Digital Signage Market Size, Share, Trends and Forecast by Type, Component, Technology, Application, Location, Size, and Region, 2026-2034

Digital Signage Market Size, Share, Trends & Forecast (2026-2034)

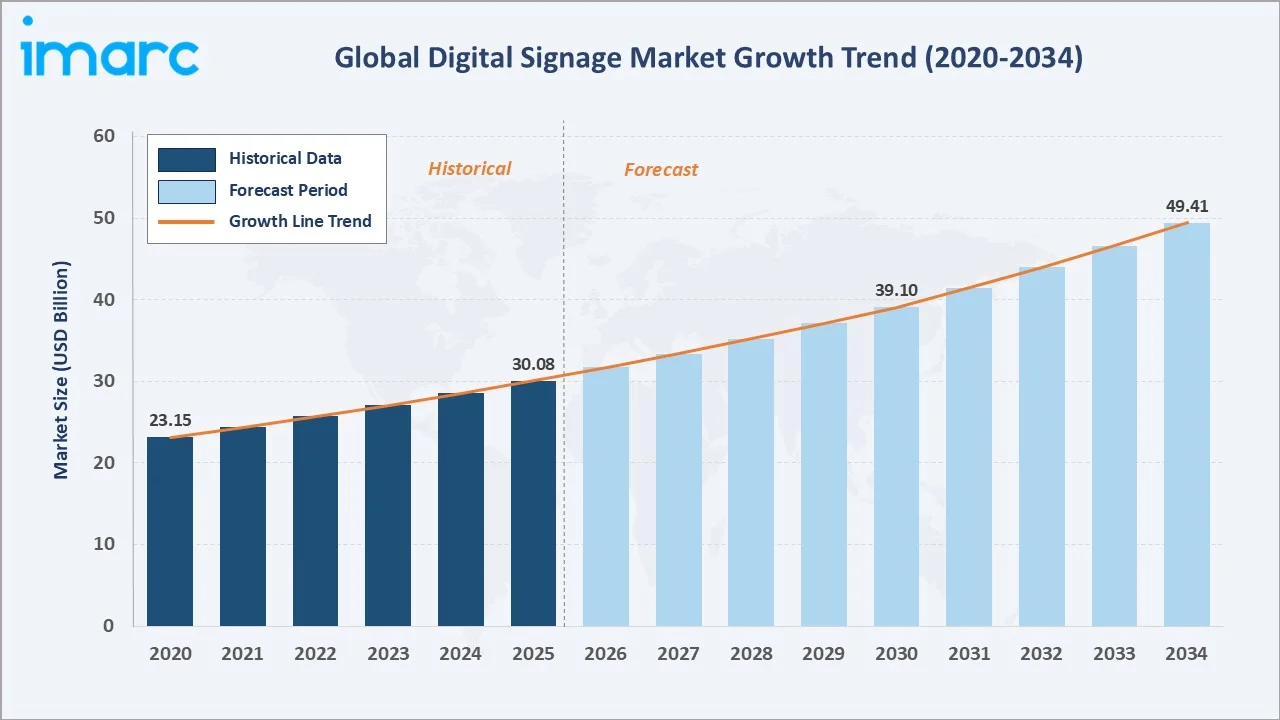

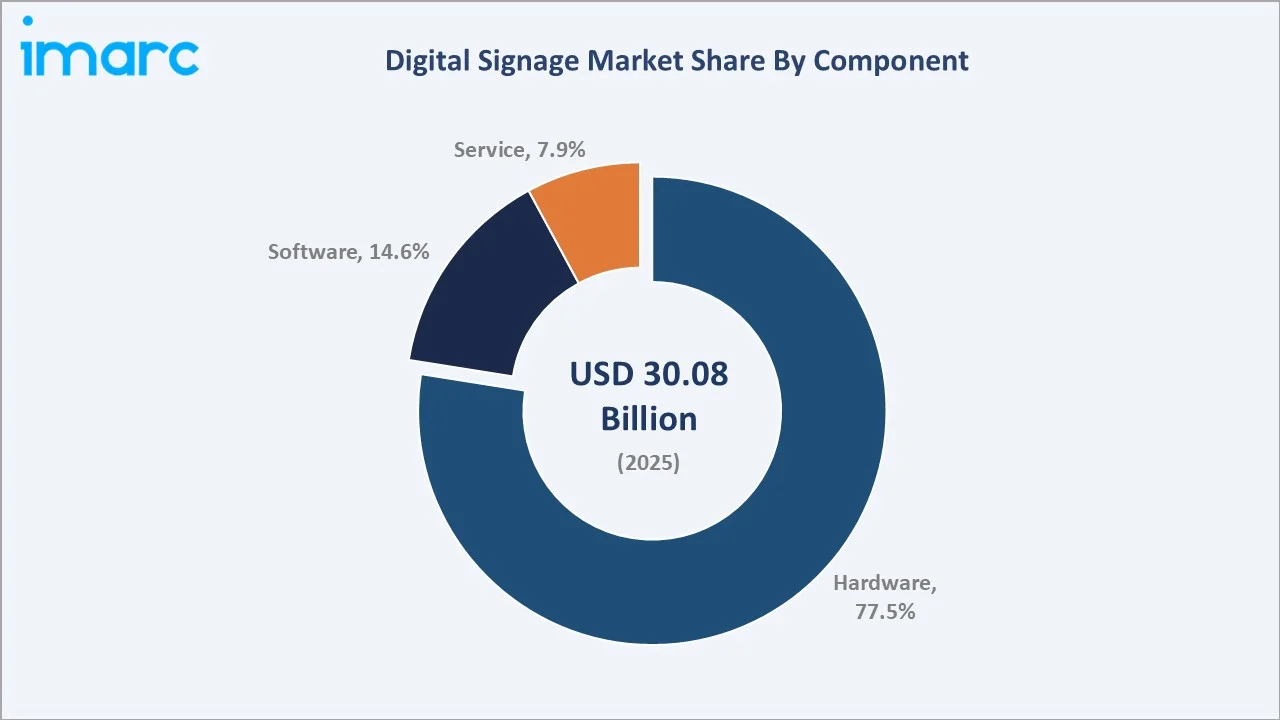

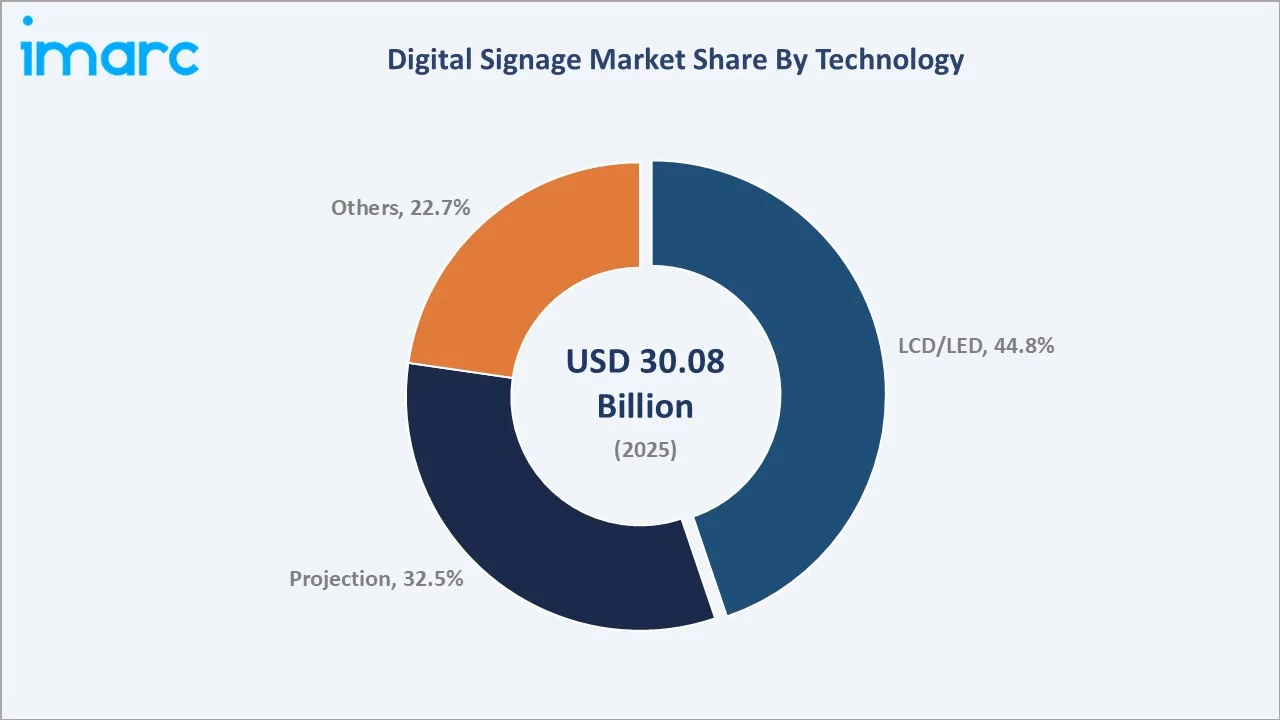

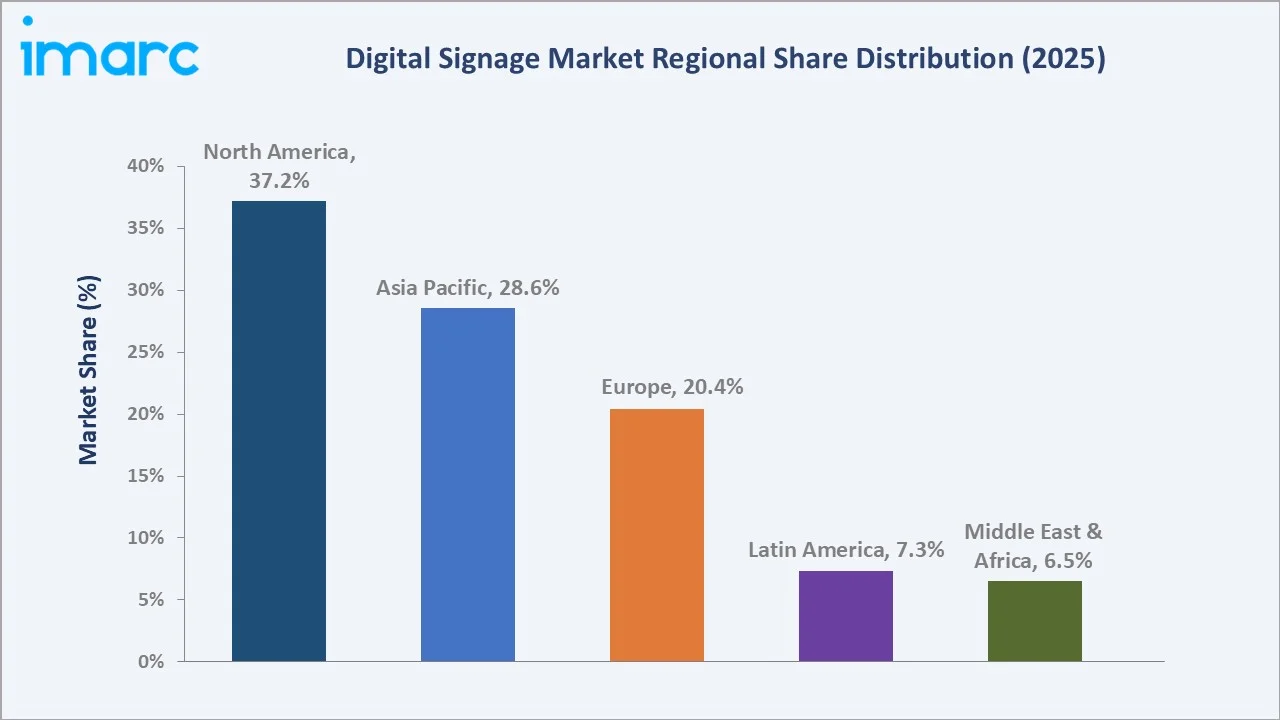

The global digital signage market reached USD 30.08 Billion in 2025 and is projected to reach USD 49.41 Billion by 2034, growing at a CAGR of 5.38% during 2026-2034. The market is driven by the rising demand for dynamic real-time visual communication, increasing adoption of interactive display technologies, and growing investments in smart retail, transportation, hospitality, and corporate infrastructure. 80% of businesses recorded a substantial growth in sales after using digital signage. Hardware dominates at 77.5%. LCD/LED leads at 44.8%. North America commands 37.2% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 30.08 Billion |

|

Forecast Market Size (2034) |

USD 49.41 Billion |

|

CAGR (2026-2034) |

5.38% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Component |

Hardware (77.5%, 2025) |

|

Dominant Technology |

LCD/LED (44.8%, 2025) |

|

Leading Region |

North America (37.2%, 2025) |

The market expanded from USD 23.15 Billion in 2020 to USD 30.08 Billion in 2025, anchored at USD 39.10 Billion in 2030, and forecast to reach USD 49.41 Billion by 2034. COVID-19 temporarily suppressed digital signage investment in 2020, while simultaneously catalyzing touch-free and hygiene-forward signage innovations that established new deployment patterns sustaining post-pandemic growth. The post-COVID recovery from 2021 has been robust, with retail, transportation, and corporate digital signage all experiencing pent-up investment realization.

To get more information on this market, Request Sample

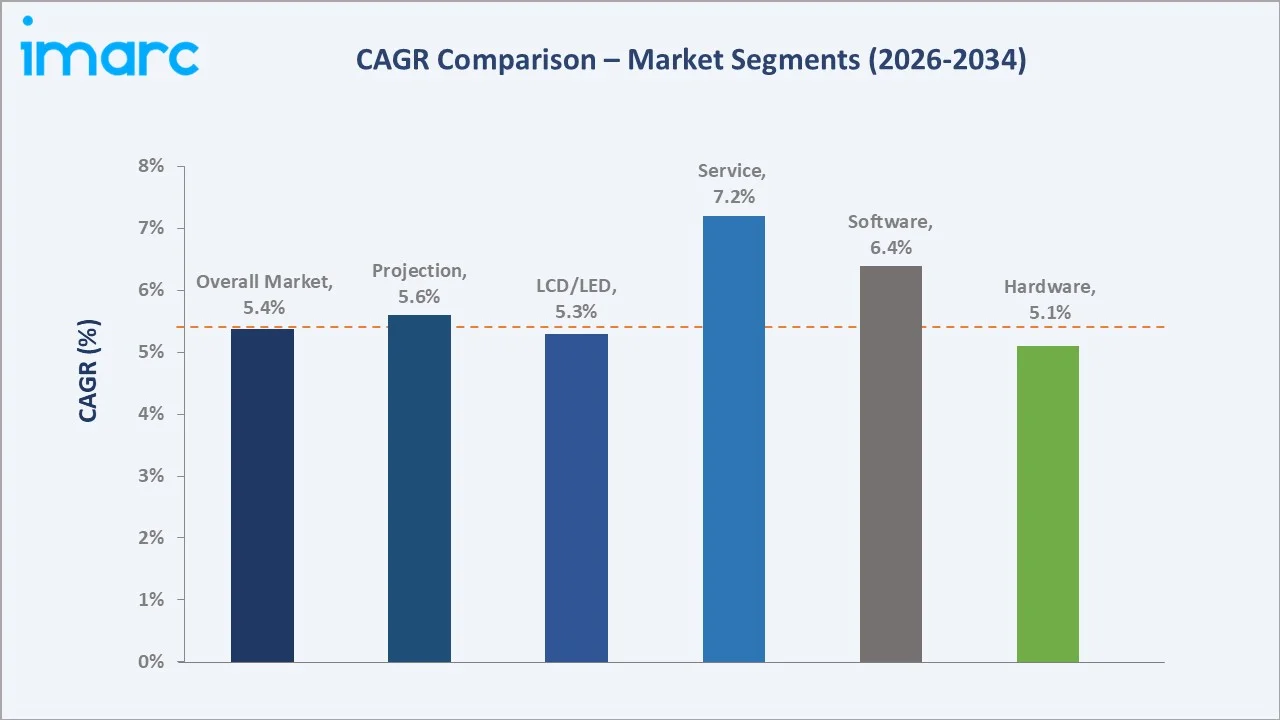

Service grows fastest at ~7.2% CAGR as digital signage deployments transition from one-time capital purchases toward managed services, content management subscriptions, and maintenance contracts, generating recurring revenue for vendors and reducing upfront cost barriers for end users. Projection grows at ~5.6% CAGR through large-venue applications.

Executive Summary

The global digital signage market reached USD 30.08 Billion in 2025, representing the convergence of display technology advancement, content management software evolution, and the fundamental commercial transformation of physical spaces from static to dynamic visual communication environments. Digital signage has evolved from the simple scrolling text displays of the 1990s and single-panel LCD menu boards of the 2000s into a sophisticated ecosystem encompassing AI-powered content personalization, programmatic advertising, interactive customer engagement, real-time data-driven content management, and the integration of physical display infrastructure with digital commerce platforms. The market is projected to reach USD 49.41 Billion by 2034 at 5.38% CAGR.

Hardware at 77.5% dominates the market as display panels, media players, mounting systems, and peripheral hardware remain the primary cost center in digital signage deployments. Each display requires physical hardware investment, depending on technology and scale, creating a large recurring revenue pool from the global installed base's upgrade and expansion cycles. LCD/LED technology at 44.8% leads through the mature commercial display industry's ability to deliver high-quality 4K visual performance at continuously declining price points, making LCD/LED the default digital signage technology for retail, QSR, corporate, healthcare, and transit applications globally. North America, at 37.2%, leads through its mature advertising ecosystem and the world's highest digital menu board density.

Key Market Insights

|

Insight |

Data |

|

Dominant Component |

Hardware - 77.5% share (2025) |

|

Dominant Technology |

LCD/LED - 44.8% market share (2025) |

|

Leading Region |

North America - 37.2% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Hardware at 77.5% reflecting the capital-intensive nature of digital signage deployment, where display panels, media players, and mounting infrastructure represent the majority of total project cost: Hardware's market dominance reflects both the absolute cost of commercial display infrastructure and the ongoing refresh cycles of the global installed digital signage base.

- LCD/LED at 44.8%, maintaining technology leadership through continuous performance improvement and price reduction, sustaining dominance across indoor and semi-outdoor applications: LCD/LED technology's market leadership reflects its dominance across the broadest range of digital signage applications. Commercial LCD panels are the default choice for indoor retail, digital menu boards, corporate, healthcare, and education applications where daylight performance is adequate, and the display is static or low-dynamic-range content.

- North America at 37.2%: North America dominates the market due to high adoption of advanced display technologies across retail, transportation, healthcare, and corporate sectors, supported by strong digital infrastructure and technology investments. The presence of major digital signage solution providers and the increasing deployment of smart advertising networks are further driving regional market growth.

Digital Signage Market Overview

The global digital signage market encompasses the design, manufacture, integration, deployment, and management of networked digital display systems for commercial, public, and institutional communication environments. Digital signage hardware includes commercial-grade display panels, outdoor high-brightness displays, transparent and flexible displays, media players, interactive displays, and mounting and enclosure systems for indoor and outdoor installation. Software encompasses content management systems (CMS) for schedule-based and real-time dynamic content publishing, audience measurement and analytics platforms, programmatic digital out-of-home advertising management, and enterprise integration. Services include system design and integration, content creation, managed services, and field maintenance.

The ecosystem integrates display panel manufacturers, LED module suppliers, commercial display system assemblers, media player manufacturers, CMS platform vendors, system integrators, DOOH media operators, and end-user verticals spanning retail, QSR, hospitality, healthcare, transportation, corporate, education, and entertainment.

Market Dynamics

To evaluate market opportunities, Request Sample

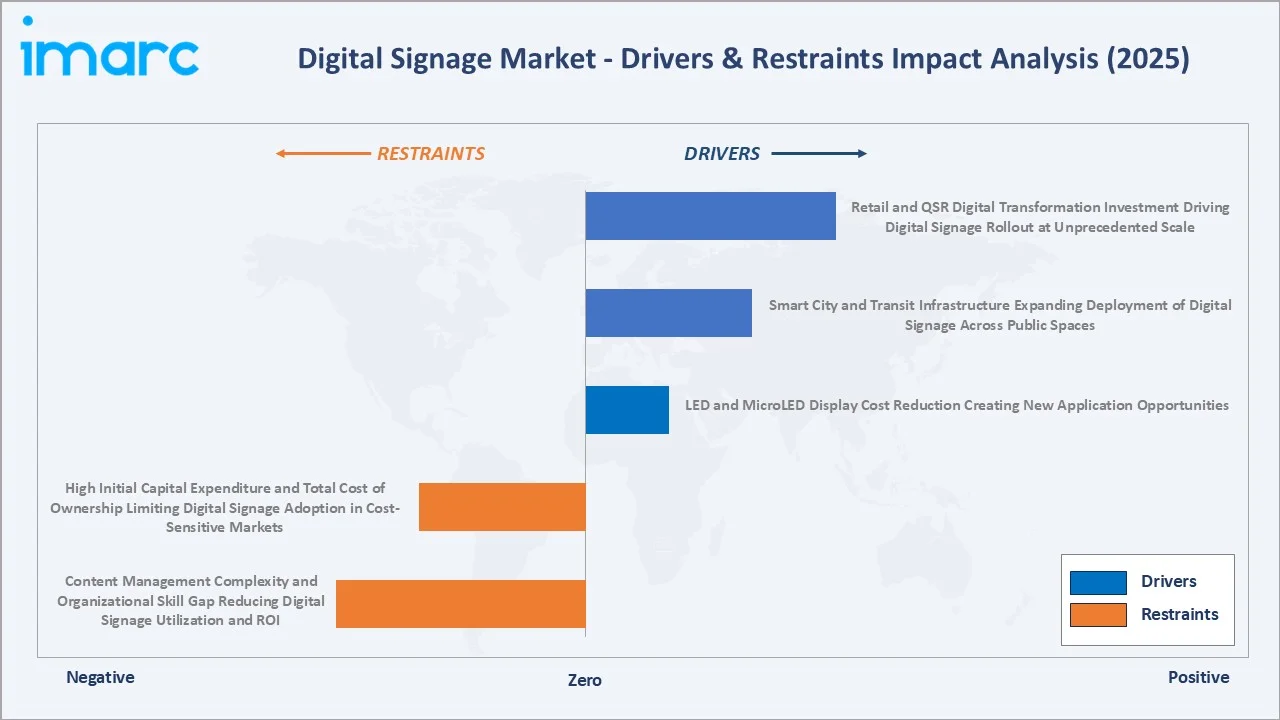

Market Drivers

- Retail and QSR Digital Transformation Investment Driving Digital Signage Rollout at Unprecedented Scale: Retail and quick-service restaurant (QSR) digital transformation represents the largest single demand driver for commercial digital signage hardware and software globally. QSR digital menu board adoption is structurally complete among major global chains, but the cycle continues through next-generation AI-capable menu board replacement; drive-through digital menu board expansion; and international expansion of digital menu board rollout to emerging markets.

- Smart City and Transit Infrastructure Expanding Deployment of Digital Signage Across Public Spaces: Cities worldwide spend over $124 billion annually on AI dashboards and sensor infrastructure. Government and transit authority investment in smart city digital infrastructure is creating new digital signage procurement streams that are structurally government-funded and less vulnerable to private sector economic cycle volatility. India's Smart Cities Mission completed 94% of the total 8,067 projects, with ₹1.64 lakh crore invested.

- LED and MicroLED Display Cost Reduction Creating New Application Opportunities: Direct-view fine-pitch LED display technology's cost reduction trajectory has expanded LED digital signage from ultra-premium luxury retail and control room applications into mainstream retail, hospitality, and corporate visualization applications.

Market Restraints

- High Initial Capital Expenditure and Total Cost of Ownership Limiting Digital Signage Adoption in Cost-Sensitive Markets: Commercial digital signage deployment costs significantly exceed consumer display pricing. This commercial premium creates cost barriers for small-medium businesses, restaurants, and retail establishments that compare commercial signage cost against consumer TV alternatives.

- Content Management Complexity and Organizational Skill Gap Reducing Digital Signage Utilization and ROI: The most commonly cited digital signage failure mode is not hardware malfunction but content neglect, displays showing outdated promotional content, static screen savers from default installation, or blank screens from CMS connectivity failure.

Market Opportunities

- AI-Powered Audience Analytics Enabling Personalized Content Delivery and Measurable Advertising ROI: Computer vision AI applied to digital signage enables content personalization and advertising ROI measurement that was impossible with traditional digital signage. Audience analytics platforms using computer vision from webcams embedded in or adjacent to digital displays provide second-by-second audience demographic measurement, enabling content scheduling optimization and post-campaign reporting.

- Healthcare Digital Signage Providing Wayfinding, Patient Education, and Waiting Room Communication Solutions: Healthcare digital signage is one of digital signage's fastest-growing verticals, driven by patient wayfinding complexity in large hospital campuses requiring digital directory and turn-by-turn wayfinding display systems, patient education content delivery in examination rooms and consultation areas, waiting room communication, and pharmacy digital signage for medication information and pharmaceutical advertising compliance.

Market Challenges

- Economic Cycle Sensitivity of Capital Investment Digital Signage Projects in Retail and Hospitality: Digital signage investment in retail, hospitality, and foodservice is highly correlated with economic cycle confidence. Capital expenditure on visual communication infrastructure is among the first investments deferred during economic uncertainty and among the first to recover in economic upturns. Economic cycle risk is managed by digital signage vendors through geographic diversification, vertical diversification, and service revenue growth.

- Fragmentation of CMS Platform Standards Creating Integration Complexity for Multi-Vendor Enterprise Deployments: Enterprise digital signage deployments frequently involve multiple hardware vendors and multiple CMS platforms, creating integration complexity that multiplies IT management burden and content operations cost. The lack of universal digital signage interoperability standards means that content created in one CMS platform frequently requires reformatting or recreation for another, creating vendor lock-in dynamics that favor sticking with incumbent CMS vendors even when alternatives offer better capabilities.

Emerging Market Trends

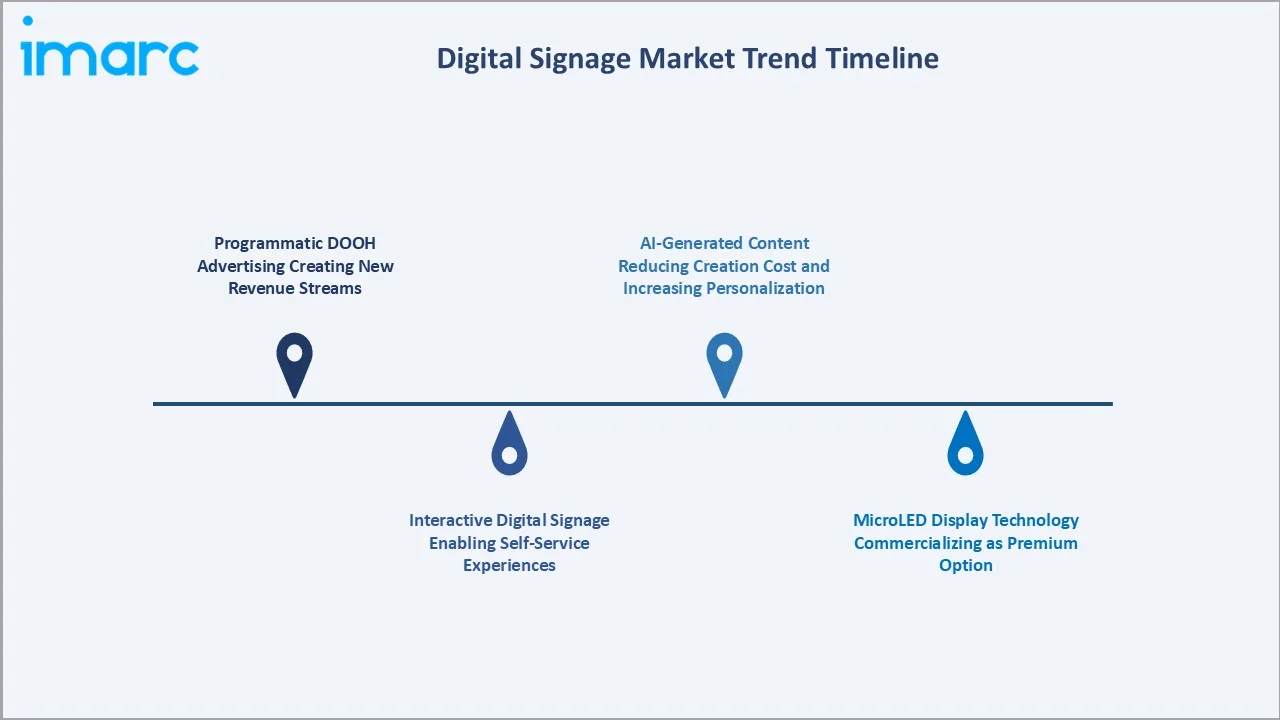

1. Programmatic DOOH Advertising Creating New Revenue Streams for Digital Signage Operators

Programmatic digital out-of-home (DOOH) advertising enables automated, data-driven advertisement buying and real-time content delivery across digital display networks. This technology allows signage operators to optimize ad inventory utilization, target audiences more precisely, and generate higher advertising revenues through dynamic campaign management. In February 2026, JCDecaux SE announced the global expansion of its programmatic digital out-of-home (pDOOH) media solution following the successful launch of its airport-focused programmatic advertising offering in 2024. The expanded solution now covers street furniture, transportation hubs, and retail environments, enabling brands to execute integrated global advertising campaigns and engage audiences across multiple consumer touchpoints through JCDecaux’s digital advertising network.

2. Interactive Digital Signage Enabling Self-Service and Engagement Experiences

Interactive digital signage enables personalized self-service and immersive customer engagement experiences across retail, hospitality, transportation, and healthcare sectors. Businesses are increasingly deploying touch-enabled kiosks, smart wayfinding displays, and AI-powered interactive screens to improve customer convenience and reduce service wait times. These solutions also support real-time product information, targeted promotions, and seamless digital transactions. Rising consumer preference for contactless and personalized experiences is further accelerating the adoption of interactive signage technologies.

3. MicroLED Display Technology Commercializing as Premium Digital Signage Option

MicroLED display technology is emerging due to its superior brightness, high contrast ratio, energy efficiency, and longer operational lifespan compared to conventional display technologies. Businesses are increasingly adopting MicroLED signage for luxury retail stores, corporate environments, entertainment venues, and smart city applications that require ultra-high-resolution visual experiences. Samsung showcased its 130-inch Micro RGB signage display (QPHX model) to commercial audiences for the first time at ISE 2026. Originally introduced at CES 2026 for the ultra-premium home entertainment segment, the display incorporates advanced Micro LED technology and the Micro RGB AI Engine Pro to provide enhanced color performance, high picture quality, and an ultra-slim form factor suited for premium retail and flagship commercial environments.

4. AI-Generated Content Reducing Digital Signage Content Creation Cost and Increasing Personalization

AI-generated content is helping businesses reduce content production costs while enabling highly personalized and dynamic advertising experiences. Companies are increasingly using generative AI tools to automatically create promotional visuals, localized advertisements, and audience-specific messaging in real time. These technologies improve campaign scalability, accelerate content deployment, and enhance customer engagement through data-driven personalization. Growing demand for targeted advertising and operational efficiency is further driving the adoption of AI-powered digital signage content platforms.

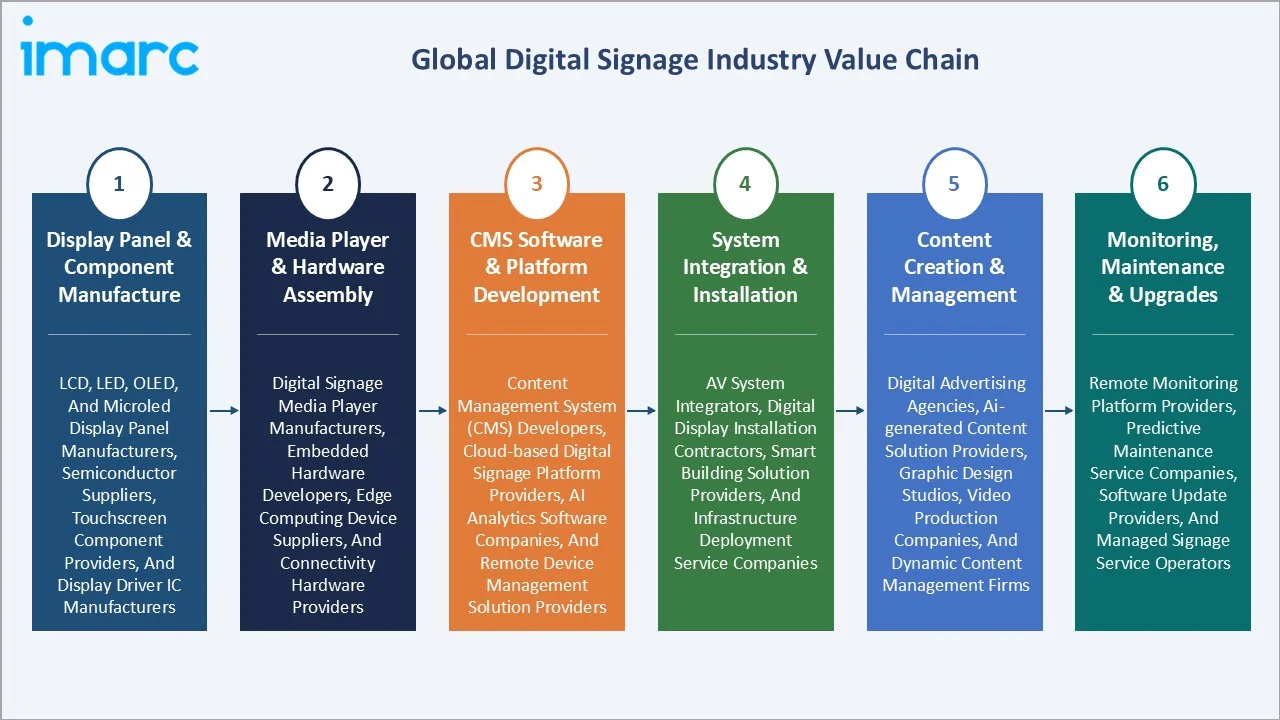

Industry Value Chain Analysis

The global digital signage value chain integrates display panel and component manufacture, media player and hardware assembly, CMS software platform development, system integration and installation, content creation and management, and ongoing monitoring, maintenance, and system upgrades. Display panel manufacture is the most capital-intensive value chain stage, creating semiconductor industry-scale capital barriers to entry that sustain market concentration.

|

Stage |

Key Participants |

|

Display Panel & Component Manufacture |

LCD, LED, OLED, and MicroLED display panel manufacturers, semiconductor suppliers, touchscreen component providers, and display driver IC manufacturers. |

|

Media Player & Hardware Assembly |

Digital signage media player manufacturers, embedded hardware developers, edge computing device suppliers, and connectivity hardware providers. |

|

CMS Software & Platform Development |

Content management system (CMS) developers, cloud-based digital signage platform providers, AI analytics software companies, and remote device management solution providers. |

|

System Integration & Installation |

AV system integrators, digital display installation contractors, smart building solution providers, and infrastructure deployment service companies. |

|

Content Creation & Management |

Digital advertising agencies, AI-generated content solution providers, graphic design studios, video production companies, and dynamic content management firms. |

|

Monitoring, Maintenance & Upgrades |

Remote monitoring platform providers, predictive maintenance service companies, software update providers, and managed signage service operators. |

The monitoring, maintenance, and upgrades tier is becoming the digital signage industry's most commercially important strategic battleground as vendors recognize that long-term customer relationships and recurring revenue require post-installation service engagement.

Technology Landscape in the Digital Signage Industry

Commercial LCD and LED Display Technology

Commercial LCD and LED display technologies enable high-resolution, energy-efficient, and scalable visual communication solutions across retail, transportation, hospitality, and corporate environments. Advancements in ultra-thin displays, higher brightness levels, and improved color accuracy are enhancing visibility and customer engagement in both indoor and outdoor applications. In October 2025, Samsung unveiled its 115-inch 4K Smart Signage display, presenting it as a solution designed to combine the advantages of videowall and LED display technologies. Described as the world’s largest LCD display, the model expands upon the company’s earlier 105-inch QPDX 5K display platform.

Digital Signage Media Player Technology

Digital signage media player technology enables seamless content processing, remote display management, and real-time multimedia delivery across connected display networks. Advanced media players support high-resolution video playback, cloud-based content synchronization, AI-driven analytics, and interactive applications for retail, transportation, healthcare, and corporate environments. These technologies also improve system reliability, scalability, and operational efficiency through centralized control and edge computing capabilities. Growing demand for dynamic and data-driven digital communication is accelerating innovation in smart media player solutions.

Audience Analytics and Measurement Technology

Audience analytics and measurement technologies are enabling businesses to track viewer engagement, foot traffic patterns, dwell time, and audience demographics in real time. Companies are increasingly integrating AI-powered cameras, computer vision, sensors, and location analytics tools to deliver targeted and data-driven advertising campaigns. These technologies improve campaign effectiveness, optimize content placement, and enhance return on advertising investment for digital signage operators. Rising demand for measurable and personalized advertising experiences is further accelerating the adoption of advanced audience analytics solutions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

🔒 |

🔒 |

2025 |

|

Component |

Hardware |

77.5% |

2025 |

|

Technology |

LCD/LED |

44.8% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Location |

🔒 |

🔒 |

2025 |

|

Size |

🔒 |

🔒 |

2025 |

|

Region |

North America |

37.2% |

2025 |

By Component

Hardware leads at 77.5% market share (2025). Hardware encompasses commercial display panels, media players, mounting and installation hardware, interactive hardware, and power and connectivity infrastructure.

To access detailed market analysis, Request Sample

Software at 14.6% encompasses CMS platforms, scheduling software, interactive application development, analytics and reporting, and integration middleware. Service at 7.9% encompasses system integration services, managed services, and professional services. Service's 7.2% CAGR is the highest among components, reflecting the growing market and enterprise preference for operational model digital signage delivery.

By Technology

LCD/LED leads at 44.8% market share (2025). This category encompasses commercial LCD displays, direct-view fine-pitch LED video walls, and outdoor SMD LED billboard and sports venue displays. LCD/LED's price reduction is expanding the addressable deployment market to lower-budget applications while sustaining market value through the premium fine-pitch LED video wall segment's growth.

Projection at 32.5% encompasses corporate auditorium and large-venue projectors, museum and architectural projection mapping, digital dome and planetarium projection, and laser phosphor rear-projection systems. Others at 22.7% encompasses OLED commercial displays, MicroLED, e-Paper, and emerging display technologies, including holographic and flexible/rollable display formats.

Regional Market Insights

|

Region |

Share (2025) |

Key Digital Signage Market Drivers & Characteristics |

|

North America |

37.2% |

Driven by strong adoption of programmatic DOOH advertising, advanced retail digitalization, and widespread deployment of interactive display technologies across commercial sectors. |

|

Asia Pacific |

28.6% |

Driven by rapid urbanization, smart city development, expanding retail infrastructure, and increasing investments in large-format LED and interactive display technologies. |

|

Europe |

20.4% |

Characterized by strong demand for energy-efficient display systems, sustainable advertising technologies, and growing deployment of smart transportation and public information displays. |

|

Latin America |

7.3% |

Supported by expanding retail modernization, rising digital advertising adoption, and increasing investments in transportation and hospitality infrastructure. |

|

Middle East and Africa |

6.5% |

Growing due to rising smart city projects, luxury retail expansion, tourism infrastructure development, and increasing adoption of large-scale outdoor digital displays. |

North America's 37.2% market share is anchored by the world's most sophisticated DOOH advertising ecosystem, the world's highest QSR digital menu board density, and the world's largest enterprise digital signage installation base.

Asia Pacific, at 28.6%, is led by China's world-leading outdoor LED spectaculars and Japan's precision transit and retail signage culture, with India's rapidly growing digital signage market as the region's highest-growth national market. Europe, at 20.4%, features JCDecaux's global DOOH leadership, the UK's sophisticated transit digital signage network, and EU sustainability regulation driving energy-efficient display procurement. Latin America, at 7.3%, is growing through Brazil and Mexico QSR digital menu board rollout and urban outdoor digital advertising conversion, driving the expansion of the Digital Signage Market in Latin America. Middle East and Africa, at 6.5%, is anchored by Dubai's spectacular retail and outdoor digital environments and growing smart city digital infrastructure investments.

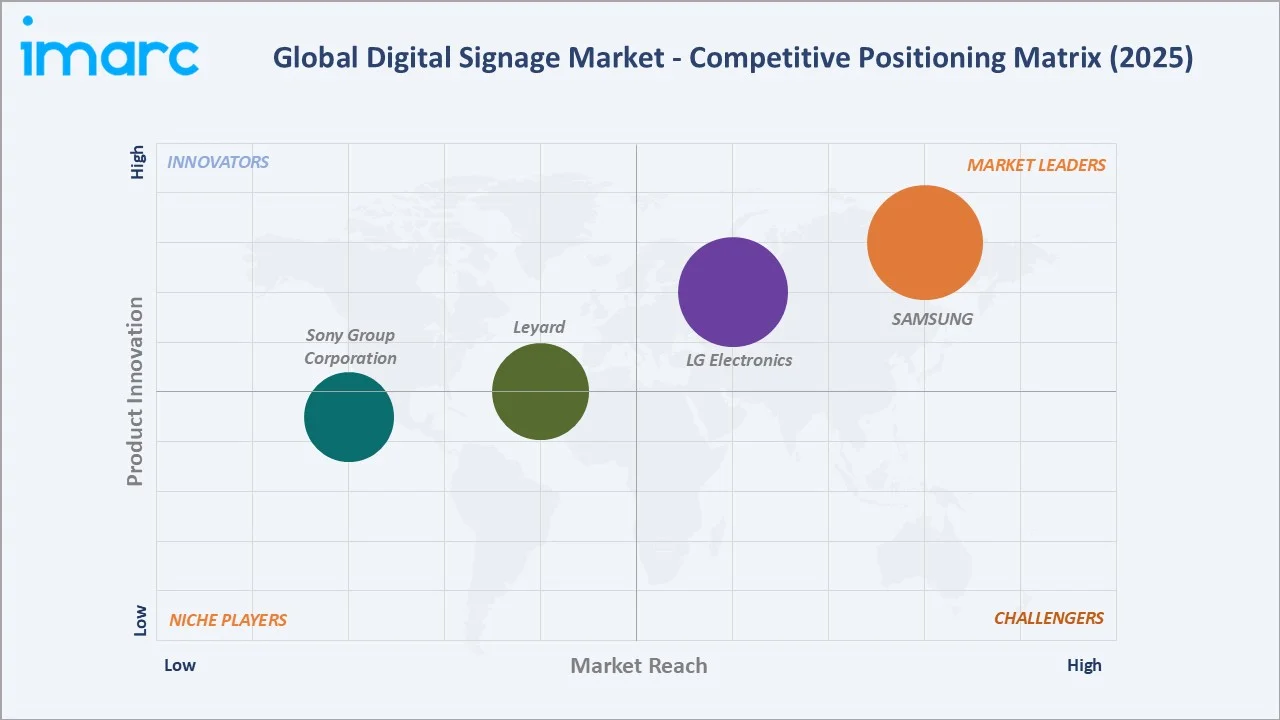

Competitive Landscape

The global digital signage competitive landscape features hardware-dominant competition at the display and media player levels, technology-specific competition in specialized segments, and software competition at the CMS level. The competitive dynamics are increasingly shifting from hardware specification competition toward platform and ecosystem competition.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

SAMSUNG |

QLED 8K Signage, Crystal UHD Signage, Spatial Signage, The Wall |

Market Leader |

Strong expertise in advanced display technologies, ultra-high-resolution commercial signage solutions, and smart display ecosystems. |

|

LG Electronics |

LED Indoor Signage, LED Outdoor Signage, OLED signage |

Market Leader |

LG's OLED Signage provides a lifelike expression of all colours in the ultimate design. LG's LED Signage consists of a wide range of indoor and outdoor signage. |

|

Leyard |

NCV Series, LA Series, SV Indoor Series, Planar Systems |

Established Player |

As the world's premier display provider, Leyard provide display products to any customer, at any time. |

|

Sony Group Corporation |

BRAVIA Signage Free |

Established Player |

Premium professional display technologies and entertainment digital signage applications. |

The competitive landscape is being reshaped by the display technology transition, investments in MicroLED and direct-view LED alongside OLED commercial display, and MicroLED leadership is progressively obsoleting the LCD-only competitive positioning of lower-tier commercial display competitors.

Key Company Profiles

SAMSUNG

Samsung is the world's largest commercial display manufacturer and the digital signage market's dominant hardware supplier, with Samsung Business's SMART Signage division generating high commercial display revenue.

- Key Products: QLED 8K Signage, Crystal UHD Signage, Spatial Signage, and The Wall.

- Recent Developments: In February 2026, Samsung Electronics announced the expansion of its commercial display portfolio at ISE 2026 in Barcelona, highlighted by the global debut of Samsung Spatial Signage. The company also introduced new AI-powered content capabilities through Samsung VXT, expanded its supersized commercial display lineup, and strengthened enterprise collaboration with Cisco-certified wide-format display solutions. Samsung stated that the integration of glasses-free 3D Spatial Signage and AI-enhanced content technologies is aimed at delivering more immersive and engaging commercial display experiences across diverse business environments.

- Strategic Focus: Focused on expanding AI-powered, immersive, and ultra-large-format digital signage solutions to strengthen commercial display experiences across retail, corporate, transportation, and smart infrastructure sectors.

LG Electronics

LG Electronics is Samsung's primary competitor in commercial display and digital signage, with world-leading OLED commercial display technology creating meaningful differentiation beyond the LCD commodity competition.

- Key Products: LED Indoor Signage, LED Outdoor Signage, OLED signage.

- Recent Developments: In January 2025, LG Electronics USA and BrightSign LLC collaborated, resulting in a new series of LG ultra-high definition (UHD) digital signage displays running BrightSignOS.

- Strategic Focus: Focused on advancing OLED and advanced commercial display technologies to enhance interactive digital signage solutions for retail, hospitality, transportation, and enterprise environments.

Market Concentration Analysis

The global digital signage market is moderately concentrated at the hardware level and fragmented at the software and services levels. Samsung and LG Electronics solutions together hold approximately 50-55% of global commercial display hardware revenue, a dominant position maintained through their integrated LCD panel manufacturing and their respective software ecosystem investments. The CMS software segment is highly fragmented but holds only 5-8% of the total global digital signage CMS market.

Market concentration at the total industry level is declining as the software and services segments grow faster than hardware, Samsung and LG Electronics’ combined 50-55% hardware share equates to a 40-45% share of the total digital signage market, and as software and service grow from 22.5% to 27-30% of total market by 2034, hardware leaders' total market concentration will diminish even without losing hardware market share. This dynamic favors CMS software and managed service vendors who are growing their total market share faster than hardware vendors despite smaller absolute revenues.

Investment & Growth Opportunities

Highest Growth Segments

Service component (~7.2% CAGR), software component (~6.4% CAGR), projection technology (~5.6% CAGR), MicroLED/OLED/Others technology (~6.0%+ CAGR), and programmatic DOOH software infrastructure (~20-25% CAGR for programmatic DOOH as a sub-segment of digital signage software) represent the global digital signage market's highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Retail media network infrastructure represents one of digital signage's most commercially compelling emerging opportunities. Each major grocery, pharmacy, and mass merchant retailer converting its in-store digital signage from cost-center to profit-center creates digital signage investment justification that purely cost-based ROI models cannot match.

Investment Themes

- Programmatic DOOH software infrastructure scaling as data-driven outdoor advertising transforms media owner economics: Programmatic DOOH SSP (supply-side platform) software connecting digital signage media owners to programmatic ad demand generates 5-10% transaction fee revenue on advertising traded through the platform.

- Healthcare digital signage managed services as recession-resistant recurring revenue business: Healthcare digital signage operates under procurement cycles determined by capital planning and is increasingly specified as a 5-10 year managed service contract where the vendor provides hardware, software, content, and field maintenance in a monthly per-screen fee structure.

Future Market Outlook (2026-2034)

The global digital signage market is projected to grow from USD 30.08 Billion in 2025 to USD 49.41 Billion by 2034, delivering a 5.38% CAGR over the forecast period. The market's anchor value of USD 39.10 Billion in 2030 represents a digital signage industry where MicroLED display technology has achieved mainstream commercial deployment in premium retail, hospitality, and corporate applications; AI-powered content management has become standard CMS functionality rather than a premium add-on; programmatic DOOH advertising; and the global installed digital signage base requiring ongoing software licensing, maintenance, and upgrade investment.

Three structural forces define global digital signage market growth through 2034 with high confidence: the secular conversion of static to digital signage in public and commercial environments, the technology-driven service model transition, and the emergence of digital signage as advertising infrastructure.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including VP of Business Sales; Digital Signage Product Management Directors; digital signage system integration VPs; DOOH media technology directors; programmatic DOOH platform executives; and end-user digital signage program managers.

Secondary Research

Secondary research encompassed Digital Signage Federation (DSF) Market Statistics 2025; Market Intelligence Industry Outlook 2025; Company Annual Reports; press releases and analyst briefing materials; industry white papers; Global Out-of-Home Advertising Report; DPAA (Digital Place-Based Advertising Association) programmatic DOOH benchmarking study 2025; Consulting Professional Display Market Report 2024. Over 55 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up component and technology models calibrated against revenue disclosures, market sizing, Samsung and LG Electronics commercial display shipment data, and SaaS revenue modeling. Key forecast inputs include commercial display panel price decline curves, MicroLED production cost reduction projections, programmatic DOOH advertising spend growth, and QSR/retail digital signage replacement cycle timing calibrated against individual chain digital menu board installation vintage data.

Digital Signage Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Video Walls, Video Screen, Transparent LED Screen, Digital Poster, Kiosks, Others |

| Components Covered | Hardware, Software, Service |

| Technologies Covered | LCD/LED, Projection, Others |

| Applications Covered | Retail, Hospitality, Entertainment, Stadiums and Playgrounds, Corporate, Banking, Healthcare, Education, Transport, Others |

| Locations Covered | Indoor, Outdoor |

| Sizes Covered | Below 32 Inches, 32 To 52 Inches, More Than 52 Inches |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | SAMSUNG, LG Electronics, Leyard, Sony Group Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the digital signage market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global digital signage market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the digital signage industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Digital Signage Market Report

The global digital signage market reached USD 30.08 Billion in 2025, driven by retail and QSR digital transformation investment, smart city and transit infrastructure expansion, programmatic DOOH advertising ecosystem growth, LED display technology cost reduction enabling new application segments, and the corporate hybrid work digital communication investment driving workplace signage deployment.

The market grows at 5.38% CAGR during 2026-2034, reaching USD 49.41 Billion by 2034, driven by MicroLED mainstream commercial deployment, AI-powered content management becoming standard CMS capability, programmatic DOOH, secular conversion of static to digital signage expanding the installed base, and service model transition from one-time hardware to recurring SaaS and managed service revenue.

Hardware leads at 77.5% through commercial display panels, media players, and mounting systems, representing the majority of the project cost.

LCD/LED leads at 44.8% as the default technology for retail, QSR, corporate, healthcare, and transit applications, where daylight-readable performance at declining price points sustains deployment volume.

North America leads at 37.2% through the world's most sophisticated programmatic DOOH advertising ecosystem, the highest QSR digital menu board density, and the largest enterprise digital signage installed base.

Leading companies include SAMSUNG, LG Electronics, Leyard, and Sony Group Corporation, among others.

The market is projected to reach approximately USD 39.10 Billion by 2030, with MicroLED enabling premium retail and hospitality mainstream deployment, AI-powered content management standard in leading CMS platforms, programmatic DOOH growth, and the global installed digital signage base requiring ongoing software licensing, content management, and hardware refresh investment.

Programmatic Digital Out-of-Home (pDOOH) enables real-time, audience-targeted advertising purchase on digital outdoor and indoor screens using programmatic auction mechanisms identical to online display advertising.

MicroLED uses microscale LED chips transfer-printed onto glass substrates to create self-emissive, infinite-contrast, high-brightness displays with LCD-level resolution in any size configuration.

AI is transforming digital signage at three levels. Content optimization AI: ML models analyzing historical audience engagement data to automatically schedule content types that generate the highest dwell time and brand recall for the current audience profile. Generative AI content creation: enabling CMS platforms to auto-generate promotional visuals from product data without human graphic design. Real-time trigger AI: AI systems monitor audience analytics, POS data, weather, and inventory levels to trigger contextually relevant content without human CMS operator intervention, reducing content operations labor cost while increasing signage relevance and conversion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)