eHealth Market Size, Share, Trends and Forecast Report by Product, Services, End User, and Region, 2026-2034

eHealth Market Size, Share, Trends & Forecast (2026-2034)

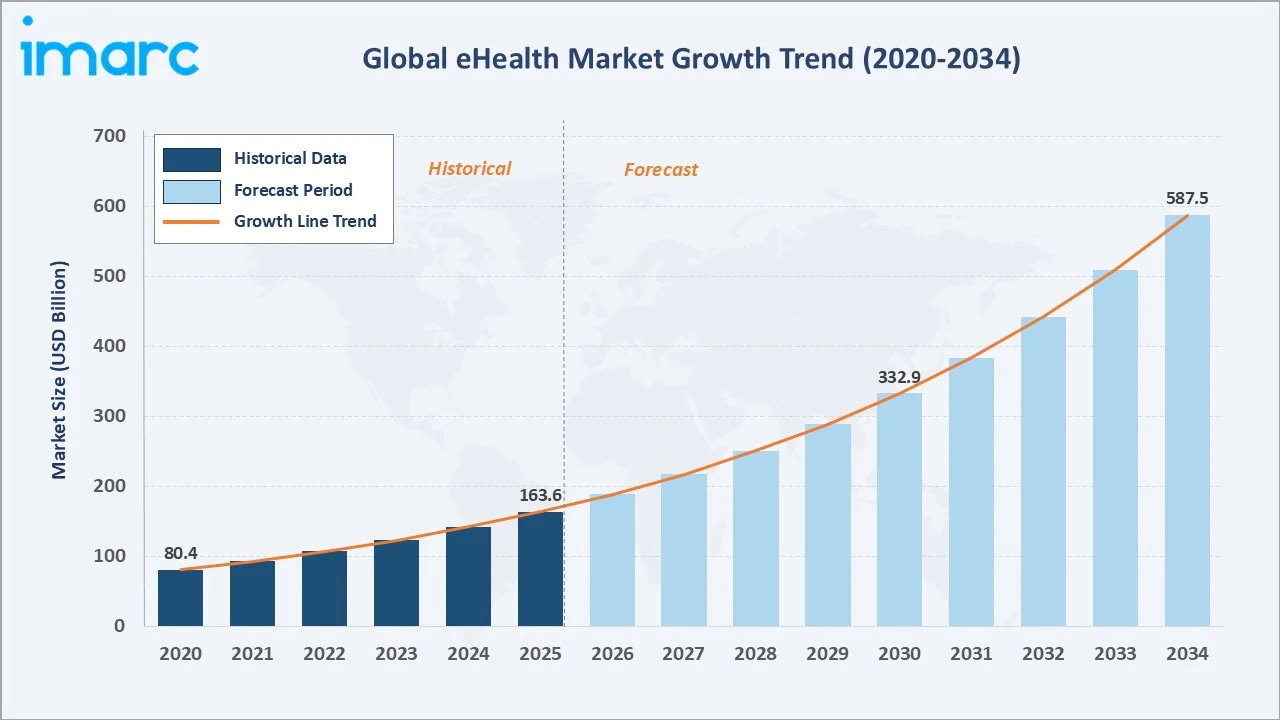

The global eHealth market reached USD 163.6 Billion in 2025 and is projected to reach USD 587.5 Billion by 2034, exhibiting a CAGR of 15.30% during 2026-2034. Growth is anchored by accelerating digital transformation across healthcare systems, the rising prevalence of chronic diseases, an aging global population, government digital health initiatives, and rapid integration of AI, cloud computing, IoT, and mobile health solutions.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 163.6 Billion |

|

Market Forecast (2034) |

USD 587.5 Billion |

|

CAGR (2026-2034) |

15.30% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

Key drivers include the rise of telemedicine, electronic health records (EHRs), mobile health applications, remote patient monitoring, and AI-enabled diagnostics, which collectively enhance accessibility, efficiency, and personalized care.

To get more information on this market, Request Sample

Growing patient demand for convenience, government initiatives promoting healthcare digitization, and investments in interoperable health IT infrastructure are further accelerating adoption.

Executive Summary

The global eHealth market accounted for USD 163.6 Billion in 2025 and is expected to reach USD 587.5 Billion by 2034. It is among the fastest-growing healthcare technology categories, expanding at a 15.30% CAGR through 2034 amid sustained digital transformation across providers, payers, and patient channels.

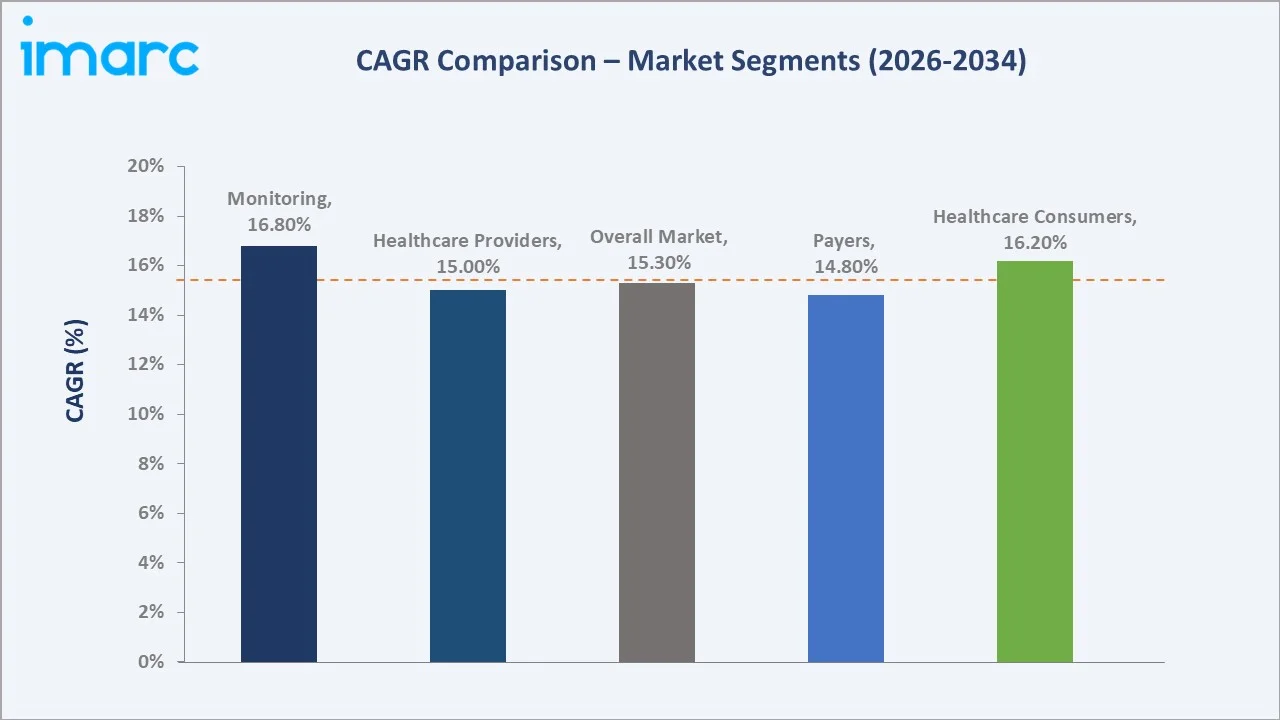

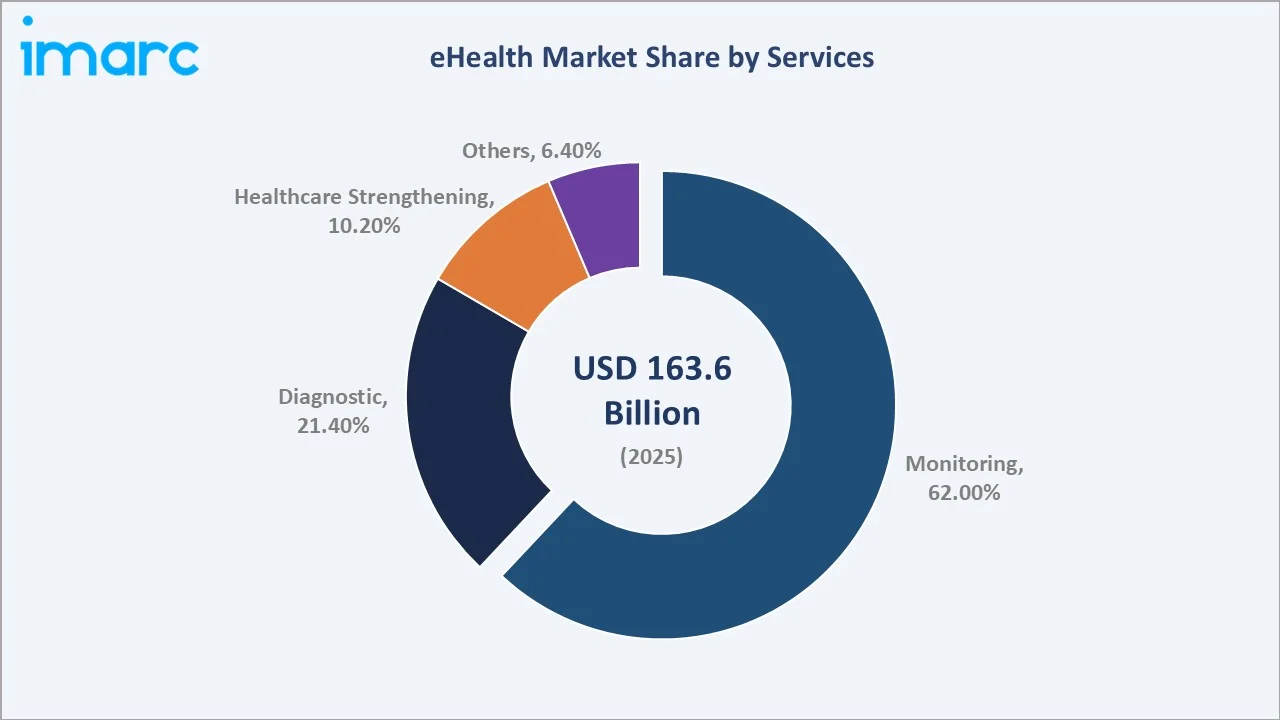

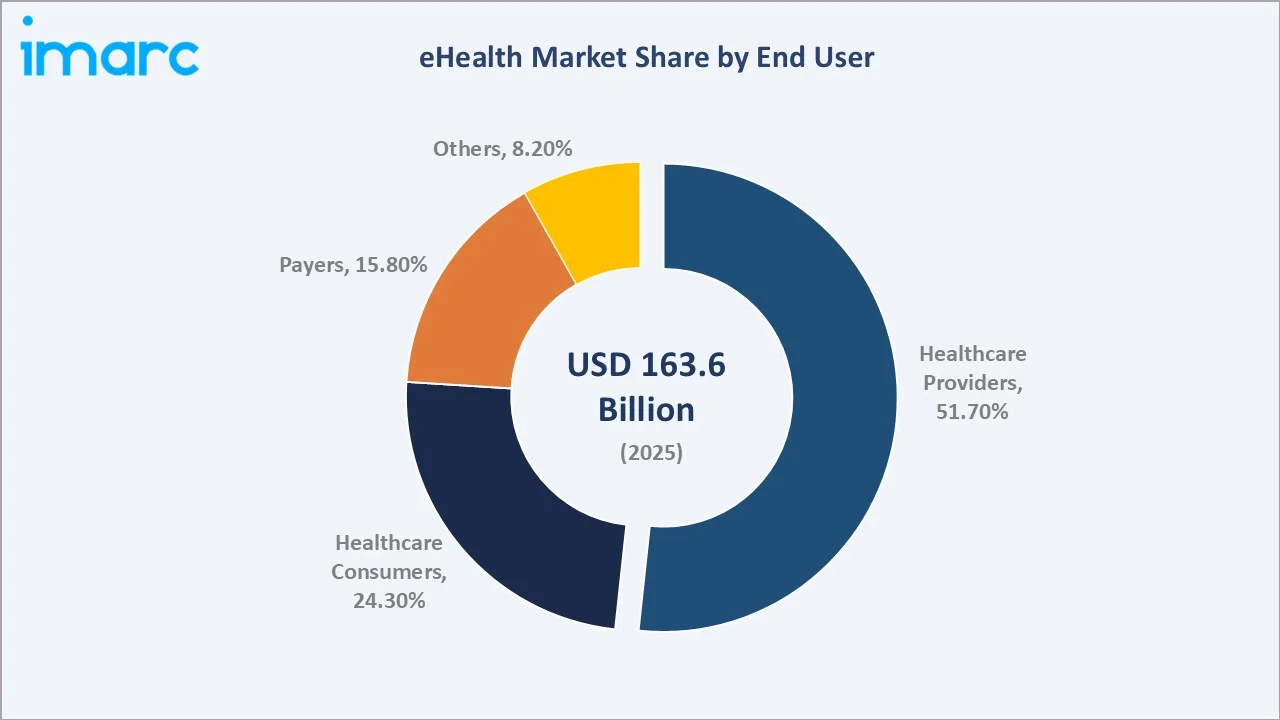

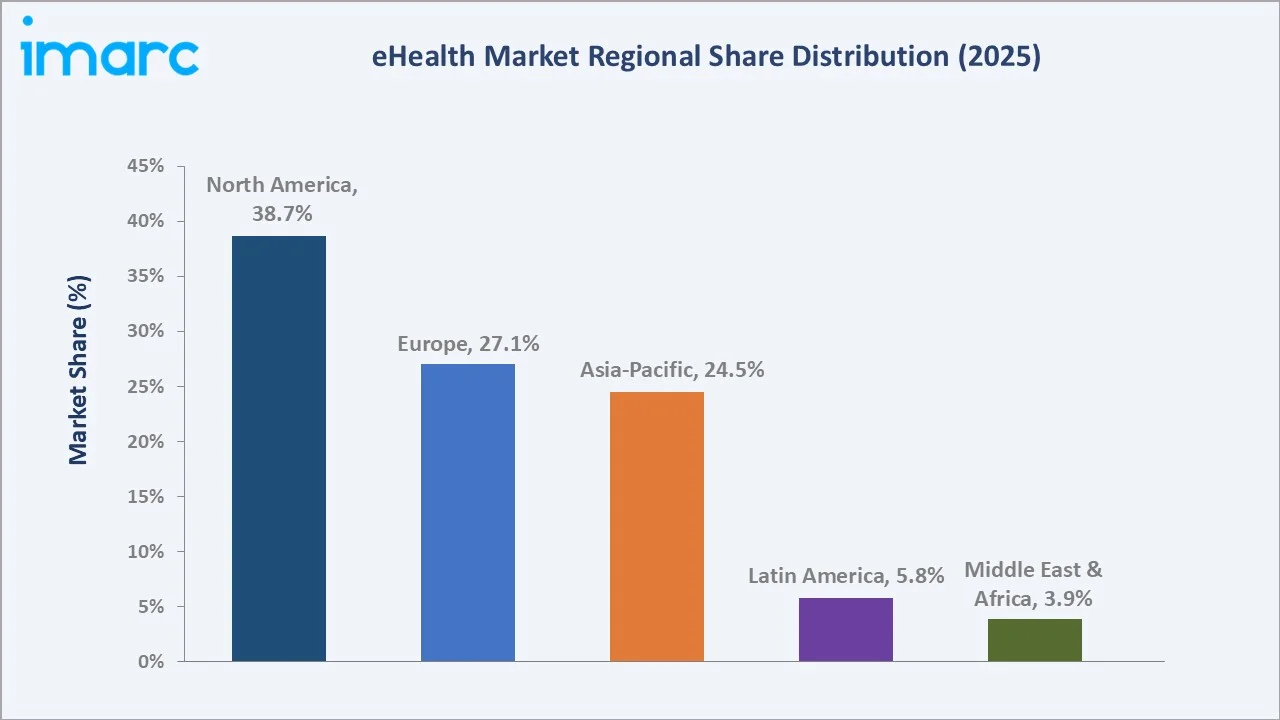

Approximately 96% of non-federal acute care hospitals in the United States have implemented certified electronic health record (EHR) systems, and the World Health Organization estimates that 70% of healthcare providers globally are adopting digital strategies. Monitoring services dominate the service mix at 62.0% share, healthcare providers anchor end-user demand at 51.7%, and North America retains regional leadership at 38.7% of global revenue.

Key 2024–2025 milestones include the July 2025 White House and Centers for Medicare & Medicaid Services (CMS) initiative to build a patient-centric healthcare ecosystem with FHIR-based APIs and CMS-Aligned Networks involving 60+ organizations; the January 2024 launch of Eli Lilly and Company’s LillyDirect direct-to-consumer telehealth platform for diabetes, obesity, and migraine therapies; and the April 2024 launch of eHealth Inc.'s eHealth ePerks rewards program with 200,000+ Medicare customers.

Key Market Insights

|

Indicator |

Value (2025) |

|

Leading Services |

Monitoring (62.0%) |

|

Leading End User |

Healthcare Providers (51.7%) |

|

Fastest-Growing Services |

Monitoring (~16.8% CAGR) |

|

Fastest-Growing End User |

Healthcare Consumers (~16.2% CAGR) |

|

Largest Region |

North America (38.7%) |

|

Key Players (Top 5) |

Oracle, Epic Systems Corporation, Veradigm LLC, athenahealth, Inc., Koninklijke Philips NV |

Key Analytical Observations Supporting the Above Data:

- Monitoring services account for 62.0% of the global eHealth market in 2025, reflecting strong demand for remote patient monitoring (RPM), wearable device integration, chronic-disease management platforms, and continuous biometric tracking across hospital and home settings.

- Diagnostic services at 21.4% (2025) encompass AI-enabled imaging analysis, point-of-care diagnostics integration, lab information systems, and clinical decision support tools, with rapid adoption driven by FDA-cleared AI diagnostic devices and pathology automation.

- Healthcare providers lead end-user adoption at 51.7% (2025), encompassing hospitals, clinics, ambulatory care, and home-health operators. Healthcare consumers at 24.3% (2025) reflect the use of direct-to-consumer telehealth, patient portals, and mobile health applications.

- Payers at 15.8% (2025) include health insurers, government payment programs, and integrated payer-provider organizations adopting analytics-led population health management and care coordination platforms.

- North America's 38.7% regional share reflects 96% acute-care hospital EHR adoption in the United States, the July 2025 CMS patient-centric ecosystem initiative, and the highest concentration of eHealth venture capital and major listed eHealth vendors.

eHealth Market Overview

eHealth refers to the application of information and communications technologies (ICTs) across healthcare delivery, public health, and clinical research. The category spans electronic health records (EHR/EMR), telehealth and telemedicine platforms, mobile health (mHealth) applications, remote patient monitoring (RPM), health information exchanges (HIE), e-prescribing, clinical decision support systems, healthcare analytics, and AI-enabled diagnostic and management tools.

Approximately 96% of US acute-care hospitals have implemented certified EHR systems, and 70% of healthcare providers globally are adopting digital tools according to WHO data. The 21st Century Cures Act and its Cures Rule have accelerated FHIR API adoption, with most United States hospitals now enabling patient access to apps of their choice. Government initiatives across North America, Europe, and Asia-Pacific continue to expand the addressable opportunity through digital health funding, interoperability mandates, and reimbursement support.

Market Dynamics

To evaluate market opportunities, Request Sample

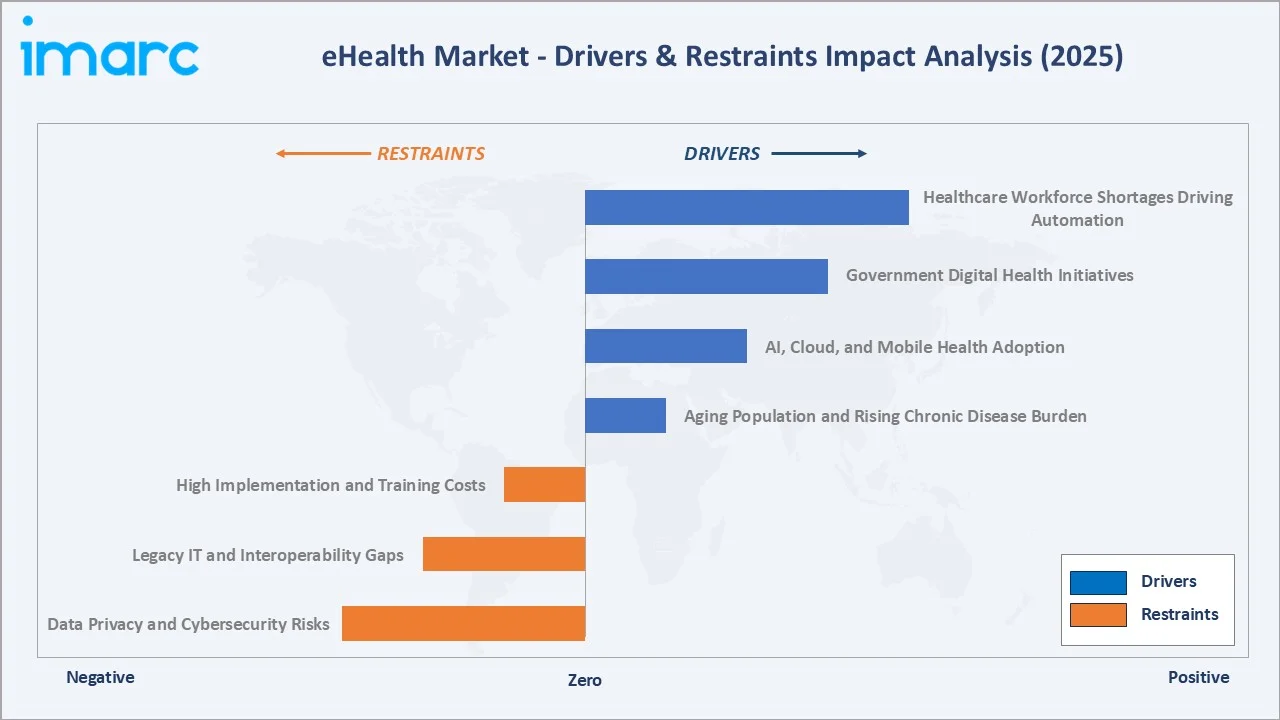

Market Drivers

- Aging Population and Rising Chronic Disease Burden: Global population aging and rising prevalence of chronic conditions including diabetes, cardiovascular disease, and cancer are driving structural demand for continuous monitoring, telehealth consultations, and digital therapeutic interventions.

- AI, Cloud, and Mobile Health Adoption: Rapid integration of AI, cloud computing, IoT, and mobile health across diagnostic imaging, clinical workflows, and patient engagement is accelerating eHealth platform adoption. Hybrid and multicloud strategies are scaling data interoperability, while AI is automating clinical documentation, predictive analytics, and treatment recommendations.

- Government Digital Health Initiatives: Major government programs worldwide are accelerating eHealth adoption. In July 2025, the White House and CMS launched a national initiative for a patient-centric healthcare ecosystem with FHIR-based APIs and CMS-Aligned Networks involving 60+ organizations. Mauritius launched the One Patient One Record project in January 2024.

- Healthcare Workforce Shortages Driving Automation: Persistent healthcare workforce shortages across nursing, primary care, and specialty clinicians are accelerating adoption of AI-assisted documentation, virtual care, and remote patient monitoring. Digital tools redistribute clinical workload, support care continuity, and enable scaled service delivery.

Market Restraints

- Data Privacy and Cybersecurity Risks: Healthcare data is among the most sensitive personal information, with stringent compliance obligations under HIPAA, GDPR, and equivalent national frameworks. Escalating ransomware and data-breach incidents continue to drive cybersecurity investment requirements and impose significant operational risk.

- Legacy IT and Interoperability Gaps: Many healthcare systems operate fragmented legacy IT environments. Achieving interoperability across vendors, care settings, and national systems requires substantial investment, FHIR API adoption, and change management. Integration complexity remains a barrier despite regulatory mandates.

- High Implementation and Training Costs: Enterprise eHealth deployments require multi-year capital investment in software, hardware, integration services, and workforce training. Small and mid-sized practices face disproportionate cost burdens, slowing penetration in resource-constrained settings.

Market Opportunities

- AI-Powered Diagnostic and Decision-Support Platforms: AI clinical decision support, computer vision in radiology, and predictive analytics are scaling rapidly. Vendors with FDA-cleared, regulator-approved AI portfolios are positioned for multi-year contract value as health systems integrate AI into core clinical workflows.

- Direct-to-Consumer Telehealth Models: Eli Lilly and Company’s January 2024 launch of LillyDirect, an online platform enabling direct telehealth access for diabetes, obesity, and migraine therapies, exemplifies the rapidly expanding D2C telehealth opportunity. Pharma-led and platform-led direct telehealth models are expanding consumer-pay revenue.

Market Challenges

- Regulatory and Reimbursement Variability: Reimbursement frameworks for telehealth, RPM, and digital therapeutics vary substantially across countries and US states, with shifting policy environments affecting deployment economics. Coverage policy fragmentation slows speed-to-market for new digital health offerings.

- Digital Literacy and Access Inequalities: Older adults, low-income populations, and rural residents face barriers to digital health adoption, risking widening health disparities. Differences in broadband access, device ownership, and digital skills slow deployment in underserved communities and limit market reach.

Emerging Market Trends

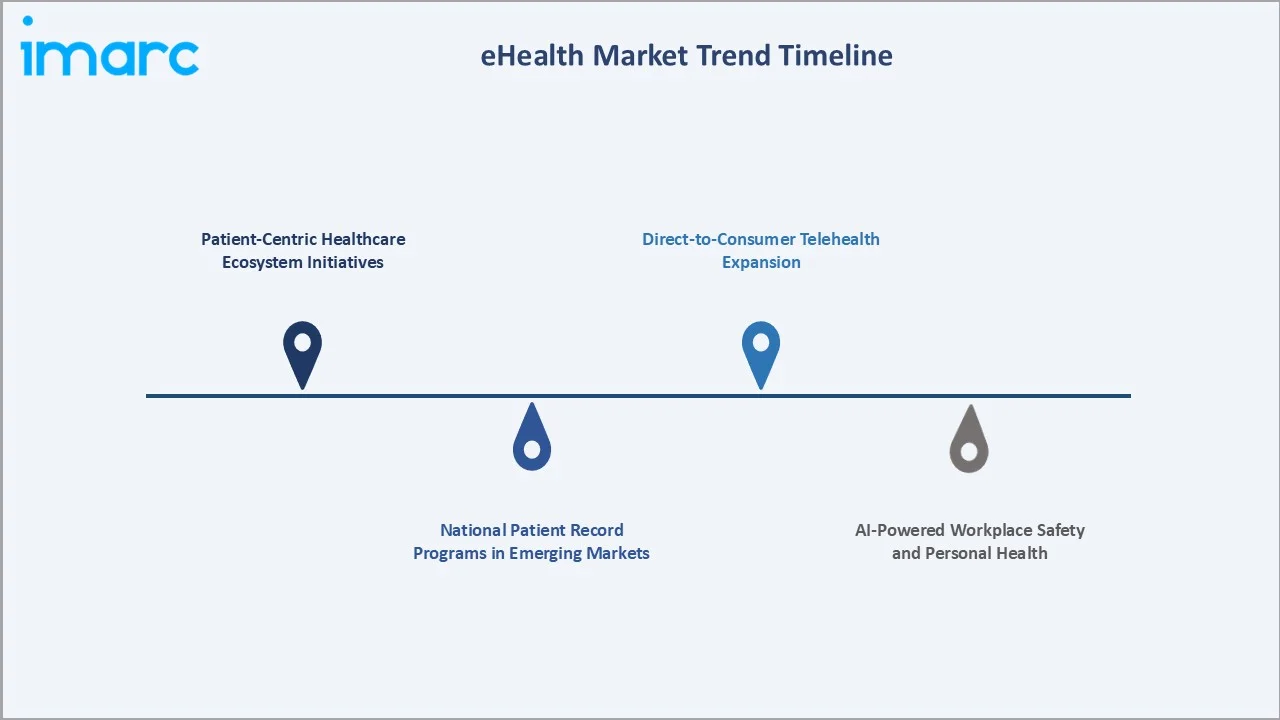

1. Patient-Centric Healthcare Ecosystem Initiatives

In July 2025, the White House and CMS announced a national initiative to build a patient-centric healthcare ecosystem focused on interoperability, secure data exchange, and integration of EHRs with digital health platforms across the US healthcare system. The program involves commitments from 60+ organizations, including major tech companies, supporting CMS-Aligned Networks, FHIR-based APIs, and a national provider directory.

2. Direct-to-Consumer Telehealth Expansion

In January 2024, Eli Lilly and Company launched LillyDirect, an online platform that simplifies patient access to prescription drugs for diabetes, obesity, and migraine through independent telehealth providers. The platform exemplifies the D2C telehealth model that integrates pharmaceutical brands with digital prescribing, dispensing, and patient support, expanding pharma-aligned revenue streams.

3. AI-Powered Workplace Safety and Personal Health

In October 2024, RED.Health launched the RED Assist app, an AI-powered workplace safety solution offering ambulance booking, GP consultation, emergency room consultation, SOS alerts, and women's safety features. Powered by RED AI with real-time health guidance, the app illustrates the integration of AI personal assistants into mainstream consumer health.

4. National Patient Record Programs in Emerging Markets

In January 2024, the Republic of Mauritius launched the One Patient One Record project, leveraging state-of-the-art technology to enable cost-efficient, patient-centric, and accountable healthcare. Similar national EHR programs across emerging markets are accelerating eHealth deployment opportunities for global vendors with localization and compliance capabilities.

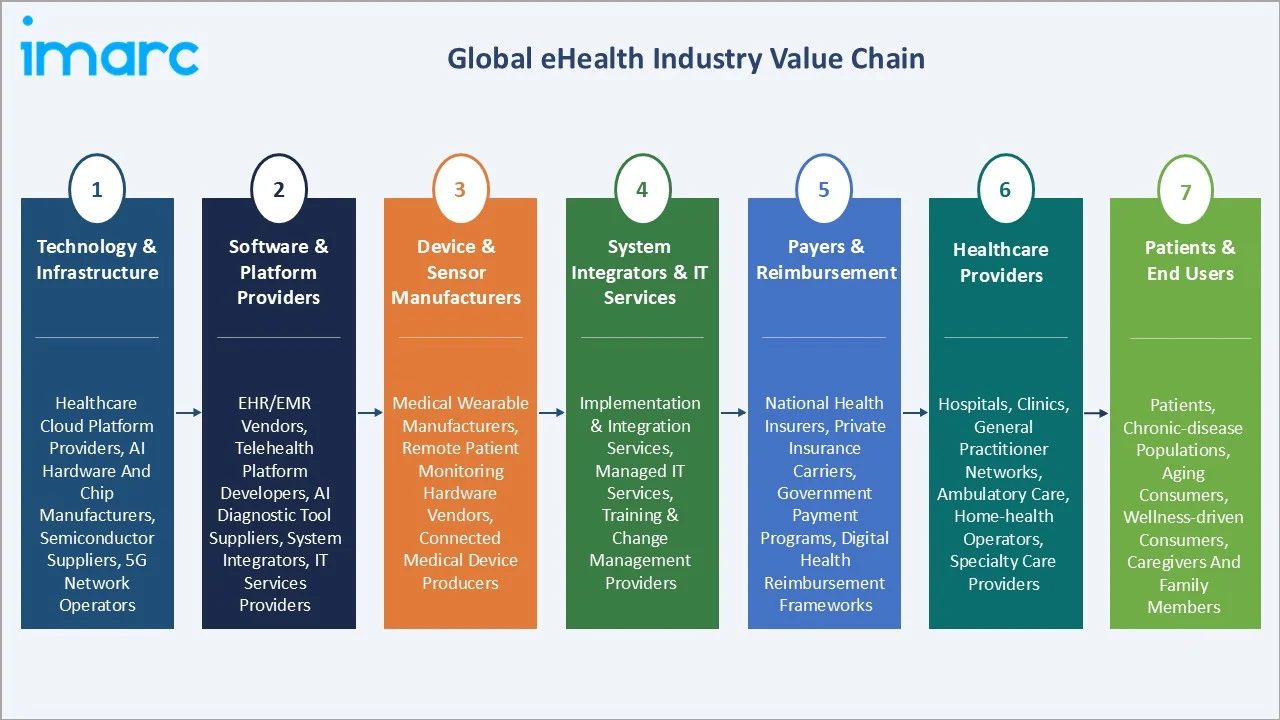

Industry Value Chain Analysis

|

Stage |

Key Players / Activities |

|

Technology & Infrastructure |

Healthcare cloud platform providers, AI hardware and chip manufacturers, semiconductor suppliers, 5G network operators |

|

Software & Platform Providers |

EHR/EMR vendors, telehealth platform developers, AI diagnostic tool suppliers, mobile health application developers |

|

Device & Sensor Manufacturers |

Medical wearable manufacturers, remote patient monitoring hardware vendors, connected medical device producers |

|

System Integrators & IT Services |

Implementation & integration services, managed IT services, training & change management providers |

|

Payers & Reimbursement |

National health insurers, private insurance carriers, government payment programs, digital health reimbursement frameworks |

|

Healthcare Providers |

Hospitals, clinics, general practitioner networks, ambulatory care, home-health operators, specialty care providers |

|

Patients & End Users |

Patients, chronic-disease populations, aging consumers, wellness-driven consumers, caregivers and family members |

Technology Landscape in the eHealth Industry

Cloud-Based EHR and Clinical Platforms

Vendors are advancing scalable, modular offerings that can be deployed in large hospital systems and small practices alike. Voice-based data entry, predictive analytics for chronic disease management, and blockchain integration for secure patient data sharing are being piloted across North America, Europe, and Asia-Pacific.

AI and Machine Learning Diagnostic Tools

AI applications span medical imaging, pathology, clinical decision support, and population health analytics. FDA-cleared AI diagnostic devices, voice-over charting, and treatment recommendation engines are increasingly embedded in EHR and imaging platforms. AI is also automating revenue cycle management, prior authorization, and clinical documentation across major health systems.

Wearables, Remote Patient Monitoring, and Connected Devices

Connected medical wearables and home RPM devices enable continuous health data capture. Apple, Fitbit, and Samsung consumer wearables integrate with Philips, Medtronic, and other medical-grade RPM platforms. Wearable adoption is supported by Medicare RPM reimbursement codes and chronic-disease management protocols.

Telehealth Platforms and Digital Therapeutics

Teladoc Health, Doximity, Amwell, and emerging direct-to-consumer telehealth platforms anchor virtual care delivery. Digital therapeutics (DTx) span chronic-disease, mental health, and rehabilitation applications. The LillyDirect launch (January 2024) and similar pharma-led platforms illustrate the convergence of pharmaceutical brands with telehealth delivery.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Services | Monitoring | 62.0% | 2025 |

| End User | Healthcare Providers | 51.7% | 2025 |

| Product | 🔒 | 🔒 | 2025 |

| Region | North America | 38.7% | 2025 |

By Services

Monitoring services dominate with a 62.0% share in 2025, reflecting strong demand for remote patient monitoring, wearable device integration, chronic-disease management platforms, and continuous biometric tracking. Monitoring is projected to grow at approximately 16.8% CAGR through 2034, the fastest among service segments, supported by Medicare RPM reimbursement codes and chronic-disease management programs.

To access detailed market analysis, Request Sample

Diagnostic services account for 21.4% in 2025, encompassing AI-enabled imaging analysis, point-of-care diagnostics integration, lab information systems, and clinical decision support tools. Healthcare strengthening services at 10.2% include health information exchanges, population health management, and care coordination platforms.

By End User

Healthcare providers lead with a 51.7% share in 2025, encompassing hospitals, clinics, ambulatory care, specialty centers, and home-health operators. Providers anchor enterprise EHR adoption, clinical workflow automation, and integrated care delivery. The segment is supported by mandatory EHR adoption requirements and meaningful use incentive frameworks in major markets.

Healthcare consumers at 24.3% reflect direct-to-consumer telehealth, patient portals, mobile health applications, and wellness-driven self-monitoring. Payers at 15.8% include health insurers, government payment programs, and integrated payer-provider organizations leveraging analytics for population health management.

Regional Market Insights

North America leads at 38.7% in 2025, supported by 96% acute-care hospital EHR adoption in the United States and the global concentration of major listed eHealth vendors including Oracle, Epic Systems Corporation, and Veradigm LLC. Canada's national digital health strategies and provincial health information exchange programs add to regional scale.

Europe at 27.1% holds the second-largest share, anchored by the European Health Data Space (EHDS) regulation, EU AI Act compliance, and national digital health strategies across Germany, France, the UK, Italy, and the Nordics.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.7% |

Acute-care hospital EHR adoption; CMS patient-centric initiative; major listed eHealth vendor concentration; venture capital depth |

|

Europe |

27.1% |

National digital health strategies; aging population and chronic disease burden |

|

Asia-Pacific |

24.5% |

Rapid digital health adoption; government national EHR initiatives; large mobile health user base; expanding telemedicine |

|

Latin America |

5.8% |

Growing telehealth penetration; expanding mobile health adoption; government digital health investments and EHR rollouts |

|

Middle East and Africa |

3.9% |

GCC national digital health strategies; Mauritius One Patient One Record project; emerging telemedicine adoption |

Asia-Pacific at 24.5% reflects rapid digital health adoption across China, India, and Japan, supported by government national EHR initiatives and a large mobile health user base. Latin America (5.8%) and Middle East and Africa (3.9%) are emerging markets with significant headroom as national digital health programs scale.

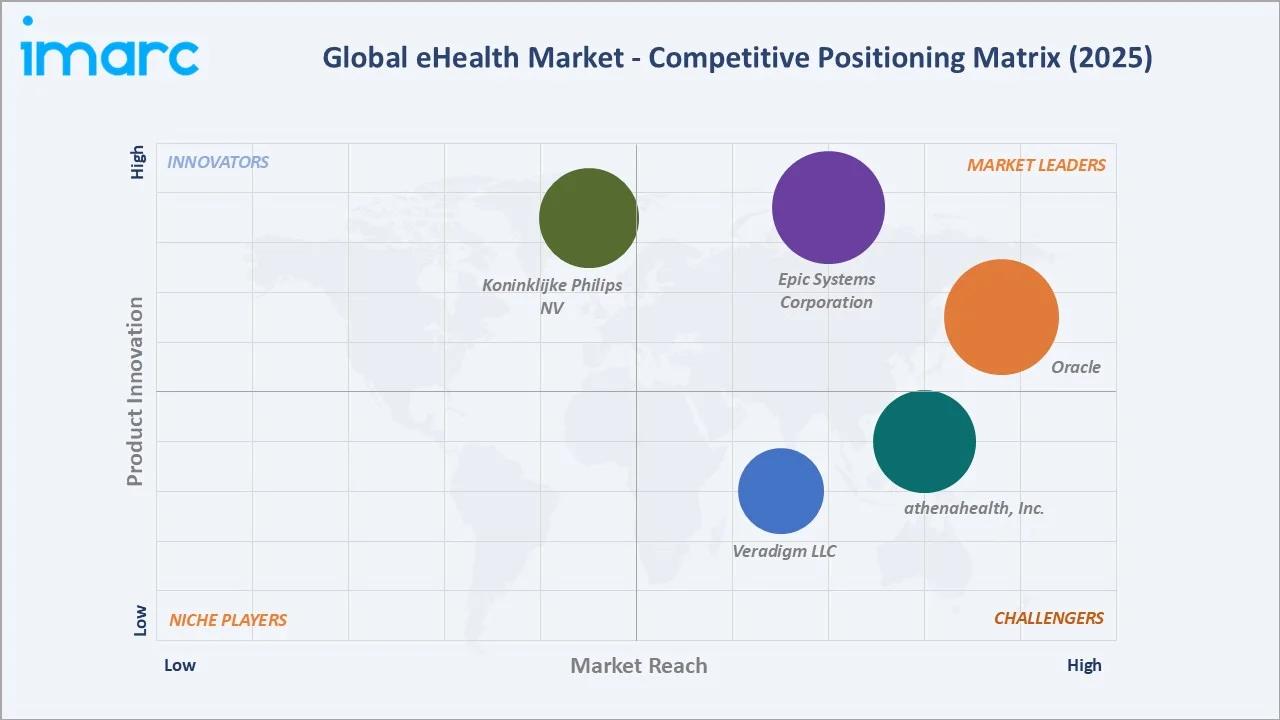

Competitive Landscape

The global eHealth market is moderately fragmented, with leading players across enterprise EHR vendors, diversified medical technology companies, digital health platforms, and emerging direct-to-consumer specialists. Key players include Oracle, Epic Systems Corporation, Veradigm LLC, athenahealth, Inc., and Koninklijke Philips NV.

|

Company Name |

Platform/Services |

Market Position |

Core Strength |

|

Oracle |

Clinical applications, payer operations, population health, security, services and support, enterprise solutions, Cerner Millennium EHR platform |

Market Leader |

Enterprise EHR platform leadership; cloud-based clinical information systems; AI-enabled clinical workflows |

|

Epic Systems Corporation |

National Telehealth Providers, Remote Patient Monitoring, Appointment Scheduling, Patient Financial Experience, among others |

Market Leader |

MyChart patient portal with significant user base; enterprise-grade interoperability and clinical specialty modules |

|

Veradigm LLC |

AI patient scheduling, EHR software, ePrescribe, gap closure alerting, eChart courier, Veradigm Payerpath, patient engagement platform, among others |

Challenger |

Diversified EHR and revenue cycle management portfolio; ambulatory and acute care platforms; analytics and population health |

|

athenahealth, Inc. |

Electronic health record, medical billing & practice management software, patient engagement, payer solutions, athenaIDX, among others |

Strong Challenger |

Cloud-native EHR and practice management; ambulatory care specialization; network-effects platform and revenue cycle services |

|

Koninklijke Philips NV |

Acute care informatics, Cloud solutions, Diagnostic and clinical informatics |

Innovator |

Cloud platform; connected care and remote patient monitoring portfolio |

The competitive structure includes enterprise EHR specialists, integrated medtech platforms, and rapidly emerging telehealth-focused entrants.

Key Company Profiles

Oracle

Oracle is a global leader in enterprise EHR platforms, hospital information systems, and cloud-based clinical analytics. Oracle serves health systems with the Cerner Millennium platform alongside new cloud-native applications.

- Product Portfolio: Cerner Millennium EHR platform, hospital information systems, cloud-based clinical data analytics, revenue cycle management, population health management, and integrated patient engagement tools.

- Recent Developments: In November 2025, Oracle announced that its next‑generation AI‑powered Oracle Health EHR has received ONC Health IT certification from the U.S. Office of the National Coordinator (ONC), allowing ambulatory clinics to deploy the system with embedded AI to improve clinical workflows and patient care.

- Strategic Focus: Cloud-native EHR platform leadership; AI-enabled clinical workflows; integration with Oracle's enterprise database and analytics stack; expansion into international health systems.

Epic Systems Corporation

Epic Systems Corporation operates the largest US EHR install base across major health systems and academic medical centers. Epic anchors enterprise EHR adoption with MyChart patient portal, Hyperdrive clinical interface, and Cosmos research platform/database.

- Product Portfolio: Care Everywhere, MyChart patient portal, Hyperdrive, Cosmos research dataset, Healthy Planet population health, Beaker lab information system, Rover mobile nursing application.

- Recent Developments: In April 2026, Epic announced that Open@Epic will return in 2026, aiming to accelerate healthcare data sharing and interoperability across its EHR systems. This initiative will enable clinicians and patients to securely access and exchange health records across different healthcare organizations, enhancing coordinated care and digital health integration.

- Strategic Focus: Enterprise EHR leadership in the US; international expansion across European and Asia-Pacific health systems; AI-enabled clinical documentation; deepening patient-facing application portfolio.

Market Concentration Analysis

The global eHealth market is moderately fragmented at the application layer, with enterprise EHR leadership concentrated among Oracle and Epic Systems Corporation in the United States, and a long tail of regional specialists across Europe, Asia-Pacific, and emerging markets.

Koninklijke Philips NV anchors diagnostic imaging and analytics, while athenahealth, Inc. and emerging direct-to-consumer platforms drive cloud-native and consumer-facing innovation. The competitive landscape continues to consolidate through M&A, exemplified by Oracle's acquisition of Cerner and the rebranding of Allscripts to Veradigm Inc.

Investment & Growth Opportunities

Fastest Growing Segments

- Monitoring services are projected to grow at approximately 16.8% CAGR through 2034, the fastest among service segments, supported by Medicare RPM reimbursement codes, chronic disease management programs, and wearable device integration.

- Healthcare consumer end-user adoption is projected to grow at approximately 16.2% CAGR through 2034, fueled by direct-to-consumer telehealth, patient portals, and mobile health application uptake.

Emerging Market Expansion

- Asia-Pacific represents the highest-growth regional opportunity, with rapid digital health adoption across China, India, Japan, and Southeast Asia driven by government national EHR initiatives.

- Emerging markets including Latin America, the Middle East, and Africa offer accelerating opportunity as national digital health programs such as Mauritius's One Patient One Record scale.

Venture and Institutional Investment Trends

- United States health-tech venture capital remains the most active funding source globally, with multi-billion-dollar investments flowing into AI diagnostics, RPM platforms, and direct-to-consumer telehealth.

- Pharma-aligned telehealth M&A is intensifying, exemplified by Eli Lilly and Company's January 2024 LillyDirect launch and adjacent pharma-platform integrations targeting diabetes, obesity, and migraine therapeutic areas.

- Strategic M&A activity continues as enterprise software, cloud, and medical technology companies acquire eHealth platforms; Oracle's acquisition of Cerner remains the largest precedent transaction at approximately USD 28.3 Billion in equity value (closed June 2022).

Future Market Outlook (2026-2034)

The global eHealth market is positioned for sustained double-digit expansion through 2034. From USD 163.6 Billion in 2025, the market is projected to reach USD 587.5 Billion by 2034, representing incremental value of approximately USD 423.9 Billion at a 15.30% CAGR, increasingly composed of AI-enabled platforms, RPM ecosystems, direct-to-consumer telehealth, and interoperable EHR infrastructure.

Monitoring services are expected to expand their share toward 65.0% by 2034, while healthcare consumer end-user adoption gains share through D2C telehealth and patient-facing applications. North America will retain regional leadership, with Asia-Pacific closing the gap as national EHR initiatives scale across China, India, and Japan.

Research Methodology

Primary Research

Primary research included structured interviews with over 100 industry participants in 2024–2025, comprising health system CIOs, eHealth platform executives, EHR vendors, telehealth operators, payer organizations, and policy stakeholders across North America, Europe, and Asia-Pacific, validating market sizing, segmentation, regional shares, and adoption trends.

Secondary Research

Secondary research covered WHO digital health publications, CMS and ONC reports, EHDS documentation, EU AI Act, OEM annual reports, HIMSS, and government national digital health strategy documents.

Forecasting Models

Market size estimations used combined top-down and bottom-up forecasting, incorporating country-level healthcare expenditure, EHR adoption rates, RPM penetration, telehealth utilization, and vendor revenue disclosures. The 15.30% CAGR reflects validation against announced government initiatives, vendor product pipelines, and demographic and chronic disease trajectories through 2034.

eHealth Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Electronic Health Records, ePrescribing, Clinical Decision Support, Telemedicine, Consumer Health Information, mHealth, Others |

| Services Covered | Monitoring, Diagnostics, Healthcare Strengthening, Others |

| End Users Covered | Healthcare Providers, Payers, Healthcare Consumers, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Oracle, Epic Systems Corporation, Veradigm LLC, athenahealth, Inc., Koninklijke Philips NV, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the eHealth market from 2020-2034.

- The eHealth market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. Further it enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the eHealth industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the eHealth Market Report

The global eHealth market reached USD 163.6 Billion in 2025 and is projected to reach USD 587.5 Billion by 2034.

The market is expected to grow at a CAGR of 15.30% during 2026-2034, driven by aging demographics, AI and cloud adoption, government digital health initiatives, and workforce-driven automation.

North America leads with a 38.7% share in 2025, supported by 96% acute-care hospital EHR adoption in the US and the July 2025 CMS patient-centric ecosystem initiative.

Monitoring services dominate with a 62.0% share in 2025, encompassing remote patient monitoring, wearable integration, and chronic-disease management platforms.

Healthcare providers lead at 51.7%, encompassing hospitals, clinics, ambulatory care, and home-health operators driving enterprise EHR adoption.

Key players include Oracle, Epic Systems Corporation, Veradigm LLC, athenahealth, Inc., and Koninklijke Philips NV.

Monitoring is growing at approximately 16.8% CAGR through 2034 due to Medicare RPM reimbursement codes, chronic-disease management program expansion, and wearable device integration into clinical workflows.

Key challenges include data privacy and cybersecurity risks, legacy IT and interoperability gaps, high implementation and training costs, regulatory and reimbursement variability, and digital literacy and access inequalities.

AI-powered diagnostic platforms, direct-to-consumer telehealth, remote patient monitoring expansion, and Asia-Pacific and emerging market national EHR programs represent the highest-growth investment opportunities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)