Asia Pacific Paper Packaging Market Size, Share, Trends and Forecast by Product Type, Grade, Packaging Level, End Use Industry, and Country, 2026-2034

Asia Pacific Paper Packaging Market Summary:

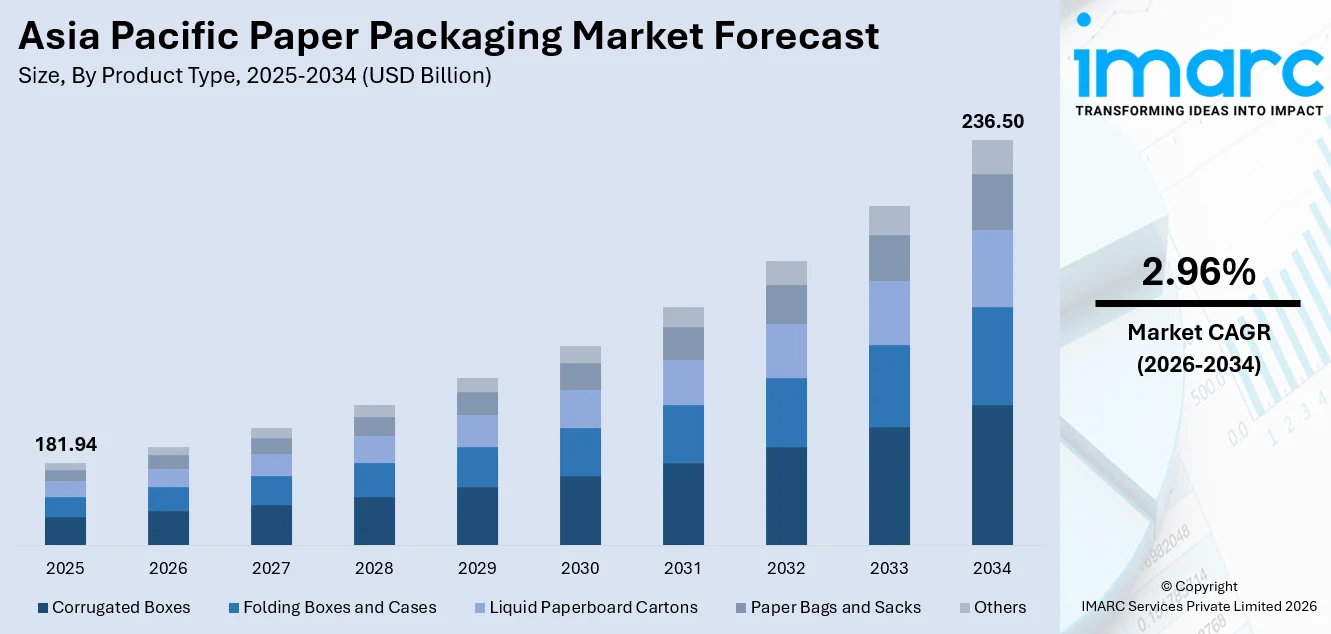

The Asia Pacific paper packaging market size was valued at USD 181.94 Billion in 2025 and is projected to reach USD 236.50 Billion by 2034, growing at a compound annual growth rate of 2.96% from 2026-2034.

The Asia Pacific paper packaging market is experiencing significant growth due to the increasing number of e-commerce transactions, growing consumer interest in eco-friendly alternatives to plastic, and the expanding food and beverage industry. Government regulations, urbanization, and consumer awareness regarding environmental responsibility are changing the dynamics of packaging choices. The Asia Pacific paper packaging market is also benefiting from large-scale production facilities and the adoption of eco-friendly packaging solutions in various industries.

Key Takeaways and Insights:

- By Product Type: Corrugated boxes dominate the market with a share of 40% in 2025, driven by widespread adoption in e-commerce logistics, food distribution, and retail supply chains across the region.

- By Grade: Solid bleached leads the market with a share of 28% in 2025, owing to its superior printability, hygiene standards, and suitability for premium food, personal care, and pharmaceutical packaging applications.

- By Packaging Level: Primary packaging holds the largest share of 45% in 2025, reflecting the critical role paper-based materials play in directly enclosing and protecting food, beverage, and consumer products at the point of sale.

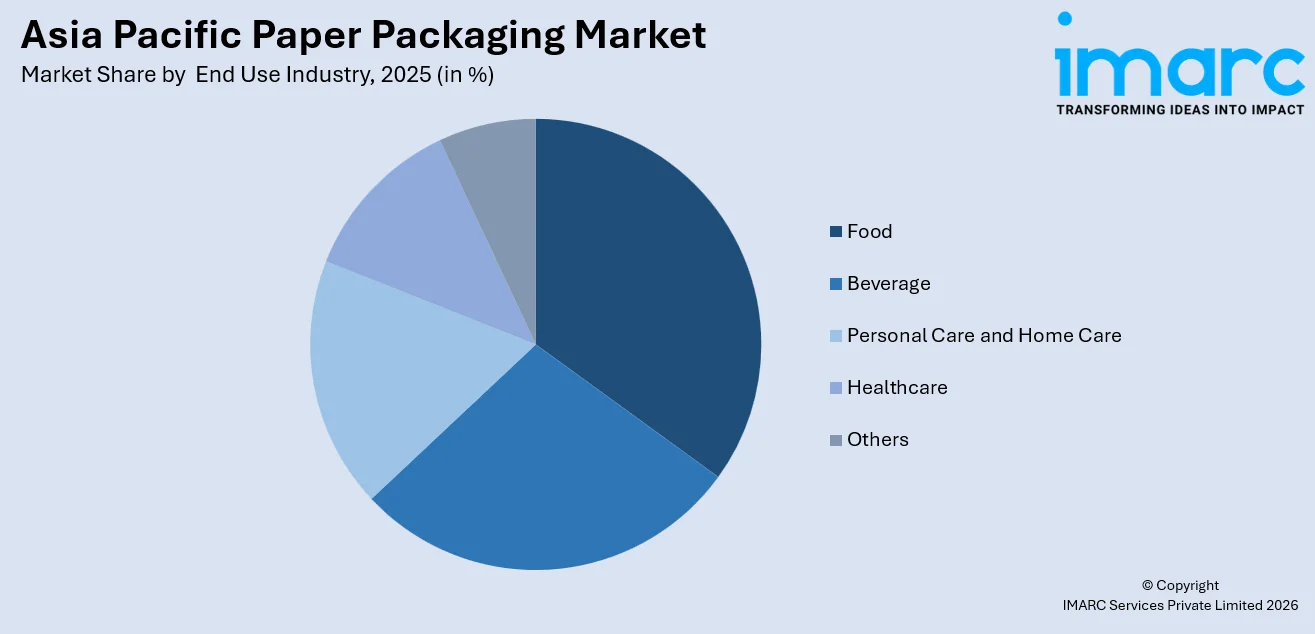

- By End Use Industry: Food dominates the market with a share of 33% in 2025, supported by growing demand for safe, hygienic, and sustainable packaging solutions across fresh, processed, and packaged food categories.

- Key Players: The Asia Pacific paper packaging market is moderately consolidated, with leading integrated producers and regional converters competing on sustainability credentials, product quality, pricing flexibility, and supply chain efficiency across diverse industry verticals.

To get more information on this market Request Sample

The Asia Pacific paper packaging market is expanding at a steady pace, underpinned by the region's large and growing consumer base, evolving retail landscape, and deepening commitment to environmental sustainability. In December 2025, Asia Pulp & Paper expanded its carton packaging operations in Java and Sumatra to strengthen eco‑friendly packaging solutions. Rising per-capita incomes and urbanization are fueling demand for packaged goods, which in turn is elevating consumption of paper-based primary, secondary, and tertiary packaging formats. The transition from plastic to paper continues to gain momentum as governments across the region implement progressive legislation and brands align their packaging strategies with circular economy objectives. Increasing investments in modern paper manufacturing capacity, technological advancements in fiber processing, and improvements in barrier coating science are collectively enhancing the performance and versatility of paper packaging, strengthening its position across high-growth application segments.

Asia Pacific Paper Packaging Market Trends:

Surge in E-Commerce and Digital Retail

The rapid proliferation of online shopping platforms across Asia Pacific is fundamentally transforming packaging demand patterns. In October 2025, Smurfit Westrock launched a dedicated clinical packaging facility and introduced its Bag‑in‑Box® Powergrip solution, an innovation aimed at meeting rising e‑commerce and medical logistics packaging needs across Asia Pacific markets. Consumers are increasingly turning to digital channels for groceries, electronics, and personal care products, generating sustained demand for durable, lightweight, and protective paper-based packaging formats tailored to last-mile delivery requirements. This structural shift toward omnichannel retail is reinforcing corrugated box adoption and elevating the strategic importance of packaging performance, contributing to Asia Pacific paper packaging market growth.

Regulatory Momentum Toward Sustainable Packaging

Governments and regulatory bodies across Asia Pacific are implementing progressively stricter frameworks to reduce single-use plastic consumption. For example, Vietnam’s National Assembly approved Resolution 247/2025/QH15 in December 2025 to strengthen environmental laws, including tighter Extended Producer Responsibility regulations for the collection and recycling of packaging waste and policies to encourage biodegradable packaging adoption. Extended Producer Responsibility schemes, mandatory recycled-content thresholds, and targeted bans on specific plastic formats are compelling brand owners and converters to accelerate adoption of recyclable, biodegradable paper-based alternatives. These policy measures are reshaping material selection across food, retail, and logistics sectors, creating a durable structural demand shift in favor of paper packaging solutions throughout the region.

Technological Advancements in Barrier Coatings

Ongoing development and commercial adoption of advanced bio-based barrier coatings, including nano-cellulose formulations and plant-derived polymer technologies, are substantially expanding the functional performance envelope of paper packaging. For example, Smart Planet Technologies commercially launched a new bio‑recyclable barrier coating for paper cups in January 2025 that uses a PLA‑based biopolymer formulation to offer compostability and recyclability while maintaining moisture and grease resistance. These innovations are enabling paper substrates to effectively replace plastic in moisture-sensitive and grease-contact applications, broadening their suitability for fresh food, dairy, and ready-to-eat product packaging. Continuous improvements in coating science are enhancing paper's competitive positioning against incumbent plastic formats across high-growth food and consumer goods segments.

Market Outlook 2026-2034:

The Asia Pacific paper packaging market is set to continue its growth trajectory over the forecast period, driven by the underlying macroeconomic trends of e-commerce penetration, plastic substitution, and food processing. Increased investments in integrated packaging mills and advanced converting machinery will further improve the capabilities of the supply chain in the region. The food and beverage industry will continue to be the mainstay of the market, while new segments such as personal care and healthcare emerge. The market generated a revenue of USD 181.94 Billion in 2025 and is projected to reach a revenue of USD 236.50 Billion by 2034, growing at a compound annual growth rate of 2.96% from 2026-2034.

Asia Pacific Paper Packaging Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Corrugated Boxes |

40% |

|

Grade |

Solid Bleached |

28% |

|

Packaging Level |

Primary Packaging |

45% |

|

End Use Industry |

Food |

33% |

Product Type Insights:

- Corrugated Boxes

- Folding Boxes and Cases

- Liquid Paperboard Cartons

- Paper Bags and Sacks

- Others

The corrugated boxes dominate with a market share of 40% of the total Asia Pacific paper packaging market in 2025.

Corrugated boxes represent the most widely adopted paper packaging format across Asia Pacific, serving as the default solution for e-commerce fulfillment, fast-moving consumer goods distribution, and food supply chain logistics. According to industry data, the global corrugated boxes market was valued at USD 212.3 billion in 2025 and is projected to grow further in the coming decade. Their inherent strength, recyclability, and compatibility with automated packaging lines make them indispensable across retail and logistics operations. The format's adaptability to custom dimensions, high-quality surface printing, and brand-specific structural designs has further elevated demand as companies increasingly treat packaging as a front-line brand communication and consumer experience tool.

Growing adoption of shelf-ready packaging formats within modern trade channels is reinforcing corrugated box demand among organized retailers and multinational consumer goods brands operating across the region's diverse and rapidly evolving markets. The high recyclability of corrugated board and strong fiber recovery rates in key markets further align this format with the region's intensifying sustainability agenda, supporting both regulatory compliance requirements and corporate environmental commitments across food, retail, electronics, and personal care sectors.

Grade Insights:

- Solid Bleached

- Coated Recycled

- Uncoated Recycled

- Others

The solid bleached leads with a share of 28% of the total Asia Pacific paper packaging market in 2025.

Solid bleached board is the preferred grade for applications requiring the highest levels of print quality, surface whiteness, and food safety compliance. Its superior brightness and smoothness make it the substrate of choice for premium consumer packaging across food, personal care, pharmaceuticals, and luxury retail categories. As brand owners across Asia Pacific place growing emphasis on packaging aesthetics as a primary purchase influence mechanism, demand for solid bleached substrates continues to strengthen in both established and emerging consumer markets throughout the region.

Converters also benefit from solid bleached board's compatibility with modern high-speed printing technologies, enabling vibrant, detailed graphics and complex structural packaging designs that meet premium consumer expectations. Growing regulatory emphasis on food-safe, non-toxic packaging materials is additionally reinforcing the grade's position as a preferred choice among food manufacturers and retailers seeking compliant, high-performance solutions. Investment in premium product lines across food, cosmetics, and pharmaceutical sectors is expected to sustain solid bleached board demand across the forecast period.

Packaging Level Insights:

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

The primary packaging dominates with a market share of 45% of the total Asia Pacific paper packaging market in 2025.

Primary packaging represents the most challenging interface between the product and the end-use consumer, demanding exceptional material properties in terms of barrier properties, safety, and visual presentation. Paper-based primary packaging types, such as folding cartons, liquid paperboard cartons, and treated paper wraps, are rapidly replacing plastic packaging alternatives in the food, personal care, and pharmaceutical sectors in the Asia Pacific region. The growing demand for more transparent, informative, and visually appealing packaging is fueling innovation at the primary packaging level.

The region's rapidly expanding food processing industry and strengthening consumer preference for sustainably packaged products are further accelerating paper's penetration into primary packaging applications. Improvements in bio-based barrier coating technologies are enhancing paper's ability to meet the moisture, oxygen, and grease resistance requirements of sensitive food and beverage products. These functional advances, combined with regulatory pressure to reduce plastic in direct food contact applications, are expected to sustain robust growth in primary paper packaging adoption throughout the forecast period.

End Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Food

- Beverage

- Personal Care and Home Care

- Healthcare

- Others

The food leads with a share of 33% of the total Asia Pacific paper packaging market in 2025.

The food industry is the most prominent end-use market for paper packaging in the Asia Pacific region, and it is driven by the crucial function of packaging in ensuring the region’s massive food production and distribution chain. Paper packaging formats are used in a wide range of food applications, including fresh produce, bakery products, processed foods, frozen foods, and quick service restaurant packaging. The rising urbanization trend, development of modern retail formats, and the growing popularity of food delivery services are driving the demand for food-grade paper packaging.

Rising consumer awareness around packaging sustainability and progressively stricter regulatory restrictions on plastic use in food-contact applications are encouraging food manufacturers and retailers to accelerate their transition toward paper-based solutions. This demand momentum is further reinforced by growing investments in food processing capacity across the region and continuous innovation in paper packaging formats designed to meet the specific protection, shelf life, and presentation requirements of diverse food product categories throughout Asia Pacific's evolving food supply chain.

Country Insights:

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

China dominates the Asia Pacific paper packaging landscape, supported by the world's largest e-commerce ecosystem, an expansive food processing industry, and government-led initiatives promoting sustainable packaging adoption. The country's extensive integrated paper mill infrastructure enables competitive production economics and efficient supply across diverse packaging applications. Rapid urbanization and rising consumer spending on packaged goods continue to reinforce China's position as the region's largest and most influential paper packaging market.

Japan's paper packaging market is distinguished by exceptionally high standards of quality, precision, and packaging innovation. The country maintains a well-established tradition of premium packaging design, supported by advanced manufacturing capabilities and deeply embedded corporate sustainability commitments. Growing adoption of recyclable board grades, investment in barrier coating technologies, and the transition away from single-use plastics within organized retail and food service sectors are collectively sustaining steady market development across the forecast period.

India represents one of the most dynamic growth opportunities within the Asia Pacific paper packaging market, driven by rapid urbanization, a large and aspirational consumer base, and progressive government policies restricting single-use plastics. The country's fast-expanding food processing, e-commerce, and consumer goods industries are generating sustained demand for corrugated and paperboard packaging. Rising domestic paper manufacturing investments are progressively improving supply chain depth, cost competitiveness, and product quality standards across the Indian market.

South Korea's paper packaging market is shaped by a sophisticated retail environment, strong environmental regulatory frameworks, and high consumer receptiveness to sustainable packaging solutions. Government mandates requiring recyclable packaging and a well-developed e-commerce sector are driving consistent adoption of corrugated and paperboard formats across food, electronics, and consumer goods categories. Leading domestic brands and multinational corporations operating in South Korea are increasingly integrating paper-based packaging into their broader sustainability and circular economy commitments.

Australia's paper packaging market is guided by national sustainability policy priorities, including phased elimination of single-use plastics and voluntary industry targets for recyclable and compostable packaging adoption. The country's well-organized food service, modern retail, and growing e-commerce sectors are sustaining reliable demand for paper-based packaging formats. Australian brand owners and retailers are increasingly prioritizing certified sustainable paper packaging to meet rising consumer environmental expectations and align with evolving national and state-level regulatory requirements.

Indonesia is emerging as an important growth market for paper packaging, supported by a large and rapidly urbanizing population, expanding food and consumer goods manufacturing industries, and increasing government focus on reducing plastic waste. Investment in new domestic paper and packaging manufacturing capacity is improving local supply availability and cost competitiveness. Rising organized retail penetration and growing e-commerce adoption across the archipelago are creating new and sustained demand opportunities for corrugated and paperboard packaging formats.

Other Asia Pacific markets, including Vietnam, Thailand, Malaysia, and the Philippines, are gaining momentum as significant growth contributors to the regional paper packaging market. Rising consumer incomes, expanding organized retail infrastructure, growing food processing industries, and progressively stricter regulatory environments are collectively driving the transition from plastic toward paper-based packaging. These markets represent attractive opportunities for packaging producers and converters seeking to establish early positions in high-growth, underserved regional markets throughout the forecast period.

Market Dynamics:

Growth Drivers:

Why is the Asia Pacific Paper Packaging Market Growing?

Rapid Urbanization and Rising Middle-Class Consumption

The Asia Pacific region is experiencing one of the most significant urban transformations in history, with large populations migrating from rural areas to cities and entering the formal consumer economy. Between 2013 and 2023, Asia Pacific flipped from having a majority rural population to a majority urban one, a shift that has supported the proliferation of modern retail formats such as convenience stores and supermarkets and boosted overall consumer spending. This transition is driving a substantial rise in demand for packaged goods across food, personal care, healthcare, and household product categories. Urbanization increases reliance on pre-packaged and processed food, amplifying the need for primary and secondary paper packaging formats. Simultaneously, rising disposable incomes within the expanding middle class are enabling greater spending on branded, premium-packaged products that rely on high-quality paperboard substrates for visual appeal and structural protection. The continued growth of modern retail formats, organized trade channels, and supermarkets across the region is further amplifying demand for shelf-ready, attractive paper packaging solutions. These combined demographic and economic trends position the Asia Pacific paper packaging market for sustained expansion.

Stringent Regulatory Framework Targeting Single-Use Plastics

Governments across Asia Pacific are implementing an increasingly rigorous regulatory agenda to curb plastic pollution and promote sustainable packaging alternatives. For example, Vietnam has committed to banning the production and import of non‑biodegradable plastic bags for domestic use from January 1, 2026, and supermarkets and shopping centres will no longer be allowed to provide such plastic bags, as part of broader plastic restriction orders that also include producer responsibility fees on packaging volumes placed on the market. Policies including outright bans on single-use plastic bags, mandatory recycled-content requirements, and Extended Producer Responsibility frameworks are compelling brand owners, retailers, and packaging manufacturers to transition toward paper-based solutions at scale. These regulations create a structural and enduring shift in material preference, benefiting paper packaging across primary, secondary, and tertiary applications. Countries with early mover regulatory environments are driving innovation in recyclable and biodegradable paper packaging formats, which are subsequently adopted across emerging markets as regulatory ambition intensifies.

Growing Food Industry and Online Food Delivery Ecosystem

The Asia Pacific food industry is one of the most dynamic in the world, characterized by a vast and diverse consumption base, rapidly evolving dietary preferences, and a booming food delivery and food service infrastructure. Yum China’s KFC and Pizza Hut are phasing out single‑use plastics, replacing them with recyclable or biodegradable alternatives. By the end of 2025, all KFC restaurants in mainland China aim to cut non‑degradable plastics by 30 %. The proliferation of quick-service restaurants, meal kit delivery services, and online grocery platforms is generating substantial and growing demand for hygienic, functional, and sustainable paper packaging. Paper-based formats, including treated kraft papers, liquid cartons, food service trays, and corrugated delivery boxes, are essential to ensuring product safety, presentation, and integrity across the complex food supply chain. Additionally, growing consumer preference for clean-label, responsibly sourced products is encouraging food manufacturers to adopt paper packaging as part of broader environmental commitments. The sustained expansion of food processing capacity and the evolution of modern food retail infrastructure across the region are reinforcing this robust demand trajectory.

Market Restraints:

What Challenges the Asia Pacific Paper Packaging Market is Facing?

Volatility in Raw Material and Pulp Prices

The paper packaging industry is highly exposed to fluctuations in the cost of wood pulp, recovered fiber, and energy, which collectively represent a significant proportion of total production costs. When raw material prices escalate due to supply disruptions, climate-related forestry challenges, or shifts in global trade flows, producers and converters face margin compression and difficulty maintaining competitive pricing, particularly in cost-sensitive markets where alternatives remain readily available. This volatility complicates long-term planning, investment decisions, and contract management for packaging manufacturers across the region.

Underdeveloped Waste Management and Recycling Infrastructure

While paper is inherently recyclable, its recovery value depends on the existence of efficient collection, sorting, and processing infrastructure. In many developing markets across Asia Pacific, waste management systems remain fragmented and under-resourced, reducing effective recycling rates and increasing the environmental footprint of paper packaging. This gap not only limits the circular economy benefits that justify paper's use over plastic, but also constrains access to recovered fiber inputs that support cost-efficient production of recycled-content board grades.

Intensifying Competition from Alternative Packaging Materials

Paper packaging faces persistent competitive pressure from flexible plastic films, multilayer laminates, and aluminum-based formats that offer superior barrier performance, lighter weight, and lower per-unit material costs in many applications. In price-sensitive consumer segments and for products requiring extended shelf life or moisture-intensive environments, alternative materials continue to maintain a functional and economic advantage over standard paper-based solutions, limiting paper's penetration in certain product categories and regions.

Competitive Landscape:

The Asia Pacific paper packaging market is characterized by a combination of integrated large-scale producers and specialized regional converters, competing across diverse product segments, grades, and geographic markets. Leading manufacturers leverage vertically integrated operations spanning plantation forests, pulp production, board manufacturing, and downstream converting, enabling superior cost management and product consistency. Investment in advanced production technologies, including high-speed converting lines, digital printing capabilities, and sophisticated barrier coating systems, is enabling players to differentiate on quality, customization, and sustainability credentials. Strategic focus areas include expanding geographic reach into high-growth emerging markets, developing next-generation recyclable and compostable packaging formats, and deepening partnerships with major food and beverage, personal care, and e-commerce companies. Competitive dynamics are further shaped by the growing importance of certified sustainable forest management, recycled-content transparency, and regulatory compliance as key purchasing criteria for brand owner customers across the region.

Recent Developments:

- In February 2026, Tetra Pak has launched advanced paper‑based barrier packaging for its high‑speed Tetra Pak® A3/Speed filling lines in Asia, enabling cartons with up to 87 % renewable content and a lower carbon footprint for products like soy milk. This marks a major step in scaling sustainable carton solutions across industrial production.

Asia Pacific Paper Packaging Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Corrugated Boxes, Folding Boxes and Cases, Liquid Paperboard Cartons, Paper Bags and Sacks, Others |

| Grades Covered | Solid Bleached, Coated Recycled, Uncoated Recycled, Others |

| Packaging Levels Covered | Primary Packaging, Secondary Packaging, Tertiary Packaging |

| End Use Industries Covered | Food, Beverage, Personal Care and Home Care, Healthcare, Others |

| Countries Covered | China, Japan, India, South Korea, Australia, Indonesia, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Asia Pacific Paper Packaging Market Report

The Asia Pacific paper packaging market size was valued at USD 181.94 Billion in 2025.

The Asia Pacific paper packaging market is expected to grow at a compound annual growth rate of 2.96% from 2026-2034 to reach USD 236.50 Billion by 2034.

Corrugated boxes held the largest share at 40%, driven by widespread use in e-commerce logistics, food distribution, and retail supply chains across the region's diverse and rapidly growing consumer markets.

Key factors driving the Asia Pacific paper packaging market include rapid urbanization, rising middle-class consumption, expanding food and beverage industries, government mandates on sustainable packaging, growing e-commerce activity, and increasing corporate sustainability commitments across the region.

Major challenges include raw material price volatility, underdeveloped recycling infrastructure in emerging markets, competition from flexible plastic packaging, and the need for significant investment in advanced converting and barrier coating technologies to expand paper's functional range.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)