Utility and Energy Analytics Market Size, Share, Trends and Forecast by Type, Deployment, Application, Vertical, and Region, 2026-2034

Utility and Energy Analytics Market Size and Share:

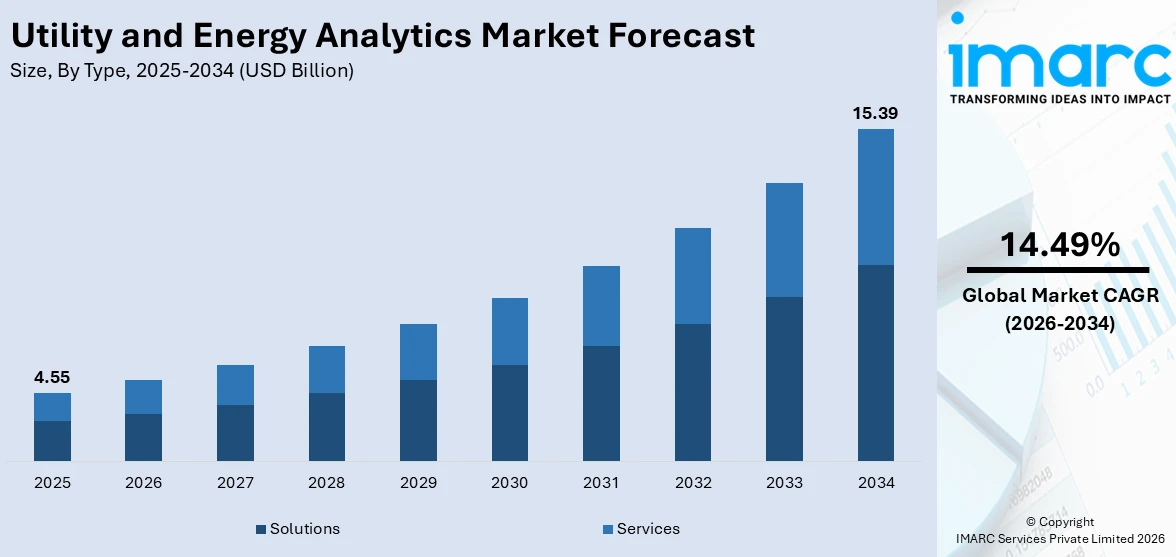

The global utility and energy analytics market size was valued at USD 4.55 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 15.39 Billion by 2034, exhibiting a CAGR of 14.49% from 2026-2034. North America currently dominates the market, holding a market share of 40% in 2025. The region benefits from a highly developed digital energy infrastructure, widespread smart meter deployments, proactive federal investments in grid modernization, and a robust ecosystem of analytics technology providers that collectively advance demand forecasting, predictive asset maintenance, and grid reliability, all strengthening the utility and energy analytics market share.

The global market is driven by a convergence of transformative forces reshaping how energy is generated, managed, and delivered worldwide. The accelerating transition toward renewable energy sources such as solar and wind power has introduced substantial variability into electricity grids, compelling utility operators to adopt sophisticated analytics platforms for real-time demand-response management and generation output forecasting. Simultaneously, the widespread proliferation of internet of things (IoT) devices, smart meters, and grid-connected sensors is producing enormous volumes of operational data that utilities are increasingly leveraging to optimize asset performance and preempt equipment failures. The surge in global electricity consumption, fueled by industrial digitalization, rapid urbanization, and the electrification of transportation, is further compelling grid operators to deploy utility and energy analytics solutions that deliver precise load-balancing capabilities and cost-reduction strategies. These compounding dynamics collectively underpin the robust utility and energy analytics market outlook globally.

The United States has emerged as a major region in the utility and energy analytics market owing to many factors. The country possesses one of the world's most advanced digital energy ecosystems, underpinned by decades of smart grid investment and a dense network of utilities actively pursuing data-driven operational transformation. Federal programs, including grid modernization initiatives funded through the Infrastructure Investment and Jobs Act, have channeled substantial capital toward analytics-ready infrastructure upgrades, creating fertile ground for solution providers across metering, forecasting, and cybersecurity domains. At the close of 2023, the count of smart meters in North America nearly hit 146 million and, with continuing expansion, is projected to reach 182.9 million by 2029, generating an unprecedented volume of granular consumption data that fuels demand for advanced analytics platforms. The rapid integration of distributed energy resources, including rooftop solar and behind-the-meter storage, is amplifying grid complexity and driving utilities to adopt real-time analytics capabilities. Strong collaboration between energy companies, technology providers, and research institutions continues to accelerate commercialization of AI-powered grid analytics solutions, sustaining the United States utility and energy analytics market forecast momentum.

To get more information on this market Request Sample

Utility and Energy Analytics Market Trends:

Rising Integration of Artificial Intelligence

The escalating adoption of artificial intelligence and machine learning within the utility and energy analytics space is fundamentally transforming how utilities generate, interpret, and act on operational data. These sophisticated technologies enable utilities to analyze massive, heterogeneous datasets drawn from smart meters, sensors, and weather feeds, identifying hidden consumption patterns and anomalies that conventional analysis methods cannot detect. AI-powered predictive maintenance platforms are enabling utilities to forecast equipment degradation before failures occur, substantially reducing unplanned downtime and associated maintenance expenditures. Machine learning (ML) models integrated into demand forecasting systems are elevating grid balancing precision, helping operators minimize reliance on costly peaker capacity and optimize dispatch schedules. The International Energy Agency projected capital investments of USD 3.3 trillion in the global energy sector by 2025, a significant portion of which is directed toward digital technologies including AI analytics. As utilities worldwide increasingly recognize AI as a critical competitive differentiator, ongoing investment in talent, data infrastructure, and integrated analytics platforms is expected to sustain robust utility and energy analytics market growth in the years ahead.

Accelerating Adoption of Cloud-Based Platforms

The migration toward cloud-based analytics deployment models is emerging as a defining structural shift in the utility and energy analytics landscape, driven by utilities' growing need for scalable compute capacity, embedded AI services, and accelerated time-to-value. Cloud platforms offer compelling economic advantages over traditional on-premises deployments, enabling utilities to process and analyze vast data volumes from smart meters, sensors, and distributed energy resources without incurring prohibitive upfront infrastructure investments. Sector-specific cloud solutions now incorporate hardened security controls and audit-ready environments that address the compliance concerns historically preventing mission-critical workload migration. ERCOT, the Texas power grid operator, forecasted demand from large flexible loads to reach 54 billion kilowatt-hours in 2025, approximately 60% higher than 2024 levels, intensifying the need for horizontally scalable cloud analytics architectures capable of handling surging data volumes. The utility and energy analytics market forecast strongly favors cloud deployment as the dominant growth modality, particularly for advanced metering infrastructure analytics, demand-response management, and customer engagement platforms.

Growing Emphasis on Grid Cybersecurity Analytics

The progressive digitalization of power grids and utility operations is generating unprecedented cybersecurity imperatives, emerging as a powerful growth catalyst for the utility and energy analytics market trends. As utilities deploy millions of interconnected smart meters, IoT sensors, and cloud-linked operational technology platforms, the attack surface for malicious actors expands correspondingly, elevating the strategic importance of advanced analytics tools that can continuously monitor network traffic, detect anomalous behavior, and trigger automated incident response workflows. AI-driven anomaly detection solutions are increasingly being embedded within operational technology environments to provide real-time threat identification capabilities that legacy security systems cannot deliver. as per IMARC Group, the global smart grid cybersecurity market was valued at 10.2 Billion in 2024, reflecting the substantial investment utilities and governments are directing toward digital infrastructure protection. Regulatory frameworks worldwide are reinforcing this momentum, mandating minimum cybersecurity standards for critical energy infrastructure and creating sustained demand for compliance-oriented analytics platforms. Vendors are responding with integrated security suites that unify operational and information technology monitoring within single analytics environments, enabling utilities to maintain operational continuity while proactively neutralizing emerging digital threats.

Utility and Energy Analytics Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global utility and energy analytics market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on type, deployment, application, and vertical.

Analysis by Type:

- Solutions

- Services

Solutions hold 68% of the market share. Utility and energy analytics solutions encompass a broad portfolio of software platforms, advanced analytics engines, and AI-powered applications specifically engineered to convert raw energy data into actionable operational insights. These platforms enable utility operators to continuously monitor grid performance, forecast electricity demand with high precision, detect equipment anomalies before failures occur, and optimize the integration of distributed energy resources across complex transmission and distribution networks. The comprehensive nature of these solutions positions them as indispensable tools for utilities pursuing digital transformation strategies. Their ability to generate demonstrable return on investment through reduced outage durations, lower maintenance expenditures, and optimized dispatch schedules drives consistently high adoption among grid operators and energy retailers. The accelerating complexity of modern energy systems, driven by renewable integration and electrification of transport, continues to amplify demand for analytics solutions capable of managing multivariable operational challenges in real time.

Analysis by Deployment:

- Cloud-based

- On-premises

Cloud-based leads the market with a share of 60%. Cloud-based platforms have captured market leadership by delivering the scalability, flexibility, and continuous feature availability that modern utility operations require. These platforms enable utilities to store and process immense volumes of smart meter, sensor, and operational technology data through elastic cloud infrastructure, eliminating the need for substantial capital investment in on-premises hardware. Vendor-managed security environments incorporating encryption, identity management, and regulatory-compliant architectures address historical concerns over critical data sovereignty, facilitating broader cloud adoption across regulated utility markets. Early adopters have demonstrated concrete operational benefits, including markedly shorter data batch-processing cycles and reduced total infrastructure expenditure, validating cloud migration as a sound financial and operational decision. The expansion of advanced metering infrastructure deployments, demand-side management programs, and distributed energy resource management systems is creating a sustained pipeline of cloud-first analytics implementations globally, reinforcing cloud-based platforms as the dominant deployment modality in the utility and energy analytics market forecast period.

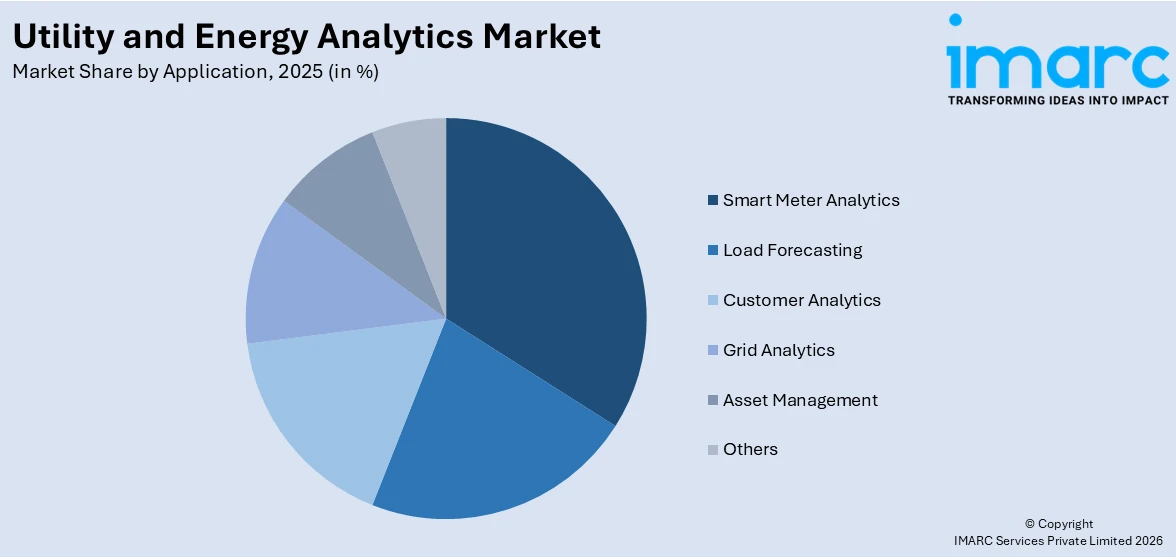

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Load Forecasting

- Customer Analytics

- Grid Analytics

- Asset Management

- Smart Meter Analytics

- Others

Smart meter analytics dominates the market, with a share of 33%. Smart meter analytics platforms provide utilities with the granular, real-time consumption data visibility that underpins virtually every aspect of modern grid management, from demand forecasting and dynamic pricing to outage detection and revenue protection. These platforms ingest high-frequency interval data generated by tens of millions of smart metering devices, applying machine learning algorithms to identify usage anomalies, detect theft, segment customers by consumption behavior, and optimize billing accuracy. The intelligence derived from smart meter datasets directly informs demand-response program design, enabling utilities to reduce peak load efficiently while enhancing customer engagement through personalized energy management insights. In 2024, Xcel Energy achieved a significant milestone by deploying 2 million Itron smart meters under its Integrated Advanced Metering Infrastructure 2.0 initiative, which aims to install a total of 3 million smart meters, demonstrating the scale of AMI investments driving analytics demand.

Analysis by Vertical:

- Oil and Gas

- Renewable Energy

- Nuclear Power

- Electricity

- Water

- Others

Oil and gas represents the leading segment, with a market share of 29%. The oil and gas sector's inherently data-intensive operational environment, encompassing upstream exploration and drilling, midstream transportation and storage, and downstream processing and distribution, creates compelling and sustained demand for advanced analytics platforms. Operators deploy analytics solutions to process data from thousands of sensors distributed across wellheads, pipelines, compressor stations, and refineries, enabling predictive maintenance that preempts costly equipment failures and reduces unplanned production downtime. Cloud-based cognitive exploration and production platforms leverage integrated analytics to enhance seismic interpretation, reservoir characterization, and well placement decision-making, improving capital deployment efficiency across development programs. Real-time pipeline integrity monitoring applications utilize anomaly detection algorithms to identify pressure deviations and potential leakage events, strengthening operational safety and regulatory compliance. The integration of AI-powered analytics into hydrocarbon production optimization workflows continues to deliver measurable efficiency gains, sustaining the oil and gas vertical's dominant position within the utility and energy analytics market segmentation.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 40% of the share, enjoys the leading position in the market. The region's dominance is anchored by the United States' advanced digital energy ecosystem, which features extensive smart meter penetration, sophisticated grid automation infrastructure, and a highly active community of technology innovators developing next-generation analytics solutions. Proactive regulatory frameworks at both federal and state levels have created structured demand for analytics capabilities across grid modernization, renewable integration, and energy efficiency program administration. Canada contributes meaningfully through sustained utility investment in smart grid upgrades and provincial carbon reduction commitments that require sophisticated energy monitoring and reporting systems. The region's concentration of leading analytics technology vendors, including global enterprise software providers and specialized energy technology firms, creates a highly competitive and innovative ecosystem that continuously accelerates solution sophistication, reinforcing North America's commanding position within the global utility and energy analytics market.

Key Regional Takeaways:

United States Utility and Energy Analytics Market Analysis

The United States market is characterized by one of the world's most mature and technologically advanced utility analytics ecosystems, shaped by decades of progressive grid digitalization investment and a highly competitive vendor landscape. Federal initiatives including the Grid Resilience and Innovation Partnerships program have directed billions of dollars toward advanced metering infrastructure, distribution automation, and analytics platform integration, creating structured demand across utility segments of all sizes. The country's investor-owned utilities, electric cooperatives, and municipal power providers are all progressively transitioning from reactive to predictive operational models, embedding analytics capabilities across asset management, demand response, and customer engagement functions. The integration of distributed energy resources including rooftop solar, battery storage, and electric vehicle (EV) charging is escalating grid operational complexity, compelling utilities to invest in real-time analytics that manage bidirectional energy flows and demand-side flexibility programs. In 2025, Itron, Inc., which is creating innovative methods for cities and utilities to handle energy and water, published its 2025 Resourcefulness Report, Grid Edge Intelligence: Five Ways Energy Utilities Can Implement AI Now. This year’s survey of 500 electric utility executives throughout the U.S. and Canada revealed that North American utilities are embracing data analytics, artificial intelligence (AI), and grid-edge intelligence much more rapidly than expected.

Europe Utility and Energy Analytics Market Analysis

Europe represents a highly significant and fast-evolving region within the global utility and energy analytics market, propelled by ambitious decarbonization commitments, comprehensive regulatory frameworks, and substantial public investment in grid digitalization. The European Union's mandate requiring 80% of electricity consumers to be equipped with smart meters by 2025 under the Energy Efficiency Directive has generated an enormous pipeline of metering data requiring advanced analytics infrastructure for processing and interpretation. The Horizon Europe program dedicated EUR 95.5 billion for the period 2021-2027. It tackles climate change, helps to achieve the UN’s Sustainable Development Goals and boosts the EU’s competitiveness and growth. The Nordic and DACH sub-regions are leading adoption of real-time energy analytics platforms for district heating automation, grid balancing, and dynamic pricing implementation, supported by sophisticated renewable energy ecosystems that require precise forecasting capabilities. The European Green Deal's ambition of climate neutrality by 2050 is accelerating utility investment in analytics-driven demand-side management and carbon footprint monitoring tools. Germany, France, and the United Kingdom serve as primary innovation hubs, hosting major analytics technology providers and utility pilot programs that influence pan-European adoption patterns.

Asia-Pacific Utility and Energy Analytics Market Analysis

Asia-Pacific is emerging as the most dynamically growing region in the global utility and energy analytics market, driven by unprecedented smart meter deployments, rapid urbanization, and assertive government-led energy digitalization programs. China has installed more than 500 million smart electricity meters, representing the world's single largest smart metering deployment and generating data volumes that are driving substantial investment in advanced analytics processing infrastructure. India has 3.90 Cr smart meter installations under its Revamped Distribution Sector Scheme. Japan and South Korea are advancing next-generation smart grid analytics integrating AI, blockchain, and edge computing to optimize complex urban energy networks. Australia is forecasting a major portion of its energy analytics deployments to be cloud-based by 2025, aligned with renewable energy integration mandates and grid resilience objectives. The region's exceptional growth trajectory is expected to continue accelerating, establishing Asia-Pacific as the fastest-growing market globally.

Latin America Utility and Energy Analytics Market Analysis

Latin America presents a growing and increasingly strategic market for utility and energy analytics solutions, driven by mounting pressures to address energy theft, aging distribution infrastructure, and the rising integration of renewable energy across the region. Mexico's expanding natural gas and electricity grid infrastructure is generating demand for analytics platforms supporting pipeline monitoring, grid management, and demand forecasting. The gradual rollout of smart metering programs across Colombia, Chile, and Argentina is creating foundational data infrastructure that is expected to catalyze analytics platform adoption over the coming years. Growing international utility sector investment in the region is further accelerating the deployment of energy management and analytics solutions.

Middle East and Africa Utility and Energy Analytics Market Analysis

The Middle East and Africa region is witnessing an accelerating adoption of utility and energy analytics solutions, underpinned by ambitious government-led grid modernization programs, large-scale renewable energy project development, and growing recognition of analytics as essential infrastructure for sustainable energy management. Saudi Arabia's Saudi Electricity Company has installed over 10 million smart meters as part of a comprehensive grid modernization program, establishing a foundational data infrastructure that is driving demand for advanced analytics platforms capable of processing high-frequency consumption data. The UAE and Qatar are leveraging analytics solutions to optimize water and electricity distribution networks as part of broader smart city development initiatives.

Competitive Landscape:

The global utility and energy analytics market is characterized by intense competitive dynamics, with established enterprise technology providers competing alongside specialized energy analytics firms and emerging AI-native startups to capture share in a rapidly expanding marketplace. Leading players are pursuing aggressive product development strategies, embedding advanced artificial intelligence and machine learning capabilities into their platforms to differentiate on analytical accuracy, predictive depth, and real-time decision-support functionality. Strategic partnerships and acquisitions are reshaping the competitive landscape as vendors seek to expand their functional footprints across the analytics value chain, from smart meter data management and grid optimization to customer engagement and regulatory compliance reporting. Cloud platform providers are deepening their energy sector specialization through industry-specific AI services and grid-native analytics templates, competing directly with established operational technology vendors that are simultaneously enhancing their own analytics portfolio breadth. Investment in cybersecurity-integrated analytics capabilities is emerging as a key competitive differentiator as utilities elevate digital security requirements within procurement processes.

The report provides a comprehensive analysis of the competitive landscape in the utility and energy analytics market with detailed profiles of all major companies, including:

- ABB Ltd.

- BuildingIQ Inc.

- Capgemini SE

- International Business Machines Corporation

- Oracle Corporation

- SAP SE

- SAS Institute Inc.

- Schneider Electric SE

- Siemens AG

- Salesforce.com Inc.

- Teradata Corporation

- TIBCO Software Inc.

Latest News and Developments:

- January 2026: Amperon, a prominent supplier of AI-driven energy forecasting and analytics services, has announced an investment from Samsung Venture Investment Corporation ("Samsung Ventures"), the corporate venture division of Samsung Group. This fresh support demonstrates ongoing investor trust in Amperon's technology and vision and will aid the company's international expansion and advanced product development in vital energy markets.

Utility and Energy Analytics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Solutions, Services |

| Deployments Covered | Cloud-based, On-premises |

| Applications Covered | Load Forecasting, Customer Analytics, Grid Analytics, Asset Management, Smart Meter Analytics, Others |

| Verticals Covered | Oil and Gas, Renewable Energy, Nuclear Power, Electricity, Water, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ABB Ltd., BuildingIQ Inc., Capgemini SE, International Business Machines Corporation, Oracle Corporation, SAP SE, SAS Institute Inc., Schneider Electric SE, Siemens AG, Salesforce.com Inc., Teradata Corporation, TIBCO Software Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the utility and energy analytics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global utility and energy analytics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the utility and energy analytics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Utility and Energy Analytics Market Report

The utility and energy analytics market was valued at USD 4.55 Billion in 2025.

The utility and energy analytics market is projected to exhibit a CAGR of 14.49% during 2026-2034, reaching a value of USD 15.39 Billion by 2034.

The utility and energy analytics market is driven by accelerating smart grid deployments, widespread adoption of IoT-enabled metering infrastructure, growing integration of renewable energy requiring real-time analytics, and rising demand for predictive maintenance solutions. Stringent government mandates targeting carbon neutrality and substantial federal investments in grid modernization are further catalyzing the market growth globally.

North America currently dominates the utility and energy analytics market, accounting for a share of 40% in 2025. The region benefits from widespread smart meter penetration exceeding, robust federal grid modernization funding, and a dense ecosystem of leading analytics technology providers that collectively drive sophisticated data-driven energy management adoption.

Some of the major players in the utility and energy analytics market include ABB Ltd., BuildingIQ Inc., Capgemini SE, International Business Machines Corporation, Oracle Corporation, SAP SE, SAS Institute Inc., Schneider Electric SE, Siemens AG, Salesforce.com Inc., Teradata Corporation, TIBCO Software Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)