Wind Energy Market Report by Component (Turbine, Support Structure, Electrical Infrastructure, and Others), Rating (≤ 2 MW, >2 ≤ 5 MW, >5 ≤ 8 MW, >8 ≤ 10 MW, >10 ≤ 12 MW, >12 MW), Installation (Offshore, Onshore), Turbine Type (Horizontal Axis, Vertical Axis), Application (Utility, Industrial, Commercial, Residential), and Region 2026-2034

Wind Energy Market Size:

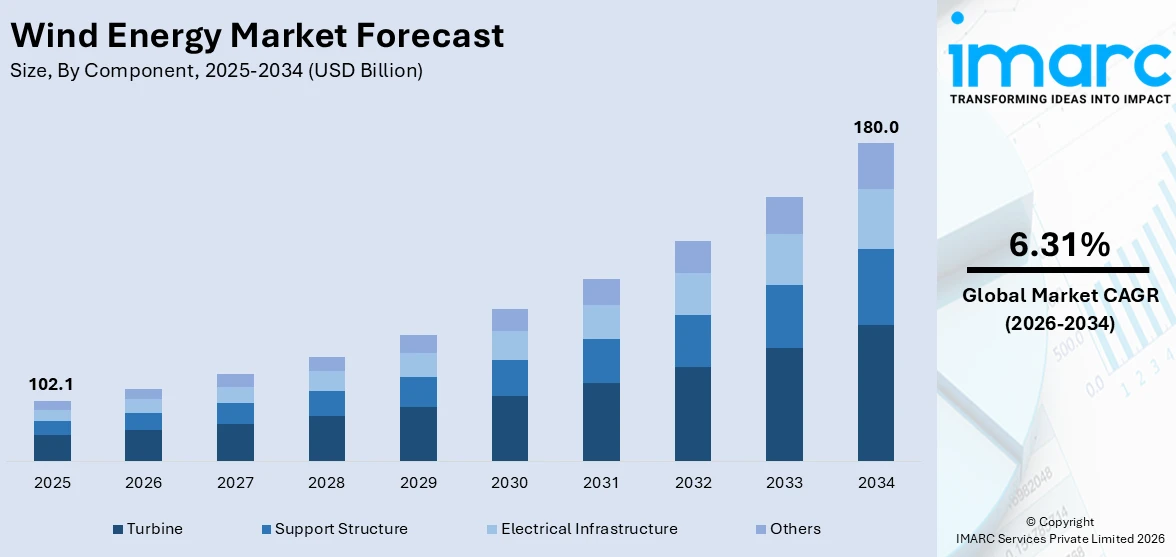

The global wind energy market size reached USD 102.1 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 180.0 Billion by 2034, exhibiting a growth rate (CAGR) of 6.31% during 2026-2034. The increasing demand for renewable energy sources, the increasing implementations of favorable policies and incentives, such as tax credits, subsidies, and feed-in tariffs, in stringent manner, and the development of energy storage technologies represent some of the key factors driving the market toward growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 102.1 Billion |

|

Market Forecast in 2034

|

USD 180.0 Billion |

| Market Growth Rate 2026-2034 | 6.31% |

Wind Energy Market Analysis:

- Major Market Drivers: The wind energy market is primarily being driven by ongoing technological advancements in turbine design, government support and incentives for renewable energy, declining cost of wind technology, and increasing environment consciousness.

- Key Market Trends: Some major key trends in the wind energy market include technological improvements in turbine efficiency, increasing investments from public and private sectors, the rising adoption of offshore wind farms, and a growing focus on repowering old wind farms.

- Geographical Trends: Asia Pacific dominates the wind energy market due to significant investments in renewable energy, the implementation of favorable government policies supporting the installation of turbines, vast availability of land, and favorable natural conditions for wind farms.

- Competitive Landscape: Some of the major market players in the wind energy industry include ABB Ltd., Acciona, Ameren Services, Bergey Windpower Co., DNV AS, EDF Power Solutions, Enercon Global GmbH, Goldwind, NextEra Energy Resources LLC, Nordex SE, Suzlon Energy Limited, Vestas, and Xcel Energy Inc., among many others.

- Challenges and Opportunities: Challenges in the wind energy market include high initial investment costs, variable wind speeds, and integration into the power grid. Opportunities arise from technological advancements, increasing government incentives, and growing global demand for sustainable energy solutions, which encourage further development and adoption of wind energy infrastructure.

To get more information on this market Request Sample

Wind Energy Market Trends:

Widespread Adoption of Renewable Energy Sources

The widespread adoption of renewable energy sources acts as a key driver for the wind energy market due to growing environmental concerns and the global commitment to reduce carbon emissions. For instance, according to the Distributed Wind Market Report 2022, published by Office of Energy Efficiency & Renewable Energy of the US Government, the government added 13,413 MW capacity with 1,751 new turbines in 15 states, reflecting a $41 million investment and increasing the total capacity to 1,075 MW. Moreover, in EU, a record 16 GW of wind power installations were added in 2022, that is a 47% increase compared to 2021. The global shift towards renewable energy, such as wind, is driven by its environmental benefits, cost-effectiveness, and scalability. Notably, a June 2022 report from the U.S. Energy Information Administration highlighted biomass as the primary source, contributing 5% to the total U.S. energy consumption in 2021. Moreover, with ambitious targets in places like Germany aiming for up to 70 GW by 2045, the wind energy market is poised for significant growth.

Robust Government Support

Robust government support is a key driver for the wind energy market as it often includes incentives such as tax rebates, subsidies, and feed-in tariffs that make wind projects financially viable. Governments also frequently set renewable energy targets and implement policies that mandate the use of cleaner energy sources, thereby fostering a more favorable investment climate. For example, the UK government announced plans in March 2023 to quadruple offshore wind capacity to 50 GW by 2030 and achieve net-zero power generation by 2035. Similarly, the EU member states are enhancing offshore wind activities by approving a €4.12 billion French scheme to support the rollout of renewable offshore wind energy, further fostering the transition to a net-zero economy, in line with the Green Deal Industrial Plan. In the US, a substantial commitment of $369 billion in February 2023 is set to stimulate investments in renewable energy. In Germany and Denmark, a significant investment of €9,000 million was announced in August 2022 for a 3 GW wind power plant, with €6,000 million allocated specifically for the offshore sector. Such support not only lowers the financial barriers associated with wind energy projects but also signals a stable market, attracting private investors and accelerating sector growth.

Technological Advancements

A key trend in the wind energy market is the focus on technological advancements, with companies investing in innovative technologies to enhance their market competitiveness. An example is WEG Industries from Brazil, which introduced a new wind turbine platform in July 2022 that features Medium-Speed Geared (MSG) drive technology, has a 7 MW capacity, and a 172-meter rotor diameter. This platform excels in its grid adaptability and can produce reactive energy during low wind periods. The turbine's design includes modular components and a taller tower, simplifying logistics and assembly, especially in difficult terrains. Furthermore, significant reductions in the levelized cost of electricity (LCOE) for wind energy have been achieved, with a 56% decrease in onshore wind LCOE from 2010 to 2020 and about a 48% reduction in offshore wind LCOE. This cost efficiency, coupled with rising capacity factors, supports the escalating global investments in wind and other energy transition technologies, which hit a record $1.3 trillion in 2022.

Wind Energy Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on component, rating, installation, turbine type, and application.

Breakup by Component:

- Turbine

- Support Structure

- Electrical Infrastructure

- Others

Turbine accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the component. This includes turbine, support structure, electrical infrastructure, and others. According to the report, turbine represented the largest segment.

The turbine segment is anticipated to lead in the global wind energy market. Wind turbines, which convert wind energy into electricity through the aerodynamic force exerted by rotor blades like airplane wings or helicopter rotors, are expected to hold a significant market share. Wind turbines offer numerous benefits: they are a cost-effective source of power, with land-based utility-scale wind being one of the most affordable energy options today, costing $32/MW-hours in 2021. Additionally, unlike power plants that burn fossil fuels, such as coal or natural gas, which contribute to public health and economic issues, wind turbines do not pollute the environment. Wind energy is also a derivative of solar energy, influenced by the sun's heating of the atmosphere, the rotation of the Earth, and its surface irregularities. Furthermore, wind turbines can be installed on existing farms or ranches, integrating seamlessly with current land uses.

Breakup by Rating:

- ≤ 2 MW

- >2 ≤ 5 MW

- >5 ≤ 8 MW

- >8 ≤ 10 MW

- >10 ≤ 12 MW

- >12 MW

>12 MW holds the largest share of the industry

A detailed breakup and analysis of the market based on the rating have also been provided in the report. This includes ≤ 2 MW, >2 ≤ 5 MW, >5 ≤ 8 MW, >8 ≤ 10 MW, >10 ≤ 12 MW, and >12 MW. According to the report, >12 MW rating accounted for the largest market share.

Wind turbines with capacities greater than 12 MW are leading the wind energy market due to their higher efficiency and productivity. These larger turbines generate more electricity from a single installation, reducing the cost per kilowatt-hour of energy produced. They are particularly advantageous for offshore wind farms where larger installations maximize output while minimizing the environmental and logistical costs associated with multiple smaller turbines. The trend towards larger turbines is driven by ongoing technological advancements that allow for greater energy capture and operational efficiencies at sea. For instance, in September 2022, the US expanded its floating offshore wind farms capacity to 15 gigawatts by 2035. This target is part of the White House's push to bolster the nation's offshore wind industry as part of its climate-change agenda.

Breakup by Installation:

- Offshore

- Onshore

Onshore represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the installation. This includes offshore and onshore. According to the report, onshore represented the largest segment.

Onshore wind energy is the predominant installation type in the wind energy market due to its lower costs and easier logistics compared to offshore installations. Onshore wind farms can be deployed faster and with fewer regulatory challenges. Countries like Spain and France have made substantial investments in onshore wind, significantly contributing to their renewable energy mix. For example, Spain has over 1,345 operational wind farms, and its wind energy accounted for about 22% of its electricity generation in 2022. Similarly, France aims to boost its onshore wind capacity to 34 GW by 2028. In the Philippines, the development of onshore wind projects like the Balaoi and Caunayan wind farms, which began in 2021, is indicative of the region's commitment to increasing its wind energy capacity. The ongoing and planned onshore wind projects across these nations are expected to keep driving the dominance of the onshore wind sector in the market during the forecast period.

Breakup by Turbine Type:

- Horizontal Axis

- Vertical Axis

Horizontal Axis exhibits a clear dominance in the market

A detailed breakup and analysis of the market based on the turbine type have also been provided in the report. This includes horizontal and vertical axis. According to the report, horizontal axis accounted for the largest market share.

Horizontal axis dominate the wind energy market due to their efficiency and technological maturity. They are designed with blades that rotate parallel to the ground, allowing them to capture more wind over a larger area and generate more power compared to vertical axis turbines. This design is also more effective at higher altitudes where wind speeds are greater. Moreover, the widespread familiarity with their maintenance and installation processes makes HAWTs the preferred choice for both onshore and offshore wind energy projects.

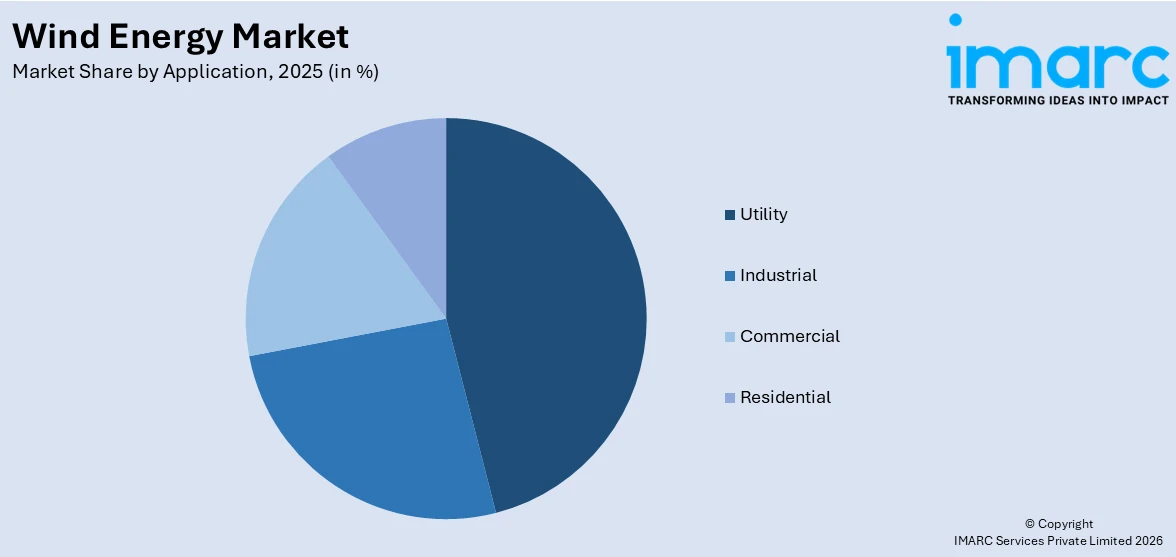

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Utility

- Industrial

- Commercial

- Residential

Utility is the predominant market segment

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes utility, industrial, commercial, and residential. According to the report, utility accounted for the largest market share.

The utility segment leads the wind energy market as large-scale wind farms efficiently produce significant amounts of electricity, addressing the energy needs of wide-ranging populations. Utilities invest in wind energy to diversify energy portfolios, minimize carbon emissions, and leverage government incentives for renewables. Wind power's falling costs and technological advancements make it essential for utilities striving to offer reliable, affordable, and sustainable energy. For instance, in October 2023, Abu Dhabi Future Energy Company initiated the UAE's first utility-scale wind project, aiming to replace fossil fuels and reduce the carbon footprint of its electricity generation sector.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific leads the market, accounting for the largest wind energy market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific represents the largest regional market for wind energy, while the Wind Energy Market in Latin America is witnessing steady growth driven by rising renewable energy investments and supportive government initiatives.

Asia Pacific is at the forefront of the global wind energy market, fueled by strong government support, substantial renewable energy investments, extensive land availability, and favorable conditions for wind farms. The region is experiencing rapid economic growth and escalating energy needs, prompting countries like China and India to significantly increase their wind energy capacities to curb carbon emissions. China is projected to lead with 1,789 GW of wind power installations by 2050. The region also shows great potential in offshore wind, with China, Japan, Korea, and Taiwan expanding their capacities. India aims to reach 500 GW of solar and wind energy by 2030, providing extensive market opportunities. Similarly, Japan plans to boost offshore wind capacity to 10 GW by 2030, emphasizing the region's aggressive push to dominate the wind energy sector globally.

Competitive Landscape:

Companies in the wind energy market are increasingly leveraging artificial intelligence (AI) to enhance wind turbine performance, increase energy production, and reduce operational costs. AI applications include advanced data analytics and predictive maintenance, which improve real-time monitoring and grid integration. For example, in April 2022, GE Research collaborated with GE Renewable Energy to introduce an AI/machine learning tool that predicts and reduces logistics costs, potentially saving billions in the industry. Additionally, significant acquisitions and partnerships are shaping the market. In 2021, Statkraft acquired Breeze Three Energy’s portfolio, expanding its European wind farms, and Maersk partnered with Vestas to optimize logistics and support sustainable energy solutions.

The report provides a comprehensive analysis of the competitive landscape in the global wind energy market with detailed profiles of all major companies, including:

- ABB Ltd.

- Acciona

- Ameren Services

- Bergey Windpower Co.

- DNV AS

- EDF Power Solutions

- Enercon Global GmbH

- Goldwind

- NextEra Energy Resources LLC

- Nordex SE

- Suzlon Energy Limited

- Vestas

- Xcel Energy Inc.

Wind Energy Market News:

- In May 2021, RWE and BASF announced plans to invest $4.9 billion in offshore wind power projects. RWE aims to construct a 2 GW offshore wind park by 2030 as part of this initiative, which is intended to provide energy to BASF's Ludwigshafen chemical complex.

- In December 2021, Iberdrola, a Spanish energy company, signed service contracts with Siemens Gamesa for 69 wind projects across Spain and Portugal. These agreements cover the maintenance of 1,963 wind turbines, which have individual power capacities ranging from 660 kW to 3.465 MW, for a duration of three to five years.

- In February 2022, Tata Power and the German electricity company RWE entered a partnership to jointly explore the development of offshore wind projects in India.

Wind Energy Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Turbine, Support Structure, Electrical Infrastructure, Others |

| Ratings Covered | ≤ 2 MW, >2 ≤ 5 MW, >5 ≤ 8 MW, >8 ≤ 10 MW, >10 ≤ 12 MW, >12 MW |

| Installations Covered | Offshore, Onshore |

| Turbine Types Covered | Horizontal Axis, Vertical Axis |

| Applications Covered | Utility, Industrial, Commercial, Residential |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ABB Ltd., Acciona, Ameren Services, Bergey Windpower Co., DNV AS, EDF Power Solutions, Enercon Global GmbH, Goldwind, NextEra Energy Resources LLC, Nordex SE, Suzlon Energy Limited, Vestas, Xcel Energy Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the wind energy market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global wind energy market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the wind energy industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Wind Energy Market Report

The global wind energy market was valued at USD 102.1 Billion in 2025.

We expect the global wind energy market to exhibit a CAGR of 6.31% during 2026-2034.

The rising consumer environmental concerns, along with the growing demand for clean and renewable energy source, such as wind energy, across the commercial, industrial, and residential sectors, as it is sustainable, cost-effective, readily available, etc., are primarily driving the global wind energy market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations, resulting in the temporary halt in the installation activities for wind turbines, thereby negatively impacting the global market for wind energy.

Based on the component, the global wind energy market can be segmented into turbine, support structure, electrical infrastructure, and others. Currently, turbine holds the majority of the total market share.

Based on the rating, the global wind energy market has been divided into ≤ 2 MW, >2 ≤ 5 MW, >5 ≤ 8 MW, >8 ≤ 10 MW, >10 ≤ 12 MW, and >12 MW. Among these, >12 MW currently exhibits a clear dominance in the market.

Based on the installation, the global wind energy market can be categorized into offshore and onshore. Currently, onshore accounts for the majority of the global market share.

Based on the turbine type, the global wind energy market has been segregated into horizontal axis and vertical axis, where horizontal axis currently holds the largest market share.

Based on the application, the global wind energy market can be bifurcated into utility, industrial, commercial, and residential. Currently, the utility sector exhibits a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where Asia-Pacific currently dominates the global market.

Some of the major players in the global wind energy market include ABB Ltd., Acciona, Ameren Services, Bergey Windpower Co., DNV AS, EDF Power Solutions, Enercon Global GmbH, Goldwind, NextEra Energy Resources LLC, Nordex SE, Suzlon Energy Limited, Vestas, and Xcel Energy Inc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)