Agriculture Industry in India Size, Share, Trends and Forecast by Subsectors, 2026-2034

Agriculture Industry in India Market Size, Share, Trends & Forecast (2026-2034)

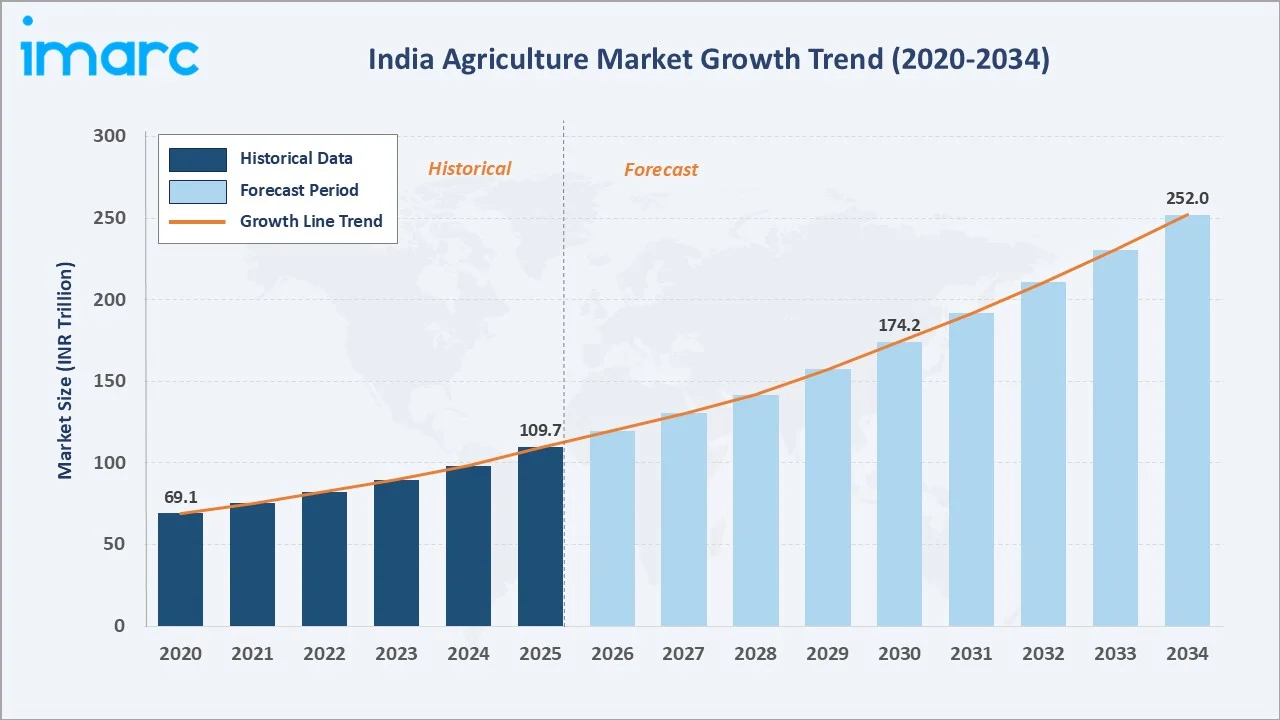

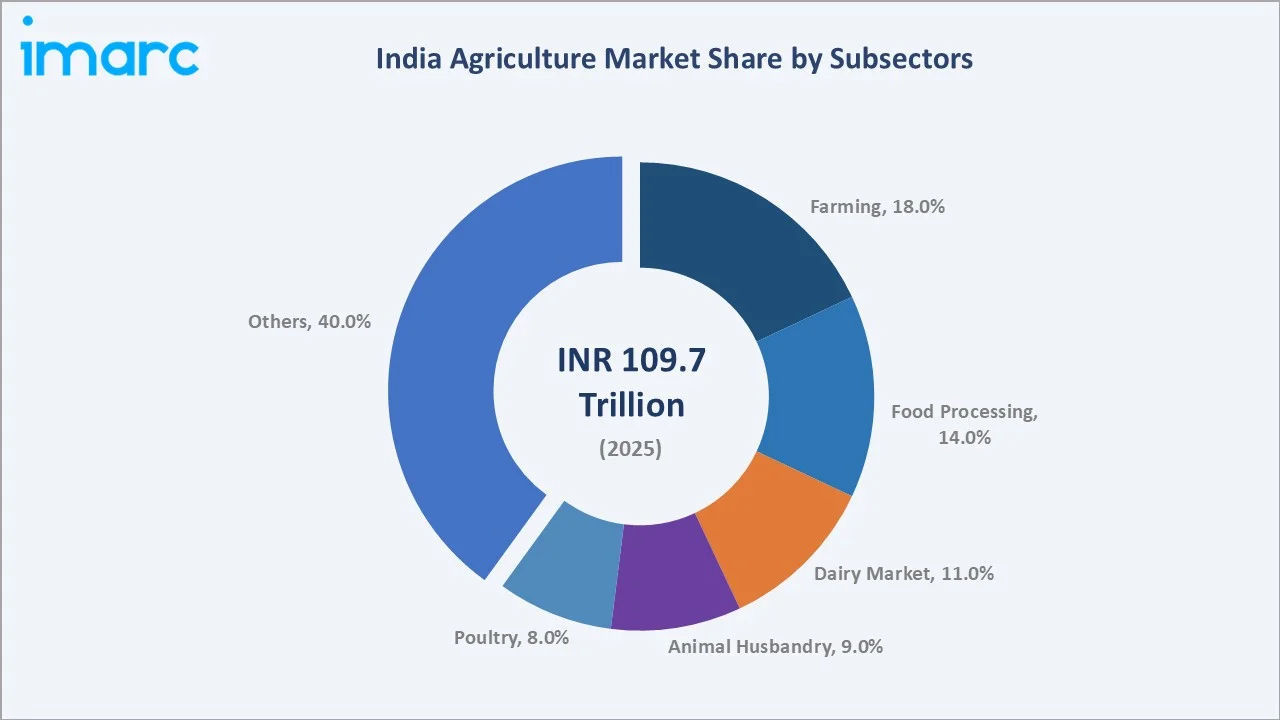

The agriculture industry in India was valued at INR 109.7 Trillion in 2025 and is projected to reach INR 252.0 Trillion by 2034, exhibiting a CAGR of 9.68% during 2026-2034. The market is driven by robust government policy support, expanding food processing capacity, rising food demand, and rapid AgriTech adoption. As of November 2025, the Pradhan Mantri Kisan Samman Nidhi (PM-KISAN) scheme disbursed more than 3.70 Lakh Crores to over 11 Crore farmer families since inception, anchoring farm-level investment.

Farming leads the subsectors segment at 18.0% in 2025, fueled by extensive cultivation of food grains, fruits, vegetables, and cash crops, supported by favorable government initiatives, expanding irrigation coverage, and rising domestic food consumption.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 109.7 Trillion |

|

Forecast Market Size (2034) |

INR 252.0 Trillion |

|

CAGR (2026-2034) |

9.68% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Subsector |

Farming (18.0%, 2025) |

|

Second Largest Subsector |

Food Processing (14.0%, 2025) |

The agriculture industry in India expanded from INR 69.1 Trillion in 2020 to INR 109.7 Trillion in 2025, reflecting consistent growth across farming, food processing, and allied sectors. Anchored at INR 174.2 Trillion in 2030, the forecast to INR 252.0 Trillion by 2034 is supported by rising domestic consumption, expanding export markets, cold chain infrastructure development, and digital transformation of agri supply chains.

To get more information on this market, Request Sample

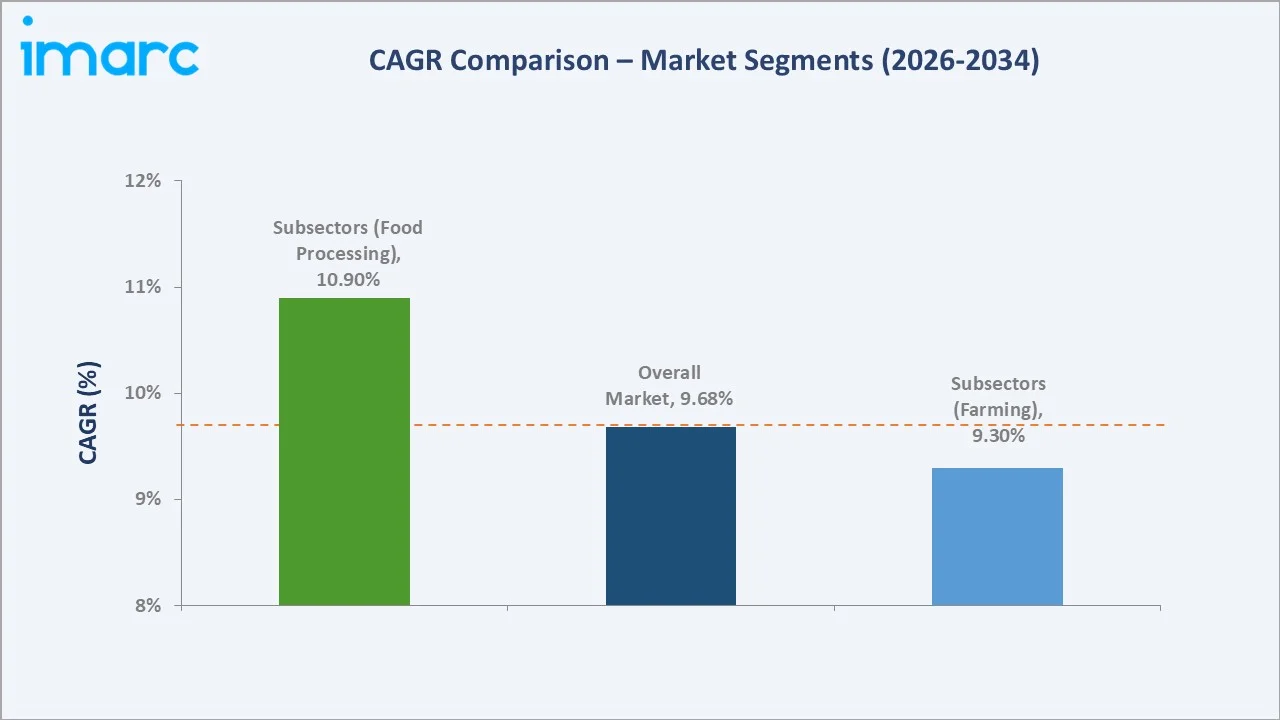

CAGR trajectories across subsectors show food processing and bio-agriculture market expanding faster than the overall 9.68% market CAGR, driven by evolving consumer preferences, value-addition opportunities, and increasing institutional investment in downstream processing infrastructure.

Executive Summary

The agriculture industry in India is on a sustained growth trajectory, expanding from INR 69.1 Trillion in 2020 to INR 252.0 Trillion by 2034. The sector has progressively moved from subsistence-oriented primary production to a diversified, value-chain-driven ecosystem encompassing food processing, dairy, animal husbandry, fisheries, cold chain logistics, and AgriTech-enabled services. Rising incomes, urbanization, and a growing middle class are reshaping food consumption patterns, while government flagship programs continue to anchor investment at the farm level.

Farming commands the largest subsector share at 18.0% in 2025, supported by extensive cultivable land and diverse agro-climatic zones. The segment also benefits from strong demand for staple crops, ongoing mechanization, improved seed adoption, and increasing integration with domestic and export-oriented agricultural value chains. The budget allocation for the Department of Agriculture and Farmers Welfare rose from INR 21,933.50 Crore (around USD 2.64 Billion) in 2013-2014 to INR 1,27,290.16 Crore (around USD 15.34 Billion) for 2025-26, indicating a significant increase in government expenditure during this timeframe.

Key Market Insights

|

Insight |

Data |

|

Leading Subsector |

Farming – 18.0% share (2025) |

|

Second Largest Subsector |

Food Processing – 14.0% share (2025) |

|

Top Companies |

ITC, GCMMF, UPL, and DCM Shriram |

Key Analytical Observations Expanding On The Data Above:

- Farming at 18.0% remains the largest subsector in 2025, underpinned by extensive crop cultivation, favorable agro-climatic diversity, strong domestic food demand, and continued government support for productivity enhancement, irrigation expansion, and farm modernization.

- Food processing at 14.0% is expanding on the back of growing organized retail, rising export of processed foods, and increasing private equity investment in downstream value-addition facilities across food parks and special economic zones. Between April 2000 and December 2024, the food processing industry attracted a total of USD 13.01 Billion in FDI.

Agriculture Industry in India Market Overview

The agriculture industry in India encompasses the production, processing, storage, distribution, and export of crops, livestock products, fisheries, and allied agricultural commodities. The ecosystem integrates input suppliers, primary producers, processors, cooperative societies, commodity exchanges, logistics providers, retail networks, and export trade channels operating across India's diverse agro-climatic zones.

The sector spans seventeen distinct subsectors, ranging from large-scale farming and food processing at the core, to emerging categories, such as bio-agriculture market, floriculture, apiculture, and sericulture at the periphery. The Indian government, through agencies, such as the Ministry of Agriculture and Farmers' Welfare and state agricultural departments, plays a central role in shaping input availability, price discovery, credit access, and market linkages.

Market Dynamics

To evaluate market opportunities, Request Sample

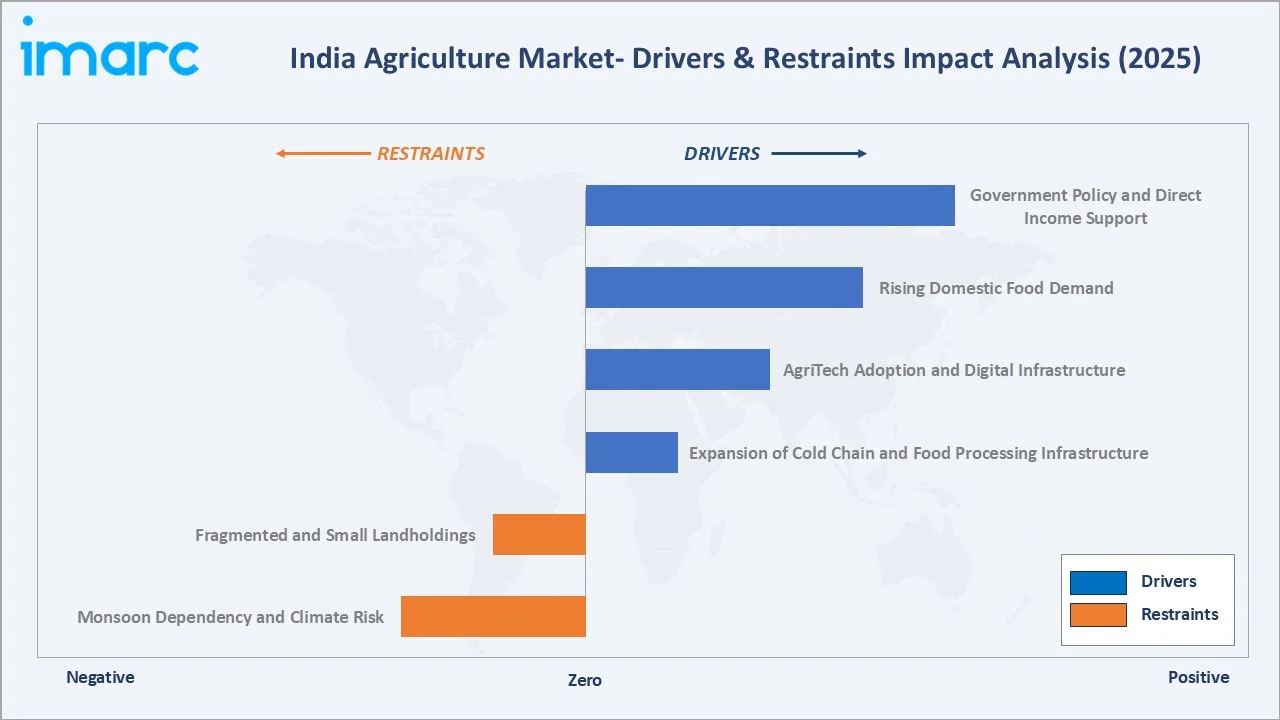

Market Drivers

- Government Policy and Direct Income Support: The PM-KISAN scheme and expanded minimum support price coverage collectively provide farmers with income security and production incentives, directly supporting farm-level investment and agricultural output growth.

- Rising Domestic Food Demand: A population of 1,425,775,850 as of April 2023, growing urbanization, rising per capita incomes, and shifting dietary preferences toward processed and protein-rich foods are creating sustained demand across farming, dairy, poultry, food processing, and fisheries subsectors.

- AgriTech Adoption and Digital Infrastructure: Rapid adoption of precision farming technologies, drone-based crop monitoring, IoT-enabled soil sensors, and the AgriStack digital public infrastructure are improving farm productivity and reducing input wastage across India's diverse agricultural landscape.

- Expansion of Cold Chain and Food Processing Infrastructure: Government-funded schemes are facilitating creation of integrated cold chain networks, food processing clusters, and mega food parks, directly supporting value addition and reducing post-harvest losses.

Market Restraints

- Fragmented and Small Landholdings: The predominance of fragmented farm plots limits the efficient use of modern machinery, reduces operational efficiency, and constrains economies of scale. Smaller holdings also face challenges in accessing institutional finance, adopting advanced agricultural technologies, and securing favorable terms in input procurement and crop marketing.

- Monsoon Dependency and Climate Risk: A significant proportion of India's cultivated area remains dependent on monsoon rainfall. Erratic monsoon patterns, rising temperatures, and increasing frequency of extreme weather events elevate production risk and contribute to yield volatility across key crop categories.

Market Opportunities

- Export Market Expansion: Growing international demand for agricultural commodities, processed foods, seafood, spices, and dairy products presents significant opportunities for the agriculture industry in India. Expanding trade partnerships, improving quality and phytosanitary compliance, strengthening supply chain infrastructure, and increasing value-added processing are expected to enhance India's competitiveness in global agricultural markets through the forecast period.

- Bio-Agriculture and Sustainable Farming: Growing consumer and regulatory preference for organic, bio-based, and chemical-free food products is creating demand for biopesticides, bio-fertilizers, and natural farming practices. The bio-agriculture market segment is expected to grow at an above-average rate through the forecast period.

Market Challenges

- Credit Access for Smallholder Farmers: Despite significant public sector banking coverage under priority sector lending mandates, access to affordable formal credit remains limited for a large proportion of small and marginal farmers, constraining investment in productivity-enhancing inputs and technologies.

- Supply Chain Fragmentation and Market Inefficiencies: Multiple intermediary layers between farm gate and end consumer and fragmented mandi regulation across states reduce price realization for farmers and create inefficiencies in commodity distribution.

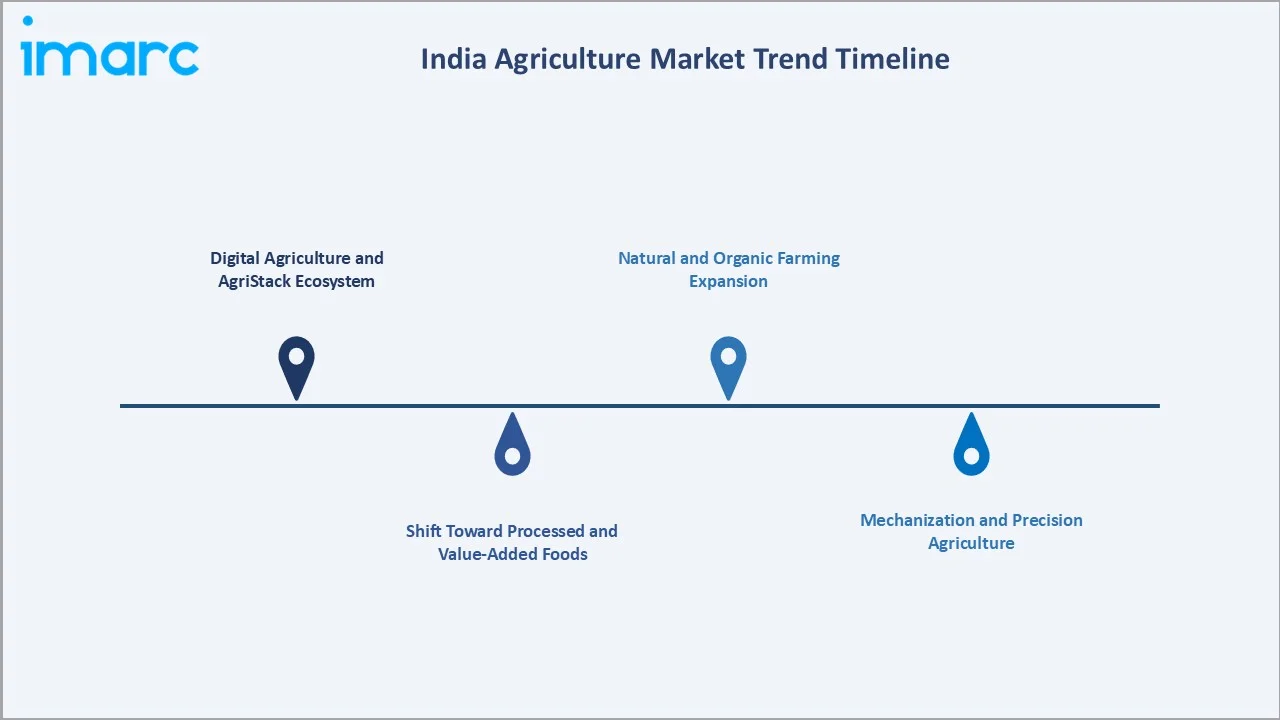

Emerging Market Trends

1. Digital Agriculture and AgriStack Ecosystem

The government's AgriStack initiative is creating a unified digital infrastructure comprising a farmer registry, geo-referenced plot registry, and crop sown registry, enabling precision targeting of subsidies, credit, insurance, and market information. This digital public infrastructure is expected to catalyze a new generation of AgriTech services, including AI-driven advisory, satellite-based crop monitoring, and e-commerce linkages for small and marginal farmers across India.

2. Shift Toward Processed and Value-Added Foods

Rising urban incomes, evolving food preferences, and expanding modern retail penetration are accelerating the shift from raw commodity sales to branded, packaged, and processed food products. This trend is encouraging greater investment in food processing facilities, cold chain infrastructure, and value-added agricultural supply chains, thereby enhancing farmer incomes and reducing post-harvest losses.

3. Natural and Organic Farming Expansion

Government policy is actively promoting zero-budget natural farming and organic certification, with India having one of the largest certified organic land areas globally. Consumer willingness to pay a premium for certified organic produce is creating new revenue streams for farmers and stimulating growth in bio-agriculture market inputs, including bio-fertilizers, biopesticides, and compost. As per IMARC Group, the India organic farming market size was valued at USD 6,133.68 Million in 2025.

4. Mechanization and Precision Agriculture

Farm mechanization levels in India remain well below global averages, presenting significant opportunity for the agriculture equipment subsector. Government subsidies on tractors, harvesters, and implements, combined with increasing availability of custom hiring centers and farmer producer organization-led machinery sharing models, are democratizing access to mechanized farming and supporting above-market growth in the agriculture equipment segment.

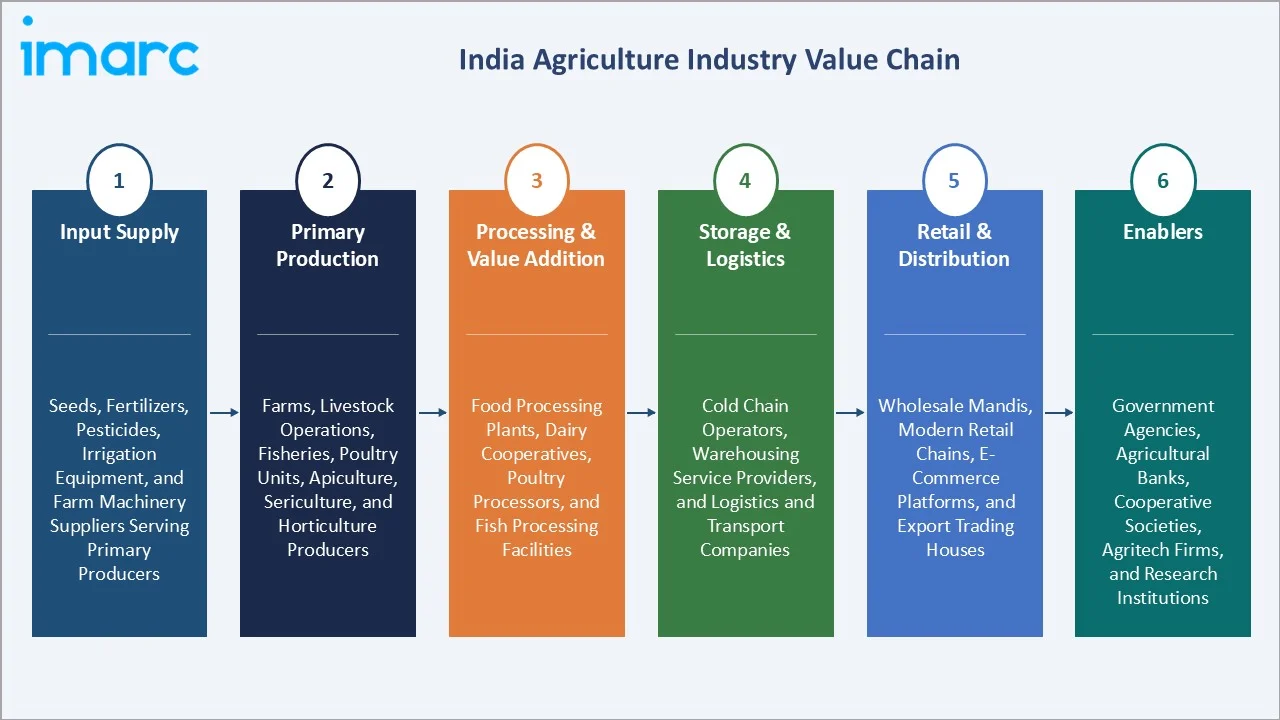

Industry Value Chain Analysis

The agriculture industry in India value chain spans six key stages from input supply through end market distribution. Food processing, cold chain and storage, and export trade capture the highest incremental value-add relative to primary production, reflecting the opportunity for farm-gate income improvement through integration with downstream processing and modern distribution networks.

|

Stage |

Key Players / Examples |

|

Input Supply |

Seeds, fertilizers, pesticides, irrigation equipment, and farm machinery suppliers serving primary producers |

|

Primary Production |

Farms, livestock operations, fisheries, poultry units, apiculture, sericulture, and horticulture producers |

|

Processing & Value Addition |

Food processing plants, dairy cooperatives, poultry processors, and fish processing facilities |

|

Storage & Logistics |

Cold chain operators, warehousing service providers, and logistics and transport companies |

|

Retail & Distribution |

Wholesale mandis, modern retail chains, e-commerce platforms, and export trading houses |

|

Enablers |

Government agencies, agricultural banks, cooperative societies, AgriTech firms, and research institutions |

Vertically integrated players, particularly those combining input supply, primary production, processing, and branded distribution, are positioned to capture the greatest value across the agriculture industry in India. Cooperative and farmer producer organization-led models at the farming level are progressively bridging the gap between smallholder production and organized downstream markets.

Technology Landscape in the Agriculture Industry in India

Precision Agriculture and Remote Sensing

Satellite imagery, drone-based crop monitoring, and IoT-enabled soil and weather sensors are enabling real-time crop health assessment, yield estimation, and precision input application across large farm operations in India. These technologies are reducing input costs, improving water use efficiency, and supporting data-driven farm management decisions.

AgriTech Platforms and Digital Market Linkages

Digital platforms are transforming market access for farmers, enabling direct price discovery, digital commodity trading, input procurement, and financial services through smartphone-based applications. Government-backed platforms and private AgriTech ventures are progressively displacing traditional mandi intermediaries in select commodity and regional markets.

Food Processing Technology and Cold Chain Innovation

Advanced food processing technologies including retort packaging, modified atmosphere packaging, and IQF technology are extending shelf life, improving food safety, and enabling export of high-value processed food products. Investments in automated cold chain infrastructure and blockchain-based traceability are reducing post-harvest losses and improving compliance with international food safety standards.

Market Segmentation Analysis

The report covers the following segment:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Subsectors |

Farming |

18.0% |

2025 |

By Subsectors

Farming leads at 18.0% in 2025, underpinned by extensive crop cultivation, government price support, and a large smallholder farmer base. The segment benefits from favorable agro-climatic conditions, expanding irrigation infrastructure, increasing mechanization, improved seed varieties, and sustained demand for food grains, fruits, vegetables, and commercial crops across domestic and export markets.

To access detailed market analysis, Request Sample

Food processing at 14.0% is expanding rapidly, supported by government investment in food processing infrastructure, rising organized retail penetration, and growing export demand for branded Indian food products.

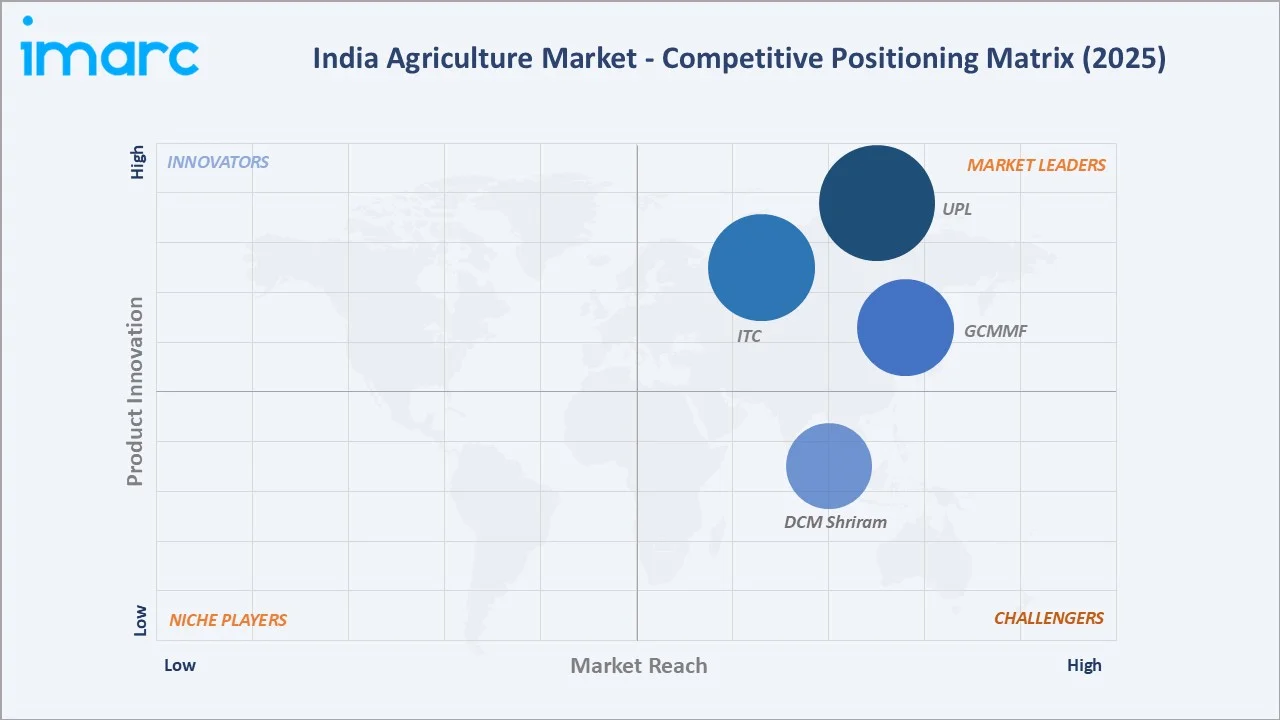

Competitive Landscape

The agriculture industry in India is highly diversified and fragmented at the primary production level, with organized competition concentrated in food processing, dairy, agri-inputs, equipment, and export trade segments. Brand strength, backward integration with farming operations, cold chain capabilities, and regulatory compliance form the key competitive moats for major participants.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

ITC |

Aashirvaad |

Leader |

Diversified agribusiness with integrated supply chain |

|

GCMMF |

Amul Dairy & Food Products |

Leader |

Cooperative-led dairy and food processing at national scale |

|

UPL |

Brucia, Centurion EZ, Saaf, Uthane M45 |

Leader |

Crop protection, seeds, and sustainable farming solutions |

|

DCM Shriram |

Shriram Farm Solutions |

Challenger |

Agri inputs, seeds, and Shriram Farm Solutions |

Key players include ITC, GCMMF, UPL, and DCM Shriram, among others.

Key Company Profiles

ITC

ITC is one of India's largest diversified conglomerates with a significant agribusiness presence spanning commodity procurement, value-added agri-products, and farmer empowerment across India. The company plays an important role in strengthening agricultural value chains by integrating sourcing, processing, storage, and export operations while promoting sustainable farming practices and rural development initiatives.

- Product Portfolio: Agri commodities, including wheat, rice, oilseeds, spices, coffee, and marine products sourced directly from farmers; value-added products across spices, frozen marine, and processed food categories.

- Recent Development: ITC's Agri Business Division was honored with multiple awards at the 4th Edition of the BW Businessworld Supply Chain Leadership Awards 2025, recognizing its benchmarks in supply chain excellence, innovation, and transformation.

- Strategic Focus: Scaling value-added agri-products portfolio across spices, coffee, and frozen marine segments; deepening farmer linkages through the e-Choupal network; and expanding organic and integrated crop management programs.

GCMMF

GCMMF is India's leading cooperative food products marketing organization, operating the Amul brand across dairy, food, and beverage categories. The federation represents a network of dairy cooperatives and serves as the apex body for milk procurement, processing, and nationwide distribution under the Amul brand, which is among India's most recognized consumer brands.

- Product Portfolio: Dairy products, including fresh milk, butter, cheese, ghee, ice cream, curd, paneer, dairy-based beverages, and value-added dairy products distributed across India and exported to several countries.

- Recent Development: The organization has continued to expand its product portfolio and distribution network, strengthening its presence across domestic and international dairy markets and growing its range of value-added dairy and food products.

- Strategic Focus: Expanding domestic and international distribution, growing value-added and premium dairy product categories, strengthening farmer cooperative procurement, and scaling Amul brand reach in urban and rural markets.

UPL

UPL is one of India's leading crop protection and agricultural inputs companies, operating across conventional agrochemicals, biological solutions, seeds, and digital agri-services. The company serves farmers, distributors, and agri-businesses across India and international markets with a broad portfolio of science-based crop management solutions.

- Product Portfolio: Crop protection products including herbicides, fungicides, insecticides, and bio-pesticides; seeds across field crops and vegetables; plant nutrition solutions; and digital agri-services for farmers, retailers, and input suppliers.

- Recent Development: The company has continued to expand its crop protection and seeds portfolio, scale its digital agri-services platform, and strengthen its presence across key agricultural input markets in India and internationally.

- Strategic Focus: Expanding digital agri-services platform, growing bio-solutions and sustainable crop protection portfolio, and scaling integrated crop management offerings across India and key international markets.

Market Concentration Analysis

The agriculture industry in India is highly fragmented at the primary production level, with several smallholder and marginal farm households participating in agricultural output. Organized market concentration is more pronounced in downstream segments, including food processing, dairy, agri-inputs, and cold chain logistics, where large national and multinational companies compete for leadership.

Barriers to scale in primary agriculture include fragmented landholdings, limited formal credit access, and price volatility. In contrast, barriers in food processing, seeds, and agri-inputs include brand equity, regulatory approvals, technology capabilities, and distribution network depth. These asymmetries favor well-capitalized companies with integrated supply chains and multi-segment presence.

Consolidation is gradually occurring in food processing, dairy, poultry, and agri-inputs through mergers, acquisitions, and farmer producer organization-mediated aggregation. Strategic partnerships between agribusiness companies, cooperative societies, and e-commerce platforms are further reshaping competitive dynamics across the agriculture industry in India.

Investment & Growth Opportunities

Fastest-Growing Segments

Bio-agriculture market is expected to grow at the highest rate through 2034, driven by consumer and regulatory preference for organic and chemical-free food production. Food processing and cold chains are the next-fastest growing segments, supported by organized retail growth, export potential, and government infrastructure investment.

Emerging Markets

Tier-2 and tier-3 cities, Northeastern India, and coastal aquaculture zones represent significant untapped market opportunity. Expanding cold chain connectivity to remote production centers, digital market access for smallholder farmers, and organized dairy and poultry sector growth in eastern and northeastern India are key emerging growth vectors.

Venture & Investment Trends

Private equity, venture capital, and strategic corporate investments are increasingly targeting AgriTech platforms, precision farming solutions, digital marketplaces, farm advisory services, and food processing infrastructure. At the same time, continued foreign and domestic investment in integrated supply chains, warehousing, logistics, and value-added agricultural processing is strengthening the sector's long-term growth outlook.

Future Market Outlook (2026-2034)

The agriculture industry in India is forecast to expand from INR 109.7 Trillion in 2025 to INR 252.0 Trillion by 2034 at a CAGR of 9.68%, adding approximately INR 142.3 Trillion in incremental annual market value over the forecast period.

Four structural forces will define the agriculture industry in India through 2034: continued government investment in farm income support and infrastructure; accelerating AgriTech and precision agriculture adoption; rapid growth in food processing, cold chain, and value-added dairy segments; and expanding international trade in high-value agricultural commodities.

By 2034, food processing, dairy, animal husbandry, and cold chains are expected to account for a significantly larger collective share of agriculture industry in India output, reflecting progressive value-chain integration and the premiumization of Indian agricultural production for both domestic and export markets.

Research Methodology

Primary Research

Primary research comprised structured interviews with agribusiness company executives, cooperative society leaders, food processing industry associations, AgriTech company founders, commodity traders, export house representatives, and government agricultural officials. These interactions validated market sizing assumptions, subsector growth trajectories, technology adoption rates, and competitive dynamics.

Secondary Research

Secondary sources included Ministry of Agriculture and Farmers' Welfare annual reports and policy documents, NABARD annual reports, APEDA export data, DPIIT FDI sector data, Food Safety and Standards Authority of India regulatory publications, and annual reports and investor presentations from listed agribusiness companies.

Forecasting Models

Market forecasts used a combination of top-down and bottom-up modeling approaches, incorporating subsector-specific demand drivers including population growth, per capita income trajectories, food consumption pattern shifts, export market trends, government spending on agriculture, and technology adoption diffusion curves.

Agriculture Industry in India Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Billion |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Subsectors Covered | Farming, Agriculture Equipment, Fertilizers, Pesticides, Warehousing, Cold Chains, Food Processing, Dairy Market, Floriculture, Apiculture, Sericulture, Seeds, Fisheries, Poultry, Animal Husbandry, Animal Feed, Bio-agriculture Market |

| Companies Covered | ITC, GCMMF, UPL, DCM Shriram, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Agriculture Industry in India Report

The agriculture industry in India was valued at INR 109.7 Trillion in 2025, driven by farming, food processing, dairy, animal husbandry, and allied sectors across the domestic agri-food ecosystem.

The market is projected to grow at a CAGR of 9.68% from 2026 to 2034, reaching INR 252.0 Trillion, supported by rising food demand, government investment, AgriTech adoption, and food processing expansion.

Farming leads at 18.0% share in 2025, fueled by extensive crop cultivation, strong domestic food demand, supportive government policies, expanding irrigation infrastructure, and the widespread adoption of improved farming practices across the country.

PM-KISAN and Pradhan Mantri Matsya Sampada Yojana are key flagship programs supporting farm income, insurance, processing infrastructure, and fisheries development.

Leading players include ITC, GCMMF, UPL, and DCM Shriram, among others.

Food processing at 14.0% share is the second-largest subsector, contributing significantly to value addition, employment, and agricultural export earnings. Organized food processing growth is expected to accelerate through the forecast period.

AgriTech platforms, precision farming tools, drone-based monitoring, and digital market linkages are improving productivity, reducing input waste, and enhancing price realization for farmers, driving long-term structural transformation of the sector.

Fragmented landholdings, monsoon dependency, post-harvest losses, limited rural credit access, and supply chain inefficiencies are the primary structural challenges constraining productivity and value realization across the sector.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)