Water Purifier Market Size, Share, Trends and Forecast by Technology Type, Distribution Channel, End-User, and Region, 2026-2034

Global Water Purifier Market Size, Share, Trends & Forecast (2026-2034)

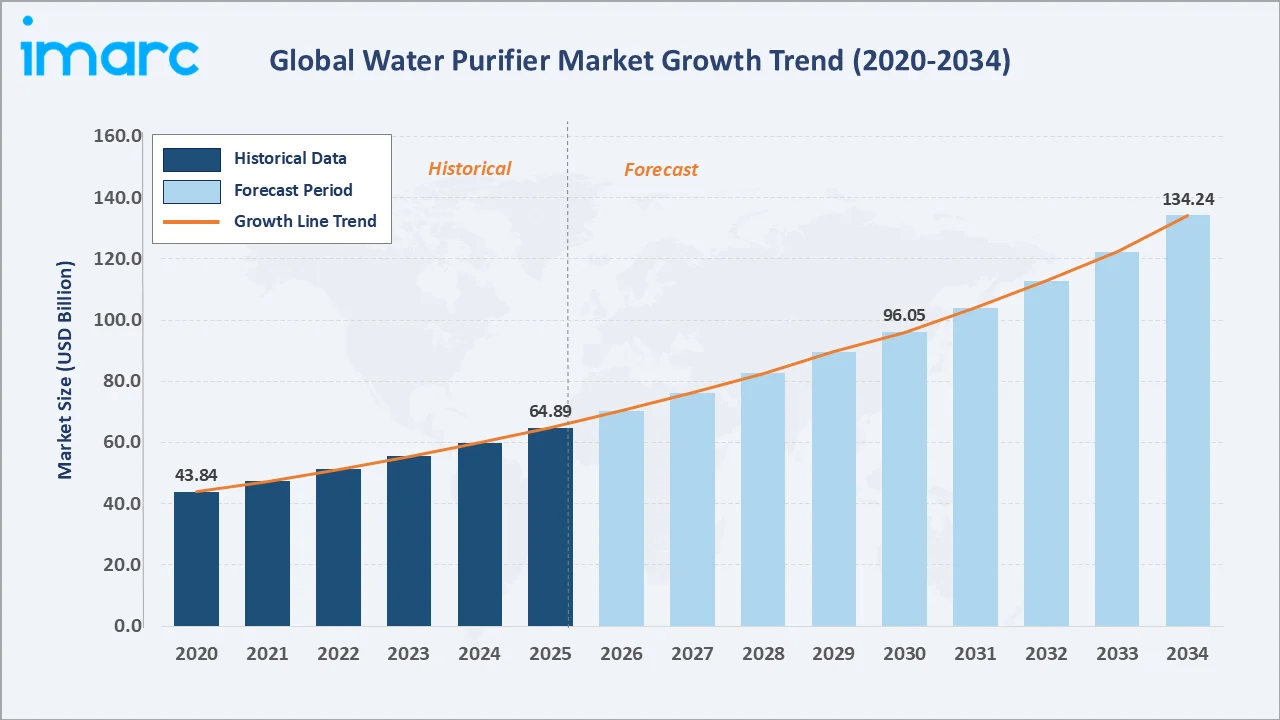

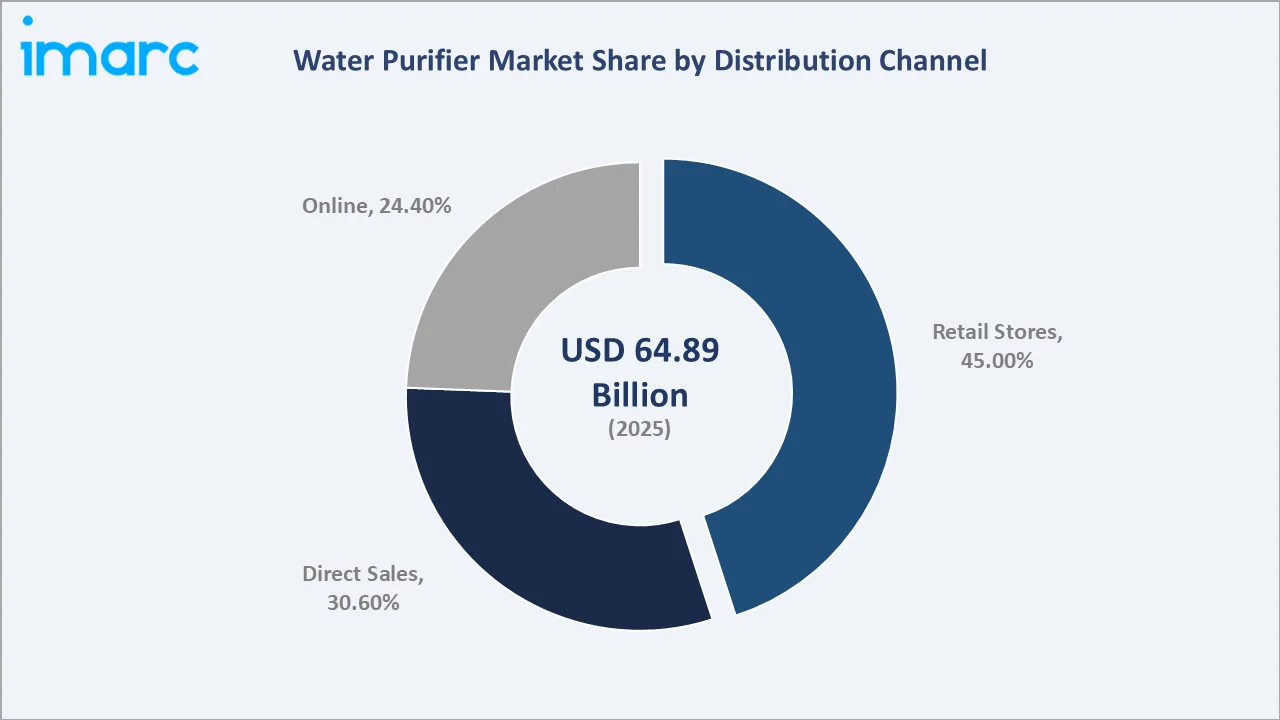

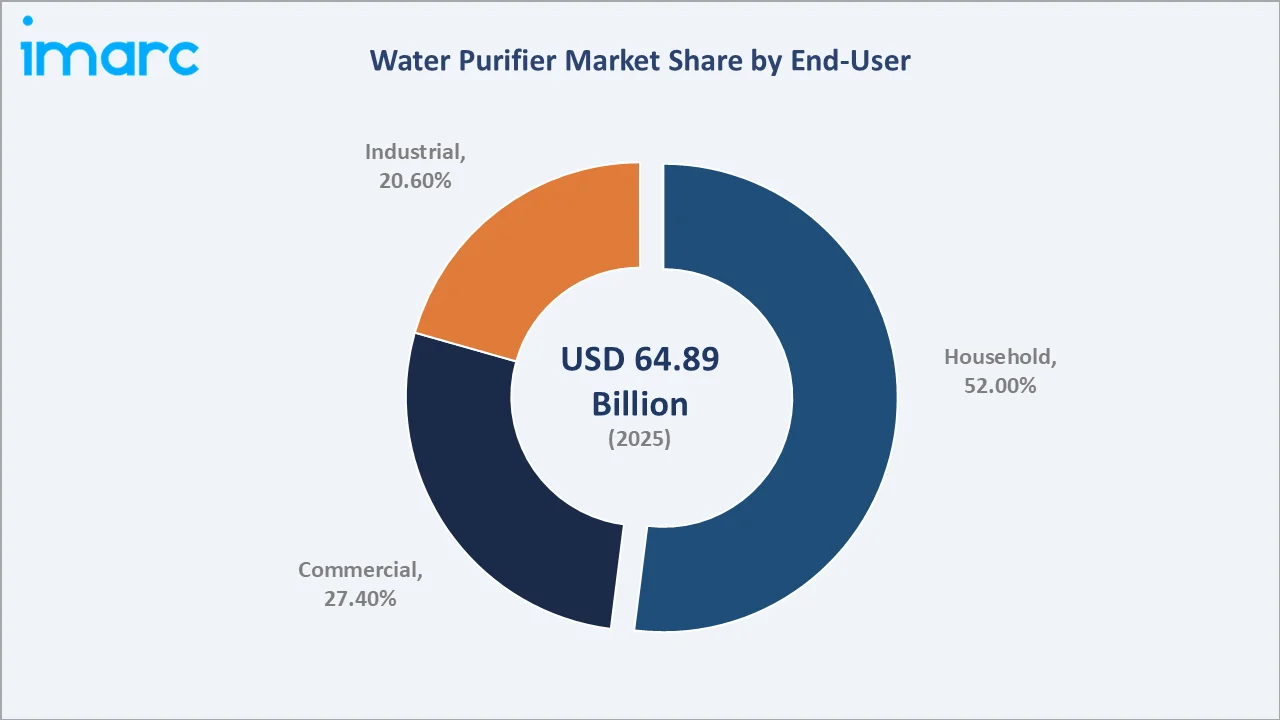

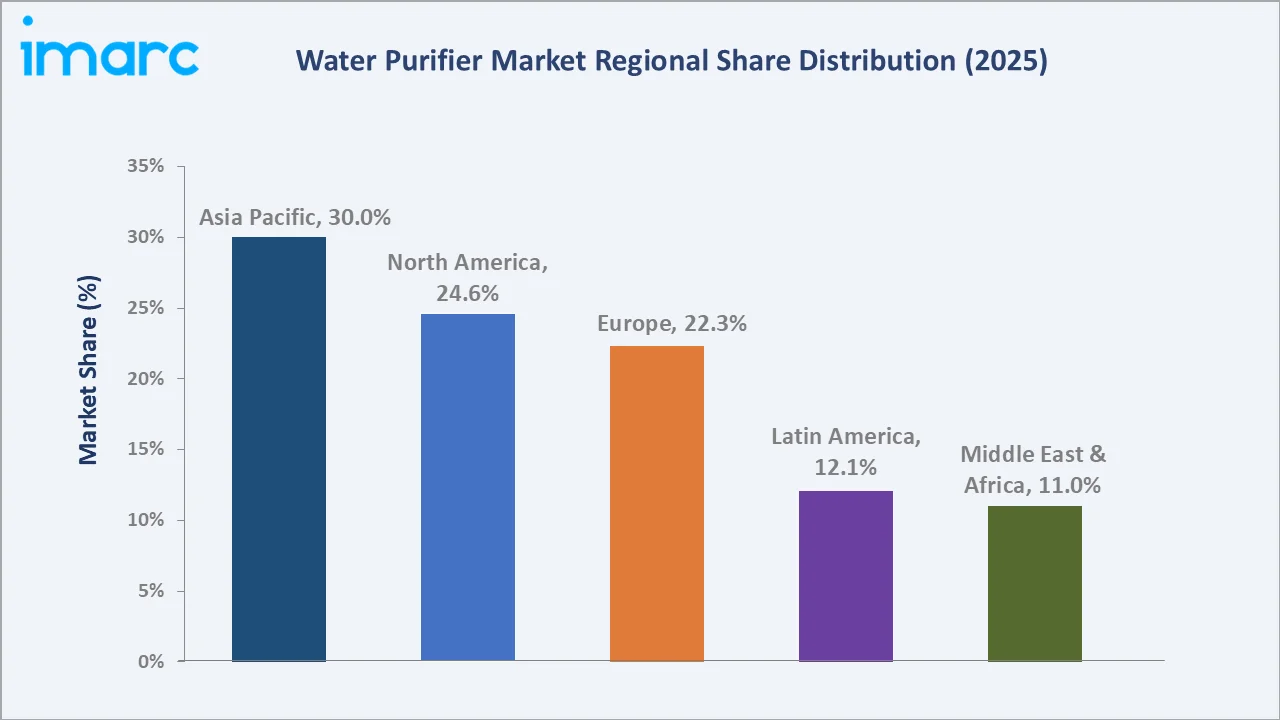

The global water purifier market size was valued at USD 64.9 Billion in 2025 and is projected to reach USD 134.2 Billion by 2034, exhibiting a CAGR of 8.16% during the forecast period 2026-2034. Rising incidence of waterborne diseases, rapid urbanization stressing aging municipal infrastructure, and a consumer shift away from single-use plastics are the primary water purifier market growth drivers. Retail stores dominate the distribution channel at 45.0% in 2025, while Household end-users represent the largest demand source at 52.0%. Asia Pacific leads the regional landscape with a 30.0% share in 2025, underpinned by large population bases, government-led safe-water programs, and accelerating health awareness across India, China, and Southeast Asia.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 64.9 Billion |

|

Forecast Market Size (2034) |

USD 134.2 Billion |

|

CAGR (2026-2034) |

8.16% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (30.0% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Distribution Channel |

Retail Stores (45.0%, 2025) |

|

Leading End-User Segment |

Household (52.0%, 2025) |

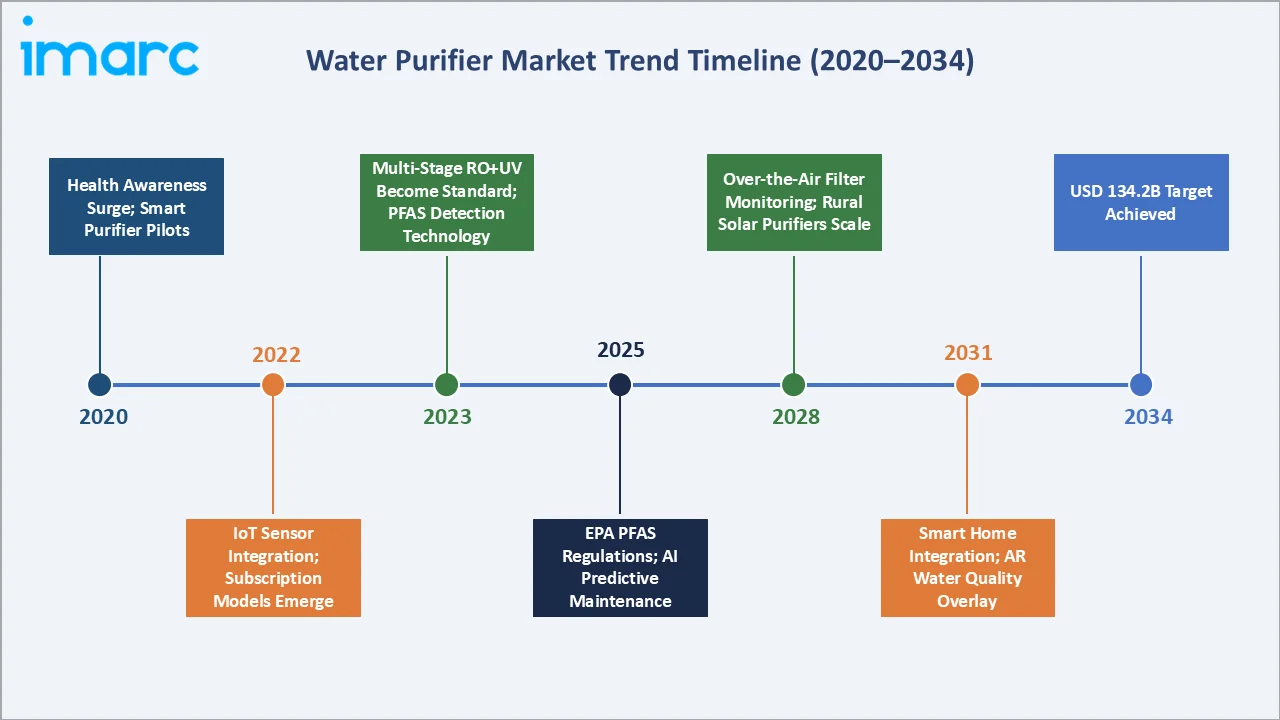

The chart illustrates global water purifier market growth from 2020–2034, showing steady historical expansion and sustained future growth driven by urbanization, contamination awareness, and regulatory adoption.

To get more information on this market, Request Sample

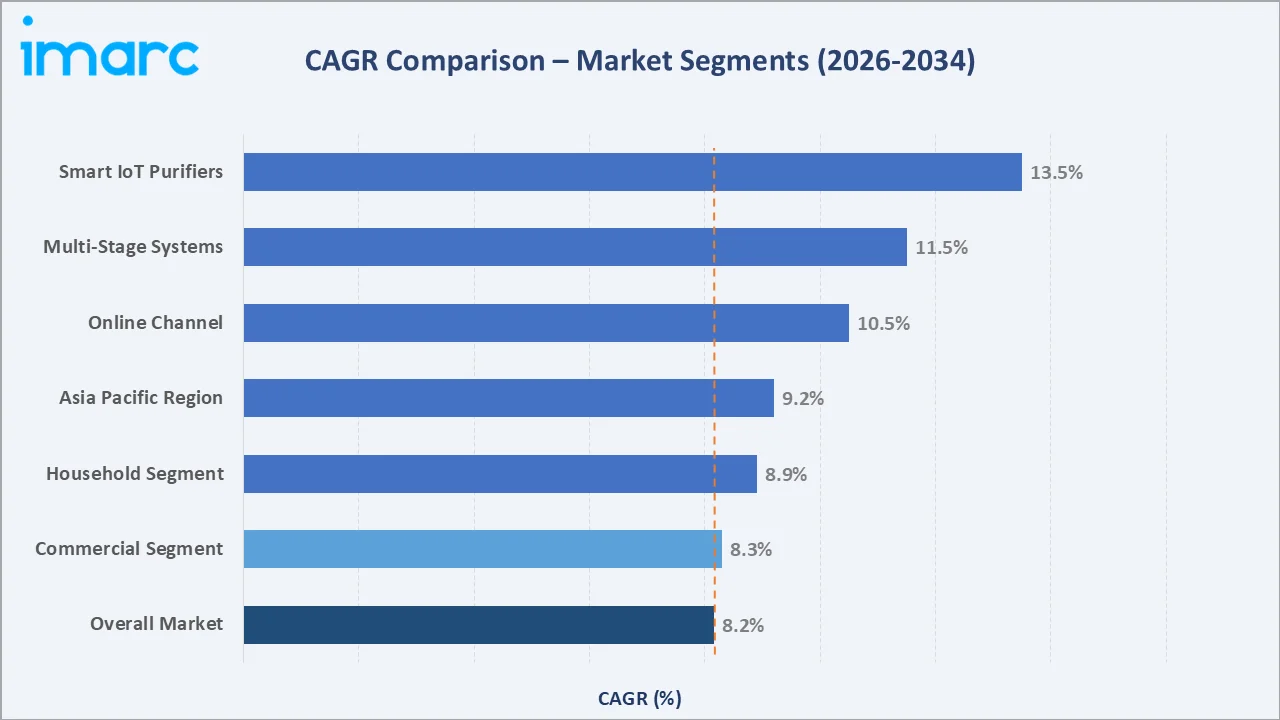

The CAGR comparison shows Smart IoT Purifiers and Multi-Stage Systems as the fastest-growing segments through 2034, surpassing the overall market CAGR of 8.16%.

Executive Summary

The global water purifier market is expanding rapidly due to rising water contamination, urbanization, and growing health awareness. Valued at USD 64.9 Billion in 2025, the market is projected to reach USD 134.2 Billion by 2034, at a CAGR of 8.16%. The World Health Organization estimates that 2 billion people consume feces-contaminated water, driving demand. In April 2024, the U.S. Environmental Protection Agency introduced national PFAS standards and announced USD 1 billion in funding, accelerating advanced filtration adoption.

Households dominate with a 52.0% share in 2025, while commercial demand holds 27.4%, driven by hospitality, healthcare, and food service sectors. Retail Stores lead distribution with 45.0%, though Online channels are growing fastest at ~10.5% CAGR. Asia Pacific leads with 30.0% share, followed by North America (24.6%) and Europe (22.3%).

Smart IoT-enabled purification and multi-stage systems combining RO, UV, and activated carbon are reshaping the market. In May 2025, Culligan International launched ZeroWater Technology with 5-stage filtration and real-time TDS monitoring, reflecting the shift toward advanced purification solutions.

Key Market Insights

|

Insight |

Data |

|

Largest End-User Segment |

Household - 52.0% share (2025) |

|

Leading Distribution Channel |

Retail Stores - 45.0% share (2025) |

|

Fastest Growing Channel |

Online - CAGR ~10.5% (2026-2034) |

|

Leading Region |

Asia Pacific - 30.0% revenue share (2025) |

|

Second Largest Region |

North America - 24.6% revenue share (2025) |

|

Top Companies |

A. O. Smith, 3M, BRITA, Coway, Kent RO, Philips |

|

Market Opportunity |

Smart IoT-enabled purifiers & emerging-market expansion |

Key Analytical Observations Supporting the Above Data:

- Household Dominance (52.0% in 2025): reflects surging point-of-use adoption driven by concerns over heavy metals, microbial pathogens, and emerging contaminants such as PFAS in municipal water supplies across Asia Pacific and North America.

- Retail Stores (45.0%) remain primary: due to consumer preference for hands-on product evaluation, in-store demonstrations, and immediate availability of replacement filters, particularly in tier-2 and tier-3 cities across India and China.

- Online Channel is the highest-growth vector: Expanding at ~10.5% CAGR through 2034, driven by e-commerce growth, subscription-based filter replacements, and competitive pricing enabling broader adoption.

- Asia Pacific's 30.0% dominance in 2025: is reinforced by India's Jal Jeevan Mission targeting universal tap water connectivity, China's urban water-safety investments, and Southeast Asia's rapidly expanding middle-class consumer base.

- Commercial segment (27.4%) growth: is being accelerated by stricter water-quality standards in food service, pharmaceutical manufacturing, and healthcare facilities that require compliant point-of-entry solutions.

Global Water Purifier Market Overview

Water purifiers are point-of-use (POU) and point-of-entry (POE) systems removing bacteria, viruses, heavy metals, and dissolved solids. Technologies include RO, UV, carbon, and hybrid filtration. The ecosystem spans suppliers, membrane manufacturers, OEMs, and multi-tier distribution networks serving households, commercial, and industrial users across 100+ countries globally.

Applications span residential kitchens, commercial food service, healthcare facilities, hospitality, industrial process water, and municipal utility augmentation. Macroeconomic drivers include global freshwater stress - the UN estimates 2 billion people lacked safely managed drinking water in 2022 - combined with rapid urbanization, rising disposable incomes in developing economies, and increasingly stringent government water-quality regulations in 60+ countries globally.

Market Dynamics

To evaluate market opportunities, Request Sample

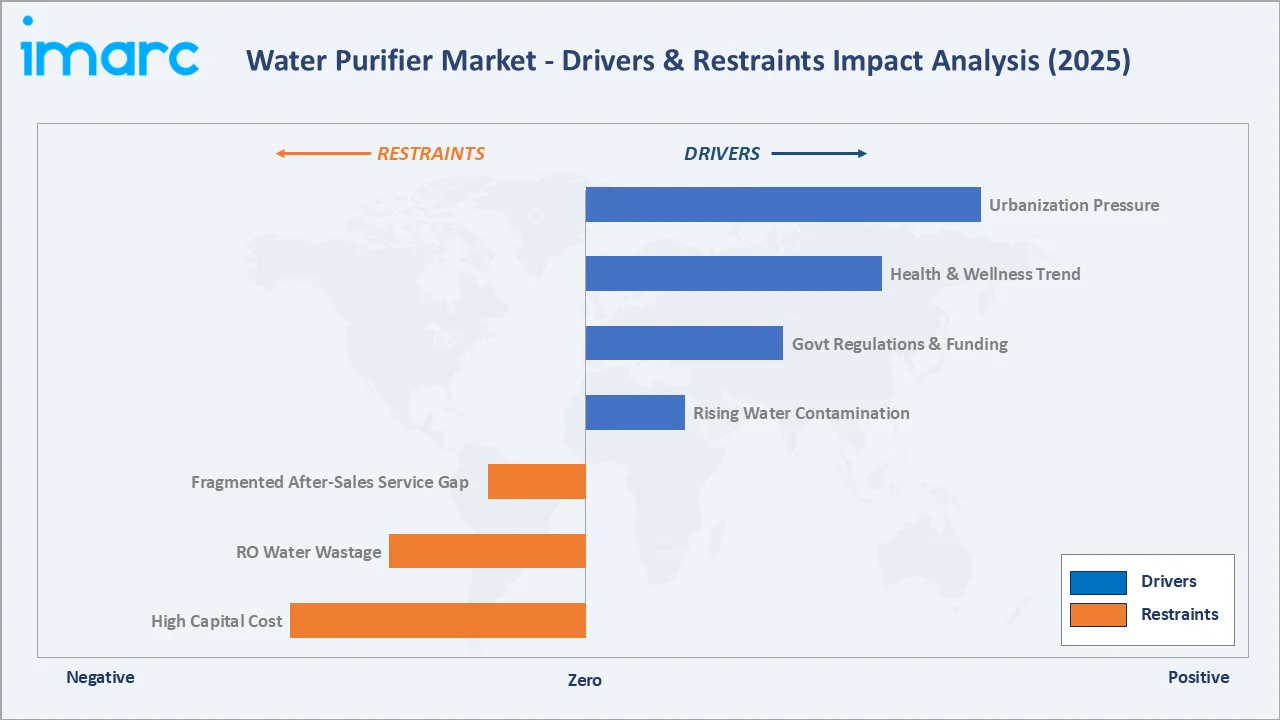

Market Drivers

- Rising Water Contamination and Waterborne Disease Burden: WHO estimates microbiologically contaminated drinking water causes 505,000 diarrhoeal deaths annually. Industrial discharge, agricultural runoff, aging infrastructure, and PFAS contamination are accelerating global demand for advanced home and commercial purification solutions.

- Urbanization and Municipal Infrastructure Stress: The United Nations projects 68% urban population by 2050, up from 56% in 2023. Asia holds 2.2+ billion urban residents and is expected to add 1.2 billion more by 2050, intensifying water infrastructure demand.

- Government Regulatory Initiatives and Clean Water Programs: India’s ₹3.60–8.69 lakh crore Jal Jeevan Mission, U.S. EPA 2024 PFAS standards with ~USD 1 billion funding, and China’s ~USD 300 billion Water Ten Plan accelerate global purification demand.

- Health and Wellness Megatrend: Rising concerns over heavy metals, microplastics, pharmaceuticals, and pesticides are driving health-essential purifier purchases, particularly among younger urban consumers across Asia Pacific and North America.

Market Restraints

- High Initial Capital Cost and Maintenance Burden: Advanced RO systems priced between USD 200 and USD 800 create affordability barriers in lower-income rural regions of Sub-Saharan Africa and South Asia, restricting penetration primarily to urban markets.

- Water Wastage in RO Technology: Conventional reverse osmosis systems waste 3–4 liters per liter purified, creating sustainability concerns in water-stressed regions like India, the Middle East, and California, driving demand for high-efficiency alternatives.

- Fragmented After-Sales Service Infrastructure: Timely filter replacement is critical for purifier performance, yet uneven service networks in rural and semi-urban markets lead to underperformance, consumer dissatisfaction, and reduced repeat purchases and referrals.

Market Opportunities

- Smart IoT-Connected Purifiers: IoT, cloud connectivity, and AI-driven maintenance are creating premium water purifiers. In May 2025, Culligan launched systems with real-time TDS monitoring, while smart water management demand continues expanding globally.

- Emerging Economy Rural Penetration: Over 700 million people in South Asia and Sub-Saharan Africa lack safe drinking water, creating opportunities for affordable gravity-fed and solar-powered purification solutions supported by government and NGO procurement.

- Commercial and Industrial Expansion: Stringent water purity standards across healthcare, pharmaceuticals, food and beverage, and data centers are accelerating commercial water purifier demand across industrial and institutional applications.

Market Challenges

- Consumer Education and Technology Differentiation: The proliferation of gravity, RO, UV, and multi-stage systems creates consumer confusion, particularly in first-purchase markets, requiring companies to invest in education and trusted brand positioning.

- Supply Chain Complexity for Membranes and UV Components: RO membranes from the U.S., Japan, and South Korea and UV lamp components face disruptions; in 2024, membrane lead times extended to 16–20 weeks, affecting OEM production and inventory.

Emerging Market Trends

1. Integration of Smart Purification Technologies

IoT-based purifiers enable real-time monitoring, predictive maintenance, and remote diagnostics. In May 2025, Culligan launched ZeroWater with TDS tracking, while AI-powered systems dynamically optimize purification performance.

2. Rising Focus on Sustainable Purification Solutions

Environmental sustainability is driving eco-friendly designs and high-recovery RO systems. In February 2025, Zurn Elkay reported saving 32.5 billion gallons and preventing 19 billion bottles, appealing to 12-15% growing eco-conscious consumers.

3. Shift Toward Multi-Stage Filtration Architectures

Consumer demand is shifting toward multi-stage systems. In October 2025, A. O. Smith launched Z2Pro Vogue 7-stage purifier, targeting microbes, heavy metals, and pesticides across diverse water sources.

4. Commercial and Healthcare Sector Expansion

Hospitals, pharmaceutical manufacturers, food processors, and hospitality chains are adopting certified point-of-entry purification systems, with regulatory compliance becoming a procurement prerequisite and driving higher value commercial demand.

5. Affordable Solutions for Emerging Market Rural Penetration

Low-cost gravity and solar purifiers priced USD 20–60 are expanding rural adoption across India, Nigeria, Bangladesh, and Kenya, while microfinance models target 600+ million households relying on untreated water.

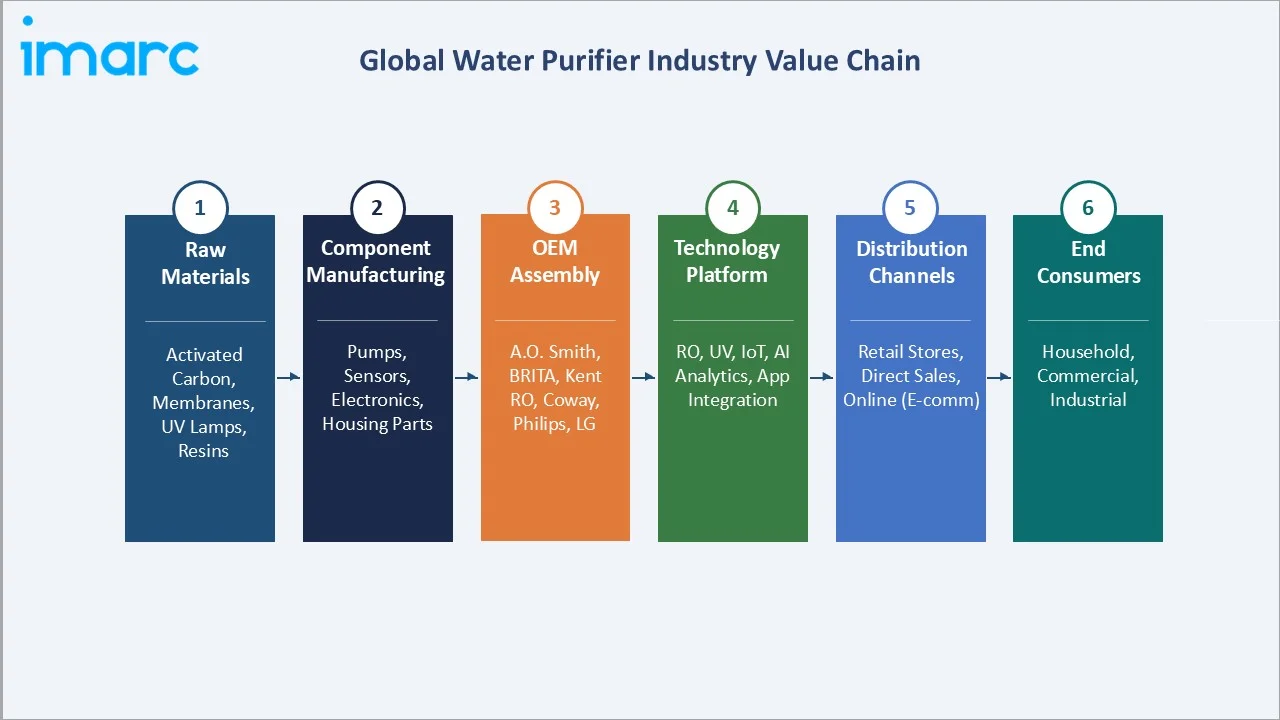

Industry Value Chain Analysis

The water purifier value chain comprises six integrated stages from raw materials to end-use consumption, each defined by distinct competitive dynamics, technology requirements, and margin structures shaping industry positioning.

|

Stage |

Key Players / Examples |

|

Raw Material Procurement |

Activated carbon (Cabot Corp), RO membranes (DowDuPont, Toray Industries), UV lamps, polypropylene filter housings |

|

Component Manufacturing |

Membrane module makers, pump suppliers (Grundfos), electronic sensor manufacturers (Texas Instruments) |

|

OEM Assembly & Branding |

A. O. Smith, BRITA, Coway, Kent RO, LG Electronics, Panasonic, Philips, Eureka Forbes, Livpure |

|

Technology Platform |

RO systems, UV-C LED modules, IoT cloud platforms, AI analytics engines, multi-stage filter architectures |

|

Distribution Channels |

Retail Stores (45.0%), Direct Sales (30.6%), Online/E-commerce (24.4%) - 2025 revenue shares |

|

End-Users |

Households (52.0%), Commercial (27.4%), Industrial (20.6%) - 2025 revenue shares |

Membrane and UV manufacturers hold strategic positions, with RO membranes accounting for 30–40% of costs, while OEM brands capture margins and online channels compress traditional retail intermediaries.

Technology Landscape in the Water Purifier Industry

Reverse Osmosis (RO) Technology

Reverse osmosis remains the dominant technology, removing 95–99% of contaminants. Traditional systems operate at 20–50% recovery rates, while newer 400 GPD tankless RO systems offer improved efficiency, compact design, and enhanced performance for residential applications.

Ultraviolet (UV) Disinfection

UV-C LED technology (260–280 nm) is emerging as an alternative to 254 nm mercury lamps, which typically last 8,000–12,000 hours. LEDs enable compact, energy-efficient systems suitable for decentralized purification, though complementary filtration remains necessary for dissolved contaminants.

IoT and Smart Connectivity

Smart water purifiers with IoT sensors monitor TDS, pH, turbidity, temperature, and chlorine, sending real-time data via Wi-Fi or Bluetooth. AI-based predictive maintenance, cloud diagnostics, OTA updates, and subscription filter services enhance performance, reduce maintenance risks, and enable recurring revenue.

Gravity and Activated Carbon Systems

Gravity-fed and activated carbon filters dominate rural markets, with coconut-shell carbon improving adsorption efficiency. Ceramic gravity filters are expanding across Sub-Saharan Africa and rural India as affordable, electricity-free drinking water solutions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology Type |

RO Purifiers |

33% |

2025 |

|

Distribution Channel |

Retail Stores |

45% |

2025 |

|

End-User |

Household |

52% |

2025 |

|

Region |

Asia Pacific |

30% |

2025 |

By Distribution Channel

Retail stores hold a 45.0% share of the global water purifier market in 2025, driven by consumer preference for demonstrations, hands-on evaluation, and expert guidance, particularly in regions requiring compatibility with diverse water chemistry.

To access detailed market analysis, Request Sample

Direct sales account for 30.6%, driven by in-home demonstrations supporting premium RO adoption. Companies like Eureka Forbes maintain large salesforces in India, while online channels at 24.4% grow through subscription-based filter services.

By End-User

The household segment holds 52.0% of global water purifier revenue in 2025, driven by rising residential demand, increasing water contamination concerns, aging infrastructure risks, and growing consumer adoption of certified home purification solutions.

Commercial demand accounts for 27.4%, driven by restaurants, hospitals, and institutions requiring compliant water purity, with 8.3% CAGR projected through 2034. Industrial users at 20.6% include pharmaceuticals, electronics, and food processing requiring ultra-pure water.

Regional Market Insights

|

Region |

Share 2025 |

Key Growth Drivers |

Regulatory Factors |

Major Companies |

|

Asia Pacific |

30.0% |

Large population, urbanization, Jal Jeevan Mission, health awareness |

India FSSAI water standards, China Water Ten Plan, WHO Guidelines |

Kent RO, Livpure, Eureka Forbes, Panasonic, Coway |

|

North America |

24.6% |

PFAS regulations, aging infrastructure, health-conscious consumers |

U.S. EPA PFAS Standards 2024, Safe Drinking Water Act |

3M, A. O. Smith, Culligan, Whirlpool, GE Appliances |

|

Europe |

22.3% |

Premium health trends, PFAS awareness, sustainability mandates |

EU Drinking Water Directive 2021, REACH regulations |

BRITA, Philips, Culligan Europe, Pentair, BWT AG |

|

Latin America |

12.1% |

Waterborne disease burden, expanding middle class, Brazil urbanization |

Brazil CONAMA standards, National Basic Sanitation Law 2020 |

Brastemp, Consul, Electrolux Latin America, BRITA |

|

Middle East & Africa |

11.0% |

Water scarcity, desalination dependence, GCC rising incomes |

GCC water quality standards, Saudi Vision 2030 water investments |

Aqua Kent ME, 3M, A. O. Smith, local distributors |

Asia Pacific holds 30.0% in 2025, driven by India and China’s population exceeding 2.8 billion and rising water quality concerns. India’s Jal Jeevan Mission has covered 15+ crore households, while North America at 24.6% grows following 2024 EPA PFAS regulations affecting nearly 100 million consumers.

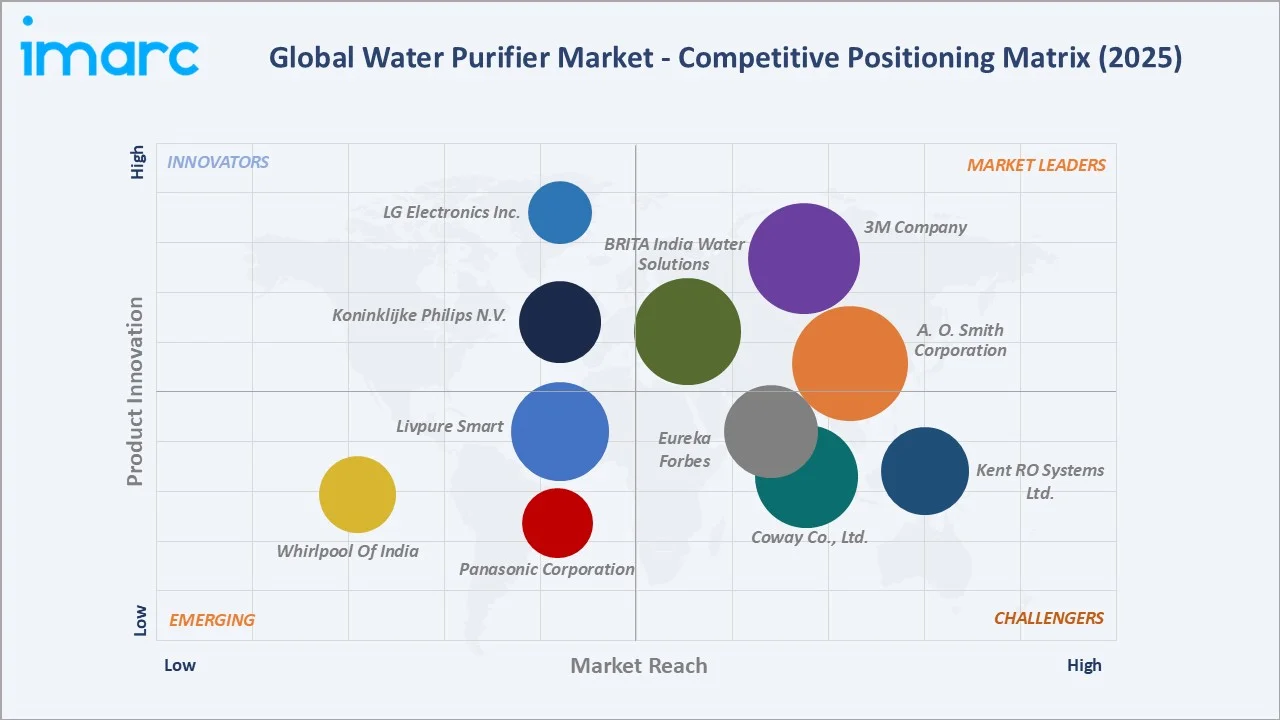

Competitive Landscape

|

Company Name |

Brand Name |

Market Position |

Key Strength |

|

A. O. Smith Corporation |

A. O. Smith Water |

Leader |

RO+UV multi-stage innovation, strong Asia-Pacific presence |

|

3M Company |

3M Water Filtration |

Leader |

Industrial/commercial filtration, NSF-certified solutions |

|

BRITA India Water Solutions Pvt. Ltd. |

BRITA |

Leader |

Consumer trust, pitcher/tap filtration, global brand equity |

|

Coway Co. Ltd. |

Coway |

Challenger |

Smart connected purifiers, subscription rental model |

|

Eureka Forbes |

Aquaguard |

Challenger |

India-dominant distribution network, D2C direct sales |

|

Kent RO Systems Ltd. |

KENT |

Challenger |

RO technology leadership in India, affordable pricing |

|

Koninklijke Philips N.V. |

Philips Water / Philips |

Challenger |

Premium countertop systems, brand trust in Europe/Asia |

|

LG Electronics Inc. |

LG PuriCare |

Challenger |

Smart IoT-enabled purifiers, Korean technology pedigree |

|

Livpure Smart |

Livpure |

Emerging |

IoT-first design, fast-growing India challenger brand |

|

Panasonic Corporation |

Panasonic |

Emerging |

Japan-engineered technology, energy efficiency focus |

|

Whirlpool Of India |

Whirlpool |

Emerging |

Consumer appliance ecosystem synergies in India |

The competitive positioning matrix evaluates 11 key players based on Market Presence (global scale, distribution reach) and Strategic Investment Level (R&D, innovation) to classify Leaders, Challengers, and Emerging Players.

Key Company Profiles

A. O. Smith Corporation

A. O. Smith, headquartered in Milwaukee, USA, is a global water technology company offering residential and commercial water purification solutions. The company operates in over 60 countries with strong growth in China and India. Its portfolio includes RO, UV, and smart connected purifiers. The company has expanded through acquisitions such as Aquasana and Pureit (2024), strengthening its global water treatment footprint and distribution network.

3M Company

3M, headquartered in St. Paul, Minnesota, provides residential, commercial, and industrial water filtration solutions using advanced materials science. Its product range includes activated carbon filters, under-sink systems, and whole-house filtration technologies designed to reduce contaminants including chlorine, heavy metals, and sediments. Growing regulatory focus on PFAS contamination and drinking water quality is increasing demand for certified filtration systems across healthcare, food service, and residential sectors..

BRITA India Water Solutions Pvt. Ltd.

BRITA, headquartered in Taunusstein, Germany, is a global water filtration company operating in over 69 countries. The company pioneered consumer water filter pitchers and offers products including MAXTRA+ cartridges and MicroDisc filtration technology that reduce chlorine, limescale, and metals. BRITA maintains strong brand recognition in Europe and Asia, supported by continuous innovation, design-focused products, and growing demand for sustainable, plastic-reducing filtration solutions.

Coway Co. Ltd.

Coway, headquartered in Seoul, South Korea, is a global wellness appliance company specializing in water purifiers and air purifiers. The company pioneered the rental-subscription service model in 1998, providing maintenance and filter replacement services. Coway operates globally with subsidiaries in Malaysia, the United States, Thailand, and other markets. Its smart water purifiers feature IoT connectivity, real-time monitoring, and premium design positioning.

Kent RO Systems Ltd.

Kent RO Systems, headquartered in Noida, India, is a leading water purifier brand known for introducing RO technology to Indian households. Founded in 1999, the company offers RO+UV+UF multi-stage purification systems and diversified healthcare appliances. Kent has built strong brand recognition through technological innovation, large product portfolio, and nationwide service network, while expanding into commercial purification solutions for institutions and offices.

Market Concentration Analysis

The global water purifier market remains moderately fragmented, with the top 5 players—A. O. Smith, 3M, BRITA, Coway, and Eureka Forbes/Kent RO—accounting for 30–35% of global revenue in 2025. This structure reflects geographic diversity, where strong regional leaders dominate local markets but demonstrate limited cross-regional expansion.

Consolidation trends are accelerating through strategic M&A and technology partnerships. The premium smart purifier segment is consolidating around IoT-enabled technology leaders, while emerging markets remain fragmented with 200+ local manufacturers across India, China, and Southeast Asia. Gradual consolidation is expected through 2034, especially in commercial and industrial segments favoring established players.

Investment & Growth Opportunities

Fastest Growing Segments

- Online Distribution Channel: Forecasted CAGR ~10.5% (2026-2034). Subscription-based filter replacement services and smart product connectivity are driving online channel premiumization and repeat purchase frequency, particularly across India, China, and North America.

- Smart IoT-Connected Purifiers: Premium smart water purifiers are expanding with IoT features, while cloud platforms enable recurring subscription revenues and predictive maintenance services.

- Commercial Sector Expansion: The commercial end-user segment is expanding steadily, driven by demand for healthcare-grade and NSF-certified systems. These solutions command higher prices and generate recurring service contracts, creating long-term revenue opportunities beyond initial hardware sales.

Emerging Markets

- South and Southeast Asia: India's Jal Jeevan Mission infrastructure rollout, combined with 400+ million households in need of in-home purification solutions, represents the single largest addressable growth opportunity globally. Indonesia, Vietnam, and Bangladesh are secondary growth markets with rapidly rising middle-class health awareness.

- Sub-Saharan Africa: Gravity-fed and solar-powered purification solutions for 600+ million people without safe water access represent a long-term development opportunity with strong NGO and development bank financing support through multilateral institutions.

Venture Investment Trends

Venture capital investment in water purification technologies reached approximately USD 1.0 billion in 2024, targeting PFAS removal startups, membrane innovation firms, and IoT water monitoring platforms. Strategic investors, including A. O. Smith Ventures and 3M Ventures, are supporting AI-driven water analytics, while impact-focused funds backed by the World Bank and ADB are financing affordable purification solutions for underserved markets.

Future Market Outlook (2026-2034)

The global water purifier market is projected to grow from USD 64.9 Billion in 2025 to USD 134.2 Billion by 2034, at a CAGR of 8.16%. Growth is supported by rising contamination concerns such as PFAS, increasing adoption of smart home–integrated water purifiers, and tightening drinking water regulations across major regions including the U.S., EU, Australia, and others implementing stricter standards.

Technological disruption will center on AI-driven predictive purification - systems that continuously adapt filtration intensity to incoming water quality, minimizing media waste and maximizing contaminant removal efficiency. Membrane technology will see continued improvements in recovery rate and selectivity, potentially enabling RO systems to achieve 85-90% water recovery by 2030. The convergence of water purification with home health monitoring will accelerate premiumization of the household segment significantly through the forecast period.

Emerging economies will drive most of the volume growth through 2034, while developed markets contribute disproportionately to value growth through premiumization. Companies that invest now in IoT platform development, subscription business model infrastructure, and distribution network depth in emerging markets will be best positioned to capture the USD 134.2 billion opportunity by 2034.

Research Methodology

Primary Research

IMARC's primary research methodology includes structured interviews with senior executives, R&D directors, procurement managers, and distribution partners across the water purifier value chain. In-depth interviews are conducted with 150-200 industry stakeholders per study, including OEM manufacturers, technology suppliers, retail channel partners, and end-user category buyers. Consumer surveys across key geographies validate demand trends and willingness-to-pay thresholds for premium purification features.

Secondary Research

Secondary data sources include WHO and UN water quality databases, U.S. EPA regulatory filings, European Commission Drinking Water Directive documents, NSF International certification databases, industry association publications (Water Quality Association, Indian Plumbing Association), and peer-reviewed academic research on water contamination trends. Company annual reports, patent databases, and trade publication analysis supplement primary intelligence.

Forecasting Models

Market size estimation employs bottom-up and top-down approaches validated through triangulation. Bottom-up modeling aggregates segment-level demand (household, commercial, industrial) across 50+ country markets. The base case 8.16% CAGR reflects the central scenario of continued urbanization, regulatory tightening, and technology adoption at observed historical rates, sensitivity-tested against multiple regulatory change scenarios.

Water Purifier Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technology Types Covered | Gravity Purifiers, RO Purifiers, UV Purifiers, Sediment Filter, Water Softener, Others |

| Distribution Channels Covered | Retail Stores, Direct Sales, Online |

| End-Users Covered | Industrial, Commercial, Household |

| Regions Covered | Europe, North America, Asia Pacific, Middle East and Africa, Latin America |

| Companies Covered | A. O. Smith Corporation, 3M Company, BRITA India Water Solutions Pvt. Ltd., Coway Co. Ltd., Eureka Forbes, Kent RO Systems Ltd., Koninklijke Philips N.V., LG Electronics Inc., Livpure Smart, Panasonic Corporation, Whirlpool Of India, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the water purifier market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global water purifier market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the water purifier industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Water Purifier Market Report

The global water purifier market was valued at USD 64.9 Billion in 2025 and is projected to reach USD 134.2 Billion by 2034, growing at a CAGR of 8.16%.

The global water purifier market is forecasted to grow at a CAGR of 8.16% from 2026 to 2034, driven by water contamination concerns and rising health awareness globally.

Asia Pacific leads with a 30.0% market share in 2025, supported by large populations in India and China, government clean-water programs, and rapid urbanization across the region.

Primary drivers include rising waterborne disease incidence, urban infrastructure stress, PFAS contamination regulations, health awareness, and the global shift from single-use plastic bottles.

Retail Stores dominate with a 45.0% share in 2025, though Online channels are the fastest growing at an estimated 10.5% CAGR due to e-commerce expansion and subscription filter models.

Household is the largest end-user segment at 52.0% in 2025, reflecting widespread residential adoption of point-of-use purification for safe drinking water across all geographies.

Leading companies include A. O. Smith, 3M, BRITA, Coway, Eureka Forbes, Kent RO Systems, Koninklijke Philips, LG Electronics, Livpure, Panasonic, and Whirlpool India.

IoT-enabled smart purifiers with real-time TDS monitoring and AI predictive maintenance are driving premiumization, with the smart segment growing 12-15% CAGR ahead of the market average.

The April 2024 EPA national PFAS drinking water standards and USD 1 billion implementation fund are catalyzing demand for NSF-certified RO and advanced carbon filtration across North America.

Major trends include smart IoT integration, sustainability-focused low-waste RO systems, multi-stage filtration architectures, commercial sector expansion, and affordable rural-market solutions.

The market is moderately fragmented. Top 5 players hold approximately 30-35% combined share in 2025. Consolidation is gradually occurring in commercial segments while household segment remains highly competitive.

India alone represents 400+ million households needing purification solutions. Combined with Southeast Asia and Sub-Saharan Africa, emerging economies represent the highest-volume growth opportunity globally through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)