Women Apparel Market Size, Share, Trends and Forecast by Product Type, Season, Distribution Channel, and Region, 2026-2034

Global Women Apparel Market Size, Share, Trends & Forecast (2026-2034)

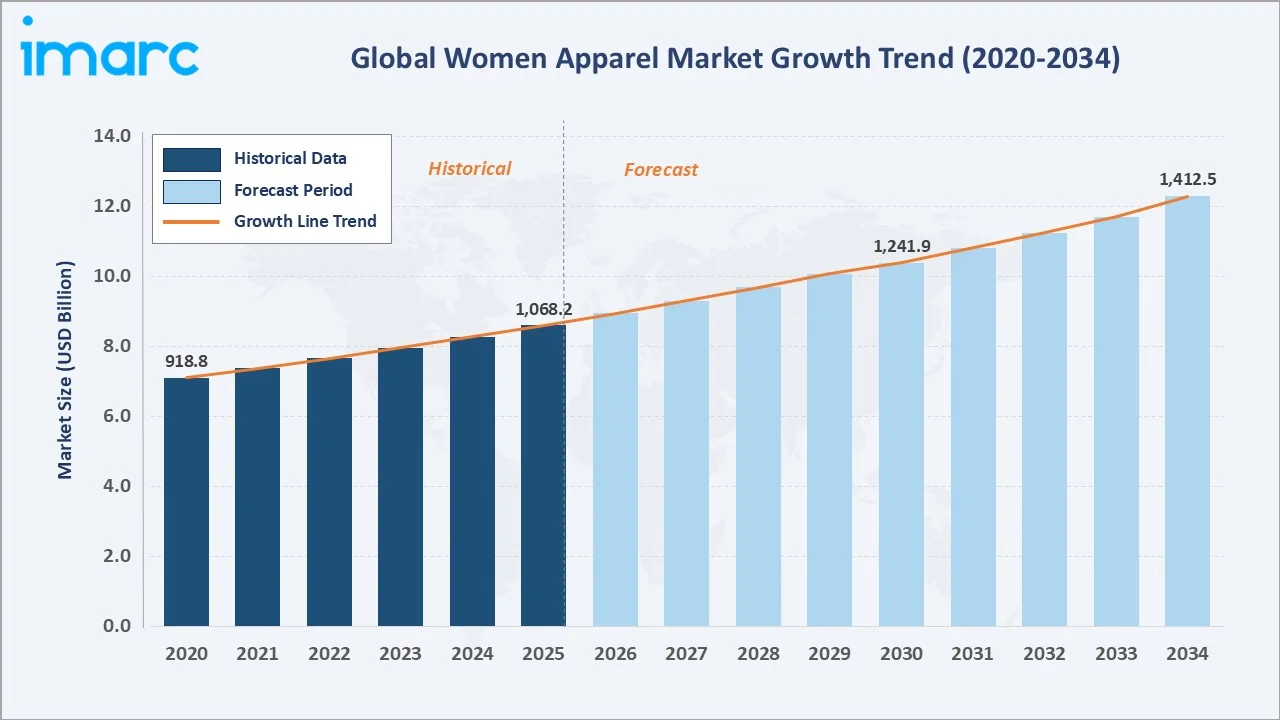

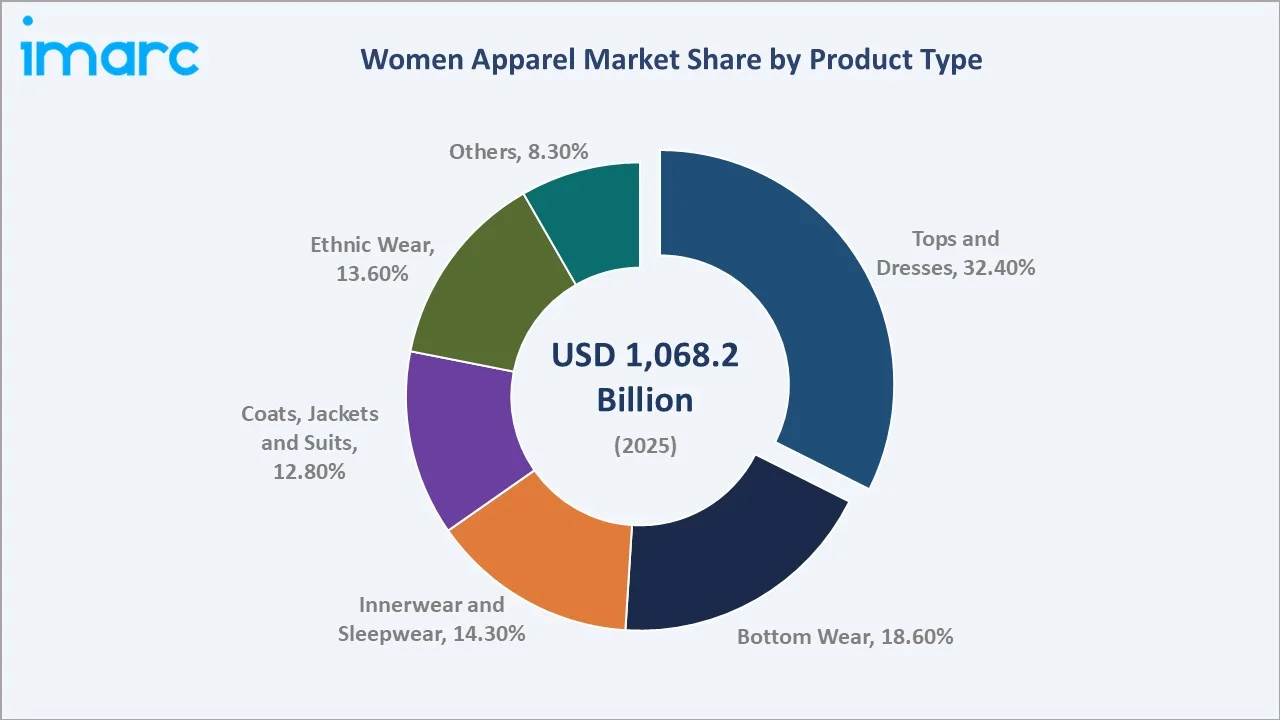

The global women apparel market was valued at USD 1,068.2 Billion in 2025 and is projected to reach USD 1,412.5 Billion by 2034, expanding at a CAGR of 3.06% during the forecast period 2026-2034. Evolving fashion trends, rising female workforce participation, growing e-commerce penetration, and the powerful influence of social media on consumer purchasing behavior are driving the market's steady expansion.

Market Snapshot

|

Report Attribute |

Key Statistics |

|

Market Size in 2025 |

USD 1,068.2 Billion |

|

Market Forecast in 2034 |

USD 1,412.5 Billion |

|

CAGR (2026-2034) |

3.06% |

|

Base Year |

2025 |

|

Forecast Years |

2026-2034 |

|

Largest Region (2025) |

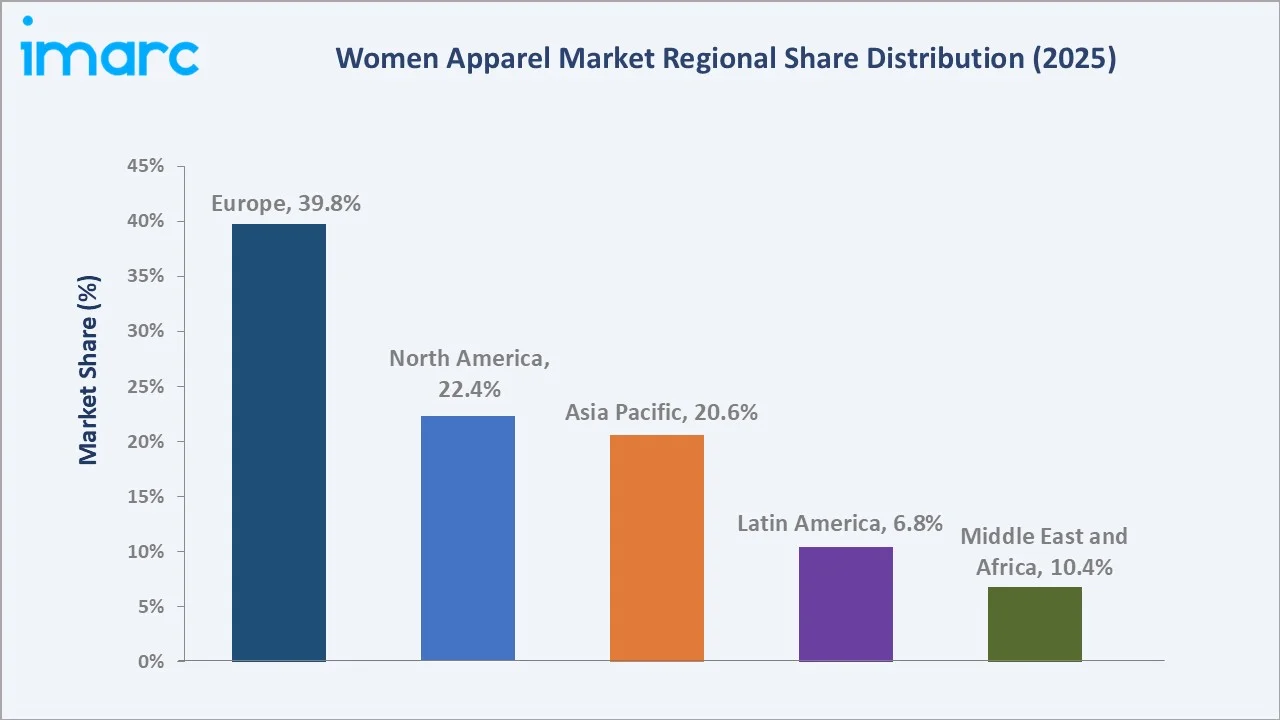

Europe - 39.8% |

|

Fastest Growing Region |

Asia Pacific |

Europe remains the dominant region, accounting for 39.8% of global revenue in 2025. Among product type, tops and dresses account for the highest revenue share at 32.4%, while online distribution channels exhibit the fastest growth.

To get more information on this market, Request Sample

The women apparel market continues to expand as consumers seek greater variety, personalization, and comfort across casual, formal, and athleisure segments. Growing awareness of sustainable fashion, along with rising demand for inclusive sizing and diverse styles, is further shaping market dynamics.

Executive Summary

The global women apparel market continues to demonstrate consistent and resilient expansion, underpinned by shifting lifestyle patterns, rapid urbanization in emerging economies, and the exponential rise of digital commerce platforms. Valued at USD 1,068.2 Billion in 2025, the market is forecast to exceed USD 1,412.5 Billion by 2034, growing at a steady CAGR of 3.06%. The proliferation of fast fashion models and the acceleration of social commerce channels have significantly broadened consumer access to diverse and affordable fashion across all geographies.

Among the key growth drivers, the rising number of working women globally remains a primary catalyst. Working women seek versatile, functional, yet stylish apparel that can transition from professional settings to casual environments. The tops and dresses segment alone represented 32.4% of the global market share in 2025, reflecting strong and consistent consumer demand for upper-body fashion staples. Premium athleisure and ethnic wear segments are gaining momentum, with ethically conscious consumers propelling sustainable fashion choices.

Europe retains its market leadership with a 39.8% share in 2025, driven by well-established fashion hubs in Paris, Milan, and London, alongside high consumer spending power. Asia Pacific emerges as the fastest-growing region owing to rapid urbanization, a burgeoning middle-class population, and the expansion of organized retail. Leading market players are investing in product innovation, omnichannel retail strategies, and sustainable manufacturing - all key areas reshaping the competitive landscape through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product Type) |

Tops and Dresses - 32.4% share (2025) |

|

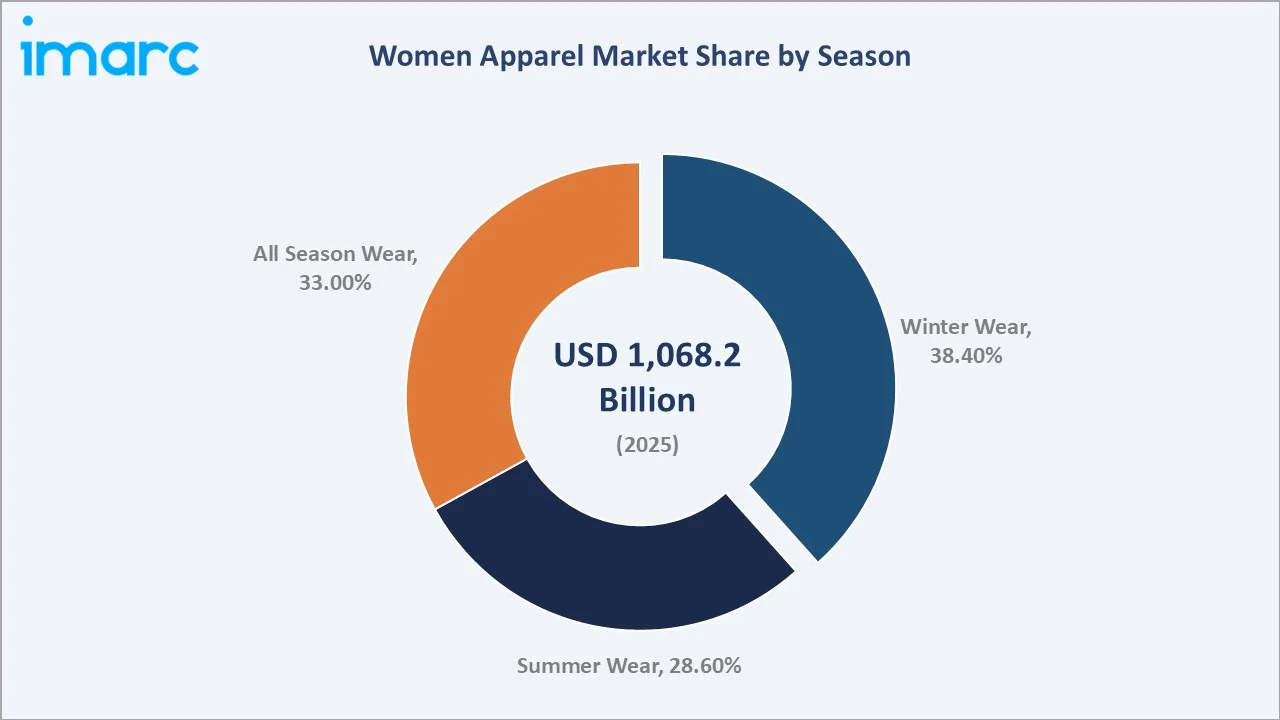

Largest Segment (Season) |

Winter Wear - 38.4% share (2025) |

|

Leading Region |

Europe - 39.8% revenue share (2025) |

|

Fastest Growing Channel |

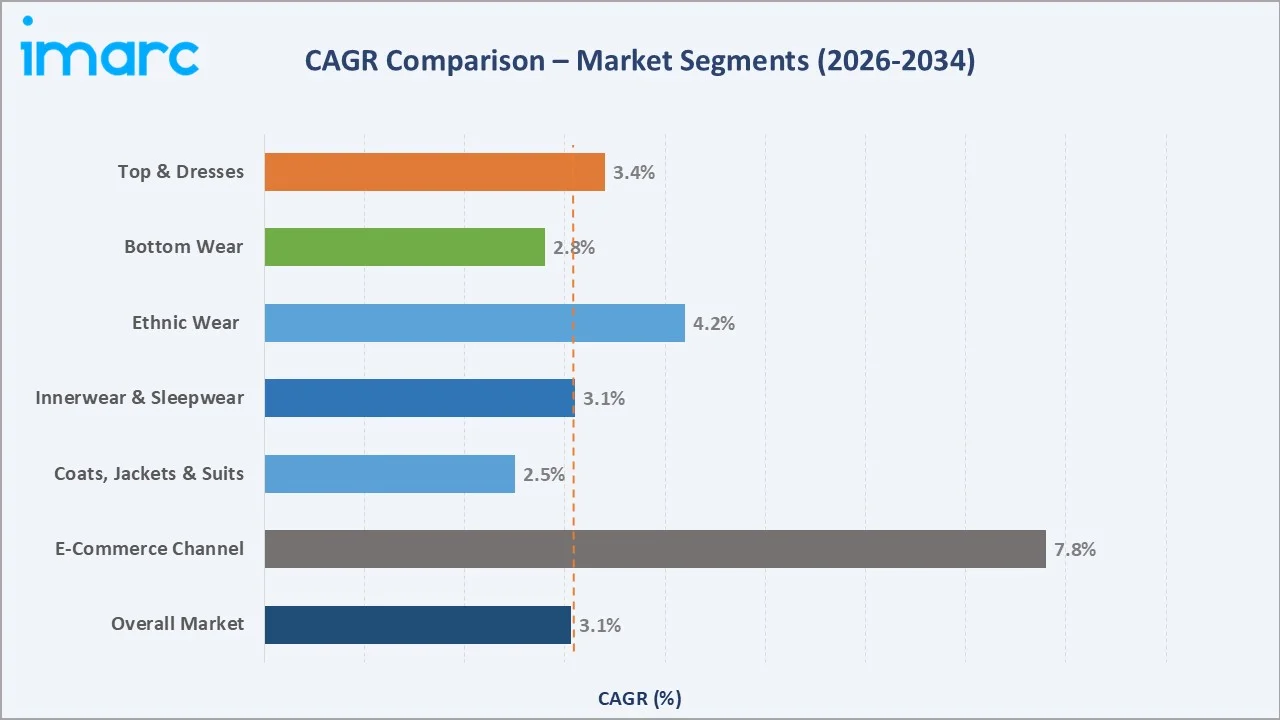

Online Stores - CAGR ~7.8% (2026-2034) |

|

Top Companies |

Inditex, H&M, Fast Retailing, LVMH, Lululemon |

|

Market Opportunity |

Asia Pacific addressable market: USD ~290 Billion by 2034 |

Key analytical observations supporting the above data:

- Tops and dresses dominate with a 32.4% market share (2025), driven by wardrobe versatility, seasonal adaptability, and the segment's capacity to serve both professional and casual lifestyle needs.

- Winter wear leads the season segmentation with a 38.4% share (2025), supported by strong cold-weather apparel demand globally, seasonal wardrobe renewal cycles, and the expansion of premium winter collections across both developed and emerging markets.

- Europe accounts for 39.8% of global revenues (2025), bolstered by a deeply entrenched luxury and fast fashion culture, premium retail infrastructure, and high per-capita apparel expenditure.

- Online stores are the fastest growing distribution channel, expanding at an estimated CAGR of 7.8% (2026-2034), supported by digital platform investments, AI-driven personalization, and mobile-first consumer behaviors in emerging economies.

- The plant-based and sustainable fashion segment is growing rapidly, with global consumers increasingly seeking eco-friendly alternatives - 77% of Gen Z shoppers prioritize sustainability when making fashion purchases.

Global Women Apparel Market Overview

The women apparel industry constitutes one of the largest and most globally recognized segments within the broader retail and consumer goods ecosystem. Encompassing a vast spectrum of product categories - from everyday casual wear and workwear to premium luxury garments and ethnic wear - the market serves an extremely diverse and influential consumer base.

Women's apparel's versatile application across consumer segments - from daily wardrobe essentials to high-fashion luxury purchases - makes it a uniquely resilient product category. Its adaptability to local cultural preferences, body diversity, and lifestyle requirements enables market penetration across geographically varied markets, from North America and Western Europe to South Asia, Southeast Asia, and the Middle East.

Macroeconomic factors, including urbanization rates, growth in female workforce participation, rising per-capita income, and digital adoption, positively affect the outlook for the women's apparel market. By 2034, women's apparel is expected to sustain its position as one of the most critical consumer spending categories globally - a testament to fashion's cultural ubiquity and commercial adaptability.

Market Dynamics

To evaluate market opportunities, Request Sample

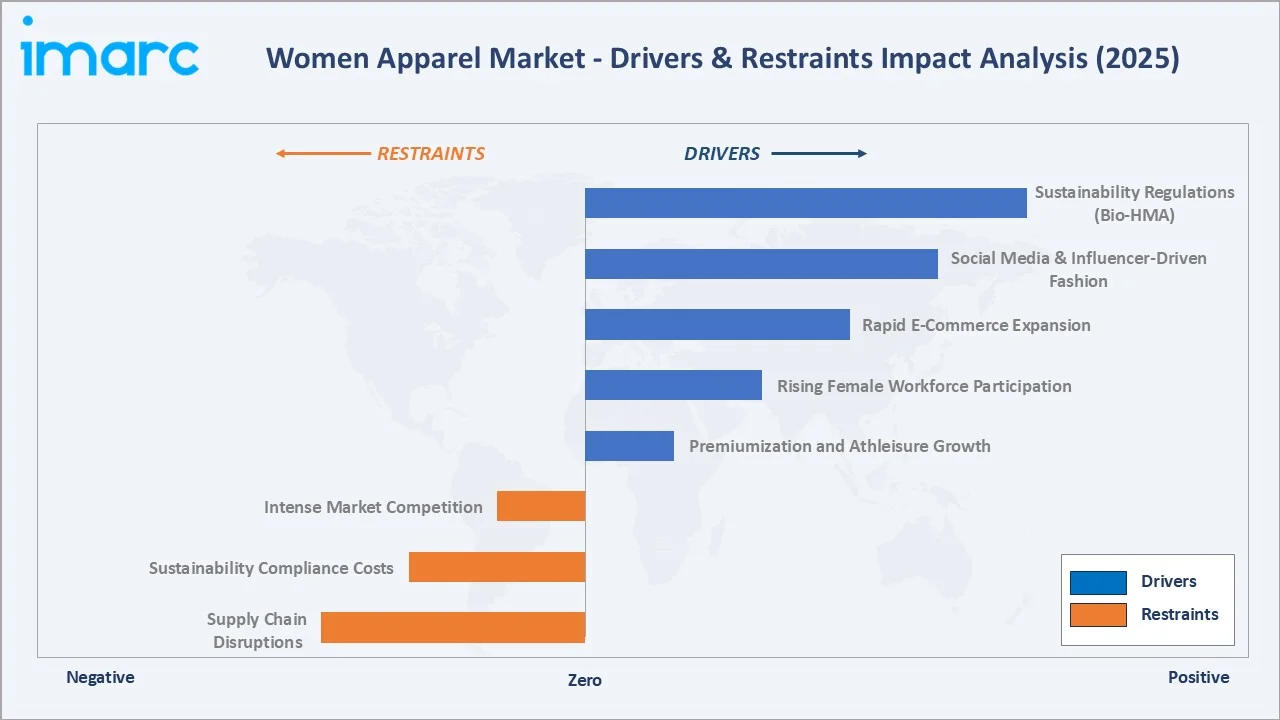

Market Drivers

- Social Media & Influencer-Driven Fashion: There were approximately 5.66 billion social media user identities worldwide as of early October 2025. This transformed how women discover and purchase apparel, with platforms such as Instagram and TikTok Shop directly enabling impulse buying and trend-driven purchases.

- Rapid E-Commerce Expansion: The U.S. retail e-commerce market recorded USD 316.1 billion in Q4 2025 sales, with women's apparel being among the top-purchased categories.

- Rising Female Workforce Participation: With the female labor force participation rate growing, demand for professional, functional, and stylish workwear is accelerating. In India, the female labor force participation rate for individuals aged 15 and above showed a steady rise from June 2025 onward, reaching 35.3% in December 2025.

- Premiumization and Athleisure Growth: Premium sportswear and athleisure apparel for women is growing at a fast rate, driven by health and wellness trends, yoga and fitness culture expansion, and lifestyle-driven fashion consumption patterns.

These drivers collectively reinforce a virtuous cycle of market expansion - social media culture triggers discovery, digital platforms enable conversion, and rising disposable incomes amplify per-basket spending. The combined effect sustains both volume and value growth simultaneously across women apparel market segments.

Market Restraints

- Supply Chain Disruptions: Geopolitical tensions, shipping delays, and raw material price volatility have elevated. For basic garments produced in small batches, the cost typically ranges from USD 8 to USD 30 per piece, squeezing margins for mid-tier brands.

- Sustainability Compliance Costs: Evolving EU textile sustainability regulations and extended producer responsibility (EPR) mandates require significant reformulation and supply chain investment - increasing operational complexity for global apparel brands.

- Intense Market Competition: The women's apparel space is highly fragmented, with thousands of fast fashion, luxury, DTC, and regional operators competing for market share, resulting in aggressive pricing pressure and reduced brand loyalty.

Market Opportunities

- Emerging Markets Expansion: Asia Pacific, Middle East, and Latin America collectively represent an incremental addressable market of approximately USD 156 billion by 2034, driven by growing middle-class populations and rising fashion consciousness among younger demographics.

- Sustainable & Circular Fashion: The global used clothing market is projected to reach USD 350 billion by 2027, opening significant opportunities for brands adopting recommerce, upcycling, and sustainable sourcing strategies.

- AI-Driven Personalization: Artificial intelligence and machine learning technologies are enabling hyper-personalized shopping experiences, as AI-powered chat boosts conversion rates by four times—12.3% compared to 3.1% on sites without AI support.

Market Challenges

- Logistics & Last-Mile Delivery Costs: According to the Last-Mile Delivery: The Future Unpacked report by DS Smith, e-commerce businesses across the United Kingdom and Europe are experiencing last-mile delivery cost increases of up to 90%.

- Counterfeit & Fast-Fashion Proliferation: The global trade in counterfeit fashion items, including clothing, footwear, handbags, and watches, exceeds USD 450 billion annually, diluting premium brand equity and undermining consumer trust in authentic women's apparel labels.

- Changes in Consumer Behavior: Rising inflation, increased living costs, and continued economic uncertainty have led consumers to become more cautious with their spending. According to a recent report, personal consumption expenditures grew by just 1.2% in Q1 2025, a sharp decline from 4% in Q4 2024.

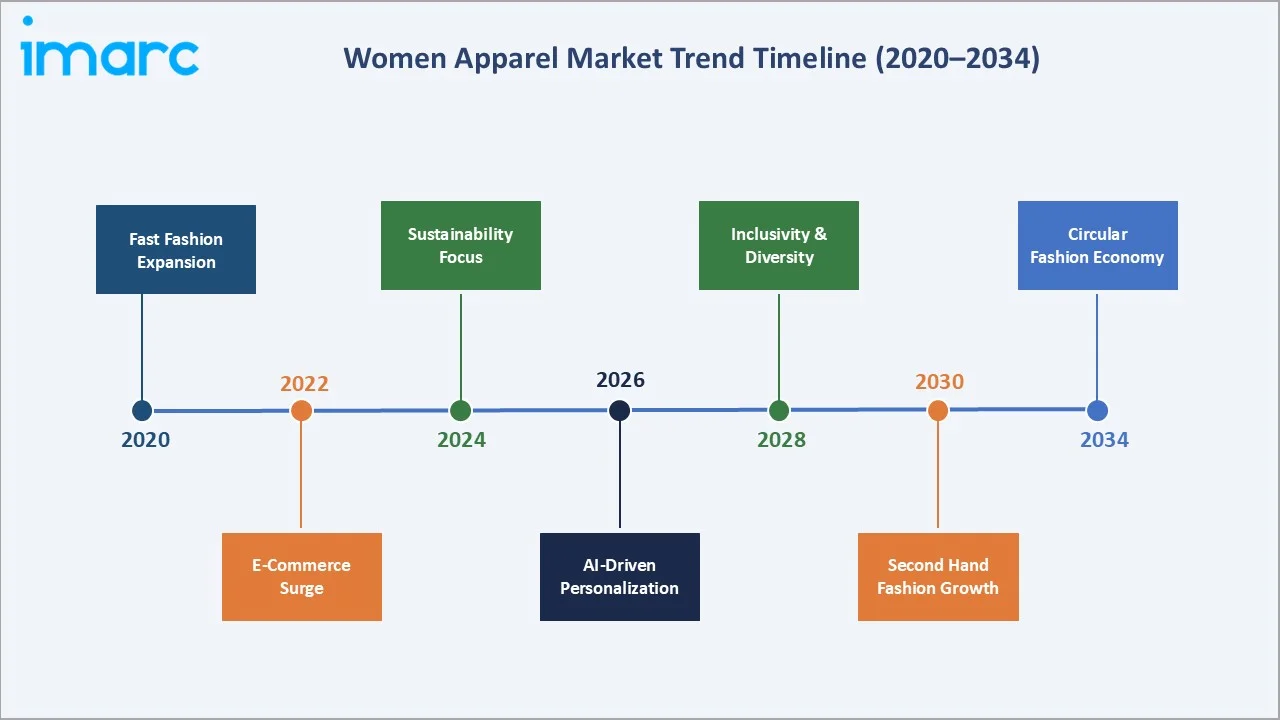

Emerging Market Trends

1. Rise of Sustainable and Ethical Fashion

Sustainability has transitioned from a niche preference to a mainstream purchasing driver in the women's apparel segment. According to the World Economic Forum, thrift store purchases are projected to grow 127% by 2026, 3 times faster than the overall clothing market. Brands are increasingly adopting organic cotton, recycled polyester, and low-impact dyeing processes to align with evolving consumer values.

2. E-Commerce and Social Commerce Transformation

U.S. retail e-commerce grew 1.7% in Q4 2025, from the third quarter of 2025, with women's fashion among the top-3 contributing categories. Social commerce channels, including TikTok Shop, Instagram Shopping, and Pinterest Checkout, are enabling frictionless purchase journeys directly within social feeds.

3. Inclusive Sizing and Body Positivity Movement

Inclusive sizing (XS to 6XL) has evolved from a differentiator to a baseline requirement for major women's apparel retailers. Businesses that prioritize fairness, consistency, and ethical practices build stronger relationships with their customers. High levels of trust drive repeat purchases and foster positive word-of-mouth recommendations.

4. Athleisure and Activewear Convergence

The convergence of activewear and everyday fashion - commonly referred to as "athleisure" - continues to be one of the defining women apparel market trends of this decade. The global women's activewear market was valued at USD 212.11 Billion in 2025 and is growing at a CAGR of 4.71% from 2026 to 2034, significantly outpacing the broader apparel market.

5. Luxury Accessible Fashion and Premiumization

A growing aspirational consumer class - particularly in Asia Pacific and the Middle East - is driving demand for "accessible luxury" women's apparel: brands positioned between mass market and ultra-premium segments. LVMH's fashion and leather goods segment achieved revenues of EUR 42.2 Billion in 2024, with women's ready-to-wear being the primary growth contributor.

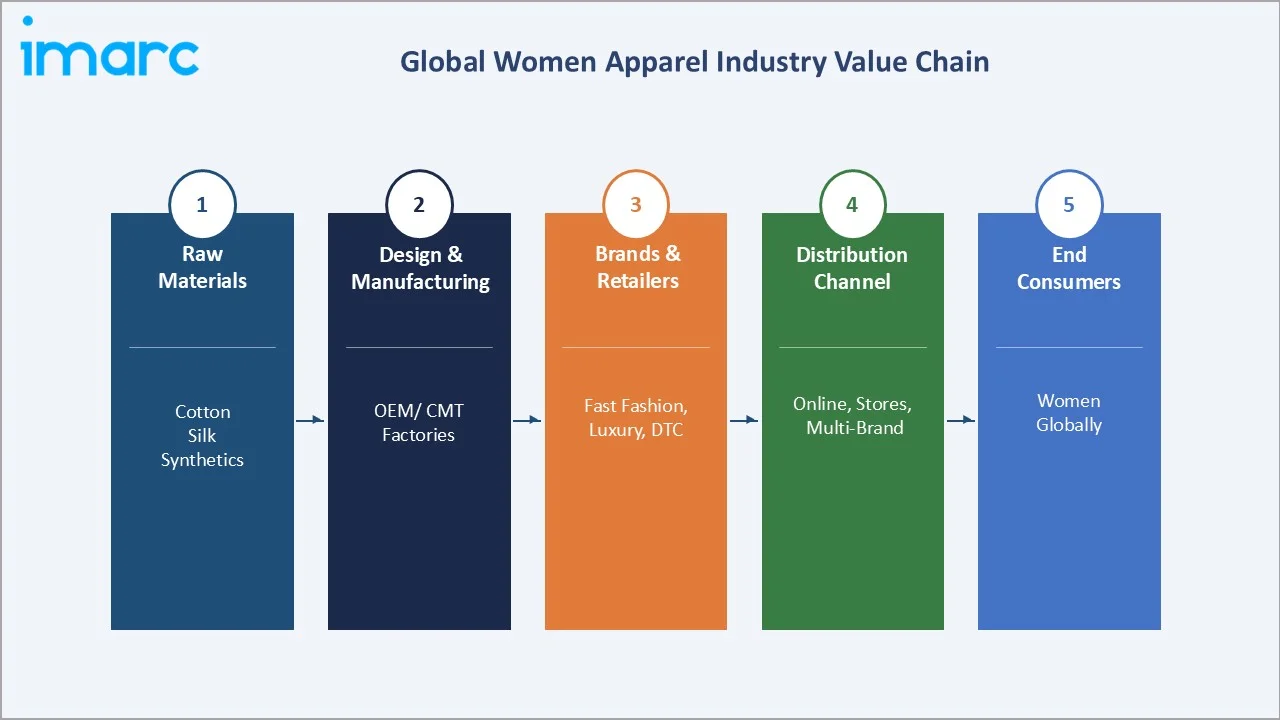

Industry Value Chain Analysis

The women apparel industry value chain spans multiple interconnected stages, from raw material procurement to end consumer delivery. Each stage is populated by specialized operators whose performance directly influences product quality, cost competitiveness, speed to market, and sustainability credentials.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Cotton, silk, polyester, nylon suppliers; natural fiber cooperatives (India, China, Bangladesh) |

|

Yarn & Fabric Manufacturing |

Textile mills (Arvind Ltd., Vardhman Group); synthetic fabric producers |

|

Garment Design & Manufacturing |

OEM/CMT factories (Bangladesh, Vietnam, China, India); design studios (Italy, France, USA) |

|

Brands & Retailers |

Inditex (Zara), H&M, Lululemon, LVMH, Gap, PVH, Fast Retailing (Uniqlo) |

|

Distribution Channels |

Exclusive brand outlets, multi-brand retail, online platforms (Amazon, ASOS, Myntra) |

|

End Consumers |

Women globally across age groups, income levels, and lifestyle preferences |

Europe and North America's dominant positions are anchored by the strength of their brand and retail stages of the value chain. In contrast, Asia Pacific's competitive advantage lies in cost-efficient manufacturing and raw material sourcing. The increasing focus on near-shoring manufacturing to reduce lead times and carbon footprints is reshaping the geographic distribution of production in the women's apparel value chain.

Technology Landscape in the Women Apparel Industry

Advanced Fabric and Material Innovation

Innovative textile science is enabling manufacturers to develop high-performance, sustainable, and functional fabric formulations for women's apparel without compromising aesthetic appeal or comfort. Bio-based polyester, recycled nylon (e.g., ECONYL from Aquafil), and smart fabrics with moisture-wicking, temperature-regulating, and antimicrobial properties witnessed high growth over the past few years.

AI-Driven Design, Personalization, and Sizing

Artificial intelligence is transforming how women's apparel brands design, develop, and deliver products. AI-powered trend forecasting tools reduce design cycle time by 30-40%, while companies that successfully leverage AI in merchandising can boost gross margins by up to 5% while reducing inventory levels by 10–15%.

Omnichannel Retail Technology and Social Commerce

The integration of augmented reality (AR) virtual try-ons, RFID inventory management, and real-time demand analytics is reshaping the women's apparel retail experience. Social commerce platforms are rapidly expanding, with TikTok Shop expected to sustain double-digit e-commerce growth through 2029. Its sales are projected to exceed $20 billion in 2026 and surpass $30 billion by 2028.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Tops and Dresses |

32.3% |

2025 |

|

Season |

Winterwear |

🔒 |

2025 |

|

Distribution Channel |

Supermarkets and Hypermarkets |

35.9% |

2025 |

|

Region |

Europe |

39.8% |

2025 |

By Product Type

To access detailed market analysis, Request Sample

Tops and dresses dominate with a 32.4% market share (2025), reflecting their status as the most versatile and frequently purchased women's apparel category. Within the segment, bottom wear experienced a notable 18.6% share in 2025, driven by post-pandemic social event normalcy and the athleisure-meets-formal trend. New product launches featuring sustainable fabrics and body-inclusive designs are further expanding consumer reach and purchase frequency within this leading segment.

By Season

Winter wear dominates with a 38.4% share (2025), reflecting the largest seasonal consumer spending window globally. Heavy outerwear, layering pieces, and holiday-season fashion collections drive high transaction volumes during autumn and winter retail cycles, with Europe and North America contributing the largest volumes.

All Season Wear represents 33.0% of the market share (2025), reflecting growing consumer preference for versatile, transitional apparel investment pieces that can be layered and styled across multiple seasons. Premium all-season collections are recording the fastest growth within this segment, driven by value-seeking behavior among middle to upper-income women consumers.

Regional Market Insights

Europe's market leadership (39.8% share, 2025) is deeply entrenched, supported by world-renowned fashion capitals in Paris, Milan, and London, high consumer spending on clothing and footwear (Europeans spend an average of EUR 490 per year on clothing), and a sophisticated, brand-conscious female consumer base. The German fashion industry generates approximately EUR 2.3 billion in gross value added annually, while Italy and France collectively drive premium women's apparel demand across the luxury and accessible luxury segments.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Major Players |

|

Europe |

39.8% |

Luxury demand, fashion hubs (Paris, Milan), and high disposable income |

EU Textile Sustainability Regulations |

Inditex, H&M, LVMH, Primark |

|

North America |

22.4% |

Fast fashion culture, strong e-commerce, and DTC brand growth |

FABRIC Act, de minimis rule review |

Gap, PVH, Lululemon, Victoria's Secret |

|

Asia Pacific |

20.6% |

Urbanization, rising middle class, young demographics |

BIS standards (India), GB textile standards (China) |

Fast Retailing, Shein, Mango, Westside |

|

Middle East and Africa |

10.4% |

Modest fashion demand, growing retail infrastructure |

Halal fashion compliance, import policies |

Zara, H&M, Max Fashion, Splash |

|

Latin America |

6.8% |

Middle-class expansion, digital adoption |

Local content requirements (Brazil) |

Renner, C&A, Riachuelo |

Asia Pacific is the clear growth engine with the fastest regional expansion trajectory. India's women's apparel market is projected to grow at double-digit rates through 2028, driven by urbanization, a young population demographic, and the rapid expansion of organized retail chains. China's domestic women's fashion market continues to evolve toward premium and international branded categories, supported by rising disposable incomes and digital-first consumer journeys. The Asia Pacific market for women's apparel represents the single largest incremental growth opportunity through 2034.

Competitive Landscape

The global women apparel market exhibits a moderately fragmented competitive structure. The top five players - Inditex, H&M, Fast Retailing, LVMH, and Lululemon - collectively account for approximately 10-12% of global market revenues in 2025. The remainder is distributed among thousands of regional and national fashion brands, DTC digital-native labels, luxury houses, and independent operators.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Inditex S.A. |

Zara, Massimo Dutti, Bershka, Pull&Bear, Stradivarius, Oysho |

Market Leader |

Fast fashion model, global supply chain speed |

|

H&M Group |

H&M, COS, Arket, Weekday |

Market Leader |

Affordable fashion, a wide global store network |

|

Fast Retailing Co. Ltd. |

Uniqlo, GU |

Strong Challenger |

Functional apparel, Japanese quality positioning |

|

LVMH |

Louis Vuitton, Dior, Celine, Fendi, Loewe, Givenchy |

Luxury Leader |

Premium brand equity, high ASP, aspirational positioning |

|

Lululemon Athletica |

Lululemon |

Fast-Growing Challenger |

Athleisure segment leadership, community-based marketing |

|

Gap Inc. |

Gap, Banana Republic, Old Navy, Athleta |

Established Player |

Diversified brand portfolio, North America retail depth |

|

PVH Corp. |

Calvin Klein, Tommy Hilfiger |

Strong Challenger |

Global brand licensing, premium casual positioning |

|

Hanesbrands |

Champion, Hanes, Bonds |

Innerwear Specialist |

activewear and basics apparel dominance, mass market distribution |

The fragmented structure drives intense competition, with players differentiating through fast product cycles, branding, and omnichannel strategies. Increasing competition from digital-native and sustainable fashion brands is further pushing incumbents to innovate and adapt to evolving consumer preferences.

Key Company Profiles

Inditex S.A. (Zara)

Inditex is the world's largest fashion retailer by global revenue, operating over 5,500 stores across 93 countries as of 2024. The company reported revenue of approximately EUR 38.6 Billion in fiscal 2024, with Zara as the flagship brand generating 72.5% of total revenues. Women's apparel is the core revenue driver across all Inditex brand portfolios.

- Product Portfolio: Zara, Massimo Dutti, Bershka, Pull&Bear, Stradivarius, Oysho (lingerie & sportswear).

- Recent Developments: Inditex expanded its RFID-enabled real-time inventory management to all Zara women's stores globally by early 2025, improving stock accuracy to 99%. The brand launched a Pre-Owned collection, enabling in-store clothing resale across major European markets in 2024.

- Strategic Focus: Digital-first customer experience, sustainable material integration (target: 100% sustainable fabrics by 2030), near-shore manufacturing expansion in Portugal and Morocco.

H&M Group

H&M Group operates more than 4,300 stores globally across 77 markets and reported net sales of approximately SEK 234.6 Billion in 2024. The H&M brand is the company's flagship women's fashion label, complemented by premium brands COS, & Other Stories, and Arket, targeting higher-income female consumers.

- Product Portfolio: H&M, COS, Monki, Weekday, & Other Stories, Arket, AFOUND (discount).

- Recent Developments: H&M partnered with Circularise in 2025 to implement digital product passports for women's garments, enabling end-to-end supply chain transparency. The group launched a dedicated rental service for premium women's formal wear in Nordic markets in late 2024.

- Strategic Focus: Portfolio brand premiumization, digital integration, textile-to-textile recycling investment (committed EUR 1 Billion in sustainability initiatives through 2030).

Fast Retailing Co., Ltd. (Uniqlo)

Fast Retailing is Japan's largest apparel retailer and the parent company of Uniqlo, GU, and Theory. The company achieved group revenues of JPY 3.1 trillion (approximately USD 21 billion) in fiscal 2024. Uniqlo's LifeWear philosophy - offering essential, high-quality everyday clothing - resonates strongly with women consumers seeking functional and timeless fashion.

- Product Portfolio: Uniqlo (women's basics, HEATTECH, AIRism lines), GU (fast fashion, younger consumers), Theory (premium workwear for women).

- Recent Developments: Uniqlo opened 100+ net new stores globally in 2024, with significant focus on North America and Southeast Asia expansion. The brand's collaboration with JW Anderson for women's collections achieved sellout status across 12 markets in 2024.

- Strategic Focus: Functional fabric innovation (HEATTECH, AIRism upgrades), Southeast Asia retail expansion, premium women's category deepening through Theory brand scaling.

LVMH (Louis Vuitton, Christian Dior, Celine)

LVMH is the world's leading luxury group, with its Fashion & Leather Goods segment generating EUR 42.2 billion in revenues in 2024. Women's ready-to-wear collections across Louis Vuitton, Dior, Givenchy, Celine, and Loewe represent the core creative and financial engines of the group's fashion division. LVMH holds a market capitalization of USD 282.97 billion as of 2025.

- Product Portfolio: Louis Vuitton (RTW, leather goods), Christian Dior (couture & RTW), Celine, Givenchy, Loewe, Fendi - all featuring significant women's apparel and accessories collections.

- Recent Developments: LVMH invested EUR 500 Million in French fashion production capacity in 2024 as part of its "Savoir-Faire" artisanal manufacturing commitment, directly benefiting women's couture and RTW lines. Creative director appointments at Dior and Givenchy in 2024-2025 have reinvigorated women's runway collection momentum.

- Strategic Focus: Exclusive product scarcity and heritage storytelling, digital luxury experience via LV's own e-commerce expansion, China luxury market recovery strategy through flagship boutique reinvestment.

Market Concentration Analysis

The global women apparel market exhibits moderate fragmentation overall, with the top five players, Inditex, H&M Group, Fast Retailing, LVMH, and Lululemon, collectively controlling approximately 10-12% of global market revenues in 2025.

The luxury women's apparel sub-segment is notably more concentrated than the mass market segment. The top three luxury groups (LVMH, Kering, and Richemont) command approximately 45-50% of the luxury women's fashion market, reflecting the segment's brand-driven, heritage-centric nature. In contrast, the fast fashion segment - while dominated by Inditex and H&M - is experiencing growing competition from digitally native disruptors, including Shein, which has captured an estimated 18% share of the global fast fashion market as of 2025.

Consolidation activity has accelerated across the women's apparel industry. Notable M&A transactions include Authentic Brands Group's portfolio expansions and private equity interest in premium athleisure brands. Strategic brand acquisitions, licensing deals, and DTC brand partnerships are expected to drive 10-15 significant transactions annually through 2034, particularly targeting sustainable fashion innovators and technology-enabled apparel platforms.

Investment & Growth Opportunities

Fastest Growing Segments

Online distribution (CAGR ~7.8%), sustainable and circular fashion, and premium athleisure represent the three highest-growth investment vectors in the global women apparel market through 2034. Investment in AI-driven personalization infrastructure, virtual sizing technology, and recommerce platforms is a particularly attractive vector.

Emerging Market Expansion

Asia Pacific and the Middle East & Africa present the most compelling geographic investment opportunities. According to CareEdge Ratings, India’s apparel retail market is set for strong growth over the next five years, with the segment projected to reach nearly ₹16 lakh crore (USD 193 Billion) by FY30. Entry via franchise partnerships, joint ventures with local fashion retailers, and DTC digital brand strategies are the preferred modes of market entry.

Venture & Strategic Investment Trends

With over 3,800 apparel brands emerging in India, the sector is increasingly focused on sustainability and personalization, attracting approximately USD 1.43 billion in funding over the past decade. Key investment themes include AI-powered styling platforms, sustainable textile recycling technology, body scanning and virtual fitting room infrastructure, and recommerce marketplace platforms.

- Key growth bets: sustainable material technology (e.g., mycelium leather, bio-based nylon), AI-driven demand forecasting, and regional franchise licensing in fast-growing Middle East and South Asian markets.

- ESG-aligned investors are increasingly targeting sustainable manufacturing and ethical sourcing initiatives within the women's apparel supply chain, reflecting the sector's growing importance in institutional investor ESG portfolios.

- Strategic PE interest in premium women's athleisure brands and luxury accessible labels remains elevated, particularly in North America and Western Europe, where brand multiples remain attractive relative to growth trajectories.

Future Market Outlook (2034)

The global women apparel market is poised for sustained, broad-based growth through 2034, anchored by digital transformation, product premiumization, and geographic expansion into high-growth emerging markets. From a projected base of USD 1,068.20 Billion in 2025, the market is forecast to reach USD 1,412.50 Billion by 2034, representing absolute incremental value addition of approximately USD 344.30 Billion over the decade - reflecting the women apparel market's enduring consumer relevance and commercial resilience.

Technological disruptions, including AI-driven personalization, digital product passports, AR virtual try-ons, and blockchain-enabled supply chain traceability, are expected to materially reshape operational economics across the value chain. Brands achieving 20-30% cost efficiency gains through AI-powered demand forecasting and inventory optimization will gain a decisive competitive advantage in high-volume markets by 2028-2030.

The next decade will witness a fundamental bifurcation of the women apparel market: a value-driven mass-market segment increasingly served by digital-native brands and recommerce platforms, and a premiumization wave pushing middle-class consumers toward accessible luxury and investment-piece fashion. Brands that successfully navigate this bifurcation, delivering quality, inclusivity, sustainability, and digital engagement simultaneously, will capture disproportionate market share growth through 2034.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 180 industry participants in 2024-2025, comprising women's apparel brand executives, retail buyers, textile manufacturers, supply chain managers, and end consumers across Europe, North America, Asia Pacific, and the Middle East. Qualitative and quantitative primary data were systematically triangulated to validate market sizing estimates and growth projections.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, regulatory filings, trade publications (Vogue Business, Business of Fashion, WWD - Women's Wear Daily), industry databases, and publicly available financial data. Over 280 secondary sources were reviewed across the IMARC research process. Data from Eurostat, OECD, World Bank, ILO, and national retail associations were incorporated to validate macroeconomic and demand-side assumptions.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, female workforce participation data, urbanization indices, consumer expenditure surveys, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty, supply chain disruptions, and regulatory changes. The CAGR of 3.06% represents the base-case forecast scenario for the 2026-2034 period.

Women Apparel Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Tops and Dresses, Bottom Wear, Innerwear and Sleepwear, Coats, Jackets and Suits, Ethnic Wear, Others |

| Seasons Covered | Summer Wear, Winter Wear, All Season Wear |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Exclusive Stores, Multi-Brand Retail Outlets, Online Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Inditex S.A., H&M Group, Fast Retailing Co. Ltd., LVMH, Lululemon Athletica, Gap Inc., PVH Corp., Hanesbrands, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the women apparel market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global women apparel market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the women apparel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Women Apparel Market Report

The global women apparel market was valued at USD 1,068.2 Billion in 2025 and is projected to reach USD 1,412.5 Billion by 2034, growing at a CAGR of 3.06%.

The women apparel market is expected to grow at a CAGR of 3.06% during the forecast period 2026-2034, reflecting steady demand across both retail and e-commerce channels globally.

Tops and dresses are the largest segment with a 32.4% market share in 2025, supported by their versatility, high purchase frequency, and broad consumer appeal across age groups.

Winter wear is the largest seasonal segment, accounting for a 38.4% market share in 2025, driven by strong cold-weather apparel demand, seasonal wardrobe renewal cycles, and premium outerwear collections across key markets in Europe and North America.

Europe is the dominant region, holding a 39.8% market share in 2025, driven by high-income consumers, fashion hubs in Paris and Milan, and strong organized retail infrastructure.

Asia Pacific is the fastest-growing region, driven by urbanization, rising middle-class incomes, young demographics, and the rapid expansion of organized fashion retail in India and China.

Key drivers include rising female workforce participation, social media and influencer-driven fashion demand, e-commerce expansion, premiumization trends, and the growing athleisure and sustainable fashion segments.

Sustainable fashion, social commerce, inclusive sizing, athleisure convergence, and AI-driven personalization are the fastest-growing trends through 2034.

The leading companies include Inditex (Zara), H&M Group, Fast Retailing (Uniqlo), LVMH, Lululemon Athletica, Gap Inc., PVH Corp. (Calvin Klein, Tommy Hilfiger), and Hanesbrands.

Online stores represent the fastest-growing distribution channel at an estimated CAGR of 7.8% (2026-2034), driven by AI personalization, virtual try-ons, and social commerce platforms like TikTok Shop and Instagram.

High-growth investment opportunities include sustainable and circular fashion technology, premium athleisure brands, AI-powered styling platforms, and emerging market fashion retail expansion in India, Saudi Arabia, and Southeast Asia.

Key challenges include supply chain disruptions, sustainability compliance costs, intense competition from fast-fashion disruptors like Shein, counterfeit fashion proliferation, and rising last-mile delivery costs in e-commerce.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade