A2P Messaging Market Size, Share, Trends and Forecast by Component, Deployment Mode, SMS Traffic, Application, End User, and Region, 2026-2034

Global A2P Messaging Market Size, Share, Trends & Forecast (2026-2034)

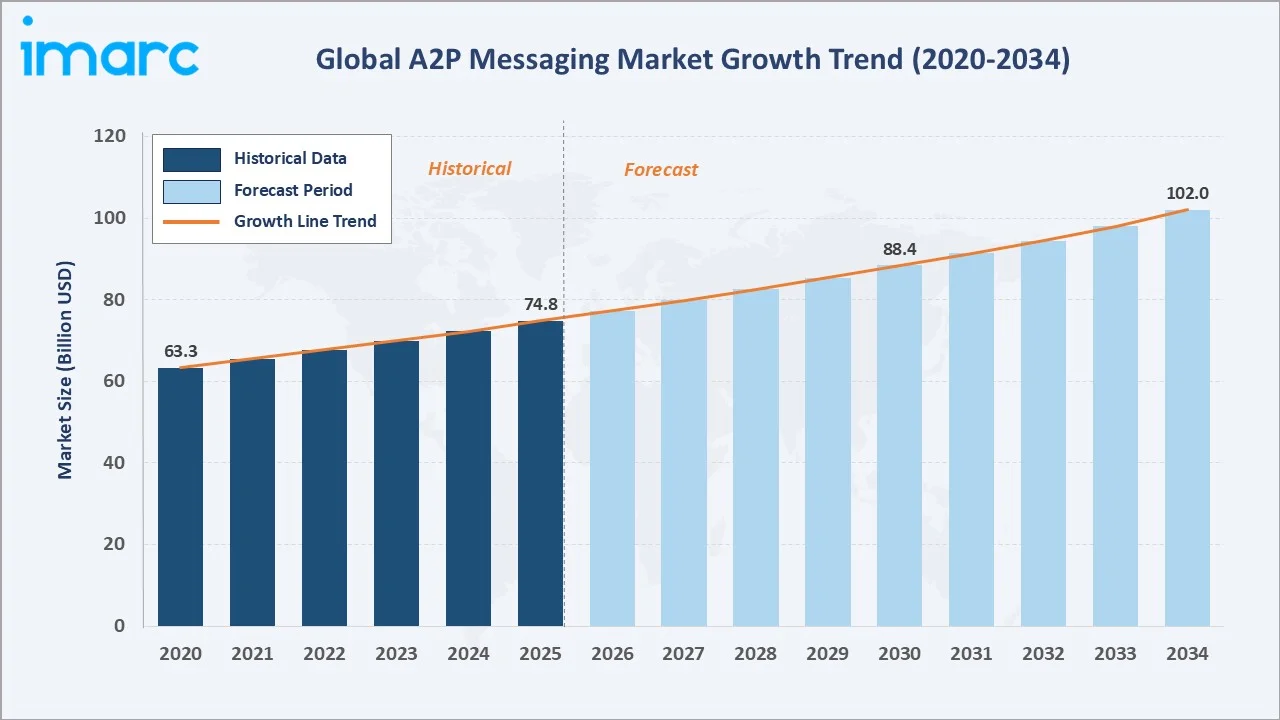

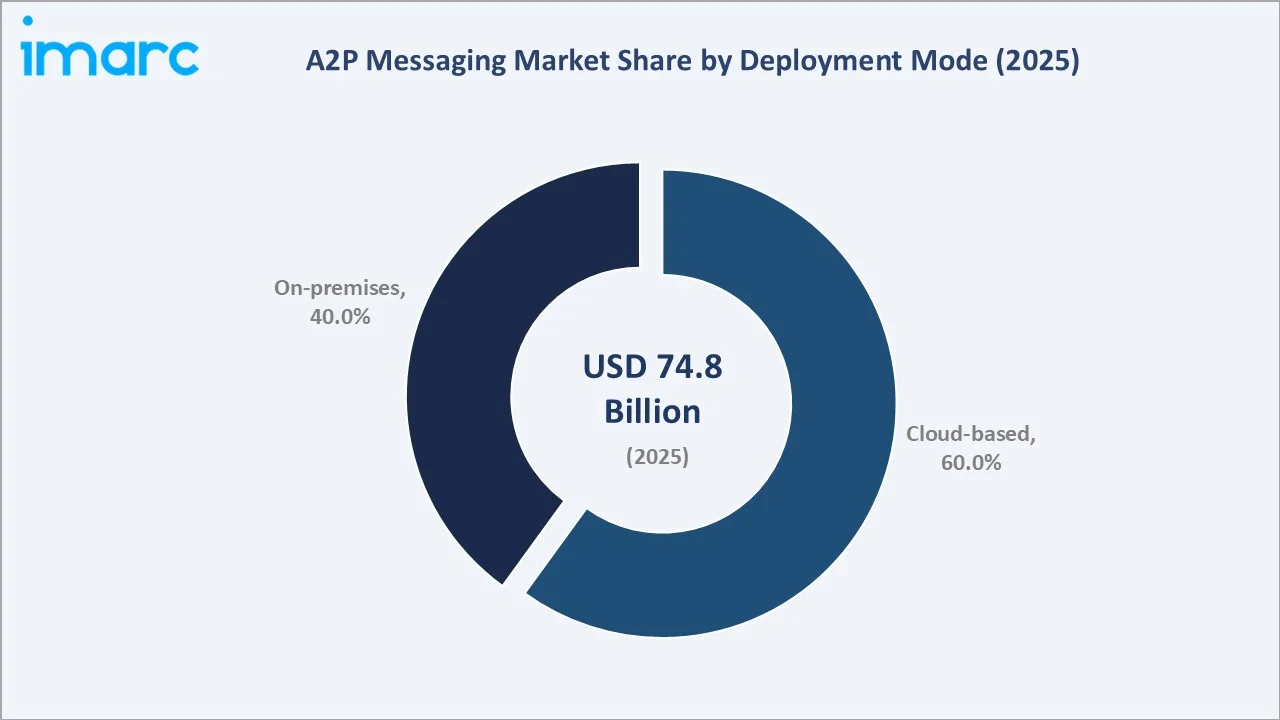

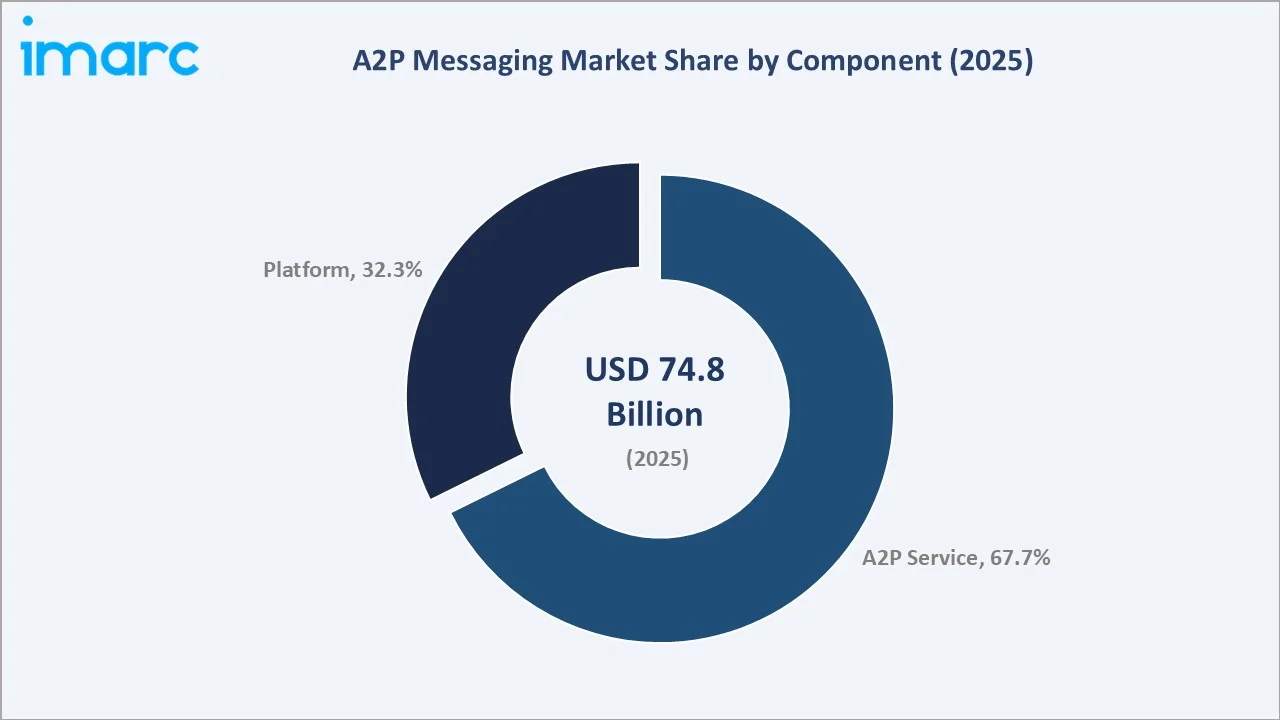

The global A2P messaging market size reached USD 74.8 Billion in 2025 and is projected to reach USD 102.0 Billion by 2034, exhibiting a CAGR of 3.40% during the forecast period 2026-2034. Rising enterprise demand for real-time mobile communication, expanding global mobile subscriber penetration, and accelerating e-commerce applications are driving A2P messaging market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 74.8 Billion |

|

Forecast Market Size (2034) |

USD 102.0 Billion |

|

CAGR (2026-2034) |

3.40% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (44.5% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (~4.5% CAGR, 2026-2034) |

|

Leading Component |

A2P Service (67.7%, 2025) |

|

Leading Deployment Mode |

Cloud-based (60.0%, 2025) |

The global A2P messaging market growth trajectory from 2020 through 2034 reflects consistent expansion—from USD 63.3 Billion in 2020 to a forecast of USD 102.0 Billion by 2034—driven by rising enterprise digital communication budgets, OTP adoption, and expanding mobile commerce ecosystems globally.

To get more information on this market, Request Sample

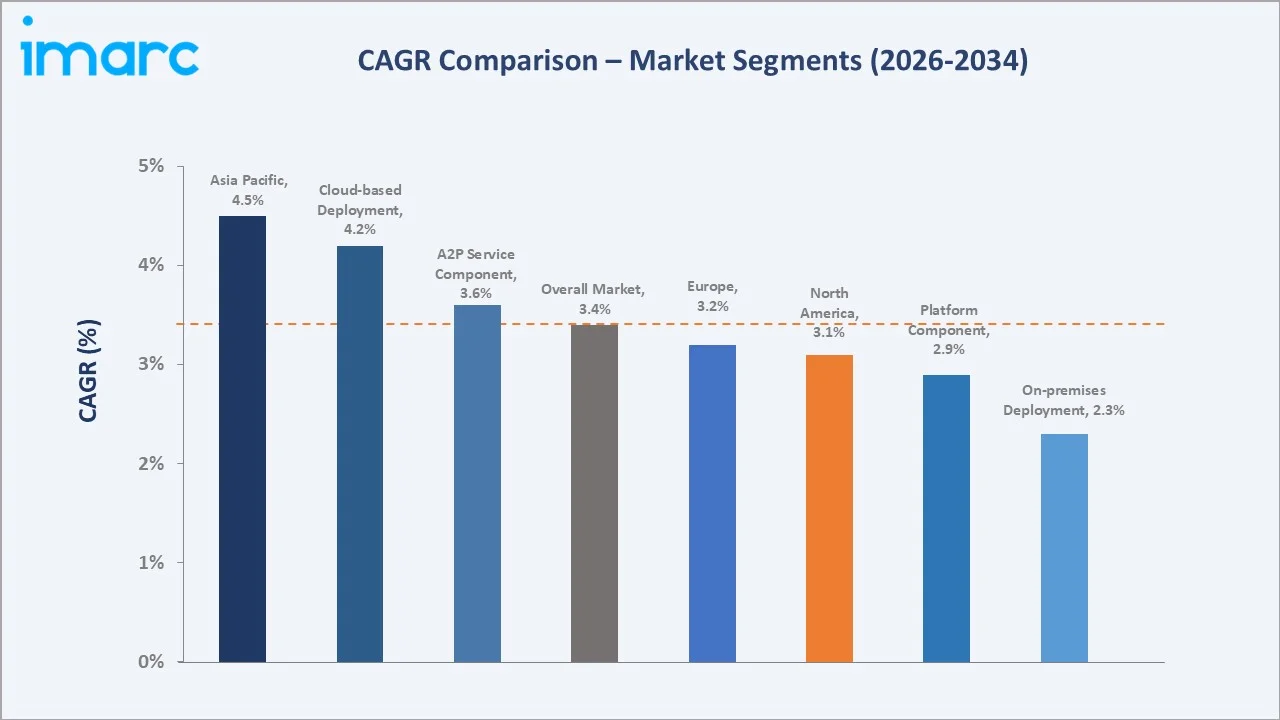

Segment-level CAGR comparisons highlight Cloud-based deployment at ~4.2% and Asia Pacific at ~4.5% as the fastest-growing sub-categories within the global A2P messaging market forecast through 2034, both outpacing the overall market CAGR of 3.40%.

Executive Summary

The global A2P messaging market is undergoing sustained and structural expansion, driven by enterprise-led demand for secure, real-time mobile communication. Valued at USD 74.8 Billion in 2025 and forecast to reach USD 102.0 Billion by 2034 at a CAGR of 3.40%, the market benefits from the rapid proliferation of mobile subscriptions globally. This expanding addressable base structurally amplifies enterprise A2P messaging demand across authentication, notifications, and promotions.

The A2P Service component commands 67.7% of the market in 2025, fuelled by OTP authentication, transactional alerts, and marketing communications. Cloud-based deployment represents 60.0% of the market in 2025, driven by scalability advantages, faster deployment, and reduced total cost of ownership versus on-premises alternatives. Growing cloud provider competition is expanding accessibility for SMEs seeking rapid A2P integration.

Asia Pacific leads with 44.5% global revenue share in 2025, anchored by India and China's massive mobile subscriber bases and Southeast Asia's fintech growth. North America holds 23.6% and Europe 18.7%. The A2P messaging market outlook remains robust as enterprise digital transformation, 5G network buildouts, and Rich Communication Services (RCS) adoption converge to broaden A2P communication functionality and addressable revenue through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

A2P Service – 67.7% share (2025) |

|

Second Component |

Platform – 32.3% share (2025) |

|

Leading Deployment Mode |

Cloud-based – 60.0% share (2025) |

|

Second Deployment Mode |

On-premises – 40.0% share (2025) |

|

Leading Region |

Asia Pacific – 44.5% revenue share (2025) |

|

Top Companies |

Twilio Inc., Sinch, Telefonaktiebolaget LM Ericsson, Infobip Ltd., and Syniverse Technologies, LLC |

|

Market Opportunity |

RCS messaging upgrade + OTP-driven enterprise authentication demand |

Key Analytical Observations Supporting the Above Data:

- A2P Service dominance at 67.7% in 2025 reflects the high operational volume of OTP delivery, transactional SMS, and automated notification services across BFSI, e-commerce, and healthcare. Enterprises scaling real-time alert infrastructure continue to prefer managed A2P service models with built-in compliance and delivery guarantees.

- Platform segment at 32.3% is driven by mid-to-large enterprises seeking self-managed, customizable A2P messaging with bulk messaging APIs, route optimization, and campaign analytics—reducing dependency on third-party aggregators.

- Cloud-based deployment's 60.0% share is underpinned by SME demand for elastic scaling, faster deployment timelines, and managed infrastructure. Cloud A2P platforms can accommodate campaign-driven volume spikes without capital investment in physical hardware.

- Asia Pacific's 44.5% revenue leadership reflects China and India's massive mobile bases combined with rapid fintech and e-commerce growth. India's UPI platform processed over 228.5 billion transactions in a in 2025, generating substantial A2P OTP traffic.

Global A2P Messaging Market Overview

Application-to-Person (A2P) messaging refers to the automated transmission of SMS messages from a software application or enterprise system to individual mobile phone users. The global A2P messaging market encompasses platforms, aggregation services, and carrier infrastructure supporting automated communication across BFSI, e-commerce, healthcare, travel, government, and retail verticals. Core use cases iclude OTP delivery, transactional alerts, appointment reminders, promotional campaigns, and two-factor authentication workflows.

The industry operates at the intersection of telecommunications infrastructure, enterprise software, and mobile commerce. Growth is supported by macroeconomic tailwinds including rising smartphone penetration—global smartphone users exceeded 6.9 billion in 2024—alongside digital-first business adoption, escalating cybersecurity requirements, and the broad shift toward mobile-first customer engagement. Regulatory frameworks such as Telephone Consumer Protection Act of 1991 (TCPA) in the United States, The General Data Protection Regulation (GDPR) in Europe, and The Telecom Regulatory Authority of India (TRAI) regulations in India are shaping compliance-led messaging product design and accelerating demand for certified A2P platforms.

Market Dynamics

To evaluate market opportunities, Request Sample

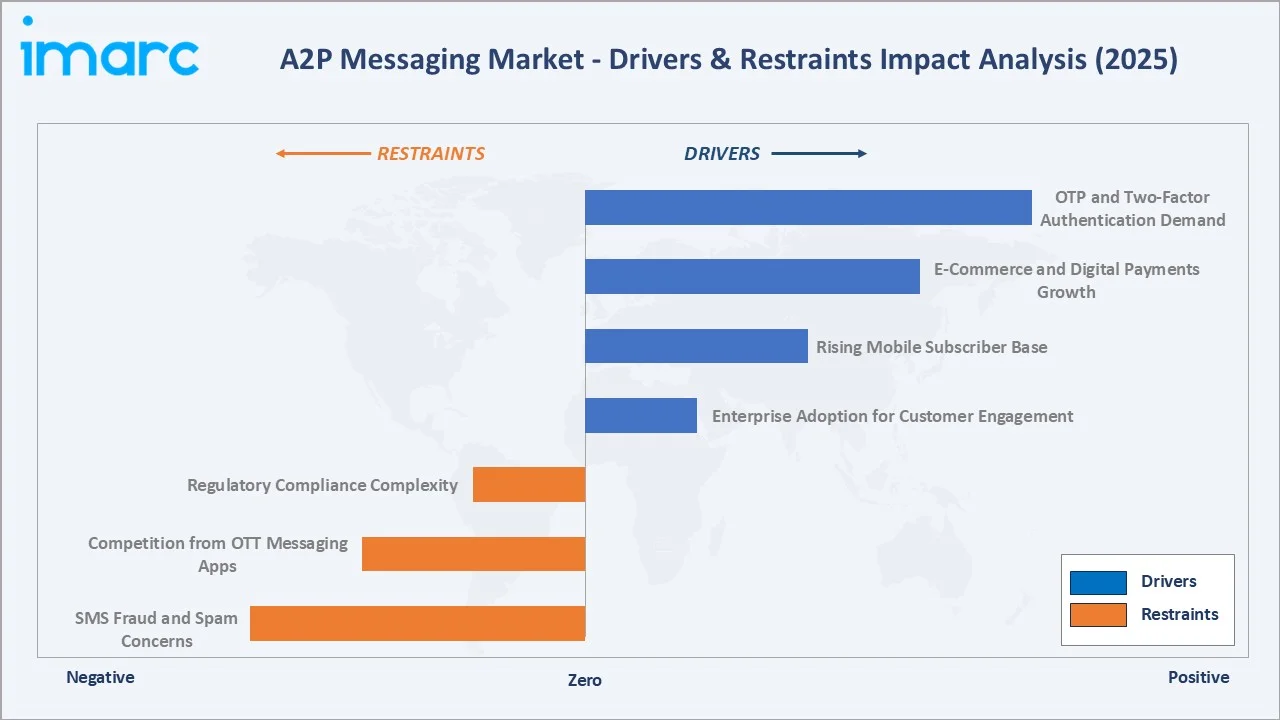

Market Drivers

- Enterprise Adoption for Customer Engagement: Enterprises across BFSI, e-commerce, healthcare, and logistics are embedding A2P messaging into customer lifecycle touchpoints. Mobile advertising expenditure in the United States was projected to exceed significant levels in 2024, reflecting the scale of digital communication budgets being directed toward mobile-first engagement.

- Rising Mobile Subscriber Base: Rising mobile subscriber penetration, highlighted by growth tracked by GSMA, is a key driver for the global A2P messaging market. A larger user base increases demand for OTPs, alerts, and promotional messages, enabling enterprises to scale customer communication, improve engagement, and expand digital service delivery across industries.

- E-Commerce and Digital Payments Growth: Global e-commerce sales are forecast to grow strongly in 2024, accelerating demand for A2P messaging to deliver order confirmations, shipment alerts, discount vouchers, and payment authentication codes across digital commerce platforms.

- OTP and Two-Factor Authentication Demand: Escalating cybersecurity threats compel financial institutions, digital platforms, and governments to mandate SMS-based 2FA. High SMS open rates and sub-90-second response windows make A2P SMS the preferred OTP delivery vector over email or app-based alternatives.

Market Restraints

- SMS Fraud and Spam Concerns: Rising SMS phishing attacks and grey-route message fraud create reputational risks and compliance overhead for A2P messaging platforms and enterprises, increasing investment requirements in anti-fraud infrastructure.

- Competition from OTT Messaging Applications: WhatsApp Business API, Apple Messages for Business, and Google's RCS Business Messaging offer richer, lower-cost enterprise communication alternatives gradually capturing share from traditional A2P SMS in developed markets.

- Regulatory Compliance Complexity: Cross-border A2P campaigns must navigate divergent regulatory regimes—TCPA in the USA, GDPR in Europe, TRAI in India—increasing compliance cost and slowing international messaging program rollouts.

Market Opportunities

- RCS Business Messaging Adoption: Rich Communication Services (RCS) enables branded sender IDs, rich media, and interactive messages within native SMS apps. Brands adopting RCS report significantly higher click-through rates than traditional A2P SMS, representing a major monetization upgrade opportunity for platform providers.

- Emerging Market Expansion: Southeast Asia, Sub-Saharan Africa, and Latin America represent high-growth opportunity zones where mobile-first digital services are expanding rapidly. Fintech penetration and government digital identity programs are generating substantial new A2P traffic volumes through 2034.

- AI-Driven Personalization: AI and NLP integration into A2P platforms enables context-aware, dynamically personalized messaging at scale. Early adopters report notable improvements in conversion rates from AI-optimized messaging flows, driving premium platform tier adoption.

Market Challenges

- Grey Route Traffic and Revenue Leakage: Grey route traffic—messages routed through unauthorized paths bypassing commercial A2P channels—represents a persistent revenue leakage challenge for telecom operators and legitimate aggregators globally.

- Price Compression and Margin Pressure: Intense competition among SMS aggregators and Communications Platform as a Service (CPaaS) providers is compressing per-message pricing. Sustaining margin growth requires upselling to managed services, analytics dashboards, and omnichannel platforms beyond core SMS delivery.

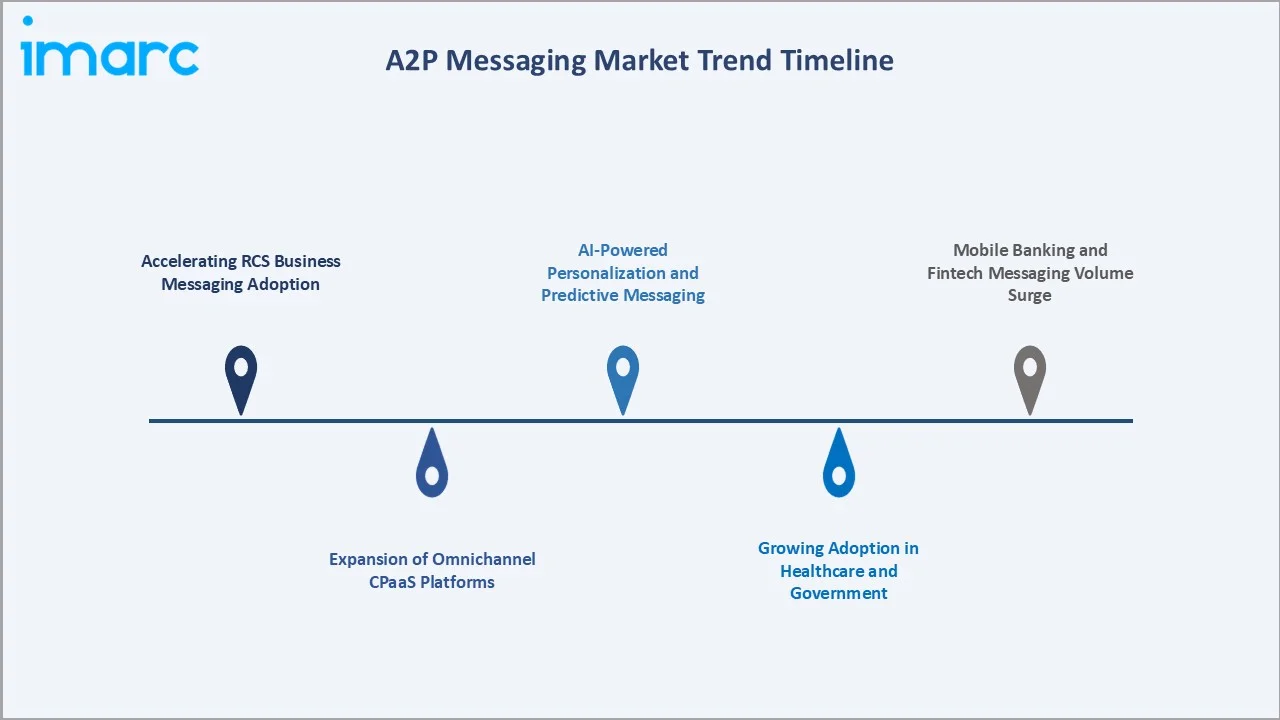

Emerging Market Trends

1. Accelerating RCS Business Messaging Adoption

Rich Communication Services is emerging as the next evolution of A2P SMS, offering branded sender IDs, rich media, and interactive message formats. Google’s RCS rollout across Android devices has positioned RCS as a mainstream enterprise channel. Brands adopting RCS report significantly higher click-through rates than traditional A2P SMS, making RCS Business Messaging a priority investment for enterprise communication teams through 2030.

2. Expansion of Omnichannel CPaaS Platforms

The market is shifting from pure-play SMS aggregation toward full Communication Platform-as-a-Service (CPaaS) solutions integrating SMS, voice, email, and OTT messaging in a unified API layer. Major platforms—Twilio, Sinch, and Infobip—are investing heavily in omnichannel orchestration capabilities. The global CPaaS market is projected to exceed a substantial valuation by 2030.

3. AI-Powered Personalization and Predictive Messaging

AI integration within A2P platforms enables enterprises to deliver context-aware, real-time personalized messages based on customer behaviour, location, and transaction history. Machine learning models optimize send-time, message frequency, and content variant selection. Early adopters report notable improvements in conversion rates from AI-optimized messaging flows versus static batch campaigns.

4. Growing Adoption in Healthcare and Government

Post-pandemic, healthcare systems globally have accelerated A2P messaging adoption for appointment reminders, prescription notifications, vaccination alerts, and remote patient monitoring updates. The United States healthcare SMS marketing segment is projected to grow steadily through 2030, reflecting deep vertical penetration. Government digital identity and citizen service programs are creating additional high-volume A2P demand.

5. Mobile Banking and Fintech Messaging Volume Surge

Digital banking expansion across Asia, Africa, and Latin America is generating exponential A2P messaging volumes for OTP delivery, balance alerts, fraud warnings, and transaction confirmations. India’s Unified Payments Interface processes massive transaction volumes monthly, with each transaction triggering multiple A2P SMS touchpoints across the payment value chain.

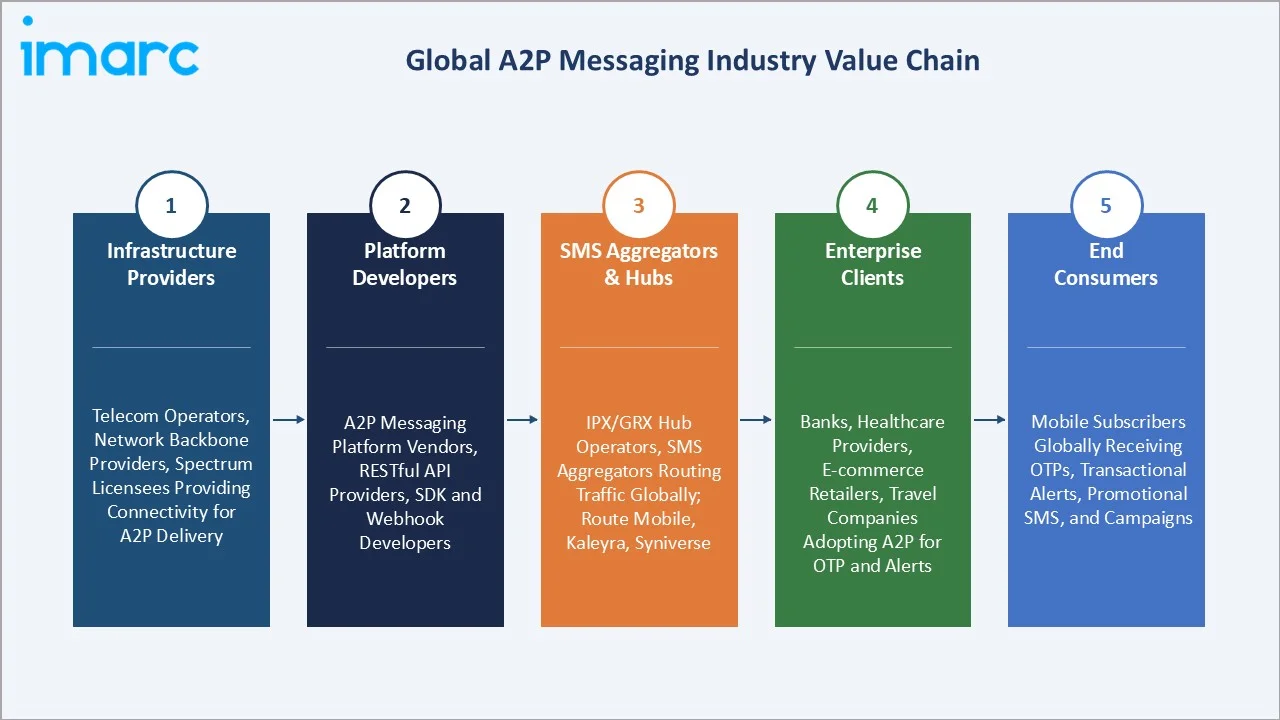

Industry Value Chain Analysis

The global A2P messaging industry value chain spans five integrated stages from infrastructure provisioning through end consumer delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements relevant to the overall A2P messaging market analysis.

|

Value Chain Stage |

Description |

|

Infrastructure Providers |

Telecom operators, network backbone providers, spectrum licensees providing connectivity for A2P message delivery |

|

Platform Developers |

A2P messaging platform vendors, RESTful API providers, SDK and webhook developers |

|

SMS Aggregators & Hubs |

IPX/GRX hub operators, SMS aggregators routing traffic globally; Route Mobile, Kaleyra, Syniverse, Tata Communications |

|

Enterprise Clients |

Banks, healthcare providers, e-commerce retailers, travel companies — adopting A2P for OTP, alerts, and promotional campaigns |

|

End Consumers |

Mobile subscribers globally receiving OTPs, transactional alerts, promotional SMS, and interactive campaign messages |

SMS aggregators and CPaaS platform vendors hold the highest strategic value by integrating carrier relationships, compliance management, and enterprise API functionality into scalable messaging infrastructure. Cloud-based platforms are reshaping the aggregator tier, enabling enterprise-direct connectivity that reduces intermediary layers and improves message delivery economics and transparency.

Technology Landscape in the A2P Messaging Industry

Messaging Protocol Innovation

SMS remains the foundational A2P protocol, supported by universal device compatibility and very high open rates. RCS (Rich Communication Services) is rapidly emerging as the next-generation replacement, enabling multimedia content, read receipts, branded messaging, and interactive buttons within native phone messaging apps. Global RCS active users have reached a substantial base, with Google and Samsung both defaulting to RCS-enabled messaging clients.

Cloud Platform Architecture

Cloud-native A2P messaging architectures are replacing legacy on-premises SMS gateway deployments. Containerized microservices, event-driven architecture, and serverless computing models enable real-time message throughput at scale. Leading platforms process massive message volumes with ultra-low delivery latency, providing the responsiveness required for time-critical OTP delivery in banking and payment applications.

AI and Machine Learning Integration

Artificial intelligence is being embedded across A2P platform layers for content personalization, fraud detection, delivery route optimization, and predictive analytics. NLP models enable two-way conversational A2P interactions in customer service applications. AI-driven anti-spam and grey-route detection algorithms are improving message integrity, with leading platforms reporting significant reduction in fraudulent message delivery following AI-layer deployment.

API and Developer Ecosystem

Developer-centric A2P platforms led by Twilio and Vonage have transformed enterprise messaging procurement from carrier negotiations to self-service RESTful API integration. The addressable developer ecosystem integrating A2P APIs has expanded globally, with low-code integration tools enabling rapid deployment within CRM, ERP, and e-commerce platforms across major verticals.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Platform |

32.3% |

2025 |

|

Deployment Mode |

Cloud-based |

60.0% |

2025 |

|

SMS Traffic |

National Traffic |

🔒 |

2025 |

|

Application |

Customer Relationship Management Services |

🔒 |

2025 |

| End User | BFSI | 21.2% | 2025 |

|

Region |

Asia Pacific |

44.5% |

2025 |

By Deployment Mode

To access detailed market analysis, Request Sample

Cloud-based deployment leads the global A2P messaging market with a 60.0% share in 2025. Cloud A2P platforms offer integrated SMS, MMS, and multi-channel messaging from a unified infrastructure, with elastic scaling that accommodates campaign-driven volume spikes. Rapid deployment timelines—often days versus weeks for on-premises systems—are a critical advantage for fast-growing digital-first enterprises.

By Component

A2P Service is the dominant component seg`ment at 67.7% market share in 2025. A2P services encompass the full spectrum of managed messaging delivery—including OTP services, promotional campaigns, transactional alert services, and carrier relationship management. Enterprises prefer managed A2P service models for built-in compliance, quality-of-service guarantees, and global delivery reach without requiring internal platform engineering investment. The segment sustains strong demand from BFSI, e-commerce, and healthcare verticals requiring high-volume, time-critical delivery.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

44.5% |

Mobile banking growth, e-commerce boom, smartphone proliferation, government digital transformation programs in India and China |

|

North America |

23.6% |

Enterprise BFSI adoption, OTP-driven banking, TCPA-compliant mobile marketing, healthcare messaging expansion |

|

Europe |

18.7% |

GDPR-compliant A2P, fintech proliferation, strong BFSI adoption, regulatory authentication mandates across EU markets |

|

Latin America |

7.8% |

Growing e-commerce, BFSI digital penetration, rising mobile subscriber base in Brazil and Mexico |

|

Middle East & Africa |

5.4% |

Mobile-first consumers, expanding telecom networks, government digital transformation programs in UAE and KSA |

Asia Pacific commands 44.5% global revenue share in 2025. China remains the single largest national A2P messaging market by volume, with Alibaba, JD.com, and WeChat Pay ecosystems generating billions of transactional A2P messages monthly. India is the fastest-growing sub-market—UPI-driven payment OTP volumes, and government digital service programs are creating structural A2P demand. Southeast Asia's e-commerce and super-app ecosystems in Indonesia, Vietnam, and Thailand add further volume growth through 2034.

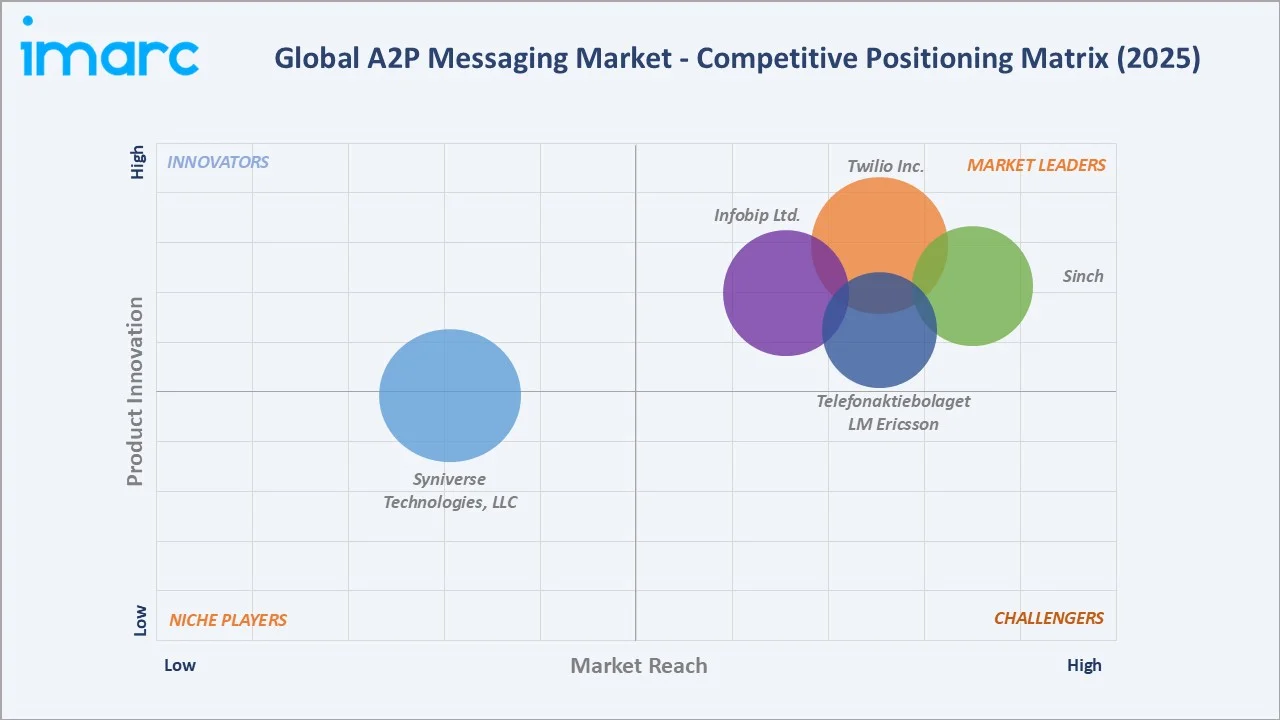

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Twilio Inc. |

Twilio |

Leader |

Cloud API platform, developer-first CPaaS ecosystem |

|

Sinch |

Sinch |

Leader |

Full CPaaS suite, global acquisition-led growth |

|

Telefonaktiebolaget LM Ericsson |

Vonage |

Leader |

Telecom-grade A2P, Ericsson infrastructure backbone, strong EMEA presence |

|

Infobip Ltd. |

Infobip |

Leader |

Omnichannel platform, AI-driven personalization |

|

Syniverse Technologies, LLC |

Syniverse |

Emerging |

Carrier interconnect expertise, fraud prevention, roaming-centric A2P |

The global A2P messaging market's competitive landscape is moderately concentrated at the platform and CPaaS tier. Twilio Inc., Sinch, Telefonaktiebolaget LM Ericsson compete on global carrier network breadth, API developer ecosystem depth, and omnichannel platform capabilities.

Key Company Profiles

Twilio Inc.

Twilio Inc. is a U.S.-based cloud communications platform provider headquartered in San Francisco, California. Founded in 2008, the company enables developers and enterprises to embed communication capabilities such as messaging, voice, video, and email directly into applications through APIs.

- Product & Platform Portfolio: Twilio's A2P portfolio includes Programmable SMS, Programmable Messaging API, Twilio Engage (customer data platform), Twilio Verify (OTP and 2FA), and the Twilio Segment customer intelligence platform for personalized enterprise campaigns.

- Recent Developments: In 2025, Twilio has unveiled its next-generation Customer Engagement Platform, positioning itself as an AI- and data-powered foundation for omnichannel customer interactions. The platform unifies messaging, voice, email, and data-driven workflows into a single infrastructure layer, enabling enterprises to build more personalized and real-time engagement experiences at scale.

- Strategic Focus:

- Twilio's strategy centers on transitioning customers from API-level messaging to full customer engagement platform subscriptions via Twilio Engage and Segment, targeting higher-value recurring revenue, stronger data differentiation, and reduced churn.

Sinch

Sinch is a Sweden-based cloud communications platform provider headquartered in Stockholm. Founded in 2008, the company enables businesses to engage customers through messaging, voice, email, and verification solutions via APIs and cloud-based platforms.

- Product & Platform Portfolio: Sinch's portfolio spans SMS API, RCS Business Messaging, WhatsApp Business API, voice services, and the Sinch Engage omnichannel messaging platform serving mid-market to enterprise clients across retail, BFSI, and logistics.

- Recent Developments: In 2021, Sinch completed the acquisition of MessageMedia, strengthening its position in the global cloud communications and A2P messaging market. The deal integrates MessageMedia’s SMB-focused messaging capabilities into Sinch’s broader CPaaS ecosystem, expanding its reach in SMS-based customer engagement, notifications, and conversational messaging.

- Strategic Focus: Sinch is focused on cross-selling multi-channel messaging capabilities across its acquired customer base while expanding RCS Business Messaging adoption ahead of anticipated carrier-side RCS monetization at scale through 2027.

Infobip Ltd.

Infobip Ltd. is a global cloud communications platform provider founded in 2006, with headquarters in London, United Kingdom. The company delivers omnichannel communication solutions that enable businesses to engage customers across messaging, voice, email, and digital channels.

- Product & Platform Portfolio: Infobip's platform includes Moments (customer journey automation), Answers (AI chatbot), Conversations (contact centre), and Signals (fraud prevention), alongside its core A2P SMS, RCS, and WhatsApp Business API infrastructure.

- Recent Developments: In 2023, Infobip launched its AI Hub, a generative AI-powered upgrade to its communications platform designed to enable end-to-end conversational customer experiences. The solution integrates advanced analytics, AI, and generative AI tools into its SaaS portfolio, allowing businesses to build personalized, automated interactions across the full customer journey.

- Strategic Focus: Infobip's strategy focuses on deepening vertical specialization in BFSI, retail, and healthcare while positioning fraud management and compliance capabilities as key differentiators versus API-first CPaaS competitors.

Market Concentration Analysis

The global A2P messaging market exhibits moderate concentration at the platform and CPaaS tier. The top five players— Twilio Inc., Sinch, Telefonaktiebolaget LM Ericsson, Infobip Ltd., Syniverse Technologies, LLC—collectively account for an estimated 35–42% of global platform-tier revenue in 2025.

The market is experiencing bifurcated consolidation dynamics. At the CPaaS and enterprise platform tier, M&A activity is accelerating. Simultaneously, the SMS aggregation mid-tier is consolidating as regulatory anti-grey-route enforcement and direct carrier interconnect requirements raise compliance barriers, favouring larger, well-capitalized aggregators.

Investment & Growth Opportunities

Fastest-Growing Segments

Cloud-based A2P deployment is the highest-growth infrastructure sub-segment, advancing at approximately 4.2% CAGR through 2034. RCS Business Messaging represents the highest-growth messaging format, with enterprise adoption accelerating as Google's RCS ecosystem matures across global Android device fleets. BFSI-vertical A2P messaging is the largest revenue opportunity, driven by OTP, fraud alert, and mobile banking notification volumes expanding alongside digital banking penetration globally.

Emerging Market Expansion

India represents the highest-potential emerging market, rapid fintech expansion, and government-led digital services adoption generating structural A2P volume growth. Southeast Asia's super-app ecosystems (Grab, GoTo, Sea Group) and Sub-Saharan Africa's mobile money platforms (M-Pesa, MTN MoMo) are creating new high-frequency A2P messaging demand in regions where traditional banking infrastructure remains limited.

Venture and Strategic Investment Trends

Strategic investment in A2P market infrastructure is concentrated in three priority areas: RCS platform readiness and carrier monetization infrastructure; AI-driven personalization and conversational messaging capabilities; and fraud detection and grey-route elimination technology. Venture capital is flowing into AI-native messaging platforms and conversational AI companies expanding the A2P use case set beyond traditional SMS into interactive, two-way customer engagement workflows valued at higher per-message economics.

Future Market Outlook (2026-2034)

The global A2P messaging market forecast projects steady value expansion from USD 74.8 Billion in 2025 to USD 102.0 Billion by 2034 at a CAGR of 3.40%. Asia Pacific will retain regional leadership while advancing structurally through India and Southeast Asia market deepening. North America and Europe will sustain value growth through compliance-driven enterprise investment and RCS adoption cycles.

Three key structural shifts will reshape the A2P messaging market through 2034. First, RCS monetization at scale will transition enterprise messaging from cost-centre SMS delivery toward premium-priced, engagement-driven RCS campaigns—fundamentally changing platform revenue models. Second, AI-native messaging platforms will capture disproportionate share by delivering measurable ROI improvement over legacy batch campaigns.

Third, emerging market volume growth from India, Southeast Asia, and Africa will offset any SMS volume moderation in mature markets from OTT and RCS substitution, sustaining overall market CAGR through 2034.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024–2025 with A2P messaging industry stakeholders—including product executives at CPaaS platform providers, SMS aggregators, telecom operators, enterprise IT and digital marketing leaders, and institutional analysts. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines across key verticals and geographies.

Secondary Research

Secondary sources include GSMA Mobile Connectivity reports, FCC telecom filings, TRAI regulatory publications, ITU global ICT statistics, company annual reports and investor presentations, trade publications including Mobile Ecosystem Forum research, Gartner CPaaS analysis, and regional telecom association databases. E-commerce and digital banking data were sourced from Statista, World Bank digital finance reports, and central bank digital payment infrastructure disclosures.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, mobile penetration indices, digital commerce transaction volumes, and historical A2P messaging market evolution. Scenario analysis (base, optimistic, and conservative cases) was applied to account for macroeconomic uncertainty, RCS adoption timing variability, and competitive pricing dynamics.

A2P Messaging Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Platform, A2P Service |

| Deployment Modes Covered | On-premises, Cloud-based |

| SMS Traffics Covered | National Traffic, Multi-Country |

| Applications Covered | Authentication Services, Promotional and Marketing Services, Pushed Content Services, Interactive Messages Services, Customer Relationship Management Services, Others |

| End Users Covered | BFSI, Retail and Ecommerce, E-Governance, Hyperlocal Businesses, Healthcare, Travel and Hospitality, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Twilio Inc., Sinch, Telefonaktiebolaget LM Ericsson, Infobip Ltd., Syniverse Technologies, LLC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the A2P messaging market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global A2P messaging market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the A2P messaging industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the A2P Messaging Market Report

The global A2P messaging market reached USD 74.8 Billion in 2025, driven by enterprise demand for mobile communication, OTP authentication, and mobile marketing across BFSI, e-commerce, and healthcare verticals worldwide.

The market is projected to reach USD 102.0 Billion by 2034 at a CAGR of 3.40% during 2026-2034, supported by mobile subscriber growth, RCS Business Messaging adoption, and digital commerce expansion globally.

A2P Service leads with 67.7% share in 2025, driven by high-volume OTP delivery, managed transactional alert services, and compliance-driven messaging across BFSI, e-commerce, and healthcare enterprise deployments worldwide.

Cloud-based deployment dominates at 60.0% share in 2025, preferred for scalability, faster deployment, and lower total cost of ownership versus on-premises systems—especially among SMEs and digital-first businesses.

Asia Pacific dominates with 44.5% share in 2025. Mobile banking expansion, e-commerce transaction volumes in China and India, and Southeast Asia's digital commerce growth underpin its leadership through 2034.

Key drivers include rising mobile subscriber penetration, expanding e-commerce activity, OTP demand in digital banking, SMS 98% open rates, and growing enterprise investment in mobile customer engagement globally.

Cloud-based deployment (~4.2% CAGR) and Asia Pacific region (~4.5% CAGR) are the fastest-growing sub-categories, driven by SME adoption, fintech expansion in India, and e-commerce growth across Southeast Asia through 2034.

Key players include Twilio Inc., Sinch, Telefonaktiebolaget LM Ericsson, Infobip Ltd., and Syniverse Technologies, LLC.

RCS (Rich Communication Services) is the next-generation SMS protocol enabling multimedia, interactive messaging within native phone apps. RCS Business Messaging is expected to replace legacy A2P SMS at premium pricing tiers, driving higher per-message revenue and engagement rates through 2034.

Priority opportunities include RCS platform infrastructure, AI-native personalization engines, fraud detection technology, India and Southeast Asia market expansion, and omnichannel CPaaS platforms integrating SMS, voice, and OTT messaging in unified API frameworks.

Key challenges include grey-route SMS fraud, regulatory compliance complexity across TCPA/GDPR/TRAI frameworks, price compression in the aggregation tier, and competition from WhatsApp Business API and other OTT messaging platforms.

AI enables dynamic message personalization, predictive send-time optimization, intelligent opt-out management, and anti-spam detection.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)