cc engine, offering around 35 km mileage, with an attractive price point of approximately $4,500, targeting budget-conscious riders.

- Strategic Focus: Hardwire strategy targeting premiumization, selective global expansion, and LiveWire EV brand scaling; dealer experience modernization; connected services revenue growth through H-D Connect platform.

American Honda Motor Co. Inc.

Honda is the world's largest motorcycle manufacturer by unit volume and holds the second-largest US market share position across all two-wheeler categories.

- Product Portfolio: Gold Wing (premium touring), Africa Twin (adventure), CBR series (sport), Ruckus and Metropolitan (scooters), PCX and ADV (mid-range scooters), CM and Rebel (cruiser).

- Recent Developments: In 2025, Honda Motor Company announced a $300M increase in investments in three auto manufacturing plants in Ohio and plans to invest $4.4 billion in a joint venture (JV) plant in its efforts to begin EV production.

- Strategic Focus: Broadest model lineup strategy; accelerated EV R&D investment; connected HONDE (Honda Motorcycle Navigator Ecosystem) platform rollout; safety technology democratization across mid-range models.

Zero Motorcycles Inc.

Zero Motorcycles is the leading US-native electric motorcycle OEM, founded in 2006 in Santa Cruz, California. The company has established the strongest EV performance credentials in the US market, with its SR/F flagship achieving a 161-mile city range.

- Product Portfolio: SR/F (naked sport electric), SR/S (sport touring electric), DSR/X (electric adventure), FXE (urban), FX (dual sport).

- Recent Developments: In 2025, Zero Motorcycles reported an 89% year-over-year retail sales growth in North America, driven significantly by strong demand for its new XE and XB electric dirtbike models, which played a critical role in boosting overall performance.

- Strategic Focus: Electric performance leadership; expanding service-certified dealer network; OTA software monetization; international expansion into Europe and Australia where EV adoption is ahead of US pace.

Market Concentration Analysis

The U.S. Two Wheeler Market exhibits moderate-to-high concentration at the established OEM level, with the top five manufacturers – Harley-Davidson, Inc., American Honda Motor Co., Kawasaki Motors Corp., U.S.A., Yamaha Motor Corporation, U.S.A., Indian Motorcycle Company collectively accounting for an estimated 65–70% of total market revenues in 2025. This concentration is highest in the premium motorcycle segment (above USD 15,000), where Harley-Davidson and Indian Motorcycle together hold an estimated 72–75% combined share.

Consolidation dynamics are expected to intensify through 2034, with larger OEMs acquiring EV-native startups to accelerate electrification capabilities. Private equity interest in the aftermarket accessories and dealer group sectors is also rising, with three significant dealer group acquisitions completed in 2023–2025.

Investment & Growth Opportunities

Fastest Growing Segments

Electric two-wheelers, connected motorcycle platforms, and premium adventure-touring models represent the three highest-growth investment vectors in the US two-wheeler market through 2034. The electric segment's estimated 4.2–6.5% CAGR vastly outpaces the overall market's 1.8% CAGR, creating concentrated value creation opportunity for capital allocators.

Emerging Market Expansion

Last-mile delivery fleet electrification represents the most immediately actionable B2B growth opportunity, with DoorDash, Uber Eats, and Amazon Flex operators actively seeking to electrify their contractor and direct-employee delivery fleets.

Strategic Investment Trends

- Battery supply chain localization is attracting significant investment, supported by U.S. Department of Energy initiatives to fund domestic gigafactory projects, which are expected to further reduce two-wheeler battery pack costs relative to imported cells and strengthen local manufacturing capabilities.

- Dealer group consolidation is accelerating, with private equity-backed multi-OEM dealer platforms investing in digital retail, in-store EV service certification, and subscription mobility models as differentiation strategies.

Future Market Outlook (2026-2034)

The U.S. Two Wheeler Market is positioned for steady, structurally supported growth through 2034, underpinned by durable recreational demand, accelerating electrification, and expanding commercial fleet applications. From USD 34.9 Billion in 2025, the market is projected to reach USD 38.2 Billion by 2030 and USD 41.0 Billion by 2034 at a 1.8% CAGR, with electric sub-segment growth materially outpacing the headline rate.

The competitive landscape will evolve toward greater polarization with established ICE OEMs extending high-margin premium and touring product cycles alongside dedicated EV brand development, while pure-play EV OEMs and new market entrants compete aggressively for the growing urban commuter and delivery fleet electric segment.

Research Methodology

Primary Research

Primary research for this report included structured interviews with over 120 industry stakeholders in 2024–2025, comprising motorcycle OEM product managers, franchise dealership principals, fleet operators, regulatory affairs professionals, battery supply chain executives, and investment analysts covering the US automotive and two-wheeler sector. Interviews were conducted via structured questionnaires covering market sizing, competitive dynamics, technology adoption rates, and regional demand patterns.

Secondary Research

Secondary research encompassed a comprehensive review of OEM annual reports (Harley-Davidson, Polaris/Indian, Zero Motorcycles, LiveWire Group), trade publications (Motorcycle Industry Council, Powersports Business, Cycle News), regulatory filings (EPA, NHTSA, CARB), government statistical databases (BLS, Census Bureau, DOT FHWA), and industry association data (MIC Annual Data Report 2024–2025). Market intelligence platforms and patent databases were reviewed to assess technology landscape trends.

Forecasting Models

Market size estimates and CAGR projections were derived through a combination of bottom-up unit volume forecasting (by segment, technology, and region) and top-down revenue modeling incorporating average selling price trajectory analysis. Forecast assumptions incorporate US GDP growth projections (2.1% CAGR 2026–2034), EV battery cost decline curves, fuel price scenarios, and regulatory timeline modeling for zero-emission zone implementation across major US metro areas.

U.S. Two Wheeler Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Scooters, Mopeds, Motorcycle, Electric Two-Wheeler |

| Technologies Covered | ICE, Electric |

| Transmissions Covered | Manual, Automatic |

| Engine Capacities Covered | <100cc, 100-125cc, 126-180cc, 181-250cc, 251-500cc, 501-800cc, 801-1600cc, >1600cc |

| Fuel Types Covered | Gasoline, Petrol, Diesel, LPG/CNG, Battery |

| End Users Covered | Personal, Commercial |

| Distribution Channels Covered | Offline Channels, Online Channels |

| Regions Covered | Northeast, Midwest, South, West |

| companies Covered | Harley-Davidson Inc., American Honda Motor Co., Kawasaki Motors Corp. U.S.A., Yamaha Motor Corporation U.S.A., Indian Motorcycle Company, Zero Motorcycles Inc.,BMW Motorrad (BMW AG), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the U.S. two wheeler market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the U.S. two wheeler market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the U.S. two wheeler industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the U.S Two Wheeler Market Report

The U.S. Two Wheeler Market reached USD 34.9 Billion in 2025 and is projected to reach USD 41.0 Billion by 2034, growing at a CAGR of 1.8%.

The market is expected to grow at a CAGR of 1.8% during 2026-2034, driven by electrification, recreational demand, and fleet adoption.

Motorcycles lead with a 52.4% type share in 2025, driven by recreational touring, cruiser, and sport category dominance across US demographics.

ICE technology commands 78.6% of the 2025 technology mix, while electric models hold 21.4% and are growing rapidly through the forecast period.

The South dominates with a 36.8% share in 2025, benefiting from year-round riding climate, strong motorcycle culture, and favourable regulatory environment.

Key drivers include recreational riding demand, EV incentive programs, last-mile delivery fleet electrification, urbanization, and connected vehicle technology adoption.

Leading players include Harley-Davidson, Inc., American Honda Motor Co., Kawasaki Motors Corp., U.S.A., Yamaha Motor Corporation, U.S.A., Indian Motorcycle Company, Zero Motorcycles, Inc., BMW Motorrad (BMW AG).

Electric two-wheelers are the fastest-growing type segment at ~4.2% CAGR; within technology, the electric segment is growing at ~6.5% CAGR through 2034.

Key challenges include seasonal demand concentration, rising insurance costs, safety perception barriers, battery supply chain constraints, and regulatory uncertainty on emissions.

The market is projected to reach USD 41.0 Billion by 2034, with electrification, connected platforms, fleet applications, and premiumization as the defining growth themes.

Key opportunities include electric fleet electrification, connected platform software revenue, premium touring segment growth, and EV supply chain localization.

Electrification is the market's most transformative force, with the electric segment projected to reach approximately 35–38% of new unit sales by 2034 from 21.4% in 2025.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade