Alternative Data Market Size, Share, Trends and Forecast by Data Type, End Use Industry, and Region, 2026-2034

Global Alternative Data Market Size, Share, Trends & Forecast 2026-2034

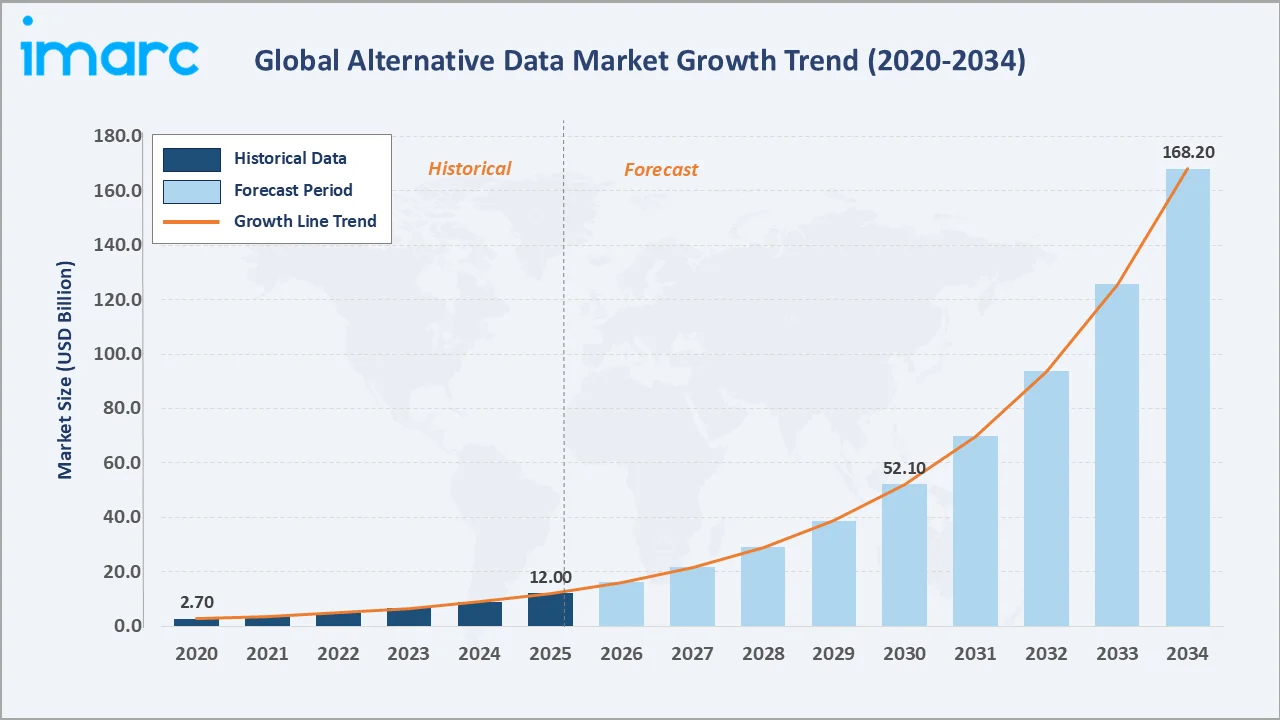

The global alternative data market size reached USD 12 Billion in 2025 and is projected to reach USD 168.2 Billion by 2034, at a CAGR of 34.0% during 2026-2034. Explosive growth in AI/ML adoption, the 78% penetration of alternative data among hedge funds, and digital data proliferation from IoT and mobile platforms are the primary growth engines. Credit and debit card transactions lead data type at 17.9%, while BFSI dominates end-use at 17.5%. North America holds an overwhelming 68.9% regional share in 2025, anchored by Wall Street's data-driven investment culture and a dense technology ecosystem.

Market Snapshot

|

Metric |

Value |

|

Market Size 2025 |

USD 12 Billion |

|

Forecast Market Size 2034 |

USD 168.2 Billion |

|

CAGR (2026-2034) |

34.0% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (68.9%, 2025) |

|

Fastest-Growing Region |

Asia-Pacific (~38.2% CAGR, 2026-2034) |

|

Leading Data Type |

Credit & Debit Card Transactions (17.9%, 2025) |

|

Leading End-Use |

BFSI (17.5%, 2025) |

The alternative data market growth trajectory from 2020 through 2034. The market surged to USD 12 Billion in 2025 and the forecast to USD 168.2 Billion, driven by AI-augmented data analytics and enterprise-wide adoption.

To get more information on this market, Request Sample

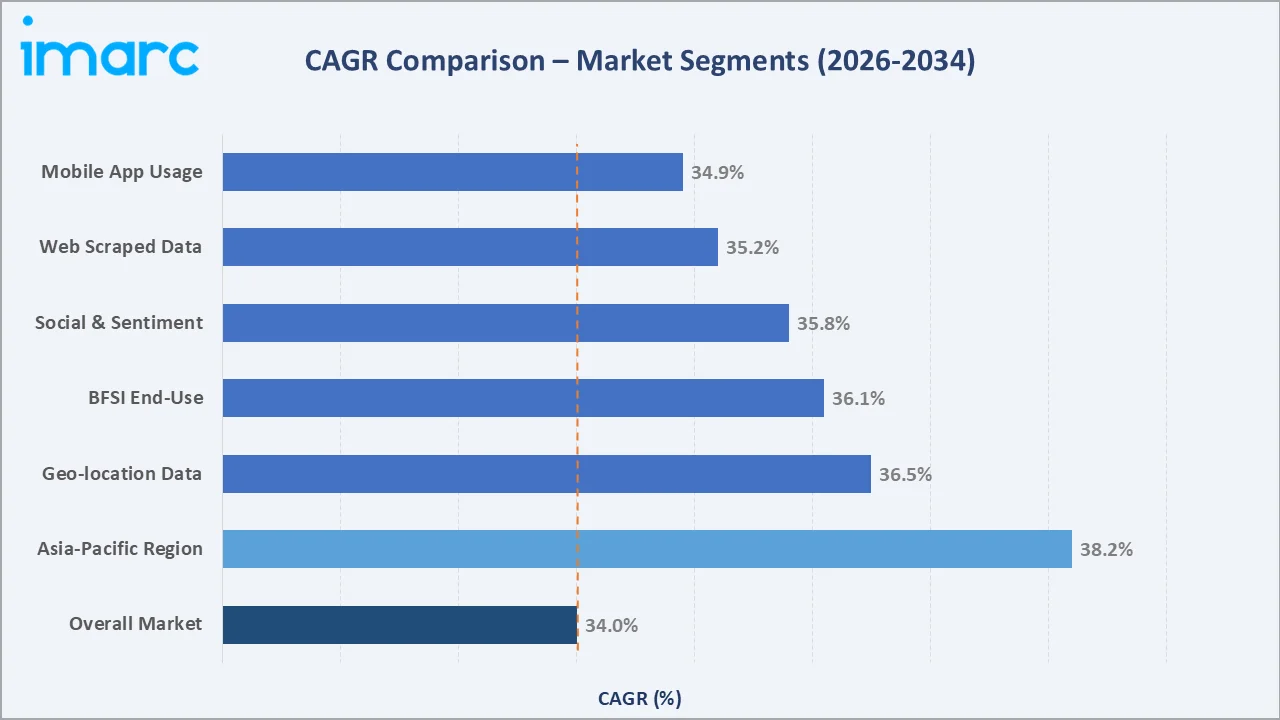

The CAGR across key segments, Asia-Pacific leads at ~38.2% CAGR, while geo-location data at ~36.5% and social and sentiment data at ~35.8% are the fastest-growing data type sub-categories through 2034.

Executive Summary

The global alternative data market is one of the fastest-growing segments in the broader data economy, expanding at 34.0% CAGR from USD 12 Billion in 2025 to USD 168.2 Billion by 2034. Alternative data encompasses all non-traditional, non-public data sources used to generate investment signals and business intelligence, ranging from credit card transaction flows and mobile app usage telemetry to satellite imagery, web scraping outputs, and social sentiment feeds. Industry surveys confirm that 78% of hedge funds integrated some form of alternative data into their investment models by 2022.

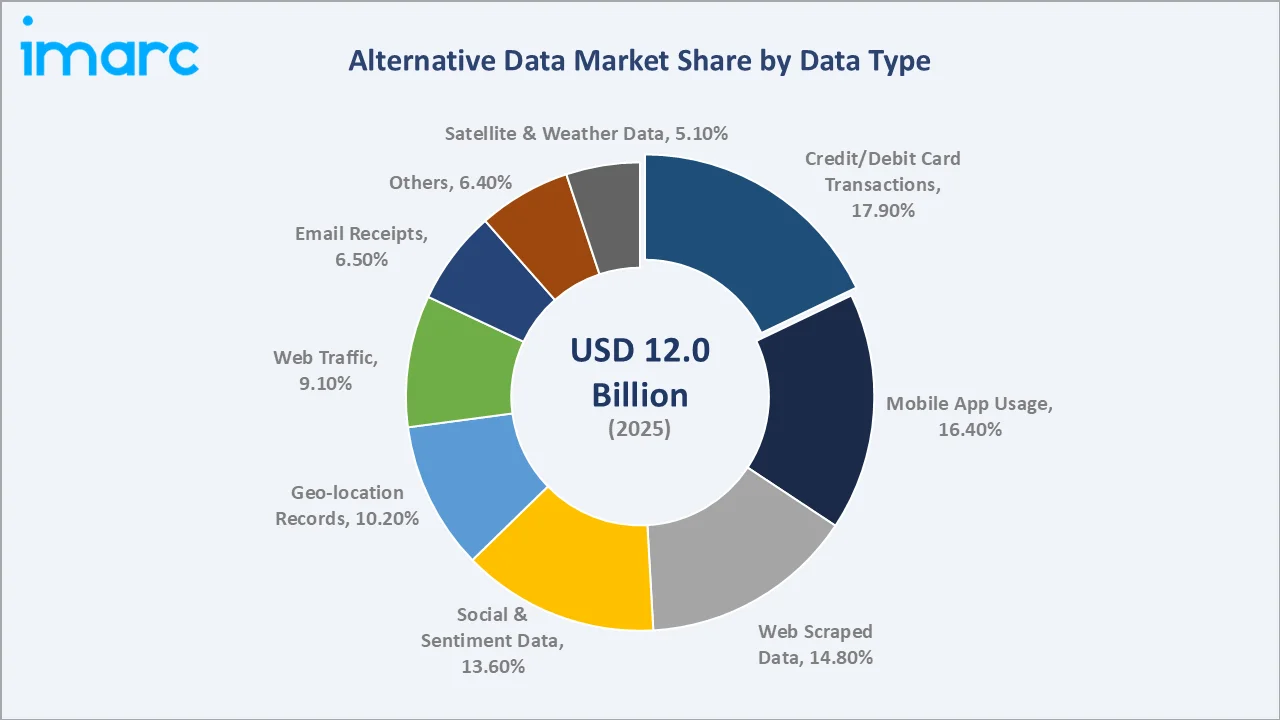

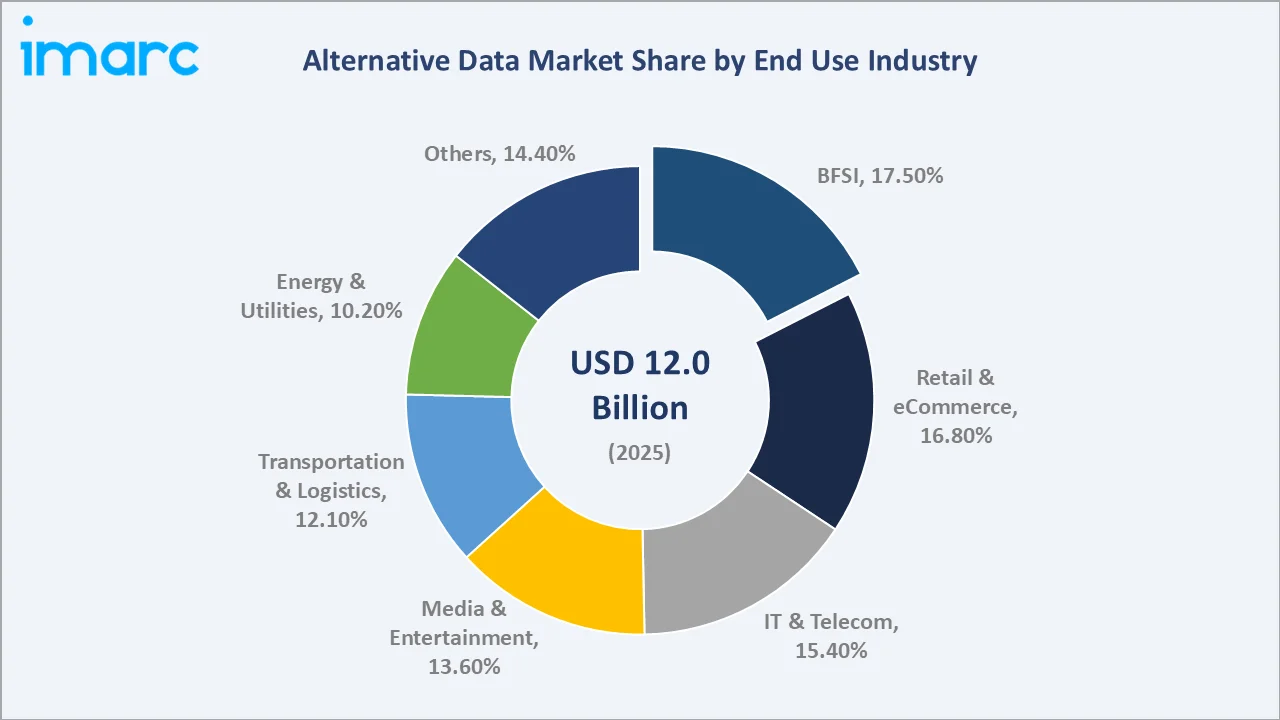

Credit and debit card transactions lead data type at 17.9% in 2025, providing near-real-time consumer spending signals that investment firms use to front-run earnings surprises. Mobile application usage at 16.4% and web scraped data at 14.8% collectively represent the two most scalable digital data collection channels. BFSI commands 17.5% of end-use industry demand, followed by retail and eCommerce at 16.8%, both industries where millisecond information advantages translate directly into commercial returns.

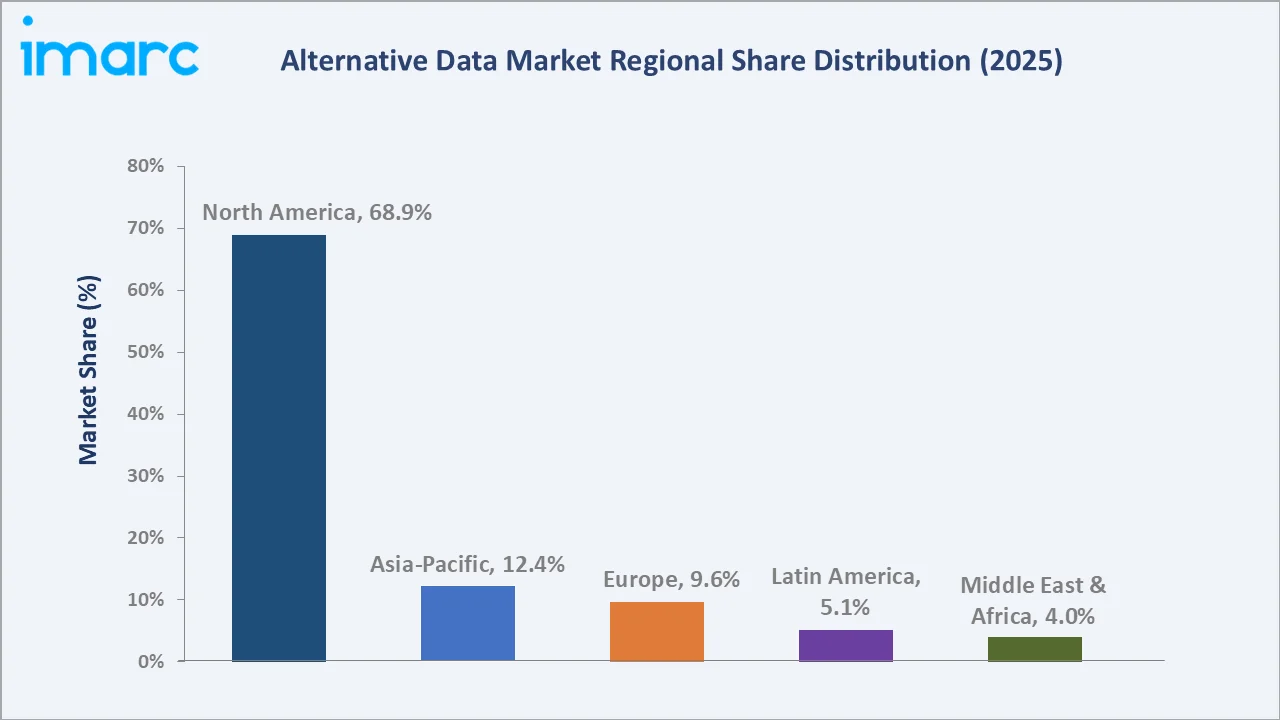

North America's 68.9% regional dominance reflects the US financial industry's unparalleled density and willingness to allocate data procurement budgets. Asia-Pacific at 12.4% in 2025 is growing fastest at ~38.2% CAGR as Asian financial centers and technology companies accelerate adoption.

Key Market Insights

|

Insight |

Data / Finding |

|

Largest Data Type |

Credit & Debit Card Transactions - 17.9% (2025) |

|

Leading End-Use |

BFSI - 17.5% (2025) |

|

Leading Region |

North America - 68.9% (2025) |

|

Fastest Region |

Asia-Pacific - ~38.2% CAGR (2026-2034) |

Analytical Observations Supporting the Above:

- Credit and debit card transactions at 17.9% in 2025, represent the highest-signal alternative data category for retail equity investors. According to BattleFin and Neudata, hedge funds that use transaction-based nowcasting models have consistently generated 2–5% excess alpha.

- BFSI at 17.5% in 2025, is the dominant end-use industry because financial services firms have the highest willingness-to-pay for alpha-generating information and the most quantitatively skilled teams to operationalize alternative signals.

- North America's 68.9% share in 2025 is structurally sustained by the US financial industry's annual revenue base and the concentration of systematic and quantitative hedge funds in New York, Greenwich, and Chicago.

- Asia-Pacific at 12.4% in 2025, growing at ~38.2% CAGR is driven by rapid digital adoption in China, India, South Korea, and Southeast Asia. China's 1.1 billion smartphone users generate extraordinary mobile behavioral data volumes.

Global Alternative Data Market Overview

Alternative data refers to information generated outside traditional financial reporting channels, encompassing consumer behavioral signals, digital exhaust from online activity, physical world observations, and network-derived intelligence. Core categories span credit and debit card transaction aggregations, mobile application behavioral telemetry, web-scraped pricing and product data, social media sentiment analysis, satellite and aerial imagery, geo-location foot traffic records, email receipt panels, and web traffic analytics.

The ecosystem integrates data generators (IoT devices, digital platforms, payment networks), aggregators and cleaners (alt data firms, data brokers), AI/ML analytics platforms, data marketplaces (Bloomberg, Refinitiv, Nasdaq Data Link), and end-use consumers spanning institutional investors, corporates, and government agencies.

Market Dynamics

To evaluate market opportunities, Request Sample

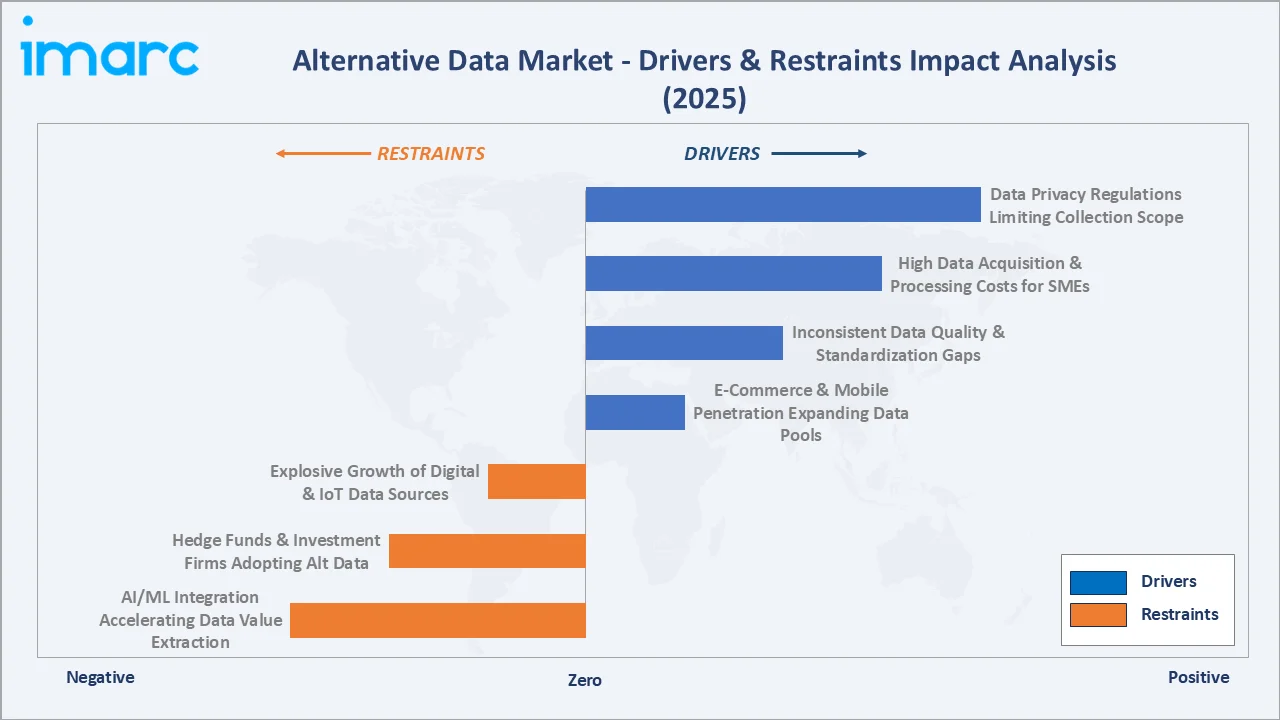

Market Drivers

- AI and ML Integration Accelerating Data Value Extraction: The integration of generative AI and machine learning into alternative data workflows is the most powerful acceleration force. More than 70% of advanced hedge funds applying machine learning to alternative datasets, improving forecast accuracy by 20–30%.

- Hedge Fund and Institutional Investor Adoption: Firms using ML-augmented alternative data models reported 20-30% improvement in commodity price forecasting accuracy. This institutional adoption represents a structurally growing procurement demand base.

- IoT and Digital Platform Data Proliferation: Digital platform expansion, global social media users reaching 5.17 billion in 2024, or 63.7 per cent of the global population, creates exponentially expanding raw alternative data supply that simultaneously increases data volume and reduces per-unit procurement costs.

- E-Commerce and Mobile Penetration Expanding Data Pools: Mobile app install and usage data from 6.9 billion smartphone users globally provides unprecedented consumer engagement intelligence.

Market Restraints

- Data Privacy Regulations Limiting Collection Scope: GDPR enforcement actions totaling EUR 4.5 Billion between 2018 and 2024 demonstrate the real regulatory cost exposure for alternative data collection practices that fail privacy compliance standards.

- High Data Acquisition and Processing Costs for SMEs: Building in-house alternative data processing infrastructure, capable of ingesting and normalizing high-frequency web-scraped or card transaction data.

Market Opportunities

- ESG Alternative Data Growing into USD 1 Billion+ Market: Environmental, social, and governance analytics is emerging as a distinct high-value alternative data category. Satellite-derived carbon emission proxies, supply chain labor practice web scraping, and corporate diversity data extracted from public filings are inputs for ESG rating differentiation.

- Emerging Markets Alternative Data Gaps Creating First-Mover Opportunities: India's 131 billion UPI transactions in FY2024, Southeast Asia's 460 million digital consumers, and Africa's 600 million mobile subscribers generate alternative data pools that remain largely unmonetized as structured analytical products.

- GenAI-Powered Alternative Data Products Reducing Processing Barriers: Generative AI is enabling non-quantitative analysts to access alternative data insights without specialized data science capabilities.

Market Challenges

- Material Non-Public Information (MNPI) Compliance Risks: The SEC's evolving interpretation of what constitutes MNPI in the context of alternative data creates ongoing legal uncertainty for investment managers.

- Data Vendor Fragmentation Creating Integration Complexity: Enterprise integration of 10-20 alternative data feeds requires dedicated data engineering infrastructure that creates significant organizational complexity and ongoing maintenance costs, reducing net value realization from alternative data investment.

Emerging Market Trends

1. Generative AI Transforming Unstructured Data Processing

Generative AI models, particularly GPT-4 class LLMs, can now process, summarize, and extract signals from unstructured text data, including earnings call transcripts, regulatory filings, news articles, and social media, at unprecedented scale and speed. Bloomberg launched its Bloomberg GPT model in 2023, trained on 700 billion tokens of financial text, directly targeting the alternative data analytics use case.

2. Real-Time Alternative Data Enabling Millisecond Investment Decisions

High-frequency and ultra-low-latency alternative data feeds, including real-time web traffic, live social sentiment, and streaming transaction data, are enabling systematic trading strategies that execute on alternative signals within milliseconds of data generation.

3. Satellite Imagery Becoming Mainstream Intelligence Tool

Commercial satellite operators, including Planet Labs and Maxar Technologies, are generating petabytes of daily Earth observation data. AI-processed satellite imagery is used to count parking lot car volumes as retail traffic proxies, monitor crude oil tank shadow levels for inventory estimates, and track agricultural field health for commodity price forecasting.

4. Cross-Dataset Alternative Data Signal Fusion

Leading quantitative funds are combining multiple alternative data sources, credit card spending, combined with foot traffic, combined with social sentiment for a single retail chain, into fused multi-signal models that generate substantially higher predictive accuracy than any individual data source.

5. ESG Alternative Data Mainstreaming Across Asset Classes

ESG investment mandates, with over USD 30 Trillion in global ESG-labeled assets under management in 2022, are expected to surpass USD 40 trillion by 2030 (Bloomberg Intelligence), and are creating structural demand for alternative data that measures environmental and social factors beyond company self-disclosure.

Industry Value Chain Analysis

The alternative data value chain spans six stages from raw data generation through end-use analytical decisions. The highest value add occurs at the data processing and analytics stages, where AI/ML transforms raw signals into actionable investment intelligence.

|

Stage |

Key Players / Examples |

|

Raw Data Sources |

Web platforms (Google, Meta, Amazon), payment networks (Visa, Mastercard), IoT sensors, satellite operators (Planet Labs, Maxar), mobile carriers |

|

Data Collection |

Web scrapers, API aggregators, panel operators, satellite download stations, sensor network integrators, email receipt panel companies |

|

Data Processing |

AI/ML cleaning, NLP annotation firms, geospatial processors, data normalization platforms, anonymization engines |

|

Data Distribution |

Bloomberg Data License, Refinitiv Eikon, Nasdaq Data Link (Quandl), FactSet, S&P Capital IQ, dedicated alt data marketplaces |

|

Analytics & Insights |

Quantitative hedge funds, asset management firms, corporate strategy teams, risk analytics providers, and AI signal generation platforms |

|

End-Use Decisions |

Portfolio construction, risk management, M&A due diligence, supply chain optimization, marketing personalization, and regulatory compliance |

The data distribution and analytics stages command the highest margin capture. Bloomberg's data services division generates Billions annually in data licensing revenue, with alternative data products. Palantir's US commercial segment, generated USD 702 Million in 2023, demonstrating the premium pricing achievable for AI-augmented alternative data analytics platforms.

Technology Landscape in the Alternative Data Industry

AI/ML Signal Extraction from Unstructured Data

Natural language processing (NLP) and large language models are the core enabling technologies for alternative data value creation. Bloomberg GPT (2023), trained on 700 billion financial tokens, demonstrates domain-specific LLM capability that improves signal extraction accuracy for financial alternative data applications.

Cloud-Native Alternative Data Infrastructure

Cloud platforms, including AWS, Microsoft Azure, and Google Cloud, have become the backbone of alternative data processing infrastructure. Cloud democratization is reducing IT costs by 20-30%, enabling mid-tier asset managers to access capabilities previously limited to multi-billion-dollar quantitative hedge funds.

Real-Time Streaming Alternative Data Technology

Real-time streaming data commands 5-10x price premiums versus batch-delivered equivalents, representing the highest-margin alternative data product category for vendors in 2025.

Geospatial Analytics and Computer Vision

Computer vision AI applied to satellite and aerial imagery is converting visual data into quantitative signals at a commercial scale. Geospatial AI platforms, including Descartes Labs, process millions of satellite images daily to generate agriculture, energy, and transportation intelligence products that institutional investors access through standardized data feeds.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Data Type |

Credit and Debit Card Transactions |

17.9% |

2025 |

|

End Use Industry |

BFSI |

17.5% |

2025 |

|

Region |

North America |

68.9% |

2025 |

By Data Type

Credit and debit card transactions lead at 17.9% in 2025 as the most commercially validated alternative data category. About US$130 million is spent on card data annually by asset managers, according to Opimas estimates. These signals generate a 2-3 week lead time advantage over official retail sector earnings, directly explaining their premium in investment manager data procurement budgets.

To access detailed market analysis, Request Sample

Mobile application usage at 16.4% reflects the intelligence value of 6.9 billion smartphone behavioral data streams. Web scraped data (14.8%) encompasses pricing intelligence, job posting trend analysis, and product availability tracking from millions of websites daily. Social and sentiment data (13.6%) processes billions of social media posts, news articles, and forum discussions through NLP models to generate market sentiment indices. Satellite and weather data at 5.1% is growing fastest within the type segments as commercial satellite constellation expansion reduces imagery costs by 30-40% annually.

By End-Use Industry

BFSI commands 17.5% of end-use demand in 2025, driven by hedge fund, asset management, and quantitative trading firm procurement of high-frequency investment signals. The global hedge fund industry manages approximately USD 4.5 trillion in 2024 (HFR), with alternative data procurement budgets. This concentrated, high-value procurement base makes BFSI the alternative data market's anchor demand vertical.

Retail and eCommerce at 16.8% (2025) reflects commercial use of alternative data for competitive pricing intelligence, consumer demand forecasting, and supply chain optimization. IT and Telecommunications at 15.4% uses alternative data for network optimization, churn prediction, and competitive benchmarking. Energy and Utilities at 10.2% applies satellite and weather data to grid load forecasting and renewable energy production prediction.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers |

|

North America |

68.9% |

US hedge fund & quant fund density; SEC compliance culture; Silicon Valley data firms; VC investment in alt data |

|

Asia-Pacific |

12.4% |

China 1.1B smartphone users; India UPI 131B transactions FY2024; Singapore fintech hub; crypto/DeFi data growth |

|

Europe |

9.6% |

MiFID II data transparency; ESG mandates; London hedge fund cluster; GDPR-compliant data products |

|

Latin America |

5.1% |

Brazil digital payment expansion; Mexico fintech growth; regional e-commerce data monetization |

|

Middle East & Africa |

4.0% |

UAE sovereign wealth alternative data adoption; Africa mobile money data; Saudi Vision 2030 fintech |

North America's 68.9% dominance in 2025 is structurally sustained by the highest global concentration of systematic and quantitative investment funds. The US SEC's guidance on alternative data, providing a compliance framework rather than prohibition, has institutionalized adoption that European regulatory complexity partially constrains.

Asia-Pacific, with 12.4% in 2025, is the fastest-growing region. China's 1.1 billion smartphone users generate mobile behavioral datasets of unparalleled scale. India's UPI digital payment system processed 131 billion transactions in FY2024, generating real-time consumer spending signals comparable in analytical value to US card network data, but with far lower current monetization rates.

Europe, with 9.6% in 2025, benefits from London's hedge fund cluster but faces GDPR compliance complexity that constrains certain personal data collection methodologies. Latin America (5.1%) and MEA (4.0%) represent earlier-stage markets with high growth potential as digital payment infrastructure matures.

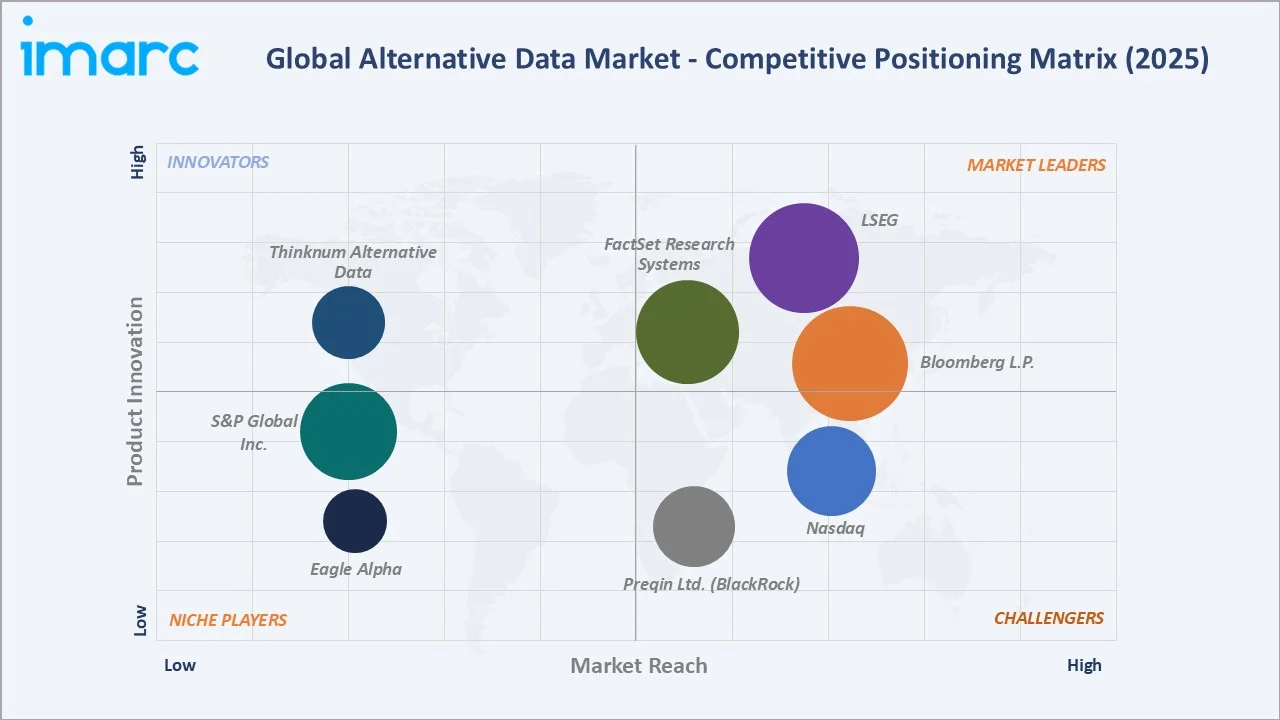

Competitive Landscape

The global alternative data market is moderately fragmented. The market bifurcates between established financial data giants leveraging distribution advantages and specialized pure-play alternative data firms competing on data exclusivity and signal alpha.

|

Company Name |

Key Platform / Services |

Market Position |

Core Strength |

|

Bloomberg L.P. |

Bloomberg Terminal and Data License |

Leader |

Real-time financial + alternative data integration; global coverage |

|

London Stock Exchange Group (LSEG) |

LSEG Workspace |

Leader |

Multi-asset data, trading analytics, alternative datasets |

|

FactSet Research Systems |

Featured Datasets includes Environmental, Social, and Governance, Geographic Revenue Exposure, Industry Classifications with Revenue, Intellectual Capital, Sentiment, and Shipping and Supply Chain |

Leader |

Integrated analytics, portfolio tools, alt data integration |

|

S&P Global Inc. |

Alternative datasets via Cloud, Data Feed, API Solutions and Capital IQ Pro |

Leader |

AI-driven analytics, credit intelligence, alt data capabilities |

|

Nasdaq |

Nasdaq Data Link |

Challenger |

Alternative data marketplace, API-based delivery |

|

Preqin Ltd. (A BlackRock’s Subsidiary) |

Preqin Pro |

Challenger |

Private market & hedge fund data intelligence |

|

Thinknum Alternative Data |

Thinknum Spark |

Challenger |

Web-scraped datasets, consumer/company signals |

|

Eagle Alpha |

Data Vendor Solution Data Buyer Solution |

Emerging |

Alternative data sourcing, vendor intelligence |

The competitive positioning of key alternative data market participants across global market presence and strategic investment dimensions in 2025.

Key Company Profiles

Bloomberg L.P.

Bloomberg L.P. is the world's largest financial data and media company, privately held and headquartered in New York City. Bloomberg's data services division generates billions, with alternative data products including Bloomberg Second Measure (consumer spending), Bloomberg Satellite (geospatial analytics), and Bloomberg ESG Data forming a fast-growing segment.

- Product Portfolio: Bloomberg Terminal and Data License

- Recent Developments: In January 2026, Bloomberg launched Data Entitlements within {ALTD <GO>} on its Terminal, enhancing its investment research solutions with near real-time insights driven by alternative data.

- Strategic Focus: Bloomberg's strategy integrates AI and GenAI capabilities across its entire alternative data product suite, using Bloomberg GPT as the underlying language model for natural language alternative data queries.

London Stock Exchange Group (LSEG)

LSEG acquired Refinitiv for USD 27 Billion in 2021, creating the second-largest global financial data operation. LSEG's World-Check risk intelligence database and Refinitiv News & Research are core alternative data assets used by banks, asset managers, and compliance officers globally.

- Product Portfolio: The company offers alternative data for extensive financial analysis and insights

- Recent Developments: In December 2025, London Stock Exchange Group (LSEG) entered into a strategic partnership with OpenAI to integrate its licensed financial data and analytics into ChatGPT .

- Strategic Focus: LSEG's strategy combines its unrivaled news and corporate fundamentals database with AI-powered alternative signal extraction, targeting the systematic trading and quantitative research community that requires structured, compliant alternative signals delivered through standardized APIs and integrated directly into trading infrastructure.

FactSet Research Systems Inc.

FactSet Research Systems is headquartered in Norwalk, Connecticut. It's Open:FactSet Marketplace, launched in 2018 and expanded aggressively through 2024, hosts alternative data providers whose datasets are accessible directly within the FactSet Workstation, making FactSet the leading neutral alternative data distribution platform in the institutional investment community.

- Product Portfolio: The company’s featured datasets include Environmental, Social, and Governance, Geographic Revenue Exposure, Industry Classifications with Revenue, Intellectual Capital, Sentiment, and Shipping and Supply Chain.

- Recent Developments: In December 2025, FactSet and Arcesium partnered to unify investment management workflows across public, private, and alternative markets, enabling more seamless data integration and operational efficiency for investment professionals .

- Strategic Focus: FactSet's strategy focuses on becoming the premier neutral alternative data marketplace and integration platform for institutional investment managers - positioning Open:FactSet as the industry standard for compliant, standardized alternative data discovery, licensing, and consumption alongside traditional financial data within a unified workflow.

Preqin Ltd.

- Preqin Ltd., a Blackrock subsidiary, specializes in alternative asset data, including private equity, hedge funds, and real estate investments.

- Product Portfolio: The company offer alternative data services under Preqin Pro.

- Recent Developments: In June 2024, BlackRock Inc. announced a $3.2 billion acquisition of private markets data provider Preqin Ltd.

- Strategic Focus: Focused on delivering deep insights into alternative investments, helping investors identify opportunities and optimize portfolios.

Market Concentration Analysis

The alternative data market's moderate fragmentation, with top 5 holding 35-49% in 2025, reflects the market's relative immaturity and the competitive advantage of data exclusivity over distribution scale. A small satellite imagery provider with exclusive access to a key shipping lane can command premium pricing that challenges large incumbents on specific analytical use cases.

Consolidation is accelerating, all transactions partially motivated by alternative data capability acquisition. The next consolidation wave (2025-2028) is expected to focus on AI-native alternative data startups being acquired by established financial data platforms seeking generative AI capabilities.

Investment & Growth Opportunities

Highest-Growth Segments

ESG alternative data at an estimated 40-45% CAGR through 2034 is the highest-growth sub-category within the alternative data market. Investment in satellite-derived carbon emission monitoring, AI-processed supply chain labor analytics, and water usage estimation from remote sensing platforms positions vendors in the most regulation-protected, premium-priced alternative data category. Real-time alternative data streaming, growing at an estimated 38-40% CAGR, commands 5-10x price premiums over batch equivalents and represents the highest per-unit revenue opportunity within the market.

Emerging Markets

South and Southeast Asia present the highest-upside emerging market for alternative data business development. India's 131 billion UPI transactions in FY2024, 958 million internet users, and high smartphone users generate consumer behavioral datasets comparable in analytical richness to US alternative data pools but with far lower current monetization. The first alternative data providers building India-focused consumer spending intelligence products for institutional investors can establish first-mover pricing and exclusivity advantages before market saturation. Southeast Asia's 460 million digital consumers across Indonesia, Vietnam, Thailand, Philippines, and Malaysia represent similar opportunities for mobile behavioral and digital commerce alternative data product development.

Venture and Strategic Investment Trends

Strategic M&A multiples for alternative data companies with proprietary, exclusive datasets range 8-15x annual recurring revenue, premium valuations reflecting the strategic scarcity of exclusive data assets. Snowflake's alternative data marketplace now hosts 350+ data providers, and its Data Cloud architecture is becoming the infrastructure layer connecting alternative data producers and consumers at scale, creating an investment opportunity in Snowflake-native alternative data application companies.

Future Market Outlook 2026-2034

The global alternative data market is forecast to expand from USD 12 Billion in 2025 to USD 168.2 Billion by 2034 at a CAGR of 34.0%, adding approximately USD 156.1 Billion in incremental market value - a 13.9x multiplication representing one of the most aggressive growth trajectories in the global data economy.

Phase 1 (2026-2028) will be defined by generative AI becoming the standard analytical layer for unstructured alternative data, real-time streaming data displacing batch delivery as the institutional standard, and ESG alternative data growing. Phase 2 (2029-2031) will see Asian alternative data markets, particularly India and Southeast Asia, reaching developed market monetization rates, quantum-scale computing enabling simultaneous cross-dataset signal fusion across 100+ data sources, and regulatory frameworks maturing globally to provide compliance certainty that accelerates corporate alternative data adoption beyond the financial services sector.

Phase 3 (2032-2034) will represent autonomous AI trading systems where alternative data signals are consumed, processed, and acted upon entirely by AI agents without human analyst intermediation, compressing data-to-decision latency from hours to microseconds and creating entirely new market microstructure dynamics driven by alternative data signal propagation speed advantages.

Research Methodology

Primary Research

Primary research encompassed over 60 structured interviews in 2024-2025 with alternative data market participants including Chief Data Officers at institutional investment managers (hedge funds, asset managers, pension funds), product managers, alternative data vendor founders and CEOs, SEC compliance counsel specializing in MNPI and alternative data, quantitative strategists at leading systematic trading firms, and VC investment partners covering data infrastructure investments.

Secondary Research

Key secondary sources include Alternativedata.org vendor database, HFR Global Hedge Fund Industry Report (2024), Institutional Investor alternative data surveys (2022-2024), Bloomberg Intelligence financial data market analysis, FactSet FY2024 Annual Report, NPCI UPI transaction data (FY2024), CNNIC China Internet Statistics (2024), PitchBook data intelligence VC investment reports, SEC enforcement action database, and trade publications including Institutional Investor, Risk.net, and the Journal of Alternative Investments.

Forecasting Models

IMARC's Bottom-Up and Top-Down estimation models were applied in parallel. Bottom-Up aggregates alternative data revenue by data type category and end-use industry vertical, calibrated against disclosed vendor revenues and industry procurement survey data. Top-Down applies global investment management AUM growth rates and alternative data penetration benchmarks across institutional investor segments.

Alternative Data Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Data Types Covered | Mobile Application Usage, Credit and Debit Card Transactions, Email Receipts, Geo-Location (Foot Traffic) Records, Satellite and Weather Data, Social and Sentiment Data, Web Scraped Data, Web Traffic, Others |

| End Use Industries Covered | Transportation and Logistics, BFSI, Retail and ECommerce, Energy and Utilities, IT and Telecommunications, Media and Entertainment, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | The United States, Canada, Germany, France, the United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Bloomberg L.P., London Stock Exchange Group (LSEG), FactSet Research Systems, S&P Global Inc., Nasdaq, Preqin Ltd. (A BlackRock’s Subsidiary), Thinknum Alternative Data, Eagle Alpha., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, alternative data market forecast, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global alternative data market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the Alternative Data industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Alternative Data Market Report

The global alternative data market reached USD 12 Billion in 2025, driven by hedge fund adoption and AI analytics integration.

The market is projected to reach USD 168.2 Billion by 2034 at a CAGR of 34.0% during ?2026-2034, representing a 13.9x multiplication from the 2025 base value.

Alternative data includes non-traditional information sources, credit card transactions, satellite imagery, social sentiment, and mobile app usage that generate investment signals and business intelligence beyond standard financial reporting.

Credit and debit card transactions lead at 17.9% in 2025. These aggregated spending signals provide a 2-3 week lead time over official retail earnings, generating premium investment signals for equity investors.

BFSI dominates at 17.5% in 2025. Hedge funds allocation to alternative data procurement, with some multi-strategy funds in data budgets annually.

North America dominates at 68.9% in 2025, driven by US hedge fund density, quantitative trading firm concentration, and a mature SEC compliance framework that institutionalizes alternative data adoption.

Asia-Pacific is fastest-growing at ~38.2% CAGR, driven by China's 1.1 billion smartphone users, India's 131 billion UPI transactions in FY2024, and Singapore's emergence as Asia's premier hedge fund hub.

Key players include Bloomberg L.P., London Stock Exchange Group (LSEG), FactSet Research Systems, S&P Global Inc., Nasdaq, Preqin Ltd. (A BlackRock’s Subsidiary), Thinknum Alternative Data, and Eagle Alpha.

Key challenges include GDPR, CCPA, and PIPL data privacy compliance constraints, SEC MNPI legal uncertainty, high procurement costs (USD 50,000-500,000 per data feed), and data quality standardization gaps.

Industry surveys confirmed 78% of hedge funds integrated alternative data by 2022. Firms using ML-augmented alternative data improvement in commodity price forecasting versus traditional analysis methods.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)