Agriculture Equipment Market Size, Share, Trends and Forecast by Equipment Type, Application, Sales Channel, and Region, 2026-2034

Agriculture Equipment Market Size, Share, Trends & Forecast (2026-2034)

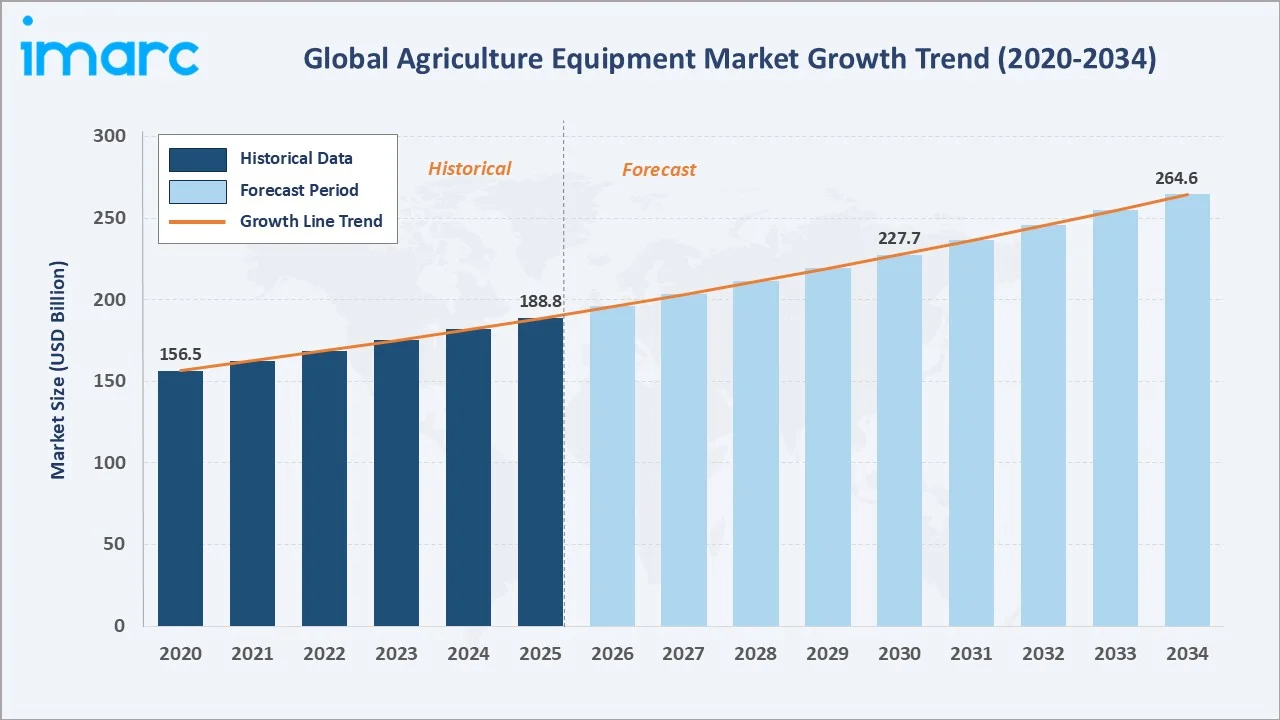

The agriculture equipment market was valued at USD 188.8 Billion in 2025 and is projected to reach USD 264.6 Billion by 2034, exhibiting a CAGR of 3.82% during 2026-2034. Growing farm mechanization across Asia-Pacific, rising demand for precision agriculture tools, government-backed subsidies for equipment modernization, and acute labor shortages are the primary drivers shaping market growth.

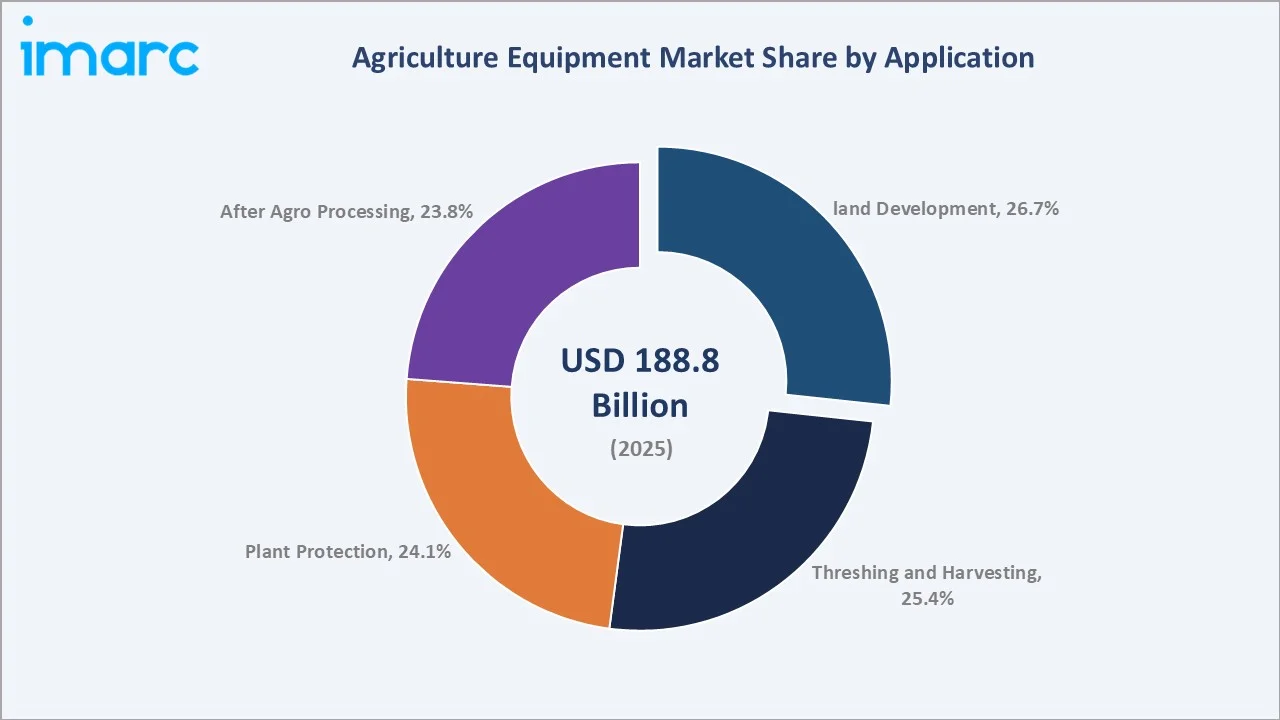

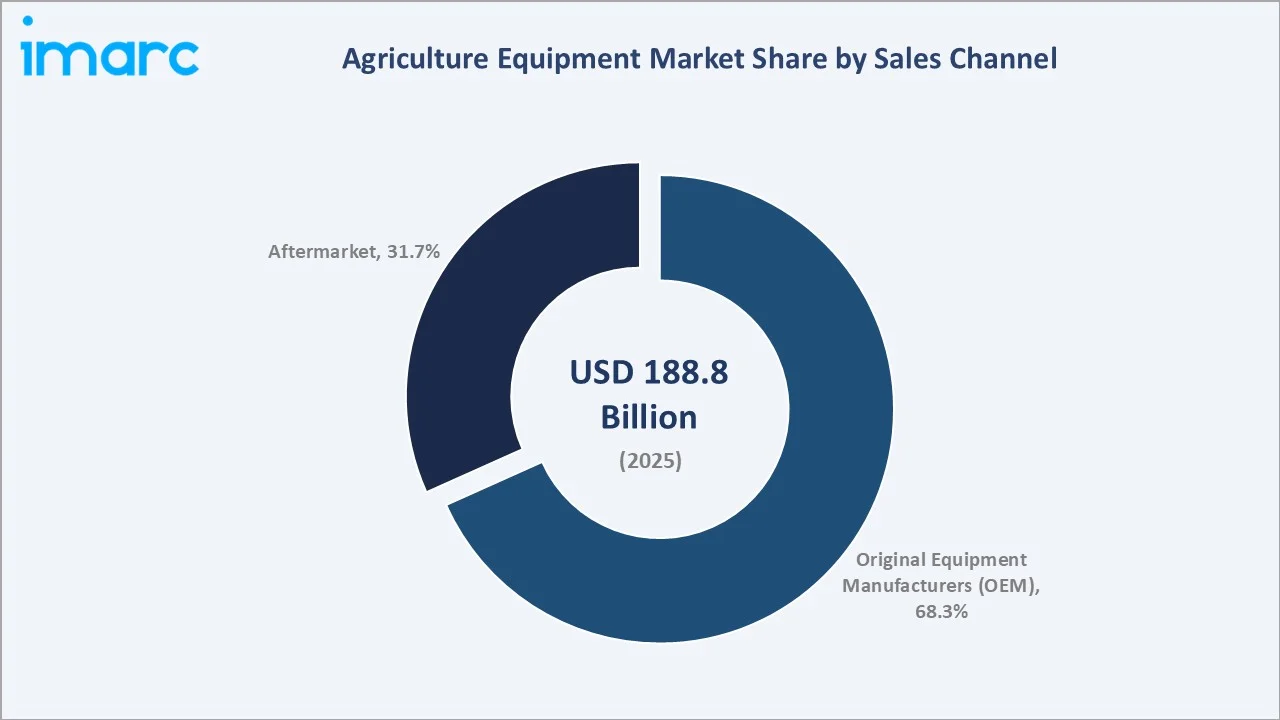

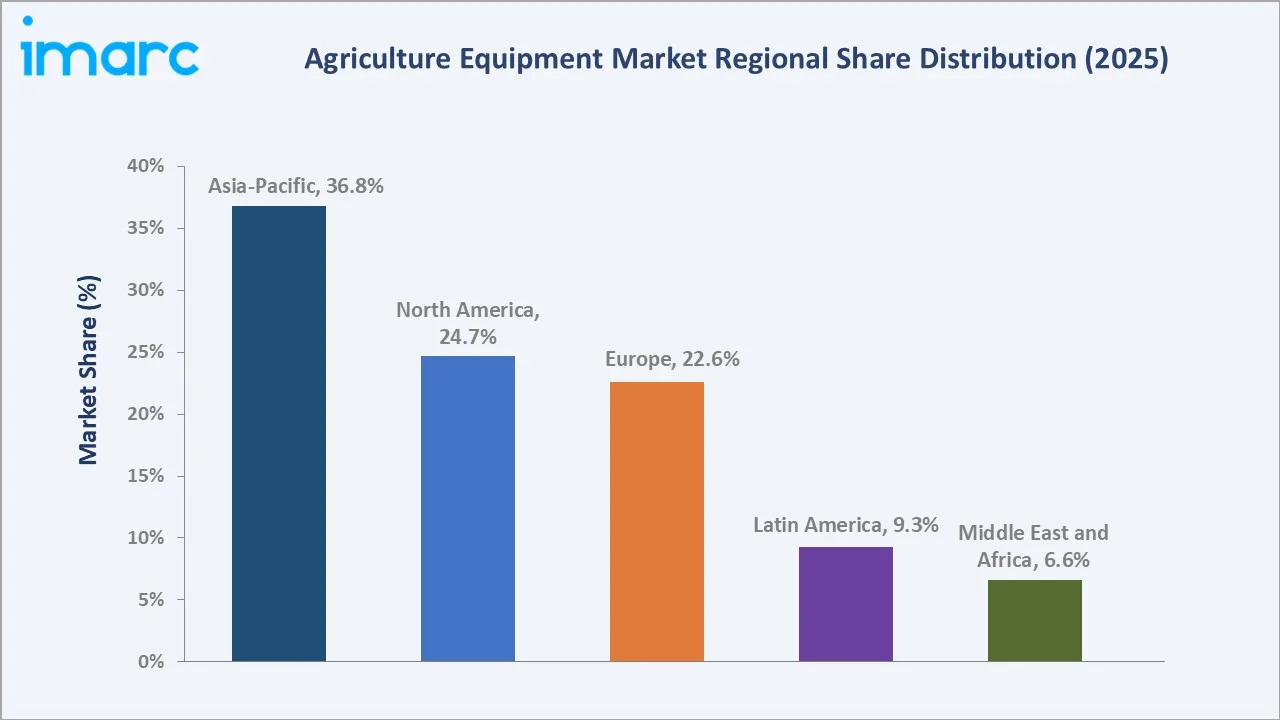

Land development leads the application segment at 26.7% in 2025, original equipment manufacturers (OEM) dominate the sales channel at 68.3%, and Asia-Pacific commands 36.8% regional share.

|

Metric |

Value |

|

Market Size (2025) |

USD 188.8 Billion |

|

Forecast Market Size (2034) |

USD 264.6 Billion |

|

CAGR (2026-2034) |

3.82% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (36.8%, 2025) |

|

Fastest Growing Region |

Latin America (4.60% CAGR, 2026-2034) |

|

Leading Application |

Land Development (26.7%, 2025) |

|

Leading Sales Channel |

Original Equipment Manufacturers (OEM) (68.3%, 2025) |

The agriculture equipment market expanded from USD 156.5 Billion in 2020 to USD 188.8 Billion in 2025, driven by increasing farm mechanization, government incentive schemes, and rising adoption of precision agriculture tools. Anchored at USD 227.7 Billion in 2030, the forecast to USD 264.6 Billion by 2034 is supported by expanding arable land in emerging economies, sustained demand for autonomous farming machinery, and growing integration of digital technologies in agricultural operations.

To get more information on this market, Request Sample

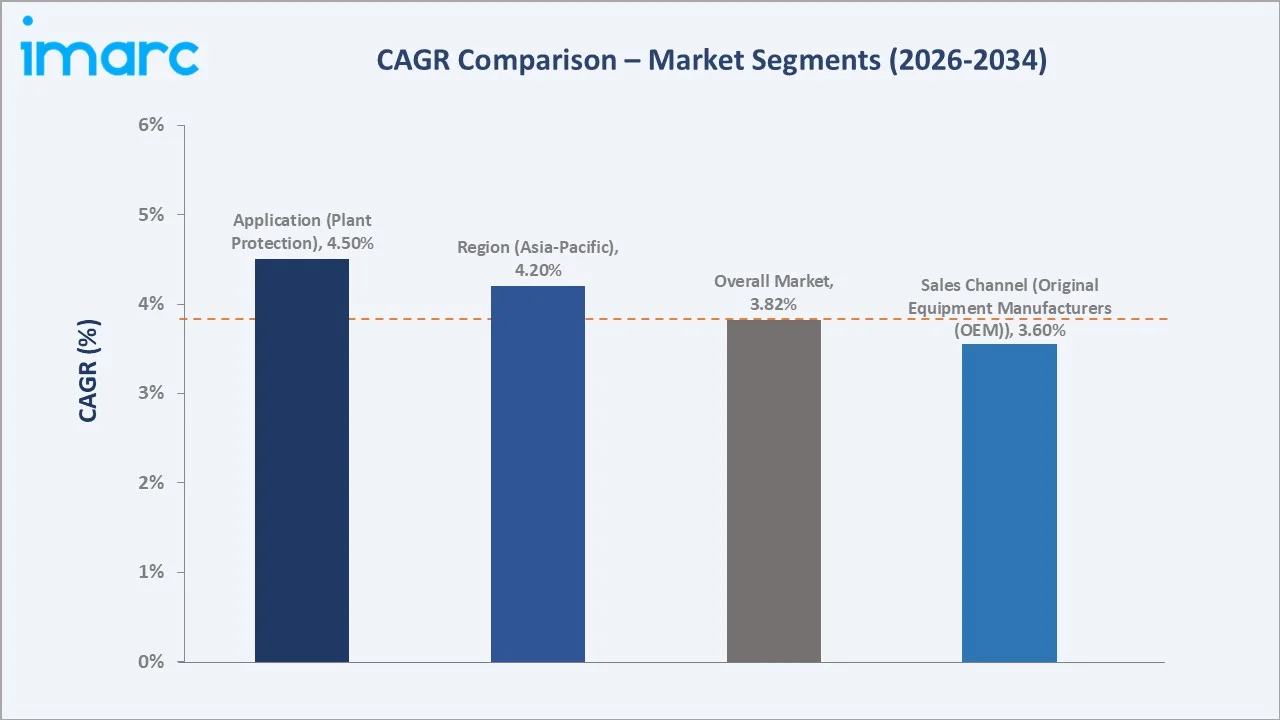

CAGR trajectories across application and sales channel sub-segments show plant protection and aftermarket categories expanding faster than the overall 3.82% market CAGR, driven by rising precision spraying demand and growing replacement equipment needs across aging farm fleets.

Executive Summary

The agriculture equipment market is on a steady growth path from USD 156.5 Billion in 2020 to USD 264.6 Billion by 2034. Farm mechanization has shifted from being a premium investment to an operational necessity across both developed and emerging agricultural economies. Falling equipment costs, rising food security concerns, and expanding crop cultivation areas are encouraging broader adoption of tractors, harvesters, sprayers, and ancillary farm machinery worldwide.

Land development commands the largest application share at 26.7% in 2025, supported by land clearing and soil preparation activities tied to expanding cultivation in Asia-Pacific and Latin America. Original equipment manufacturers (OEM) dominate the sales channel at 68.3%, reflecting strong manufacturer-dealer networks and bundled financing options. Asia-Pacific leads regional share at 36.8% in 2025, driven by large farm populations in India, China, and Southeast Asia. Agriculture serves as a fundamental pillar of India’s economy and society, supporting the livelihoods of almost 55% of its population, as of February 2026.

Key Market Insights

|

Insight |

Data |

|

Leading Application |

Land Development – 26.7% share (2025) |

|

Second Largest Application |

Threshing and Harvesting – 25.4% share (2025) |

|

Leading Sales Channel |

Original equipment manufacturers (OEM) – 68.3% share (2025) |

|

Second Largest Sales Channel |

Aftermarket – 31.7% share (2025) |

|

Leading Region |

Asia-Pacific – 36.8% share (2025) |

|

Fastest Growing Region |

Latin America (4.60% CAGR, 2026-2034) |

|

Top Companies |

Deere & Company, CNH Industrial N.V., AGCO Corporation, and Kubota Corporation |

Key Analytical Observations Expanding On The Data Above:

- Land development dominance at 26.7% reflects high demand for soil preparation, irrigation infrastructure, and land clearing equipment tied to expanding cultivation in emerging economies and intensified crop production in developed markets.

- Threshing and harvesting at 25.4% is supported by rising adoption of combine harvesters and mechanized threshers in cereal-producing regions. Growing farm labor shortages are accelerating the shift from manual harvesting to mechanized solutions across South and Southeast Asia.

- Original equipment manufacturers (OEM) dominance at 68.3% reflects the continued preference for new equipment purchases through authorized dealer channels, offering warranty support, financing options, and after-sales service packages that aftermarket channels cannot match.

- Aftermarket at 31.7% is driven by recurring replacement demand for wear-and-tear components, maintenance services, and retrofit upgrades that extend machinery lifespan and improve operational efficiency. Expanding mechanization in emerging agricultural economies is also strengthening demand for spare parts distribution networks and independent service providers.

- Asia-Pacific at 36.8% leads due to large farmland coverage, government mechanization schemes in India and China, and rapid expansion of rice and wheat cultivation.The overall wheat output from eight key wheat-producing states in India as of March 31, 2025, was projected to reach 122.724 Million Tons. Deep rural credit penetration and subsidized tractor ownership programs are key structural supports.

Agriculture Equipment Market Overview

Agriculture equipment encompasses a broad range of mechanized tools and machinery used across all stages of crop production, from soil preparation and planting to harvesting, threshing, and post-harvest processing. Key product categories include tractors, combine harvesters, planters, tillers, sprayers, seed drills, and balers.

The global ecosystem integrates raw material suppliers, drivetrain and engine manufacturers, precision technology providers, OEM assemblers, dealer-distributor networks, and end-user farming enterprises. Macroeconomic factors such as commodity price cycles, rural credit availability, and government farm support budgets materially influence equipment purchase cycles. Rising food inflation, climate-driven crop volatility, and digital agriculture adoption are reshaping equipment demand patterns across all regions.

Market Dynamics

To evaluate market opportunities, Request Sample

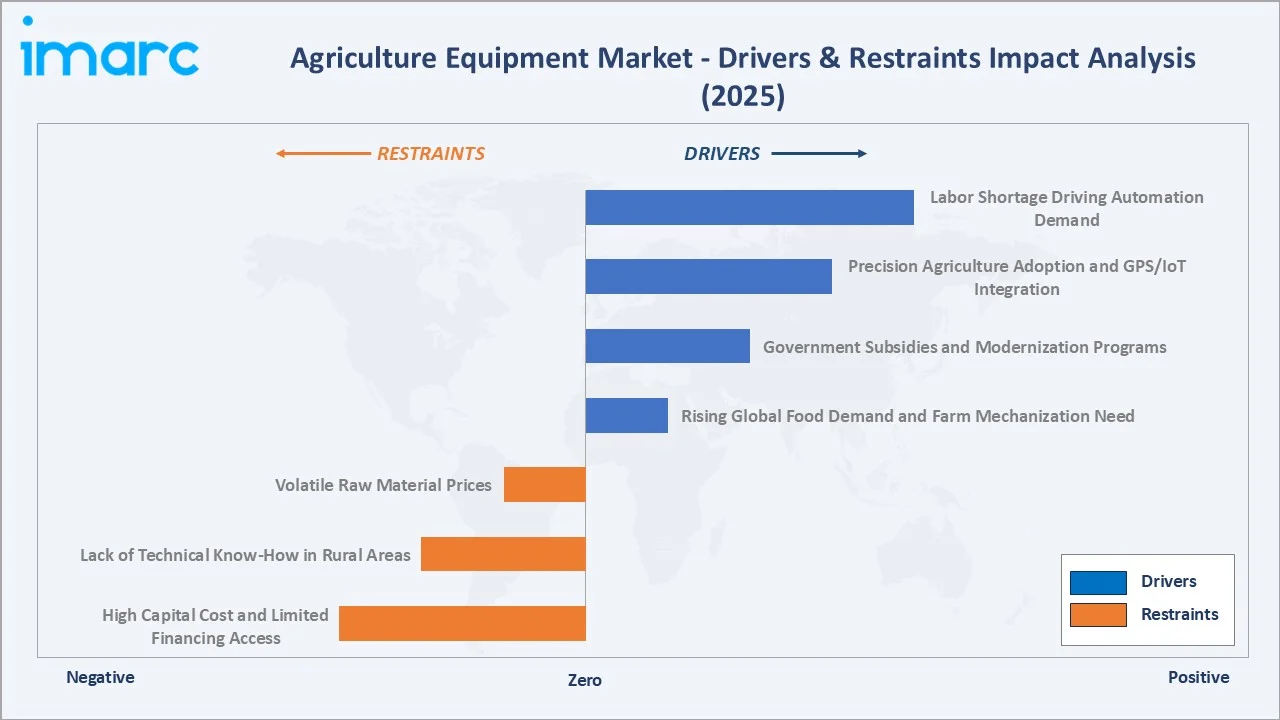

Market Drivers

- Rising Global Food Demand and Farm Mechanization Need: Expanding global population and shifting dietary preferences toward protein-intensive diets are increasing pressure on agricultural output. Farm mechanization offers a critical solution by raising yield per acre and reducing post-harvest losses, making equipment adoption a strategic necessity for food-producing nations.

- Government Subsidies and Modernization Programs: Public sector support through direct subsidies, tax exemptions, and low-interest rural credit programs is significantly lowering the effective cost of farm equipment. National mechanization missions across India, China, Brazil, and African nations are channeling billions annually toward equipment adoption, ensuring sustained market demand.

- Precision Agriculture Adoption and GPS/IoT Integration: Farmers are increasingly adopting GPS-guided tractors, variable-rate seeding systems, and sensor-based soil monitoring tools to optimize input use and improve yield outcomes. This shift toward data-driven farming is expanding the addressable market for advanced, higher-value equipment categories.

- Labor Shortage Driving Automation Demand: Accelerating rural-to-urban migration is reducing the availability of agricultural labor, particularly during planting and harvesting seasons. According to the Economic Survey 2023-24, it is anticipated that over 40% of India's population will reside in urban regions by 2030. Farmers are substituting labor with mechanized solutions, creating steady structural demand for combine harvesters, automated planters, and post-harvest processing equipment.

Market Restraints

- High Capital Cost and Limited Financing Access: Full-featured agricultural machinery requires substantial capital outlay, posing a significant adoption barrier for smallholder and subsistence farmers in low-income regions. Even as equipment costs have declined moderately, access to formal rural credit remains constrained in Sub-Saharan Africa, parts of South Asia, and rural Latin America, limiting the pace of mechanization.

- Lack of Technical Know-How in Rural Areas: Operating and maintaining advanced mechanized equipment requires a level of technical expertise that is often unavailable in smallholder farming communities. The absence of trained operators, local service networks, and spare parts availability constrains the productive use of equipment in remote agricultural zones.

- Volatile Raw Material Prices: Steel, aluminum, and electronic component prices directly affect manufacturing costs for agricultural machinery. Sharp commodity price cycles and supply chain disruptions create margin pressure for equipment manufacturers and translate into price volatility that deters farm purchases, particularly in price-sensitive emerging markets.

Market Opportunities

- Smart Farming and IoT Integration: The convergence of AI, machine learning (ML), and connected sensors with agricultural equipment is opening significant new revenue streams. Manufacturers that embed real-time diagnostics, remote monitoring, and yield mapping into equipment platforms are capturing premium pricing and recurring software service revenues.

- Emerging Market Expansion: Sub-Saharan Africa, South and Southeast Asia, and Central Asia represent large under-mechanized agricultural regions with growing rural incomes and government mechanization ambitions. Affordable entry-level equipment, local assembly partnerships, and microfinancing models are unlocking broad market access in these high-potential geographies.

Market Challenges

- Supply Chain Disruptions and Raw Material Volatility: Agricultural equipment manufacturers face ongoing risks from supply disruptions in steel, semiconductors, and hydraulic components. Extended lead times and cost escalation in global supply chains increase production costs and delay delivery timelines, compressing margins and customer satisfaction.

- Stringent Emission Regulations: Tightening off-road engine emission standards in the European Union, United States, and increasingly in India and China require manufacturers to invest significantly in compliant drivetrain development. Meeting emission norms adds product complexity and cost, particularly for smaller equipment makers.

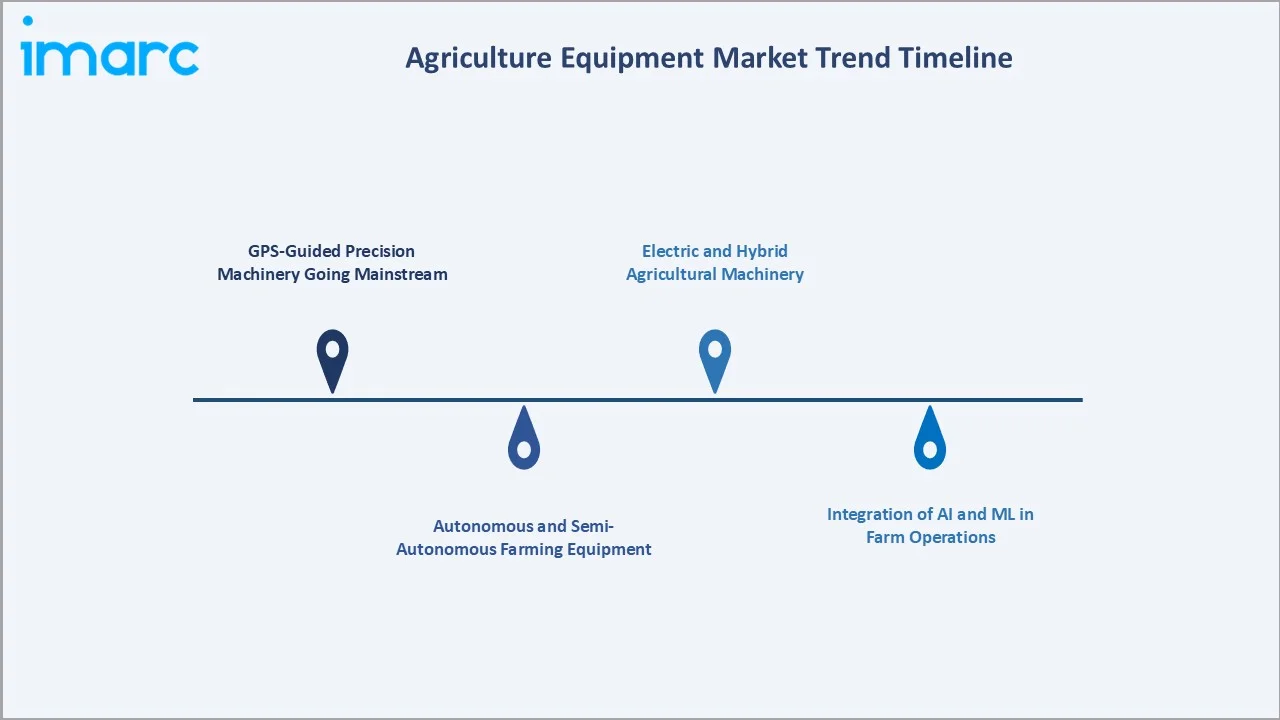

Emerging Market Trends

1. GPS-Guided Precision Machinery Going Mainstream

GPS-based auto-steering and variable-rate application systems, once exclusive to large commercial farms, are becoming standard configurations across mid-tier tractor models. Falling GNSS component costs and simplified user interfaces are extending adoption to smallholder operators in Asia-Pacific and Latin America. This trend is fundamentally reshaping equipment value propositions and average selling prices.

2. Autonomous and Semi-Autonomous Farming Equipment

Major OEMs are commercializing autonomous tractor platforms that can perform tillage, planting, and transport operations without a human operator. Semi-autonomous systems with remote monitoring capabilities are already deployed on large farms in North America and Europe. As regulatory frameworks evolve and proving grounds expand, autonomy features are expected to enter volume production models well before 2034.

3. Electric and Hybrid Agricultural Machinery

Several leading manufacturers have launched electric tractor prototypes and light-duty electric utility vehicles for farming operations. Battery-powered equipment offers lower operating costs and zero tail-pipe emissions, aligning with sustainability mandates across the European Union and North America. While current adoption remains limited to smaller-horsepower segments, the trend is expected to scale meaningfully through the forecast period.

4. Integration of AI and ML in Farm Operations

AI-powered platforms are enabling predictive maintenance scheduling, automated yield forecasting, and real-time disease detection when integrated with connected equipment. Equipment manufacturers and agri-tech firms are partnering to embed ML models into in-cab displays and fleet management software, adding software-as-a-service revenue layers to traditional equipment sales models.

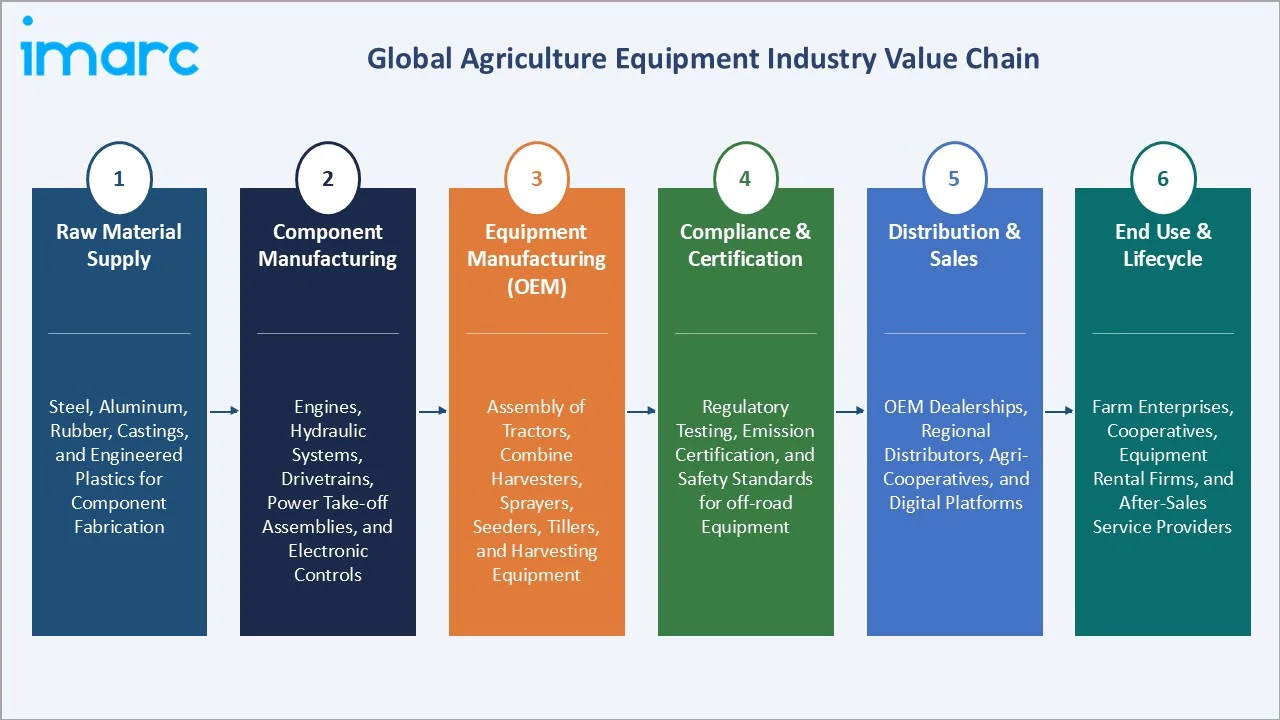

Industry Value Chain Analysis

The agriculture equipment value chain spans six core stages, from raw material procurement through end-of-life services. OEM manufacturing and precision technology integration capture the highest value-add, while dealer network depth and after-sales service capabilities generate downstream competitive advantage in this capital-intensive industry.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of steel, aluminum, rubber, castings, and engineered plastics supporting component fabrication and structural assembly needs |

|

Component Manufacturing |

Manufacturers of engines, hydraulic systems, drivetrains, power take-off assemblies, and precision electronic controls for agricultural machinery |

|

Equipment Manufacturing (OEM) |

Full-scale assembly operations producing tractors, combine harvesters, sprayers, seeders, tillers, and specialty harvesting equipment |

|

Compliance & Certification |

Regulatory testing bodies, emission certification agencies, and safety standards organizations governing off-road equipment approvals across key markets |

|

Distribution & Sales |

OEM-authorized dealerships, regional distributors, agri-cooperatives, and digital commerce platforms serving farmer end-markets |

|

End Use & Lifecycle |

Farm enterprises, agricultural cooperatives, equipment rental firms, and after-sales maintenance and spare parts service providers |

Vertically integrated manufacturers that engineer proprietary drivetrains and develop in-house hydraulic and precision technology systems achieve stronger cost control, operational efficiency, and supply chain stability compared to assemblers dependent on third-party component sourcing.

Technology Landscape in the Agriculture Equipment Industry

Precision Navigation and GNSS Technology

Multi-constellation GNSS receivers enabling sub-inch auto-steering accuracy are now available across a wide range of tractor models. Real-time kinematic (RTK) correction networks, often operated by national authorities or OEM subscription services, are expanding precision coverage into previously underserved rural areas.

Variable Rate Technology and Precision Seeding

Variable rate application (VRA) systems use field prescription maps derived from soil sampling and remote sensing data to automatically adjust seed, fertilizer, and chemical inputs across field zones. Pneumatic precision seeders and section control planters reduce input waste and improve stand uniformity, delivering measurable yield and cost benefits.

Autonomous Machinery and Robotics

Autonomous tractor platforms, robotic weeders, and self-guided sprayers are progressing from demonstration to limited commercial deployment. Machine vision systems, LiDAR sensors, and advanced path-planning algorithms are enabling equipment to operate reliably in unstructured outdoor environments.

Connectivity, Telematics, and Smart Fleet Management

Cloud-connected equipment telemetry platforms collect engine health, fuel consumption, and field productivity data across large farm fleets. Remote diagnostics reduce downtime by enabling predictive maintenance scheduling, while integrated farm management software connects equipment data with agronomic planning tools for end-to-end operational optimization.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Equipment Type |

Agricultural Tractor |

35.9% |

2025 |

|

Application |

Land Development |

26.7% |

2025 |

|

Sales Channel |

Original Equipment Manufacturers (OEM) |

68.3% |

2025 |

|

Region |

Asia-Pacific |

36.8% |

2025 |

By Application

Land development commands a 26.7% majority share in 2025, supported by strong demand for tractors equipped with front-end loaders, disk plows, and sub-soilers used in land clearing, soil inversion, and seedbed preparation. Land development activities are directly tied to agricultural expansion and intensification programs across Asia-Pacific, Sub-Saharan Africa, and Latin America.

To access detailed market analysis, Request Sample

Threshing and harvesting at 25.4% in 2025 is sustained by broad combine harvester adoption in cereal-producing nations and growing use of crop-specific harvesting machinery for rice, sugarcane, and vegetables. Seasonal labor shortages and the need to minimize post-harvest losses are further accelerating investment in high-capacity mechanized harvesting and threshing equipment across both large-scale and commercial farming operations.

By Sales Channel

Original equipment manufacturers (OEM) dominate with 68.3% share in 2025, reflecting the continued preference for new equipment purchases through authorized manufacturer channels. OEM purchases offer warranty coverage, operator training, financing packages, and service contracts that provide holistic ownership support. Fleet operators, agri-cooperatives, and large commercial farms consistently prefer OEM channels for primary equipment acquisition.

Aftermarket at 31.7% in 2025 is growing through independent spare parts distributors, remanufactured component suppliers, and digital parts marketplaces. This channel serves cost-conscious smallholder farmers and operators seeking replacement parts for aging equipment fleets. The growth of the aftermarket channel is further supported by the increasing age of installed equipment in developing regions.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

36.8% |

Large farming population, government mechanization programs, expanding arable land, and growing adoption of precision agriculture tools |

|

North America |

24.7% |

Advanced precision agriculture adoption, high farm consolidation, strong OEM dealer networks, and technology-driven equipment upgrades |

|

Europe |

22.6% |

Sustainability-driven equipment upgrades, emission compliance mandates, strong crop output, and high adoption of GPS-guided farm machinery |

|

Latin America |

9.3% |

Expanding soybean and sugarcane cultivation, rising rural incomes, government credit programs, and growing farm mechanization in Brazil and Argentina |

|

Middle East and Africa |

6.6% |

Food security investments, expanding irrigated farmland, government-sponsored mechanization schemes, and rising donor-funded agricultural development programs |

Asia-Pacific at 36.8% in 2025 leads the global market, anchored by India and China where government subsidization of tractor and equipment purchases, large smallholder farmer populations, and rapidly increasing crop output are sustaining high equipment demand. Expanding two-wheel tractor and power tiller adoption in Southeast Asia and rising use of combine harvesters in South Asia are adding incremental volume.

North America at 24.7% is characterized by large-scale commercial farming operations deploying high-horsepower, technology-rich equipment suites. Fleet replacement cycles, precision agriculture upgrades, and growing adoption of autonomous field operations are sustaining North American demand.

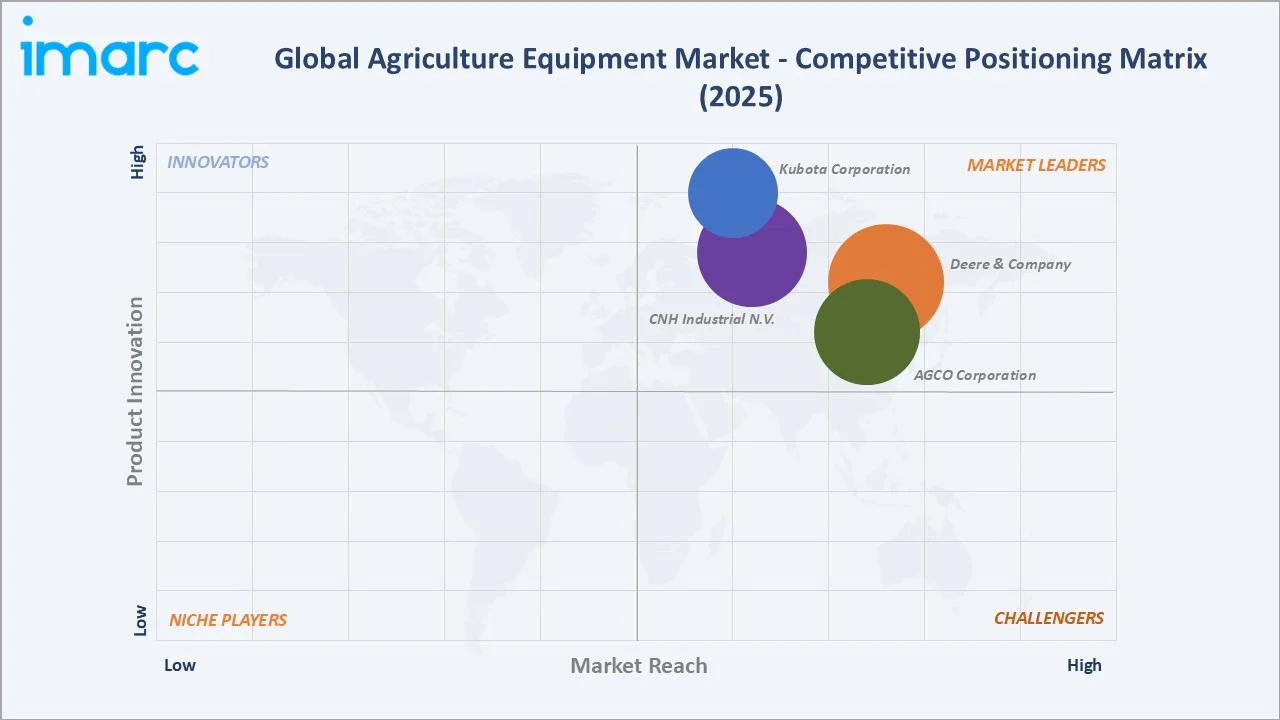

Competitive Landscape

The agriculture equipment market is moderately fragmented, with global OEM leaders holding dominant brand recognition and distribution reach while regional specialists serve price-sensitive or crop-specific equipment niches. Dealer network depth, technology platform capability, and after-sales service quality form the primary competitive moats in this capital equipment category.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Deere & Company |

John Deere 8R Series |

Leader |

Precision agriculture technology leadership; global dealer network depth |

|

CNH Industrial N.V. |

Case IH Magnum |

Leader |

Dual-brand global platform; in-house engine and drivetrain integration; broad horsepower range coverage |

|

AGCO Corporation |

Fendt |

Leader |

Premium Fendt positioning; multi-brand coverage across price tiers |

|

Kubota Corporation |

Kubota |

Leader |

Compact and mid-range tractor dominance; strong Asia-Pacific dealer network; agri-solutions expansion |

Key players include Deere & Company, CNH Industrial N.V., AGCO Corporation, and Kubota Corporation, among others.

Key Company Profiles

Deere & Company

Deere & Company is a leading global manufacturer of agricultural equipment, offering a broad range of tractors, combine harvesters, planters, and sprayers through the John Deere brand. The company operates across several countries and is supported by an extensive network of authorized dealers and service centers.

- Product Portfolio: John Deere 8R Series tractors, precision planting systems, and self-propelled sprayers.

- Recent Developments: In February 2026, Deere & Company launched a redesigned 8R and 8RX tractor lineup featuring a new JD14 engine and supervised autonomy features, including advanced headland management and path planning.

- Strategic Focus: Continuous investment in precision agriculture technology, autonomous and semi-autonomous equipment platforms, electric power offboarding solutions, and expanding global dealer and service coverage.

CNH Industrial N.V.

CNH Industrial N.V. is a global manufacturer of agricultural and construction equipment, operating brands across a comprehensive range of tractors, harvesters, planters, and hay tools. The company maintains a broad manufacturing and distribution network spanning North America, Europe, Asia, and Latin America.

- Product Portfolio: Case IH Magnum Series tractors; Case IH Steiger 715 Quadtrac tractor.

- Recent Developments: CNH Industrial continues to advance sustainable fuel alternatives and connected fleet management capabilities, with ongoing investments in precision agriculture technology across its Case IH brand portfolio.

- Strategic Focus: Dual-brand market coverage, in-house engine and drivetrain manufacturing, alternative fuel equipment development, and precision agriculture platform integration.

AGCO Corporation

AGCO Corporation is a global designer, manufacturer, and distributor of agricultural machinery, operating through multiple brands, including Fendt. The company serves a wide spectrum of farming operations, from smallholder to large commercial scale, across several countries.

- Product Portfolio: Fendt Vario Series tractors; Fendt IDEAL combine harvesters.

- Recent Developments: AGCO continues to strengthen its multi-brand product portfolio and digital agriculture capabilities, with ongoing investments in precision farming platforms, fleet management solutions, and expanding its dealer and service infrastructure across key growth regions.

- Strategic Focus: Premium Fendt brand positioning, multi-brand price-tier coverage, digital agriculture platform expansion, and broadening global distribution and after-sales capabilities.

Market Concentration Analysis

The agriculture equipment market is moderately concentrated, with the top four companies – Deere & Company, CNH Industrial N.V., AGCO Corporation, and Kubota Corporation – estimated to collectively hold approximately 55-65% of global equipment revenue in 2025. The remainder is distributed across regional specialists, local OEMs, and niche segment manufacturers.

Barriers to entry include significant capital requirements for manufacturing scale, lengthy OEM dealer relationship development, and the regulatory compliance costs associated with emission certifications across multiple jurisdictions. Software platform investment, proprietary telematics ecosystems, and established service network infrastructure further reinforce the competitive positions of incumbent leaders.

Consolidation is accelerating through precision agriculture technology acquisitions, software platform partnerships, and dealer channel consolidations. Scale advantages in global sourcing, component manufacturing, and after-sales service are strengthening the structural moats of established players, particularly as equipment complexity and technology content increase.

Investment & Growth Opportunities

Fastest-Growing Segments

Plant protection at 24.1% is expanding faster than the overall 3.82% CAGR through 2034, driven by precision spraying demand and drone-based application adoption. Aftermarket at 31.7% is growing as aging installed equipment bases in developing markets generate sustained replacement parts and service revenue opportunities.

Emerging Markets

Sub-Saharan Africa, South Asia, and Southeast Asia represent the largest under-mechanized opportunities, with low current mechanization ratios and strong structural drivers including rising food demand, expanding arable land, and improving rural credit access. Latin America, led by Brazil and Argentina, offers premium commercial farming expansion opportunities tied to soybean, corn, and sugarcane production growth.

Venture & Investment Trends

Investment is concentrated in autonomous farm machinery, AI-powered crop management platforms, electric and alternative-fuel tractors, and digital marketplace models connecting farmers to equipment financing and services. Strategic capital is also flowing into agri-drone manufacturers, precision irrigation equipment, and soil health monitoring technologies that integrate with mechanized field operations.

Future Market Outlook (2026-2034)

The agriculture equipment market is forecast to expand from USD 188.8 Billion in 2025 to USD 264.6 Billion by 2034 at a CAGR of 3.82%, adding approximately USD 75.8 Billion in incremental annual market value over the forecast period.

Four structural forces will shape the market through 2034: continued farm mechanization in Asia-Pacific and Africa; precision agriculture technology embedding into mid-range and entry-level equipment; electrification and alternative fuel adoption in line with sustainability mandates; and software platform monetization shifting equipment value from one-time hardware sales to recurring service revenues.

By 2034, autonomous field operations will be commercially deployed across large-scale farming in developed markets, and semi-autonomous capabilities will be available across mainstream tractor and combine lines. Asia-Pacific will consolidate its position as the single largest market, while Latin America will emerge as the fastest-growing region, driven by continued agricultural frontier expansion and improving rural infrastructure.

Research Methodology

Primary Research

Primary research included structured interviews with senior product managers at leading equipment manufacturers, regional distributors, agri-cooperative procurement officials, precision agriculture technology suppliers, and large-scale farm operators. Findings were used to validate market sizing estimates, segmentation splits, and regional demand dynamics.

Secondary Research

Secondary sources included FAO Agricultural Mechanization databases, national agriculture ministry reports, USDA NASS farm equipment surveys, European Commission agricultural statistics, industry association publications from CEMA (Europe) and AEM (North America), and annual reports, investor presentations, and product launch announcements from listed equipment manufacturers.

Forecasting Models

Market forecasts employed top-down and bottom-up modeling methodologies, incorporating equipment unit shipment data, average selling price trends, regional mechanization indices, government subsidy program pipelines, and macroeconomic growth projections. Scenario analysis was applied to test forecast sensitivity against commodity price cycles and agricultural credit availability variations.

Agriculture Equipment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Equipment Types Covered | Agriculture Tractor, Harvesting Equipment, Irrigation and Crop Processing Equipment, Agriculture Spraying and Handling Equipment, Soil Preparation and Cultivation Equipment, and Others |

| Applications Covered | Land Development, Threshing and Harvesting, Plant Protection, After Agro Processing |

| Sales Channels Covered | Original Equipment Manufacturers (OEM), Aftermarket |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the agriculture equipment market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global agriculture equipment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the agriculture equipment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Agriculture Equipment Market Report

The agriculture equipment market was valued at USD 188.8 Billion in 2025, supported by rising farm mechanization demand, government subsidy programs, and increasing precision agriculture adoption across major producing regions.

The market is projected to grow at a CAGR of 3.82% from 2026 to 2034, reaching USD 264.6 Billion, driven by ongoing mechanization needs, labor shortage-driven automation, and technology integration in farm equipment.

Land development leads the application segment with a 26.7% share in 2025, driven by soil preparation, land clearing, and irrigation infrastructure activities tied to agricultural expansion programs across Asia-Pacific and Latin America.

Original equipment manufacturers (OEM) dominate with 68.3% share in 2025, reflecting strong manufacturer-dealer networks, bundled financing, warranty services, and comprehensive after-sales support that drive new equipment purchases through authorized channels.

Asia-Pacific holds the largest share at 36.8% in 2025, led by India and China, where large farming populations, government mechanization programs, and expanding crop production are driving sustained equipment demand.

Leading companies include Deere & Company, CNH Industrial N.V., AGCO Corporation, and Kubota Corporation, among others.

Key trends include precision agriculture adoption, development of autonomous and semi-autonomous farm machinery, electrification of tractors and light farm equipment, and integration of AI-powered crop management platforms with mechanized field operations.

Primary drivers include rising global food demand, acute farm labor shortages, government subsidies for equipment modernization, and growing adoption of GPS and IoT-enabled precision machinery across commercial and smallholder farming operations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)