Xenon Gas Market Size, Share, Trends and Forecast by Distribution Channel, End-User, and Region, 2026-2034

Xenon Gas Market Size and Share:

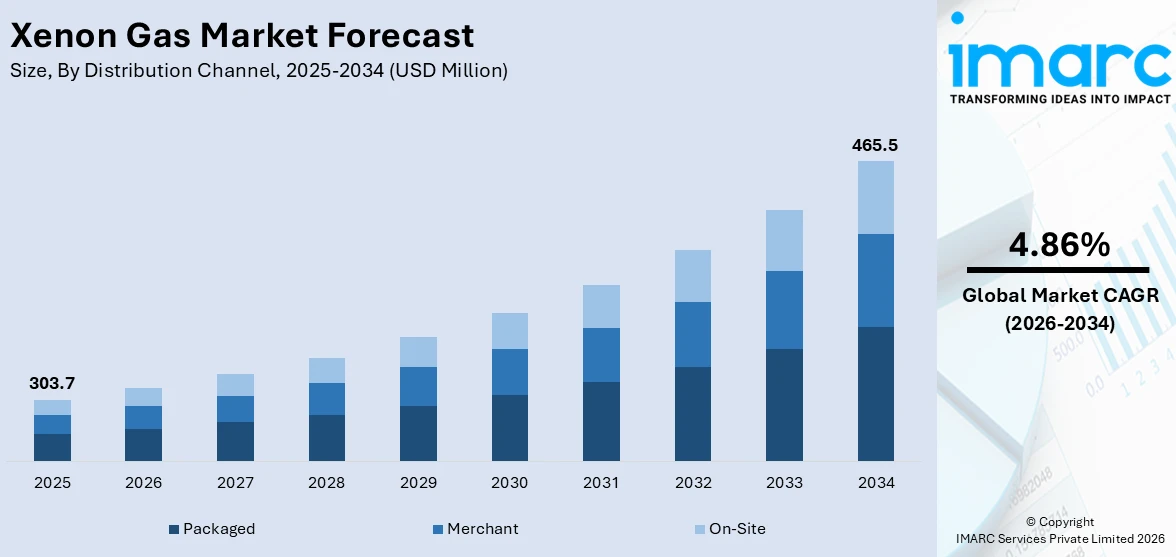

The global xenon gas market size was valued at USD 303.7 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 465.5 Million by 2034, exhibiting a CAGR of 4.86% during 2026-2034. Asia Pacific currently dominates the market, holding a significant market share of over 34.7% in 2025. The increasing demand for xenon gas due to the expanding semiconductor manufacturing, increasing satellite launches requiring ion propulsion, growing adoption in medical imaging and anesthesia, advancements in high-intensity discharge (HID) lighting, and ongoing research in nuclear energy applications, are some of the major factors positively impacting the xenon gas market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034 |

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 303.7 Million |

|

Market Forecast in 2034

|

USD 465.5 Million |

| Market Growth Rate 2026-2034 | 4.86% |

The market is significantly influenced by the increasing adoption of xenon gas in semiconductor lithography processes, particularly for advanced chip manufacturing. Additionally, the growing research in quantum computing and atomic clocks, where xenon serves as a cooling medium, further supports the market demand. Also, the increasing usage of xenon gas for medical applications is a significant growth-inducing factor for the market. A recent study published on January 15, 2025, by scientists from Washington University School of Medicine and Mass General Brigham has enhanced xenon gas's potential for treating Alzheimer's. The study demonstrated that xenon gas reduces neuroinflammation and brain atrophy in mouse models by penetrating the blood-brain barrier and activating protective microglial responses, leading to improved cognitive functions. This breakthrough is driving interest in xenon-based therapeutics for neurodegenerative diseases. In line with this, expanding the use of high-speed photography and nuclear detection technologies also contributes to the xenon gas market growth.

To get more information on this market Request Sample

The United States xenon gas market is witnessing significant growth driven by the rising demand for next-generation satellite propulsion systems, where xenon-ion thrusters offer efficiency for long-duration space missions. Furthermore, expanding semiconductor fabrication, driven by domestic investments in chip production, fuels the need for xenon in deep ultraviolet lithography. On August 8, 2024, EFC Gases and Advanced Materials announced a USD 210 Million investment to build a specialty gases and chemicals plant in McGregor, Texas, aiming to meet the growing demand from the global chip industry. The facility will produce fluorochemicals for semiconductor etching and deposition chamber cleaning, as well as fill cylinders with rare gases like krypton, xenon, and neon. Besides this, the increasing utilization of MRI spectroscopy and neuroimaging is fostering growth in the healthcare sector. Additionally, heightened investment in nuclear research and radiation detection technologies is accelerating consumption.

Xenon Gas Market Trends:

Semiconductor Manufacturing Expansion

The global semiconductor industry is experiencing a transformative period of expansion, creating unprecedented demand for xenon gas across fabrication facilities worldwide. Xenon plays an indispensable role in critical semiconductor manufacturing processes, including deep ultraviolet lithography for advanced node production, plasma etching for creating high-aspect-ratio vertical structures in 3D NAND memory chips, and ion implantation for doping semiconductor materials. The surge in need for semiconductors, driven by artificial intelligence (AI) applications, 5G/6G communications infrastructure, autonomous vehicles, and advanced computing systems, has prompted industry leaders to significantly increase global production capacity. According to the Semiconductor Industry Association, global semiconductor sales reached USD 630.5 billion in 2024, representing a 19.1% increase compared to 2023 and marking the industry's highest-ever yearly total. This robust growth directly translates to increased consumption of ultra-high purity xenon gas, as manufacturers require stringent purity levels exceeding 99.999% for advanced fabrication processes. The xenon gas market growth is further amplified by the industry's technological progression toward smaller node sizes and more complex chip architectures, which demand even higher gas purity and more sophisticated etching processes. Major semiconductor manufacturers are expanding fabrication capacity, with substantial investments concentrated in the United States, South Korea, Taiwan, and China, creating geographically distributed demand for xenon supplies.

Electric Propulsion Revolution Transforming Satellite Industry Xenon Requirements

The aerospace and satellite industries are undergoing a fundamental shift toward electric propulsion systems, positioning xenon gas as a critical enabler of next-generation space missions and commercial satellite operations. Xenon-based ion thrusters and Hall-effect thrusters have become the propulsion technology of choice for satellite station-keeping, orbit transfer, and deep space exploration missions due to their superior efficiency compared to traditional chemical propulsion systems. The proliferation of satellite mega-constellations for global broadband internet coverage, Earth observation, and communications services has created explosive demand for xenon propellant. SpaceX's Starlink constellation, OneWeb, and Amazon's Project Kuiper represent ambitious programs deploying thousands of satellites, each requiring propulsion systems for orbit maintenance and end-of-life deorbiting. While some operators have explored alternative propellants like krypton or iodine to address xenon's high cost and limited availability, xenon remains preferred for missions requiring optimal performance and reliability. In 2025, EFC Gases & Advanced Materials received a USD 5 million NASA contract for xenon gas reprocessing services, demonstrating the space agency's commitment to efficient xenon utilization and recovery. The growing sophistication of satellite technology, combined with increased launch cadence and longer mission durations, ensures continued strong demand for high-purity xenon in aerospace applications throughout the forecast period.

Medical Innovation and Neuroprotective Applications Expanding Xenon Therapeutic Potential

Xenon gas is experiencing a renaissance in medical applications, transitioning from its established role as a safe anesthetic to emerging applications in neuroprotection, neurological disease treatment, and advanced diagnostic imaging. The gas's unique properties, including its ability to cross the blood-brain barrier, excellent safety profile, minimal cardiovascular effects, and rapid onset and offset of action, make it an attractive therapeutic agent for various medical conditions. Xenon has been used clinically as an anesthetic in Europe and other regions for years, offering advantages over traditional volatile anesthetics including better hemodynamic stability and faster patient recovery. Beyond anesthesia, groundbreaking research is revealing xenon's neuroprotective mechanisms, particularly its ability to competitively block N-methyl-D-aspartate (NMDA) receptors, which play a critical role in neuronal damage following hypoxic-ischemic injury, stroke, and traumatic brain injury. Xenon's neuroprotective effects have been demonstrated in combination therapies with therapeutic hypothermia for treating neonatal hypoxic-ischemic encephalopathy, showing synergistic benefits in protecting developing brains. Medical imaging represents another growing application area, with xenon-enhanced computed tomography (CT) providing valuable functional information about cerebral blood flow following traumatic brain injury, requiring duration of gas inhalation for the procedure. The most exciting recent development involves xenon's potential in treating Alzheimer's disease and other neurodegenerative conditions. In January 2025, researchers from Mass General Brigham and Washington University School of Medicine published groundbreaking findings in Science Translational Medicine demonstrating that xenon gas inhalation reduced brain atrophy, repressed neuroinflammation, and increased protective microglial states in mouse models of Alzheimer's disease.

Xenon Gas Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global and regional levels for 2026-2034. Our report has categorized the market based on distribution channel and end-user.

Analysis by Distribution Channel:

- Packaged

- Merchant

- On-Site

Packaged leads the market with around 54.7% of market share in 2025. Packaged distribution channel primarily serves industries and applications where small to moderate quantities of xenon are required, such as in research laboratories, medical facilities, and small-scale manufacturing units. Packaged xenon is typically supplied in high-pressure gas cylinders or liquid containers, making it accessible and convenient for end-users who require the gas in manageable amounts. This distribution channel's popularity stems from its ease of handling, transportation, and storage, providing a versatile solution for customers not requiring bulk volumes. The demand in this segment is driven by the diverse applications of xenon. The flexibility of packaged xenon allows it to cater to a broad spectrum of industries, underlining its dominance in the market. Its scalability, from small to large enterprises, ensures a consistent demand, reinforcing its position as the most substantial segment in the distribution landscape.

Analysis by End-User:

Access the comprehensive market breakdown Request Sample

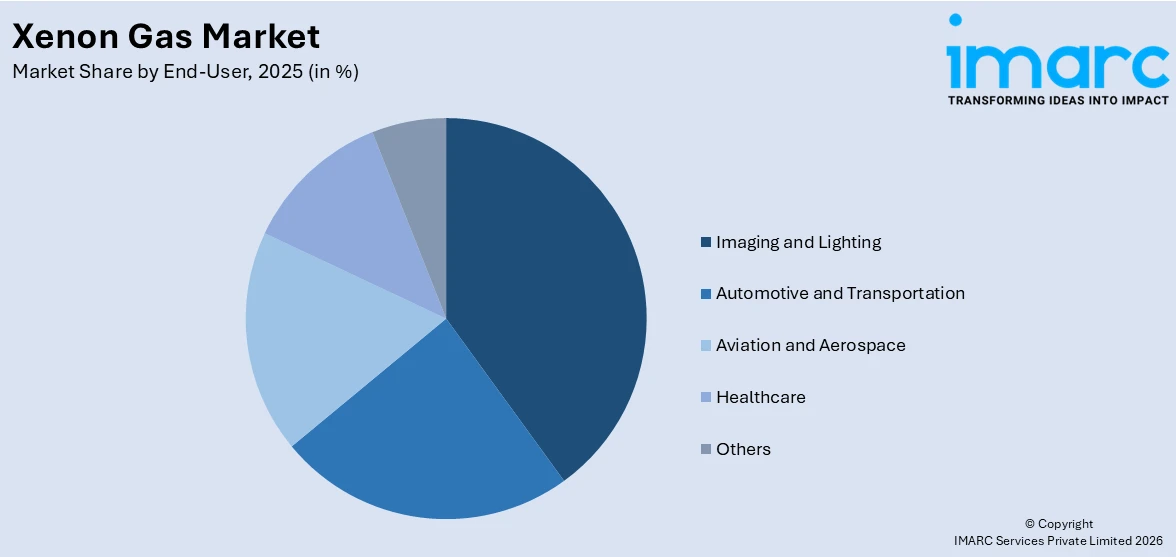

- Imaging and Lighting

- Automotive and Transportation

- Aviation and Aerospace

- Healthcare

- Others

Imaging and lighting lead the market with around 36.8% of market share in 2025, driven by the gas's exceptional properties, such as high light output and color temperature, which are ideal for high-intensity discharge lamps used in film projection, automotive headlights, and architectural lighting. The demand is further amplified by the medical imaging sector, where xenon is used in CT imaging to enhance the quality of images. Its application extends to ultraviolet light sources for sterilization and in xenon arc lamps, which provide sunlight simulation for weathering tests of materials. The versatility of xenon in providing bright, white, or ultraviolet light supports its widespread use in various lighting applications, from entertainment industry projectors to specialized uses in scientific research, where precise and high-quality light sources are crucial. The growth in this segment is propelled by technological advancements, increasing safety standards, and the rising demand for energy-efficient lighting solutions.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

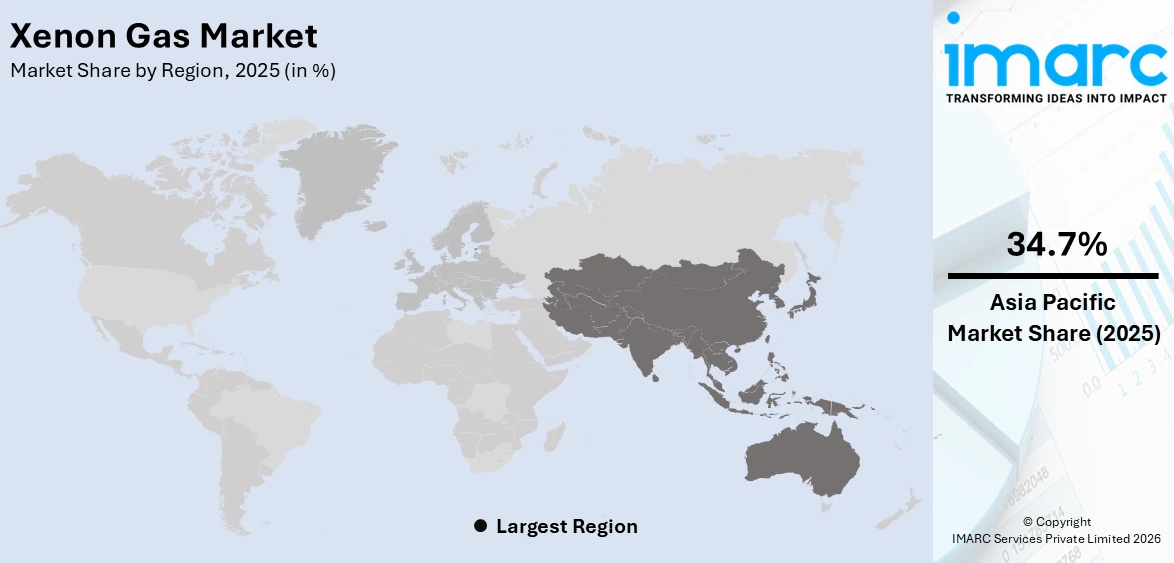

- Asia Pacific

- North America

- Europe

- Middle East and Africa

- Latin America

In 2025, Asia Pacific accounted for the largest market share of over 34.7% due to the rapid industrialization and expansion of the electronics, manufacturing, and aerospace sectors, especially in countries like China, Japan, and South Korea. China’s strategic push to develop rare gas recovery methods and expand air separation units may stabilize supply. The booming semiconductor industry, coupled with increasing investments in space research and satellite communication, fuels the demand for this gas. The region’s aerospace sector is also investing heavily in satellite propulsion technologies, increasing demand for xenon-based ion thrusters. Moreover, the region's growing focus on enhancing healthcare infrastructure contributes to the rising use of xenon in medical imaging and anesthesia applications. The market is further propelled by the strategic initiatives of local governments to support technological advancements and industrial growth, making Asia Pacific a crucial hub for the supply chain.

Key Regional Takeaways:

North America Xenon Gas Market Analysis

North America represents a strategically critical region for xenon gas demand, characterized by world-leading semiconductor manufacturing capabilities, pioneering aerospace innovation, and cutting-edge medical research infrastructure. The United States is experiencing a semiconductor manufacturing renaissance catalyzed by the CHIPS and Science Act, which has unleashed over half-a-trillion dollars in private-sector investments aimed at tripling domestic chip manufacturing capacity by 2032. This unprecedented manufacturing expansion directly drives demand for ultra-high purity xenon gas used in advanced lithography, plasma etching, and ion implantation processes critical to producing leading-edge semiconductors. Major fabrication facilities operated by Intel, Texas Instruments, Samsung, and TSMC in the region require consistent, high-volume supplies of xenon meeting stringent purity specifications. The North American aerospace sector represents another substantial demand driver, with the region serving as headquarters for major satellite operators including SpaceX, OneWeb, and emerging players developing constellation systems for global communications coverage. Electric propulsion systems using xenon enable these satellites to maintain precise orbits and perform end-of-life deorbiting maneuvers efficiently. NASA and commercial space companies rely on xenon for both robotic exploration missions and satellite operations, with the space agency actively investing in xenon reprocessing and recycling technologies to optimize utilization. North America's medical research institutions are pioneering novel xenon applications, particularly in neuroprotection and treatment of neurodegenerative diseases, potentially opening significant new demand channels as clinical trials advance toward commercialization. The region benefits from well-established rare gas supply infrastructure, with major industrial gas companies operating air separation units capable of producing and purifying xenon.

United States Xenon Gas Market Analysis

The United States holds a substantial share of the North American xenon gas market with 87.80% in 2025. The market is supported by its leadership across multiple high-technology sectors. The domestic semiconductor industry represents the primary demand driver, with American companies commanding a major of global chip revenues despite producing only a fraction of worldwide manufacturing capacity, a disparity the CHIPS Act aims to address. Major U.S.-based chipmakers operate advanced fabrication facilities utilizing xenon in excimer lasers for deep ultraviolet lithography and in plasma etching processes for creating complex three-dimensional structures in memory chips. The resurgence of domestic semiconductor manufacturing, with major new fabs under construction in Arizona, Texas, Ohio, and New York, will substantially increase xenon consumption as these facilities ramp to volume production. The U.S. aerospace sector's voracious appetite for xenon stems from both government missions and commercial satellite operations, with electric propulsion systems becoming standard across the industry. In 2024, GE Aerospace effectively showcased a one-megawatt hybrid electric propulsion system under a $5.1 million R&D contract from the U.S. Army Combat Capabilities Development Command (DEVCOM) Army Research Laboratory (ARL). Within the framework of the Applied Research Collaborative Systematic Turboshaft Electrification Project (ARC-STEP) contract, GE Aerospace engaged in research, development, testing, and assessment of a megawatt (MW) class electrified powerplant, which advanced the identification and enhancement of technologies relevant to future Army air vehicle propulsion and military electrified ground vehicles.

Europe Xenon Gas Market Analysis

Europe maintains a substantial presence in the global xenon gas market, distinguished by advanced semiconductor manufacturing capabilities, ambitious space programs, comprehensive environmental regulations, and world-class medical research infrastructure. The region hosts several major semiconductor manufacturing operations, including facilities operated by STMicroelectronics, Infineon, NXP Semiconductors, and ASML. European semiconductor facilities require high-purity xenon for various fabrication processes, with stringent quality standards ensuring consistent product performance. The European Union's commitment to achieving "technological sovereignty" and reducing dependence on external semiconductor suppliers has spurred significant investments in expanding domestic chip production capacity, which will support sustained xenon demand growth. Europe's space sector represents another important consumption driver, with the European Space Agency (ESA) and commercial operators utilizing xenon-based electric propulsion systems for scientific missions and commercial satellites. ESA's BepiColombo mission to Mercury employs xenon ion thrusters for its interplanetary voyage, demonstrating the technology's effectiveness for demanding space exploration applications. European satellite operators increasingly adopt electric propulsion to reduce launch costs and extend mission lifetimes. In 2025, Today, four leading French aerospace companies revealed an ambitious joint research initiative to explore and define a hybrid-electric propulsion system for light aircraft with enhanced propeller efficiency, in line with the decarbonization objectives established by the French Directorate General for Civil Aviation (DGAC) and the nation’s CORAC civil aviation research council. This coalition, consisting of Daher, Safran, Collins Aerospace, and Ascendance, completely endorses national and international plans for reducing carbon emissions in the aviation industry. The project is specifically aimed at aircraft that accommodate 6 to 10 passengers. With 25,000 of these aircraft operating globally, this sector has been marked as a priority to start the ecological transition of air travel by 2027.

Asia Pacific Xenon Gas Market Analysis

Asia Pacific has emerged as the dominant global region for xenon gas consumption, accounting for the largest share of worldwide demand driven by the concentration of semiconductor manufacturing capacity, rapid industrialization, and expanding space programs across the region. Countries including China, Japan, South Korea, and Taiwan host the world's most advanced semiconductor foundries and memory chip production facilities, creating enormous requirements for ultra-high purity xenon used in critical fabrication processes. In June 2025, Air Liquide inaugurated its new state-of-the-art rare gases purification unit in Cheonan, South Korea. The facility now provides high-purity krypton and xenon to major local customers in the electronics industry, utilizing Air Liquide's proprietary technologies and expertise in extreme cryogenics to meet the stringent purity requirements of semiconductor manufacturing. Located strategically near major Korean semiconductor facilities, the plant significantly strengthens rare gases supply chain reliability in this critical manufacturing hub. China's ambitious push toward semiconductor self-sufficiency, supported by substantial government investments and industrial policy incentives, has catalyzed rapid expansion of domestic chip production capacity, further amplifying regional xenon demand.

Latin America Xenon Gas Market Analysis

Latin America represents an emerging and relatively modest market for xenon gas, with demand primarily concentrated in healthcare applications, scientific research institutions, and limited industrial uses. The region's semiconductor manufacturing base remains underdeveloped compared to major global production hubs, resulting in lower industrial demand for xenon in fabrication processes. However, several Latin American countries are investing in upgrading medical infrastructure and expanding access to advanced diagnostic technologies, which may utilize xenon in specialized imaging applications and potentially as an anesthetic in select medical facilities. Research universities and scientific institutions across Brazil, Mexico, Argentina, and Chile explore xenon's unique properties for various laboratory applications and academic studies. The region's aerospace sector remains nascent, with limited domestic satellite manufacturing and operations resulting in minimal xenon demand for propulsion applications.

Middle East and Africa Xenon Gas Market Analysis

The Middle East and Africa region exhibits limited but gradually developing demand for xenon gas, primarily driven by specialized healthcare applications, emerging space programs in select countries, and nascent technology sector development. Several Gulf Cooperation Council nations, particularly the United Arab Emirates, have invested significantly in space technology and satellite programs, creating modest demand for xenon-based electric propulsion systems. The UAE's successful Mars mission and ongoing satellite operations demonstrate the region's growing space capabilities and potential for increased xenon consumption. Saudi Arabia and other Middle Eastern nations are exploring space technology development as part of economic diversification strategies, which may support future xenon demand growth. The region's healthcare sector utilizes xenon in select specialized medical applications, though adoption remains limited compared to more developed markets with established medical infrastructure. South Africa represents the most advanced market within the African continent, with established research institutions exploring xenon applications in various scientific fields. The country's relatively sophisticated medical sector may employ xenon for specialized procedures, though scale remains small.

Competitive Landscape:

The key players in the xenon gas market are actively engaged in expanding their production capacities, enhancing their technological capabilities, and forming strategic partnerships to meet the growing global demand. They are investing in advanced purification and recycling technologies to improve yield and reduce costs, ensuring a stable supply of high-purity xenon gas for various high-tech applications. These companies are also focusing on expanding their global footprint through collaborations, mergers, and acquisitions to strengthen their market presence and to capitalize on emerging opportunities in sectors like aerospace, electronics, and healthcare. Their efforts are geared towards innovation, sustainability, and meeting the stringent quality standards required in diverse end-use industries.

The report provides a comprehensive analysis of the competitive landscape in the xenon gas market with detailed profiles of all major companies, including:

- Airgas

- Air Liquide

- Linde

- Messer

- Praxair

- Air Water

- American Gas

- BASF

- Core Gas

- Matheson Tri-Gas

- Proton Gas

Recent Developments:

- October 2025: Polarean Imaging plc, a leader in commercial-stage medical imaging technology for functional Magnetic Resonance Imaging ("MRI") of the lungs, has announced an expansion of its Representative Agreement with Ascend Imaging LLC ("Ascend Imaging"), allowing coverage to extend into more US states. As part of the expanded agreement, Ascend Imaging will remain a non-exclusive, independent manufacturer's representative, aiding in the promotion and sale of the Company's Xenon MRI platform. The expansion will grow the footprint to 19 US states, an increase from the four states in the initial agreement. Ascend Imaging will keep enhancing Polarean's current commercial team by pinpointing new potential clients, fostering engagement, and aiding in the negotiation and finalization of sales opportunities.

- July 2025: Orbit Fab UK, the business developing satellite refueling platforms in space, revealed two updates today that could pave the way for xenon gas refueling. Orbit Fab secured a €750,000 ($870,000) contract from ESA, through the agency’s Advanced Research in Telecommunications Systems (ARTES) initiative, to collaborate with telecom providers in GEO to incorporate xenon refueling technology.

- May 2025: Lantheus Holdings, Inc, a prominent company in radiopharmaceuticals committed to assisting clinicians in Finding, Fighting, and Following diseases for improved patient outcomes, revealed a definitive contract to transfer its single photon emission computed tomography business to Illuminated Holdings, Inc., the parent organization of SHINE Technologies, LLC. According to the agreement, SHINE will take over Lantheus’ SPECT division, which includes its diagnostic agents (TechneLite® (Technetium Tc 99m generator), NEUROLITE® (Kit for Technetium Tc 99m Bicisate for Injection preparation), Xenon Xe-133 Gas (Xenon Xe-133 Gas), and Cardiolite® (Technetium Tc99m Sestamibi for Injection preparation kit)), the section of the North Billerica, Massachusetts campus that produces Lantheus’ SPECT items, and the SPECT-related operations in Canada.

Xenon Gas Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD, Million Liters |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Distribution Channels Covered | Packaged, Merchant, On-Site |

| End-Users Covered | Imaging and Lighting, Automotive and Transportation, Aviation and Aerospace, Healthcare, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Airgas, Air Liquide, Linde, Messer, Praxair, Air Water, American Gas, BASF, Core Gas, Matheson Tri-Gas, Proton Gas, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the xenon gas market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global xenon gas market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the xenon gas industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Xenon Gas Market Report

The xenon gas market was valued at USD 303.7 Million in 2025.

The xenon gas market is projected to exhibit a CAGR of 4.86% during 2026-2034, reaching a value of USD 465.5 Million by 2034.

The market is driven by increasing demand in aerospace, semiconductors, and medical applications. Its use in satellite ion propulsion, high-performance lighting, and anesthesia enhances market growth. Rising investments in semiconductor manufacturing and advancements in laser technology further boost demand. Additionally, the expansion of nuclear energy and research sectors contributes to market expansion.

Asia Pacific currently dominates the xenon gas market, accounting for a share of 34.7% in 2025. The dominance is fueled by rapid industrialization, growing semiconductor production, and increasing space exploration activities. The region's expanding healthcare sector, along with rising demand for high-intensity lighting and laser applications, further supports market growth.

Some of the major players in the xenon gas market include Airgas, Air Liquide, Linde, Messer, Praxair, Air Water, American Gas, BASF, Core Gas, Matheson Tri-Gas, and Proton Gas, among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)