Cheese Market Size, Share, Trends and Forecast by Source, Type, Product, Format, Distribution Channel, and Region, 2026-2034

Global Cheese Market Size, Share, Trends & Forecast 2026-2034

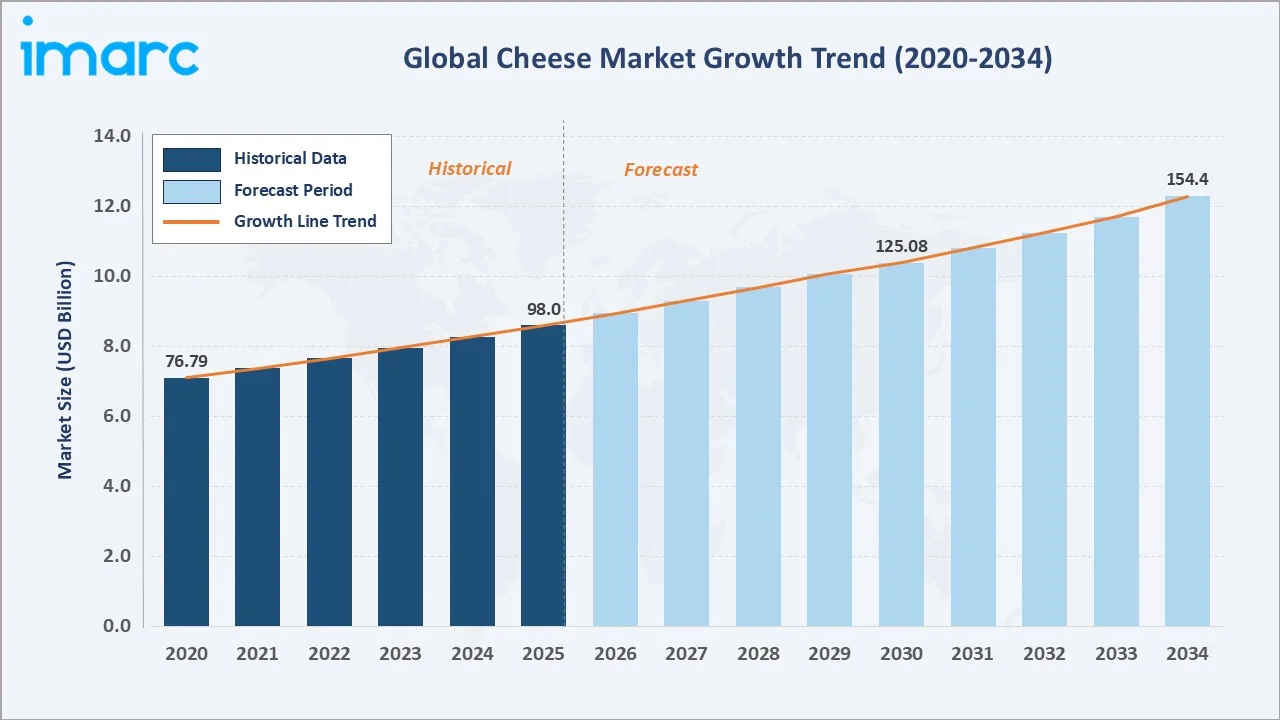

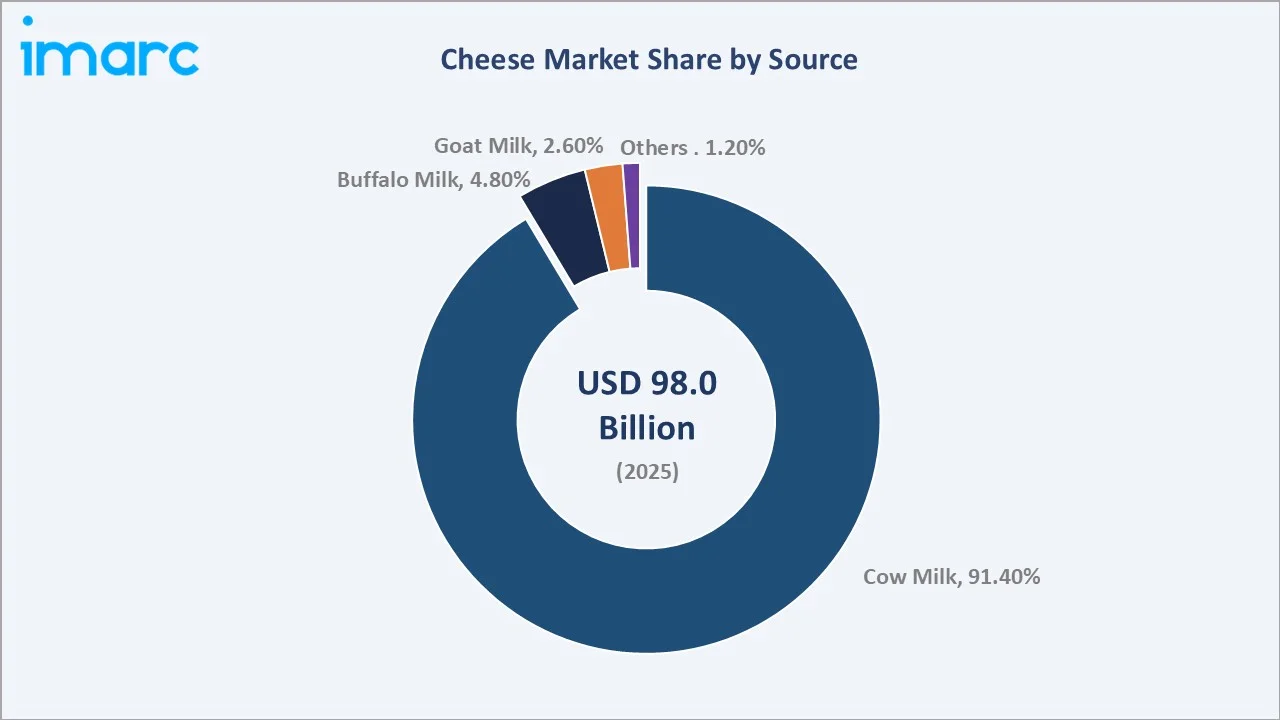

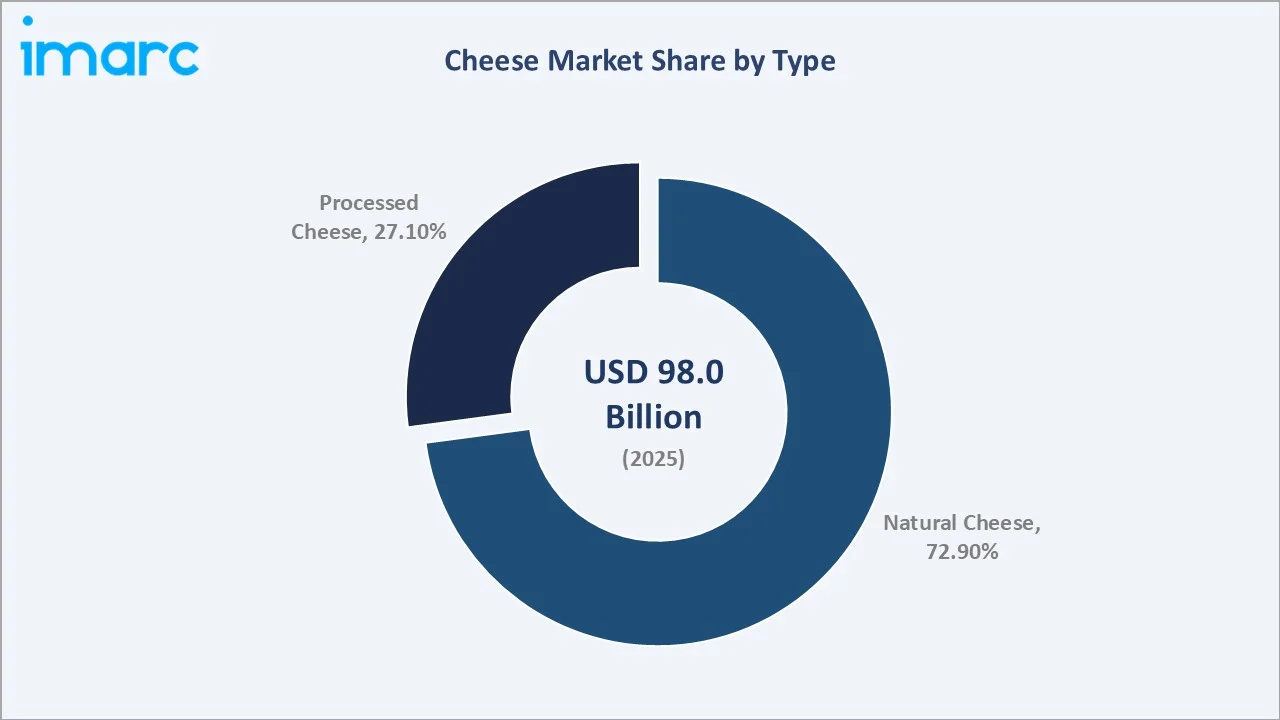

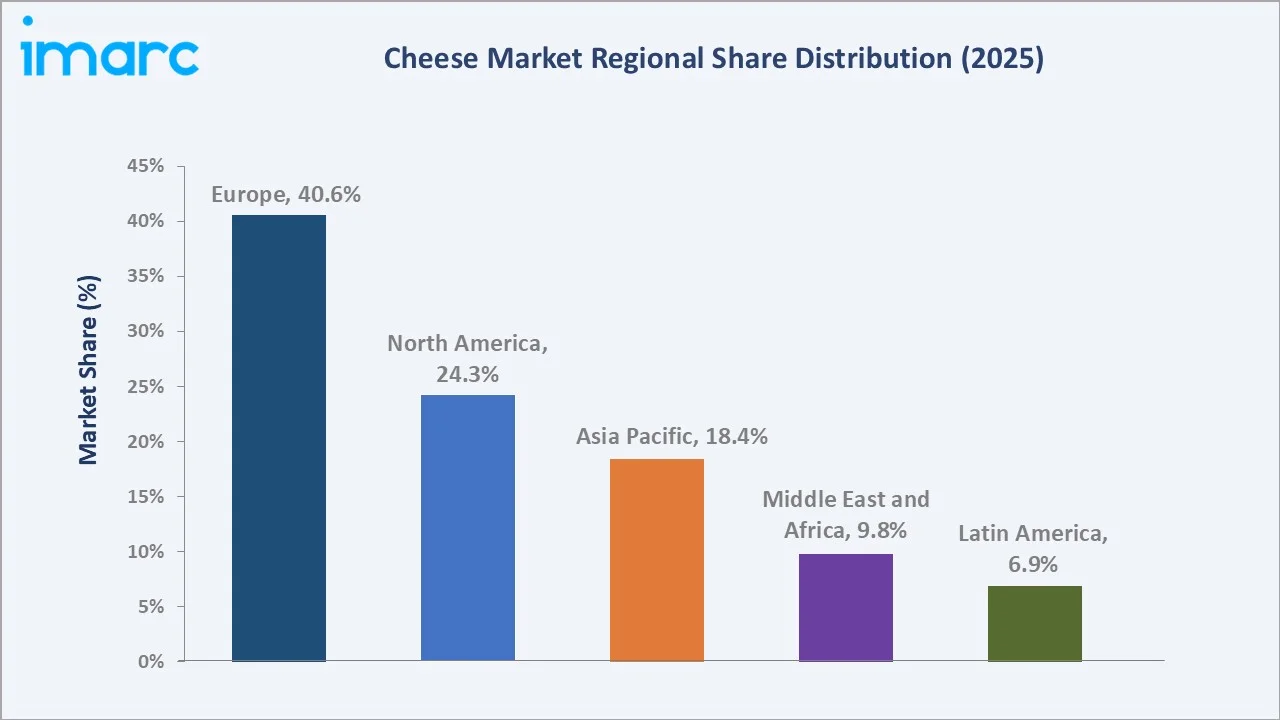

The global cheese market reached a value of USD 98.0 Billion in 2025 and is projected to reach USD 154.4 Billion by 2034, exhibiting a CAGR of 5.00% during the forecast period 2026-2034. Growth is driven by rising consumer demand for diverse dairy-based products, the expanding popularity of convenience and ready-to-eat (RTE) foods, and the growing integration of cheese in foodservice formats including pizza, burgers, pasta, and fast-casual dining globally. Europe dominates the market with a 40.6% share in 2025, reflecting deep cultural cheese traditions, diverse regional variety, and mature dairy infrastructure. Cow milk is the leading raw material at 91.4% (2025), while natural cheese commands a 72.9% type share. The market is projected to reach USD 125.08 Billion by 2030.

Market Snapshot

|

Metric |

Value |

|

Market Size (2020) |

USD 76.79 Billion |

|

Market Size (2025) |

USD 98.0 Billion |

|

Market Size (2030) |

USD 125.08 Billion |

|

Forecast Market Size (2034) |

USD 154.4 Billion |

|

CAGR (2026-2034) |

5.00% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Region |

Europe (40.6%, 2025) |

|

Fastest Growing Region |

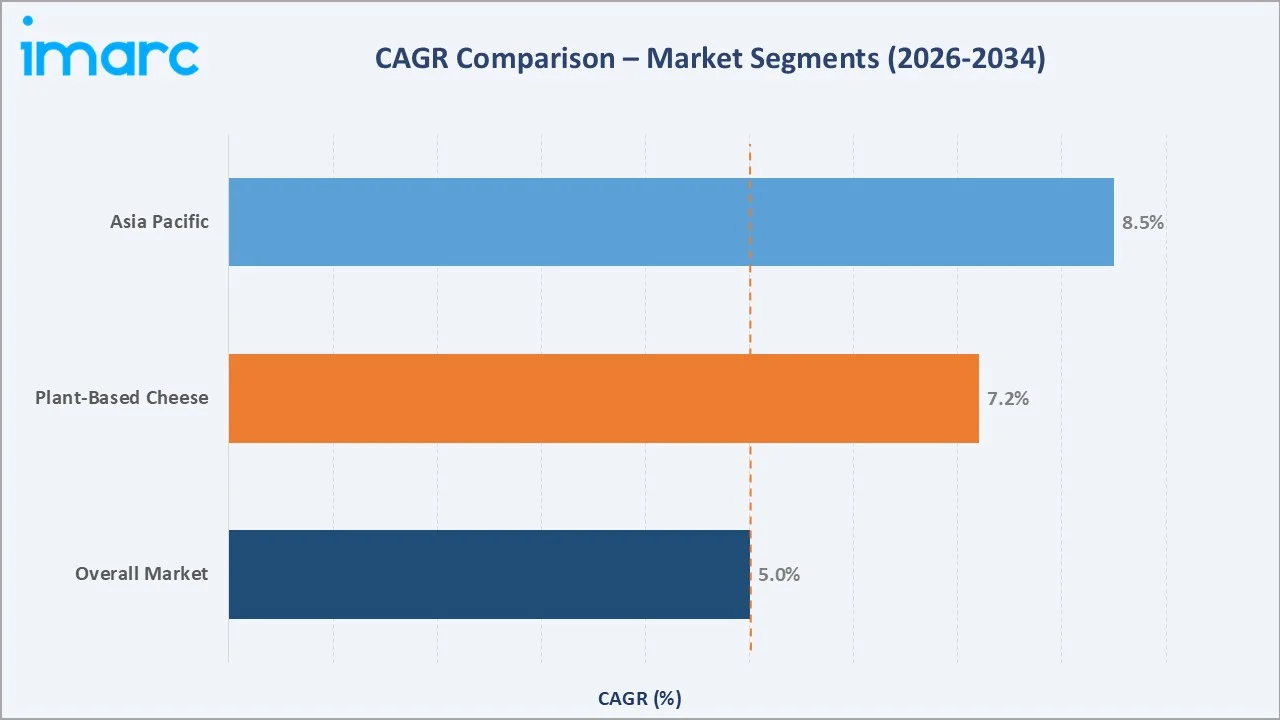

Asia Pacific (~8.5% CAGR) |

|

Dominant Milk Source |

Cow Milk (91.4%, 2025) |

|

Leading Cheese Type |

Natural Cheese (72.9%, 2025) |

The market's growth from USD 76.79 Billion in 2020 to USD 98.0 Billion in 2025 represents a 27.6% value increase over the historical period, demonstrating consistent structural demand even through post-pandemic supply chain challenges. The forecast addition of USD 56.4 Billion through 2034 underscores the sustained opportunity across both traditional dairy-intensive markets and rapidly developing consumption growth in Asia Pacific, the Middle East, and Latin America.

To get more information on this market, Request Sample

The 5.00% CAGR through 2034 is underpinned by structural demand across multiple verticals, foodservice applications (particularly pizza and fast food QSRs), rising protein-conscious retail consumption, and the emergence of plant-based and specialty cheese segments growing at 7–10% annually within the broader category.

Executive Summary

The global cheese market stood at USD 98.0 Billion in 2025, underpinned by cheese's unparalleled versatility as a food ingredient, its deep cultural integration across European, North American, and increasingly Asian and Middle Eastern cuisines, and the growing adoption of dairy-rich diets in rising-income emerging markets. The market is forecast to reach USD 154.4 Billion by 2034 at a CAGR of 5.00%, passing USD 125.08 Billion by 2030. Europe commands a 40.6% share (2025), anchored by France, Germany, Italy, the Netherlands, and the UK as both major producers and consumers of premium natural cheeses. Cow milk remains the dominant raw material at 91.4%, followed by buffalo milk (4.8%) and goat milk (2.6%). Natural cheese leads type segmentation at 72.9% versus processed at 27.1%. North America (24.3%), Asia Pacific (18.4%), the Middle East and Africa (9.8%), and Latin America (6.9%) complete the regional landscape.

Key Market Insights

|

Insight |

Data |

|

Leading Milk Source |

Cow Milk – 91.4% (2025) |

|

Leading Cheese Type |

Natural Cheese – 72.9% (2025) |

|

Fastest Growing Type |

Plant-Based Cheese (~7–10% CAGR) |

|

Leading Region |

Europe – 40.6% (2025) |

|

Fastest Growing Region |

Asia Pacific (~8.5% CAGR) |

|

Top Product by Volume |

Cheddar – 32.4% of market (2025) |

|

Top Companies |

Lactalis, Kraft Heinz, Arla Foods, Fonterra, FrieslandCampina, Saputo |

Key Analytical Observations Supporting the Above Data:

- Europe's 40.6% market dominance (2025) reflects the continent's status as both the world's largest cheese producing and consuming region, with France alone producing over 1,200 distinct cheese varieties and the EU's Protected Designation of Origin (PDO) framework preserving the premium positioning of European artisanal cheeses in global export markets.

- Cow milk’s 91.4% share (2025) reflects global dairy farming’s structural concentration around bovine production, while buffalo milk’s 4.8% share is particularly significant in South Asia and Italy (mozzarella di bufala production), and goat milk at 2.6% supports the premium specialty cheese segment.

- Natural cheese’s 72.9% leadership reflects consumer preference for minimally processed, full-flavor dairy experiences, particularly in European and North American premium retail segments where artisanal, aged, and PDO-certified varieties command significant price premiums of 40–80% over commodity processed counterparts.

- Cheddar leads product type share at 32.4% (2025) and is the most-consumed cheese variety in the U.S. and UK, while feta (11.2%) benefits from its Mediterranean diet association and growing premium positioning in foodservice and retail salad bars.

Global Cheese Market Overview

Cheese is one of humanity's oldest and most diverse food products, comprising over 1,800 recognized varieties globally produced from the milk of cows, buffaloes, goats, sheep, and other ruminants. The global ecosystem spans raw milk production, standardized cheese manufacturing at industrial scale, artisanal small-batch production, aging and maturing facilities, cold chain logistics, and multi-channel retail and foodservice distribution. As of 2025, the market is valued at USD 98.0 Billion and encompasses natural varieties including mozzarella, cheddar, parmesan, gouda, brie, and feta alongside processed cheese formats including slices, spreads, and culinary blends used across QSR, bakery, and convenience food manufacturing. Cheese's exceptional macronutrient profile, high protein (15–30g/100g), calcium, and fat, positions it as a key ingredient in protein-rich diet trends, while its culinary versatility across global cuisines ensures sustained cross-segment demand expansion through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

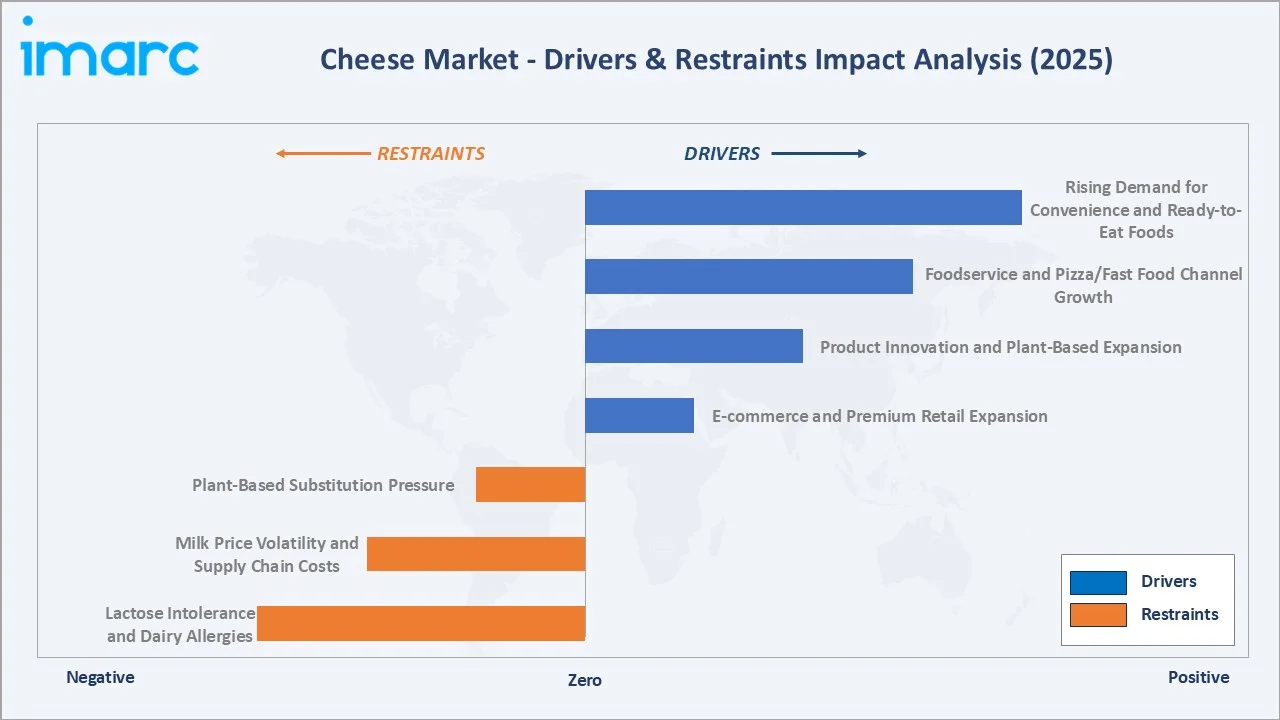

Market Drivers

- Rising Demand for Convenience and Ready-to-Eat Foods: Busy urban lifestyles are driving sustained demand for convenient cheese formats including pre-sliced, shredded, individually wrapped, and portion-controlled products. Cheese's extended shelf life compared to other fresh dairy products, combined with its high culinary versatility, makes it a preferred ingredient across meal preparation, snacking, and on-the-go consumption occasions in both developed and emerging markets.

- Foodservice and Pizza/Fast Food Channel Growth: Cheese is an indispensable ingredient across the global foodservice sector. QSR chain expansion in Asia Pacific, MEA, and Latin America is driving high-volume procurement of processed cheese slices for burgers, sandwiches, and wraps, supporting the growth of the Cheese industry in Latin America. Global casual dining expansion further sustains premium cheese demand for salads, pasta dishes, and cheese-centric appetizers.

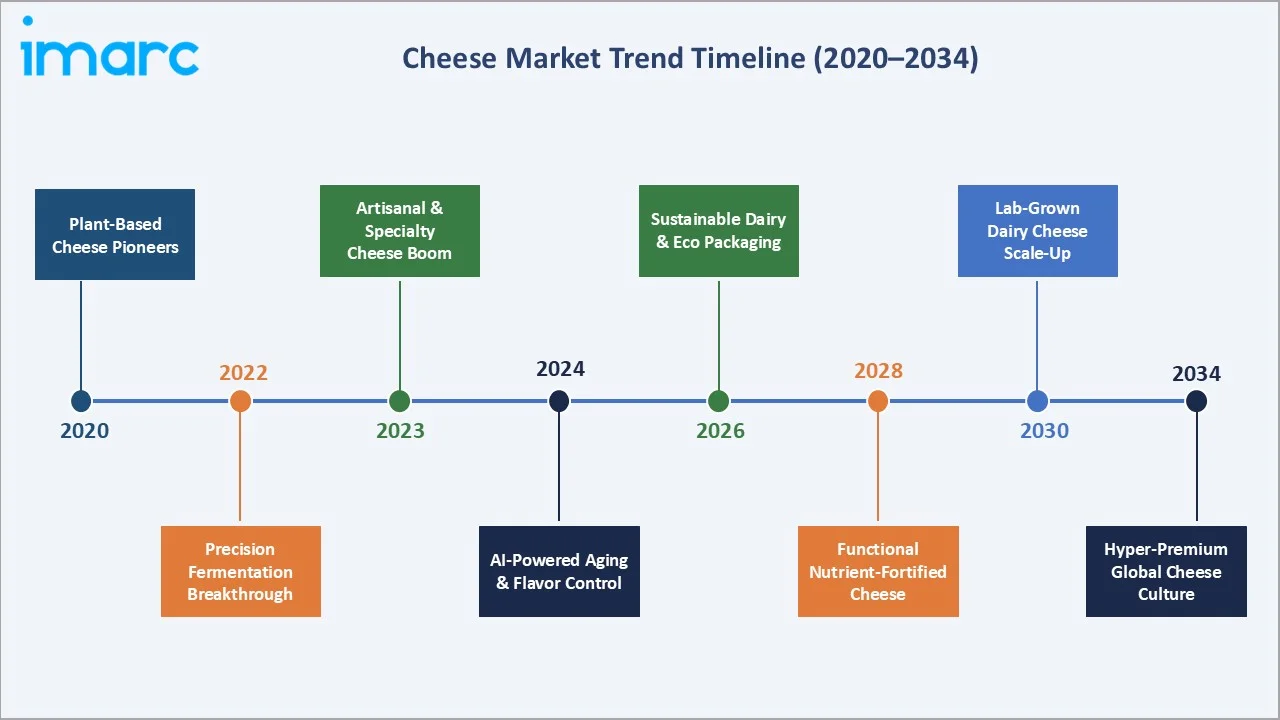

- Product Innovation and Plant-Based Expansion: Technological breakthroughs in plant-based cheese formulation are creating new market segments. In March 2023, Daiya Foods announced precision fermentation investment for dairy-identical plant-based cheese. Armored Fresh (Yangyoo subsidiary) introduced almond-milk-based plant-based cheese to U.S. national grocery retailers in October 2022. PlantWise launched vegan cheese shreds, spreads, and nuggets using natural fermentation producing authentic dairy-like flavor profiles. These innovations are expanding the addressable market to lactose-intolerant and vegan consumers without cannibalizing traditional dairy cheese demand.

- E-commerce and Premium Retail Expansion: Specialty and artisanal cheese DTC e-commerce has emerged as a high-growth distribution channel, enabling small-batch producers and regional PDO varieties to reach global consumers. Premium cheese subscriptions, curated cheeseboards, and gifting formats are growing significantly through online retail platforms, commanding significant price premiums over standard retail and expanding the overall category value.

Market Restraints

- Lactose Intolerance and Dairy Allergies: Approximately 65-70% of the global adult population has some degree of lactose malabsorption, with even higher intolerance rates in East Asia, West Africa, and parts of South Asia. This structural barrier limits cheese adoption in large populations across Asia Pacific and Africa, constraining the market's full addressable growth potential.

- Milk Price Volatility and Supply Chain Costs: Cheese production is capital-intensive and highly sensitive to raw milk price fluctuations. Commodity milk prices can vary significantly every year, driven by feed costs, climate impacts on pasture, and energy costs for refrigeration and processing. These input cost fluctuations compress manufacturer margins and create retail price volatility that can dampen consumer demand.

- Plant-Based Substitution Pressure: While plant-based cheese currently represents nearly 3% of market value, its 7–10% annual growth rate is attracting significant retail shelf space and consumer trial. In environmentally conscious consumer segments, particularly in Northern Europe, North America, and Australia, plant-based alternatives are positioning as ethical substitutes that create structural headwinds for traditional dairy cheese volume growth.

Market Opportunities

- Emerging Market Demand Expansion: Asia Pacific, the Middle East, and Latin America collectively represent the highest-growth opportunity for cheese market expansion through 2034. China's cheese consumption is growing at approximately 12% annually, driven by Western cuisine adoption, pizza QSR expansion, and rising disposable incomes in Tier-1 and Tier-2 cities. India's organized dairy processing sector is expanding cheese production for both domestic use and export.

- Artisanal and PDO Premium Segment Growth: Protected Designation of Origin (PDO) cheeses including Parmigiano-Reggiano, Grana Padano, Comté, Gruyère, and Manchego command at least 5% price premiums over standard equivalent cheeses in export markets. The growing consumer preference for authentic, traceable, and terroir-linked food products is expanding the global addressable market for European PDO cheeses across North America, Asia Pacific, and the Middle East.

- Functional and Fortified Cheese Innovation: Nutrient-fortified cheese formats including calcium-enhanced, vitamin-D-fortified, probiotic-enriched, and reduced-sodium varieties are creating new health-positioning opportunities that expand cheese's addressable consumer base. Reduced-fat, lactose-free, and protein-concentrated formats are growing in mainstream retail segments targeting health-conscious consumers.

Market Challenges

- Cold Chain Infrastructure Requirements: Natural cheese requires continuous refrigerated storage throughout the supply chain, from production to consumption. Cold chain investment requirements limit market penetration in regions with inadequate refrigeration infrastructure, including parts of Sub-Saharan Africa, South Asia, and rural Southeast Asia. Processed cheese formats mitigating cold chain requirements are growing in these markets but at lower value contribution.

- Sustainability and Dairy Carbon Footprint: Cheese production carries a significant environmental footprint, approximately 8–16 kg of CO2 equivalent per kg of hard cheese produced, varying in case of different types. Growing consumer and regulatory pressure on dairy's climate impact is driving investment in regenerative dairy farming practices, methane reduction initiatives, and carbon footprint labeling that adds operational complexity and cost.

- Fragmented Artisanal Sector Formalization: While the artisanal cheese segment is high-value, its fragmented structure of small-scale producers with limited capital, food safety compliance capacity, and export certification capability constrains its scalability and creates quality consistency challenges for retail and foodservice buyers.

Emerging Market Trends

The global cheese market is being reshaped by five converging trends that are redefining product innovation, consumer positioning, and competitive dynamics across both traditional dairy and emerging alternative-protein categories through 2034.

1. Plant-Based and Precision Fermentation Cheese Innovation

The plant-based cheese segment is the category's highest-growth frontier, attracting significant R&D and venture investment. Precision fermentation, using microorganisms to produce dairy proteins including casein and whey without animals is enabling the creation of plant-based cheeses that melt, stretch, and taste indistinguishably from dairy originals. Daiya Foods' March 2023 fermentation technology investment, Agrocorp's HerbY-Cheese launch in Singapore, and PlantWise's natural-fermentation-based vegan shreds collectively illustrate the sector's rapid maturation from novelty to mainstream commercial relevance.

2. Artisanal, Specialty, and PDO Cheese Premiumization

Consumer demand for authentic, provenance-linked, and craft food experiences is driving strong growth in premium artisanal cheese. Protected Designation of Origin (PDO) varieties including Parmigiano-Reggiano, Comté, and Manchego are achieving record export revenues. Specialty cheese shops, curated online subscription boxes, and chef-curated cheeseboards are expanding premium retail distribution, commanding significant price points above commodity equivalents.

3. Technological Innovation in Cheese Manufacturing

Precision in cheese-making is advancing through the adoption of micellar casein concentrates for enhanced protein retention and texture control, automated smart ripening facilities with IoT-monitored humidity and temperature management, and AI-driven quality control systems for consistent grading. In March 2023, PlantWise deployed natural fermentation processes creating authentic cheese flavor profiles comparable to dairy, demonstrating how biotechnology is converging with traditional cheese-making craft knowledge.

4. Sustainability and Regenerative Dairy Practices

Major dairy processors are investing in carbon footprint reduction, regenerative grazing programs, and sustainable packaging to meet both regulatory requirements and evolving consumer preferences. Arla Foods' net-zero target, FrieslandCampina's farmer sustainability programs, and Lactalis's packaging reduction commitments are reshaping procurement and operational standards across the supply chain.

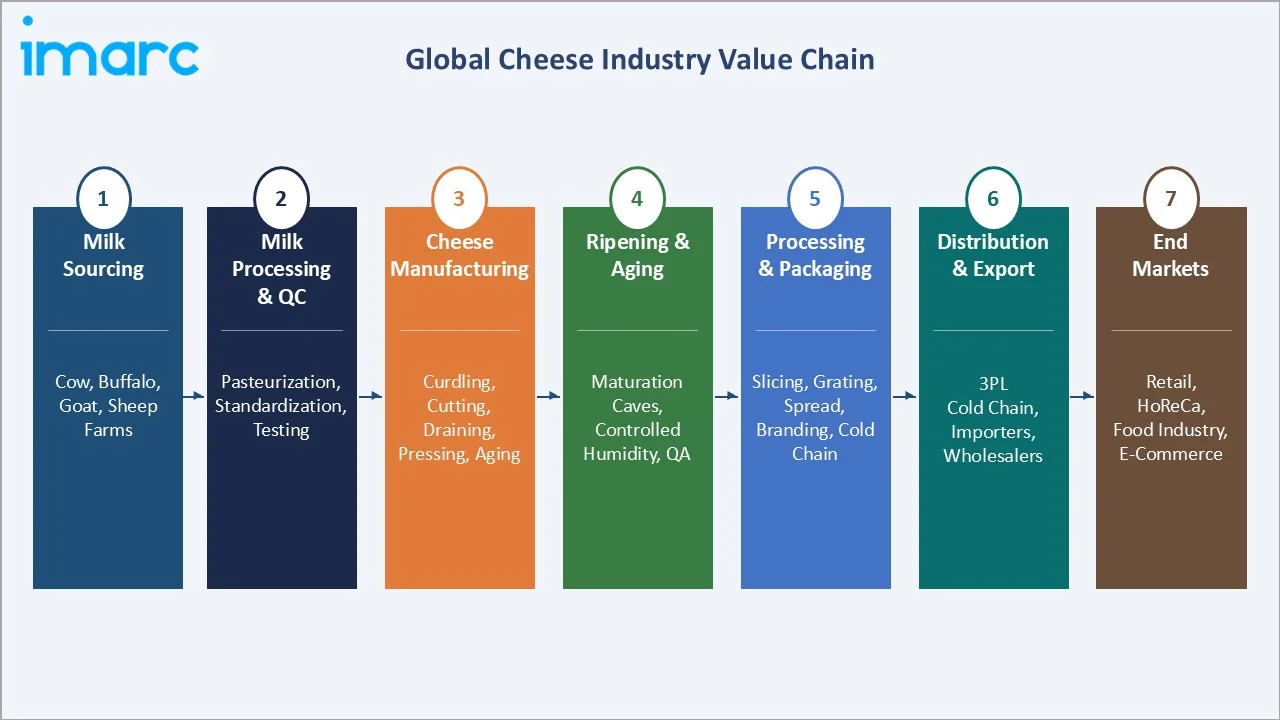

Industry Value Chain Analysis

The cheese industry value chain spans seven interconnected stages from farm-level milk production through to end-market consumption. Each stage requires specialized expertise, temperature-controlled infrastructure, and quality management systems to preserve the sensory, safety, and nutritional attributes of cheese through its journey from farm to table.

|

Stage |

Key Activities |

Representative Players |

|

Milk Sourcing |

Raw milk collection from cow, buffalo, goat, sheep farms; quality testing; farm management |

Dairy cooperatives (Arla, FrieslandCampina), contract farms, independent producers |

|

Milk Processing & QC |

Pasteurization, standardization, separation, microbiological testing, HACCP compliance |

Fonterra, Hochland, Lactalis processing facilities, cooperative intake stations |

|

Cheese Manufacturing |

Curdling, cutting, draining, pressing, salting, molding; variety-specific processes |

Lactalis, Kraft Heinz, Saputo, Emmi, regional specialty manufacturers |

|

Ripening & Aging |

Controlled cave or chamber aging; humidity/temperature monitoring; rind development; grading |

Parmigiano-Reggiano consortia, Comté affinage caves, Emmi aging facilities |

|

Processing & Packaging |

Slicing, grating, spreading, portioning; MAP packaging; branding; cold chain preparation |

Bel Group, Hochland, private-label processors, Kraft packaging lines |

|

Distribution & Export |

Cold chain 3PL, international cold shipping, import clearance, wholesale |

Lactalis export division, Dairy Farmers of America, Arla export network |

|

End Markets |

Retail supermarkets, specialty stores, foodservice/HoReCa, food manufacturing, e-commerce |

Carrefour, Walmart, Sysco, Domino's, Nestlé food ingredient division |

Technology Landscape in the Cheese Industry

Precision Fermentation and Biotechnology

Precision fermentation, using genetically engineered yeast, fungi, or bacteria to produce animal-identical proteins including casein and whey without dairy is enabling the creation of 'real' dairy cheese proteins that can melt, stretch, and behave identically to traditional dairy. Companies including Perfect Day and New Culture are advancing precision fermentation cheese proteins toward commercial scale, targeting the premium plant-based consumer while delivering the sensory experience of conventional dairy cheese at potentially lower cost-per-unit.

Smart Manufacturing and IoT-Enabled Aging

Automated sensory monitoring systems using IoT sensors, computer vision, and acoustic analysis are transforming the cheese aging process. Real-time data on rind development, moisture content, pH levels, and microbial activity enable cheesemakers to optimize aging parameters with precision previously achievable only by highly experienced affinage specialists. These systems are enabling large-scale industrial producers to achieve artisanal-quality consistency at volume.

Advanced Packaging Technology

Modified atmosphere packaging (MAP), vacuum skin packaging (VSP), and active packaging incorporating antimicrobial agents are extending cheese shelf life significantly, reducing food waste across the supply chain. Resealable formats, portion-control single-serve packaging, and recyclable sustainable packaging materials are responding to both consumer convenience demands and regulatory sustainability requirements across European and North American markets.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Source |

Cow Milk |

91.4% |

2025 |

|

Type |

Natural |

72.9% |

2025 |

|

Product |

Cheddar |

32.4% |

2025 |

|

Format |

Slices |

31.8% |

2025 |

| Distribution Channel | Supermarkets and Hypermarkets | 35.8% | 2025 |

|

Region |

Europe |

40.6% |

2025 |

By Source

The global cheese market is segmented by raw milk source, with cow milk maintaining dominant position while buffalo, goat, and other alternative milk sources represent premium and specialty high-growth sub-segments:

To access detailed market analysis, Request Sample

Goat milk cheese at 2.6% (2025) is a premium natural source segment, driven by growing consumer preference for artisanal, earthy-flavored varieties and the perception of goat cheese as more digestible and less allergenic than cow milk alternatives. France and Spain are the leading goat cheese producers, with chèvre and manchego among the most rapidly expanding PDO export categories.

By Type

Natural cheese dominates at 72.9% (2025), reflecting consumer preference for authentic, minimally processed dairy in premium retail and foodservice. Processed cheese at 27.1% maintains significant market presence through its critical role in QSR formats, burger and sandwich cheese slices, nacho cheese sauces, and spreadable processed varieties and in emerging market convenience food applications.

The natural-to-processed ratio is shifting toward natural cheese in developed markets as consumers increasingly prioritize clean-label, minimally processed food choices. However, in emerging markets including Southeast Asia, the Middle East, and Sub-Saharan Africa, processed cheese is growing faster due to its convenience, extended shelf life without refrigeration, and affordability relative to imported natural varieties.

Regional Market Insights

The global cheese market exhibits pronounced regional differentiation in production heritage, consumption patterns, preferred varieties, and growth trajectories. Europe's cultural depth in cheese production creates structural market dominance, while Asia Pacific's growth momentum is redefining the industry's geographic expansion priorities.

Europe's 40.6% dominance (2025) reflects the continent's extraordinary diversity, France alone produces over 1,200 named cheese varieties, and the EU's PDO framework protects over 180 European cheese designations, creating a commercial ecosystem where geography-linked premium products command price premiums that sustain high market value even at mature consumption levels.

Competitive Landscape

The global cheese market is moderately concentrated at the large-scale industrial processing tier, with Lactalis Group, Kraft Heinz, Arla Foods, and Fonterra collectively accounting for approximately 25–30% of global processed cheese revenues. However, the market’s natural cheese segment, representing 72.9% of total value is highly fragmented, with thousands of artisanal, cooperative, and regional producers competing across geographically defined PDO and specialty segments.

|

Company |

Key Brand(s) |

Market Position |

Primary Strategy |

|

Lactalis Group |

Président, Galbani |

Global Market Leader |

Acquisition-driven portfolio expansion, global export network, premium brand management |

|

Kraft Heinz Company |

Kraft, Philadelphia, Velveeta |

Leader – Processed & Cream |

QSR processed cheese supply, Philadelphia cream cheese global leadership, brand renovation |

|

Arla Foods |

Arla, Castello |

Leader – Natural & Cooperative |

Farmer-owned cooperative model, sustainability leadership, premium natural cheese positioning |

|

Fonterra Co-op |

Anchor, Mainland, Kapiti |

Leader – Oceania & Export |

New Zealand dairy export dominance, Asia Pacific growth, ingredient-grade mozzarella |

|

FrieslandCampina |

Milner, Maaslander |

Leader – Netherlands/Europe |

Dutch cheese export leadership, sustainability programs |

|

Saputo Inc. |

Saputo, Woolwich Dairy |

Leader – North America |

North American mozzarella scale, acquisition strategy, specialty cheese portfolio |

|

Emmi Group |

Emmi, Kaltbach, Roth |

Challenger – Premium |

Swiss premium positioning, specialty cave-aged cheeses, U.S. artisanal market entry |

|

Bel Group |

Babybel, Laughing Cow |

Challenger – Snack/Processed |

Snack cheese innovation, plant-based alternatives, global emerging market distribution |

|

Kerry Group |

Kerry Cheese |

Established – Ingredients |

Food ingredient focus, processed cheese for foodservice manufacturing, B2B supply |

|

Dairy Farmers of America |

Various |

Cooperative – USA |

U.S. dairy cooperative, mozzarella for pizza chains, commodity and specialty supply |

Lactalis Group, through its acquisitions of Galbani (Italy), Parmalat (global dairy), and control of numerous European and emerging-market cheese brands, has assembled the world's most geographically diversified dairy portfolio. Its Président brand's global premium positioning across France, Asia, and North America exemplifies how brand investment combined with supply chain scale creates durable competitive moat in an otherwise commodity-adjacent category.

Key Company Profiles

Lactalis Group

Lactalis Group is the world's largest dairy company, headquartered in Laval, France, with annual revenues exceeding USD 31 Billion in 2023. Its cheese portfolio spans premium natural varieties (Président, Galbani) to commodity-scale mozzarella and processed cheese across 100+ countries.

- Product Portfolio: Président (Brie, Camembert, Emmental, Butter), Galbani (Mozzarella, Ricotta, mascarpone), Lactel, Societe (Roquefort), and numerous regional cheese brands acquired globally.

- Recent Developments: Continued global acquisition strategy with dairy assets in Asia, Latin America, and Africa; advanced cold chain export infrastructure for premium cheese in emerging Asian markets.

- Strategic Focus: Acquisition-led global portfolio diversification, premium brand development across international markets, and sustainable dairy sourcing commitments.

Kraft Heinz Company

Kraft Heinz is the world's largest processed cheese company, with its Kraft brand dominating processed cheese slices, Velveeta commanding nacho sauce, and Philadelphia leading global cream cheese with operations across 40+ countries.

- Product Portfolio: Kraft Singles (processed slices), Velveeta (processed block and sauce), Philadelphia (cream cheese), Cracker Barrel (natural cheddar), and private-label manufacturing.

- Recent Developments: Philadelphia cream cheese expanded into new flavor and format variants globally in 2024; Kraft Singles reformulated with reduced artificial ingredients for clean-label repositioning.

- Strategic Focus: Processed cheese QSR supply chain optimization, Philadelphia global premium brand expansion, clean-label reformulation, and emerging market processed cheese adoption.

Arla Foods

Arla Foods is a farmer-owned cooperative headquartered in Viby, Denmark. It is the largest dairy company in Scandinavia and a leading natural cheese producer in Europe.

- Product Portfolio: Arla Natural Cheese (Gouda, Havarti, Edam), Castello (premium specialty cheeses including blue, brie, goat), Lurpak (butter), and ingredient-grade dairy for food manufacturers.

- Recent Developments: Launched Castello plant-based cheese alternatives across European markets in 2024; advanced Arla's climate sustainability target toward 30% carbon reduction by 2030.

- Strategic Focus: Premium natural cheese positioning (Castello), sustainability leadership, Middle East/Asia Pacific export growth, and plant-based dairy innovation.

Fonterra Co-operative Group

Fonterra is the world's largest dairy exporter, headquartered in Auckland, New Zealand. Its cheese operations supply both branded consumer products and ingredient-grade mozzarella for global pizza chains.

- Product Portfolio: Anchor (consumer dairy NZ/Asia), Mainland (natural cheese NZ), Kapiti (premium specialty), and bulk ingredient mozzarella and cheddar for food manufacturing globally.

- Recent Developments: Accelerated Asia Pacific branded cheese strategy; invested in sustainable farming programs for Fonterra's 10,000+ NZ farmer-owners targeting lower emissions per kilogram of milk solids.

- Strategic Focus: Asia Pacific consumer brand growth, ingredient-grade mozzarella export leadership, sustainable dairy farming, and New Zealand dairy industry representation.

Market Concentration Analysis

The global cheese market is structurally bifurcated: the industrial processed cheese and commodity mozzarella/cheddar segment is relatively concentrated, with the top five processors (Lactalis, Kraft Heinz, Arla, Fonterra, Saputo) controlling approximately 30–35% of global processed cheese revenues. The natural cheese segment, by contrast, is highly fragmented, with thousands of European, North American, and Oceanian dairy cooperatives, artisanal producers, and regional cheese specialists competing across geographically defined product niches.

Europe's cheese market is particularly fragmented at the artisanal and cooperative tier, France's Interprofession du Gruyère, Italy's Parmigiano-Reggiano and Grana Padano Consortia, and Spain's cheese DO system each represent collective producer organizations protecting specific geographical and production-method designations that resist commodity pricing and consolidation pressure. These PDO structures create durable competitive positions for thousands of small and medium-scale producers within clearly defined geographic and quality parameters.

Investment & Growth Opportunities

Fastest Growing Segments

Plant-based and precision fermentation cheese, premium artisanal and PDO natural cheese, goat milk and specialty alternative milk cheese, and functional/fortified cheese formats represent the highest-growth investment vectors through 2034.

Emerging Market Expansion

China's cheese market is growing at approximately 12% annually and represents an incremental opportunity. India's expanding organized dairy processing sector, leveraging its world-class buffalo and cow milk supply base is creating significant paneer and mozzarella production investment opportunities. The Middle East's Halal-certified cheese market is growing at 8–10% annually, with imported European feta and cream cheese and locally produced fresh white cheese varieties capturing rapidly rising foodservice and retail demand.

Technology and Innovation Investment Trends

- Precision fermentation dairy protein companies including Perfect Day, New Culture, and Nobell Foods are attracting significant VC investment for casein and whey production technologies enabling animal-free cheese at commercial scale.

- Aging and maturing technology innovators developing IoT-monitored smart caves, AI-powered rind management, and data-driven affinage optimization are enabling artisanal quality at industrial scale, a previously unavailable combination.

- E-commerce and DTC specialty cheese platforms are capital-efficiently capturing premium consumer segments, with platforms including Murray's Cheese, Cheesemonger's Choice, and iGourmet demonstrating the commercial viability of artisanal cheese subscription and gifting businesses at scale.

Future Market Outlook 2026-2034

The global cheese market is entering a decade of value-driven expansion, with structural demand growth anchored by foodservice channel expansion, rising protein-rich diet adoption, and category extension through plant-based and functional innovation.

Innovation will be the primary value creation lever of the next decade. Precision fermentation cheese proteins are projected to achieve cost parity with conventional dairy cheese for specific applications by 2028–2030, enabling plant-based cheese to enter the food manufacturing and foodservice ingredient market at competitive price points. This development will simultaneously create new market segments and put modest pressure on commodity cheese pricing in high-volume industrial applications. Natural and artisanal cheese will remain structurally protected by provenance, terroir, and aging-based value propositions that fermentation cannot replicate.

Research Methodology

Primary Research

Primary research for this report included structured interviews with over 170 industry participants in 2024–2025, comprising cheese manufacturers, dairy cooperative executives, specialty cheese retailers, foodservice procurement managers, food technology researchers, and end consumers across Europe, North America, Asia Pacific, and the Middle East.

Secondary Research

Secondary research encompassed a comprehensive review of company annual reports, European PDO registration databases, USDA dairy export statistics, FAO dairy production data, trade publications (Dairy Industries International, Cheese Connoisseur, CNIEL), EU dairy market reports, and industry databases (Euromonitor, Mintel, IRI). Over 320 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of bottom-up dairy supply modeling and top-down consumption demand analysis, incorporating milk production projections by species, cheese yield efficiency factors, per-capita consumption trends by region, foodservice demand indicators, and export trade flow analysis. Scenario analysis was performed across base, optimistic, and conservative cases to account for commodity price and climate-related supply uncertainty.

Cheese Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, Million Metric Tons |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sources Covered | Cow Milk, Buffalo Milk, Goat Milk, Others |

| Types Covered | Natural, Processed |

| Products Covered | Mozzarella, Cheddar, Feta, Parmesan, Roquefort, Others |

| Formats Covered | Slices, Diced/Cubes, Shredded, Blocks, Spreads, Liquid, Others |

| Distribution Channels Covered | Supermarkets And Hypermarkets, Convenience Stores, Specialty Stores, Online, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Argentina, Colombia, Chile, Peru, Turkey, Saudi Arabia, Iran, United Arab Emirates |

| Companies Covered | Lactalis Group, Kraft Heinz Company, Arla Foods, Fonterra Co-op, FrieslandCampina, Saputo Inc., Emmi Group, Bel Group, Kerry Group, Dairy Farmers of America, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the cheese market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global cheese market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the cheese industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Global Cheese Market Report

The global cheese market was valued at USD 98.0 Billion in 2025 and is projected to reach USD 154.4 Billion by 2034.

The market is forecast to grow at a CAGR of 5.00% during 2026-2034, driven by foodservice expansion, convenience food demand, protein-rich diet trends, and emerging market consumption growth.

Europe dominates with a 40.6% market share in 2025, anchored by deep cheese culture, PDO premium systems, mature dairy infrastructure, and both large-scale processing and artisanal production traditions.

Asia Pacific is the fastest-growing region at an estimated ~8.5% CAGR, driven by Western cuisine adoption, QSR pizza expansion, and rising disposable incomes in China, India, and Southeast Asia.

Cow milk leads at 91.4% 2025, reflecting global dairy farming’s bovine concentration, followed by buffalo milk (4.8%) for mozzarella di bufala and South Asian cheese production, and goat milk (2.6%) for premium artisanal specialty varieties.

Natural cheese (72.9% share, 2025 is made directly from milk through curdling, draining, and aging. Processed cheese (27.1%) blends natural cheese with emulsifying salts and additives for consistent melt, extended shelf life, and uniform flavor, ideal for QSR and convenience food applications.

Cheddar leads at 32.4% 2025, primarily driven by its essential role in the global pizza industry.

Leading companies include Lactalis Group, Kraft Heinz Company, Arla Foods, Fonterra Co-op, FrieslandCampina, Saputo Inc., Emmi Group, Bel Group, Kerry Group, and Dairy Farmers of America. etc.

High-growth opportunities include plant-based and precision fermentation cheese (7–10% CAGR), premium artisanal and PDO cheese premiumization, Asia Pacific market entry (China, India), functional fortified cheese formats, and e-commerce specialty cheese DTC platforms.

Key challenges include lactose intolerance limiting Asian and African market penetration, raw milk price volatility compressing manufacturer margins, cold chain infrastructure requirements in emerging markets, sustainability and dairy carbon footprint pressures, and plant-based substitution in environmentally conscious consumer segments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)