Water Soluble Film Market Size, Share, Trends and Forecast by Material, Application, End-Use Industry, and Region, 2026-2034

Water Soluble Film Market Size and Share:

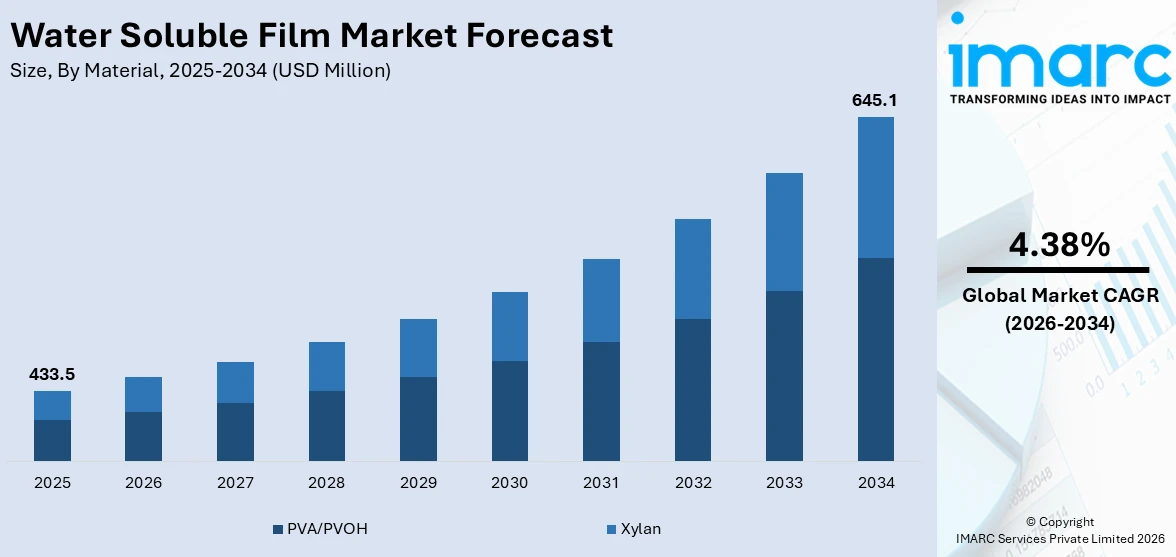

The global water soluble film market size was valued at USD 433.5 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 645.1 Million by 2034, exhibiting a CAGR of 4.38% during 2026-2034. North America currently dominates the market, holding a significant market share of over 34.7% in 2025. This can be ascribed to strong consumer demand for sustainable packaging, advanced technological developments, and stringent environmental regulations. These factors drive the adoption of eco-friendly solutions, with industries focusing on reducing plastic waste, consequently increasing the water soluble film market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 433.5 Million |

|

Market Forecast in 2034

|

USD 645.1 Million |

| Market Growth Rate 2026-2034 | 4.38% |

The global market is experiencing significant momentum due to the expansion of e-commerce and the consequent rise in demand for efficient packaging solutions that minimize environmental impact. For instance, according to industry reports, the eco-friendly packaging market is projected to increase from USD 257.73 Billion in 2025 to USD 498.29 Billion by 2034, with a compound annual growth rate (CAGR) of 7.6% between 2025 and 2034. Increased awareness regarding microplastic pollution has also accelerated the shift toward water-soluble alternatives in food-grade and personal care applications. Furthermore, the growing trend of single-dose product packaging across various sectors, including agrochemicals and industrial cleaners, enhances the appeal of these films. Strategic collaborations between film manufacturers and chemical companies are fostering innovation, enabling films with higher tensile strength and controlled solubility rates. Additionally, advancements in cold-water soluble formulations are opening new avenues in temperature-sensitive applications, further supporting water soluble film market growth.

To get more information on this market Request Sample

In the United States, the water soluble film market is primarily driven by the increasing emphasis on industrial automation and the need for pre-measured, mess-free packaging in manufacturing processes. The country's robust pharmaceutical sector has adopted water-soluble films for precise drug delivery systems, contributing significantly to market growth. Strong federal initiatives promoting sustainability and plastic reduction are also encouraging adoption across consumer and institutional segments. Furthermore, the growth of environmentally conscious start-ups and rising venture capital investment in green packaging technologies have accelerated innovation and market penetration. The expansion of industrial and institutional cleaning services, coupled with stringent occupational safety standards, further strengthens the demand for dissolvable, low-contact packaging solutions.

Water Soluble Film Market Trends:

Rising Demand in Sustainable Packaging Applications

Water-soluble films are increasingly utilized in the packaging of disinfectants and detergents due to their eco-friendly, non-toxic, and biodegradable nature. This shift aligns with global sustainability goals and consumer preferences for environmentally responsible products. In the United States alone, the Packaging & Labeling Services industry consists of over 15,309 businesses and has grown at a compound annual growth rate (CAGR) of 7.1% from 2020 to 2025. The robust expansion of this industry highlights the growing demand for innovative packaging solutions. Water-soluble films also provide effective barriers against odors, gases, bacteria, and moisture, making them suitable for a range of hygiene and cleaning applications. This trend is expected to continue as sustainability becomes central to corporate packaging strategies.

Shift Toward Circular Economy and Innovation

As industries increasingly pivot toward circular economy models, water-soluble films are emerging as a key component of sustainable packaging strategies. By 2025, over 40% of companies are expected to adopt innovative and eco-friendly packaging technologies, a shift that is driving substantial interest in dissolvable films. These films not only reduce environmental impact but also improve product safety by limiting human exposure to harsh chemicals. In response, companies are investing in R&D to develop next-generation water-soluble materials with enhanced strength, solubility control, and barrier properties. Advanced polymer chemistry, synthetic materials, and carbon-based technologies are being explored to meet growing demands. This trend reflects a broader market move toward high-performance, sustainable alternatives that support both environmental goals and functional efficiency, further creating a positive water soluble film market outlook.

Expanding Industrial and Food & Beverage Applications

Water-soluble films are gaining significant traction in the chemical industry due to their ability to protect workers from direct contact with hazardous substances. Pre-measured, single-use packaging using water-soluble films minimizes risk and enhances safety in industrial settings. Simultaneously, the food and beverage (F&B) sector is adopting these films for their excellent air-, oil-, and moisture-resistant properties, ensuring longer shelf life and improved product integrity. These advantages are offering lucrative opportunities for manufacturers to diversify applications and meet evolving industry requirements. Additionally, regulatory pressures regarding environmental compliance are compelling companies to replace traditional plastic with dissolvable alternatives. This adoption, combined with rising investment in technological innovations, is shaping the market’s expansion into previously untapped verticals, solidifying water-soluble films as a versatile solution. For instance, in October 2024, Arrow Greentech showcased its Watersol™ water-soluble packaging at PMFAI ICSCE 2024, focusing on sustainability and safety in agriculture. The technology dissolves quickly in water, reducing pollution, health risks, and waste. It ensures precise mono-dosing and eliminates plastic contamination, aligning with global environmental goals. Arrow’s eco-friendly solutions are gaining recognition for enhancing efficiency and promoting sustainable agricultural practices, while the company expands its global presence and partnerships in the agrochemical market.

Water Soluble Film Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global water soluble film market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on material, application, and end-use industry.

Analysis by Material:

- PVA/PVOH

- Xylan

PVA/PVOH stand as the largest material in 2025, holding around 77.9% of the market due to its exceptional solubility, biodegradability, and film-forming capabilities. PVA is widely preferred for its non-toxic nature, making it suitable for packaging applications in detergents, agrochemicals, and pharmaceuticals. Its ability to dissolve quickly in water without leaving residue enhances convenience and safety, particularly in single-use and unit-dose packaging. Furthermore, its superior tensile strength and resistance to oil, grease, and solvents make it ideal for industrial applications. Regulatory support for sustainable materials and increasing demand for eco-friendly alternatives further amplify its adoption. Manufacturers also favor PVA due to its compatibility with existing production technologies, driving its dominance in the material landscape of the global market.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Detergent Packaging

- Agrochemical Packaging

- Water Treatment Chemical Packaging

- Pharmaceutical Packaging

- Others

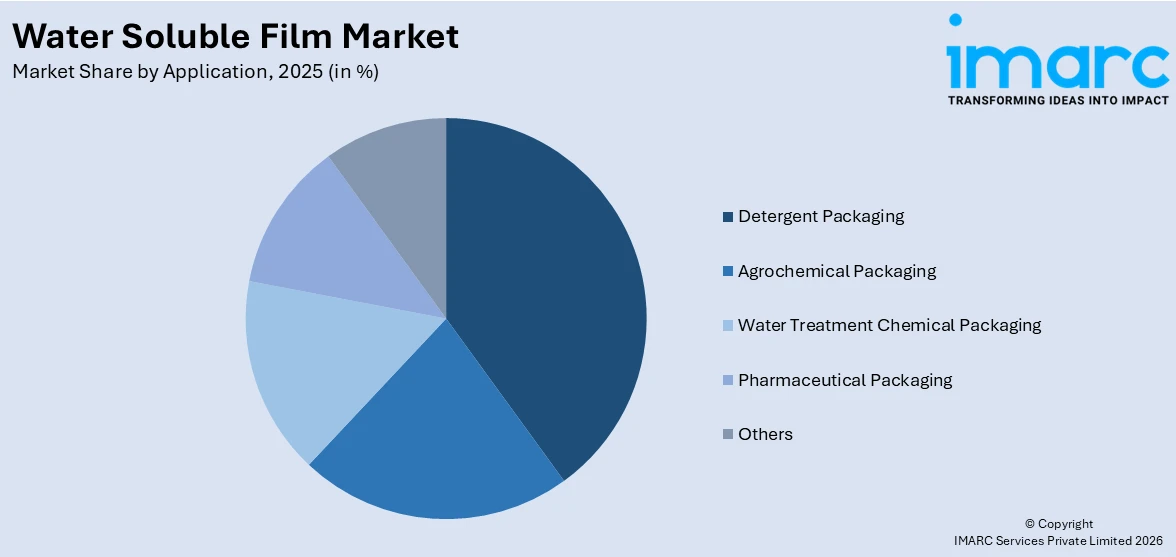

Detergent packaging leads the market with around 33.9% of market share in 2025 due to the growing demand for convenient, single-use, and eco-friendly packaging formats. Water-soluble films are ideal for unit-dose detergent capsules, reducing waste and preventing product overuse. Their ability to dissolve completely in water eliminates the need for secondary packaging and minimizes direct human contact with chemicals, enhancing safety and hygiene. Additionally, the rise in automated washing machines globally has fueled the popularity of pre-measured detergent pods, further boosting demand. Environmental regulations and consumer preference for sustainable packaging also contribute to the shift away from traditional plastic containers. These factors collectively position detergent packaging as the dominant application segment in the water-soluble film industry. For instance, in February 2024, A.I.S.E. conducted research on the biodegradability of polyvinyl alcohol (PVA) films used in liquid detergent capsules. The study, supported by Henkel, P&G, Unilever, and others, found that most PVA films meet biodegradability criteria, fully dissolving in water and not contributing to plastic or microplastic pollution. Results showed significant biodegradation within 28 days, confirming PVA's environmental safety. The findings were supported by other studies, including those from the EPA, which confirmed PVA’s biodegradability and its use in consumer products.

Analysis by End-Use Industry:

- Textile

- Agriculture

- Consumer Goods

- Healthcare

- Others

Consumer goods leads the market with around 35.9% of market share in 2025. The water soluble film market research report suggests growth driven by rising consumer awareness and demand for sustainable, user-friendly packaging solutions. Water-soluble films are increasingly utilized in everyday products such as laundry pods, dishwasher tablets, personal care items, and single-use hygiene products. These films offer convenience, precise dosage, and reduce plastic waste, aligning with growing environmental concerns and zero-waste lifestyle trends. Additionally, advancements in film technology have enabled greater durability, moisture resistance, and compatibility with various consumer applications. Major consumer goods brands are integrating water-soluble films into their sustainability initiatives, further accelerating adoption. The combination of regulatory pressures, shifting consumer preferences, and product innovation has made this segment the largest contributor to market growth.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- Asia Pacific

- Europe

- Latin America

- Middle East and Africa

In 2025, North America accounted for the largest market share of over 34.7%, primarily due to strong environmental regulations, high consumer awareness, and advanced industrial infrastructure. The region’s well-established packaging, pharmaceutical, and detergent industries are increasingly adopting biodegradable and sustainable materials to meet both regulatory requirements and shifting consumer preferences. Additionally, the widespread use of single-dose packaging in household and institutional cleaning products has fueled demand for water-soluble films. Key players in North America are heavily investing in R&D to enhance film performance, solubility, and strength, which supports further adoption across diverse applications. Government initiatives promoting plastic reduction and sustainability, coupled with the region’s focus on innovation, continue to drive market dominance in North America. For instance, according to industry reports, as of 2024, seven U.S. states, such as California, Colorado, Maine, Oregon, New Jersey, Minnesota, and Washington, have implemented active Extended Producer Responsibility (EPR) or similar packaging laws, targeting key waste streams such as packaging, electronic or electrical waste, and batteries, which are recognized globally for their volume and toxicity. EPR holds producers accountable for the entire lifecycle of their products.

Key Regional Takeaways:

United States Water Soluble Film Market Analysis

In 2025, the United States held a market share of around 86.80% in North America. United States is experiencing increased water soluble film adoption driven by the growing demand for sustainable packaging. According to industry reports, about half of US consumers are willing to pay more for sustainable packaging: across different end-use areas, about 50% of consumers are willing to pay 1 to 3% more, 25% are willing to pay 4 to 7% more, and about 12% are willing to pay 7 to 10% more. As environmental concerns escalate, industries across food, agriculture, and personal care are turning to sustainable packaging alternatives that reduce plastic waste. Water soluble film, being biodegradable and dissolvable in water, is gaining traction as an ideal solution for single-use and unit-dose packaging formats. This shift is further supported by consumer awareness and preference for environmentally friendly products, encouraging businesses to invest in sustainable packaging innovations. Regulatory focus on reducing plastic consumption is also contributing to the rapid adoption of water soluble film across multiple sectors. The sustainable packaging movement continues to redefine material usage patterns in the region, fueling long-term growth prospects for water soluble film applications.

Asia Pacific Water Soluble Film Market Analysis

Asia-Pacific is witnessing notable water soluble film adoption supported by the increasing number of packaging units. Approximately 85% of the more than 22,000 packaging units in India are Small and Medium Enterprises (SMEs). Rapid industrialization, urban population growth, and rising consumption patterns have significantly expanded packaging operations across sectors such as food, agriculture, and consumer goods. The surge in packaging units is creating a robust demand for efficient and eco-friendly materials, positioning water soluble film as a viable packaging solution. Its ability to meet diverse application requirements while minimizing environmental footprint makes it favorable in this high-volume region. Local manufacturers are actively exploring water soluble film technologies to align with evolving sustainability goals and regulatory directions. As packaging operations scale up to meet growing consumer demand, water soluble film stands out for its adaptability and environmental compliance, enhancing its role in the regional packaging landscape.

Europe Water Soluble Film Market Analysis

Europe is advancing in water soluble film adoption fueled by growing pharmaceutical packaging requirements. The Germany pharmaceutical packaging market size reached USD 6.0 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 12.5 Billion by 2033, exhibiting a growth rate (CAGR) of 7.8% during 2025-2033. With increased healthcare awareness and the rising demand for precise medication delivery formats, pharmaceutical companies are leveraging water soluble film for unit-dose and dissolvable applications. Its compatibility with sensitive compounds and hygienic benefits positions it as a preferred choice in pharmaceutical packaging. The strict regulatory environment regarding material safety and environmental impact further drives this transition. Innovations in drug delivery and packaging mechanisms are amplifying interest in water soluble film across European pharmaceutical supply chains. Sustainability remains a core priority, and water soluble film aligns with these objectives by reducing material waste and enhancing compliance with eco-design mandates. This regional demand reflects a broader trend toward functional, sustainable solutions in healthcare packaging.

Latin America Water Soluble Film Market Analysis

Latin America is seeing increased water soluble film adoption due to growing demand for flexible packaging. Latin America flexible packaging market size reached USD 8.74 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 12.21 Billion by 2033, exhibiting a growth rate (CAGR) of 3.5% during 2025-2033. As industries seek more adaptable and efficient packaging options, flexible packaging formats are gaining popularity for their convenience and reduced material usage. Water soluble film complements these needs by offering dissolution properties and environmental benefits. The shift toward lightweight and sustainable materials is reinforcing the use of water soluble film in diverse sectors. Its integration in flexible packaging supports regional goals for waste reduction and packaging efficiency.

Middle East and Africa Water Soluble Film Market Analysis

Middle East and Africa are experiencing higher water soluble film adoption driven by growing textile industries. According to reports, in 2022, the UAE textile market was valued at more than USD10 Billion and is now expected to expand by more than 5% a year over the medium term. As textile production expands, the need for efficient and eco-friendly packaging of dyes and detergents has increased. Water soluble film meets these industrial needs with its dissolvable and non-contaminating properties. Its application enhances workflow efficiency and aligns with cleaner production initiatives. The regional textile sector’s focus on sustainability and chemical handling efficiency is accelerating the shift toward water soluble film usage in operational processes.

Competitive Landscape:

The water soluble film market forecast indicates a competitive landscape marked by moderate to high fragmentation, with a mix of global and regional players vying for market share through product quality, innovation, and pricing strategies. The market is driven by rising demand in sectors such as agriculture, pharmaceuticals, home care, and food packaging due to the film’s eco-friendly and biodegradable properties. Key competitive factors include technological advancements, custom formulations, and strong distribution networks. Companies often invest in R&D to enhance film solubility, strength, and compatibility with various substances. Strategic partnerships, capacity expansions, and sustainability initiatives are common approaches to gain market share. Additionally, regulatory support for green packaging and increased environmental awareness are compelling firms to innovate while meeting stringent safety and performance standards. For instance, in May 2024, Ecopol announced that its Hydrolene® LTF/LJ film received the prestigious "OK biodegradable WATER®" certification from TÜV AUSTRIA, demonstrating its ability to decompose effectively in freshwater environments. This certification follows the success of Hydrolene® LTF/TB, highlighting Ecopol's commitment to sustainability. The achievement reinforces their mission to reduce environmental impact and mitigate waste in rivers, lakes, and freshwater ecosystems, marking a significant step toward a greener, more sustainable future.

The report provides a comprehensive analysis of the competitive landscape in the water soluble film market with detailed profiles of all major companies, including:

- Kuraray Co. Ltd.

- Nippon Synthetic Chemical Industry Co. Ltd.

- Sekisui Chemical Co., Ltd.

- Aicello Corporation

- Arrow GreenTech Ltd.

- Cortec Corporation

- Changzhou Kelin PVA Water Soluble Films Co., Ltd.

- Jiangmen Proudly Water-soluble Plastic Co., Ltd.

- AMC (UK) Ltd.

- 3M Company

- Mitsubishi Chemical Corporation

- DuPont de Nemours, Inc.

- Fujian Zhongsu Biodegradable Films Co., Ltd.

- Dezhou Huamao Textile Co. Ltd.

- Neptun Technologies GmbH

Latest News and Developments:

- February 2025: Arrow Greentech Ltd. Showcased its sustainable water-soluble film innovations at the ICSCE Buyer-Seller Meet 2025, indicating ongoing product development and launches focused on eco-friendly packaging solutions.

- April 2024: Polyva launched its new water-soluble film technologies, emphasizing advancements in sustainable packaging solutions designed for pesticide powders and granules. The company continues to lead in developing innovative, eco-friendly packaging options with improved performance in high humidity environments.

- April 2024: Kao Corporation accelerated its sustainability efforts with innovations such as stick-shaped powdered laundry detergent in water-soluble film and refillable dishwashing liquid packs, reflecting its commitment to achieving net zero plastic packaging waste by 2040 and negative waste by 2050.

Water Soluble Film Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Materials Covered | PVA/PVOH, Xylan |

| Applications Covered | Detergent Packaging, Agrochemical Packaging, Water Treatment Chemical Packaging, Pharmaceutical Packaging, Others |

| End-Use Industries Covered | Textile, Agriculture, Consumer Goods, Healthcare, Others |

| Region Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

| Companies Covered | Kuraray Co. Ltd., Nippon Synthetic Chemical Industry Co. Ltd., Sekisui Chemical Co., Ltd., Aicello Corporation, Arrow GreenTech Ltd., Cortec Corporation, Changzhou Kelin PVA Water Soluble Films Co., Ltd., Jiangmen Proudly Water-soluble Plastic Co., Ltd., AMC (UK) Ltd., 3M Company, Mitsubishi Chemical Corporation, DuPont de Nemours, Inc., Fujian Zhongsu Biodegradable Films Co., Ltd., Dezhou Huamao Textile Co. Ltd., and Neptun Technologies GmbH |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the water soluble film market from 2020-2034.

- The water soluble film market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the water soluble film industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Water Soluble Film Market Report

The water soluble film market was valued at USD 433.5 Million in 2025.

The water soluble film market is projected to exhibit a CAGR of 4.38% during 2026-2034, reaching a value of USD 645.1 Million by 2034.

The water soluble film market is driven by rising environmental concerns, growing demand for biodegradable packaging, and increasing use in industries like agriculture, pharmaceuticals, and detergents. Regulatory support for sustainable materials, advancements in film technology, and consumer preference for eco-friendly products further contribute to the market’s steady global growth.

In 2025, North America dominated the water soluble film market, holding a market share of over 34.7%. This is driven by growing demand for sustainable packaging, strong presence of key manufacturers, increasing environmental regulations, and rising adoption in industries such as agriculture, pharmaceuticals, and detergents seeking eco-friendly and efficient packaging solutions.

Some of the major players in the water soluble film market include Kuraray Co. Ltd., Nippon Synthetic Chemical Industry Co. Ltd., Sekisui Chemical Co., Ltd., Aicello Corporation, Arrow GreenTech Ltd., Cortec Corporation, Changzhou Kelin PVA Water Soluble Films Co., Ltd., Jiangmen Proudly Water-soluble Plastic Co., Ltd., AMC (UK) Ltd., 3M Company, Mitsubishi Chemical Corporation, DuPont de Nemours, Inc., Fujian Zhongsu Biodegradable Films Co., Ltd., Dezhou Huamao Textile Co. Ltd., Neptun Technologies GmbH, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)