Commercial Drones Market Size, Share, Trends and Forecast by Weight, System, Product, Mode of Operation, Application, End Use, and Region, 2026-2034

Commercial Drones Market Size and Share:

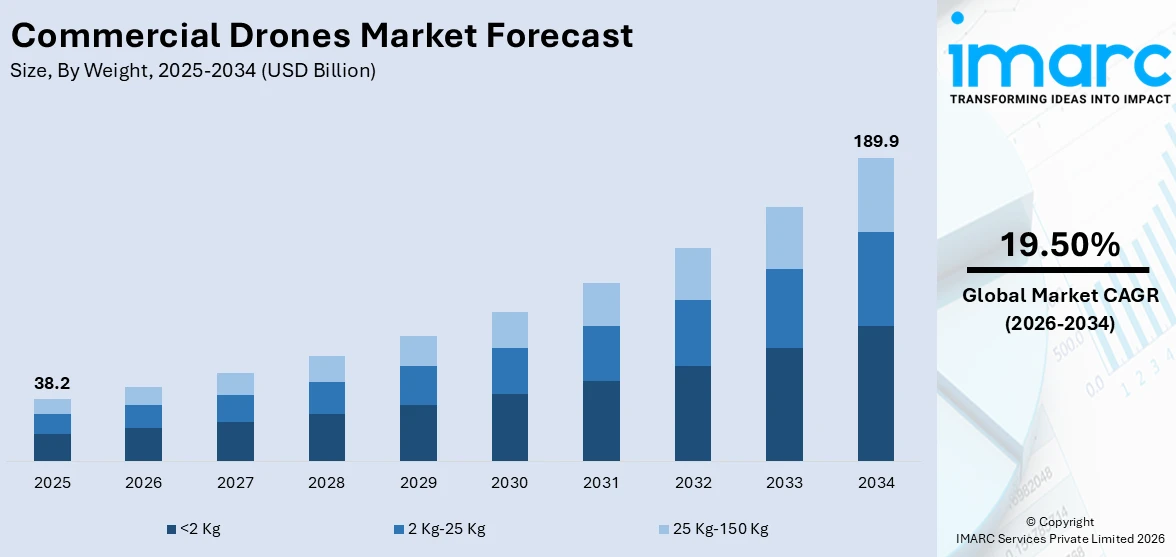

The global commercial drones market size was valued at USD 38.2 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 189.9 Billion by 2034, exhibiting a CAGR of 19.50% during 2026-2034. North America currently dominates the market, holding a significant market share of 39.7% in 2025. Because of the sophisticated regulatory frameworks, significant investments in drone technology, and broad use in sectors like agriculture, logistics, and surveillance, North America is the largest market. Moreover, the robust ecosystem of creative manufacturers and technology suppliers is propelling the market growth in the region.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 38.2 Billion |

| Market Forecast in 2034 | USD 189.9 Billion |

| Market Growth Rate 2026-2034 | 19.50% |

Improvements in drone technology, such as longer battery life, autonomous navigation, and better image capabilities, are driving the demand for commercial drones. Due to their effectiveness and affordability, they are becoming more popular in sectors including construction, logistics, and agriculture. The industry is expanding even more quickly due to the growing need for precision farming, aerial data collection, and infrastructure inspection. Globally, supportive government policies and regulatory easing promote the use of drones for commercial purposes. Drones' operational capabilities are further enhanced by rising investments in drone research and development (R&D) activities as well as the incorporation of AI and machine learning (ML) into drones. The demand for quicker delivery services and expanding e-commerce are major factors propelling the market growth.

To get more information on this market Request Sample

The United States has emerged as a key market that can be attributed to favorable legislative developments, such the FAA's Part 107 regulations, which streamline commercial drone operations. Both the public and private sectors are making significant investments in drone technology, which encourages innovations. With applications in crop monitoring, infrastructure inspection, and last-mile delivery, the extensive use of drones in sectors, such precision agriculture, energy, construction, and logistics, is propelling the market expansion in the country. The market is also driven by the strong demand for surveillance and reconnaissance from the public safety and defense sectors in the US. Furthermore, the nation's strong tech environment and the presence of significant drone manufacturers and tech companies is spurring innovations. The market is expanding due to the growing interest in combining drones and AI for advanced analytics. As per the IMARC Group’s report, the United States commercial drones market is projected to exhibit a growth rate (CAGR) of 16.10% during 2024-2032

Commercial Drones Market Trends:

Rapid Technological Advancements

The development of technology represents the primary factor improving the commercial drone market scope, transforming capabilities and widening applications. Further evolvements, such as longer flight time, higher payload endurance, and mind integration can improve the performance of drones and open new possibilities in various industries. These technologies improve operational efficiency and provide drones with the capability to focus on more complex operations, ranging from long-distance inspections and parcel delivery services to aerial mapping. Advancements in autonomous navigation and global positioning system (GPS) systems enable precise and efficient operations. The integration of artificial intelligence (AI) and machine learning (ML) allows drones to process data in real-time, enabling applications like predictive analytics and automated decision-making.

Expanding Applications Across Industries

The growing use of commercial drones in infrastructure inspections and agricultural monitoring is offering a favorable market outlook. However, the agriculture sector remains an important field within this area, with drones being used for crop surveillance, soil analysis, and precision agriculture. The meteoric increase in drone certifications shows how they are becoming critical in boosting operational efficiency, data collection, and decision-making processes in several industries. In logistics, drones are being adopted for last-mile delivery, enabling faster and cost-effective shipping solutions. Energy and mining industries leverage drones for pipeline inspection, asset monitoring, and exploration in challenging terrains. Moreover, drones play a critical role in public safety and disaster management, aiding in search-and-rescue missions and surveillance.

Supportive Regulatory Environment

A favorable regulatory framework represents another major growth-inducing factor in commercial drone market growth. As per the Federal Aviation Administration (FAA), to date, 200,000+ commercial drones have been registered in the USA. This very fact shows how drones are widely being used for commercial use. Through the FAA's initiatives including the Part 107 regulation and the USA Integration Pilot Program (IPP), the agency has defined direction and standards for drone operators to integrate unmanned aircraft into the National Airspace System (NAS) safely and responsibly. In an accommodating regulatory setting, companies are given the go-ahead to use drones for creative solutions that in the end boost business growth and productivity across industries.

Growing employment of commercial drones for industrial applications

The increasing deployment of commercial drones in fields like construction, real estate, and security is greatly changing operations by offering improved abilities for surveying, monitoring, and safety. Drones are progressively utilized in construction undertakings for aerial assessments, site evaluations, and progress monitoring, enabling faster and more precise data gathering. In real estate, drones provide vibrant aerial photos that highlight properties from distinct angles, enhancing marketing and sales efforts. Moreover, drones are crucial for enhancing safety by overseeing dangerous zones, performing regular checks on inaccessible infrastructure, and aiding in emergency response situations. The incorporation of drones in these fields is lowering operational expenses, enhancing efficiency, and facilitating real-time decision-making, thereby aiding a wider movement toward automation and innovation in commercial uses. For instance, in 2024, Garuda Aerospace launched its novel innovation, the Trishul Border Patrol Surveillance Drone, which is created to improve security and monitoring efficiency of border security forces.

Commercial Drones Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global commercial drones market, along with forecasts at the global, regional, and country levels for 2026-2034. The market has been categorized based on weight, system, product, mode of operation, application, end use, and region.

Analysis by Weight:

- <2 Kg

- 2 Kg-25 Kg

- 25 Kg-150 Kg

<2 Kg commercial drones lead the market with 78.0% of market share in 2025. The rising interest in drones weighing up to 2 kg is due to their portability, ease of use, and ease of being registered and operated is creating a positive market outlook. The high acceptance of solar-powered drones for a broad range of existing markets is propelling the market growth. Portable drones with acrobatics and dexterity are the best option when it comes to the roles of aerial photography, mapping, surveillance, and inspection of various industries like agriculture, construction, and real estate. On the other hand, regulatory frameworks of the FAA Part 107 rule that provide simplified requirements to operate for businesses is further expanding the use of these drones. Being a lightweight solution with the capability to fly affordably for a variety of purposes, light drones under 2 kilograms are one the key components that will shape the drone market in the future.

Analysis by System:

- Hardware

- Airframe

- Propulsion System

- Payloads

- Others

- Software

Hardware leads the market with 59.0% of market share in 2025. In the commercial drones market, the hardware section is mainly characterized as the technology strictly followed by the increase in the components’ reliability and the regulations. The robustness of private equity funds reflects the expanding use of drone technology across diverse industries. It is through the hardware components, such as airframes, propulsion systems, sensors, and communicating devices, that commercial drones are made to be operable and thus they can be able to deliver their intended roles. For instance, the NASA researchers at Armstrong are developing systems to integrate wireless sensors into aircraft avionics, aiming to increase throughput up to 40 Mbps. The development of drones continues to expand beyond basic applications, and this highlights the necessity for carrying out hardware solutions that can provide longevity, effectiveness and adaptation alongside quickly evolving technologies. Moreover, materials and safety regulations are the other causes which is creating the need for hardware parts that are industrial standard compliant and used to make sure that the drone operations are safe and dependable, thereby fueling the market growth.

Analysis by Product:

- Fixed Wing

- Rotary Blade

- Hybrid

Rotary blade leads the market with 78.4% of market share in 2025. The application of rotary blade machinery for entertainment drones is mainly attributed to their versatility, agility, and efficiency in various applications. The expansion of these services suggests the rising use of drone technology in different industries. Multirotor drones, as the name indicates, are the most common due to their fluidity and dexterity. They are intensely used in industries like agriculture, construction, and safety of public for purposes like aerial photography, surveillance, and inspection. The fast development of the rotor design and flight control systems is resulting in an improvement in the performance and efficiency of the rotary wing drones, making these drones an essential tool for their users in search of cost-effective aerial solutions. The demand for drone technologies is getting higher with the diversified applications and benefits, resulting in the rotary blades to be the main force to reshape a steadily growing commercial drone industry.

Analysis by Mode of Operation:

- Remotely Operated

- Semi-Autonomous

- Autonomous

Remotely operated leads the market with 58.9% of market share in 2025. The rising demand for remotely operated drones due to the need for enhanced effectiveness, security, and versatility in numerous operations is propelling the market growth. These drones have many benefits, such as the capability to reach isolated or potentially dangerous areas and perform aerial surveys and checks while having the skills to meticulously and accurately complete tasks. The increasing adoption of the latest technology in drones, as real-time video transmission and autonomous flights can be done with the help of remote operators from a safe distance, reducing risks and increasing productivity, is strengthening the market growth. The growing adoption of remotely operated drones for various applications ranging from aerial photography, surveillance, mapping to delivery services is offering a favorable market outlook. However, the FAA's Part 107 regulations cover the clear rules and requirements that must be followed by remote pilots.

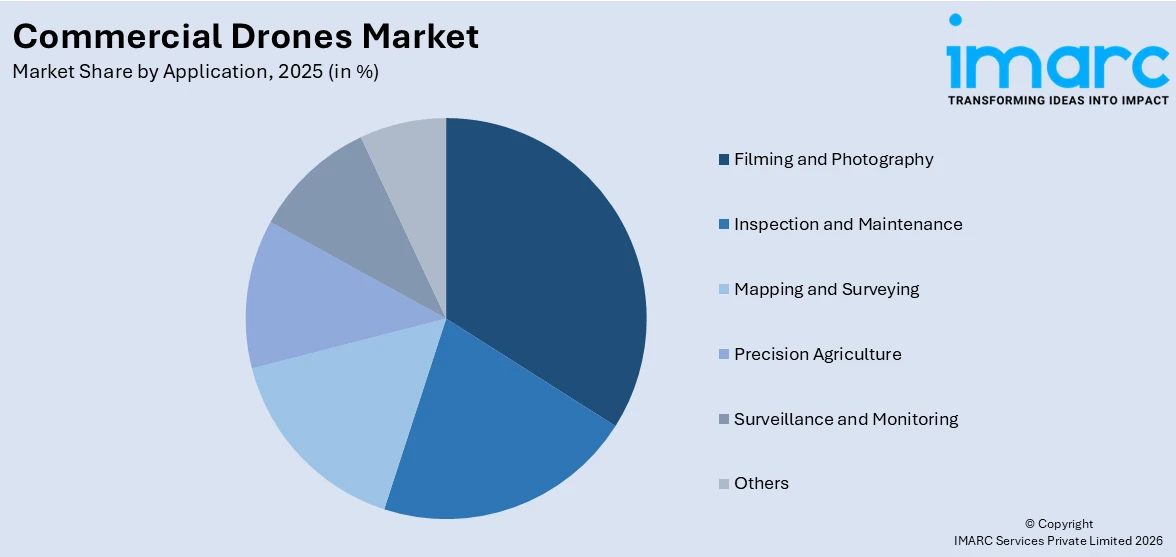

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Filming and Photography

- Inspection and Maintenance

- Mapping and Surveying

- Precision Agriculture

- Surveillance and Monitoring

- Others

Filming and photography lead the market with 32.6% of market share in 2025. In the drones industry, the area of filming and photography dominates the market due to rising need for aerial imaging solutions in different applications. The figure accentuates the expanding market for aerial photography and videography which, in turn, is creating the need for commercial drones. The specific feature of drones is that they can get views and dynamic shots that previously were a challenge to obtain, thereby helping the filmmaking, photography, and advertising industries to revolutionize. Driven by the innovation in drone technology that includes better camera stabilization and high-resolution imaging possibilities enables the filmmakers, photographers, and content creators to attain breathtaking aerial imagery effortlessly and accurately. Moreover, drones are known to produce cheaper results than those obtained from the conventional aerial photography methods, hence they are gaining popularity among the experts and newbies.

Analysis by End Use:

- Agriculture

- Delivery and Logistics

- Energy

- Media and Entertainment

- Real Estate and Construction

- Security and Law Enforcement

- Others

Media and entertainment lead the market with 21.2% of market share in 2025. The media and entertainment sector is using commercial drones due to the need for fresh aerial photography and videography services. Drones are becoming the norm in this industry and revolutionizing filmmaking, advertising, and event coverage, which is propelling the growth of the market. As drone technology evolves to achieve a level of perfect camera stabilization as well as high-resolution imaging, media professionals are now capable of capturing stunning aerial footage with much less effort. Apart from this, drones offer the possibility to do aerial filming instead of expensive solutions, such as helicopters or cranes. As a result, the drone is becoming more popular with production companies and filmmakers, which is bolstering the growth of the market.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounts for the largest market share of 39.7%. North America dominates the commercial drones market share as the region features strict regulatory standards and the FAA (FAI) serves as the key actor that ensures safety in the national airspace system (NAS). Moreover, North America already has an inbuilt superior infrastructure and technological competencies so that drone technology and adoptions can move swiftly across different industries. These devices can be utilized in such a wide range of disciplines, such as construction, agriculture, and public safety. Commercial drones are also becoming an integral part of businesses aiming to solve tasks in an affordable and timely manner. Furthermore, the regional market structure has a broad range of fundamental elements, such as research institutes, technology companies, and regulatory bodies, which fosters a favorable environment for the continuous breakthroughs and the growth of the commercial drones industry.

Key Regional Takeaways:

United States Commercial Drones Market Analysis

In 2025, US accounts for 82.4% of the total North America commercial drones market share. The US commercial drone market is growing, fueled by significant investments in agriculture, delivery, logistics, and energy. The agricultural industry uses drones for precision farming, which is leading to a 20% increase in crop yields and tremendous cost savings. Delivery services, such as Amazon Prime Air, are extending the use of drones to reduce delivery times by up to 30%. The energy sector is using drones to inspect wind turbines and solar panels, reducing operational costs by up to 40%. This development will be the venture capital efforts of The Veteran Fund, which recently closed an oversubscribed Fund I in November 2024 with a view to drive innovations in areas, such as drones, AI, and cybersecurity, through the investment in veteran-led startups. This reflects a growing recognition of dual-use technologies that address both national security and commercial opportunities in determining the future of US innovations.

Europe Commercial Drones Market Analysis

The European Union's strategic initiatives are making Europe's commercial drone market one of the most promising. According to the Drone Strategy 2.0, which was adopted by the European Commission in 2023, the Commission will develop a large-scale commercial drone market by 2030 through regulatory advancements and safety frameworks. The regulatory environment in the EU is considered the most advanced in the world as it has supported hundreds of thousands of flight hours for various applications like infrastructure surveying, medical deliveries, and environmental monitoring. The deployment of the 'U-space' system is increasing operations across Europe as it aimed at safely managing drone traffic. The strategy brings integrated drones into emergency services and into surveillance and urgent delivery alongside other innovative applications. The European Commission is investing almost a trillion dollars in drone initiatives, which is impelling the market growth.

Asia Pacific Commercial Drones Market Analysis

This region is witnessing rapid expansion of Asia Pacific commercial drones with increased investment and contributions by leading manufacturers in this region. Among the largest drone manufacturers is Shenzhen, China-based DJI, which accounts for 70% of the world's drone market share. From popular Mavic to Phantom series, DJI made aerial photography and video available for hobbyists as well as professionals. Additionally, their Matrice and Phantom RTK series are driving the growth in enterprise solutions for agriculture, public safety, and inspections. Other companies, such as Yuneec International, are also contributing to the market, offering commercial-grade drones for industrial inspections and search-and-rescue missions. As per industrial report, the use of drones in agriculture is also being seen for crop monitoring, and India is also investing in drone technology under its "Make in India" initiative, which is expected to reach USD 1.5 Billion by 2026.

Latin America Commercial Drones Market Analysis

Latin America's commercial drones market is going steadily. This expansion is being led by innovative business leaders, government agencies, and receptive buyers, alongside less crowded skies, and a favorable regulatory environment. The largest economy of this region, Brazil is forecasted to be the biggest market for commercial drones, with the sector for agriculture leading the demand for drones. Moreover, Mexican companies are also testing drones for last-mile deliveries. In the energy sector, Brazil's Petrobras is integrating drones for offshore oil platform inspections. All these factors are making Latin America a growing hub for drone technology in various sectors.

Middle East and Africa Commercial Drones Market Analysis

The Middle East and Africa commercial drones’ market is growing rapidly with investments in several sectors. Drones are being used in agriculture for crop monitoring and irrigation optimization in the arid regions of the Middle East. The energy sector in the region is also rapidly adopting drones for oil and gas infrastructure inspections. Security and law enforcement sectors are investing in drones for surveillance, especially in South Africa where drones are deployed for border patrols and anti-poaching activities.

Competitive Landscape:

Key players in the industry conduct a vast range of activities, ranging from research and development (R&D) activities to strategic and collaborative alliances for positioning them as the front runners. For instance, among the major drone manufacturers, DJI has been working on improving their products. Currently, DJI has the highest market share standing, as they offer cost-effective and easy to use drones. Moreover, companies, such as Parrot, Autel Robotics, and Skydio, are focusing on the advancement of more sophisticated drone technologies, such as AI-based autonomous flight options and the ability to avoid obstacles, to best suit the ever-changing needs of commercial users. In addition, key players frequently resort to strategic alliances and collaborations like software development, data analysis, and industry-specific solutions that are designed to assist them in widening their market reach, as well as to exploit their complementary strengths, thereby driving innovations and growth within the market.

The report has provided a comprehensive analysis of the competitive landscape in the global industrial gases market. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Aeronavics Ltd.

- AeroVironment Inc.

- Autel Robotics

- Delair

- Insitu Inc. (The Boeing Company)

- Leptron Unmanned Aircraft Systems Inc.

- PrecisionHawk Inc

- SenseFly (AgEagle Aerial Sys)

- Skydio Inc.

- SZ DJI Technology Co. Ltd. (iFlight Technology Company Limited)

- Yuneec International.

Recent Developments:

- November 2024: Safe Pro Group Inc. signed a memorandum of understanding with a U.S. prime contractor to create new threat detection solutions based on its AI-powered drone imagery processing technology. The company will focus on U.S., E.U., and NATO contracts, primarily those funded by government R&D. Safe Pro's SpotlightAI technology, compatible with commercially available drones, has already been deployed in Ukraine for landmine and unexploded ordnance (UXO) detection, processing more than 840,000 images and identifying more than 10,900 landmines.

- November 2024: Palladyne AI Corp. has expanded its collaboration with Red Cat Holdings and Teal Drones by integrating Palladyne Pilot AI software into Teal's drones. This is aimed at enhancing autonomous drone capabilities for defense, public safety, and commercial use. It also aligns with Red Cat's selection for the U.S. Army's Short Range Reconnaissance Program, with deliveries starting in 2025.

- October 2024: SCALE Nanotech introduced its revolutionary GMOD, technology for enhancement of communications in drones, avionics, and even space research. GMOD - Graphene modulator which offers ultra-low power consumption high speed data transmission coupled with reliability for operating even at extreme levels. This guarantees efficient remote or power constrained environments-which is fundamental for any commercial and civil aviation sector. SCALE Nanotech demoed GMOD at the Valencia Digital Summit, attracting much attention from other sectors.

- December 2024: Adani Defence and Aerospace has provided a second Drishti-10 Starliner surveillance drone to the Indian Navy, enhancing the capabilities of India’s maritime forces to oversee shipping routes and reduce piracy threats.

- January 2025: DJI, the worldwide frontrunner in consumer drones and innovative camera technology, revealed DJI Flip, a fresh line of all-in-one vlogging camera drones.

Commercial Drones Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Weights Covered | <2 Kg, 2 Kg-25 Kg, and 25 Kg-150 Kg |

| Systems Covered |

|

| Products Covered | Fixed Wing, Rotary Blade, Hybrid |

| Modes of Operations Covered | Remotely Operated, Semi-Autonomous, Autonomous |

| Applications Covered | Filming and Photography, Inspection and Maintenance, Mapping and Surveying, Precision Agriculture, Surveillance and Monitoring, Others |

| End Uses Covered | Agriculture, Delivery and Logistics, Energy, Media and Entertainment, Real Estate and Construction, Security and Law Enforcement, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Aeronavics Ltd., AeroVironment Inc., Autel Robotics, Delair, Insitu Inc. (The Boeing Company), Leptron Unmanned Aircraft Systems Inc., PrecisionHawk Inc., SenseFly (AgEagle Aerial Sys), Skydio Inc., SZ DJI Technology Co. Ltd. (iFlight Technology Company Limited), Yuneec International, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, commercial drones market forecast, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global commercial drones market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the commercial drones industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Commercial Drones Market Report

Commercial drones, also known as unmanned aerial vehicles (UAVs), are remotely operated or autonomous aircraft used for various business applications. Equipped with advanced technologies like cameras, sensors, and GPS, they serve industries, such as agriculture, construction, logistics, and surveillance. These drones enhance efficiency, reduce operational costs, and provide innovative solutions for tasks like data collection, inspections, and delivery services.

The commercial drones market was valued at USD 38.2 Billion in 2025.

IMARC estimates the global commercial drones market to exhibit a CAGR of 19.50% during 2026-2034.

Advancements in drone technology, increasing demand across industries like agriculture, logistics, and construction, and supportive regulatory frameworks are some of the factors supporting the market growth. The integration of AI and IoT enhances drone capabilities, while applications in precision agriculture, infrastructure inspection, and delivery services are increasing their adoption. Additionally, rising investments in drone innovations and cost-effective operations are stimulating the market growth.

According to the report, <2 Kg represents the largest segment, as lightweight drones under 2 kg are highly preferred due to their portability, ease of operation, and suitability for diverse applications like photography and inspections.

Hardware leads the market by type because drone hardware, including airframes, propulsion systems, and sensors, is the core component essential for drone performance and constitutes the bulk of production costs.

Rotary blade is the leading segment by product. Rotary blade drones offer superior maneuverability and the ability to hover, making them ideal for applications requiring precision and stability, such as filming and surveying.

Remotely operated holds the biggest market share due to their versatility, lower costs compared to autonomous models, and the ability to control them in real-time across varied scenarios.

Filming and photography dominate the market on account of the demand for high-quality aerial imagery in media, advertising, and real estate sectors.

Media and entertainment leads the market owing to its reliance on drones for dynamic and cost-effective aerial shots, enhancing visual storytelling and reducing the need for traditional, expensive equipment like cranes and helicopters.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, wherein North America currently dominates the global market.

Some of the major players in the global commercial drones market include Aeronavics Ltd., AeroVironment Inc., Autel Robotics, Delair, Insitu Inc. (The Boeing Company), Leptron Unmanned Aircraft Systems Inc., PrecisionHawk Inc., SenseFly (AgEagle Aerial Sys), Skydio Inc., SZ DJI Technology Co. Ltd. (iFlight Technology Company Limited), Yuneec International, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)