Antifouling Paints and Coatings Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

Antifouling Paints and Coatings Market Size, Share, Trends & Forecast (2026-2034)

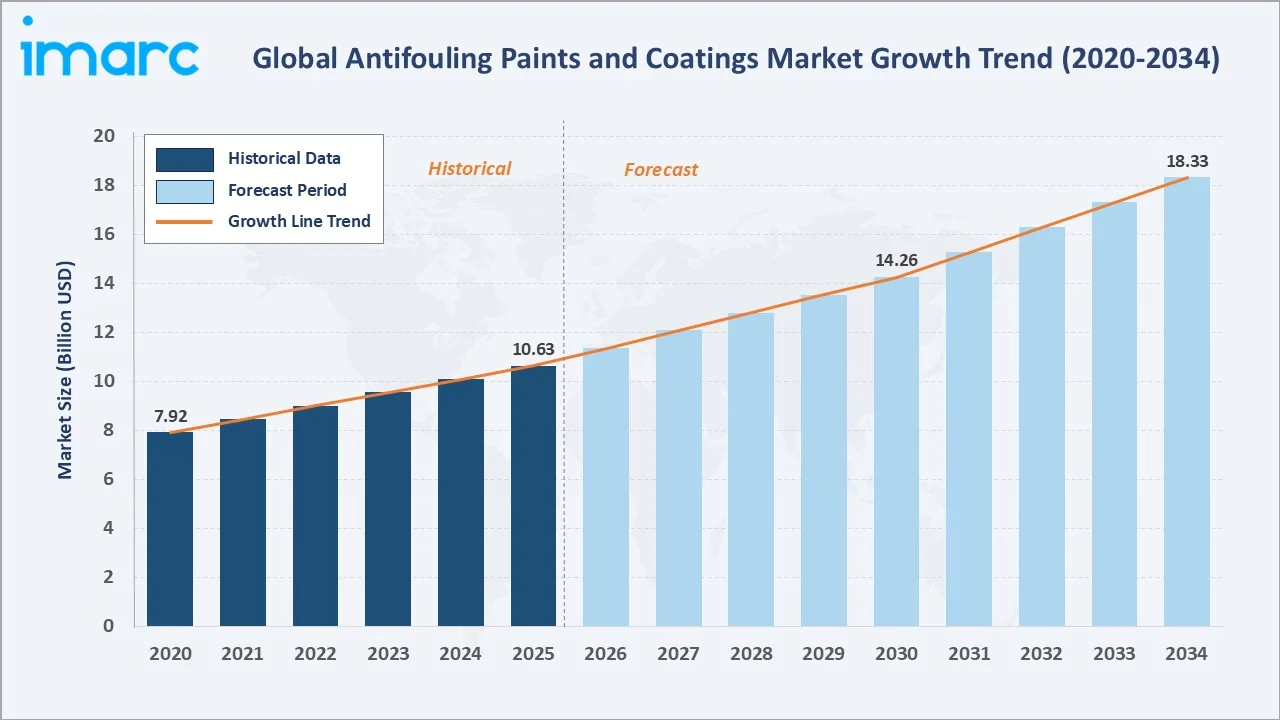

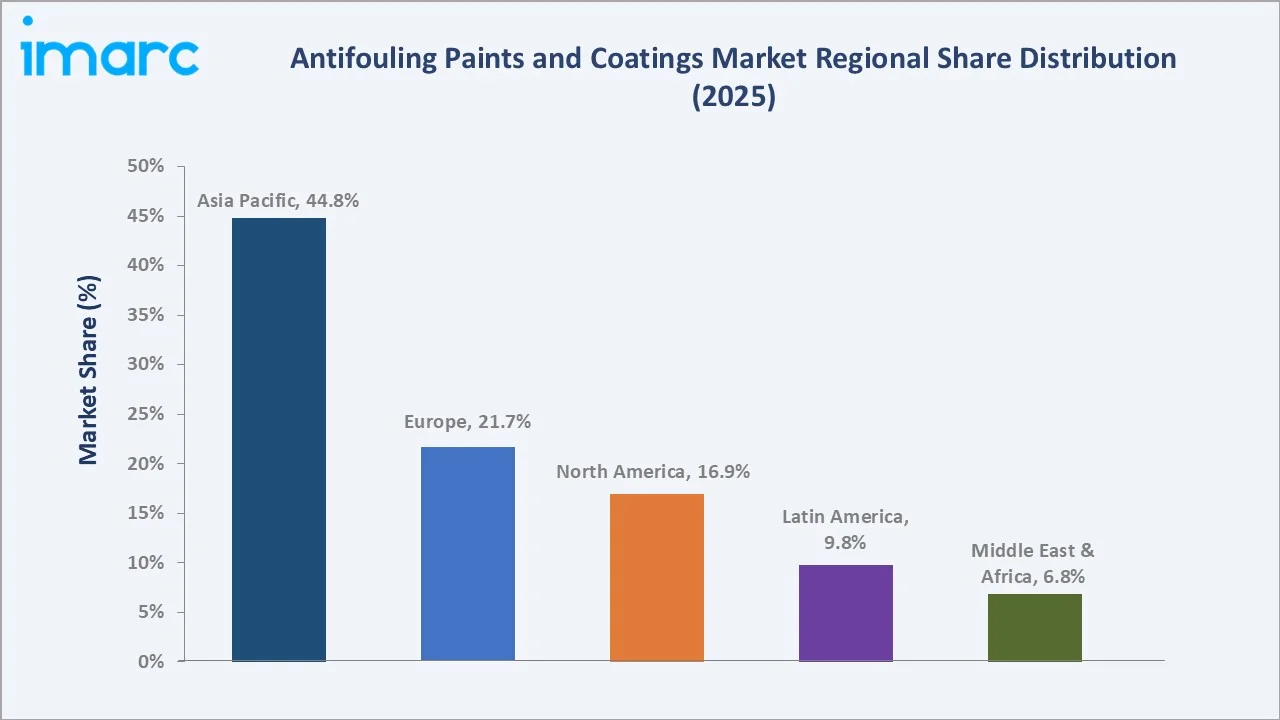

The global antifouling paints and coatings market reached USD 10.63 Billion in 2025 and is projected to reach USD 18.33 Billion by 2034, growing at a CAGR of 6.05% during 2026-2034. The market is driven by increasing shipbuilding and marine transportation activities, along with rising demand for eco‑friendly, corrosion‑resistant coatings to protect vessels and offshore structures from biofouling and improve fuel efficiency. Maritime transport forms the foundation of global trade, handling more than 80% of the world’s traded goods by volume. This extensive reliance on shipping drives the antifouling paints and coatings market as vessel owners and operators seek to protect hulls from biofouling, corrosion, and drag. Copper-based leads at 41.3%. Shipping vessels dominate the application at 38.9%. Asia Pacific commands 44.8% of the global market share.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 10.63 Billion |

| Forecast Market Size (2034) | USD 18.33 Billion |

| CAGR (2026-2034) | 6.05% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Dominant Type | Copper-Based (41.3%, 2025) |

| Dominant Application | Shipping Vessels (38.9%, 2025) |

| Leading Region | Asia Pacific (44.8%, 2025) |

The global antifouling paints and coatings market expanded from USD 7.92 Billion in 2020 to USD 10.63 Billion in 2025, anchored at USD 14.26 Billion in 2030, and forecast to reach USD 18.33 Billion by 2034. Antifouling paints and coatings prevent the attachment and growth of aquatic organisms on submerged marine surfaces through biocidal chemistry or physical fouling release mechanisms.

To get more information on this market, Request Sample

Silicone elastomers grow fastest at ~8.2% CAGR, creating fleet operator incentive to adopt premium fouling release coatings for quantifiable fuel efficiency documentation above standard biocidal antifouling. Shipping vessels application grows at ~6.1% CAGR through global fleet expansion driven by post-COVID trade recovery and LNG fleet build-out. Drilling rigs and platforms grow at ~6.4% CAGR through deepwater project investments.

Executive Summary

The global antifouling paints and coatings market at USD 10.63 Billion in 2025 represents one of the most commercially fundamental protective coating categories in the global maritime industry, a product category whose commercial necessity is defined by the immutable biological reality that all submerged marine surfaces become colonized by biofouling organisms within weeks of immersion without chemical or physical protection, creating measurable economic penalties that make antifouling coating investment commercially compelling above any alternative hull management approach. The market is projected to reach USD 18.33 Billion by 2034.

Copper-based at 41.3% leads through cost-effectiveness and well-established performance for the global commercial fleet's budget-driven procurement. Shipping vessels at 38.9% leads the application. Asia Pacific leads regionally at 44.8%.

Key Market Insights

| Insight | Data |

|---|---|

| Dominant Type | Copper-Based – 41.3% share (2025) |

| Dominant Application | Shipping Vessels – 38.9% market share (2025) |

| Leading Region | Asia Pacific – 44.8% share (2025) |

| Market Opportunity | Biocide-free silicone fouling release; deepwater platform coating innovation; naval vessel antifouling; eco-friendly copper-free SPC |

Key Analytical Observations Supporting The Above Data:

- Copper-Based at 41.3%: Copper-based antifouling paints dominate due to their effective protection against biofouling organisms, long-lasting performance, and proven track record in reducing hull drag and maintenance costs for marine vessels.

- Shipping Vessels at 38.9%: Shipping vessels dominate because they require continuous protection against biofouling to maintain fuel efficiency, reduce maintenance costs, and comply with international maritime regulations, making them the primary end users of these coatings.

- Asia Pacific at 44.8%: The Asia Pacific region dominates regionally due to its large shipbuilding industry, extensive maritime trade routes, and high concentration of commercial and naval vessels, driving strong regional demand for protective coatings.

Antifouling Paints and Coatings Market Overview

The global antifouling paints and coatings market operates within the broader marine and protective coatings industry as the most commercially and technically differentiated single marine coating category above commodity industrial protective coatings. Antifouling's commercial uniqueness is its biologically active mechanism; antifouling paints are the only major industrial coating category whose primary function is biological rather than corrosion or chemical protection, requiring understanding of marine biology, ecotoxicology, and regulatory biocide approval above pure coating chemistry expertise.

The market ecosystem integrates globally distributed biocide and resin raw material supply, antifouling paint formulation and manufacturing at regional paint plants, technical specification and testing at the shipyard, regulatory compliance, and hull performance monitoring during vessel operation. Macroeconomic factors include growth in global maritime trade, increasing shipbuilding activities, and rising demand for fuel-efficient and environmentally compliant vessels.

Market Dynamics

To evaluate market opportunities, Request Sample

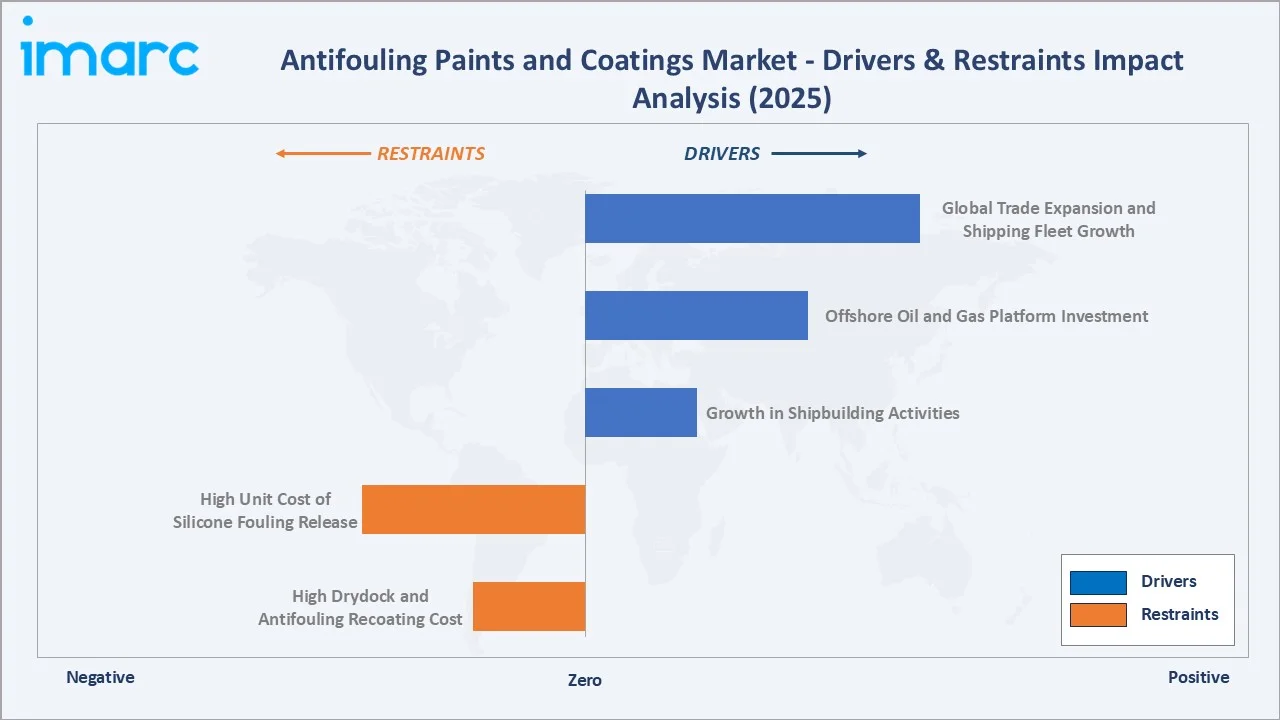

Market Drivers

- Global Trade Expansion and Shipping Fleet Growth: In 2025, global trade in goods and commercial services rose by 7% to reach US$34.65 trillion, up from a 4% increase the previous year. Trade in goods grew by 6%, while services expanded more rapidly, increasing by 8%. This expansion of global trade and the growth of the shipping fleet are increasing the number of vessels requiring protection against biofouling and corrosion. As more goods are transported worldwide, shipping companies prioritize hull efficiency and durability, boosting demand for antifouling coatings. The rise in new ship construction, fleet modernization, and the replacement of older vessels further stimulates market growth. This trend ensures widespread adoption of advanced antifouling solutions across commercial, naval, and offshore vessels, supporting sustained market expansion.

- Offshore Oil and Gas Platform Investment: Investments in offshore oil and gas platforms increase demand for protective coatings that prevent biofouling, corrosion, and structural degradation in harsh marine environments. These platforms require durable, long-lasting coatings to maintain operational efficiency, reduce maintenance costs, and ensure safety. As exploration and production activities expand globally, the need for advanced antifouling solutions on rigs, subsea structures, and support vessels grows, directly supporting market growth in the marine and offshore sectors.

- Growth in Shipbuilding Activities: Growth in shipbuilding activities is increasing the demand for protective coatings on newly constructed commercial, naval, and recreational vessels. As shipyards expand production to meet global trade and fleet renewal needs, more hull surfaces require biofouling prevention and corrosion protection. This growth stimulates demand for advanced antifouling solutions that enhance vessel efficiency, reduce maintenance, and extend service life, thereby supporting sustained market expansion.

Market Restraints

- High Drydock and Antifouling Recoating Cost: High drydock and antifouling recoating costs increase the overall maintenance expenses for vessel operators. Frequent hull recoating and drydock periods are capital-intensive, especially for large fleets, making operators cautious about adopting advanced or premium antifouling coatings. These high costs can limit market penetration, particularly among smaller shipping companies or in regions with price-sensitive operators, slowing overall growth despite rising demand for vessel protection and fuel efficiency.

- High Unit Cost of Silicone Fouling Release: The high unit cost of silicone fouling release coatings makes these advanced coatings less accessible for price-sensitive vessel operators. Despite their effectiveness in preventing biofouling and reducing fuel consumption, the premium price limits widespread adoption, especially for smaller ships or fleets with tight maintenance budgets. This cost barrier slows market growth and encourages some operators to continue using more affordable, conventional antifouling coatings.

Market Opportunities

- Underwater Robotic Hull Cleaning: Underwater robotic hull cleaning enhances the maintenance and longevity of coated vessels without requiring costly drydock periods. These robotic systems allow frequent, in-situ cleaning to remove biofouling, improving fuel efficiency and reducing drag while preserving the integrity of antifouling coatings. In May 2024, CLIIN Robotics unveiled its latest advancement: Robotic Antifouling, designed to revolutionize vessel maintenance with enhanced efficiency, sustainability, and performance. Maintaining a clean hull, it reduces fuel consumption, lowers greenhouse gas emissions, promotes sustainability, and ensures cost-effectiveness while also helping to prevent the spread of invasive species.

- Advancement in Eco-Friendly Coatings: Advancements in eco-friendly coatings enable non-toxic, low-VOC, and silicone-based solutions that comply with stringent environmental regulations. These coatings effectively prevent biofouling while minimizing ecological impact, appealing to environmentally conscious shipping companies and regulatory bodies. As global maritime operations increasingly prioritize sustainability, the demand for green antifouling solutions grows, encouraging innovation and adoption of premium, high-performance coatings across commercial, naval, and offshore vessels.

Market Challenges

- Competition from Conventional Coatings: Competition from conventional coatings offering lower-cost alternatives to advanced or eco-friendly antifouling solutions. Many vessel operators continue to rely on traditional paints due to familiarity, proven performance, and affordability, limiting the adoption of premium or high-performance coatings. This price sensitivity slows market growth and innovation, especially in regions or segments where operational budgets are constrained, despite increasing demand for sustainable and high-efficiency antifouling solutions.

- Technical Challenges: Technical challenges create complexities in application, performance, and durability across different vessel types and hull materials. Proper coating requires precise surface preparation, correct thickness, and adherence to environmental conditions, while biofouling resistance can vary with water temperature, salinity, and marine organisms. These operational and performance uncertainties increase maintenance requirements, raise costs, and can deter adoption of advanced antifouling solutions, especially among operators unfamiliar with newer coating technologies.

Emerging Market Trends

1. Biofouling as an Invasive Species Vector Creating a Biosecurity-Driven Market

Vessel hulls and submerged marine structures can transport harmful organisms across regions, prompting stricter regulations and compliance requirements. This trend increases demand for advanced antifouling coatings that effectively prevent biofouling, protect marine ecosystems, and help shipping companies meet international biosecurity standards. Consequently, coatings that combine high-performance fouling prevention with environmental safety are becoming increasingly important, shaping market growth.

2. Hull Performance Management Transforming Antifouling from Product to Service

Hull performance management is transforming antifouling coatings from a one-time product into an ongoing service. Through sensors, IoT, and data analytics, ship operators can continuously monitor hull condition, fouling levels, and coating effectiveness. This enables predictive maintenance, optimized recoating schedules, and fuel efficiency improvements. In February 2026, GIT Coatings launched its next-generation graphene-based hard foul-release coating, XGIT-FORCE. This introduction represents a major shift in the maritime industry, moving beyond conventional biocide-based antifouling methods toward a new era focused on advanced hull performance management.

3. Fluoropolymer and Nano-Technology Creating Next-Generation Fouling Release Surface

Fluoropolymers and nanotechnology are enhancing the smoothness, durability, and hydrophobic properties of hull coatings. These advanced coatings prevent marine organisms from adhering, reducing drag, fuel consumption, and maintenance needs. By combining nanoscale surface engineering with fluoropolymer chemistry, manufacturers can develop coatings that are long-lasting, environmentally friendly, and effective across diverse marine conditions. This trend supports the shift toward high-performance, sustainable antifouling solutions, driving innovation and premium adoption in the market.

4. Naval and Defence Antifouling Creating Above-Commercial-Grade Specification Premium Market

Naval and defense antifouling coatings delivering performance levels that exceed commercial-grade specifications. These coatings are designed to withstand harsh marine environments, provide superior biofouling protection, and maintain operational efficiency for naval and defense vessels. The demand for high-durability, low-maintenance, and environmentally compliant coatings in military applications drives innovation and adoption. This trend positions antifouling solutions as high-value, specialty products, catering to fleets requiring exceptional performance and long service life beyond standard commercial requirements.

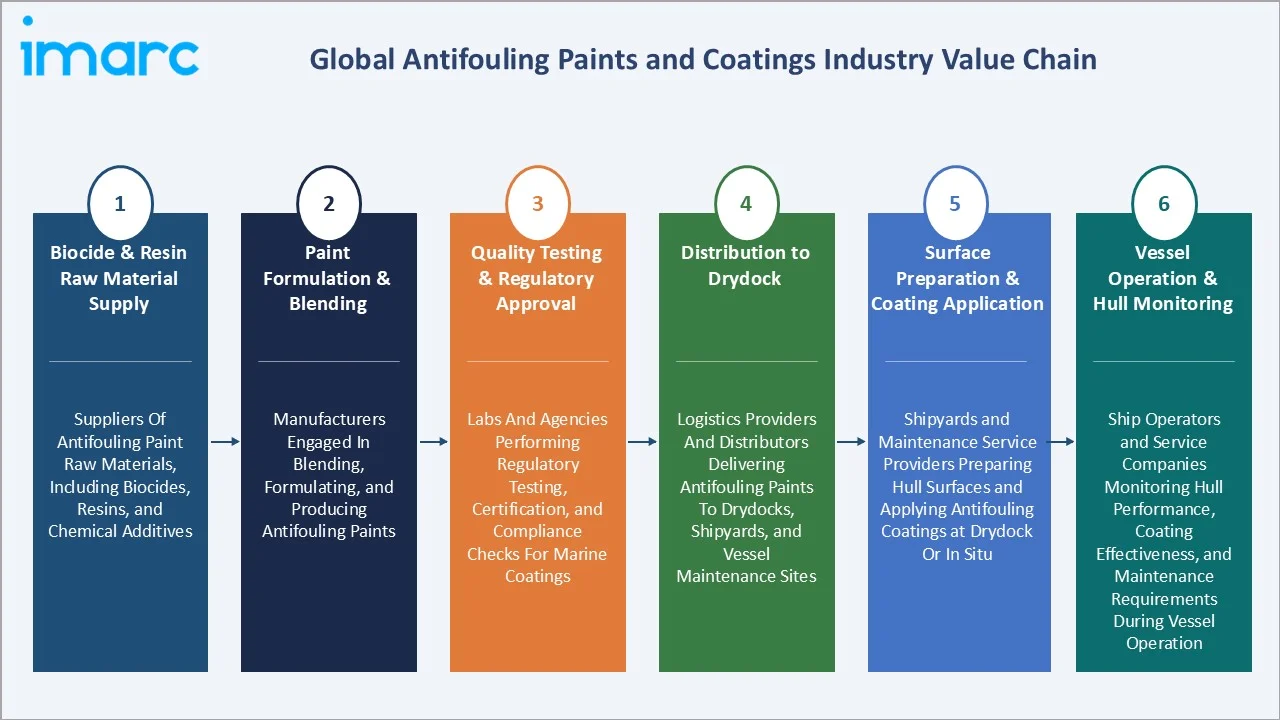

Industry Value Chain Analysis

The global antifouling paints and coatings value chain encompasses biocide and resin raw material production, antifouling paint formulation and manufacturing at regional paint plants, technical specification and testing, regulatory compliance and approval, drydock application, and vessel operation with hull performance monitoring.

| Stage | Key Players / Examples |

|---|---|

| Biocide & Resin Raw Material Supply | Suppliers of antifouling paint raw materials, including biocides, resins, and chemical additives. |

| Paint Formulation & Blending | Manufacturers engaged in blending, formulating, and producing antifouling paints. |

| Quality Testing & Regulatory Approval | Labs and agencies performing regulatory testing, certification, and compliance checks for marine coatings. |

| Distribution to Drydock | Logistics providers and distributors delivering antifouling paints to drydocks, shipyards, and vessel maintenance sites. |

| Surface Preparation & Coating Application | Shipyards and maintenance service providers preparing hull surfaces and applying antifouling coatings at drydock or in situ. |

| Vessel Operation & Hull Monitoring | Ship operators and service companies monitoring hull performance, coating effectiveness, and maintenance requirements during vessel operation. |

The drydock application stage creates the most commercially time-sensitive point in the antifouling value chain, drydock schedules creating fixed windows where coating application must be completed within the contracted drydock period, creating demand for technically competent coating applicators, readily available paint supply from local distribution warehouse, and pre-agreed technical specification from class society and flag state.

Technology Landscape in the Antifouling Paints and Coatings Industry

Self-Polishing Copolymer Chemistry

Self-polishing copolymer chemistry is shaping the technology landscape in the antifouling paints and coatings industry by enabling coatings that gradually wear away to expose fresh biocides, maintaining long-lasting protection against biofouling. This approach ensures consistent fouling prevention, reduced maintenance frequency, and improved hull efficiency over time. By combining controlled polymer degradation with biocide release, manufacturers can produce high-performance, durable, and environmentally compliant coatings. This technology enhances operational efficiency, fuel savings, and compliance with international maritime regulations, driving innovation and adoption in the market.

Fouling Release Coating Technology

Fouling release coating technology is shaping the antifouling paints and coatings industry by providing non-toxic, low-friction surfaces that prevent marine organisms from adhering to hulls. These coatings reduce drag, improve fuel efficiency, and minimize maintenance needs without relying on traditional biocides. By combining advanced polymers and surface engineering, fouling-release coatings offer long-lasting, environmentally friendly protection suitable for commercial, naval, and offshore vessels. This innovation supports sustainability, regulatory compliance, and operational efficiency, driving adoption of premium antifouling solutions across the maritime sector.

Biocide-Free Hull Coating Technology

Biocide-free hull coating technology offering effective fouling prevention without relying on harmful chemicals, reducing environmental impact on marine ecosystems. These coatings use low-friction, non-stick surfaces or advanced polymers to prevent organism adhesion, enhancing fuel efficiency and reducing maintenance. By eliminating toxic biocides, they help manufacturers and vessel operators comply with stringent environmental regulations while supporting sustainable and eco-friendly shipping practices. In March 2026, Nippon Paint Marine introduced AQUATERRAS 1100, a new low-VOC hull coating designed to minimize environmental impact and meet regulatory standards in key shipbuilding markets such as China and Korea. The coating features HydroPhix, a micro-domain structure combining hydrophilic and hydrophobic elements that effectively prevent marine organisms from adhering to hull surfaces without relying on biocides.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Copper-Based |

41.3% |

2025 |

|

Application |

Shipping Vessels |

38.9% |

2025 |

|

Region |

Asia Pacific |

44.8% |

2025 |

By Type

Copper-based leads at 41.3% (2025). The copper-based segment encompasses traditional ablative copper antifouling, hard copper antifouling, and copper SPC (self-polishing copolymer), collectively serving the commercial fleet's cost-driven antifouling procurement above premium technology alternatives.

To access detailed market analysis, Request Sample

Self-polishing copolymer at 27.6% grows at ~6.8% CAGR through premium fleet specification upgrade and copper-free SPC adoption in environmentally restricted waters. Silicone elastomers at 18.4% grow fastest at ~8.2% CAGR. Others at 12.7% include hard epoxy, ablative non-copper, and experimental antifouling formulations.

By Application

Shipping vessels lead at 38.9% (2025). The shipping vessel segment encompasses bulk carriers, tankers, container ships, general cargo vessels, LNG/LPG carriers, cruise ships, and naval vessels, the fleet's periodic drydock recoating creating the most structurally recurring antifouling demand market.

Drilling rigs and production platforms at 19.8% represent the most commercially premium per-unit antifouling application. Fishing boats at 14.6% create distributed small-vessel antifouling demand through the world's registered fishing vessels. Yachts and other boats at 12.3% encompass the premium leisure marine antifouling market. Mooring lines at 8.1% and inland waterways at 6.3% represent growing specialty antifouling applications.

Regional Market Insights

| Region | Share (2025) | Key Antifouling Paints and Coatings Market Drivers & Characteristics |

|---|---|---|

| Asia Pacific | 44.8% | Driven by a strong shipbuilding industry, high maritime trade activity, and significant demand from commercial and naval fleets. |

| Europe | 21.7% | Driven by a combination of significant commercial fleet ownership, established maritime infrastructure, and regulatory compliance for environmentally safe antifouling solutions. |

| North America | 16.9% | Dominated by the USA, with a multifaceted antifouling paints market driven by commercial shipping, naval fleets, and offshore operations. |

| Latin America | 9.8% | Anchored by Brazil, the region’s most commercially significant hub for shipping and shipbuilding, driving the adoption of antifouling coatings. |

| Middle East & Africa | 6.8% | Represents a commercially heterogeneous market with growing demand from offshore oil, gas, and maritime operations, emphasizing premium and high-performance antifouling solutions. |

Asia Pacific's 44.8% market dominance reflects the region's combined shipbuilding capacity and existing fleet maintenance drydock activity. Europe's 21.7% reflects its dual role as an antifouling technology innovator and a significant fleet owner market. North America's 16.9% reflects the unique combination of one of the largest recreational marine antifouling markets and the most premium naval antifouling specification market.

Latin America's 9.8% is growing at above-market CAGR through Brazil's deepwater platform expansion and Chile's fishing fleet. The Middle East and Africa's 6.8% are growing through offshore platform expansion and field development, creating new offshore antifouling procurement.

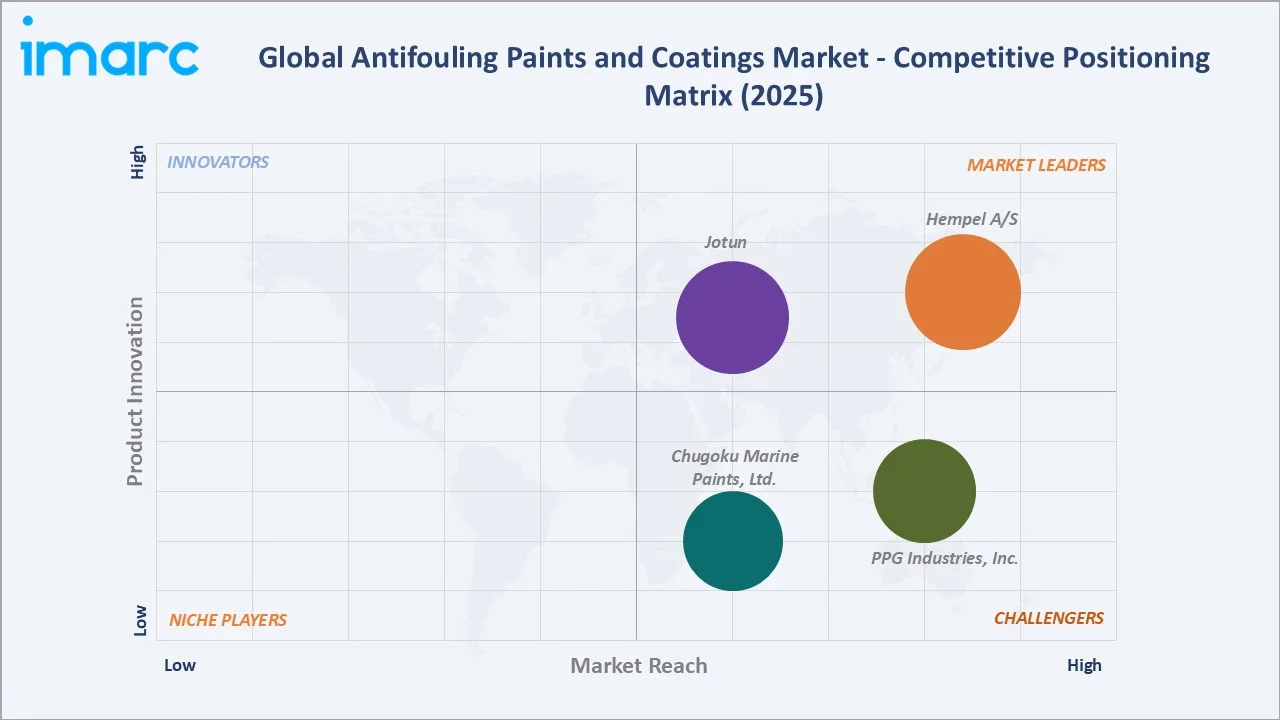

Competitive Landscape

The global antifouling paints and coatings competitive landscape is characterized by a mix of global coatings majors and specialized marine chemical manufacturers competing on performance, sustainability, and regulatory compliance. Key players focus on R&D, eco‑friendly formulations, and strategic partnerships with shipyards and naval fleets to differentiate their offerings. Intense innovation around biocide‑free, fouling‑release, and smart coating technologies enhances competition, while regional producers also cater to localized demand dynamics. This competitive environment drives continuous product improvements and market expansion globally.

| Company Name | Key Brands | Market Position | Core Strength |

|---|---|---|---|

| Hempel A/S | Hempaspeed TF, Hempaguard, Hempasil, Silic One | Market Leader | Hempel A/S is a global leader in marine coatings, playing a pivotal role in developing advanced antifouling and fouling release technologies that improve vessel fuel efficiency and reduce CO2 emissions. |

| Jotun | SeaQuantum, SeaMate, SeaForce | Market Leader | Jotun is a global leader in marine antifouling paints, specializing in silyl-based, self-polishing coatings that prevent fouling organisms on hulls. |

| PPG Industries, Inc. | SIGMAGLIDE, SIGMA SAILADVANCE, PPG Nexeon | Strong Challenger | PPG Industries, Inc., through the SIGMA brand, offers silicone coatings and low-friction, biocidal systems that reduce drag and improve fuel efficiency. |

| Chugoku Marine Paints, Ltd. | SEAFLO NEO, SEA GRANDPRIX | Strong Challenger | Chugoku Marine Paints, Ltd. is a global leader in marine coatings, specifically known for developing high-performance, environmentally conscious antifouling technologies that reduce hull friction, fuel consumption, and CO2 emissions. |

The competitive landscape's most commercially consequential dynamic is the regulatory compliance market, creating above-standard revenue growth for premium antifouling above commodity copper products. The Japanese manufacturer coalition represents the competitive landscape's most commercially significant geographic cooperation between competing manufacturers above the standard competitive-only relationship between antifouling market participants globally.

Key Company Profiles

Hempel A/S

Hempel A/S is a leading global coatings manufacturer, with a strong presence in the marine coatings sector, including antifouling paints and protective solutions. The company is known for a wide range of antifouling and fouling‑release coatings designed to protect commercial, naval, and recreational vessels from biofouling, corrosion, and performance degradation.

- Key Brands: Hempaspeed TF, Hempaguard, Hempasil, Silic One.

- Recent Developments: In February 2026, Hempel completed the inaugural application of its next-generation silicone hull coating, Hempaguard NB, on one of the newbuilding vessels, Tangier Mærsk, the first of a new series of six 9,000 TEU ships ordered by Maersk. This milestone extends the proven performance of Hempaguard directly to vessels straight from the shipyard.

- Strategic Focus: Advancing high‑performance, eco‑friendly marine coating solutions, including next‑generation silicone and fouling‑release technologies, while partnering with major shipowners and shipyards to enhance hull efficiency, regulatory compliance, and sustainability across global fleets.

Jotun

Jotun is a multinational coatings manufacturer, known for its broad range of marine paints and protective coating solutions, including antifouling paints used on commercial ships, naval vessels, and offshore structures. With a global presence spanning shipyards, service centers, and distributors, Jotun delivers products designed to prevent biofouling, enhance hull performance, and protect marine assets against corrosion and wear.

- Key Brands: SeaQuantum, SeaMate, SeaForce.

- Recent Developments: In June 2025, Lloyd's Register (LR) granted Jotun’s SeaQuantum Skate antifouling coating the world’s first recognized enhanced antifouling type approval, along with type approval certification for its HullSkater hull cleaning equipment.

- Strategic Focus: Developing high‑performance, environmentally compliant coating solutions that protect vessels and offshore structures, while enhancing fuel efficiency and reducing maintenance costs.

Market Concentration Analysis

The global antifouling paints and coatings market is moderately concentrated in the premium specialty segment and more competitive in the commercial mainstream segment. Japan's market is the most commercially concentrated nationally. Market concentration is evolving through digital service differentiation. This service differentiation is progressively creating commercial concentration around the technology leaders above the broader antifouling market's manufacturing geography, as Japan and Chinese producers compete primarily on product performance and price above equivalent service ecosystem development.

Investment & Growth Opportunities

Highest Growth Segments

Silicone elastomers fouling release (~8.2% CAGR), drilling rigs and production platforms (~6.4% CAGR), copper-free SPC adoption (~7.5% CAGR from small base), naval vessel antifouling (~6.8% CAGR through global naval expansion), Asia Pacific drydock recoating (~7.0% CAGR through fleet maintenance), and underwater robotic hull cleaning service (~20-25% CAGR from small base) represent the highest-growth antifouling market investment vectors through 2034.

Emerging Investment Opportunities

The mandatory biofouling management regulation investment opportunity, positioning antifouling product and hull inspection service capability ahead of the anticipated mandatory biofouling management regulation, creating first-mover commercial positioning for compliance-service offering above the current voluntary market for hull condition documentation, represents the most commercially leveraged single regulatory event investment opportunity in the antifouling market's near-term horizon.

Investment Themes

- Deepwater offshore platform antifouling specification investment: Each semi-submersible and jack-up rig in the deepwater project pipeline creates an aggregate high offshore antifouling procurement opportunity from the 2025-2030 deepwater project sanction and construction pipeline.

- Copper-free SPC product development and commercialization for EU biocidal products regulation compliance market: The biocidal regulation's progressive restriction of copper antifouling leaching rates in restricted coastal waters and potential future copper active substance review creates a long-term commercial displacement opportunity for copper-free SPC using organic biocides DCOIT and ZnPT as copper replacement.

Future Market Outlook (2026-2034)

The global antifouling paints and coatings market is projected to grow from USD 10.63 Billion in 2025 to USD 18.33 Billion by 2034, delivering a 6.05% CAGR over the forecast period. The market's anchor value of USD 14.26 Billion in 2030 represents the antifouling industry at a structural inflection. The commercial mainstream is progressively shifting from biocidal copper toward eco-friendly SPC and fouling release technology through the combined forces of regulatory pull, EU biocidal products regulation pressure, and technology cost reduction that progressively closes the price gap between premium fouling release and commodity copper antifouling.

Three structural forces define the antifouling market's growth through 2034: global commercial fleet expansion through LNG trade growth, container fleet capacity recovery, and offshore fleet build-out, creating the most commercially certain demand driver above any technology or regulation uncertainty, anticipated mandatory biofouling management creating the most commercially consequential dual-regulatory demand pull in the antifouling market's history, and fouling release technology cost reduction creating commercial viability for medium-segment fleet operators above the current large-container-line and LNG carrier premium segment.

Research Methodology

Primary Research

Primary research comprised structured interviews with global antifouling paints and coatings industry stakeholders, including R&D directors, technical service managers, procurement directors, drydock facility technical managers, marine environment specialists, and fleet operator surveys from commercial vessel operating companies across Asia Pacific, Europe, and North America.

Secondary Research

Secondary research encompassed biofouling management deliberation records, EU biocidal products regulation active substance evaluation dossiers, company annual reports, copper antifouling restriction guidelines, and antifouling management guidance. Over 60 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a vessel fleet segment model: global commercial fleet by vessel type multiplied by average antifouling system cost per vessel type multiplied by annual recoating frequency, creating annual antifouling paint demand. The offshore platform segment is modelled separately through the active platform count multiplied by the average coating system cost. Premium product mix upgrade applied as a revenue multiplier above unit volume growth.

Antifouling Paints and Coatings Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Copper-Based, Self-Polishing Copolymer, Silicone Elastomers, and Others |

| Applications Covered | Shipping Vessels, Drilling Rigs & Production Platforms, Fishing Boats, Yachts & Other Boats, Mooring Lines, Inland Waterways |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Hempel A/S, Jotun, PPG Industries, Inc., Chugoku Marine Paints, Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Antifouling Paints and Coatings Market Report

The global antifouling paints and coatings market reached USD 10.63 Billion in 2025, driven by growing global maritime trade, expansion of shipping fleets, and increasing shipbuilding activities, coupled with rising demand for eco-friendly, high-performance coatings that improve fuel efficiency, reduce maintenance, and comply with environmental regulations.

The global antifouling paints and coatings market grows at 6.05% CAGR during 2026-2034, reaching USD 18.33 Billion by 2034. The overall growth is sustained by global fleet expansion, anticipated mandatory biofouling regulation, deepwater offshore platform investment, and premium antifouling product mix upgrade from copper toward fouling release technology.

Copper-based leads at 41.3% through cost-effectiveness and performance track record for global commercial fleet procurement.

Shipping vessels lead at 38.9% through the global commercial fleet's vessels requiring periodic antifouling recoating every 2.5-7.5 years.

Asia Pacific leads at 44.8% through China, South Korea, and Japan's combined dominance in global shipbuilding, creating the world's most concentrated antifouling paint application from newbuild construction alone, supplemented by Asia Pacific's largest vessel fleet maintenance drydock activity.

Leading companies include Hempel A/S, Jotun, PPG Industries, Inc., and Chugoku Marine Paints, Ltd., among others.

The global antifouling paints and coatings market is projected to reach approximately USD 14.26 Billion by 2030, with silicone fouling release reaching 25-28% of premium fleet specification and Asia Pacific domestic Chinese antifouling manufacturers achieving international quality standards, creating competitive pressure on European premium brand pricing above the current premium brand protection through technical performance gap.

Three priority investment opportunities: fouling release premium antifouling manufacturing scale-up for fleet upgrade market, deepwater offshore platform antifouling specification for the semi-submersible newbuild pipeline, and copper-free SPC product development for EU biocidal products regulation compliance.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)