Airfreight Forwarding Market Size, Share, Trends and Forecast by Type, Service Type, End Use Industry, and Region, 2026-2034

Global Airfreight Forwarding Market Size, Share, Trends & Forecast (2026-2034)

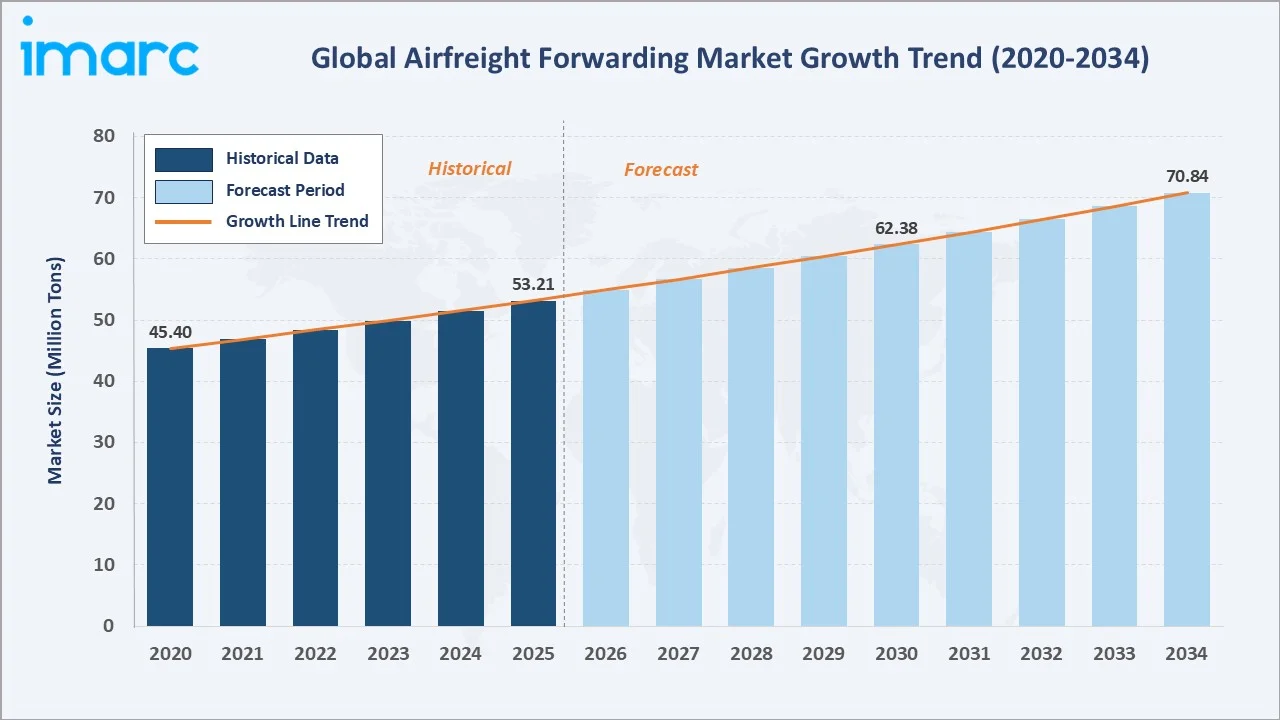

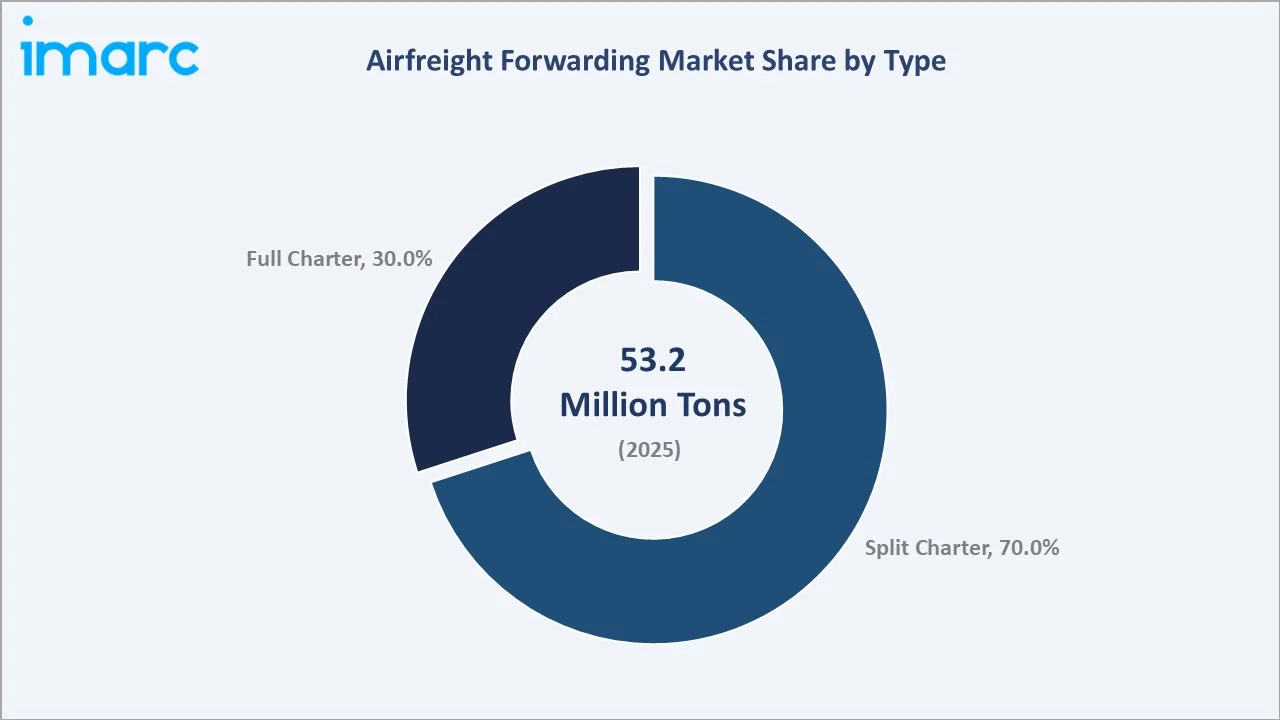

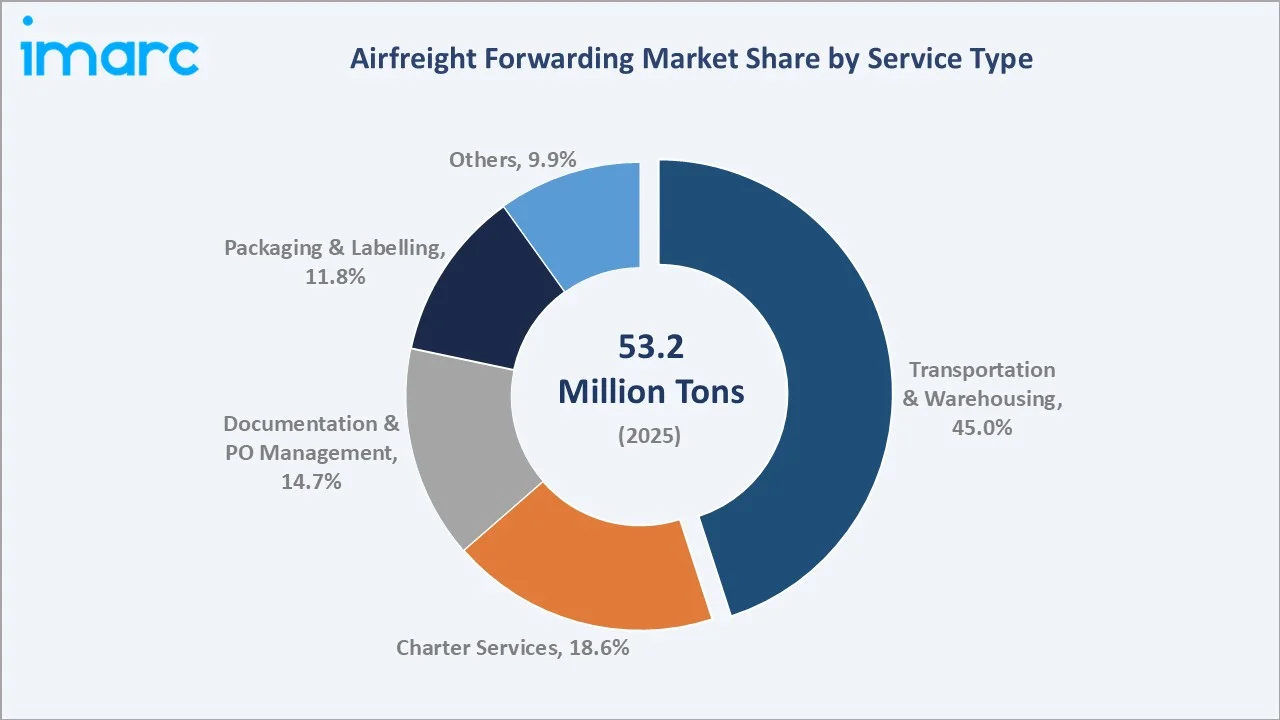

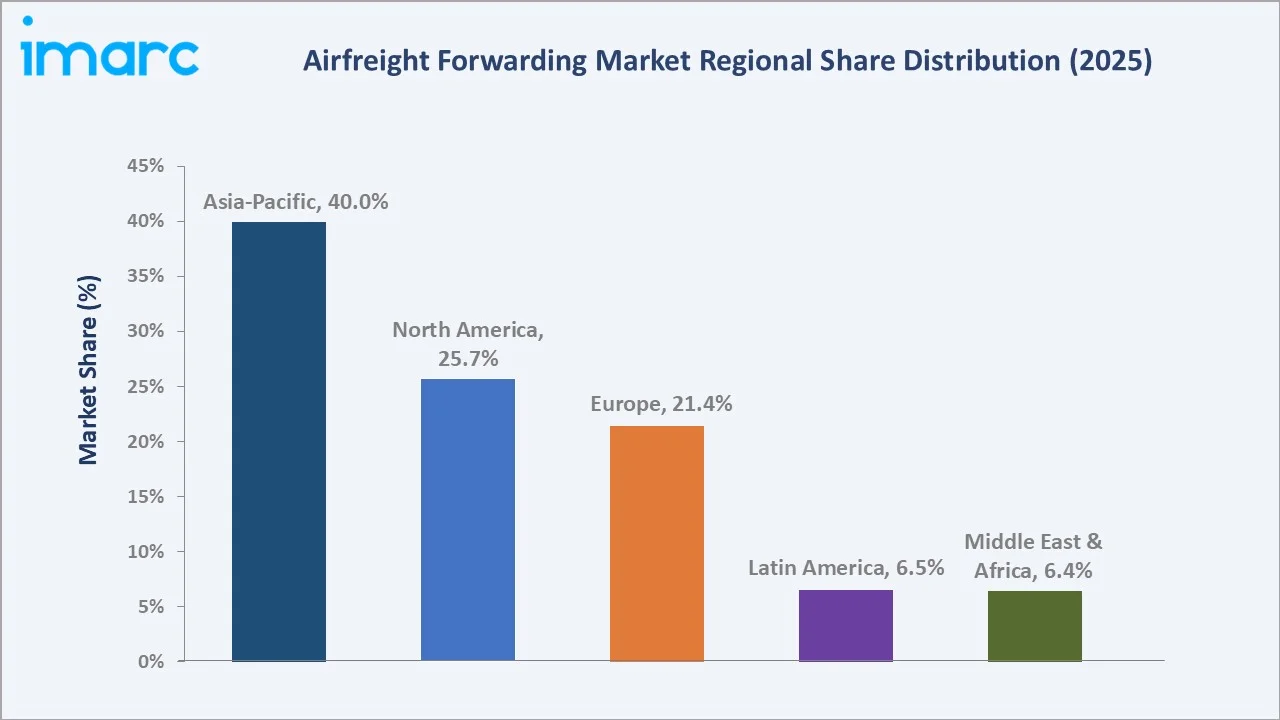

The global airfreight forwarding market size reached 53.21 Million Tons in 2025 and is projected to reach 70.84 Million Tons by 2034, exhibiting a CAGR of 3.23% during the forecast period 2026-2034. Rising e-commerce volumes, healthcare cold-chain expansion, global trade recovery, and rapid digitalization of air cargo operations are driving the airfreight forwarding market growth. Split Charter services lead with 70.0% share in 2025, while Transportation and Warehousing accounts for 45.0% of global service demand. Asia-Pacific dominates with 40.0% of global volume in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

53.21 Million Tons |

|

Forecast Market Size (2034) |

70.84 Million Tons |

|

CAGR (2026-2034) |

3.23% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (40.0% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~3.7%) |

|

Leading Type |

Split Charter (70.0%, 2025) |

|

Leading Service Type |

Transportation & Warehousing (45.0%, 2025) |

The global airfreight forwarding market growth trajectory from 2020 through 2034 contrasts historical expansion against a steady forecast curve powered by e-commerce volumes, healthcare logistics, and digital freight adoption across Asia-Pacific, North America, and Europe.

To get more information on this market, Request Sample

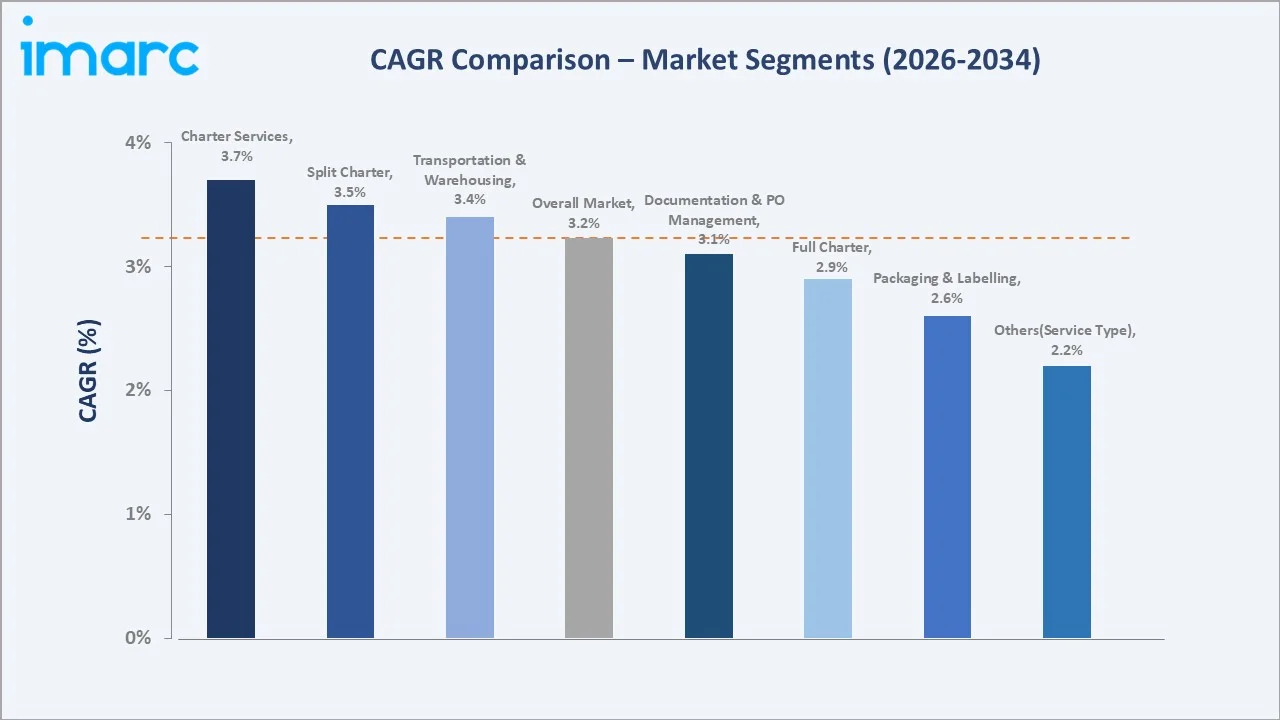

Segment-level CAGR comparisons highlight Charter Services and Split Charter as the fastest-growing sub-categories within the global airfreight forwarding market forecast through 2034, while traditional packaging and labelling services trail the market average.

Executive Summary

The global airfreight forwarding market is in a phase of steady recovery and structural modernization. Growth is anchored in e-commerce parcel acceleration, healthcare cold-chain demand, and digital transformation of air cargo operations. The market reached 53.21 Million Tons in 2025 and is forecast to expand to 70.84 Million Tons by 2034 at a CAGR of 3.23%.

By type, Split Charter services command 70.0% share in 2025, driven by consolidation economics and flexible capacity use. Full Charter holds 30.0%, powered by high-volume bulk contracts. On the service side, Transportation and Warehousing leads at 45.0%, while Charter Services at 18.6% is expanding on time-critical shipment demand.

Asia-Pacific leads global share at 40.0% in 2025, led by China's manufacturing exports and India's rising e-commerce outbound volumes. North America follows at 25.7%, Europe at 21.4%. The airfreight forwarding market outlook remains constructive as digitalization, sustainable aviation fuel rollout, and integrated logistics platforms reshape the competitive landscape.

Key Market Insights

|

Insight |

Data |

|

Largest Type |

Split Charter - 70.0% share (2025) |

|

Largest Service Type |

Transportation & Warehousing - 45.0% share (2025) |

|

Second Service Type |

Charter Services - 18.6% share (2025) |

|

Leading Region |

Asia-Pacific - 40.0% volume share (2025) |

|

Fastest Growing Region |

Asia-Pacific - ~3.7% CAGR (2026-2034) |

|

Top Companies |

Deutsche Post AG, Kuehne + Nagel, DSV, Expeditors International of Washington, Inc., CMA CGM, Nippon Express Holdings, UPS SCS Inc, Sinotrans Limited, Hellmann Worldwide Logistics SE & Co. KG. |

|

Market Opportunity |

E-commerce express air cargo and pharma cold chain |

Key Analytical Observations Supporting the Above Data:

- Split Charter's 70.0% dominance in 2025 reflects shipper preference for shared-capacity economics and the growing role of consolidators handling multi-customer loads across Asia-Pacific and Europe trade lanes.

- Transportation and Warehousing at 45.0% underscores the core operational services forwarders provide, covering integrated pick-up, airport handling, and delivery across major hubs such as Hong Kong, Shanghai, Frankfurt, and Memphis.

- Charter Services' 18.6% share is expanding on time-critical cargo demand from semiconductor, automotive parts, and pharmaceutical shippers. IATA data shows global air cargo volumes grew roughly 11% in 2024, supporting chartered capacity.

- Asia-Pacific's 40.0% global dominance is anchored by China's outbound exports, India's 10% e-commerce export growth in 2024, and the ASEAN manufacturing corridor serving North America and European retailers.

- E-commerce and cold chain demand together account for roughly 40% of new air cargo growth. Cross-border B2C parcel volumes crossed billions of shipments globally in 2024, lifting forwarder revenues across premium express lanes.

Global Airfreight Forwarding Market Overview

Airfreight forwarding is the specialized logistics service of arranging and managing cargo shipments by air on behalf of shippers. The industry covers a broad portfolio of services ranging from charter arrangement, space booking, and consolidation to warehousing, packaging, labelling, customs documentation, and last-mile delivery. Forwarders act as the key intermediary between shippers and airline carriers, supplying end-to-end visibility and compliance.

The market operates at the intersection of global trade flows, airline capacity cycles, and digital logistics platforms. Growth is supported by e-commerce outbound volumes, pharmaceutical cold-chain demand, and government-backed digital customs programs. Structurally, the industry is shifting toward integrated digital freight platforms, e-AWB adoption (over 80% globally in 2024), IoT-enabled shipment tracking, and sustainable aviation fuel procurement, which are redefining forwarder value propositions.

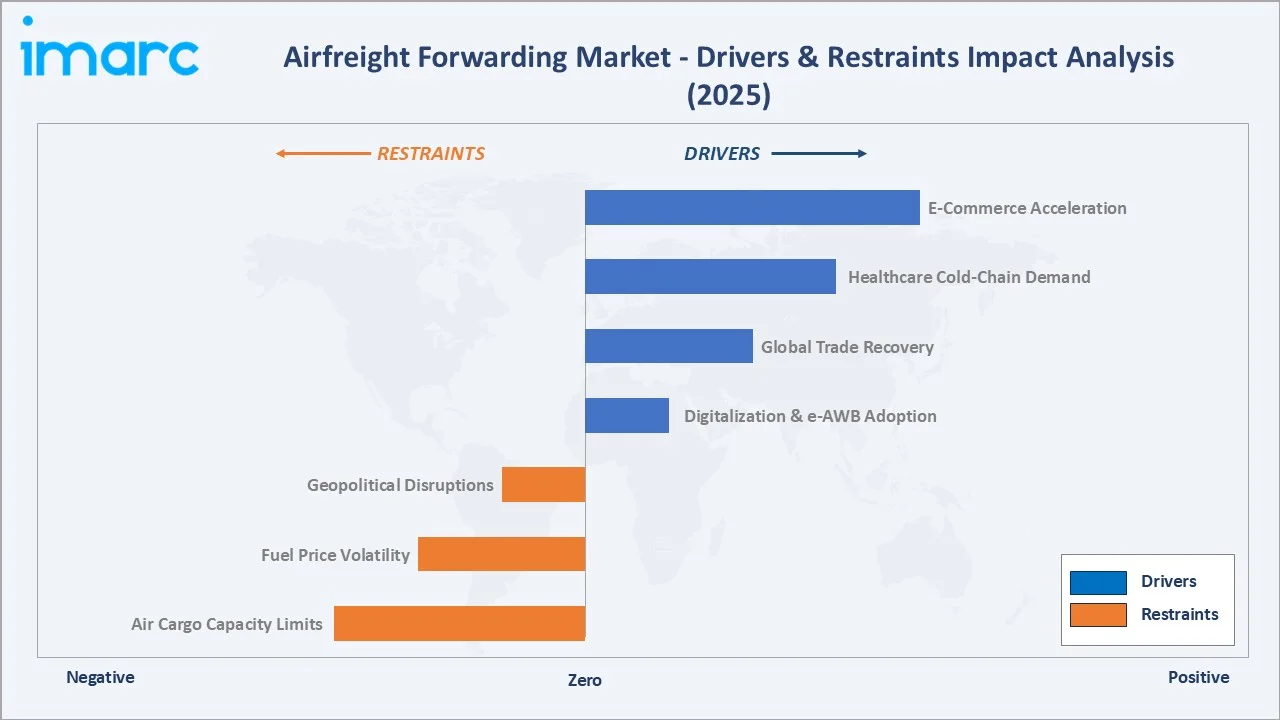

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

- E-commerce Acceleration: Global cross-border e-commerce parcel volumes crossed billions of shipments in 2024, driving strong demand for express air cargo. Retailers such as SHEIN, Temu, and Amazon source a growing share of outbound volumes via airfreight forwarders for delivery-time reliability in North American and European markets.

- Healthcare Cold-Chain Demand: The global pharma cold-chain logistics market surpassed USD 21 billion in 2024. Stringent temperature-controlled requirements for vaccines, biologics, and clinical trials are driving shippers toward certified forwarders with GDP-compliant handling capabilities.

- Global Trade Recovery: IATA reported that global air cargo traffic, measured in cargo tonne-kilometres, grew 11.3% year-on-year in 2024, returning above pre-pandemic levels. Manufacturing rebound in Asia-Pacific and consumer goods demand in North America are lifting outbound forwarder volumes across major trade lanes.

- Digitalization and e-AWB Adoption: The industry-wide electronic air waybill (e-AWB) penetration crossed 80% in 2024. Digital freight platforms, API-based quote-to-book tools, and blockchain-enabled documentation are cutting transit times and compliance costs, creating a structural tailwind for technology-led forwarders.

Market Restraints

- Air Cargo Capacity Limits: Belly-hold capacity on passenger aircraft and dedicated freighter fleets remain tight on key Asia-Europe and trans-Pacific lanes, driving freight rate volatility.

- Fuel Price Volatility: Jet fuel prices swung more than 25% in 2024, directly impacting forwarder margins as shippers resist surcharge pass-through in competitive tenders across mature markets.

- Geopolitical Disruptions: Red Sea routing disruptions, Russia-Ukraine airspace closures, and US-China trade tensions are rerouting cargo flows, adding transit time and cost complexity for forwarders managing East-West lanes.

Market Opportunities

- Pharma and Biologics Cold Chain: IATA's Center of Excellence for Independent Validators (CEIV Pharma) certification is now held by over 450 airports, airlines, and forwarders globally. Certified forwarders command premiums prices on temperature-sensitive shipments, creating strong margin opportunities.

- E-commerce Express Lanes: Cross-border B2C express air volumes are projected to grow exponentially annually by 2030. Forwarders that integrate with e-commerce platforms via API-based booking and last-mile delivery partners are capturing outsized volume growth in Asia-Pacific and Europe.

- Digital Freight Platforms: Venture-backed digital forwarders (Flexport, Forto, Beacon) raised over USD 1.5 billion collectively during 2023-2024. Their platform approach is reshaping customer expectations for instant quoting, real-time tracking, and transparent pricing across the traditional forwarder base.

Market Challenges

- Sustainability Pressure: Corporate shippers are mandating Scope 3 emissions reporting. Sustainable aviation fuel (SAF) currently costs 2-5x conventional jet fuel, squeezing forwarder margins as environmental compliance commitments rise across EU, UK, and US jurisdictions.

- Talent and Automation Gap: Legacy forwarders face a widening gap between customer expectation for digital service and internal IT maturity. Operational skill shortages in customs brokerage and cargo handling are driving wage inflation across US and European hubs.

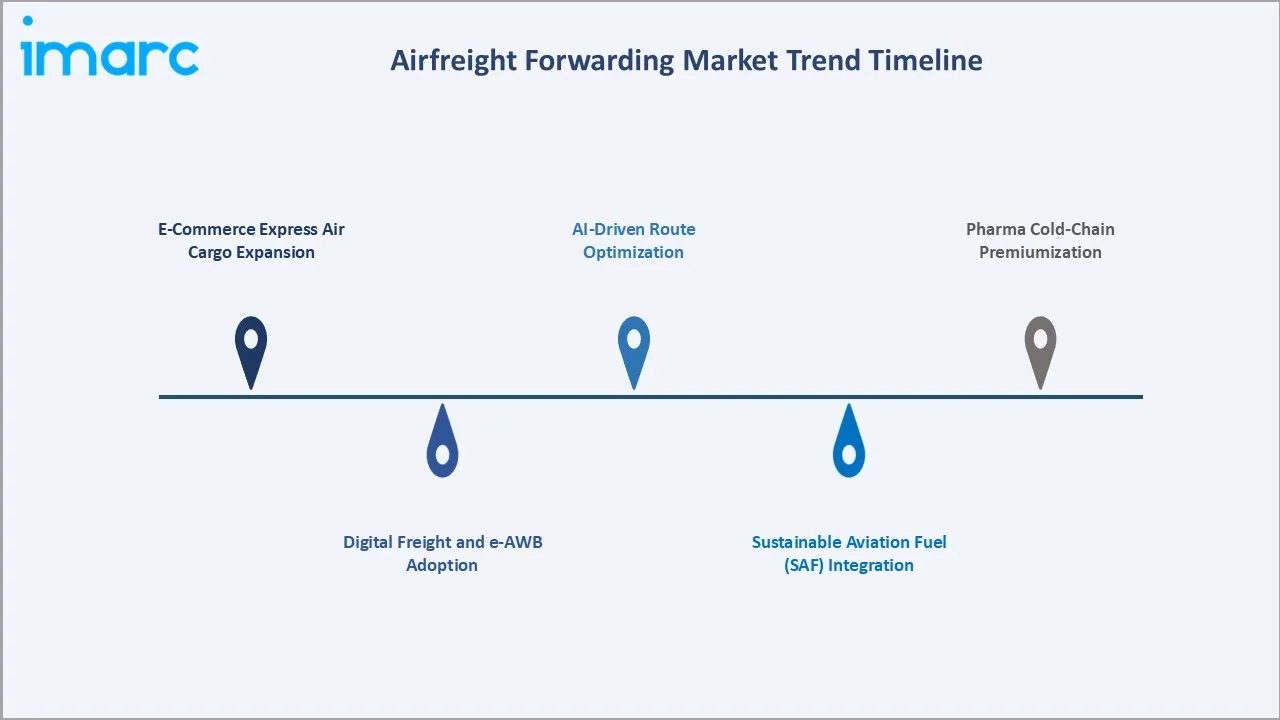

Emerging Market Trends

1. E-Commerce Express Air Cargo Expansion

Cross-border B2C e-commerce is the single largest growth engine for air cargo forwarding through 2030. Platforms such as SHEIN, Temu, and Alibaba are moving substantial outbound volumes via dedicated forwarder contracts. Dedicated freighter capacity on China–North America and China–Europe lanes expanded significantly in 2024, with freighters accounting for 77% of Trans-Pacific and 58% of Europe–Asia air cargo volumes

2. Digital Freight and e-AWB Adoption

Electronic air waybill penetration increased globally in 2024. API-based booking, blockchain documentation, and AI-driven rate optimization are reshaping forwarder-shipper interactions. Companies such as DHL and Kuehne+Nagel have invested heavily in proprietary digital platforms to protect margins and speed up transaction cycles.

3. Sustainable Aviation Fuel (SAF) Integration

Under the EU’s ReFuelEU Aviation framework, sustainable aviation fuel (SAF) supply is mandated to begin at 2% from 2025, with progressively increasing blending requirements over time, reaching substantially higher levels by 2050. Shippers such as Unilever, Maersk, and Nestle are co-investing with forwarders in book-and-claim SAF programs, creating a new premium service tier for carbon-conscious shippers across North American and European trade lanes.

4. AI-Driven Route Optimization

Forwarders are deploying machine learning for dynamic routing, capacity forecasting, and predictive ETA calculation. AI adoption is expected to reduce transit variability and improve ETA accuracy on major trade lanes through 2030, driven by real-time data integration and predictive optimization, delivering measurable service differentiation and customer retention benefits for early adopters.

5. Pharma Cold-Chain Premiumization

CEIV Pharma certified forwarders are securing long-term contracts with global pharma majors such as Pfizer, Novartis, and Sanofi. Temperature-controlled air cargo volumes are growing faster than the overall market, supported by strong demand from pharmaceuticals and biologics, with growth typically in the mid- to high-single digits, supported by biologics and cell-and-gene therapy logistics demand.

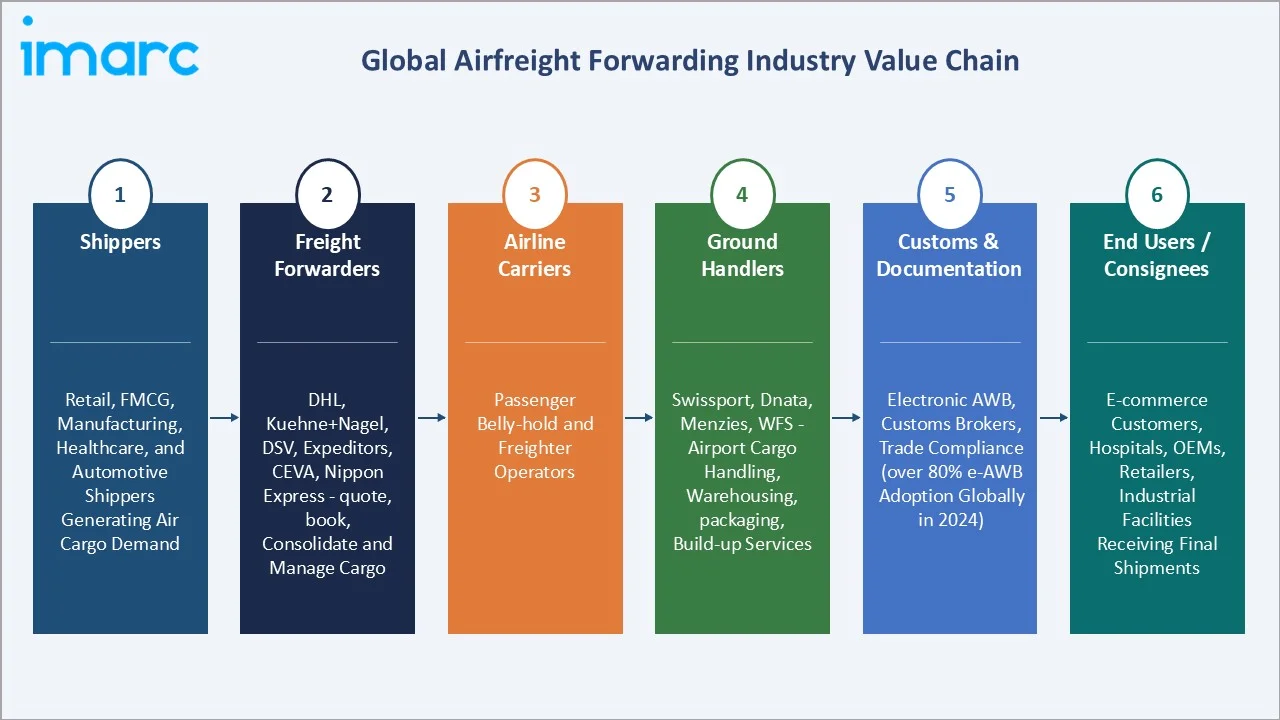

Industry Value Chain Analysis

The global airfreight forwarding value chain spans six integrated stages, from shipper origination through final delivery. Each stage has distinct competitive dynamics, margin profiles, and technology investment profiles relevant to the overall airfreight forwarding market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Shippers |

Retail, FMCG, manufacturing, consumer appliances, healthcare, and automotive shippers generating cargo demand |

|

Freight Forwarders |

DHL, Kuehne+Nagel, DSV, Expeditors, CEVA, Bolloré, Nippon Express, UPS SCS, Hellmann, Sinotrans - quote, book, consolidate, and manage cargo |

|

Airline Carriers |

Passenger belly-hold (British Airways, Lufthansa, Singapore Airlines) and dedicated freighter (FedEx, UPS, Cargolux, Qatar Airways Cargo) operators |

|

Ground Handlers |

Swissport, dnata, Menzies, WFS - airport cargo handling, warehousing, packaging, labelling, and build-up services |

|

Customs & Documentation |

Electronic AWB, customs brokers, trade compliance (over 80% e-AWB adoption globally in 2024) |

|

End Users / Consignees |

E-commerce customers, hospitals, OEMs, retailers, and industrial facilities receiving final shipments |

Freight forwarders capture the highest strategic value by integrating shipper demand, airline capacity, ground handling, and customs into turnkey logistics solutions. Digital-first forwarders and integrated logistics platforms are reshaping the traditional intermediary role, capturing margin through data-driven automation and consolidated purchasing power with airline carriers.

Technology Landscape in the Airfreight Forwarding Industry

Digital Freight Platforms and e-AWB

Electronic air waybill adoption crossed 80% globally in 2024, per IATA. Digital freight platforms from DHL, Kuehne+Nagel, and DSV integrate quote, booking, tracking, and invoicing into unified customer portals. API-based connectivity with shipper ERP systems is becoming standard practice across large enterprise accounts.

IoT and Real-Time Shipment Tracking

IoT-enabled cargo tracking devices measuring temperature, humidity, shock, and location are now standard for pharma and high-value shipments. The global installed base of IoT-enabled tracking devices across cargo units—including air freight ULDs, containers, and pallets—reached approximately 13.8 million active devices in 2024, reflecting rapid adoption of real-time visibility solutions across logistics networks.

AI and Predictive Analytics

Machine learning is being used for dynamic pricing, capacity forecasting, and predictive ETA calculation. Generative AI tools are also being piloted for customs document automation and customer query handling across core operations.

Sustainable Aviation Fuel and Automation

SAF procurement programs, warehouse robotics, and autonomous cargo handling equipment are being deployed at major hubs including Frankfurt, Hong Kong, and Memphis. Forwarders are integrating SAF book-and-claim certificates into customer reporting to support Scope 3 emissions disclosure for enterprise shippers.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Split Charter |

70% |

2025 |

|

Service Type |

Transportation and Warehousing |

45% |

2025 |

| End Use Industry | Retail and FMCG |

30% |

2025 |

|

Region |

Asia Pacific |

40% |

2025 |

IMARC Group provides an analysis of the key trends in each segment of the global airfreight forwarding market, along with forecasts at the global, regional, and country levels from 2026 to 2034. The market has been categorized based on type and service type.

By Type

Split Charter leads the global airfreight forwarding market type segment with a 70.0% share in 2025. Demand is driven by shipper preference for shared-capacity economics and consolidator-led multi-customer loads across major trade lanes. Split Charter typically delivers cost savings of 20-30% versus Full Charter for shipments below 50 tons, making it the default option for mid-sized e-commerce, FMCG, and electronics cargo flows across Asia-Pacific, Europe, and North America.

To access detailed market analysis, Request Sample

Full Charter accounts for 30.0% of global type demand. It is favored for oversized, urgent, or mission-critical shipments such as automotive parts for production-stoppage recovery, defense logistics, humanitarian relief cargo, and project logistics for energy and mining. Full Charter volumes surged during the 2020-2022 pandemic period as passenger belly-hold capacity collapsed, and retention is now stabilizing around long-term contract shipper relationships.

By Service Type

Transportation and Warehousing is the dominant service-type segment at 45.0% of global demand in 2025. This covers integrated pick-up, airport handling, storage, and delivery - the core operational workflow for every forwarder engagement. Major global hubs such as Hong Kong (HKG), Shanghai (PVG), Frankfurt (FRA), and Memphis (MEM) anchor this segment. Leading forwarders are investing heavily in automated warehouses and cross-dock facilities to capture margin and improve shipment throughput.

Charter Services represent 18.6% of service-type demand and are expanding fastest at an estimated 3.7% CAGR through 2034. Time-critical shipment demand from semiconductor, automotive parts, and pharmaceutical shippers drives charter bookings. Documentation and PO Management holds 14.7% share, underpinned by customs compliance and e-AWB services. Packaging and Labelling at 11.8% covers value-added hub services including cold-chain packaging and export compliance labelling. The Others segment (9.9%) covers insurance, track-and-trace, and specialized value-added services.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

40.0% |

China manufacturing exports, India e-commerce outbound, ASEAN electronics hub, Japan pharma cold chain |

|

North America |

25.7% |

U.S. e-commerce imports, Mexico nearshoring, healthcare and semiconductor cargo, Memphis and Louisville hubs |

|

Europe |

21.4% |

Germany-UK intra-regional trade, SAF mandates, Frankfurt and Amsterdam hubs, pharma cold chain |

|

Latin America |

6.5% |

Brazil and Mexico outbound, perishables to North America, automotive parts imports |

|

Middle East & Africa |

6.4% |

Dubai and Doha transhipment hubs, GCC pharma imports, African outbound perishables and minerals |

Asia-Pacific commands 40.0% of global volume share in 2025. China is the single most important national market, anchored by manufacturing exports across electronics, apparel, and consumer goods. India's Foreign Trade Policy 2023 targets USD 2 trillion in exports by 2030, lifting outbound air cargo flows. The ASEAN manufacturing corridor (Vietnam, Thailand, Malaysia) is absorbing China-plus-one sourcing shifts, while Japan and South Korea anchor pharma and semiconductor lane demand. Asia-Pacific is also forecast to be the fastest-growing region, advancing at approximately 3.7% CAGR through 2034.

North America holds 25.7% of global volume. U.S. e-commerce import demand, semiconductor cargo, and healthcare cold-chain shipments underpin growth. Memphis (MEM) and Louisville (SDF) remain the world's top cargo hubs, anchored by FedEx and UPS integrator operations. USMCA-enabled Mexico nearshoring is lifting southbound air cargo flows across automotive, electronics, and medical device categories.

Europe holds 21.4%, characterized by Germany-UK intra-regional flows, SAF mandate compliance, and luxury goods exports. The EU's ReFuelEU Aviation regulation mandates 2% SAF blending from 2025, driving forwarders to invest in book-and-claim programs. Frankfurt (FRA), Amsterdam (AMS), and Liège (LGG) are key hubs, while Lufthansa Cargo and Air France-KLM Cargo anchor lane capacity for the major forwarders.

Latin America accounts for 6.5%, led by Brazil, Mexico, and Colombia. Perishables exports such as salmon, berries, and flowers to North America anchor regional volumes. The Middle East & Africa represents 6.4%, driven by Dubai (DXB) and Doha (DOH) as global transhipment hubs, plus GCC pharma imports and African outbound minerals and perishables.

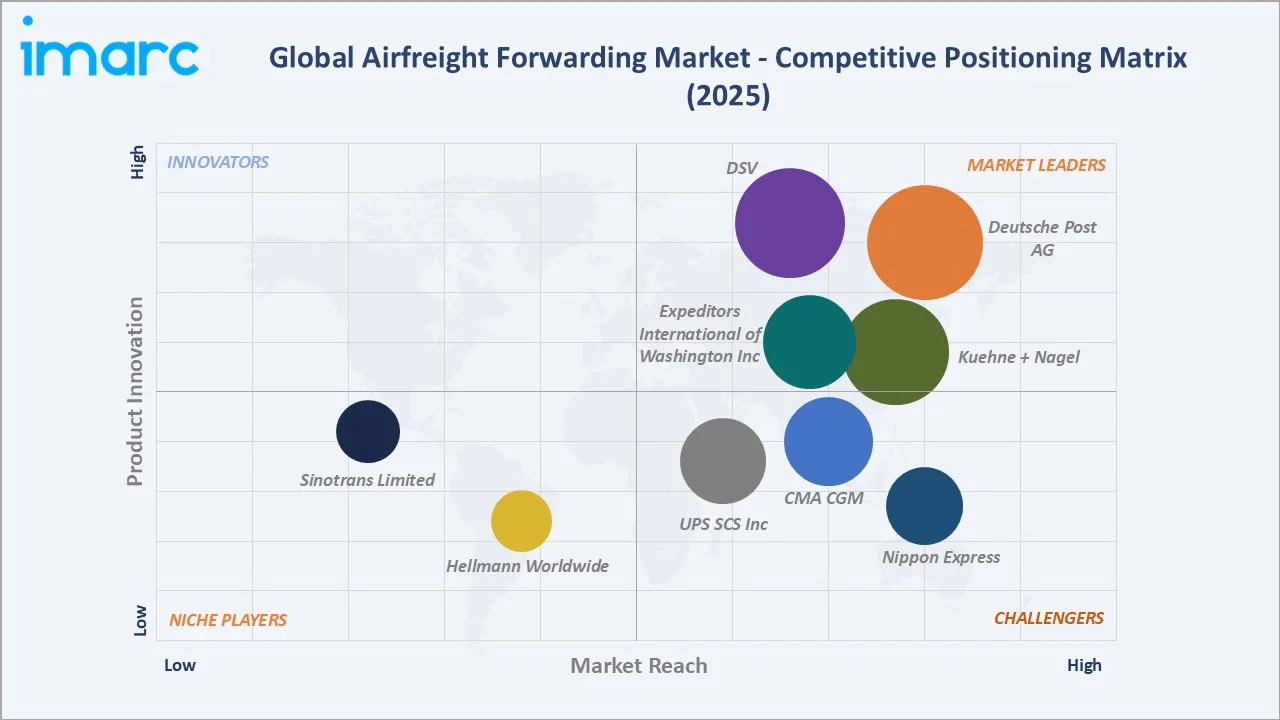

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Deutsche Post AG |

DHL Global Forwarding |

Leader |

Global network scale, digital platform, pharma cold chain |

|

Kuehne + Nagel |

Kuehne+Nagel |

Leader |

Global lane coverage, seafreight-airfreight integration |

|

DSV |

DSV |

Leader |

Europe hub density, Agility acquisition integration |

|

Expeditors International of Washington, Inc. |

Expeditors |

Leader |

Technology-led service, non-asset-based model |

|

CMA CGM |

CEVA Logistics, Bollore Logistics |

Challenger |

Contract logistics depth, CMA CGM synergy |

|

Nippon Express Holdings |

Nippon Express |

Challenger |

Japan and Asia-Pacific network, pharma focus |

|

UPS SCS Inc |

UPS Supply Chain Solutions |

Challenger |

Integrator model, Worldport Louisville hub |

|

Sinotrans Limited |

Sinotrans Limited |

Emerging |

China domestic leader, belt-and-road lane access |

|

Hellmann Worldwide Logistics SE & Co. KG |

Hellmann Worldwide Logistics |

Emerging |

Mid-market shipper focus, Europe and Asia balance |

The global airfreight forwarding market's competitive landscape is moderately concentrated, with the top five players accounting for a large share of global forwarded air cargo tonnage. Leading players compete on global network coverage, digital freight platforms, pharma cold-chain certifications, and lane-specific capacity partnerships with airline carriers. Strategic M&A remains a key tool - DSV acquired Panalpina (2019), while CMA CGM acquired both CEVA Logistics and Bolloré Logistics to build a multi-modal logistics platform.

Key Company Profiles

Deutsche Post AG

Deutsche Post AG, operating through its DHL Global Forwarding, is the largest airfreight forwarder globally by tonnage. Headquartered in Bonn, Germany, DHL serves shippers across more than 220 countries with an integrated network of airfreight, ocean freight, contract logistics, and parcel services.

- Product & Platform Portfolio: DHL's airfreight portfolio covers DHL Air Connect time-definite services, DHL Thermonet for temperature-controlled pharma, DHL Lifeconex for clinical trials, and the myDHLi digital platform for quote-booking-tracking. Additional services include charter brokerage, customs brokerage, and cargo insurance.

- Recent Developments: In 2024, DHL continued to enhance its digital logistics capabilities through platforms such as myDHLi, while expanding automation and AI-driven solutions. The company also scaled its sustainability efforts through significant sustainable aviation fuel (SAF) partnerships and targets of over 30% SAF blending by 2030, alongside ongoing expansion of CEIV Pharma-certified operations across its global network

- Strategic Focus: DHL's strategy centers on digital platform leadership, pharma cold-chain expansion, and sustainable aviation fuel procurement. It is investing heavily in Asia-Pacific hub capacity including the Hong Kong Central Asia Hub to capture China e-commerce and Southeast Asia manufacturing outbound flows.

Kuehne + Nagel

Kuehne + Nagel is a Swiss-headquartered global logistics provider and one of the top three airfreight forwarders worldwide. Based in Schindellegi, Switzerland, the company operates across 100+ countries with a strong position in seafreight, airfreight, contract logistics, and integrated logistics.

- Product & Platform Portfolio: Kuehne+Nagel's airfreight portfolio includes KN Login digital platform, KN PharmaChain for cold-chain pharma, KN SecureChain for high-value cargo, and KN ExpertChain for aerospace and perishables. The company also operates dedicated charter brokerage, customs, and insurance services.

- Recent Developments: In 2024, Kuehne+Nagel launched its Book & Claim Sustainable Aviation Fuel program, allowing shippers to offset air cargo emissions. The company also expanded KN PharmaChain certification coverage and invested in AI-driven capacity forecasting tools across its global operations.

- Strategic Focus: Kuehne+Nagel's strategy emphasizes vertical specialization in pharma, aerospace, perishables, and high-tech categories. Continued investment in KN Login digital capability and SAF programs position the company to capture premium contract logistics revenue with enterprise shippers.

DSV

DSV, headquartered in Hedehusene, Denmark, is a global logistics leader with a strong presence across airfreight, seafreight, road, and contract logistics. Following the 2019 Panalpina acquisition and the announced 2024 acquisition of DB Schenker, DSV is positioned to become one of the largest logistics providers globally by revenue.

- Product & Platform Portfolio: DSV Air & Sea offers airfreight express, standard, and economy services, plus specialized solutions for automotive, healthcare, technology, and industrial verticals. Digital tools include myDSV online booking, real-time tracking, and customs brokerage integration across major global lanes.

- Recent Developments: In September 2024, DSV announced the acquisition of DB Schenker from Deutsche Bahn for approximately EUR 14.3 billion, pending regulatory approval. Completion is expected in 2025, positioning the combined entity as the world's largest logistics company by airfreight tonnage and overall revenue.

- Strategic Focus: DSV's strategy centers on scale-led integration, operational efficiency, and margin expansion through the Schenker merger. The company is prioritizing European hub density, Asia-Pacific lane investment, and digital customer interface upgrades to retain enterprise shipper accounts.

Market Concentration Analysis

The global airfreight forwarding market is moderately concentrated. The top five players - DHL Global Forwarding, Kuehne+Nagel, DSV (pro-forma post-Schenker), Expeditors, and CEVA Logistics - together account for approximately 35-42% of global air cargo forwarded tonnage in 2025. The remaining market share is distributed across mid-sized global players such as UPS SCS, Nippon Express, Hellmann, and Sinotrans, plus a large number of regional and national forwarders.

The industry is in an active consolidation phase. DSV's announced acquisition of DB Schenker in 2024, CMA CGM's integration of CEVA and Bolloré, and continued M&A among mid-market players are reshaping the competitive landscape. Scale, digital platform capability, pharma certification coverage, and lane-specific airline partnerships are the primary drivers of consolidation through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Charter Services is the highest-growth service sub-segment at approximately 3.7% CAGR through 2034, driven by time-critical semiconductor, automotive parts, and pharma cargo. Split Charter continues to lead volume at 70.0% type share as e-commerce consolidation expands. Pharma cold-chain shipments represent the highest-margin opportunity, with certified forwarders commanding 15-25% price premiums over standard airfreight.

Emerging Market Expansion

India represents the highest-potential emerging market, driven by Foreign Trade Policy 2023 export targets and rapid e-commerce outbound volume growth of 15% annually. Southeast Asia (Vietnam, Indonesia, Thailand) is absorbing China-plus-one manufacturing shifts. Africa and Latin America perishables and minerals exports offer under-penetrated opportunities for forwarders with localized network investment through 2034.

Venture and Strategic Investment Trends

Digital forwarders (Flexport, Forto, Beacon) raised more than USD 1.5 billion collectively during 2023-2024. Strategic M&A is reshaping the landscape - DSV's 2024 acquisition of DB Schenker for EUR 14.3 billion is the largest logistics deal in recent history. Investment priorities include AI-driven route optimization, IoT tracking, SAF procurement platforms, and pharma cold-chain capacity expansion for global shipper accounts.

Future Market Outlook (2026-2034)

The global airfreight forwarding market forecast projects steady volume expansion from 53.21 Million Tons in 2025 to 70.84 Million Tons by 2034 at a CAGR of 3.23%. Asia-Pacific will retain regional leadership and accelerate structurally, while North America and Europe sustain premium volume growth through e-commerce imports and pharma cold-chain demand.

Three structural shifts will reshape the airfreight forwarding market through 2034. First, digital freight platforms will become the default shipper interface, with e-AWB reaching near-universal adoption by 2028 and AI-driven route optimization becoming a competitive differentiator. Second, sustainable aviation fuel adoption will climb under EU and US regulatory mandates, restructuring forwarder cost and pricing dynamics. Third, industry consolidation will accelerate, with the top five players expected to reach 50%+ global share by 2030 through M&A and organic scale expansion.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with air cargo industry stakeholders, including sales and product directors at global forwarders, procurement managers at enterprise shippers across pharma, retail, and technology categories, airline cargo sales representatives, and airport cargo handling operators. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include IATA World Air Transport Statistics, ICAO air cargo volume data, WTO global trade reports, WCO customs statistics, company annual reports, SEC and stock-exchange filings from DHL, DSV, Kuehne+Nagel, Expeditors, and UPS, and trade publications including Air Cargo News, Journal of Commerce, and Lloyds Loading List.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating global GDP growth rates, air cargo tonne-kilometre trends, e-commerce parcel volume projections, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic and geopolitical uncertainty.

Airfreight Forwarding Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scpoe of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Full Charter, Split Charter |

| Service Types Covered | Packaging and Labelling, Documentation and PO Management, Charter Services, Transportation and Warehousing, Others |

| End Use IndustrIes Covered | Retail and FMCG, Manufacturing, Consumer Appliances, Healthcare, Others |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Deutsche Post AG, Kuehne + Nagel, DSV, Expeditors International of Washington, Inc., CMA CGM, Nippon Express Holdings, UPS SCS Inc, Sinotrans Limited, Hellmann Worldwide Logistics SE & Co. KG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Airfreight Forwarding Market Report

The global airfreight forwarding market reached 53.21 Million Tons in 2025, driven by e-commerce volumes, healthcare cold-chain expansion, and global trade recovery across Asia-Pacific, North America, and Europe.

The market is projected to reach 70.84 Million Tons by 2034, growing at a CAGR of 3.23% during 2026-2034, supported by digital freight platforms, e-commerce expansion, and pharma cold-chain demand.

Split Charter leads with a 70.0% share in 2025, driven by shared-capacity economics and consolidator-led multi-customer loads across major Asia-Europe and trans-Pacific trade lanes.

Transportation and Warehousing is the largest service segment at 45.0% share in 2025, covering integrated pick-up, airport handling, warehousing, and delivery operations across global forwarder networks.

Asia-Pacific dominates with a 40.0% share in 2025, anchored by China's manufacturing exports, India's e-commerce outbound volumes, and the ASEAN electronics and apparel manufacturing corridor.

Key drivers include e-commerce acceleration, healthcare cold-chain demand, global trade recovery, e-AWB adoption above 80%, IoT-enabled shipment tracking, and digital freight platform expansion globally.

Major players include Deutsche Post AG, Kuehne + Nagel, DSV, Expeditors International of Washington, Inc., CMA CGM, Nippon Express Holdings, UPS SCS Inc, Sinotrans Limited, Hellmann Worldwide Logistics SE & Co. KG.

Charter Services is the fastest-growing service segment, advancing at approximately 3.7% CAGR through 2034, driven by time-critical semiconductor, automotive parts, and pharmaceutical cargo demand.

Opportunities include pharma cold-chain platforms, e-commerce express lanes, AI-driven route optimization, SAF procurement programs, and India and Southeast Asia emerging market network expansion through 2034.

Sustainable aviation fuel mandates such as EU ReFuelEU Aviation (2% SAF by 2025) and shipper Scope 3 reporting are driving forwarders to launch SAF book-and-claim programs and carbon reporting tools.

E-commerce is the single largest growth engine, with cross-border B2C parcel volumes crossing 5 billion shipments globally in 2024 and driving premium express air cargo demand across major trade lanes.

The market is moderately concentrated - the top five players (DHL, Kuehne+Nagel, DSV, Expeditors, CEVA) hold about 35-42% of global forwarded air cargo tonnage in 2025, with ongoing M&A consolidation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)