Brazil Telecom Market Size, Share, Trends and Forecast by Service, and Region, 2026-2034

Brazil Telecom Market Size, Share, Trends & Forecast (2026-2034)

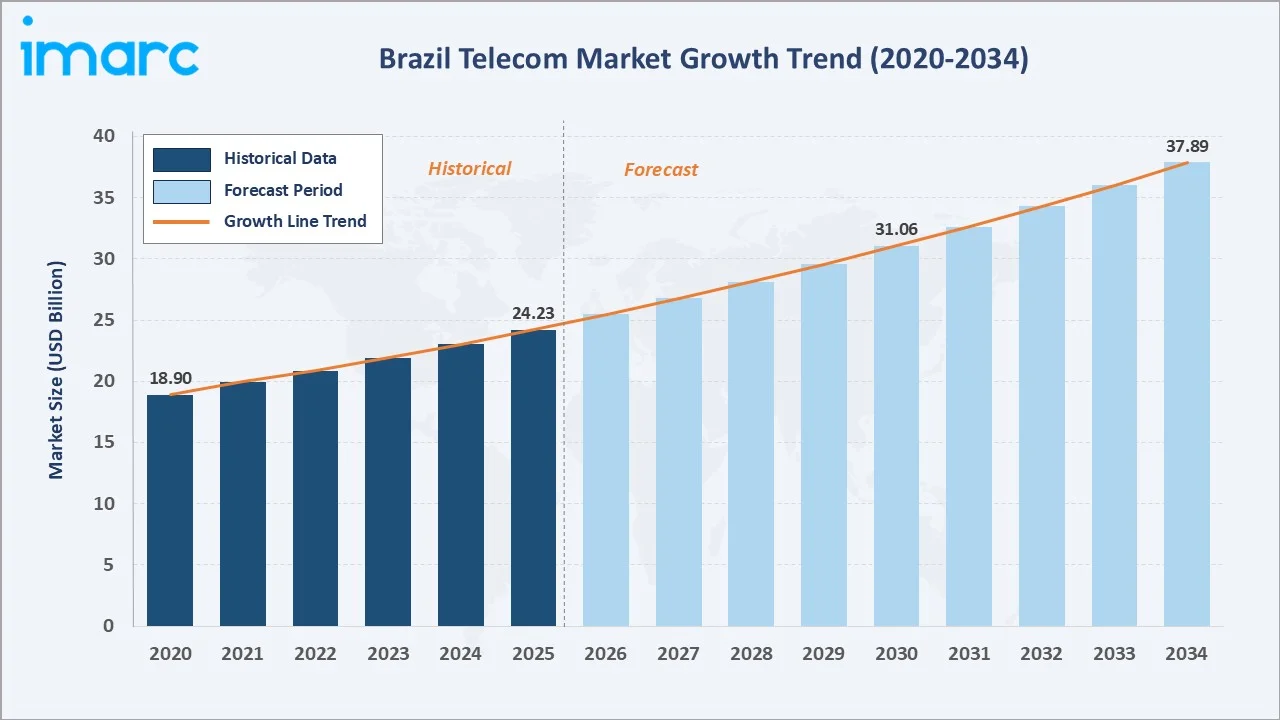

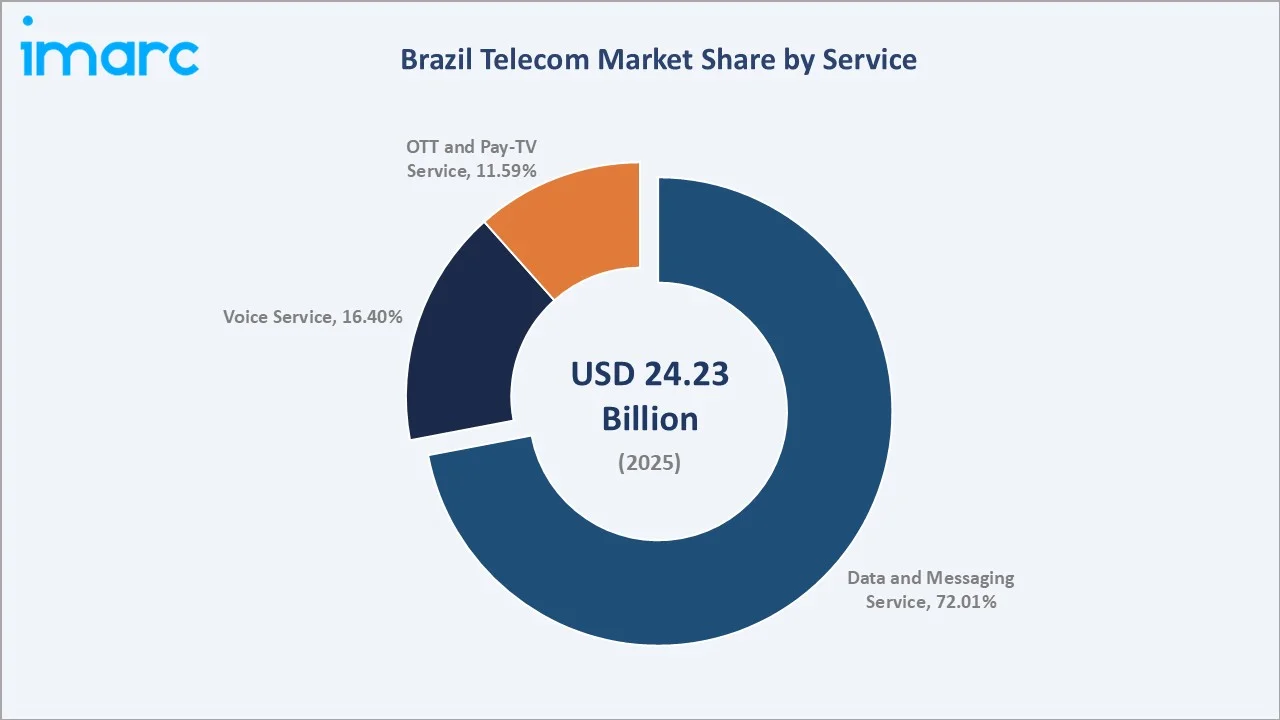

The Brazil telecom market was valued at USD 24.23 Billion in 2025 and is projected to reach USD 37.89 Billion by 2034, exhibiting a CAGR of 5.09% during 2026-2034. The market is driven by expanding 5G network deployments, rising mobile data consumption, increasing smartphone penetration, and growing enterprise demand for cloud-based and digital connectivity solutions.

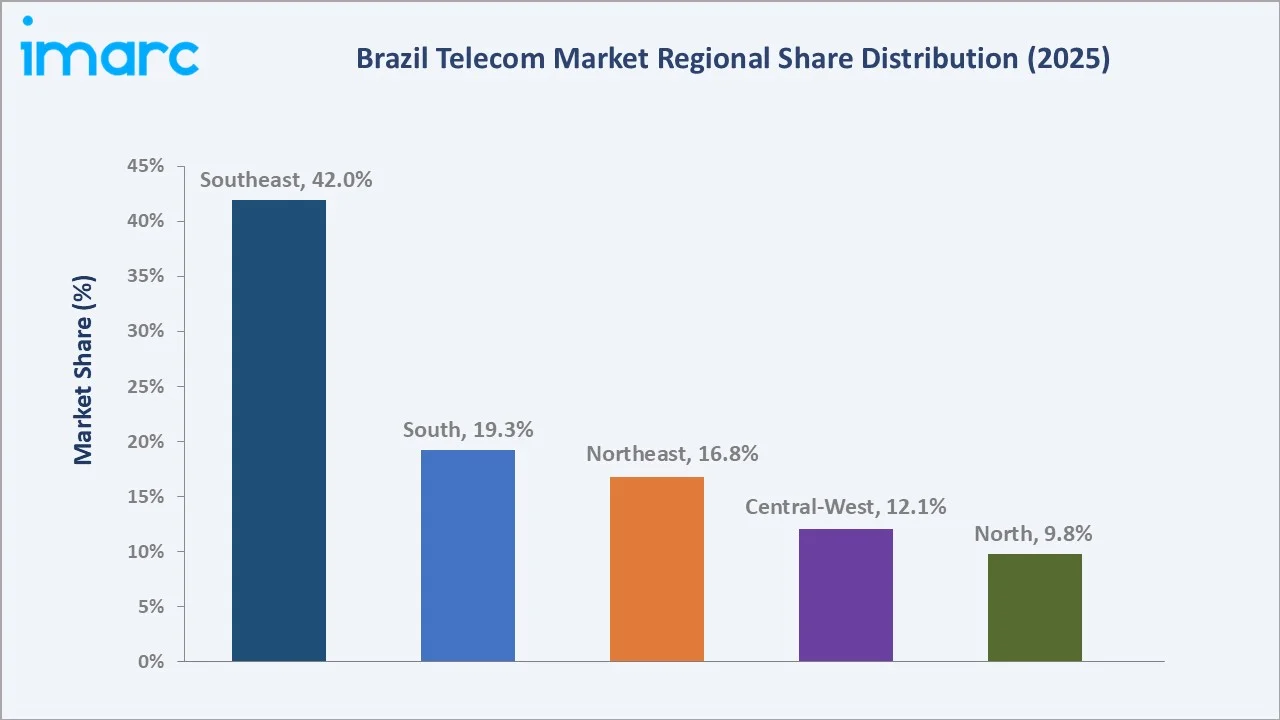

Data and messaging service leads at 72.01% and Southeast commands 42.0% of the market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 24.23 Billion |

|

Forecast Market Size (2034) |

USD 37.89 Billion |

|

CAGR (2026-2034) |

5.09% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Southeast (42.0%, 2025) |

|

Leading Service |

Data and Messaging Service (72.01%, 2025) |

The Brazil telecom market expanded from USD 18.90 Billion in 2020 to USD 24.23 Billion in 2025, driven by rapid mobile broadband uptake, digital inclusion initiatives, and early 5G adoption. Anchored at USD 31.06 Billion in 2030, the forecast to USD 37.89 Billion by 2034 is supported by continued fiber-to-the-home expansion, enterprise digitization, and growing demand for connected services.

To get more information on this market, Request Sample

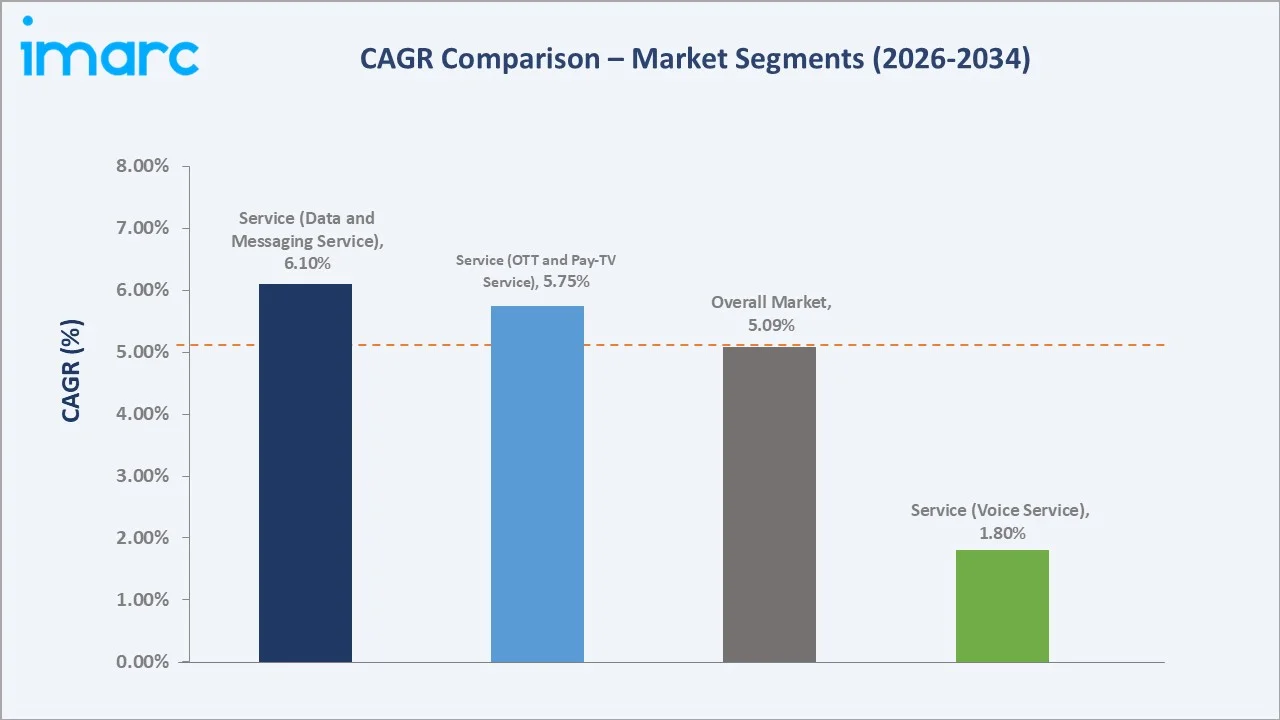

CAGR trajectories across service sub-segments show data and messaging service and OTT and pay-TV service expanding faster than the overall 5.09% market CAGR through 2034, driven by 5G deployments, mobile video streaming, and the growing adoption of digital entertainment and cloud-based applications.

Executive Summary

The Brazil telecom market is on a consistent growth path from USD 18.90 Billion in 2020 to USD 37.89 Billion by 2034. The market has undergone significant structural shifts, transitioning from legacy voice-led revenue models to broadband and data-centric architectures. Fiber-to-the-home rollouts, 5G commercialization, and enterprise digitization are reshaping competitive dynamics and expanding the total addressable market.

Data and messaging service dominates at 72.01% in 2025, reflecting accelerating mobile internet consumption. As per a report from Brazilian telecom regulator Anatel, in Q2 2024, the typical mobile data usage per user increased by 11% to 5.63 GB, compared to 5.08 GB during the same quarter in 2023. Southeast commands 42.0%, led by dense urban centers, such as São Paulo and Rio de Janeiro, where enterprise demand and consumer digital adoption remain highest.

Key Market Insights

|

Insight |

Data |

|

Leading Service |

Data and Messaging Service – 72.01% share (2025) |

|

Second Largest Service |

Voice Service – 16.40% share (2025) |

|

Leading Region |

Southeast – 42.0% share (2025) |

|

Top Companies |

Telefónica S.A., Telecom Italia, V.tal, Brisanet |

Key Analytical Observations Supporting the Above Data:

- Data and messaging service dominance at 72.01% is underpinned by rapid mobile broadband infrastructure expansion, while ongoing 5G rollout initiatives and increasing smartphone usage continue to accelerate data traffic volumes across urban and semi-urban regions. Brazil's Communications Minister Frederico de Siqueira Filho declared that as of April 2026, the country surpassed its 5G rollout targets, reaching more than 60 Million individuals, which was about 70% of the population.

- Voice service at 16.40% reflects the continued relevance of mobile voice calls despite the shift to OTT-based communication. Revenue from voice services is declining gradually as operators pivot toward data-centric pricing and bundle offerings.

- Southeast at 42.0% reflects the concentration of economic activity, enterprise demand, and technology-ready consumers. The region hosts Brazil's largest cities and attracts the highest levels of telecom infrastructure investment.

- North at 9.8% represents the most underpenetrated market with the highest growth potential. Government connectivity mandates linked to the 5G auction and improving broadband affordability are accelerating adoption in historically underserved areas.

Brazil Telecom Market Overview

Telecom refers to the transmission of voice, data, video, and internet services across wired and wireless communication networks that enable connectivity between individuals, businesses, and digital systems. It includes mobile communication, fixed-line telephony, broadband internet, satellite communication, and digital media services supported by network infrastructure, spectrum assets, fiber-optic systems, and data transmission technologies.

The ecosystem integrates spectrum rights holders, mobile network operators, fixed-line and fiber providers, OTT platform operators, equipment manufacturers, and independent tower companies. Macroeconomic factors including urbanization, a growing middle class, and digital financial inclusion are driving sustained demand. The network infrastructure spans 4G LTE, rapidly expanding 5G standalone deployments, and a competitive fiber-to-the-home buildout targeting underserved municipalities nationwide.

Market Dynamics

To evaluate market opportunities, Request Sample

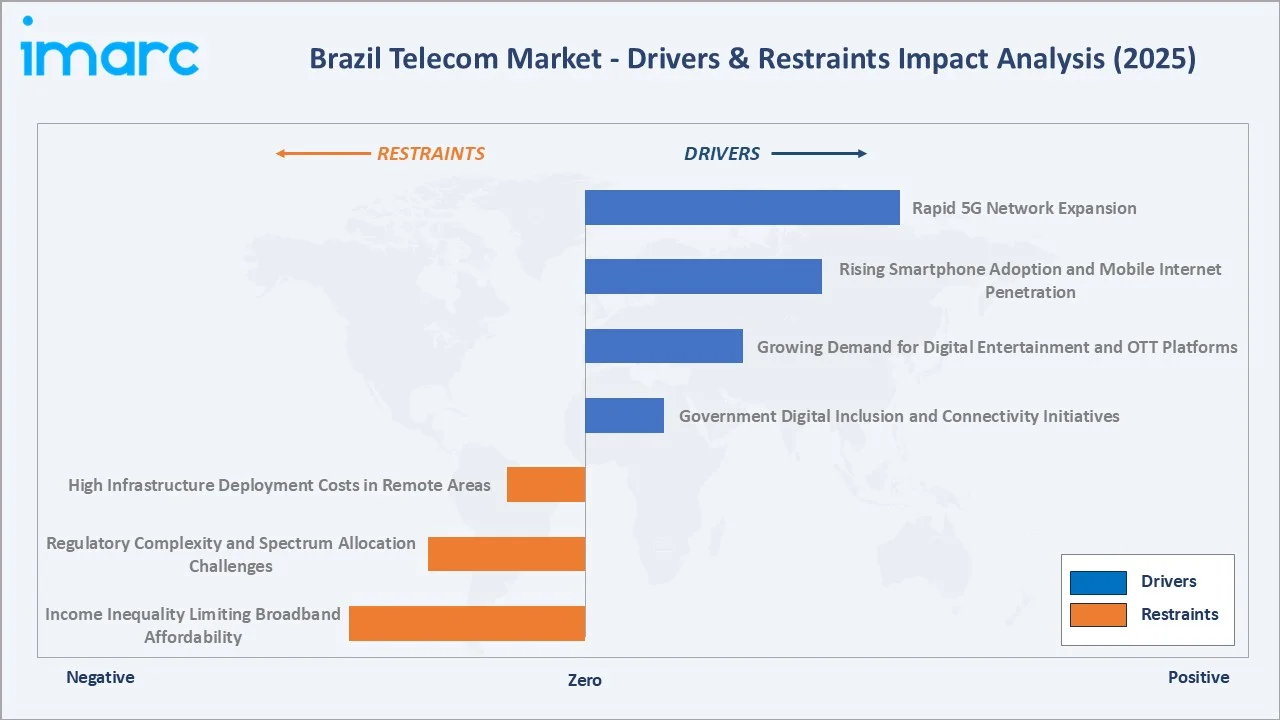

Market Drivers

- Rapid 5G Network Expansion: Operator-led deployment of 5G networks across Brazil's major urban centers is enabling ultra-fast mobile connectivity and creating new monetization opportunities through enhanced mobile broadband and enterprise services. 5G coverage is progressively expanding beyond early commercial launch cities into secondary markets.

- Rising Smartphone Adoption and Mobile Internet Penetration: Growing smartphone usage and expanding mobile internet accessibility are driving sustained demand for telecom data and messaging services.

- Growing Demand for Digital Entertainment and OTT Platforms: Widespread adoption of video streaming, music platforms, and online gaming is generating significant incremental data traffic, incentivizing operators to invest in network capacity and offer bundled digital content subscriptions. As per IMARC Group, the Brazil online gaming market size was valued at USD 3.46 Billion in 2025.

- Government Digital Inclusion and Connectivity Initiatives: Federal programs aimed at expanding internet access in rural and low-income areas, including obligations tied to the 5G spectrum auction, are driving operator investment in underserved regions and broadening the addressable market.

Market Restraints

- High Infrastructure Deployment Costs in Remote Areas: Significant infrastructure gaps persist across rural and semi-urban regions, where high capital expenditure requirements and challenging geographic conditions continue to limit broadband and fiber network expansion. The elevated cost of deploying telecom infrastructure in low-density areas remains a major barrier without sustained government support and investment incentives.

- Regulatory Complexity and Spectrum Allocation Challenges: Evolving spectrum management policies, licensing requirements, and municipal permitting processes can delay network rollout timelines and increase compliance costs for operators, particularly smaller regional providers seeking to expand coverage.

- Income Inequality Limiting Broadband Affordability: Significant income disparity across Brazil's regions constrains broadband adoption in lower-income households, limiting ARPU growth potential and requiring operators to offer low-cost data plans that compress margins.

Market Opportunities

- Fiber-to-the-Home Expansion in Secondary Cities: Hundreds of smaller Brazilian cities remain underserved by high-speed fiber broadband, representing a significant addressable market for regional ISPs and national operators pursuing geographic diversification strategies.

- IoT and Smart City Deployments: The proliferation of connected devices across smart agriculture, logistics, utilities, and urban management is creating growing demand for enterprise IoT connectivity, offering operators diversified revenue opportunities beyond traditional consumer services.

- Cloud and Enterprise Connectivity Growth: Rising adoption of cloud computing, hybrid work models, and digital transformation among Brazilian enterprises is driving demand for high-bandwidth, low-latency connectivity, SD-WAN solutions, and managed network services.

Market Challenges

- Intense Price Competition Compressing Margins: The highly competitive Brazilian telecom market, with multiple national operators and numerous regional ISPs, exerts significant downward pressure on service tariffs, making it difficult for operators to translate revenue growth into improved profitability.

- Customer Churn and Retention in Saturated Mobile Segments: High mobile subscriber penetration in urban markets intensifies competition for retention, requiring sustained investment in network quality, customer experience, and value-added services to reduce churn rates.

Emerging Market Trends

1. 5G Network Deployment Acceleration

Telecom operators are rapidly expanding standalone 5G network deployments across major metropolitan areas, with coverage increasingly extending into secondary cities and developing regions. The ongoing rollout is enabling advanced connectivity applications, including ultra-low latency services, mobile edge computing, IoT integration, and private enterprise network solutions, while supporting broader digital transformation initiatives across industries.

2. Fiber-to-the-Home Expansion Displacing Legacy Copper Networks

Brazil's fiber-to-the-home network has expanded significantly, with ISPs and national operators actively replacing copper-based infrastructure with high-speed fiber connections across urban and semi-urban areas. This transition is improving network capacity, reducing operational maintenance costs, and enabling operators to offer competitive gigabit-capable broadband plans that drive subscriber migration from legacy technologies.

3. OTT Services Reshaping Pay-TV and Voice Revenue Streams

The rapid growth of streaming platforms and OTT messaging applications is structurally eroding traditional pay-TV subscriptions and voice call revenues. Brazilian operators are responding by bundling OTT content within service packages and shifting toward data-centric revenue models to offset declining legacy revenue streams.

4. IoT Adoption Driving Enterprise Telecom Demand

The deployment of IoT devices across agriculture, logistics, manufacturing, and smart city infrastructure is generating growing demand for specialized enterprise connectivity. Operators are investing in dedicated IoT network slices, NB-IoT and LTE-M technologies, and managed connectivity platforms to capture enterprise IoT revenue opportunities.

5. Digital Financial Services Integration with Telecom Infrastructure

Telecom operators in Brazil are increasingly leveraging their subscriber base and distribution networks to offer digital financial services including mobile payments, digital wallets, and micro-insurance products. This convergence enhances customer stickiness and opens new non-traditional revenue streams in a highly competitive market environment.

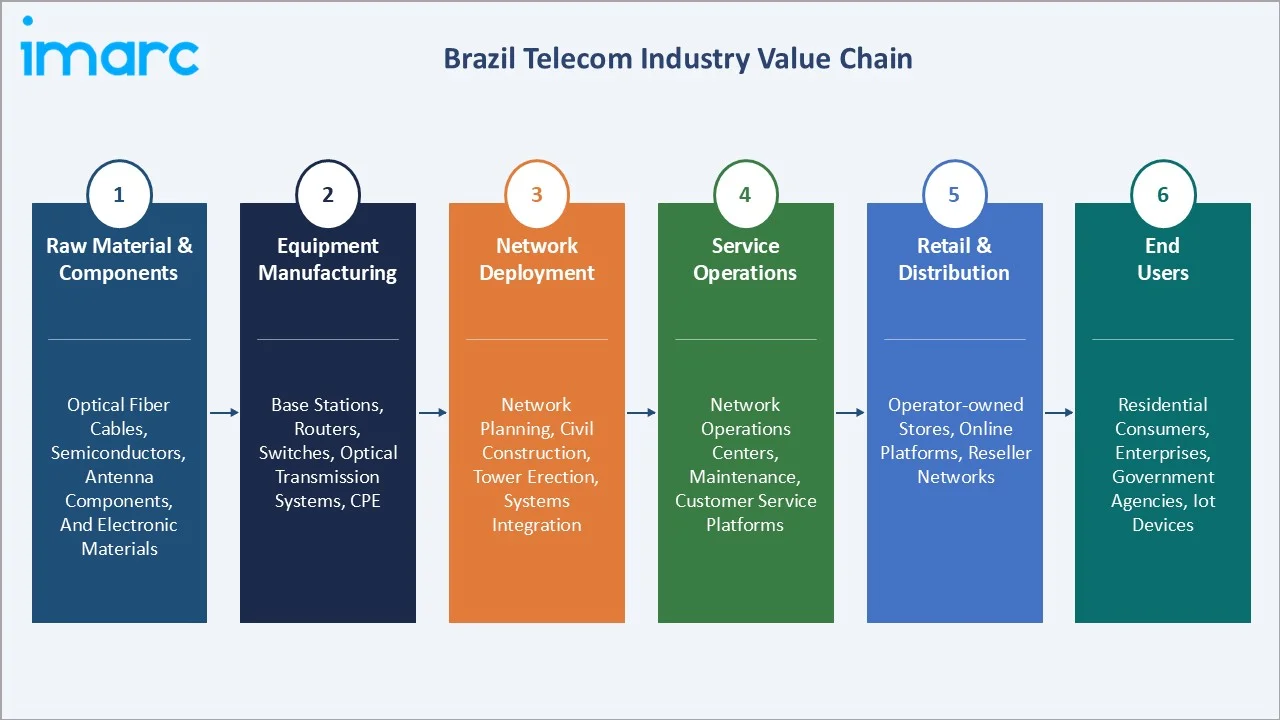

Industry Value Chain Analysis

The Brazil telecom market value chain spans six stages from component supply through end user service consumption. Network deployment and service operations capture the highest value-add for operators, while equipment manufacturing and infrastructure supply represent critical upstream dependencies in this capital-intensive industry.

|

Stage |

Key Players / Examples |

|

Raw Material & Components |

Suppliers of optical fiber cables, semiconductors, antenna components, and electronic materials supporting network equipment production |

|

Equipment Manufacturing |

Manufacturers producing base stations, routers, switches, optical transmission systems, and customer premises equipment for telecom networks |

|

Network Deployment |

Companies providing network planning, civil construction, tower erection, and systems integration services for telecom infrastructure deployment |

|

Service Operations |

Network operations centers, maintenance teams, customer service platforms, and quality management systems ensuring reliable service delivery |

|

Retail & Distribution |

Operator-owned stores, independent dealers, online platforms, and reseller networks distributing telecom products and service plans |

|

End Users |

Residential consumers, enterprises, government agencies, and IoT devices consuming voice, data, and digital communication services |

Vertically integrated operators, which manage network operations, retail channels, and digital service platforms in-house, achieve superior customer lifetime value compared to wholesale-only or infrastructure-only players. Regional ISPs compete effectively within defined geographic footprints by concentrating resources on last-mile fiber deployment and local customer service.

Technology Landscape in the Brazil Telecom Industry

5G and Next-Generation Network Infrastructure

Brazil's 5G deployment is progressing rapidly across both standalone and non-standalone architectures. Operators are investing in massive MIMO antenna systems, small cell densification, and open RAN frameworks to improve capacity and coverage efficiency. 5G standalone networks are enabling network slicing for differentiated enterprise service quality levels.

Fixed Wireless Access and FTTH Technology

Fiber-to-the-home using GPON and XGS-PON standards is being deployed at scale by major operators and regional ISPs. Fixed wireless access using 5G NR and LTE technologies is serving as a cost-effective alternative for connecting suburban and semi-urban areas where fiber trenching remains economically challenging.

Cloud, Edge Computing, and Network Virtualization

Telecom operators are migrating core network functions to cloud-native architectures using NFV and SDN technologies. Multi-access edge computing infrastructure is being deployed to support low-latency applications in smart manufacturing, connected vehicles, and augmented reality (AR), enabling operators to offer differentiated premium services.

IoT and Machine-to-Machine Connectivity

Dedicated IoT connectivity platforms leveraging NB-IoT, LTE-M, and 5G network slicing are enabling operators to address the growing enterprise IoT market. Smart agriculture, asset tracking, smart metering, and logistics monitoring are among the primary application areas driving adoption of these specialized connectivity solutions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Service |

Data and Messaging Service |

72.01% |

2025 |

|

Region |

Southeast |

42.0% |

2025 |

By Service

Data and messaging service commands a 72.01% majority share in 2025, driven by mass mobile internet adoption, growing 5G subscriber bases, and the shift in consumer behavior toward app-based messaging, video calls, and mobile content consumption. These services continue to benefit as operators upgrade infrastructure and offer competitive unlimited data plans.

To access detailed market analysis, Request Sample

Voice service at 16.40% in 2025 reflects the continued use of traditional mobile voice calls, particularly in rural areas and among older demographics. Operators maintain voice service packages as part of broader bundled offerings, though standalone voice revenue continues to face structural decline.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Southeast |

42.0% |

High urbanization, strong economic base, major enterprise concentration, and high digital adoption rates |

|

South |

19.3% |

Growing enterprise connectivity demand, expanding fiber networks, and increasing adoption of digital services |

|

Northeast |

16.8% |

Increasing mobile broadband penetration, government digital inclusion programs, and expanding urban connectivity |

|

Central-West |

12.1% |

Rising agribusiness connectivity demand, expanding urban centers, and growing enterprise services uptake |

|

North |

9.8% |

Expanding 4G and 5G coverage in underserved areas, government connectivity initiatives, and increasing smartphone adoption |

Southeast at 42.0% in 2025 leads the Brazil telecom market, driven by elevated urbanization rates, a high density of corporate clients, and mature consumer adoption of digital services. São Paulo alone accounts for a significant share of national telecom revenues, supported by well-developed infrastructure and strong competitive operator presence. Major operators have concentrated their premium service launches and fiber network densification efforts in this region.

North at 9.8% represents the most promising growth frontier through 2034. Operator investment in tower infrastructure, spectrum utilization obligations from the 5G auction, and government connectivity programs are progressively improving access across the Amazon basin and remote municipalities. Rising smartphone penetration and affordable data pricing are expected to accelerate subscriber growth in this historically underserved region.

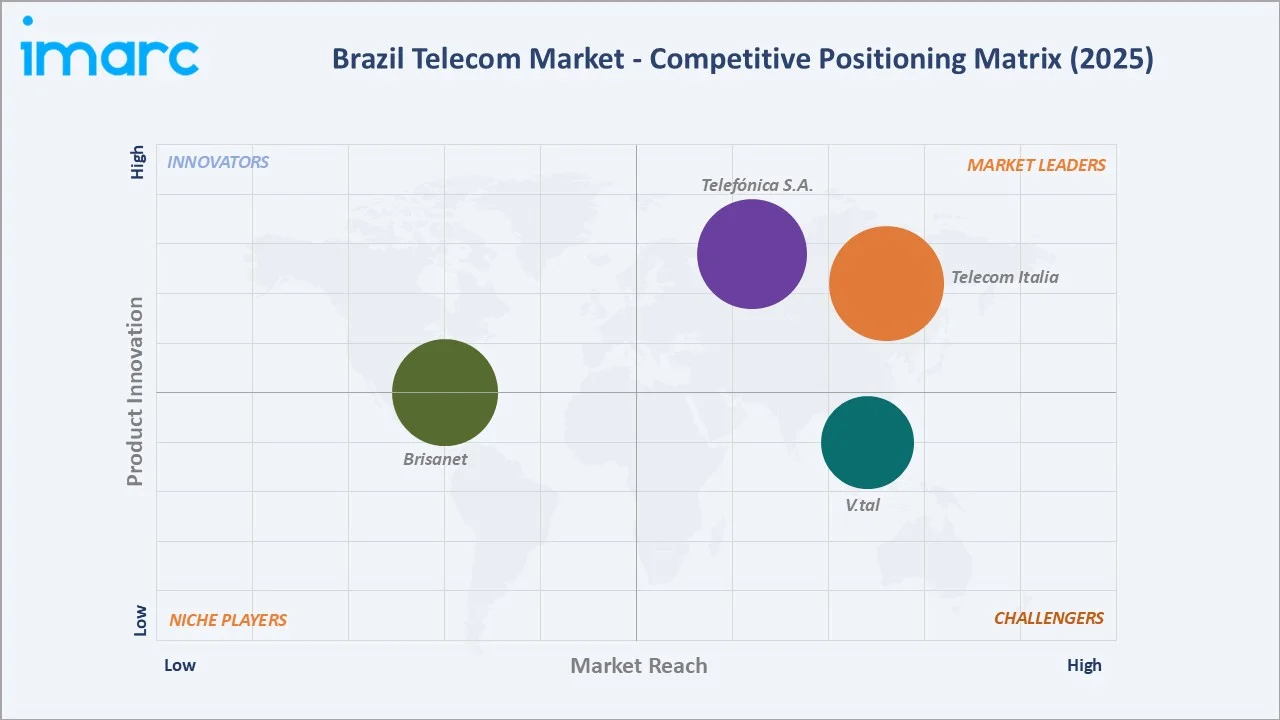

Competitive Landscape

The Brazil telecom market is moderately concentrated, with major operators maintaining strong positions across mobile and broadband services. Competition is shaped by ongoing fiber network expansion, infrastructure sharing arrangements, service quality enhancements, pricing strategies, and the integration of bundled digital offerings, such as streaming, cloud, and enterprise connectivity services.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Telefónica S.A. |

Vivo |

Leader |

Premium mobile and fiber services, enterprise connectivity leadership, and digital transformation offerings |

|

Telecom Italia |

TIM Brasil |

Leader |

5G network expansion, mobile data growth strategy, and B2B connectivity services development |

|

V.tal |

V.tal |

Challenger |

Neutral wholesale fiber network operator, largest FTTH infrastructure in Brazil, enabling ISPs and operators to expand coverage |

|

Brisanet |

Brisanet |

Leader |

Fiber broadband expansion in Northeast and Midwest Brazil, competitive pricing, and underserved market penetration |

Key players include Telefónica S.A., Telecom Italia, V.tal, and Brisanet, among others.

Key Company Profiles

Telefónica S.A.

Telefónica S.A. is a multinational telecommunications company headquartered in Spain, operating in Brazil under the Vivo brand. It is among the largest telecom operators in Brazil by revenue and subscriber base, offering integrated mobile and fixed connectivity services.

- Product Portfolio: Mobile voice and data services, fiber broadband, enterprise connectivity, digital services, and IoT solutions offered under the Vivo brand.

- Recent Developments: The company has continued to expand its fiber and 5G network infrastructure across Brazil, focusing on growing its convergent service offerings and strengthening its enterprise digital solutions portfolio.

- Strategic Focus: Premium mobile and broadband service delivery, enterprise digitization solutions, and strategic network infrastructure expansion across Brazilian markets.

Telecom Italia

Telecom Italia is a telecommunications company that operates in Brazil through its subsidiary TIM Brasil, one of the country's leading mobile network operators. TIM Brasil provides mobile voice and data services to millions of subscribers across Brazil through its nationwide mobile network.

- Product Portfolio: Mobile voice and data services (4G LTE and 5G), fiber broadband, prepaid and postpaid mobile plans, and enterprise connectivity solutions offered under the TIM Brasil brand.

- Recent Developments: The company has continued to expand its 5G network coverage across Brazilian cities and advance its fiber broadband services, supporting growth in both its mobile and fixed connectivity segments.

- Strategic Focus: Mobile network expansion, 5G deployment acceleration, enterprise connectivity services development, and broadening its fixed broadband service portfolio in Brazil.

V.tal

V.tal is a digital infrastructure company operating the largest neutral fiber optic network in Brazil. It provides wholesale connectivity solutions, fiber-to-the-home infrastructure, and data center services to telecom operators, internet service providers, and enterprises across the country.

- Product Portfolio: Long-haul fiber backbone connectivity, neutral ecosystem data centers, and digital infrastructure services offered under the V.tal brand.

- Recent Developments: The company has continued to expand its neutral fiber infrastructure across Brazil, extending coverage to additional municipalities and strengthening its wholesale connectivity and digital infrastructure service portfolio.

- Strategic Focus: Neutral open-access fiber network expansion, wholesale connectivity infrastructure growth, and digital infrastructure services development across Brazil.

Market Concentration Analysis

The Brazil telecom market is moderately concentrated at the national level, with the top key players (Telefónica S.A., Telecom Italia, V.tal, and Brisanet) collectively commanding over 80% of mobile subscriber share. The fiber broadband segment is more fragmented, with hundreds of regional ISPs competing alongside national operators.

Barriers to entry include spectrum licensing requirements, high capital investment for network deployment, ANATEL regulatory compliance, and the economies of scale advantage held by established national operators. However, the fiber broadband segment offers accessible entry points for regional ISPs with focused geographic strategies and local customer relationships.

Consolidation trends include operator acquisitions of smaller regional ISPs by national players, infrastructure sharing agreements to reduce deployment costs, and the continued shakeout of weaker operators in saturated urban markets. The competitive environment is expected to remain dynamic through 2034 as 5G monetization and fiber penetration rates evolve across regions.

Investment & Growth Opportunities

Fastest-Growing Segments

Data and messaging service at 72.01% in 2025 is expanding faster than the overall 5.09% market CAGR through 2034, driven by 5G commercialization, mobile video streaming, and growing adoption of cloud-based enterprise applications. OTT and pay-TV service at 11.59% is the second-fastest growing segment as Brazilian consumers shift toward streaming-based entertainment, creating opportunities for operators offering convergent connectivity-and-content bundles.

Emerging Market Opportunities

North at 9.8% and Northeast at 16.8% present the largest untapped market opportunities, with accelerating urbanization, improving affordability, and government connectivity programs creating conditions for rapid subscriber growth. Enterprise IoT, smart agriculture connectivity, and digital government services represent high-growth verticals beyond traditional consumer telecom services.

Venture & Investment Trends

Capital allocation is concentrated in 5G spectrum deployment, fiber-to-the-home last-mile infrastructure, cloud and edge computing facilities, and digital service platforms. Investment is also expanding into satellite connectivity for rural areas, IoT network infrastructure, and enterprise managed services platforms that generate recurring revenue streams beyond commodity bandwidth.

Future Market Outlook (2026-2034)

The Brazil telecom market is forecast to expand from USD 24.23 Billion in 2025 to USD 37.89 Billion by 2034 at a CAGR of 5.09%, adding approximately USD 13.66 Billion in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: accelerating 5G monetization through enterprise and advanced consumer applications; fiber-to-the-home coverage reaching a majority of Brazilian households; the rise of IoT and smart connectivity as a diversified revenue stream; and the consolidation of OTT and digital service bundling within operator commercial offerings.

By 2034, data services are expected to account for an even larger share of total market revenue as voice service revenues continue their structural decline. Operators capable of scaling fiber infrastructure, monetizing 5G capabilities, and delivering differentiated digital services will be best positioned to capture growth in an increasingly competitive market landscape.

Research Methodology

Primary Research

Primary research included interviews with senior executives at Brazilian telecom operators, regulatory affairs professionals, infrastructure vendors, enterprise connectivity managers, and digital service platform leaders. These interviews validated market sizing, service segment splits, regional dynamics, and competitive positioning assessments.

Secondary Research

Secondary sources included ANATEL publications and regulatory filings, annual reports and investor presentations from listed Brazilian telecom operators, ITU statistical databases, World Bank connectivity data, and trade publications covering the Brazilian telecommunications sector.

Forecasting Models

Market forecasts used top-down and bottom-up models combining subscriber growth projections, ARPU evolution, service adoption rates, infrastructure investment timelines, and regulatory scenario analysis. Sensitivity analysis addressed variations in 5G rollout pace, macroeconomic conditions, and competitive pricing dynamics.

Brazil Telecom Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Services Covered |

|

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Telefónica S.A., Telecom Italia, V.tal, Brisanet, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Brazil Telecom Market Report

The Brazil telecom market was valued at USD 24.23 Billion in 2025, driven by strong mobile broadband demand, fiber expansion, and growing digital service adoption across the country.

The market is projected to grow at a CAGR of 5.09% from 2026 to 2034, reaching USD 37.89 Billion, supported by 5G deployments and data service monetization across segments.

Data and messaging service leads at 72.01% in 2025, driven by mass mobile internet adoption, 5G rollout, and consumer shift toward digital communication and streaming platforms.

Southeast commands 42.0% in 2025, led by São Paulo and Rio de Janeiro, driven by urban density, enterprise demand, and advanced network infrastructure availability.

North at 9.8% is the fastest growing, driven by expanding 5G coverage, government connectivity initiatives, and rising smartphone adoption in historically underserved areas.

Key players include Telefónica S.A., Telecom Italia, V.tal, and Brisanet, among others.

Fiber-to-the-home expansion is replacing legacy copper networks, enabling gigabit connectivity, improving operator margins, and opening competitive opportunities for regional ISPs across Brazil.

Investment opportunities include 5G infrastructure, fiber last-mile deployment in secondary cities, enterprise IoT platforms, and digital service convergence across mobile and broadband segments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade