Acrylic Staple Fiber Price Update: Mixed Movements Across Key Markets in Q1 2026

27-May-2026

Produced through wet spinning of acrylonitrile polymer, acrylic staple fiber delivers soft, resilient filaments rated for colorfastness, mildew resistance, and UV stability at competitive cost. The fiber is cost-competitive against wool. Anchoring global demand are apparel mills, home furnishing converters, industrial nonwoven producers, and filtration equipment manufacturers, while upstream acrylonitrile feedstock costs, energy expenditure during polymerization, and ocean freight dynamics govern acrylic staple fiber prices at any given point in the procurement cycle.

Global Market Overview:

Globally, the acrylic staple fiber industry was valued at USD 3.3 Billion in 2025. Market projections indicate steady growth, with the industry expected to reach USD 4.5 Billion by 2034, with a compound annual growth rate (CAGR) of 3.39% during 2026-2034. Sustained demand fundamentals remain solid. Evolving sustainability certification requirements and expanding technical textile, filtration, and protective clothing applications collectively continue to shape the acrylic staple fiber price trend in producing regions.

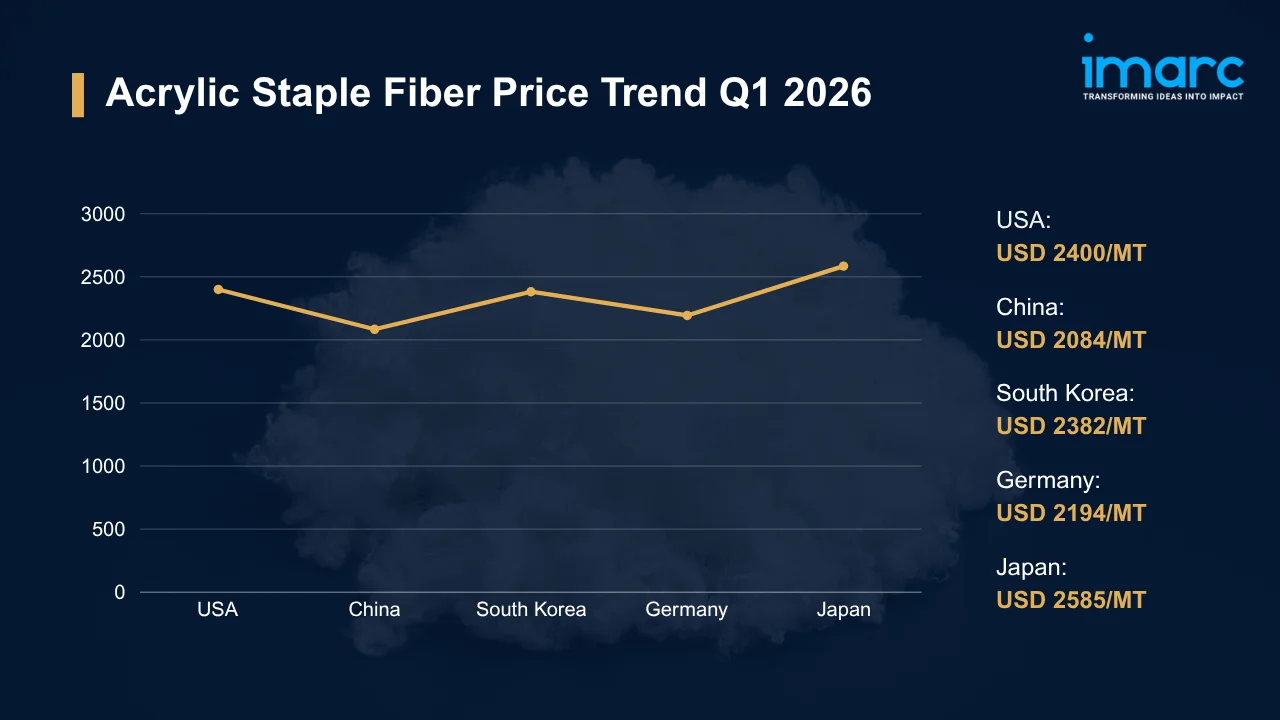

Acrylic Staple Fiber Price Trend Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 2,400 | +3.21% | ↑ |

| China | 2,084 | +1.45% | ↑ |

| South Korea | 2,382 | +2.31% | ↑ |

| Germany | 2,194 | -1.91% | ↓ |

| Japan | 2,585 | +2.63% | ↑ |

To access real-time prices Request Sample

What Moved Prices:

USA:

- At USD 2,400/MT in Q1 2026, acrylic staple fiber prices in the USA posted their strongest quarterly reading since mid-2025, driven by resumed procurement across apparel converters and nonwoven manufacturers following year-end inventory drawdowns. Buying broadened rapidly across distribution channels. Reinforcing the upward push, domestic supply availability tightened as producer utilization lifted.

- Lifting utilization rates to meet rising converter orders, Gulf Coast producers tightened prompt availability. Spot premiums re-entered quotations. Captured in the acrylic staple fiber price chart for Q1 2026, spot offers above prior-quarter contract levels cleared as buyers sought prompt delivery from both domestic producers and import channels.

China:

- Reaching USD 2,084/MT in Q1 2026, acrylic staple fiber prices in China posted the first material quarterly recovery since early 2025, as mills restocked post-Lunar New Year while drawing down inventories accumulated through late 2025. Export-oriented yarn producers reactivated orders. Into late February, buying momentum continued.

- Holding relatively stable despite firmer energy benchmarks, acrylonitrile feedstock costs limited pass-through to fiber valuations. Domestic competitive pricing remained a constraint. Partially offsetting that constraint, export demand from South and Southeast Asian buyers absorbed excess domestic supply and prevented deeper inventory overhangs from forming at key distribution points.

South Korea:

- In Q1 2026, acrylic staple fiber prices in South Korea rose to USD 2,382/MT as improved export order flows from East Asian textile markets coincided with seasonal restocking ahead of spring garment production. The demand recovery proved genuine. Targeting spring and summer collections, yarn converters firmed contract pricing and absorbed available fiber volumes.

- Capping the upside despite firmer end-use demand, competitive Chinese import flows maintained market pricing pressure through the quarter. Acrylonitrile costs held stable. At Korean gateway ports, congestion that had built through year-end cleared progressively through January, restoring import logistics efficiency for fiber distributors and reducing delivery uncertainty for domestic converters.

Germany:

- At USD 2,194/MT, acrylic staple fiber prices in Germany declined 1.91% in Q1 2026, pressured by a European textile sector maintaining the most conservative procurement posture it has held since early 2024. Spot order books stayed thin. Prioritizing inventory drawdown over fresh fiber, apparel and industrial textile buyers resisted restocking throughout the period.

- With ample Asian import availability and moderate European energy cost stabilization both undermining any price floor support, domestic sellers faced no leverage in contract negotiations. Automotive interior demand stayed sluggish. Across multiple import origins, competitive tendering from Chinese and Korean suppliers reinforced the downward correction through the quarter.

Japan:

- At USD 2,585/MT in Q1 2026, acrylic staple fiber prices in Japan advanced 2.63%, as downstream textile manufacturers resumed seasonal buying following the year-end period, with spring garment production schedules simultaneously firming across major apparel converters. Export order inquiries improved through the period. From regional apparel buyers, order volumes lifted into February.

- Remaining moderate through the quarter, feedstock costs provided producers with room for upward price revisions without compressing margins severely or triggering supply-side curtailments. Inventory availability tightened at key distribution points. Against this backdrop, buyers accepted firmer contract offers to secure prompt delivery, reinforcing the upward trend across Japanese fiber markets.

Drivers Influencing the Market:

Several factors continue to shape acrylic staple fiber pricing and market behavior:

- Textile and Apparel Sector Demand: Across apparel manufacturing, home furnishing conversion, and industrial nonwoven production, acrylic staple fiber captures the bulk of global consumption. Seasonal collection changeovers introduce variability. Cost-competitive against wool and cashmere at current price points, acrylic staple fiber secures recurring volume from value-segment apparel producers, while emerging middle-class consumption in South and Southeast Asia underpins long-term demand growth beyond the near-term procurement cycle.

- Upstream Acrylonitrile Feedstock Costs: Synthesized via propylene ammoxidation, acrylonitrile accounts for a substantial share of acrylic staple fiber production cost, linking fiber valuations directly to crude oil refinery economics and petrochemical feedstock market dynamics. Few large producers hold most capacity. Resulting spot tightness from any unplanned outage amplifies quickly, while export quota adjustments among producing countries further reshape feedstock availability across a supply chain with limited buffer capacity.

- Energy Expenditure in Wet Spinning and Polymer Processing: Electricity and natural gas costs across polymerization, wet-spinning, and drying stages drive a significant share of acrylic staple fiber production expense. Per the EIA, US industrial natural gas consumption averaged a record 23.6 Billion cubic feet per day in 2025. Reflecting sustained industrial activity, record consumption levels sustain energy cost pressure on producers. Supply tightening amplifies input cost volatility across manufacturing-intensive regions.

- Ocean Freight and Logistics Economics: Freight rate fluctuations across major global shipping routes directly affect landed costs for acrylic staple fiber importers. Rapid changes in container shipping costs can quickly alter regional price competitiveness and significantly influence the acrylic staple fiber price index across import-dependent markets.

- Environmental and Regulatory Compliance: Across regulated markets, chemical safety frameworks governing acrylonitrile handling, waste solvent management, and production discharge are tightening, imposing rising compliance expenditures on producers and distributors. EU REACH registration costs compound this. Enforced rigorously, these requirements generate structural pricing premiums for affected producers, while evolving extended producer responsibility schemes for synthetic textiles progressively add compliance overhead across European and North American markets.

- Trade Policy and Currency Dynamics: Governing the competitive positioning of Chinese, South Korean, and Japanese supply in Western markets are tariff structures, anti-dumping duties, and preferential trade arrangements that shift with each round of bilateral negotiations. Yen and won movements matter separately. When either currency weakens against the US dollar, export-origin producers gain cost advantages that compress price spreads for import-dependent buyers, requiring real-time currency and trade-policy signals to be embedded into landed cost benchmarking frameworks.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In March 2025, Toray Industries, Inc. implemented a mass balance methodology across its TORAYLON™ acrylic staple fiber production process, enabling allocation of attributes from biomass and recycled plastic inputs. The product line received ISCC PLUS certification, confirming compliance with established sustainability and carbon traceability standards.

Outlook & Strategic Takeaways:

Looking ahead, the acrylic staple fiber market is expected to expand steadily through 2034, driven by sustained demand from the apparel, home furnishing, and technical textile sectors alongside growing filtration and protective clothing applications. Acrylonitrile feedstock cost trajectories and emerging sustainability certification requirements for synthetic fiber producers will remain the pivotal variables shaping the acrylic staple fiber price forecast across major production and consumption regions through the forecast horizon.

To navigate this complex landscape, stakeholders should:

- Monitor Regional Price Differentials: Track quarterly pricing variations across the USA, China, South Korea, Germany, and Japan to identify cost-efficient procurement windows. Establish cross-origin benchmarking protocols that compare landed costs against prevailing contract rates for optimal sourcing strategy.

- Assess Freight Market Developments: Monitor container shipping rate movements on Asia-Europe and Transpacific corridors to anticipate landed cost shifts for import-dependent buyers. Negotiate logistics contracts with rate-adjustment clauses tied to prevailing Drewry World Container Index benchmarks.

- Evaluate Downstream Demand Indicators: Track apparel production indices and home furnishing order books across principal consumption regions to correlate demand signals with procurement planning cycles. Align sourcing schedules with seasonal buying patterns to reduce inventory overhang and optimize stock positioning.

- Review Regulatory Compliance Expenditures: Audit current costs associated with acrylonitrile handling, synthetic fiber waste management, and EU REACH compliance obligations to identify operational efficiencies. Engage regulatory specialists to ensure compliance frameworks remain current with evolving extended producer responsibility requirements for synthetic textiles.

- Strengthen Currency Exposure Management: Implement hedging strategies for procurement denominated in Japanese yen and South Korean won to stabilize acrylic staple fiber price per MT in USD terms. Coordinate treasury and procurement functions to align foreign exchange coverage with anticipated import payment timelines.

- Explore Emerging Application Segments: Investigate growth potential in technical textiles, filtration media, and recycled-content synthetic fiber blends as portfolio diversification pathways. Partner with material science specialists to assess the viability of bio-based acrylic fiber variants in emerging end markets.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates: 12 deliverables/year

- Quarterly Updates: 4 deliverables/year

- Biannual Updates: 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)