Vaccine Market Size, Share, Trends and Forecast by Technology, Patient Type, Indication, Route of Administration, Product Type, Treatment Type, End User, Distribution Channel, and Region, 2026-2034

Global Vaccine Market Size, Share, Trends & Forecast (2026-2034)

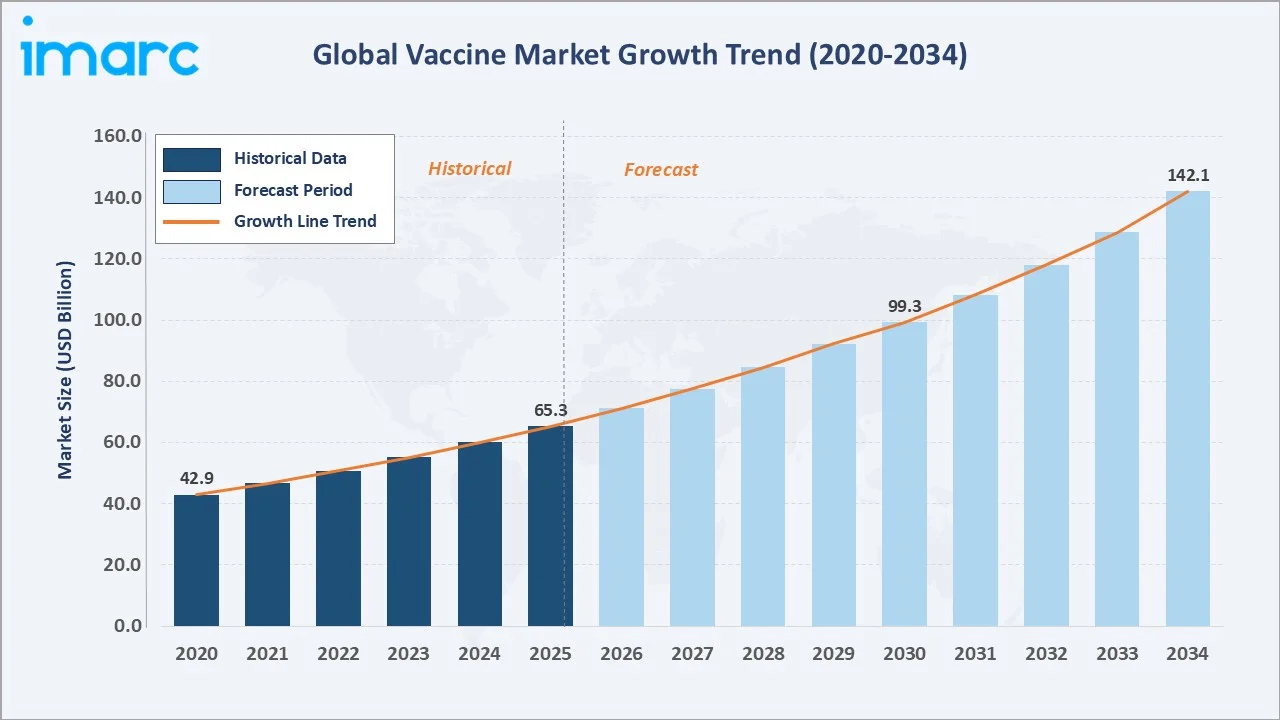

The global vaccine market size reached USD 65.3 Billion in 2025 and is projected to reach USD 142.1 Billion by 2034, exhibiting a CAGR of 8.75% during 2026-2034. Rising incidence of infectious diseases, government-led immunization programs, and rapid advances in mRNA and recombinant vaccine platforms are the primary forces driving vaccine market growth.

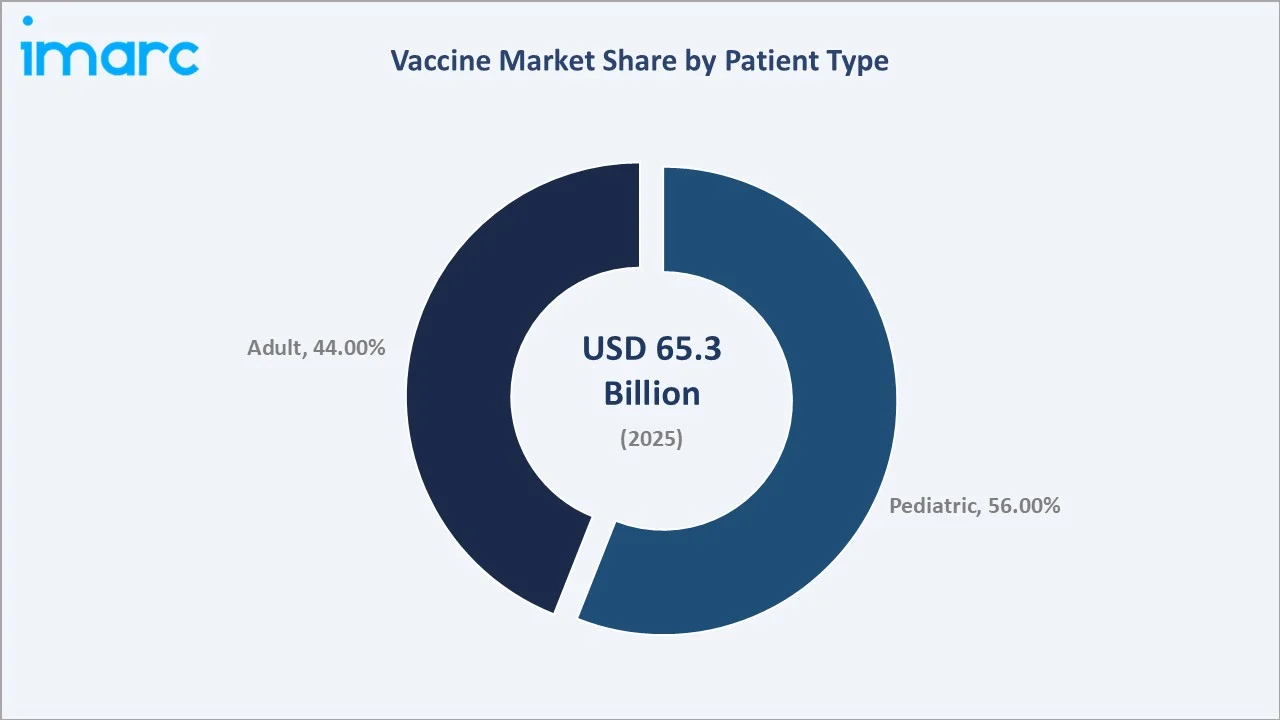

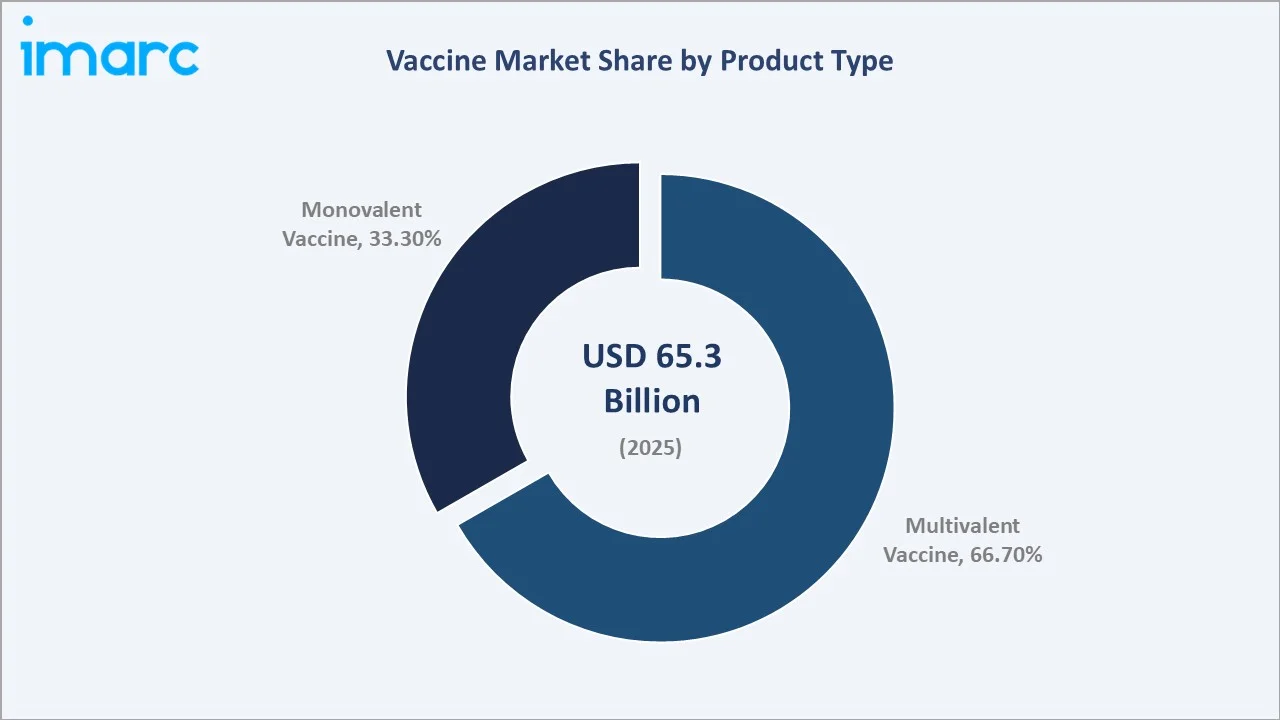

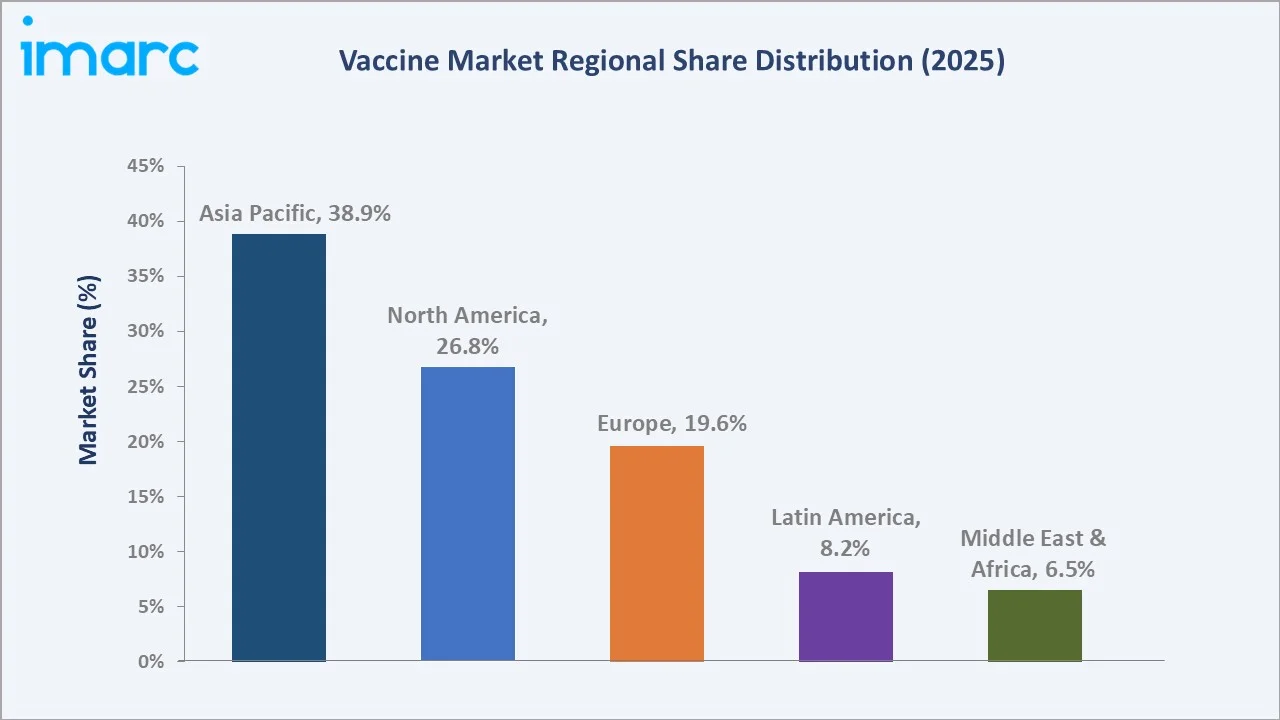

Paediatric vaccines dominate at 56.0% in 2025, while Multivalent Vaccines lead the product segment at 66.7%. Asia Pacific commands a dominant 38.9% regional share in 2025, reflecting large population bases and expanding public health investment.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 65.3 Billion |

|

Forecast Market Size (2034) |

USD 142.1 Billion |

|

CAGR (2026-2034) |

8.75% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (38.9% share, 2025) |

|

Second Region |

North America (26.8% share, 2025) |

|

Leading Patient Type |

Paediatric (56.0%, 2025) |

|

Leading Product Type |

Multivalent Vaccine (66.7%, 2025) |

The global vaccine market growth trajectory from 2020 through 2034, with the historical expansion to USD 65.3 Billion in 2025, reflects consistent immunization-driven demand, while the forecast to USD 142.1 Billion captures accelerating mRNA innovation, adult immunization programs, and Asia Pacific public health investment.

To get more information on this market, Request Sample

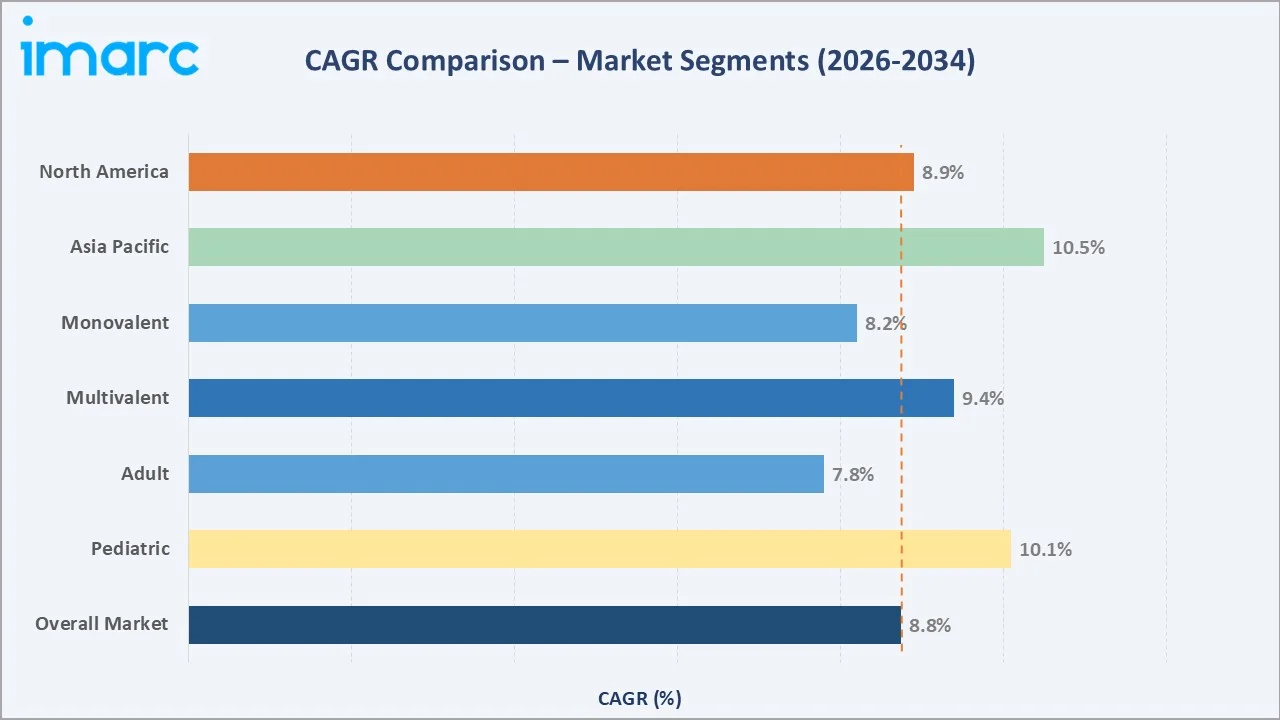

The CAGR trajectories across key patient type, product type, and regional sub-segments, with Paediatric vaccines at ~10.1% CAGR and Asia Pacific at ~10.5% CAGR, represent the fastest-growing categories within the global vaccine industry analysis through 2034.

Executive Summary

The global vaccine market is on a sustained growth trajectory from USD 65.3 Billion in 2025 to USD 142.1 Billion by 2034. Vaccines remain a cornerstone of global public health infrastructure, providing immunization against infectious diseases across all age groups and geographies, with demand driven by national immunization programs, pandemic preparedness, and adult immunization expansion.

Paediatric vaccines dominate patient type at 56.0% in 2025, underpinned by mandatory childhood immunization schedules across all WHO member states and the continuous expansion of national immunization programs in Asia, Africa, and Latin America. Adult immunization (44.0%) is the fastest-growing segment, driven by RSV, shingles, and COVID-19 booster demand.

Multivalent vaccines lead product type at 66.7% in 2025, reflecting the clinical and commercial preference for combination products that reduce injection burden, improve compliance, and simplify national immunization schedules. Monovalent vaccines (33.3%) retain critical roles in specific disease prevention and outbreak response.

Asia Pacific dominates at 38.9% in 2025, reflecting China and India's combined population of 2.8 billion and robust government immunization programs. North America (26.8%) and Europe (19.6%) follow, driven by advanced vaccine technology adoption and high per-dose pricing.

Key Market Insights

|

Insight |

Data |

|

Leading Patient Type |

Paediatric - 56.0% share (2025) |

|

Leading Product Type |

Multivalent Vaccine - 66.7% share (2025) |

|

Leading Region |

Asia Pacific - 38.9% revenue share (2025) |

|

Second Region |

North America - 26.8% revenue share (2025) |

|

Top Companies |

Pfizer, GSK, Sanofi, Merck & Co., Moderna, AstraZeneca, Bharat Biotech, Serum Institute of India, Johnson & Johnson, Novavax |

Key Analytical Observations Expanding On The Above Data:

- Paediatric dominance (56.0%): Paediatric vaccines, with 56.0% in 2025, dominate because mandatory childhood immunization schedules ensure non-discretionary, government-procured demand. GAVI Alliance procurement guarantees market access across 57 low-income countries, driving high-volume paediatric vaccine purchasing.

- Multivalent product leadership (66.7%): Multivalent vaccines, with 66.7% in 2025, lead because they reduce healthcare system costs by combining multiple antigens in single products. DTP-HepB-Hib pentavalent vaccines, for example, replace five separate injections with one, dramatically improving schedule compliance and cold-chain efficiency.

- Asia Pacific dominance (38.9%): Asia Pacific's 38.9% dominance in 2025 reflects the largest global population concentration, with India's Universal Immunization Programme covering 26 million infants annually and China's National Immunization Program providing 14 free vaccines under its public health mandate.

- North America premium pricing (26.8%): North America's 26.8% share reflects the highest per-dose vaccine pricing globally, with Prevnar 20 at around USD 280/dose and Shingrix at around USD 260/dose driving premium revenue despite lower unit volumes than emerging market programs.

Global Vaccine Market Overview

The vaccine is a biological preparation that provides active acquired immunity to a particular infectious disease. Vaccines contain an agent resembling a disease-causing microorganism and are made from weakened or killed forms of the microbe, its toxins, or one of its surface proteins, stimulating the immune system to recognize the agent as a threat and respond to future encounters.

The global vaccine ecosystem integrates vaccine antigen manufacturers, adjuvant and excipient suppliers, contract development and manufacturing organizations (CDMOs), regulatory authorities, national immunization program managers, cold-chain logistics providers, global health financing bodies (GAVI, CEPI), and end-use healthcare facilities spanning hospitals, clinics, pharmacies, and public health centers.

Market Dynamics

To evaluate market opportunities, Request Sample

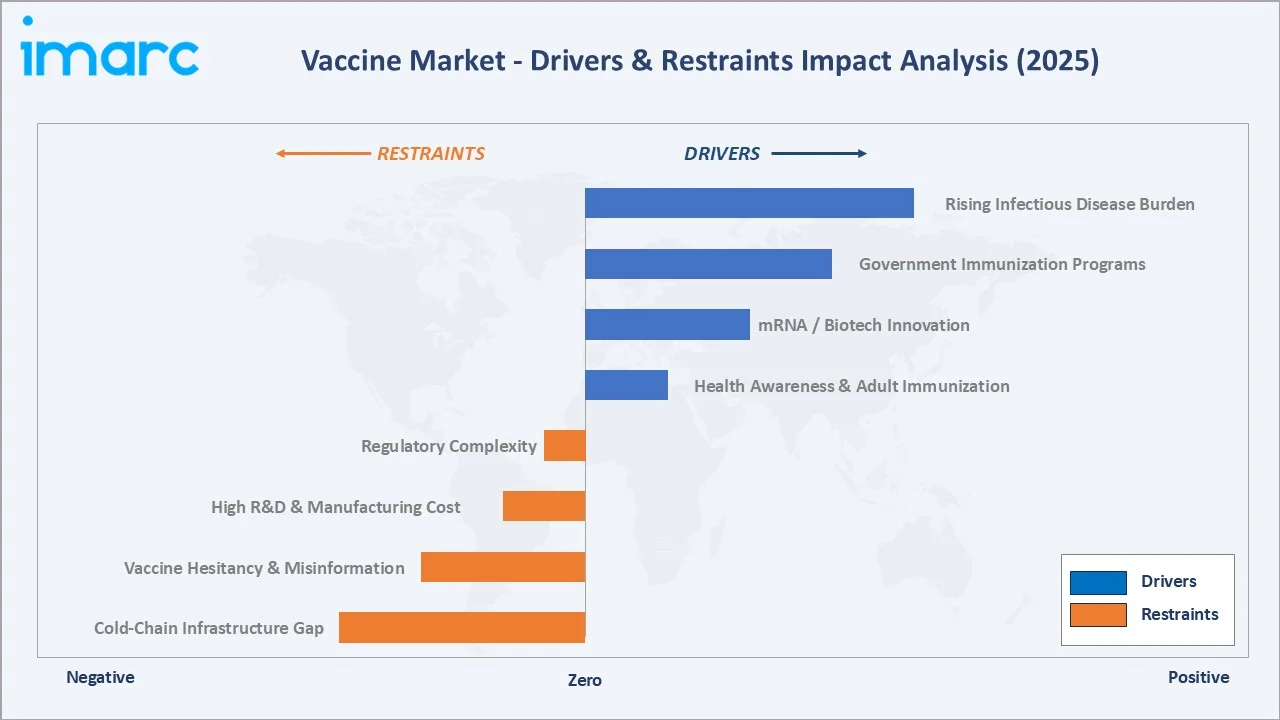

Market Drivers

- Rising Infectious Disease Burden: The COVID-19 pandemic underscored the critical importance of sustained investment in vaccine preparedness, prompting governments and global health organizations to significantly scale up funding for pandemic vaccine development, stockpiling, and R&D infrastructure worldwide.

- Government Immunization Programs: WHO's Immunization Agenda 2030 targets 90% national immunization coverage across all member states by 2030, committing governments to sustained vaccine procurement investment. GAVI's 2021-2025 strategy commits USD 15.6 Billion to vaccine access in 57 low-income countries.

- mRNA Platform Innovation: Moderna and BioNTech's mRNA platform success in COVID-19 opened application to influenza, RSV, cancer, and HIV vaccine development.

Market Restraints

- Cold-Chain Infrastructure Gaps: Inadequate cold-chain infrastructure across low- and middle-income countries remains a significant barrier to vaccine access, as temperature-sensitive vaccines require uninterrupted refrigeration from manufacture to administration, a requirement that many healthcare facilities in remote and resource-limited settings are unable to consistently meet.

- Vaccine Hesitancy and Misinformation: Measles cases tripled in Europe between 2023 and 2025 after MMR uptake fell below the 95% herd-immunity threshold. Declining immunization confidence and the spread of misinformation continue to suppress vaccination rates, limiting demand growth and slowing the adoption of new vaccines in key markets. At the same time, heightened regulatory scrutiny and safety concerns around approvals increase development timelines and costs, further constraining market expansion.

Market Opportunities

- Therapeutic and Personalized Cancer Vaccines: mRNA cancer vaccine platforms from Moderna/Merck (mRNA-4157) and BioNTech demonstrated 44% reduction in melanoma recurrence in Phase 2 trials, opening a significant personalized cancer vaccine opportunity by 2034 that extends vaccine market beyond traditional infectious disease prevention.

- Adult Immunization Expansion in High-Income Markets: Less than 50% of US adults aged 65+ receive annual flu vaccination , representing a substantial addressable market. Medicare's coverage of RSV vaccines for adults 60+ creates new reimbursement pathways for adult immunization revenue growth.

Market Challenges

- CDMO Concentration and Supply Chain Fragility: The global vaccine supply chain is exposed to concentration risk, as a limited number of contract development and manufacturing organizations control a significant share of aseptic fill-finish capacity worldwide. Regulatory non-compliance events or facility disruptions at any major CDMO can cascade into significant delivery delays, underscoring the need for diversified manufacturing partnerships across the vaccine industry.

- Regulatory Complexity and Approval Timeline Variability: Vaccine regulatory pathways vary substantially across FDA, EMA, and WHO prequalification frameworks, with multi-region approval processes adding 12-24 months to global commercial launches and requiring duplicate clinical data submissions for major market access.

Emerging Market Trends

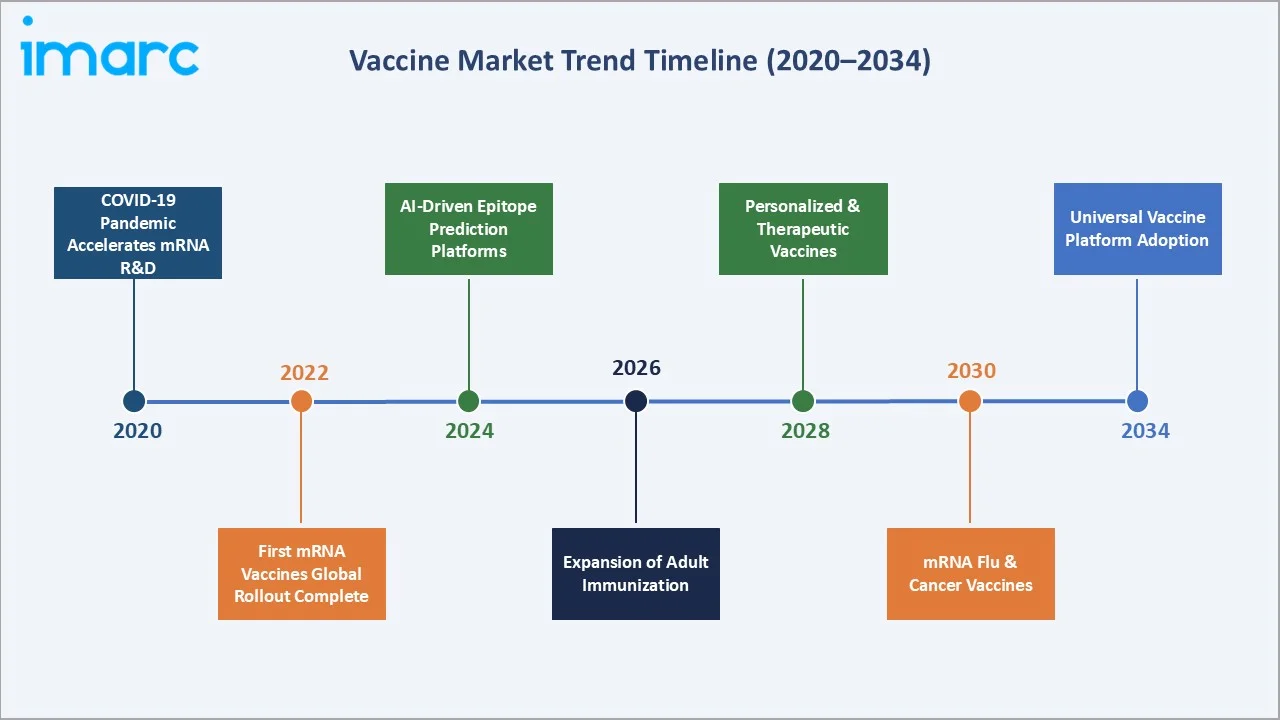

1. mRNA Platform Expansion Beyond COVID-19

Moderna's mRNA platform is being recycled across influenza, RSV, CMV, HIV, and cancer indications, leveraging the same lipid nanoparticle delivery technology that enabled its 18-month COVID-19 vaccine development. Moderna's February 2025 partnership with OpenAI applies large language models to epitope prediction, compressing pre-clinical timelines significantly.

2. AI-Accelerated Vaccine Discovery

GSK's AI-curated TLR7/8 adjuvant boosted antibody titers in elderly volunteers by 60% compared with standard alum adjuvants in trials published in 2025. A Nipah vaccine entered Phase I trials nine months after WHO flagged the outbreak, demonstrating AI-accelerated responsiveness to emerging infectious disease threats.

3. Needle-Free and Cold-Chain-Independent Delivery

Vaxxas advanced its high-density micro-array patch to Phase III in August 2025. The technology delivers antigens through 5,000 dissolving projections, eliminating cold-chain and skilled-personnel barriers while reducing last-mile cost by an estimated 40% in tropical climates, transforming reach in low-income markets.

4. Combination Vaccine Portfolio Expansion

Pfizer and Mitsubishi Tanabe Pharma launched GOBIK in Japan in March 2024, a six-in-one combination vaccine replacing multiple individual injections. Pipeline data show 15+ next-generation combination vaccines in Phase 2-3, reflecting the industry's strategic prioritization of schedule simplification and immunization compliance improvement.

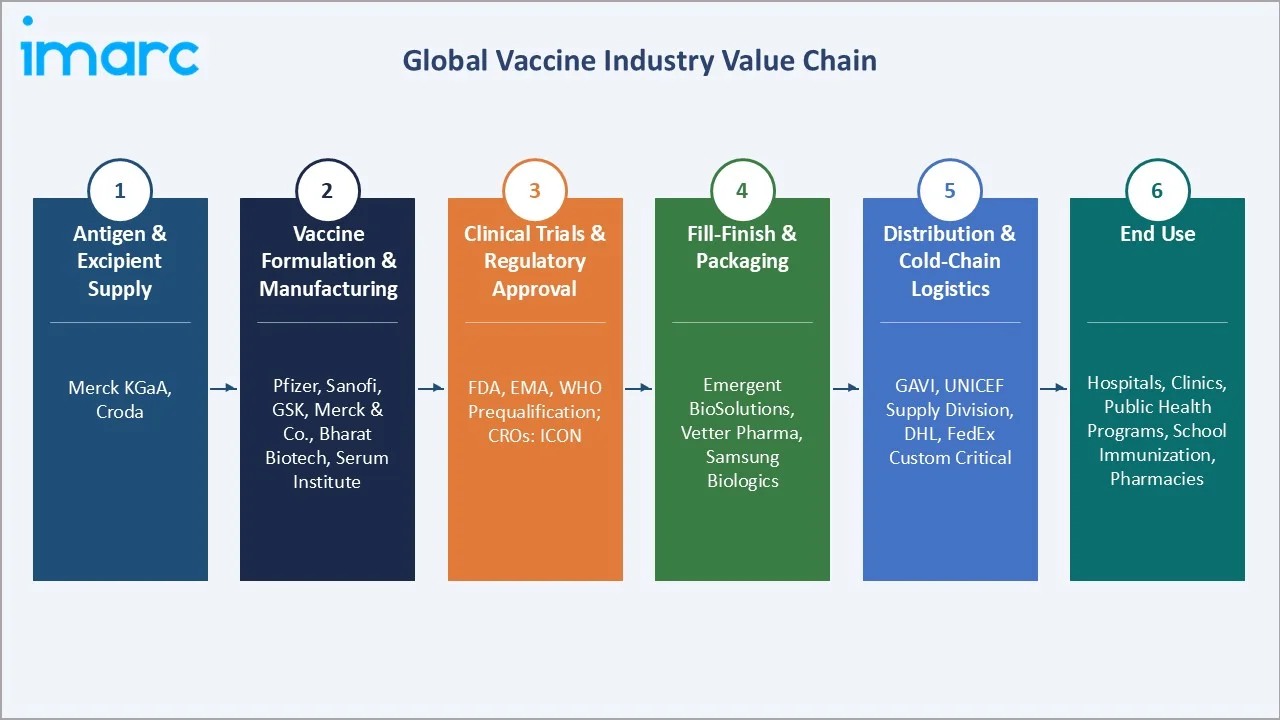

Industry Value Chain Analysis

The vaccine value chain spans six stages from antigen sourcing through immunization delivery. Fill-finish manufacturing and regulatory approval capture the highest risk-adjusted margin points, while cold-chain distribution and last-mile delivery generate the most significant access barriers in low-income markets.

|

Stage |

Key Players / Examples |

|

Antigen & Excipient Supply |

Merck KGaA, Croda |

|

Vaccine Formulation & Manufacturing |

Pfizer, Sanofi, GSK, Merck & Co., Bharat Biotech, Serum Institute |

|

Clinical Trials & Regulatory Approval |

FDA, EMA, WHO Prequalification; CROs: ICON |

|

Fill-Finish & Packaging |

Emergent BioSolutions, Vetter Pharma, Samsung Biologics |

|

Distribution & Cold-Chain Logistics |

GAVI, UNICEF Supply Division, DHL, FedEx Custom Critical |

|

End Use |

Hospitals, Clinics, Public Health Programs, School Immunization, Pharmacies |

Integrated manufacturers with captive fill-finish capabilities, such as Pfizer's USD 450 Million Kalamazoo mRNA capacity expansion, achieve lower per-dose production costs than processors relying entirely on CDMO fill-finish, providing a meaningful competitive cost advantage in government tender negotiations.

Technology Landscape in the Vaccine Industry

mRNA and Lipid Nanoparticle Delivery Technology

mRNA vaccine technology encodes the antigen of interest in messenger RNA, which is delivered intracellularly via lipid nanoparticle carriers that protect the mRNA from degradation and facilitate cellular uptake. The platform allows antigen redesign within weeks of pathogen identification, enabling rapid pandemic response with no live pathogen handling requirements.

Recombinant and Subunit Vaccine Platforms

Recombinant vaccine platforms express specific pathogen antigens in cell culture systems, yielding highly purified subunit vaccines without live pathogen risk. GSK's AS01B adjuvant system, used in Shingrix, amplifies immune response to recombinant antigens, achieving 97% efficacy against shingles and demonstrating adjuvant technology's central role in next-generation vaccine design.

Thermostable Formulation Technology: Next-generation thermostable vaccine formulations using lyophilization and novel excipient systems are extending shelf life at ambient temperatures, reducing cold-chain dependency. PATH and USAID-funded programs targeting 37°C stability for 12+ months are a priority for expanding immunization reach in resource-limited settings.

Digital Health and Immunization Tracking Platforms

WHO's SMART Immunization guidelines promote digital immunization registries integrating with national health information systems. QR-code-based vaccination records, piloted in India's CoWIN platform covering 2 billion vaccine doses, are being adopted as global models for immunization tracking, adverse event surveillance, and coverage monitoring.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Technology | 🔒 | 🔒 | 2025 |

| Patient Type | Paediatric | 56.0% | 2025 |

| Indication | Bacterial Diseases | 🔒 | 2025 |

| Administration | Intramuscular and Subcutaneous Administration | 🔒 | 2025 |

| Product Type | Multivalent Vaccine | 66.7% | 2025 |

| Treatment Type | Preventive Vaccine | 56.2% | 2025 |

| End User | Hospitals | 57.3% | 2025 |

| Distribution Channel | Hospital Pharmacies | 🔒 | 2025 |

| Region | Asia Pacific | 38.9% | 2025 |

By Patient Type

Paediatric vaccines command a 56.0% majority share in 2025, underpinned by universal childhood immunization mandates across WHO member states, GAVI-funded procurement programs in 57 low-income countries, and the biological imperative of early childhood immunization to prevent disease mortality in the most vulnerable population segment.

To access detailed market analysis, Request Sample

Adult vaccines at 44.0% in 2025 represent the fastest-growing patient segment, driven by RSV vaccines for adults 60+ (Pfizer's Abrysvo, GSK's Arexvy), shingles vaccination in adults 50+ (Shingrix), and COVID-19 booster programs that have normalized adult immunization as an annual preventive health behavior in high-income markets.

By Product Type

Multivalent vaccines dominate at 66.7% in 2025, representing the strategic preference of national immunization programs for combination products that simplify schedules and improve coverage rates. Pentavalent (DTP-HepB-Hib), hexavalent, and MMR-V combinations each eliminate multiple injections, reducing immunization visits and improving compliance across all healthcare settings.

Monovalent vaccines at 33.3% retain essential roles in outbreak response, specific high-risk population targeting, and diseases where combination formulation is clinically impractical. HPV monovalent vaccines (Gardasil 9), rabies, yellow fever, and typhoid Vi polysaccharide vaccines represent high-value monovalent categories growing at premium pricing in emerging markets.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

38.9% |

India's Universal Immunization Programme; China NIP expansion; ASEAN health infrastructure investment |

|

North America |

26.8% |

Premium adult immunization pricing; mRNA technology leadership; Medicare RSV coverage expansion |

|

Europe |

19.6% |

EU Vaccination Roadmap; pandemic preparedness investment; adult immunization mandates in France, Italy |

|

Latin America |

8.2% |

Brazil NIP expansion; PAHO revolving fund procurement; Mexico infant immunization program scaling |

|

Middle East & Africa |

6.5% |

GAVI accelerated support; African Union Vaccine Manufacturing Partnership; GCC healthcare investment |

Asia Pacific's 38.9% market dominance in 2025 is driven by the world's two largest national immunization programs operating simultaneously. India's Universal Immunization Programme covers 26 million infants annually with 12 vaccines, while China's National Immunization Program mandates 14 free vaccines with near-universal coverage. The region's Serum Institute of India supplies 65% of GAVI-procured vaccines globally, combining manufacturing scale with price competitiveness.

North America, with 26.8% in 2025, benefits from the world's highest per-dose vaccine pricing, driven by premium adult immunization products. FDA-authorized RSV vaccines create substantial per-dose revenue concentration in US and Canadian markets that far exceeds volume share.

Competitive Landscape

The global vaccine market is moderately concentrated, with the top five players (Pfizer, GSK, Sanofi, Merck, and Moderna) collectively holding approximately 70-75% of total global market revenue. Asia Pacific's market is served by a mix of global multinationals and regional manufacturers including Serum Institute and Bharat Biotech, while North American and European markets are dominated by the global innovators.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Pfizer Inc. |

Prevnar 20, Comirnaty (COVID), Abrysvo (RSV) |

Leader |

mRNA + pneumococcal; adult vaccines; global manufacturing |

|

GSK plc |

Shingrix, Arexvy (RSV), Bexsero |

Leader |

Adult immunization; adjuvant platform; shingles and meningococcal |

|

Sanofi |

Fluzone, Pentacel, Polio vaccines |

Leader |

Paediatric combination vaccines; influenza; global NIP supply |

|

Merck & Co. Inc. |

Gardasil 9, M-M-R II, RotaTeq, Vaqta |

Leader |

HPV and MMR leadership; new USD 1B Durham facility (2025) |

|

Moderna Inc. |

Spikevax (COVID), MRESVIA, mRNA flu pipeline |

Challenger |

mRNA platform expansion; AI-driven antigen design; flu & cancer |

|

AstraZeneca plc |

Fluenz Tetra |

Specialist |

Needle-free influenza; mRNA/VLP pipeline in early development |

|

Serum Institute of India |

COVISHIELD, Covovax, Polio vaccines |

Leader (LMIC) |

World's largest volume producer; GAVI supply; price leadership |

|

Bharat Biotech International |

COVAXIN, Rotavac, Typbar TCV, Jenvac |

Emerging |

India domestic + export; indigenously developed platforms |

|

Novavax Inc. |

Nuvaxovid (COVID), CIC vaccine pipeline |

Emerging |

Protein subunit nanoparticle; protein-based alternative platforms |

The competitive positioning of key global vaccine market participants across global market presence and strategic investment dimensions in 2025. Key players include Pfizer Inc, GSK plc, Sanofi, Merck & Co. Inc., Moderna Inc., AstraZeneca plc, Serum Institute of India, Bharat Biotech International, and Novavax Inc.

Key Company Profiles

Pfizer Inc.

Pfizer is the one of the world's largest vaccine companies by revenue, combining its historical pneumococcal franchise (Prevnar) with COVID-19 vaccine leadership (Comirnaty) and RSV innovation (Abrysvo). It’s million-dollars Kalamazoo mRNA fill-finish expansion adds 200 million annual doses, securing production resilience across its growing mRNA pipeline.

- Product Portfolio: Prevnar 20 (pneumococcal), Comirnaty (COVID-19 mRNA), Abrysvo (RSV adult), Trumenba, pediatric combination vaccines.

- Recent Developments: In May 2023, Pfizer secured FDA approval for Abrysvo for adults 60+ years. Top line results for the Phase 3 VALOR - Vaccine Against Lyme for Outdoor Recreationists, demonstrating efficacy of 73.2% from 28 days post-dose 4 (March 2026).

- Strategic Focus: Pfizer's strategy leverages its vertically integrated mRNA capability to compete across pneumococcal, RSV, influenza, and cancer vaccine segments, expanding beyond COVID-19 into durable adult immunization revenue streams.

GSK plc

GSK is the world's leading adult immunization company, with Shingrix (shingles) and Arexvy (RSV) representing the two most commercially successful adult vaccine launches in history. GSK's proprietary AS01B adjuvant system is a durable competitive advantage enabling premium pricing across its shingles and malaria vaccine portfolios.

- Product Portfolio: Shingrix (shingles), Arexvy (RSV adult), Bexsero/Menveo (meningococcal), Infanrix Hexa (paediatric combination), Mosquirix (malaria).

- Recent Developments: In July 2024, GSK and CureVac restructured their mRNA collaboration, granting GSK full rights to develop and commercialize mRNA vaccines for influenza and COVID-19.

- Strategic Focus: GSK's strategy targets leadership in adult immunization, leveraging Shingrix and Arexvy as platform-building commercial successes to fund next-generation mRNA influenza and combination vaccine R&D through 2034.

Sanofi SA

Sanofi is the global leader in paediatric combination vaccines and influenza immunization, with its Pasteur division supplying governments across more than 100 countries. Its joint venture with AstraZeneca for nirsevimab (BEYFORTUS), an RSV monoclonal antibody for newborns, represents the landmark 2023 product launch in the RSV prevention market.

- Product Portfolio: Fluzone/Fluzone HD (influenza), Pentacel (paediatric 5-in-1), Polio-based combinations, and Verorab (rabies).

- Recent Developments: In April 2024, Sanofi launched Verorab in the UK for pre- and post-exposure rabies prophylaxis, extending its rabies vaccine global franchise beyond endemic markets.

- Strategic Focus: Sanofi focuses on maintaining national immunization program supply relationships globally for paediatric combinations, while expanding into premium adult segments via influenza high-dose and RSV through 2034.

Merck & Co. Inc.

Merck is the global leader in HPV prevention through Gardasil 9, which remains the only vaccine capable of preventing cervical cancer across nine HPV genotypes. Merck opened a new USD 1 Billion, 225,000 sq ft vaccine manufacturing facility in Durham, North Carolina in March 2025, substantially expanding its domestic production capacity.

- Product Portfolio: Gardasil 9 (HPV), M-M-R II (measles-mumps-rubella), RotaTeq (rotavirus), Vaqta (hepatitis A), Pneumovax 23 (pneumococcal 23-valent).

- Recent Developments: In March 2025, Merck opened its new USD 1 Billion Durham, NC vaccine manufacturing facility, strengthening US-domestic HPV and MMR vaccine production capacity.

- Strategic Focus: Merck's strategy centers on defending Gardasil 9's global HPV leadership through market expansion in Asia and Africa, while investing in next-generation RSV and pneumococcal pipeline candidates to address mature product LOE cycles.

Market Concentration Analysis

The global vaccine market is moderately concentrated at the global level, with no single company holding more than 20-25% of total global market revenue. The top five players (Pfizer, GSK, Sanofi, Merck, Moderna) collectively capture approximately 70-75% of revenue, reflecting both innovation leadership and manufacturing scale advantages.

Consolidation in the Asia Pacific market differs structurally from Western markets, as Serum Institute of India and Bharat Biotech hold disproportionate volume share in government tender procurement channels, supplying GAVI at USD 1-3/dose compared to multinational pricing of USD 20-200+/dose. This dual-market structure means global revenue concentration overstates innovation market concentration.

Investment & Growth Opportunities

Fastest-Growing Segments

Adult RSV vaccines at approximately 12% CAGR through 2034 represent the highest-growth product category, driven by Pfizer's Abrysvo and GSK's Arexvy expanding coverage across the 60+ population globally. mRNA influenza vaccines in Phase 3 development from Moderna and BioNTech represent the next major platform expansion opportunity.

Emerging Markets

Middle East & Africa at approximately 8.5% CAGR is the fastest-growing region for vaccines through 2034. The African Union's Vaccine Manufacturing Partnership targets producing 60% of Africa's vaccine needs on the continent by 2040, generating substantial greenfield manufacturing investment in South Africa, Egypt, Senegal, and Nigeria that will reshape regional supply chains.

Venture & Investment Trends

CEPI's USD 3.5 Billion 100-Days Mission commitment to compress pandemic vaccine development to 100 days from pathogen identification is driving substantial investment in AI-accelerated antigen design, platform-ready clinical trial infrastructure, and real-time genomic surveillance networks that reduce outbreak response timelines.

Future Market Outlook (2026-2034)

The global vaccine market is forecast to expand from USD 65.3 Billion in 2025 to USD 142.1 Billion by 2034, adding USD 76.8 Billion in incremental annual market value over the forecast period. This sustained, high-CAGR growth reflects the market's transition from communicable disease prevention toward therapeutic vaccine applications.

Three technological forces will most significantly shape the vaccine industry landscape through 2034. AI-driven universal flu vaccine candidates targeting conserved neuraminidase epitopes could eliminate annual reformulation requirements. Self-amplifying mRNA platforms requiring 10-100x lower antigen dose than conventional mRNA will transform manufacturing economics.

Research Methodology

Primary Research

Primary research encompassed structured interviews with vaccine industry stakeholders, including senior regulatory affairs professionals, national immunization program managers, EPC procurement specialists at UNICEF Supply Division and GAVI, cold-chain logistics managers, and clinical development leaders at major vaccine manufacturers. Primary data validated market sizing, patient type and product type segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include WHO Global Vaccine Action Plan progress reports, GAVI Alliance annual reports (2020-2025), CEPI portfolio updates, CDC immunization coverage data, EMA and FDA approval databases, IQVIA vaccine market data, PATH vaccine development roadmaps, and trade publications including Vaccine (Elsevier), Human Vaccines & Immunotherapeutics, and BioPharma Dive.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating disease incidence data, national immunization program coverage targets, per-dose pricing trends, pipeline conversion probability estimates, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative) was performed to account for macroeconomic and regulatory uncertainty.

Vaccine Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Conjugate Vaccines, Inactivated and Subunit Vaccines, Live Attenuated Vaccines, Recombinant Vaccines, Toxoid Vaccines, Others |

| Patient Types Covered | Pediatric, Adult |

| Indications Covered |

|

| Route of Administrations Covered | Intramuscular and Subcutaneous Administration, Oral Administration, Others |

| Product Types Covered | Multivalent Vaccine, Monovalent Vaccine |

| Treatment Types Covered | Preventive Vaccine, Therapeutic Vaccine |

| End Users Covered | Hospitals, Clinics, Vaccination Centers, Academic and Research Institutes, Others |

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies, Institutional Sales, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Turkey, GCC Countries, Israel |

| Companies Covered | Pfizer Inc., GSK plc, Sanofi, Merck & Co. Inc., Moderna Inc., AstraZeneca plc, Serum Institute of India, Bharat Biotech International, Novavax Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the vaccine market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global vaccine market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the vaccine industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Vaccine Market Report

The global vaccine market reached USD 65.3 Billion in 2025, reflecting sustained demand from government immunization programs, pandemic preparedness investment, and adult immunization expansion in high-income markets.

The market is projected to reach USD 142.1 Billion by 2034, growing at a CAGR of 8.75% during 2026-2034, driven by mRNA platform expansion, therapeutic vaccine emergence, and Asia Pacific immunization program scaling.

Paediatric vaccines lead with a 56.0% share in 2025, driven by mandatory childhood immunization schedules across all WHO member states and GAVI-funded procurement programs in 57 low-income countries.

Multivalent vaccines dominate at 66.7% in 2025, reflecting national immunization program preference for combination products that simplify schedules, reduce injection burden, and improve immunization compliance rates globally.

Asia Pacific commands a dominant 38.9% market share in 2025, driven by India's Universal Immunization Programme, China's National Immunization Program, and Serum Institute of India's position as the world's largest vaccine manufacturer by volume.

Adult RSV vaccines represent the fastest-growing product category, with mRNA-based influenza and therapeutic cancer vaccines in Phase 3 trials positioned to be the next major commercial launches by 2026-2028.

Leading companies include Pfizer Inc, GSK plc, Sanofi, Merck & Co. Inc., Moderna Inc., AstraZeneca plc, Serum Institute of India, Bharat Biotech International, and Novavax Inc.

Key applications include childhood routine immunization, adult immunization (shingles, RSV, flu, pneumococcal), travel vaccination, outbreak response (Ebola, cholera, meningitis), pandemic preparedness, and emerging therapeutic applications in cancer and chronic infectious diseases.

mRNA technology has transformed vaccine development speed and antigen flexibility, enabling 100-day pandemic response timelines, AI-assisted epitope design, and expansion into therapeutic cancer and HIV vaccine applications that extend the market far beyond traditional infectious disease prevention.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)