Computer Numerical Control (CNC) Market Size, Share, Trends and Forecast by Machine Type, End Use Industry, and Region, 2026-2034

Computer Numerical Control (CNC) Market Size, Share, Trends & Forecast (2026-2034)

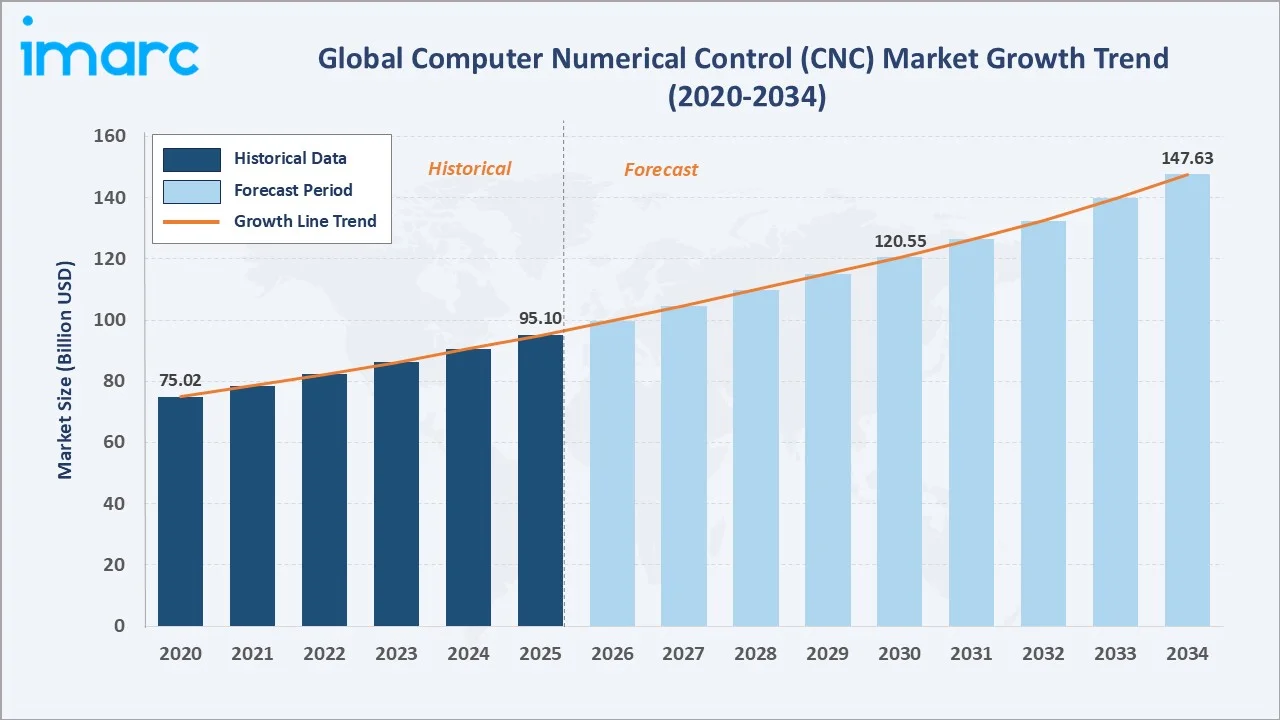

The global computer numerical control (CNC) market reached USD 95.10 Billion in 2025 and is projected to reach USD 147.63 Billion by 2034, growing at a CAGR of 4.86% during 2026-2034. The market is driven by rising adoption of precision manufacturing automation, Industry 4.0 integration, technological advancements in multi-axis machining, and growing demand from the automobile, aerospace, and defense industries worldwide.

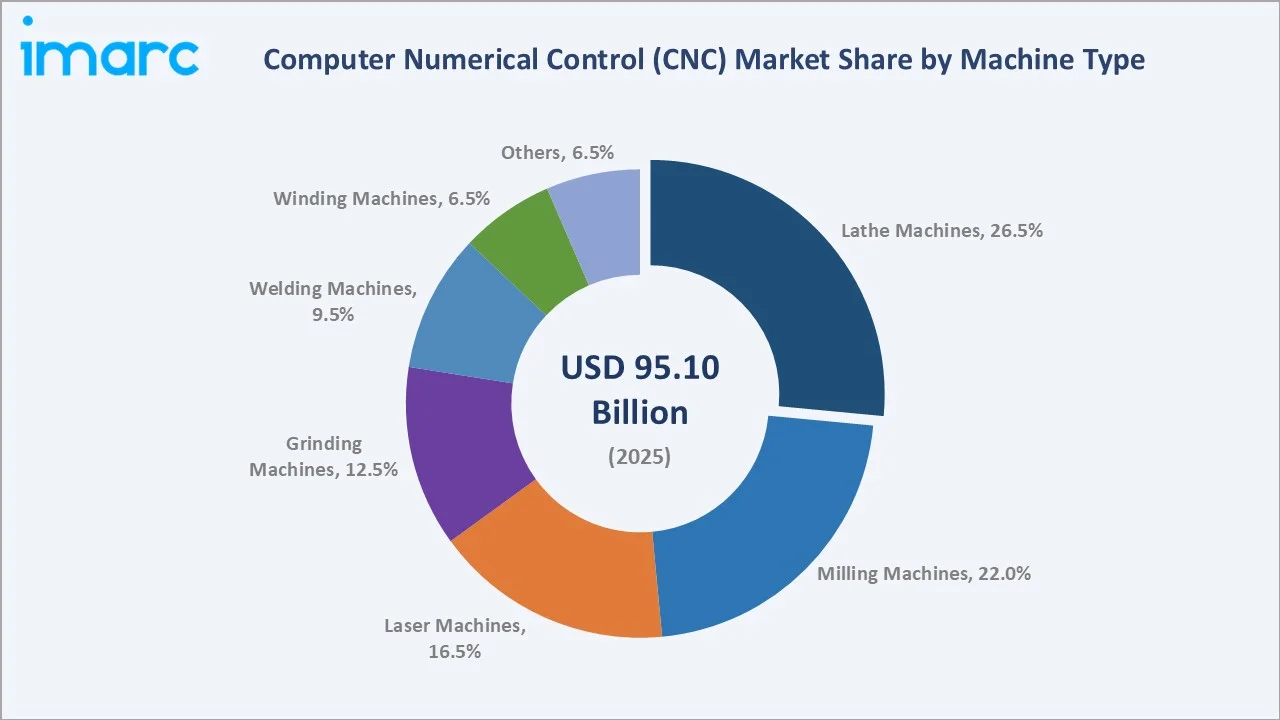

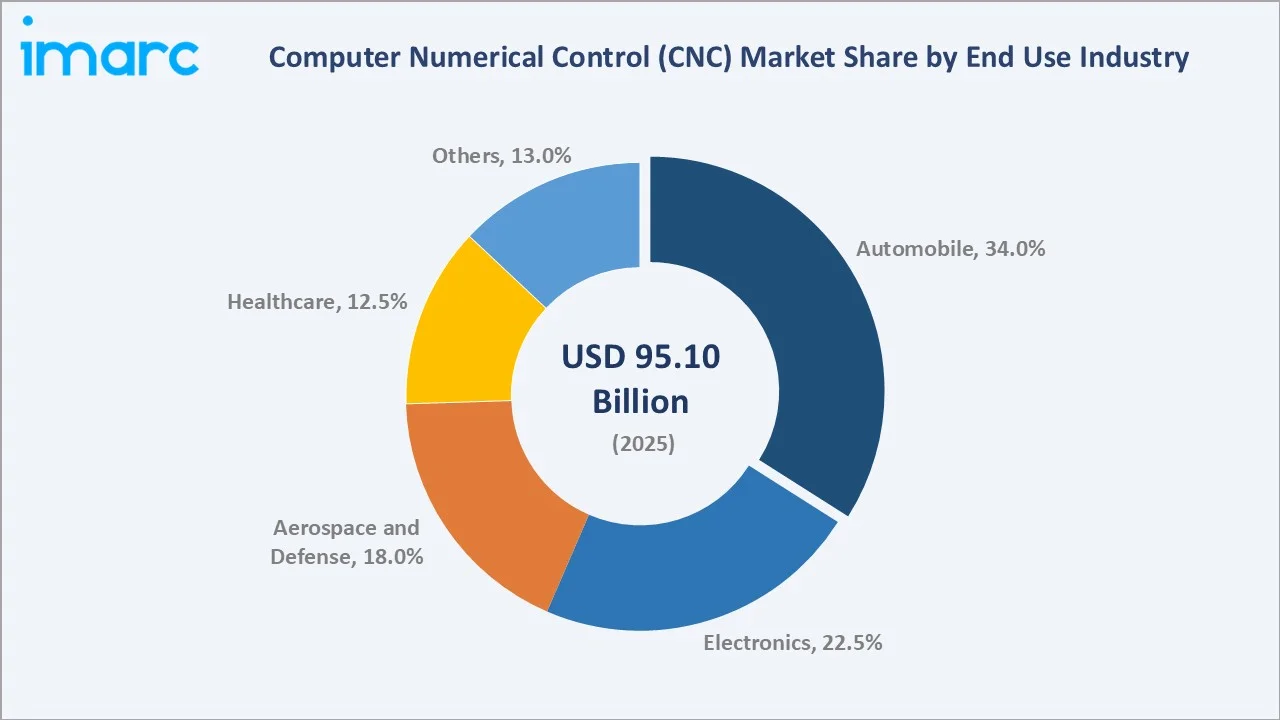

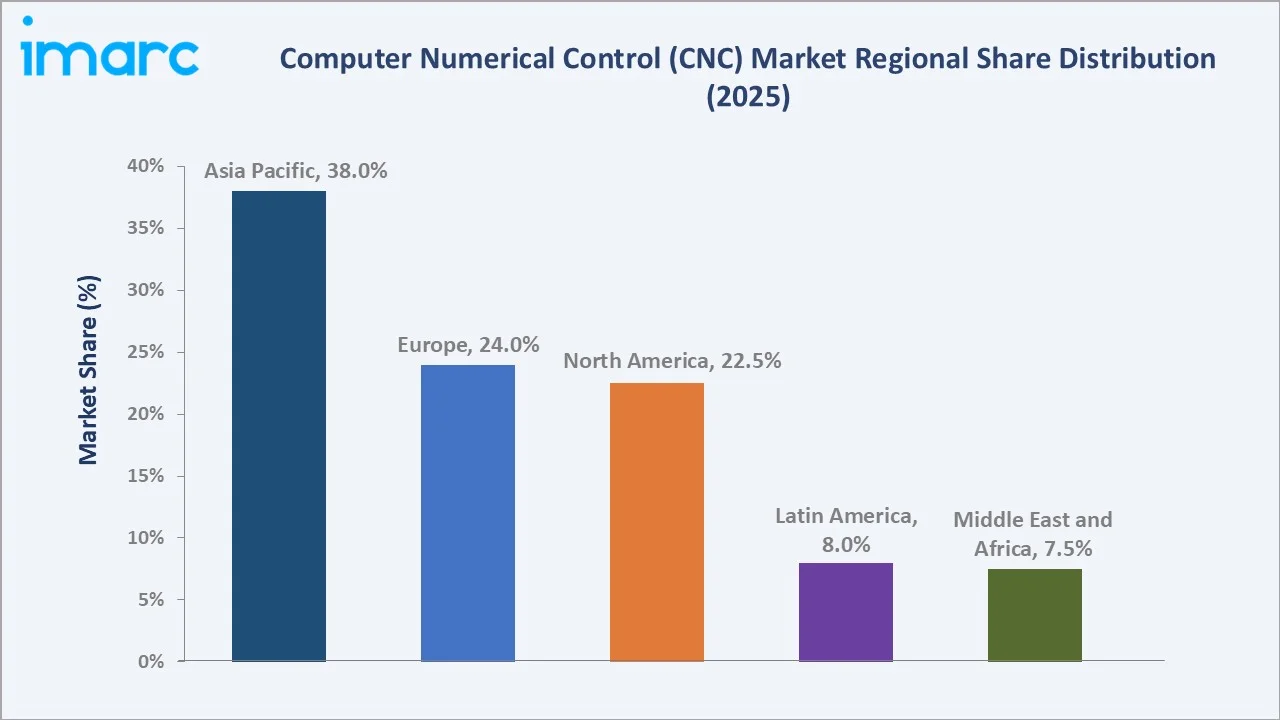

Lathe Machines from the machine type segment dominate at 26.5%. Automobile leads end use industry at 34.0%. Asia Pacific commands 38.0% of global market share, driven by China and Japan's manufacturing scale and regional automation investments.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 95.10 Billion |

|

Forecast Market Size (2034) |

USD 147.63 Billion |

|

CAGR (2026-2034) |

4.86% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Machine Type |

Lathe Machines (26.5%, 2025) |

|

Dominant End Use Industry |

Automobile (34.0%, 2025) |

|

Leading Region |

Asia Pacific (38.0%, 2025) |

The market expanded from USD 75.02 Billion in 2020 to USD 95.10 Billion in 2025, anchored at USD 120.55 Billion in 2030 and forecast to reach USD 147.63 Billion by 2034. Supply chain disruptions of 2021-2022 created temporary capital equipment procurement slowdowns but reinforced the structural automation demand trajectory, which recovered through 2023-2025 as manufacturers accelerated reshoring and factory automation investments.

To get more information on this market, Request Sample

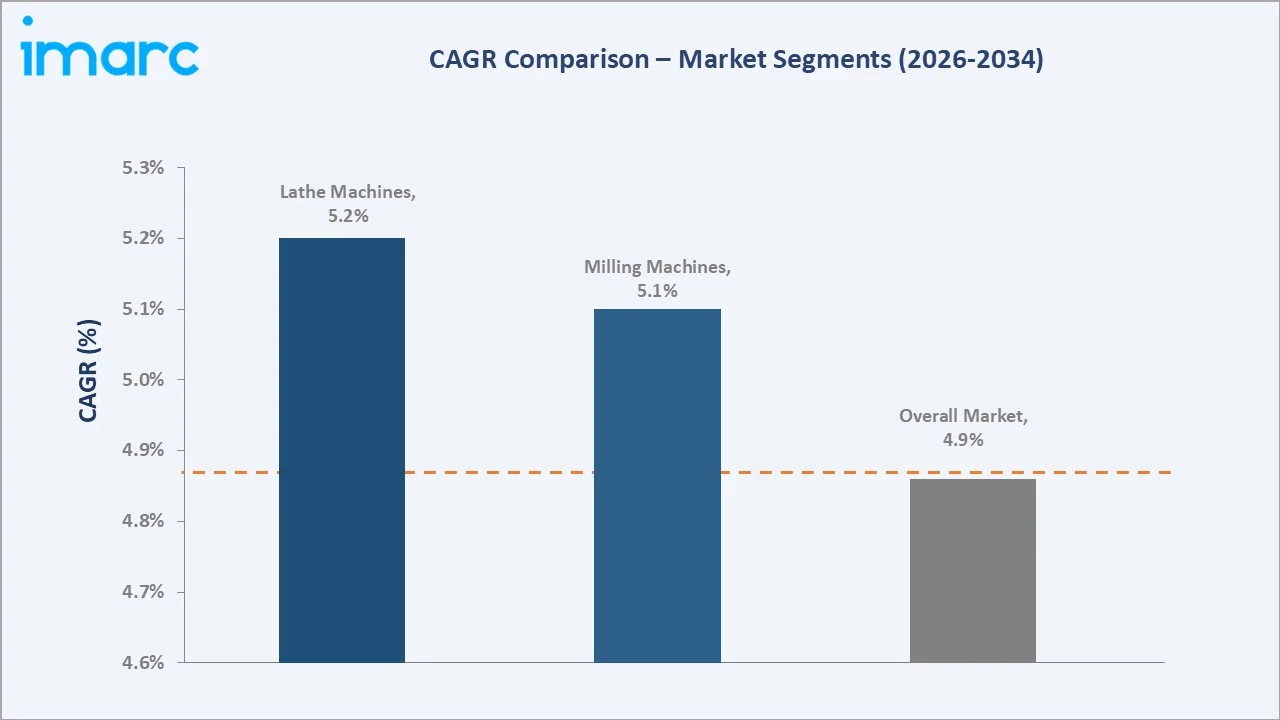

Lathe Machines grow steadily as the dominant machine type through the forecast period, supported by high-volume automotive and general engineering component turning operations globally. The automobile end use segment at 34.0% reflects the sector's highest dependency on CNC precision machining for engine components, transmission parts, and structural assemblies.

Executive Summary

The global computer numerical control (CNC) market reached USD 95.10 Billion in 2025, representing one of the manufacturing sector's most established precision automation technology markets, driven by the structural shift toward automated precision machining across all major industrial end use categories. The CNC machine tool is the defining precision manufacturing platform across automobile, aerospace, electronics, and healthcare. The market is projected to reach USD 147.63 Billion by 2034.

Lathe Machines at 26.5% dominate by capturing the highest-volume CNC machining application across automotive, general engineering, and industrial component manufacturing. Automobile at 34.0% leads through the highest dependency on CNC precision machining for powertrain and structural component production. Asia Pacific at 38.0% leads globally through China's large-scale manufacturing base, Japan's CNC machine tool manufacturing expertise, and the region's combined industrial automation expansion.

Key Market Insights

|

Insight |

Data |

|

Dominant Machine Type |

Lathe Machines – 26.5% share (2025) |

|

Dominant End Use Industry |

Automobile – 34.0% market share (2025) |

|

Leading Region |

Asia Pacific – 38.0% market share (2025) |

|

Market Opportunity |

AI-integrated CNC; 5-axis precision machining; additive-subtractive hybrid CNC; IoT predictive maintenance; SME-focused affordable CNC systems |

Key Analytical Observations Supporting the Above Data:

- Lathe Machines at 26.5%: Lathe machines dominate as they are fundamental to turning operations across automotive, aerospace, and general engineering. Their ability to produce high-precision cylindrical components efficiently makes them the highest-demand CNC machine type globally, deployed in both high-volume production and job shop environments worldwide.

- Automobile at 34.0%: The automobile sector leads through its high-volume and complexity requirements for CNC-machined components including engine blocks, crankshafts, gearbox housings, and suspension components. Expanding EV production further accelerates CNC demand for battery housing, motor casing, and power electronics enclosure machining at scale.

- Asia Pacific at 38.0%: Asia Pacific dominates through China's world-leading manufacturing scale across electronics, automobile, and general industry, combined with Japan's globally recognized CNC machine tool manufacturing expertise and South Korea's electronics precision production base, making the region both the largest consumer and manufacturer of CNC systems.

Computer Numerical Control (CNC) Market Overview

The global CNC market encompasses the design, manufacture, and supply of all computer-controlled machine tools used across precision manufacturing for components and parts production in automobile, aerospace and defense, electronics, and healthcare end use sectors globally.

The ecosystem integrates CNC machine tool manufacturers, CNC controller manufacturers, precision tooling suppliers, servo motor and drive manufacturers, CAD/CAM software providers, automation system integrators, and end-use manufacturers across automobile, aerospace, electronics, and healthcare industries. Macroeconomic factors include rising industrial automation investment, manufacturing reshoring trends, Industry 4.0 adoption, and government manufacturing incentives.

Market Dynamics

To evaluate market opportunities, Request Sample

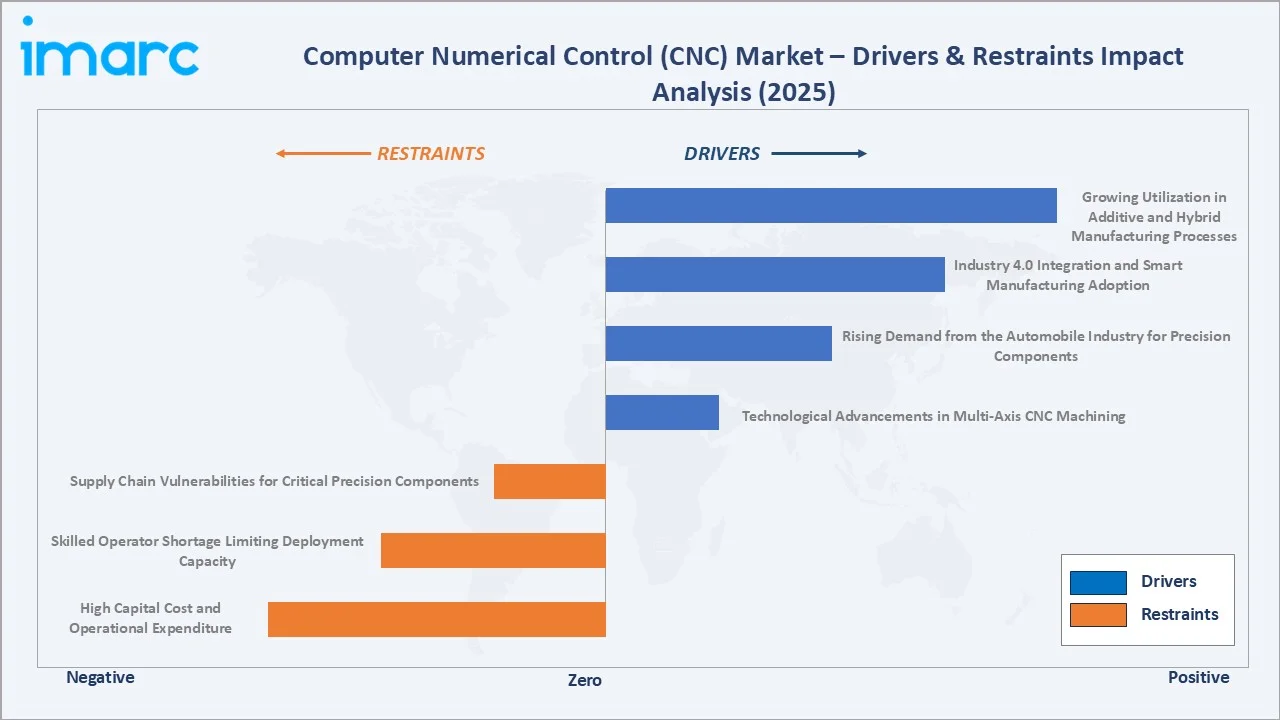

Market Drivers

- Technological Advancements in Multi-Axis CNC Machining: The emergence of 4-axis, 5-axis, and 6-axis CNC machining provides higher accuracy, complex geometry capability, and enhanced surface finish for demanding aerospace, medical, and precision engineering applications. Multi-axis CNC reduces setup times, improves part quality, and enables single-setup complex component production, increasing productivity and reducing manufacturing costs for high-value components.

- Rising Demand from the Automobile Industry for Precision Components: Growing automotive production globally requires high-volume precision CNC-machined components including engine blocks, cylinder heads, crankshafts, gearbox casings, and suspension components. Expanding electric vehicle production further accelerates CNC demand for battery housing, motor housings, and power electronics enclosures requiring high-precision machining at scale.

- Industry 4.0 Integration and Smart Manufacturing Adoption: CNC machine integration with IoT sensors, cloud connectivity, real-time monitoring, and AI-based predictive maintenance creates smart factory capabilities that improve uptime, optimize cutting parameters, and reduce scrap. Smart CNC systems self-correct based on sensor feedback, driving technology upgrade demand in aerospace and medical device manufacturing environments.

- Growing Utilization in Additive and Hybrid Manufacturing Processes: CNC is increasingly adopted in additive manufacturing post-processing and hybrid manufacturing combining additive and subtractive operations, expanding the addressable market beyond traditional machining sectors and increasing per-machine utilization in advanced manufacturing facilities.

Market Restraints

- High Capital Cost and Operational Expenditure: Advanced multi-axis CNC machining centers require significant upfront capital investment, precision tooling expenditure, and skilled operator training. High costs create adoption barriers for small and medium-sized manufacturers in emerging markets, limiting market penetration below the technology's addressable potential across global manufacturing.

- Skilled Operator Shortage Limiting Deployment Capacity: CNC operation and programming require skilled machinists proficient in CAD/CAM software, G-code programming, and precision measurement. The global shortage of CNC-skilled technicians constrains manufacturing capacity expansion and limits the pace of CNC adoption across multiple end use industries globally.

- Supply Chain Vulnerabilities for Critical Precision Components: CNC machine production depends on precision ball screws, linear guides, spindle bearings, servo motors, and CNC controllers from concentrated suppliers. Supply disruptions from geopolitical tensions or trade restrictions create production delays and cost increases for CNC machine manufacturers and end users.

Market Opportunities

- AI-Integrated CNC Controller Development for Autonomous Machining: AI-integrated CNC controllers using machine learning to optimize cutting parameters, predict tool wear, and adjust feeds based on real-time sensor data create significant technology differentiation opportunities. CNC manufacturers embedding adaptive control and digital twin capabilities create sustainable competitive advantages and recurring software revenue streams.

- Electric Vehicle Component Machining Market Expansion: EV production creates new high-volume CNC machining demand for battery housing, motor casing, and power electronics enclosures. Per-vehicle CNC-machined component value for BEVs is comparable to ICE vehicles, representing a structurally growing new application pool for CNC machine tool investment through the forecast period.

Market Challenges

- Chinese Domestic CNC Manufacturers Creating Competitive Pressure: Chinese domestic CNC machine tool manufacturers are increasingly gaining quality certification and technology capability for mainstream applications, creating competitive pricing pressure on international suppliers in both the Chinese domestic market and emerging economy export markets.

- Increasing Precision Requirements as Component Complexity Grows: As aerospace, medical, and automotive designs become increasingly complex with tighter tolerances, conventional CNC capabilities face growing technical gaps requiring continuous R&D investment. Meeting sub-micron requirements for aerospace turbine components and medical implants demands sustained precision engineering investment.

Emerging Market Trends

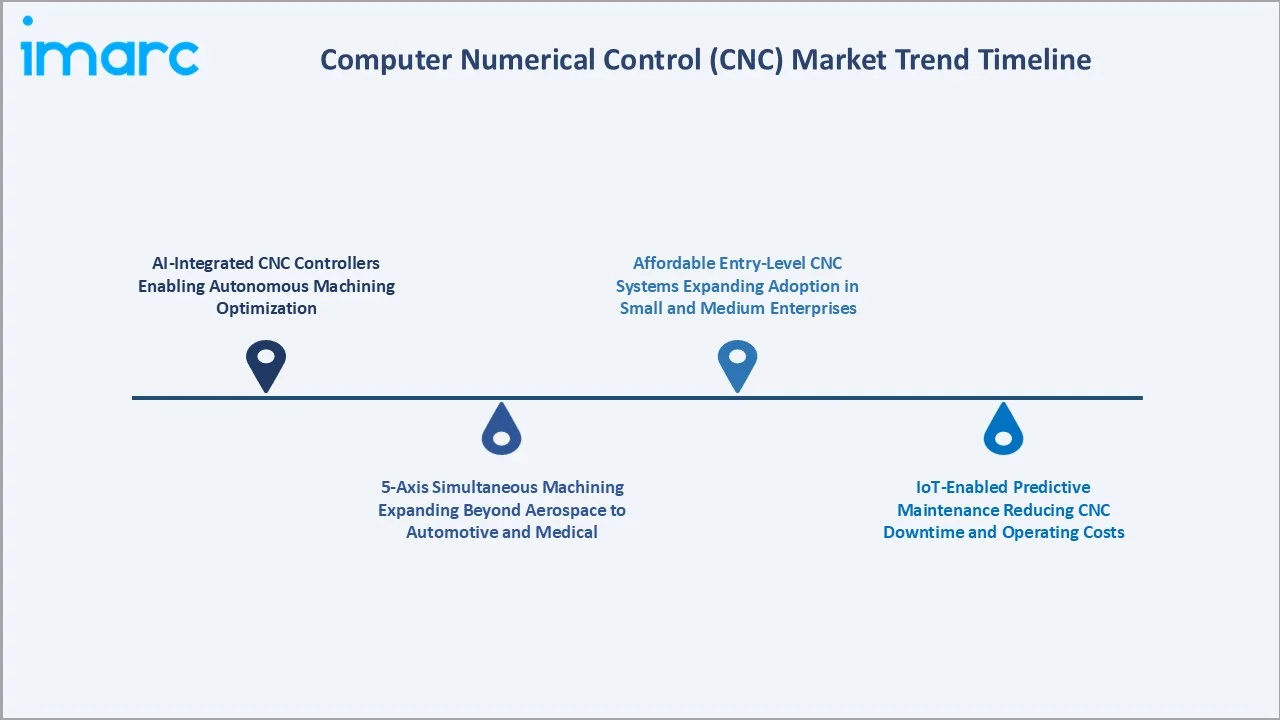

1. AI-Integrated CNC Controllers Enabling Autonomous Machining Optimization

AI-integrated CNC controllers use machine learning algorithms to continuously optimize cutting parameters, predict tool wear, and adjust feeds and speeds based on real-time vibration and force sensor data. This reduces scrap rates, extends tool life, and improves surface quality without operator intervention, creating productivity gains for end users in high-volume precision manufacturing environments.

2. 5-Axis Simultaneous Machining Expanding Beyond Aerospace to Automotive and Medical

5-axis simultaneous CNC machining enables complex turbine blades, medical implants, and automotive die molds to be completed in a single setup, reducing fixturing, improving geometric accuracy, and shortening lead times. Growing adoption beyond traditional aerospace into medical device and high-value automotive component manufacturing is expanding the market for 5-axis machining centers globally.

3. IoT-Enabled Predictive Maintenance Reducing CNC Downtime and Operating Costs

IoT-enabled CNC systems with embedded vibration, temperature, and spindle load sensors transmit real-time machine health data to cloud-based predictive maintenance platforms. Manufacturers can predict bearing failures and servo issues before breakdown, reducing unplanned downtime and extending machine life in high-utilization automotive and aerospace manufacturing environments.

4. Affordable Entry-Level CNC Systems Expanding Adoption in Small and Medium Enterprises

Declining entry-level CNC machining center prices and conversational CNC controls that simplify programming are expanding CNC adoption in small and medium manufacturing enterprises globally. This democratization creates a large incremental demand pool beyond traditional industrial customers, particularly in emerging economies across Asia, Latin America, and the Middle East.

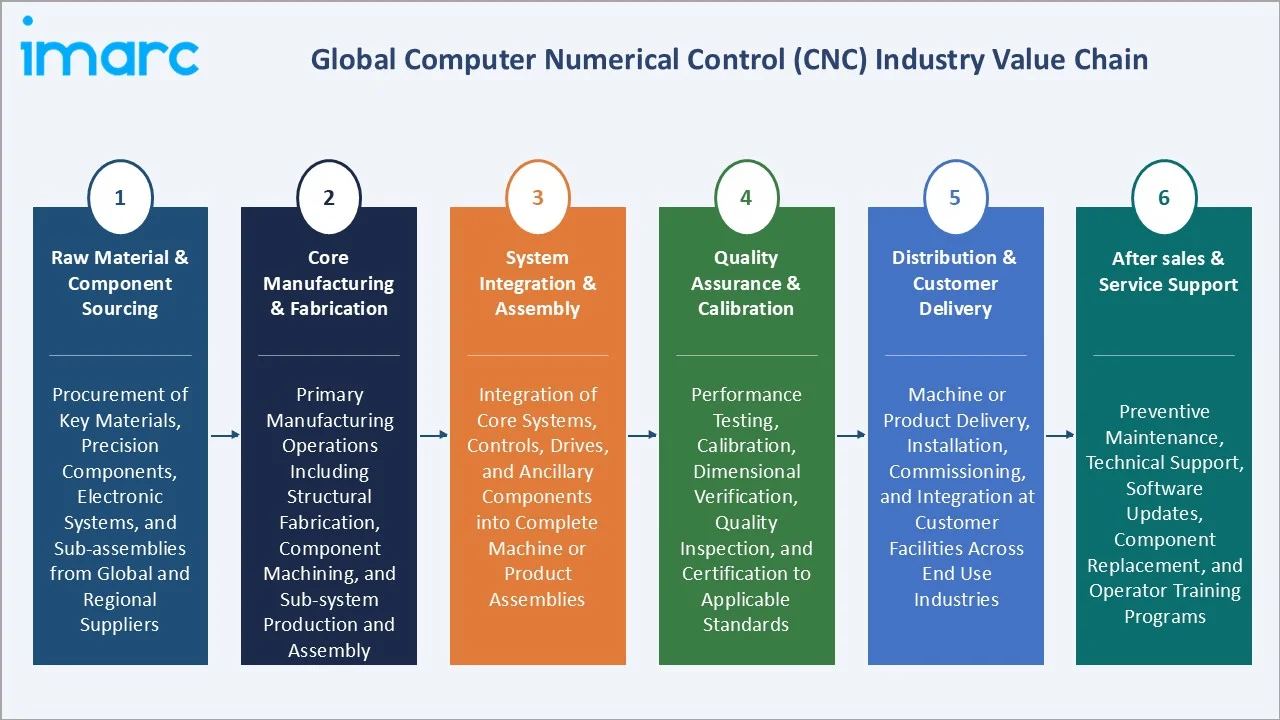

Industry Value Chain Analysis

The CNC value chain integrates raw material and component sourcing, core manufacturing and fabrication, system integration and assembly, quality assurance and calibration, customer delivery, and aftersales service. The commercial architecture is progressively shifting toward turnkey integrated manufacturing cell delivery, replacing standalone machine supply as the primary commercial format for large industrial customers.

|

Stage |

Key Activities |

|

Raw Material & Component Sourcing |

Procurement of key materials, precision components, electronic systems, and sub-assemblies from global and regional suppliers |

|

Core Manufacturing & Fabrication |

Primary manufacturing operations including structural fabrication, component machining, and sub-system production and assembly |

|

System Integration & Assembly |

Integration of core systems, controls, drives, and ancillary components into complete machine or product assemblies |

|

Quality Assurance & Calibration |

Performance testing, calibration, dimensional verification, quality inspection, and certification to applicable standards |

|

Distribution & Customer Delivery |

Machine or product delivery, installation, commissioning, and integration at customer facilities across end use industries |

|

After sales & Service Support |

Preventive maintenance, technical support, software updates, component replacement, and operator training programs |

The system integration and motion control tier is the CNC value chain's most commercially critical segment, as proprietary controller platforms from Fanuc, Siemens, and Mitsubishi create switching cost advantages and recurring software revenue opportunities for established market leaders throughout the forecast period.

Technology Landscape in the Computer Numerical Control (CNC) Industry

Multi-Axis Simultaneous Machining Technology

Multi-axis CNC machining, encompassing 4-axis, 5-axis, and 6-axis configurations, enables complex component production in single setups. The technology offers superior geometric accuracy, reduced fixturing, and comprehensive surface access, making it the preferred platform for aerospace, medical, and precision die-mold applications requiring the highest dimensional tolerances and surface quality standards.

CNC Controller and Software Technology

Advanced CNC controller platforms from Fanuc, Siemens SINUMERIK, and Mitsubishi integrate AI-based machining optimization, servo synchronization, and digital twin simulation capabilities. Modern CNC controllers support Industry 4.0 connectivity protocols including OPC-UA, enabling integration with MES, ERP, and cloud-based predictive maintenance systems in smart factory environments.

High-Speed and High-Precision Spindle Technology

High-speed spindle technology enabling 30,000+ RPM operation supports precision finishing of aluminum aerospace components, medical implants, and electronics housings at high material removal rates. Advanced spindle designs with hydrostatic bearings, active vibration damping, and integrated thermal compensation maintain dimensional accuracy under sustained high-speed cutting conditions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Machine Type |

Lathe Machines |

26.5% |

2025 |

|

End Use Industry |

Automobile |

34.0% |

2025 |

|

Region |

Asia Pacific |

38.0% |

2025 |

By Machine Type

Lathe Machines lead at 26.5% in 2025, capturing the dominant share through widespread high-volume turning operations in automobile, general engineering, and industrial component manufacturing, representing the most established CNC machining process globally.

To access detailed market analysis, Request Sample

Milling Machines at 22.0% represent the second-largest segment, capturing complex surface and profile machining demand across aerospace, die-mold, and electronics enclosure manufacturing. Laser Machines at 16.5% serve sheet metal cutting, marking, and engraving applications, growing at above-market CAGR. Grinding Machines at 12.5% address precision finishing demand in aerospace, bearing, and automotive drivetrain component manufacturing. Welding Machines at 9.5%, Winding Machines at 6.5%, and Others at 6.5% complete the machine type market structure.

By End Use Industry

Automobile leads at 34.0% through the highest volume and complexity requirements for CNC-machined powertrain and structural components. The segment's sustained demand reflects continuous production of both ICE and electric vehicle components requiring precision CNC machining, with EV production adding new component categories.

Electronics at 22.5% reflects the growing precision requirement for CNC-machined enclosures, heat sinks, and precision connectors serving semiconductor and consumer electronics production. Aerospace and Defense at 18.0% captures the highest per-part-value CNC machining application for turbine blades, structural airframe components, and precision guidance system parts. Healthcare at 12.5% encompasses surgical instruments, orthopedic implants, and medical device components. Others at 13.0% completes the end-use market structure.

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

Asia Pacific |

38.0% |

Largest regional market driven by extensive manufacturing scale, rising industrial automation, growing domestic demand, and government-supported manufacturing expansion programs |

|

Europe |

24.0% |

Mature market supported by precision engineering traditions, high-value manufacturing sectors, stringent quality requirements, and demand for advanced manufacturing technologies |

|

North America |

22.5% |

Driven by high-value manufacturing investments, reshoring initiatives, strong aerospace and defense production, and growing demand for precision automated manufacturing |

|

Latin America |

8.0% |

Emerging market with growing industrial base, increasing automation adoption, and expanding manufacturing investments in key economies |

|

Middle East and Africa |

7.5% |

Nascent but growing market with industrial diversification programs, infrastructure development, and rising manufacturing sector investment driving adoption |

Asia Pacific, at 38.0%, leads through China's world-largest manufacturing base across automotive, electronics, and general industry, combined with Japan's globally recognized CNC machine tool manufacturing expertise. Europe, at 24.0%, reflects Germany's dominant precision engineering manufacturing base and the region's tradition of high-value precision component manufacturing.

North America, at 22.5%, reflects US aerospace and defense precision manufacturing strength and the accelerating automotive reshoring trend driving new CNC machine tool investment. Latin America, at 8.0%, and Middle East and Africa, at 7.5%, represent growing CNC markets driven by automotive investments in Brazil and Mexico, and industrial diversification programs in GCC economies, respectively.

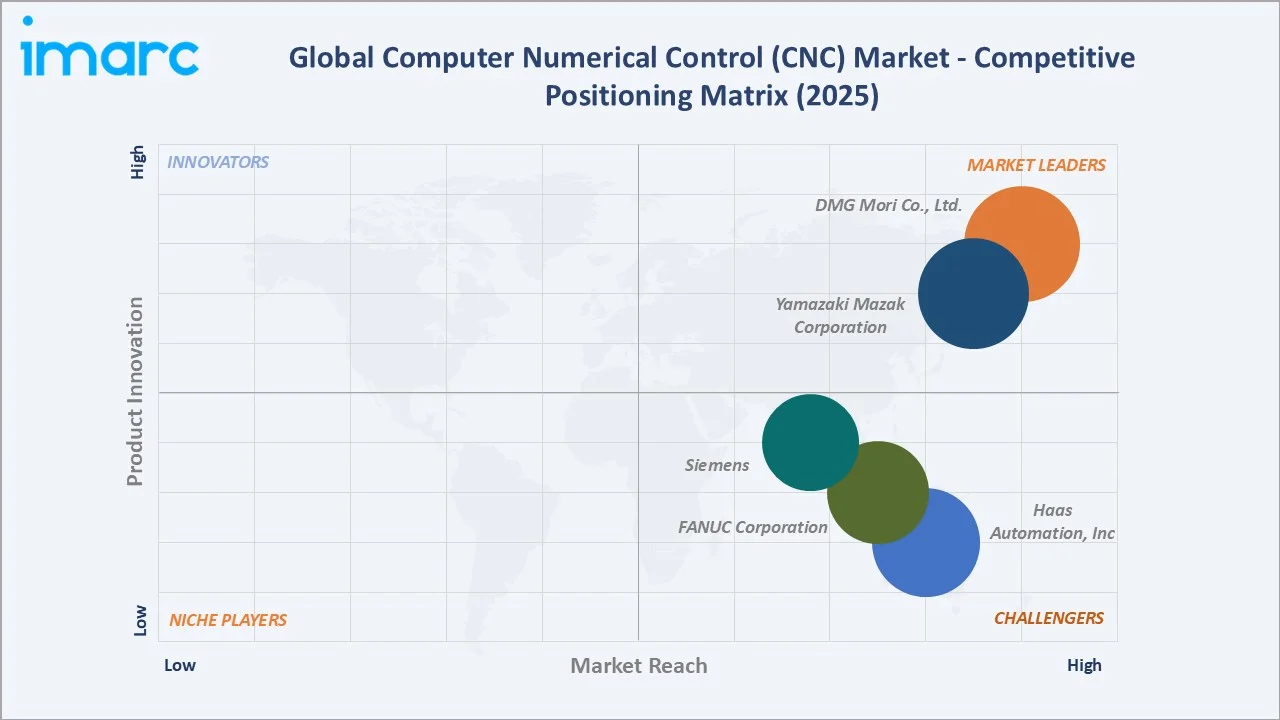

Competitive Landscape

The global CNC market competitive landscape is moderately fragmented with three distinct competitive tiers: global full-line CNC machine tool manufacturers, specialized CNC controller and technology companies, and regional precision machine tool manufacturers serving specific geographic and application markets.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

DMG Mori Co., Ltd. |

Milling Machines, LASERTEC, Turning Machines, Grinding Machines, Boring Machines |

Market Leader |

Global leader in 5-axis machining centers and turning-milling complexes with integrated digital manufacturing solutions |

|

Yamazaki Mazak Corporation |

Quick Turn, QTE, Slant Turn, Power Master, Dual Turn 200, Mega Turn, Mazatrol |

Market Leader |

Pioneer in multi-tasking CNC machines and SMOOTH CNC control platform for complex precision component production |

|

Haas Automation, Inc |

VF Series, Universal Machines, DC Series, VP-5 Prismatic, Drill/Tap/Mill Series, Drill/Tap/Mill Series |

Strong Challenger |

Largest CNC machining center manufacturer in the Western world with highest US market penetration and global dealer network |

|

FANUC Corporation |

FANUC Series 500i-A, FANUC Series 0i-MODEL F Plus, FANUC Series 30i/31i/32i-MODEL B Plus, FANUC Power Motion i-A Plus, FANUC Digital Servo Adapter-MODEL B, FANUC iPC series, FANUC iHMI |

Strong Challenger |

Dominant CNC controller and machine tool manufacturer with the highest global installed base of CNC control systems |

|

Siemens |

SINUMERIK ONE, SINUMERIK 828, SINUMERIK 808 |

Strong Challenger |

Global leader in CNC control systems and digital manufacturing solutions for high-precision machining environments |

Key players include DMG Mori Co., Ltd., Yamazaki Mazak Corporation, Haas Automation, Inc, FANUC Corporation, Siemens, and others.

Key Company Profiles

DMG Mori Co., Ltd.

DMG Mori Co., Ltd. is a Japan and Germany-based global CNC machine tool manufacturer with a strong market position through its comprehensive portfolio of turning, milling, and multi-tasking machining centers, serving the aerospace, automotive, and medical industries with world-leading 5-axis machining capabilities.

- Key Products: Milling Machines, LASERTEC, Turning Machines, Grinding Machines, Boring Machines

- Strategic Focus: Expanding integrated digital manufacturing solutions, CELOS control platform connectivity, and additive-subtractive hybrid machining capabilities for high-value aerospace, automotive, and medical component machining applications.

Yamazaki Mazak Corporation

Yamazaki Mazak Corporation is a Japan-based CNC machine tool manufacturer and global leader in multi-tasking machining technology, recognized for its comprehensive range of machining centers and turning machines.

- Key Products: Quick Turn, QTE, Slant Turn, Power Master, Dual Turn 200, Mega Turn, Mazatrol

- Recent Developments: In December 2025, Yamazaki Mazak launched the QRX-50MSY SG, a compact CNC lathe designed to improve productivity through its dual-turret and dual-spindle configuration. The machine enables simultaneous turning and milling operations, as well as concurrent machining on both spindles, significantly reducing cycle times compared to conventional one-turret, two-spindle systems.

- Strategic Focus: Advancing multi-tasking machining technology, expanding the SMOOTH CNC digital manufacturing ecosystem, and increasing automation integration through robotic cell solutions for unmanned manufacturing environments globally.

Haas Automation, Inc

Haas Automation is a US-based CNC machine tool manufacturer and the largest machine tool builder in the Western world, known for cost-effective, high-reliability machining centers and CNC lathes serving job shops, production manufacturers, and educational institutions globally.

- Key Products: VF Series, Universal Machines, DC Series, VP-5 Prismatic, Drill/Tap/Mill Series, Drill/Tap/Mill Series

- Strategic Focus: Maintaining cost-leadership in CNC machining centers and lathes, expanding automation integration options, and growing its global dealer network to serve the small and medium enterprise manufacturing market segment.

Market Concentration Analysis

The CNC market is moderately fragmented at the full-line machine tool manufacturer level, with the top 6-7 companies collectively accounting for an estimated 35-45% of global CNC market revenue across machine tools, controllers, and cutting tool systems.

The CNC controller and drive system market is more concentrated, with Fanuc, Siemens, and Mitsubishi Electric collectively accounting for approximately 60-70% of global CNC controller installations. Market concentration is declining gradually as Chinese domestic CNC manufacturers gain quality certification for mainstream international applications and expand beyond the Chinese domestic sector.

Investment & Growth Opportunities

Highest Growth Segments

5-axis machining centers (~7-9% CAGR), AI-integrated CNC systems (~10-12% CAGR), medical device precision CNC machining (~8% CAGR), electric vehicle motor and battery housing CNC machining (~12% CAGR), and additive-subtractive hybrid CNC platforms (~15-20% CAGR from smaller base) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Electric vehicle component CNC machining represents the CNC market's highest near-term incremental demand opportunity, with battery housing, motor casing, and power electronics enclosure machining creating new high-volume precision machining demand at EV production facilities globally. European commercial vehicle electrification mandates and US automotive reshoring are creating structurally growing demand pools through the forecast period.

Investment Themes

- AI-integrated CNC controller platform development for autonomous machining optimization: CNC manufacturers embedding AI-based adaptive control, real-time tool wear compensation, and predictive maintenance create sustainable technology differentiation and recurring software revenue above hardware sales margins, fundamentally shifting the competitive basis toward integrated manufacturing intelligence platforms.

- Entry-level CNC machining center manufacturing targeting SME market expansion in emerging economies: Affordable, reliable, and easy-to-operate CNC systems with strong local service networks in Asia, Latin America, and the Middle East capture the largest incremental demand growth pool and create significant market expansion for manufacturers delivering value-engineered precision at accessible price points.

Future Market Outlook (2026-2034)

The global CNC market is projected to grow from USD 95.10 Billion in 2025 to USD 147.63 Billion by 2034, delivering a 4.86% CAGR over the forecast period. The market anchor of USD 120.55 Billion in 2030 reflects an industry at its most transformative commercial inflection, with AI-integrated machining, EV component precision machining, and smart factory connectivity becoming mainstream commercial formats.

Three structural forces define CNC market growth through 2034. The manufacturing automation imperative, driven by rising labor costs and quality requirements, continues expanding CNC adoption across emerging market manufacturing. The electric vehicle production transition creates new CNC demand for battery and drivetrain components while maintaining automotive CNC demand overall. The aerospace production ramp-up, driven by commercial aircraft backlogs through 2030, creates sustained high-value precision CNC machining demand globally.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including CNC machine tool manufacturers; automotive and aerospace procurement managers; CNC application engineers and machinists; machine tool distributors and system integrators; and Industry 4.0 digital manufacturing technology specialists across key regions.

Secondary Research

Secondary research encompassed company annual reports; Japan Machine Tool Builders Association production and export data; European machine tool industry association statistics; US manufacturing technology consumption surveys by AMT; China Machine Tool and Tool Builders Association data; CNC market research reports 2025; and automotive and aerospace production volume forecasts. Over 60 secondary sources were reviewed and cross-referenced.

Forecasting Models

Market revenue forecasts developed using end-use demand bottom-up model: (i) CNC machine demand by end use industry sector production volumes; (ii) average CNC machine value per industry application; (iii) replacement and upgrade cycle demand overlay; (iv) technology premium adjustment for advanced multi-axis and AI-integrated system pricing above standard machining center pricing tiers.

Computer Numerical Control (CNC) Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Machine Types Covered | Lathe Machines, Milling Machines, Laser Machines, Grinding Machines, Welding Machines, Winding Machines, Others |

| End Use Industries Covered | Aerospace and Defense, Automobile, Electronics, Healthcare, Others |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | DMG Mori Co., Ltd., Yamazaki Mazak Corporation, Haas Automation, Inc, FANUC Corporation, Siemens, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the computer numerical control (CNC) market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global computer numerical control (CNC) market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the computer numerical control (CNC) industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Computer Numerical Control (CNC) Market Report

The global CNC market reached USD 95.10 Billion in 2025, driven by Lathe Machines at 26.5% machine type share, automobile end use leading at 34.0%, and Asia Pacific commanding 38.0% regional share through China and Japan manufacturing scale and regional industrial automation expansion programs.

The CNC market grows at 4.86% CAGR during 2026-2034, reaching USD 147.63 Billion by 2034. This growth reflects industrial automation expansion, electric vehicle production creating new precision machining demand, Industry 4.0 adoption driving technology upgrades, and growing SME demand in emerging economies worldwide.

Lathe Machines lead at 26.5%, capturing the largest share through high-volume turning operations in automobile, general engineering, and industrial component manufacturing globally. Milling Machines at 22.0% represent the second-largest segment, while Laser Machines at 16.5% are among the fastest-growing technology segments.

The Automobile industry leads at 34.0% through the highest volume and complexity requirements for CNC-machined powertrain and structural component manufacturing. Electronics at 22.5% and Aerospace and Defense at 18.0% represent the next largest end use categories by CNC market revenue share in 2025.

Asia Pacific leads at 38.0% through China's extensive manufacturing base across automotive, electronics, and general industry, combined with Japan's CNC machine tool manufacturing expertise. The region benefits from being both the largest consumer and manufacturer of CNC systems globally.

Leading companies include DMG Mori Co., Ltd., Yamazaki Mazak Corporation, Haas Automation, Inc, FANUC Corporation, Siemens, and others.

The CNC market is projected to reach approximately USD 120.55 billion by 2030, with AI-integrated CNC controllers becoming standard on new machine platforms, 5-axis machining expanding into mainstream automotive and medical applications, and electric vehicle component machining emerging as a significant demand category.

Three priority investment opportunities: AI-integrated CNC controller platform development for autonomous machining optimization; entry-level CNC machining centers targeting SME market expansion in emerging economies; and electric vehicle component precision machining capability for battery housing, motor casing, and drivetrain component production at scale.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)