Women's Health Market Size, Share, Trends and Forecast by Age Group, Application, Distribution Channel, and Region, 2026-2034

Global Women’s Health Market Size, Share, Trends & Forecast (2026-2034)

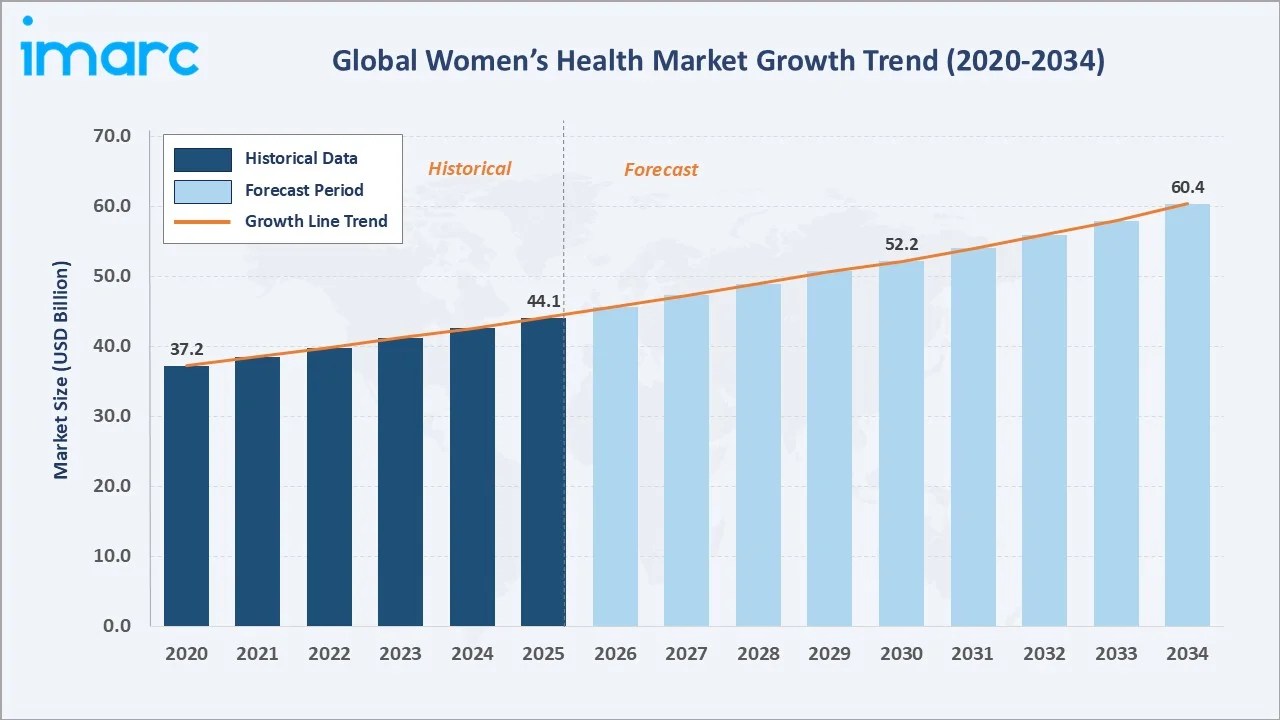

The global women’s health market size reached USD 44.1 Billion in 2025 and is projected to reach USD 60.4 Billion by 2034, exhibiting a CAGR of 3.45% during 2026-2034. Rising global awareness of gender-specific health conditions, expanding access to reproductive and preventive care, and the growing prevalence of post-menopausal disorders are the primary forces driving market growth.

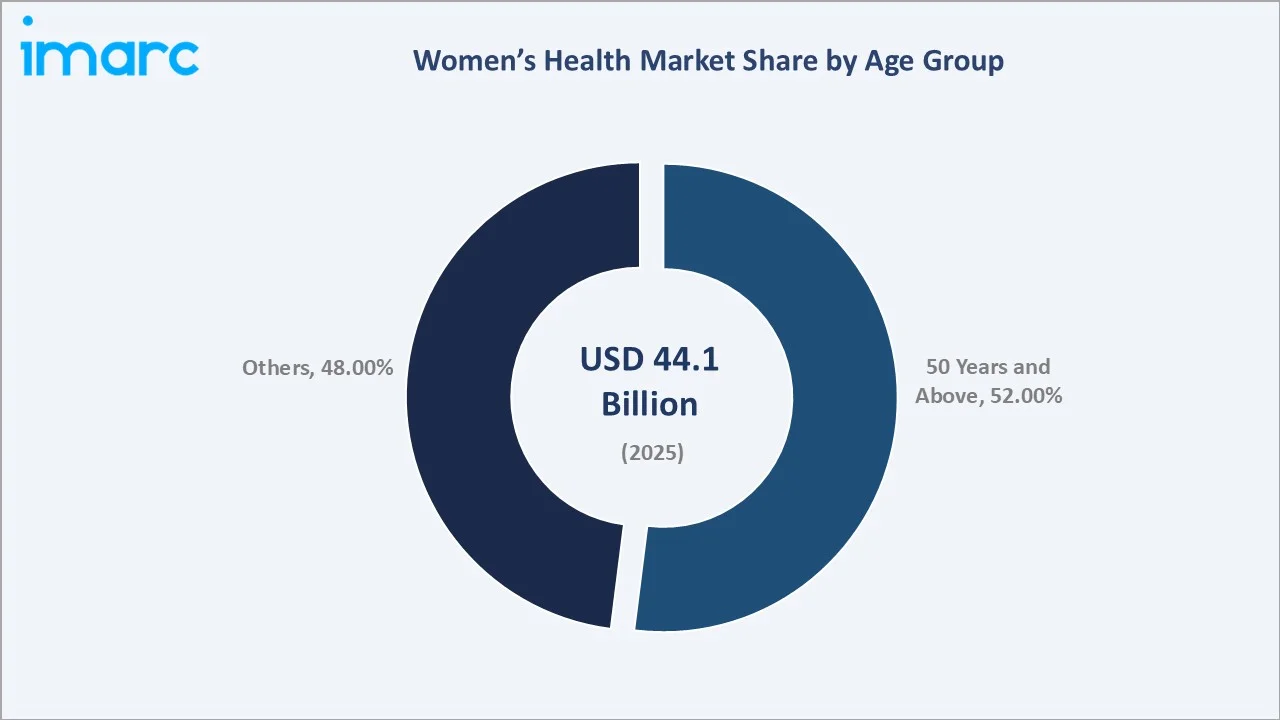

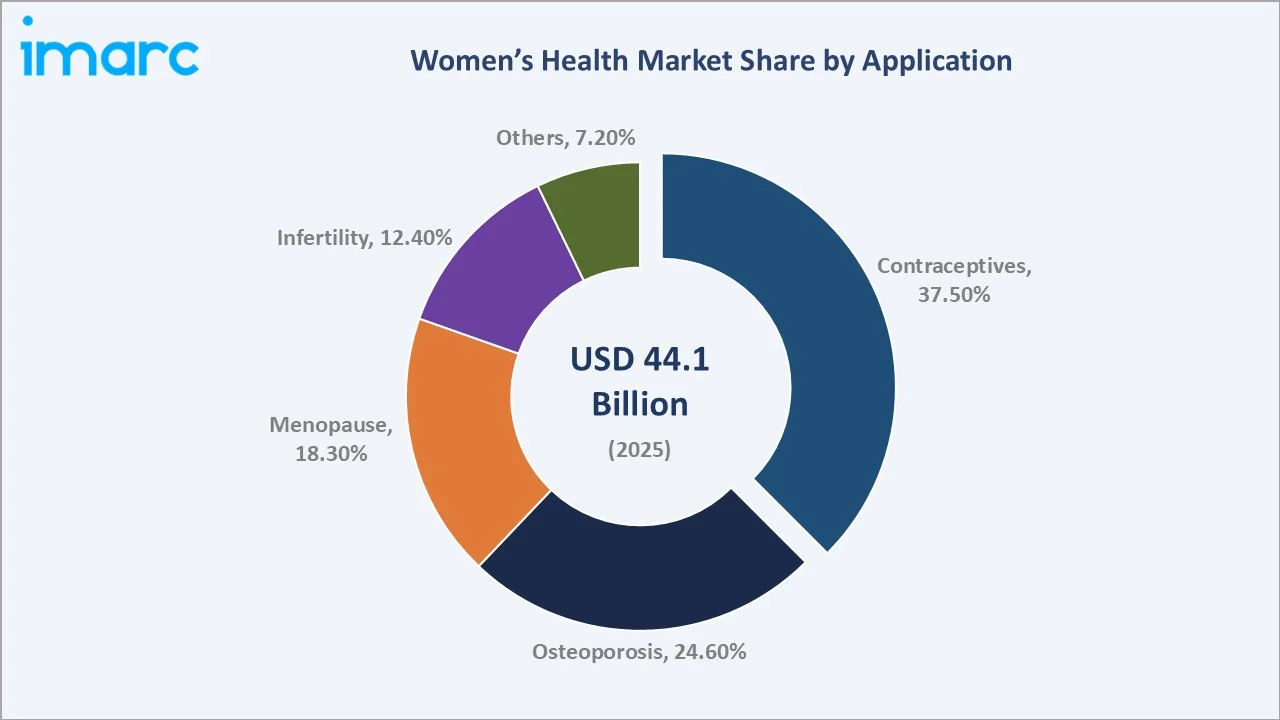

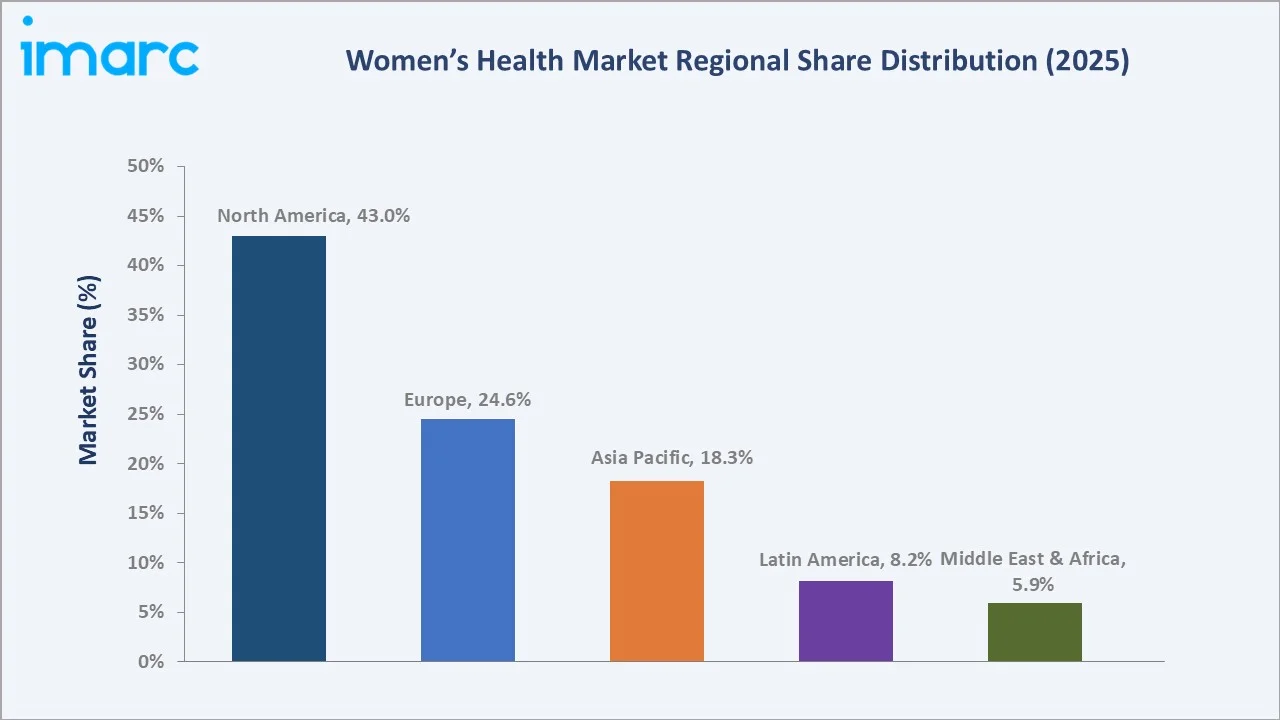

The 50 Years and Above age group commands a dominant 52.0% share in 2025. Contraceptives lead the application segment at 37.5%, while North America holds a 43.0% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 44.1 Billion |

|

Forecast Market Size (2034) |

USD 60.4 Billion |

|

CAGR (2026-2034) |

3.45% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (43.0% share, 2025) |

|

Leading Age Group |

50 Years and Above (52.0%, 2025) |

|

Leading Application |

Contraceptives (37.5%, 2025) |

The global women’s health market growth trajectory from 2020 through 2034, with historical expansion to USD 44.1 Billion in 2025, reflects consistent demand driven by demographic aging and healthcare investment, while the forecast to USD 60.4 Billion captures accelerating innovation in diagnostics, therapeutics, and digital health platforms.

To get more information on this market, Request Sample

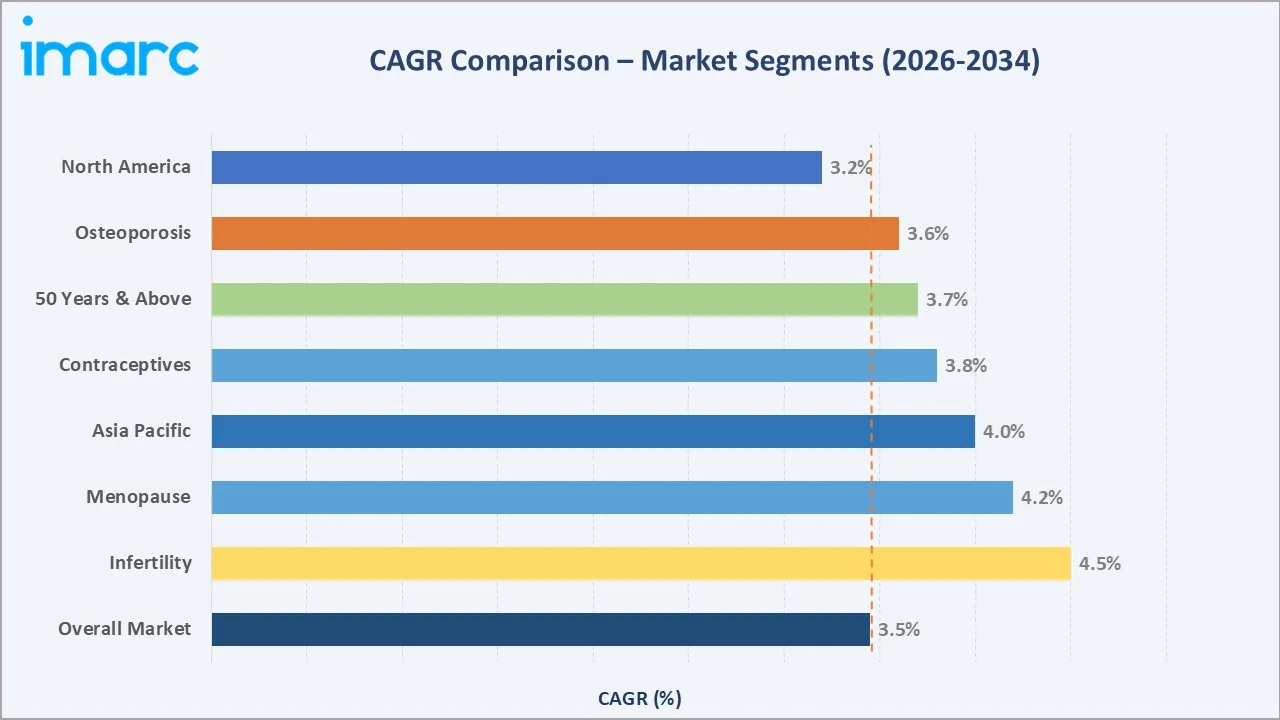

The CAGR trajectories across key application and age group sub-segments, with infertility at ~4.5% CAGR and menopause at ~4.2% CAGR, are the fastest-growing categories within the global women’s health industry analysis through 2034.

Executive Summary

The global women’s health market is on a sustained growth trajectory from USD 44.1 Billion in 2025 to USD 60.4 Billion by 2034. Women’s health encompasses diagnostics, therapeutics, medical devices, and digital platforms addressing conditions unique to or disproportionately affecting women across all life stages.

The 50 Years and Above age group dominates at 52.0% in 2025, driven by post-menopausal osteoporosis, menopause management, and age-related reproductive health concerns. Contraceptives lead the application segment at 37.5%, reflecting the large, recurring global demand for family planning solutions.

North America commands 43.0% of the global market in 2025, supported by advanced healthcare infrastructure, strong R&D investment, and high awareness of women’s health conditions. Asia Pacific, at 18.3%, represents the fastest-growing region driven by expanding healthcare access and population scale.

Key Market Insights

|

Insight |

Data |

|

Leading Age Group |

50 Years and Above – 52.0% share (2025) |

|

Leading Application |

Contraceptives – 37.5% share (2025) |

|

Second Application |

Osteoporosis – 24.6% share (2025) |

|

Leading Region |

North America – 43.0% revenue share (2025) |

|

Second Region |

Europe – 24.6% revenue share (2025) |

|

Top Companies |

Abbott, AbbVie Inc., Bayer AG, Pfizer Inc., Hologic, Inc., Amgen Inc., Novo Nordisk A/S, F. Hoffmann-La Roche Ltd |

Key Analytical Observations Expanding On The Above Data:

- The 50 Years and Above cohort, with 52.0% in 2025, dominates because of the convergence of post-menopausal conditions including osteoporosis, vasomotor symptoms, and cardiovascular risk, all requiring long-term, recurring therapeutic management.

- Contraceptives, with 37.5% in 2025, lead the application segment because of the broad global base of reproductive-age women requiring consistent access to both hormonal and non-hormonal family planning solutions, underpinned by strong government and NGO procurement.

- North America’s 43.0% dominance in 2025 reflects multiple structural forces: the highest per-capita healthcare spending globally, concentrated presence of leading pharmaceutical companies, and the most advanced regulatory environment for women’s health drug approvals.

- Europe, with 24.6% in 2025, benefits from universal healthcare systems that ensure broad access to women’s health therapeutics, combined with strong EMA regulatory frameworks supporting consistent product approvals.

Global Women’s Health Market Overview

Women’s health encompasses the specialized medical products, therapeutics, diagnostics, and healthcare services addressing conditions that are unique to or disproportionately affect women, spanning reproductive health, maternal care, gynecologic oncology, hormonal disorders, and age-related conditions.

The global ecosystem integrates pharmaceutical manufacturers, medical device companies, diagnostic laboratories, digital health platforms, hospital systems, retail and online pharmacy distribution channels, regulatory authorities, and government and NGO health agencies working collectively to deliver comprehensive care.

Market Dynamics

To evaluate market opportunities, Request Sample

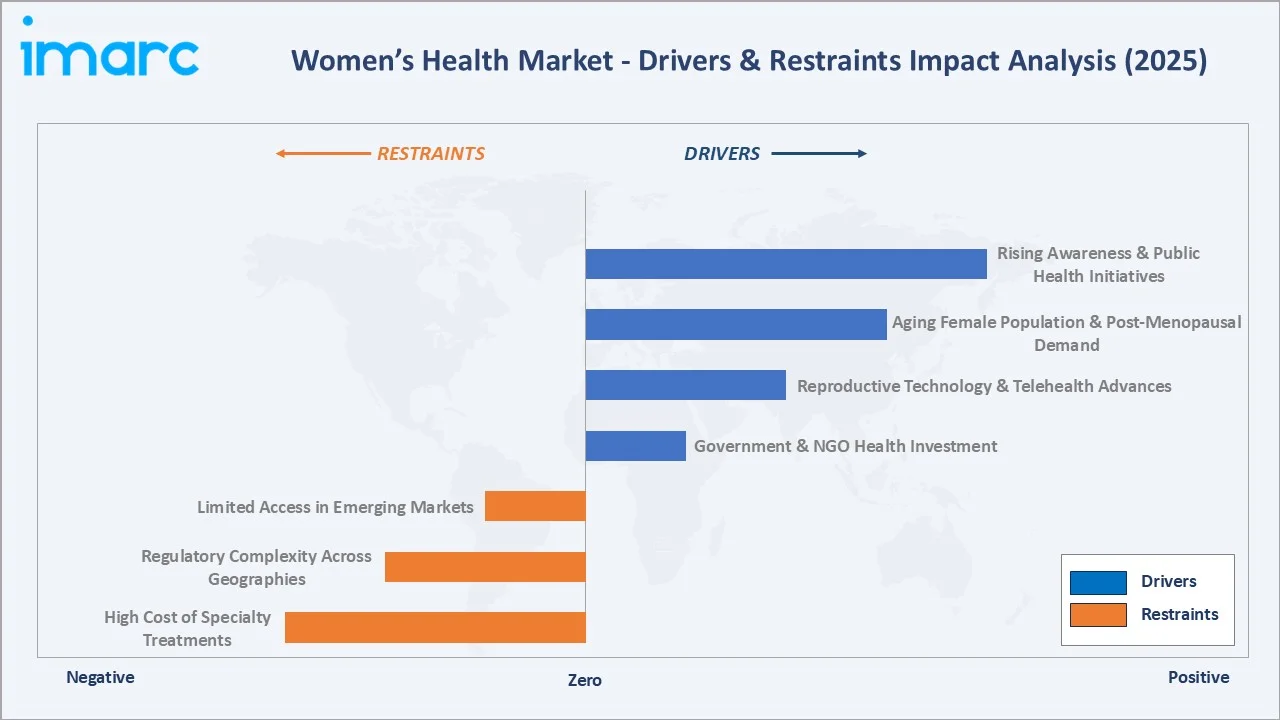

Market Drivers

- Rising Awareness and Public Health Initiatives: Governing bodies and NGOs globally are prioritizing women’s health, leading to improved screening, diagnosis, and treatment programs for breast cancer, cervical cancer, osteoporosis, and menopause, directly expanding demand for specialized products.

- Aging Female Population and Post-Menopausal Demand: The global demographic shift toward aging populations is increasing the proportion of women in the 50+ bracket, driving demand for osteoporosis treatments, menopausal therapies, and cardiovascular health products tailored to post-menopausal women. By 2030, 1 in 6 people in the world will be aged 60 years or over. At this time the share of the population aged 60 years and over will increase from 1 billion in 2020 to 1.4 billion.

- Advances in Reproductive Technology and Telehealth: Innovations in assisted reproductive technologies, AI-driven fertility diagnostics, and telehealth platforms are broadening access to care, particularly in infertility management, and enabling patient-centric treatment pathways.

Market Restraints

- High Cost of Specialty Treatments and Diagnostics: Advanced women’s health therapeutics, including biological agents for endometriosis and fertility treatments, command premium price points that limit adoption in price-sensitive markets and underinsured patient populations.

- Regulatory Complexity Across Geographies: Varied regulatory frameworks and approval timelines across the US, EU, Asia Pacific, and emerging markets create market entry barriers, delaying access to innovative therapies and increasing compliance costs.

Market Opportunities

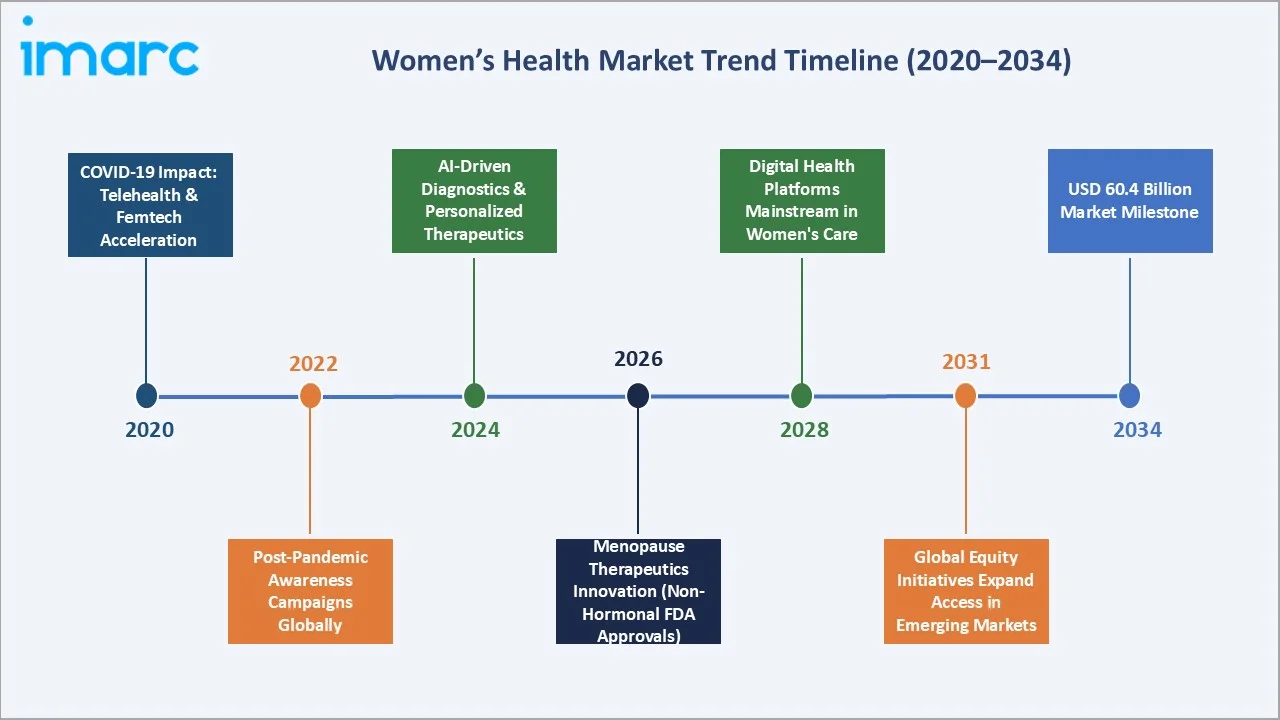

- Digital Health and FemTech Expansion: The rapid proliferation of mobile health applications for menstrual tracking, fertility monitoring, menopause management, and chronic condition support is creating substantial new channels for patient engagement and data-driven care. In January 2026, Qatar Science & Technology Park (QSTP), part of Qatar Foundation, has partnered with Merck to launch a FemTech accelerator aimed at advancing innovation in women’s health. The initiative focuses on supporting up to 30 high-potential startups developing cutting-edge solutions using technologies such as AI, robotics, and materials science. The program is designed to help these startups scale by providing mentorship, market access, and opportunities to pilot their solutions within Qatar and across the MENA region.

- Emerging Markets Healthcare Infrastructure Growth: Government investment in healthcare infrastructure across Asia Pacific, Latin America, and Africa is expanding women’s health service access, generating growing demand for both branded and generic therapeutics.

Market Challenges

- Gender Gap in Clinical Research: Historical underrepresentation of women in clinical trials has resulted in evidence gaps for female-specific drug dosing and efficacy, creating ongoing challenges in developing optimally targeted women’s health therapeutics.

- Limited Access in Rural and Low-Income Settings: Infrastructure gaps in developing economies restrict access to contraceptives, maternal care, and screening programs, creating persistent unmet need despite overall market growth.

Emerging Market Trends

1. FemTech and AI-Driven Personalized Women’s Healthcare

Artificial intelligence and machine learning integration into women’s health platforms is transforming diagnostics and treatment personalization. AI-driven tools for early cancer detection, PCOS diagnosis, and fertility cycle prediction are improving clinical outcomes and reducing time to diagnosis.

2. Non-Hormonal Menopause Therapeutics Innovation

Regulatory approvals of novel non-hormonal therapies for vasomotor symptoms of menopause represent a paradigm shift, addressing the large population of women who are unable or unwilling to use hormone replacement therapy, and significantly expanding the addressable market for menopause management.

3. Expansion of Reproductive Health Telemedicine

Telehealth adoption in obstetrics and gynecology, accelerated by COVID-19, has become a permanent feature of women’s healthcare delivery. Remote consultations for contraceptive management, fertility counseling, and prenatal care are improving access in underserved geographies.

4. Biosimilars Expanding Access to Biological Therapies

The entry of biosimilars for established biological women’s health treatments, including hormonal therapies and fertility drugs, is materially reducing treatment costs and expanding patient access in both developed and emerging markets, supporting volume growth.

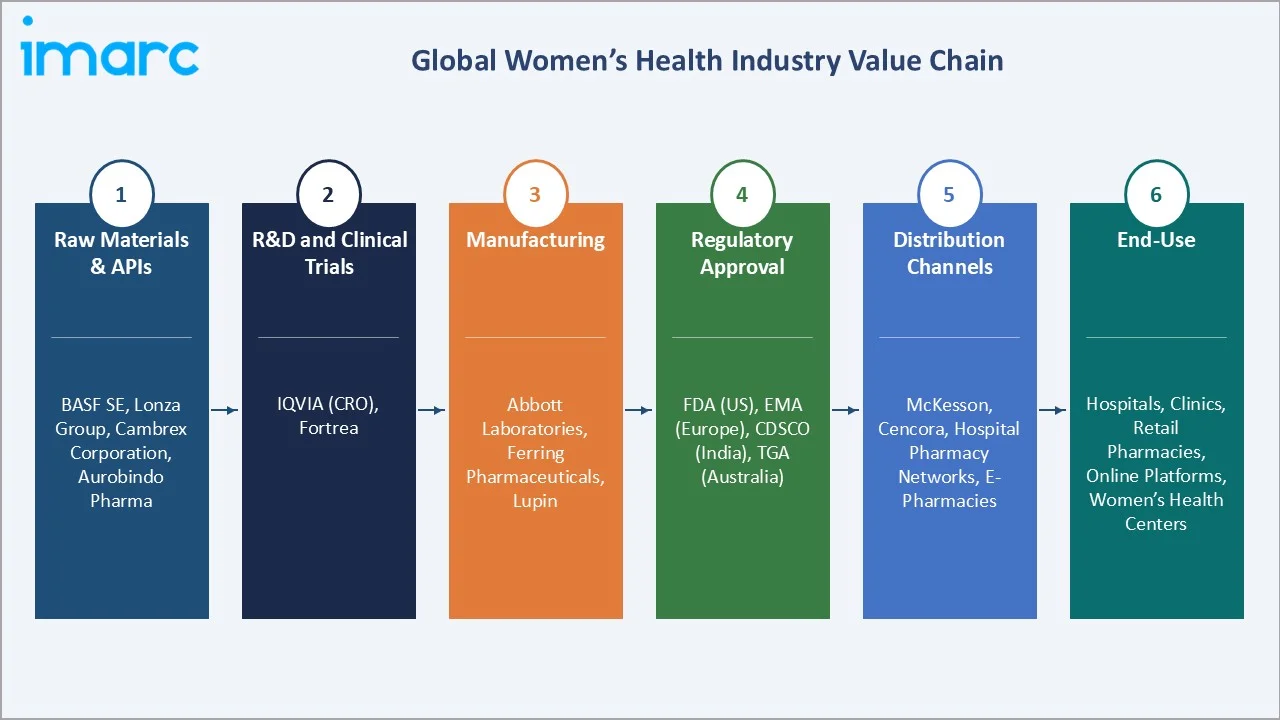

Industry Value Chain Analysis

The women’s health value chain spans six stages from raw material and API supply through end-user patient care. R&D and manufacturing capture the highest value-add margins, while distribution logistics and regulatory navigation generate significant investment requirements for market participants.

|

Stage |

Key Players / Examples |

|

Raw Materials & APIs |

BASF SE, Lonza Group, Cambrex Corporation, Aurobindo Pharma |

|

R&D and Clinical Trials |

IQVIA (CRO), Fortrea |

|

Manufacturing |

Abbott Laboratories, Ferring Pharmaceuticals, Lupin |

|

Regulatory Approval |

FDA (US), EMA (Europe), CDSCO (India), TGA (Australia) |

|

Distribution Channels |

McKesson, Cencora, hospital pharmacy networks, e-pharmacies |

|

End Use |

Hospitals, clinics, retail pharmacies, online platforms, women’s health centers |

Integrated pharmaceutical companies with captive R&D capabilities and established regulatory relationships achieve faster time-to-market advantages. Vertical integration from API synthesis through branded formulation enables cost structures and quality controls that support sustainable competitive positioning.

Technology Landscape in the Women’s Health Industry

Diagnostics Technology: AI-Enhanced Imaging and Genomics

AI-powered mammography and cervical cytology imaging platforms are materially improving early detection accuracy. Next-generation sequencing (NGS) for BRCA1/2 and hereditary cancer risk assessment is becoming standard of care in oncology-adjacent women’s health segments.

Therapeutics Innovation: Biologics and Small Molecule Advances

Targeted biological therapies for endometriosis, uterine fibroids, and polycystic ovary syndrome (PCOS) are expanding the treatment landscape. Novel GnRH antagonists and selective progesterone receptor modulators represent significant therapeutic advances in hormonal condition management.

Digital Health and Wearable Technology Integration

Connected wearable devices for fertility monitoring, menstrual cycle tracking, and menopause symptom management are generating large-scale real-world evidence data sets. Integration with EHR systems is enabling more informed clinical decision-making and personalized therapeutic protocols.

Drug Delivery Innovation: Long-Acting Contraceptives and IUDs

Advances in intrauterine device (IUD) technology, subdermal implants, and extended-cycle oral contraceptives are improving patient compliance and expanding the contraceptive market. Next-generation drug delivery systems are enabling precise hormonal release profiles.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Age Group | 50 Years and Above | 52.0% | 2025 |

| Application | Contraceptives | 37.5% | 2025 |

| Distribution Channel | Hospital Pharmacies | 🔒 | 2025 |

| Region | North America | 43.0% | 2025 |

By Age Group

To access detailed market analysis, Request Sample

The 50 Years and above age group commands a 52.0% majority share in 2025 owing to the convergence of multiple high-prevalence chronic conditions in post-menopausal women, including osteoporosis, cardiovascular disease, and hormonal deficiency disorders, each requiring long-term pharmaceutical management.

The others category, representing women below 50 years, accounts for 48.0% in 2025. This cohort drives demand across contraceptives, infertility treatments, maternal health products, and management of reproductive conditions such as endometriosis, PCOS, and uterine fibroids.

By Application

Contraceptives dominate the application segment at 37.5% in 2025, driven by the large global population of reproductive-age women, strong government procurement programs, and diversified product portfolios spanning hormonal, barrier, and long-acting reversible contraception (LARC) methods.

Osteoporosis, at 24.6% in 2025, represents the second-largest application owing to the high global prevalence of post-menopausal bone density loss, with bisphosphonates, denosumab, and emerging anabolic therapies generating significant recurring prescription demand. Menopause (18.3%), Infertility (12.4%), and Others (7.2%) complete the application mix.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

43.0% |

Advanced healthcare infrastructure; high R&D investment; strong regulatory approval pipeline |

|

Europe |

24.6% |

Universal healthcare access; EMA approvals; aging population driving menopause & osteoporosis demand |

|

Asia Pacific |

18.3% |

Large population base; government health investment; rising awareness & access to contraceptives |

|

Latin America |

8.2% |

Brazil & Mexico healthcare expansion; growing contraceptive access programs; NGO-driven awareness |

|

Middle East & Africa |

5.9% |

GCC healthcare modernization; maternal health investment; growing private healthcare sector |

North America’s 43.0% market dominance in 2025 reflects the most structurally favorable combination of healthcare investment intensity, pharmaceutical innovation output, and patient awareness of women’s health conditions of any global region. The United States alone accounts for most of the North American market revenue. The female population is projected to grow from an estimated 167.51 million in 2021 to 172.45 million by 2027, thereby increasing the demand of women’s health in the market.

Europe, with 24.6% in 2025, benefits from universal healthcare systems ensuring broad patient access to women’s health products across all income levels. Government-funded national screening programs for breast and cervical cancer and strong NPO-led awareness campaigns further support demand.

Competitive Landscape

The global women’s health market is moderately concentrated, with large diversified pharmaceutical companies holding leading positions through broad product portfolios spanning contraceptives, hormone therapies, osteoporosis treatments, and fertility products, while specialty players compete in targeted therapeutic niches.

|

Company |

Key Products |

Position |

Strategic Focus |

|

Abbott |

Fertility and pregnancy diagnositics, Resyniv, Femoston |

Leader |

Diagnostics + therapeutics |

|

AbbVie Inc. |

Orilissa, Lupron, Elahere |

Leader |

Endometriosis & oncology |

|

Bayer AG |

Mirena, Kyleena, Yasmin, Yasminelle |

Leader |

Contraceptives & gynecology |

|

Pfizer Inc. |

Premarin, Prempro/Premphase |

Leader |

Menopause & bone health |

|

Hologic, Inc. |

Affirm Breast Biopsy Guidance System, ATEC Breast Biopsy System, Aptima HPV Assays, NovaSure Endometrial Ablation |

Challenger |

Diagnostics & screening |

|

Amgen Inc. |

Prolia, XGEVA |

Challenger |

Bone health biologics |

|

Novo Nordisk A/S |

Vagifem, Activelle, Novofem, Trisequens, Estrofem |

Emerging |

Hormonal & metabolic |

|

F. Hoffmann-La Roche Ltd |

Elecsys PAPP-A, Elecsys free βhCG, Harmony Prenatal Kit, Elecsys CMV IgG Avidity |

Leader |

Prenatal diagnostics & molecular screening |

Key players include Abbott, AbbVie Inc., Bayer AG, Pfizer Inc., Hologic, Inc., Amgen Inc., Novo Nordisk A/S, F. Hoffmann-La Roche Ltd, and others.

Key Company Profiles

Abbott

Abbott is a globally diversified healthcare company with a significant presence in women’s health diagnostics and fertility testing. Abbott’s diagnostics division offers advanced immunoassay-based pregnancy, fertility hormone, and sexually transmitted infection testing platforms deployed across hospital, clinic, and point-of-care settings.

- Product Portfolio: Fertility and pregnancy diagnostics

- Recent Developments: In May 2022, Abbott partnered with Women as One to launch an initiative aimed at increasing the participation of underrepresented physicians in leading clinical trials. The program focuses on equipping female and minority cardiologists with the skills and training needed to engage in clinical research and improve diversity in trial leadership.

- Strategic Focus: Abbott’s strategy leverages its diagnostics scale to support early detection and preventive care in women’s health, with investments in connected health platforms for remote monitoring.

AbbVie Inc.

AbbVie is a research-based pharmaceutical company with leading women’s health assets in endometriosis, uterine fibroids, and fertility. Its FDA-approved Orilissa (elagolix) is the first new oral treatment for endometriosis in over a decade, addressing a condition affecting approximately 10% of reproductive-age women globally.

- Product Portfolio: Orilissa, Lupron, Elahere.

- Recent Developments: In September 2025, AbbVie begun construction on a $70 million expansion of its biologic’s facility in Worcester, Massachusetts, aiming to strengthen its manufacturing and R&D capabilities in the United States. The project will add new biologics manufacturing areas along with a three-story building that includes laboratory, warehouse, and office space. This expansion is intended to boost production capacity and support the development of current and next-generation treatments, particularly in oncology and immunology.

- Strategic Focus: AbbVie’s women’s health strategy centers on building the leading endometriosis and uterine fibroid franchise through clinical differentiation and broad patient access programs.

Bayer AG

Bayer AG is one of the world’s leading women’s health companies, with a comprehensive contraceptive portfolio spanning oral contraceptives, intrauterine devices (IUDs), and injectable formulations that collectively address the global family planning market. Bayer’s women’s health division maintains presence in over 100 countries.

- Product Portfolio: Mirena, Kyleena, Yasmin, Yasminelle.

- Recent Developments: In February 2026, Bayer, in collaboration with VML Health, launched a global campaign aimed at challenging the widespread tendency to normalize pain and discomfort in women’s health. The initiative, titled Anything but Normal, seeks to shift perceptions around symptoms that are often dismissed as routine.

- Strategic Focus: Bayer’s strategy differentiates on breadth of contraceptive portfolio and long-acting reversible contraception (LARC) leadership, targeting both premium branded and access-focused market segments globally.

Pfizer Inc.

Pfizer maintains a significant women’s health presence through its established franchises in menopausal hormone therapy and osteoporosis treatment. Premarin, one of the world’s most recognized hormone therapy brands, and Reclast, a leading bisphosphonate for osteoporosis, anchor Pfizer’s women’s health portfolio.

- Product Portfolio: Premarin, Prempro/Premphase.

- Recent Developments: In January 2026, The Pfizer Foundation announced a $10 million, three-year investment to expand its breast cancer initiative into Kenya and Ethiopia, aiming to improve access to timely diagnosis, treatment, and care. The funding will support local partners, AMPATH in Kenya and Innovations in Healthcare, alongside the Clinton Health Access Initiative, in Ethiopia, to strengthen healthcare systems and address barriers that delay or limit access to care.

- Strategic Focus: Pfizer’s women’s health strategy focuses on sustaining its established menopause and bone health franchise value while exploring partnership-driven entry into emerging women’s health therapeutic areas.

Market Concentration Analysis

The global women’s health market is moderately concentrated at the global level, with the top five companies collectively holding an estimated 30-35% of total global market revenue. Large pharmaceutical companies including AbbVie, Bayer, Pfizer, and Abbott hold diversified portfolios spanning multiple therapeutic categories.

Consolidation through M&A is an active feature of the market, with large pharmaceutical companies acquiring specialty women’s health companies to access differentiated assets in fertility, endometriosis, and digital health. Specialty players with FDA-approved novel agents command premium acquisition valuations.

Investment & Growth Opportunities

Fastest-Growing Segments

Infertility at ~4.5% CAGR through 2034 is the highest-growth application segment, driven by rising rates of delayed childbearing, increasing diagnosis of PCOS and endometriosis, and expanding access to assisted reproductive technologies globally.

Emerging Markets

Asia Pacific at ~4.0% CAGR is the fastest-growing region for women’s health through 2034, with China’s two-child policy legacy, India’s expanding healthcare infrastructure investment, and Southeast Asia’s growing middle-class healthcare spending driving demand for both branded and generic women’s health products.

Venture & Investment Trends

FemTech investment is attracting significant venture capital, with AI-powered fertility diagnostics, menopause management platforms, and women’s preventive health applications receiving growing funding. Strategic partnerships between pharmaceutical companies and digital health startups are accelerating product innovation pipelines.

Future Market Outlook (2026-2034)

The global women’s health market is forecast to expand from USD 44.1 Billion in 2025 to USD 60.4 Billion by 2034 at a CAGR of 3.45%. This growth reflects non-discretionary demand characteristics tied to demographic aging and reproductive health needs.

Three technological forces will most significantly shape the women’s health industry through 2034. AI-enhanced diagnostics enabling earlier and more accurate detection of gynecologic cancers will expand addressable markets. Non-hormonal therapeutic innovation for menopause will open a significant underserved population.

Research Methodology

Primary Research

Primary research encompassed structured interviews with women’s health industry stakeholders including senior commercial managers, gynecologists, reproductive endocrinologists, pharmacists, and NGO health program directors. Primary data validated market sizing, segment shares, and technology adoption timelines.

Secondary Research

Key secondary sources include WHO Women’s Health Report, UNFPA State of World Population Report, Centers for Disease Control and Prevention reproductive health data, FDA drug approval databases, EMA product authorization records, IQVIA market intelligence reports, and peer-reviewed publications in leading obstetrics and gynecology journals.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating demographic data, disease prevalence rates, healthcare expenditure trends, and historical market evolution patterns. Scenario analysis was performed to account for macroeconomic uncertainty.

Women's Health Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Age Group Covered |

|

| Applications Covered | Contraceptives, Osteoporosis, Menopause, Infertility, Others |

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Abbott, AbbVie Inc., Bayer AG, Pfizer Inc., Hologic, Inc., Amgen Inc., Novo Nordisk A/S, F. Hoffmann-La Roche Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the women’s health market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global women’s health market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the women’s health industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Women's Health Market Report

The global women’s health market reached USD 44.1 Billion in 2025, reflecting consistent demand growth driven by aging demographics, increasing awareness, and expansion of treatment options across all major therapeutic categories.

The market is projected to reach USD 60.4 Billion by 2034, growing at a CAGR of 3.45% during 2026-2034, driven by aging populations, infertility treatment expansion, and digital health platform integration.

The 50 Years and Above age group leads with a 52.0% share in 2025, driven by the high prevalence of post-menopausal osteoporosis, menopause-related conditions, and cardiovascular health disorders requiring sustained therapeutic management.

Contraceptives lead at 37.5% in 2025, representing the largest, most recurring demand segment driven by global reproductive-age populations, government-funded family planning programs, and diverse product availability.

North America commands a dominant 43.0% market share in 2025, driven by the advanced US healthcare system, high per-capita pharmaceutical spending, and the concentrated presence of leading women’s health innovators.

Infertility is the fastest-growing application at ~4.5% CAGR through 2034, driven by rising rates of delayed motherhood, increasing diagnostic rates for PCOS and endometriosis, and expanding ART technology access globally.

Leading companies include Abbott, AbbVie Inc., Bayer AG, Pfizer Inc., Hologic, Inc., Amgen Inc., Novo Nordisk A/S, F. Hoffmann-La Roche Ltd, and others.

Key applications include contraceptives, osteoporosis management, menopause therapies, infertility treatments, endometriosis and uterine fibroid management, cervical and breast cancer screening, and maternal health products.

FemTech platforms for fertility tracking, menopause management, and chronic condition monitoring are creating new patient engagement channels, improving adherence, and generating real-world data that is informing more personalized clinical care pathways.

Osteoporosis represents the second-largest application at 24.6% in 2025. Post-menopausal estrogen decline accelerates bone density loss, creating large, sustained demand for bisphosphonates, biological agents such as denosumab, and emerging anabolic therapies.

Asia Pacific, at 18.3% in 2025, is growing at ~4.0% CAGR through 2034. China’s expanding healthcare infrastructure, India’s large reproductive-age population, and government investments across Southeast Asia are driving growing demand for both innovative and generic women’s health products.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)