Brazil E-commerce Market Size, Share, Trends and Forecast by Type and Region, 2026-2034

Brazil E-commerce Market Size, Share, Trends & Forecast (2026-2034)

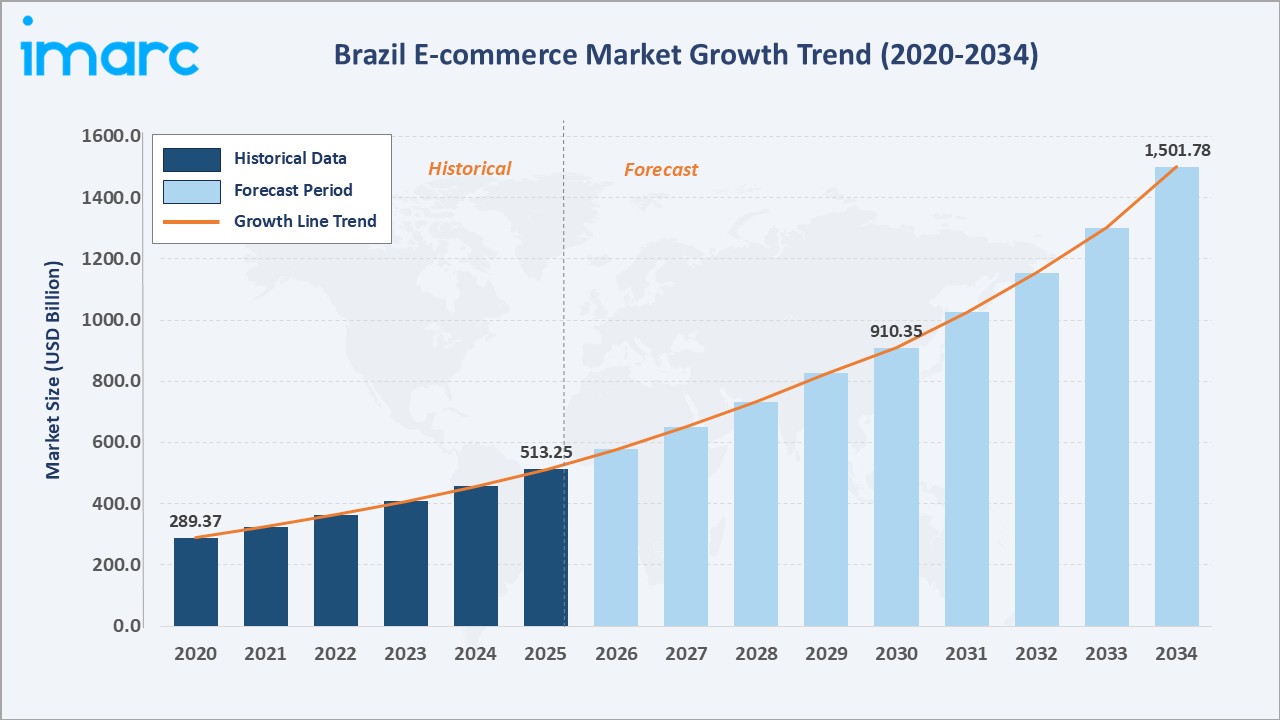

The Brazil e-commerce market reached USD 513.25 Billion in 2025 and is projected to reach USD 1,501.78 Billion by 2034, growing at a CAGR of 12.14% during 2026-2034. Increasing internet penetration, a rising middle-class population, rapid advancements in digital payment systems, and the widespread adoption of mobile commerce are key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 513.25 Billion |

|

Forecast Market Size (2034) |

USD 1,501.78 Billion |

|

CAGR (2026-2034) |

12.14% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Southeast (52.6% share, 2025) |

|

Dominant Type Segment |

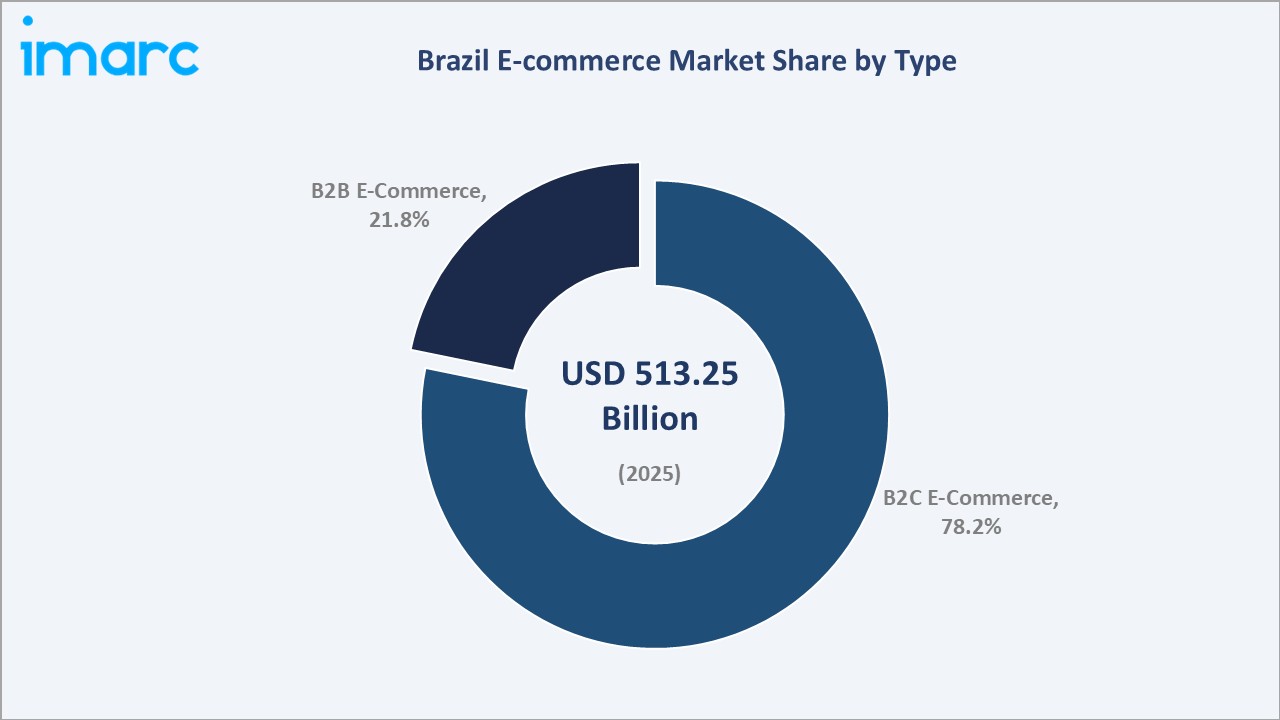

B2C E-commerce (78.2%, 2025) |

To get more information on this market, Request Sample

The revolutionary launch of Pix, Brazil's instant payment system, has dramatically reduced transaction friction, with Pix payments representing nearly 30% of e-commerce transactions by 2024. Government initiatives supporting digital infrastructure, the expansion of online marketplaces, and improvements in last-mile delivery logistics are further strengthening the market's growth foundations.

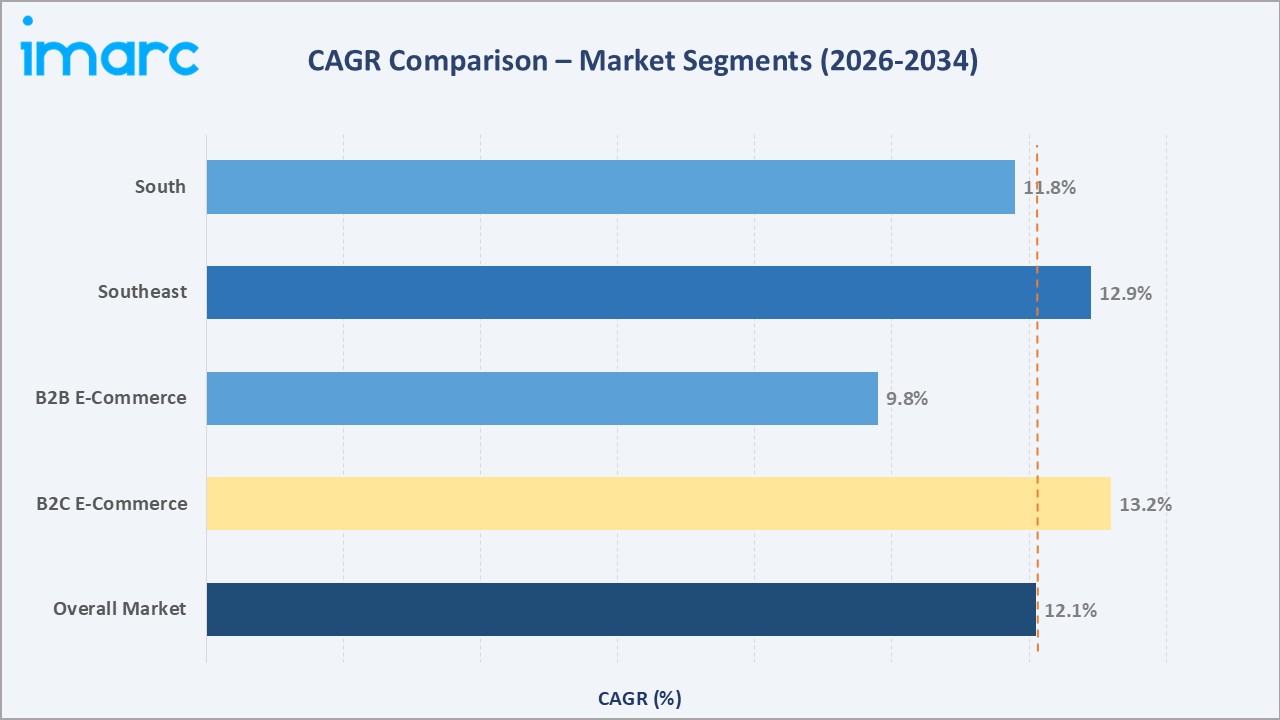

The Southeast region leads with a 52.6% share in 2025, while B2C e-commerce dominates the type segment at 78.2%. Key players include Amazon.com Inc., MercadoLibre, Inc., Shopee, Magazine Luiza, MadeiraMadeira Comércio Eletrônico S/A, and Apple Inc.

Executive Summary

The Brazil e-commerce market is on a transformative growth trajectory, powered by a convergence of digital payment innovation, smartphone proliferation, logistics modernization, and rising consumer purchasing power. The market reached USD 513.25 Billion in 2025 and is forecast to exceed USD 1,501.78 Billion by 2034, reflecting an impressive CAGR of 12.14%. Brazil represents Latin America's largest and most dynamic e-commerce market, commanding over 60% of sales volume, and is increasingly recognized as a global benchmark for digital payment ecosystem innovation.

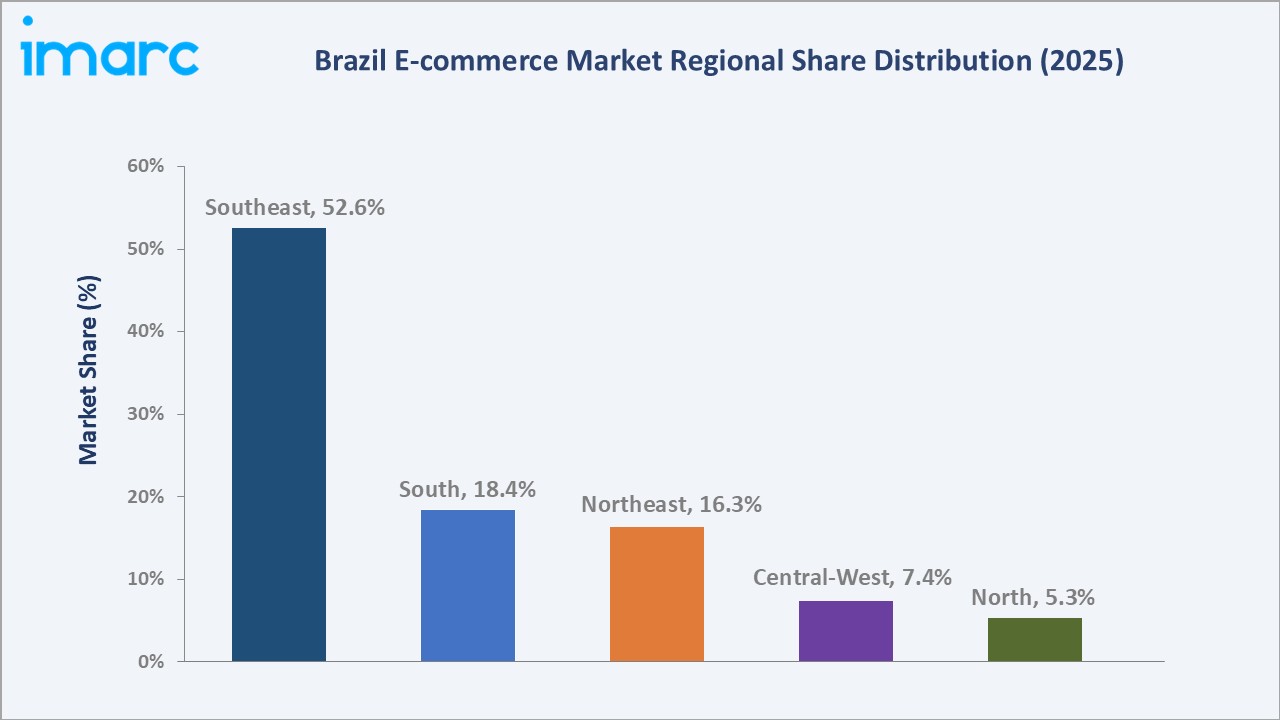

The Southeast region dominates with a 52.6% market share (2025), anchored by São Paulo and Rio de Janeiro, Brazil's two largest urban consumer markets, each characterized by high smartphone penetration, dense logistics networks, and high-income consumer concentrations. The South (18.4%), Northeast (16.3%), Central-West (7.4%), and North (5.3%) regions are all growing, supported by expanding internet infrastructure and government connectivity programs targeting underserved communities.

B2C e-commerce commands 78.2% of the market (2025), driven by the mass consumer adoption of online retail across fashion, electronics, home goods, and food delivery categories. B2B e-commerce (21.8%) is a fast-growing segment, propelled by business procurement digitization and marketplace-driven wholesale commerce. Key players, Amazon.com Inc., MercadoLibre, Inc., Shopee, and Magazine Luiza, continue to compete intensively on logistics speed, payment flexibility, and seller ecosystem expansion.

Key Market Insights

|

Insight |

Data |

|

Dominant Type Segment |

B2C E-Commerce – 78.2% share (2025) |

|

Fastest Growing Type |

B2B E-Commerce (accelerating digitization of business procurement) |

|

Leading Region |

Southeast – 52.6% revenue share (2025) |

|

Fastest Growing Region |

Northeast (rising internet penetration and mobile commerce adoption) |

|

Top Companies |

Amazon.com Inc., MercadoLibre, Inc., Shopee, Magazine Luiza, MadeiraMadeira Comércio Eletrônico S/A, Apple Inc. |

|

Key Market Opportunity |

Social commerce and live shopping projected at USD 85+ Billion by 2034 |

Key Analytical Observations Supporting the Above Data:

- B2C e-commerce accounts for 78.2% of Brazil's e-commerce market in 2025, driven by expanding product categories from electronics and fashion to grocery delivery, underpinned by Pix instant payment adoption and same-day delivery infrastructure in major metropolitan areas.

- B2B e-commerce holds 21.8% of the market, representing one of the fastest-growing segments as Brazilian SMEs and enterprises rapidly digitize procurement, inventory management, and supplier relationship management through B2B marketplace platforms.

- The Southeast region generates 52.6% of national e-commerce revenues (2025), reflecting São Paulo's role as Brazil's commercial capital and Latin America's largest consumer market.

- Pix, launched by Brazil's Central Bank in 2020, processed nearly 30% of all e-commerce transactions by 2024, representing the world's most successful government-led instant payment system and a structural competitive advantage for Brazil's e-commerce ecosystem globally.

- Brazil had 187.9 million Internet users at the start of 2024 (86.6% penetration), with 210.3 million active mobile connections and a 41.2% improvement in median mobile Internet speeds year-over-year, creating a powerful tailwind for mobile-first commerce growth.

Brazil E-commerce Market Overview

Brazil's e-commerce market constitutes the largest and most sophisticated online retail ecosystem in Latin America, encompassing B2C retail marketplaces, B2B digital procurement platforms, digital financial services, food delivery, online travel, and digital content and media commerce. The market has undergone a structural transformation since 2020, accelerated by COVID-19's forced digitization of consumer purchasing habits and permanently elevated by Brazil's Central Bank-led payment infrastructure modernization.

The Brazilian e-commerce ecosystem is uniquely defined by its payment innovation leadership. The Pix instant payment system, free, 24/7, and requiring only a CPF number or mobile phone number, has democratized digital commerce by enabling financial inclusion among previously unbanked populations. Combined with Brazil's deeply social digital culture (2nd largest WhatsApp market globally), e-commerce in Brazil has evolved into a social commerce-native ecosystem, with WhatsApp Business serving as a primary sales channel for millions of Brazilian micro-entrepreneurs.

The market ecosystem spans technology infrastructure providers (cloud, CDN, cybersecurity), marketplace platforms, payment gateway operators, logistics and fulfilment networks, and sellers ranging from global multinationals to individual CPF-registered microentrepreneurs. Brazil's continental geography creates unique logistics challenges, with the Norte and Centro-Oeste regions requiring innovative last-mile delivery solutions to capture their full market potential through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

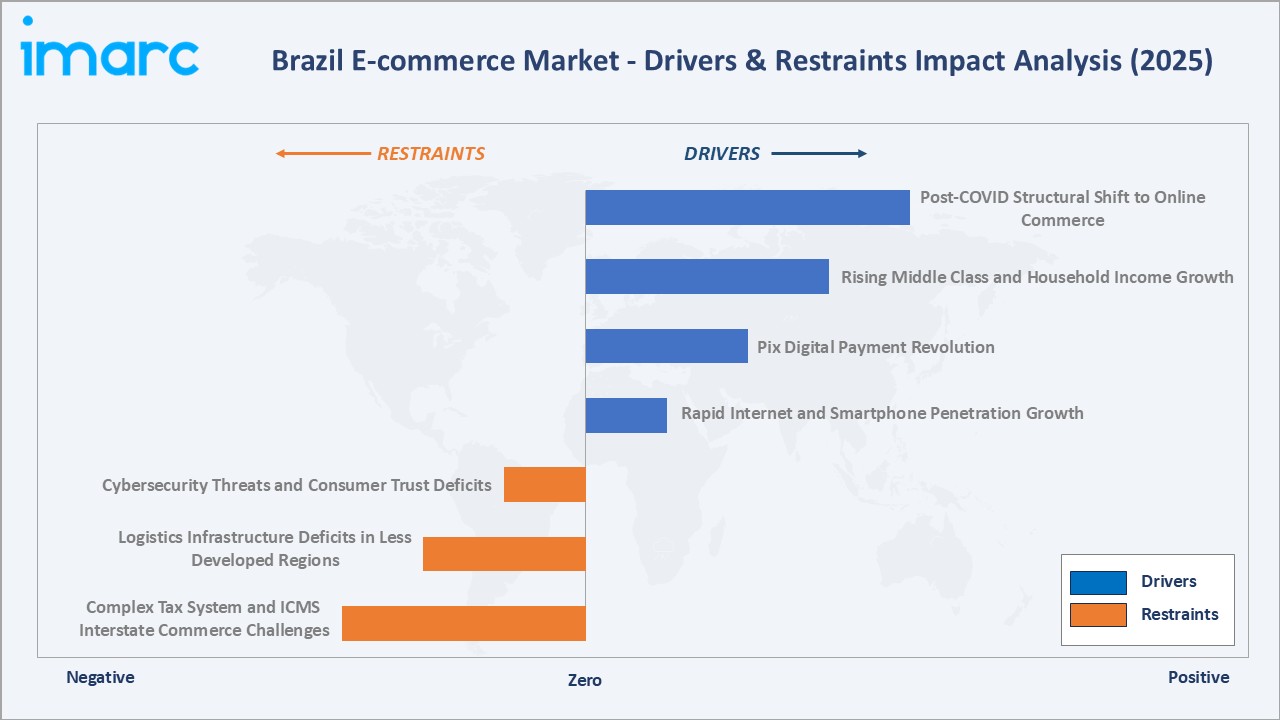

Market Drivers

- Rapid Internet and Smartphone Penetration Growth: Brazil's Internet user base of 187.9 million (86.6% penetration, 2024) and 210.3 million mobile connections (96.6% of population) create an exceptionally large and still-growing addressable market for e-commerce.

- Pix Digital Payment Revolution: Brazil's Pix instant payment system, processing over BRL 17.2 trillion in 2023 transactions, has become the world's most successful government-led digital payment initiative, with nearly 30% of e-commerce transactions processed via Pix by 2024.

- Rising Middle Class and Household Income Growth: Tendências forecasts that the proportion of Brazilians in Class C and above, currently accounting for 50.1% of households in 2024, could rise to 54.8% by 2034. This is increasing household discretionary spending on e-commerce categories, including electronics, fashion, beauty, and home goods.

- Post-COVID Structural Shift to Online Commerce: In 2020, 91% of Brazilians made at least one online purchase, as consumers who adopted e-commerce during lockdowns maintained their online shopping habits.

These drivers create a reinforcing growth cycle, payment innovation reduces friction, expanding the addressable consumer base; infrastructure investment improves delivery quality, increasing repeat purchase rates; and rising incomes expand transaction values and category breadth, collectively compounding market growth velocity.

Market Restraints

- Complex Tax System and ICMS Interstate Commerce Challenges: Brazil's highly complex tax system, with multiple state-level ICMS (Imposto sobre Circulação de Mercadorias e Serviços) rates creating differential tax burdens for cross-border interstate e-commerce, imposes significant compliance costs on marketplace operators and cross-state sellers, artificially constraining national market integration.

- Logistics Infrastructure Deficits in Less Developed Regions: Brazil's continental scale creates acute last-mile delivery challenges in the Norte, Nordeste, and Centro-Oeste regions, where road infrastructure limitations, sparse population density, and limited logistics hub coverage result in delivery times of 7–21 days compared to 1–3 days in Southeast metropolitan areas, constraining e-commerce adoption in high-potential regional markets.

- Cybersecurity Threats and Consumer Trust Deficits: Losses from scams on Brazil’s instant payment system surged by 43% in 2024, totaling around BRL 2.7 billion (approximately USD 510 million) over two years, according to the country’s banking federation, Febraban.

Market Opportunities

- Social Commerce and WhatsApp Business Expansion: Brazil is one of the world's leading social commerce markets, with around 70% of Brazilian companies utilizing WhatsApp as part of their marketing and sales strategies. The formalization of WhatsApp Pay integration with Pix is creating a seamless social-commerce-to-payment pipeline that could unlock USD 30–50 billion in additional commerce volume annually by 2030.

- Cross-Border E-Commerce and Import Simplification: Brazil's regulatory framework changes for cross-border e-commerce, including the Remessa Conforme program establishing clearer import tax obligations, are formalizing and expanding the cross-border online retail channel.

- Regional Market Expansion in Northeast and North: The Northeast region's 16.3% share (2025) represents significant untapped potential, with approximately 58 million consumers and growing digital payment adoption driven by Pix.

Market Challenges

- Economic Volatility and Currency Risk: Brazil's BRL/USD exchange rate volatility, with periods of 25–40% annual depreciation, creates pricing instability for cross-border e-commerce, complicates international marketplace expansion strategies, and reduces the real-value growth rates reported in USD-denominated market assessments.

- Regulatory Complexity and E-commerce Taxation Reform: Ongoing Brazilian tax reform (PEC 45/2019 implementation) is creating transitional regulatory uncertainty for e-commerce businesses, particularly regarding the treatment of digital services, marketplace seller liability for tax collection, and the treatment of platform-mediated transactions under the new dual VAT (CBS/IBS) framework.

Emerging Market Trends

1. Increasing Internet and Smartphone Usage Driving Mobile-First Commerce

Brazil's mobile-first internet adoption is reshaping e-commerce architecture, with over 70% of e-commerce sessions originating from mobile devices in 2024. Marketplace apps, including Mercado Livre, Shopee, and Magazine Luíza's app, dominate consumer engagement, with app-based purchasing growing at 22% annually.

2. Significant Advancements in Digital Payment Systems

The World Economic Forum has highlighted Brazil's fintech-driven financial inclusion model as a global benchmark. Pix's 2024 extension to automatic recurring payments (Pix Automático) is expected to further increase e-commerce subscription service adoption across streaming, SaaS, and subscription commerce platforms.

3. Rise of Social Commerce and Live Shopping

Live shopping events, where influencers sell products in real-time via streaming platforms, generated over BRL 2 billion in transactions in 2024, growing at 120% year-over-year. This trend is particularly powerful in fashion, beauty, and consumer electronics categories among Brazil's 144 million social media users.

4. Same-Day and Ultra-Fast Delivery Infrastructure Expansion

In March 2026. Amazon introduced its “Amazon Now” service in Brazil, offering delivery of everyday essentials and groceries within 15 minutes, marking an expansion of its presence in Latin America’s largest economy. Drone delivery pilot programs in Minas Gerais and São Paulo indicate that by 2030, 40% of Brazilian e-commerce packages in major metros could be delivered within 2 hours, fundamentally changing consumer purchase behavior.

5. AI-Powered Personalization and Omnichannel Retail Integration

Magazine Luíza's AI platform, LuizaLabs, processes 200 million daily product recommendations. The integration of online and offline touchpoints, BOPIS (Buy Online Pick Up In Store), QR code-enabled in-store reordering, and phygital showrooms is emerging as a key competitive differentiator among omnichannel Brazilian retailers targeting the 2026–2034 growth cycle.

Industry Value Chain Analysis

The Brazil e-commerce value chain encompasses multiple interconnected layers, from seller onboarding and inventory management through platform-mediated transactions, payment processing, logistics fulfilment, and post-purchase service. Each layer is populated by specialized operators whose performance directly influences platform competitiveness, customer satisfaction, and market growth velocity.

|

Stage |

Key Players / Examples |

|

Sellers & Merchants |

Brazilian brands, SMEs, individual sellers (CPF), cross-border importers |

|

E-commerce Platforms |

Mercado Livre, Amazon Brazil, Shopee, Magazine Luíza, Casas Bahia |

|

Payment Gateways & Fintech |

Mercado Pago, PicPay, PagSeguro (UOL), Cielo, Stone, Pix (BCB infrastructure) |

|

Logistics & Fulfilment |

Mercado Envios, Correios, Loggi, TotalExpress, Amazon Logistics, Jadlog, Sequoia Logística |

|

End Consumers (B2C/B2B) |

DataReportal reports 180+ million internet users in Brazil as of January 2025; SME buyers (B2B); household consumers (B2C) |

Technology Landscape in the Brazil E-commerce Industry

Digital Payment Infrastructure and Open Finance

Brazil's open finance ecosystem (Open Banking Phase 4 launched in 2022) is enabling third-party financial service providers to access consumer banking data with consent, powering next-generation credit assessment, personalized BNPL offers, and frictionless account-to-account payment initiation within e-commerce checkout flows.

AI, Machine Learning, and Recommendation Engines

Leading Brazilian e-commerce platforms are deploying sophisticated AI capabilities, including NLP-powered search (replacing keyword-matching), visual search (camera-based product discovery), dynamic personalized homepages, and predictive inventory management. Mercado Libre leverages AI and machine learning to detect platform irregularities, with only 0.74% of over 614 million listings removed for rule violations in H1 2023.

Logistics Technology and Last-Mile Innovation

Autonomous delivery vehicles, smart parcel lockers (MeLi Places network: 4,000+ locations in Brazil), drone delivery pilot programs, and AI-optimized route planning are converging to address Brazil's last-mile delivery cost challenge. MELI Logistics' proprietary network now handles over 70% of Mercado Livre's Brazilian shipments, enabling delivery time guarantees that third-party carriers cannot match.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

B2C E-Commerce |

78.2% |

2025 |

|

Region |

Southeast |

52.6% |

2025 |

By Type

To access detailed market analysis, Request Sample

B2C E-commerce dominates with a 78.2% share in 2025 (approximately USD 401.36 Billion), reflecting the mass consumer adoption of online retail across Brazil's 187.9 million internet users. B2C commerce in Brazil is characterized by marketplace-dominant buying behavior; the top five marketplace platforms collectively account for over 70% of B2C transaction volume.

B2B E-commerce holds 21.8% of the market (approximately USD 111.89 Billion in 2025), representing a rapidly digitizing segment as Brazilian businesses increasingly conduct procurement, inventory restocking, and supplier management through digital channels. B2B marketplace platforms, including Mercado Livre's business tier.

Regional Market Insights

The Southeast region's 52.6% market share (2025, approximately USD 270.17 Billion) is anchored by São Paulo, Latin America's largest city and commercial capital, which alone accounts for an estimated 30%+ of Brazil's total e-commerce GMV. The Southeast's dominance reflects its concentration of high-income consumers, advanced logistics infrastructure, technology talent, and headquarters concentration of all major Brazilian e-commerce platforms.

|

Region |

Share (2025) |

Key Growth Drivers |

Key Challenge |

|

Southeast |

52.6% |

High-income urban consumers, advanced logistics, all major HQs |

Market saturation in premium segments |

|

South |

18.4% |

High consumer spending, strong SME base, German/Italian heritage of online retail |

Distance from major fulfilment hubs |

|

Northeast |

16.3% |

Fastest-growing internet access, Pix financial inclusion, large young population |

Logistics cost; limited fulfilment hub coverage |

|

Central-West |

7.4% |

Agribusiness wealth, Brasília government market, growing middle class |

Geographic isolation; long delivery times |

|

North |

5.3% |

Growing connectivity (Zona Franca de Manaus), Norte Conectado programme |

River logistics: extreme geographic isolation |

The South region (18.4%, 2025) is Brazil's second most developed e-commerce market, characterized by high consumer spending power, strong artisanal and SME seller presence on marketplaces, and particularly high adoption of e-commerce among the region's German and Italian-heritage consumer communities.

Competitive Landscape

The Brazil e-commerce market exhibits a moderately concentrated structure at the platform level, with the top three platforms, Amazon.com Inc., MercadoLibre, Inc., and Shopee, collectively accounting for approximately 55–65% of total e-commerce GMV in 2025. The balance is distributed among Brazilian national champions, vertical specialists (KaBuM for tech/gaming, MadeiraMadeira for home/furniture), and thousands of direct-to-consumer brand sites.

|

Company |

Headquarters |

Market Position |

Core Strength |

|

Amazon.com Inc. |

USA (Brazil: SP) |

Market Leader |

Prime membership, logistics expansion (250 distribution centers), and marketplace scale |

|

MercadoLibre, Inc. |

Uruguay (Global HQ: Montevideo); Brazil HQ: São Paulo |

Market Leader |

Integrated marketplace + Mercado Pago fintech + Mercado Envios logistics + Mercado Ads; fastest delivery network in Brazil |

|

Shopee |

Singapore (Brazil HQ: SP) |

Strong Challenger |

Aggressive seller subsidies, gamification, social features, and price competitiveness |

|

Magazine Luiza |

Brazil (Franca, SP) |

National Champion |

LuizaLabs AI, 1,000+ physical stores, Magalu super-app, fintech integration |

|

MadeiraMadeira Comércio Eletrônico S/A |

Brazil (Curitiba, PR) |

Vertical Leader |

Brazil's largest home & furniture e-commerce; 3M+ products/SKUs |

|

Apple Inc. |

USA (Brazil: SP) |

Premium Specialist |

Apple Store Brazil; premium consumer electronics; AppleCare |

Increasing adoption of mobile commerce, digital payments such as Pix, and social commerce via platforms like WhatsApp are intensifying competition, pushing companies to invest in AI-driven personalization, logistics infrastructure, and last-mile delivery to differentiate and capture market share.

Key Company Profiles

Amazon.com Inc.

Amazon has invested heavily in Brazilian logistics infrastructure, establishing fulfilment centers across São Paulo, Rio de Janeiro, Minas Gerais, Rio Grande do Sul, Ceará, and Pernambuco.

- Product Portfolio: Amazon Marketplace, Amazon Prime, Amazon Business (B2B), AWS Brazil, Kindle, Alexa, Amazon Advertising.

- Recent Developments: Amazon launched its “Amazon Now” service in Brazil, partnered with Rappi, offering 15-minute delivery of groceries and essentials starting in São Paulo.

- Strategic Focus: Prime membership growth, logistics network densification, AWS cloud expansion for Brazilian enterprises, and Amazon Advertising revenue growth from marketplace sellers.

Magazine Luiza

Magazine Luíza is Brazil's most innovative omnichannel retailer, pioneering the integration of its 1,000+ physical stores with its digital marketplace through the Magalu super-app. Magalu's LuizaLabs technology division has positioned the company as a Brazilian tech retail company, driving superior customer retention through Magalu Pay fintech integration and AI-powered personalization.

- Product Portfolio: Magalu marketplace, KaBuM (tech/gaming), Netshoes (sports), Magalu Pay, Magalu Ads.

- Recent Developments: Acquired KaBuM and integrated it as Brazil's leading tech/gaming e-commerce vertical.

- Strategic Focus: Super-app ecosystem monetization, Magalu Pay financial services penetration, seller ecosystem expansion across all Brazilian regions, and LuizaLabs AI capability commercialization.

Shopee

Shopee, operated by Singapore's Sea Limited, entered Brazil in 2019 and rapidly became one of the country's top three e-commerce platforms through aggressive seller subsidization, free shipping promotions, gamified shopping experiences, and social commerce features tailored to Brazil's mobile-native consumer culture. Shopee's asset-light marketplace model (relying primarily on seller-shipped logistics) enables highly competitive pricing across fashion, beauty, and everyday consumer goods.

- Product Portfolio: Shopee marketplace, ShopeePay (Pix-integrated), Shopee Live (live shopping), Shopee Ads.

- Recent Developments: Launched Shopee Live streaming commerce feature offering exclusive coupons, Shopee coins, among other features to the customers.

- Strategic Focus: Mobile-first market share consolidation, Shopee Live social commerce expansion, seller base growth in the Northeast and South regions, and ShopeePay financial services monetization.

Market Concentration Analysis

The Brazilian e-commerce market's platform layer is moderately concentrated, with Mercado Livre, Amazon Brazil, and Shopee collectively commanding approximately 55–65% of total GMV in 2025. However, the seller ecosystem beneath these platforms is highly fragmented, with over 3 million registered marketplace sellers in Brazil, creating a competitive long-tail of product assortment.

Consolidation is accelerating in the mid-market segment, with Magalu's acquisitions of KaBuM, creating a multi-vertical digital commerce platform that increasingly resembles a super-app ecosystem. Private equity and international strategic interest in Brazilian e-commerce logistics, fintech-integrated commerce, and B2B digitization platforms remains elevated, with 8–12 significant M&A transactions expected annually through 2034.

Investment & Growth Opportunities

Fastest Growing Segments

B2B e-commerce digitization (CAGR ~15%), social commerce and live shopping (CAGR ~35%), and quick commerce/rapid delivery (CAGR ~28%) represent the three highest-growth investment vectors in the Brazil e-commerce market through 2034. Together, these segments address a total addressable opportunity of approximately USD 200+ billion within Brazil's e-commerce ecosystem by 2034.

Emerging Market Expansion

The Northeast and North regions collectively represent an incremental USD 80+ billion e-commerce opportunity by 2034, driven by rising internet penetration (Norte Conectado federal program targeting 100% 4G coverage by 2028), financial inclusion via Pix, and a young mobile-native demographic population of approximately 85 million consumers. Entry via marketplace seller ecosystem expansion, regional distribution center investment, and social commerce partnerships with Northeast-based influencers are the preferred investment strategies for capturing accelerating regional growth.

Venture and Institutional Investment Trends

Brazilian e-commerce and e-commerce-adjacent (logistics tech, payment fintech, social commerce) startups attracted approximately USD 3.2 billion in venture and PE investment in 2024, despite a broader global venture capital correction. Key funding themes include quick commerce platforms, B2B procurement digitization, AI-powered commerce personalization, and logistics technology for last-mile optimization in underserved Brazilian regions.

- Key investment themes: Pix-native commerce infrastructure, AI-powered recommendation and fraud prevention platforms, drone and autonomous last-mile delivery networks, and B2B marketplace verticals for food service, construction, and agribusiness.

- Family offices and Brazilian institutional investors (Itaú, BTG, XP) are increasing direct e-commerce equity positions, targeting high-growth marketplace verticals and logistics network operators with defensible regional coverage.

- Cross-border strategic investment from Asian e-commerce giants (Shein manufacturing supply chain integration, TikTok Shop Brazil launch preparation) is reshaping the competitive dynamics of the social commerce and fashion e-commerce segments.

Future Market Outlook (2026-2034)

The Brazil e-commerce market is positioned for continued, robust growth through 2034. From a base of USD 513.25 Billion in 2025, the market is projected to reach USD 1,501.78 Billion by 2034, representing total incremental value creation of approximately USD 988.53 Billion over the forecast decade, the largest absolute e-commerce growth opportunity in Latin America.

Regulatory evolution, particularly Brazil's tax reform implementation (CBS/IBS framework), digital services regulation, and the Central Bank's ongoing Open Finance expansion, will define the competitive operating environment through 2034. Platforms and marketplace operators that build compliance-ready infrastructure, deepen Pix and Open Finance integration, and execute regional market expansion strategies will capture disproportionate market share growth.

Long-term, the market's trajectory is tied to three structural macro-themes: digital payment infrastructure deepening, social commerce maturation (WhatsApp Pay + TikTok Shop formalizing BRL billions in informal social commerce transactions), and logistics infrastructure closing the coverage gap between Southeast and Norte/Nordeste regions. Brazil's e-commerce market sits at the convergence of all three, positioning it among the world's highest-conviction long-term digital commerce investment destinations.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 100 industry participants in 2024–2025, including e-commerce marketplace operators, logistics service providers, payment technology companies, digital marketing specialists, retail executives, and end consumers across São Paulo, Rio de Janeiro, Belo Horizonte, Recife, and Fortaleza.

Secondary Research

Secondary research encompassed a systematic review of company annual reports and investor presentations (Mercado Livre, Magazine Luíza, Sea Limited), Brazilian Central Bank digital payment statistics (Pix transaction data), Anatel connectivity reports, industry databases (Euromonitor, Similarweb, DataReportal), trade publica0tions (E-Commerce Brasil, Ecommerce News), and Associação Brasileira de Comércio Eletrônico (ABComm) annual market data.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating Brazilian GDP growth projections, internet user growth trajectories, smartphone penetration rates, digital payment adoption curves, and historical e-commerce GMV growth rates. A base-case CAGR of 12.14% reflects consensus analyst estimates validated against reported platform GMV growth rates and ABComm annual industry reporting.

Brazil E-commerce Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Amazon.com Inc., MercadoLibre, Inc., Shopee, Magazine Luiza, MadeiraMadeira Comércio Eletrônico S/A, Apple Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Brazil E-commerce Market Report

The Brazil e-commerce market reached USD 513.25 Billion in 2025. It is projected to reach USD 1,501.78 Billion by 2034.

The Brazil e-commerce market is expected to grow at a CAGR of 12.14% during the forecast period from 2026 to 2034, supported by rising internet penetration, Pix digital payment adoption, expanding logistics infrastructure, and growing middle-class consumer purchasing power.

The Southeast region leads with a 52.6% revenue share in 2025, driven by the concentration of Brazil's highest-income consumer markets in São Paulo and Rio de Janeiro, the location of all major e-commerce platform headquarters and fulfilment infrastructure, and the most advanced logistics network in the country.

B2C e-commerce dominates with a 78.2% share in 2025, driven by mass consumer adoption of online retail across electronics, fashion, home goods, and food delivery categories on Brazil's major marketplace platforms.

Key players include Amazon.com Inc., MercadoLibre, Inc., Shopee, Magazine Luiza, MadeiraMadeira Comércio Eletrônico S/A, and Apple Inc.

Pix, launched by Brazil's Central Bank in November 2020, has transformed e-commerce payments by providing instant, zero-cost, 24/7 account-to-account transfers accessible to all Brazilians with a CPF number. By 2024, Pix represented nearly 30% of e-commerce transactions, reducing cart abandonment rates, enabling financial inclusion for previously unbanked consumers, and lowering payment processing costs for merchants by approximately 1.5–2.5% compared to card processing fees.

Key challenges include Brazil's complex multi-tier tax system, significant logistics cost, and coverage deficits in the Norte and Nordeste regions, cybersecurity and e-commerce fraud, currency volatility impacting cross-border commerce, and transitional regulatory uncertainty associated with Brazil's ongoing comprehensive tax reform implementation.

B2B e-commerce (21.8% share, 2025) is expected to grow faster than B2C through 2034, driven by Brazilian SME digitization programs, the expansion of B2B marketplace platforms for food service, construction, and agribusiness procurement, and the integration of Open Finance-enabled credit solutions into B2B transaction workflows.

Significant investment opportunities exist in B2B marketplace digitization (food service, agribusiness, construction), social commerce infrastructure (WhatsApp Pay integration, TikTok Shop expansion), Northeast and North regional logistics network development, AI-powered personalization platforms, and quick commerce operations in secondary Brazilian cities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade