Electronic Warfare Market Size, Share, Trends and Forecast by Product, Equipment, Capacity, Platform, and Region, 2026-2034

Electronic Warfare Market Size and Share:

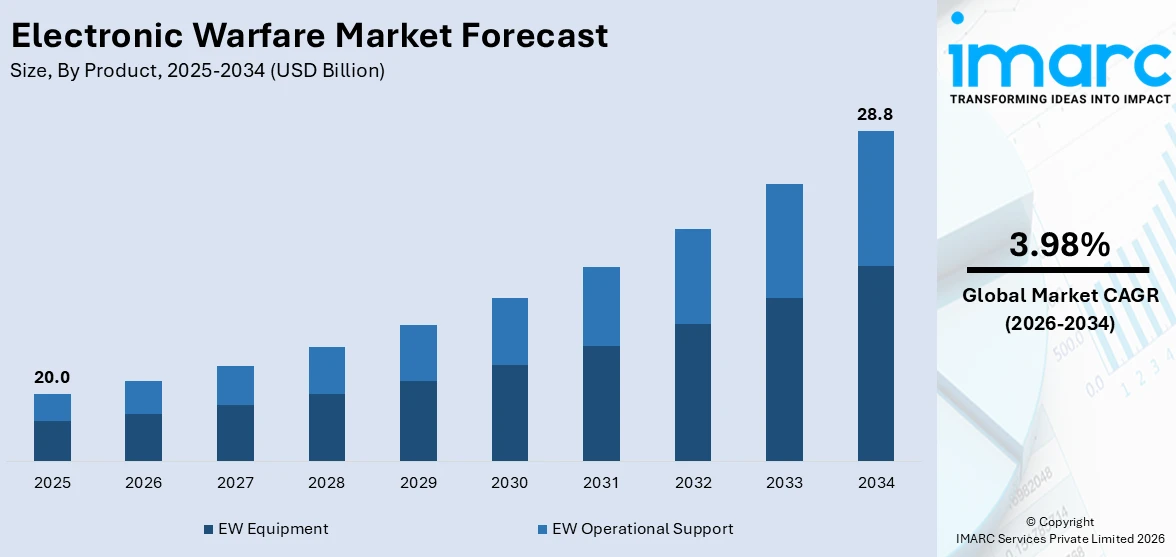

The global electronic warfare market size was valued at USD 20.0 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 28.8 Billion by 2034, exhibiting a CAGR of 3.98% from 2026-2034. North America currently dominates the market, holding a market share of 42% in 2025. The region benefits from substantial federal defense budgets, robust military modernization programs across all branches of the armed forces, sustained investments in electromagnetic spectrum dominance capabilities, and the presence of leading defense technology companies driving innovation, all contributing to the electronic warfare market share.

Global investments in sophisticated electronic warfare capabilities are increasing because to the escalating geopolitical tensions in a number of areas, including Eastern Europe and the Indo-Pacific. In order to preserve spectrum superiority in increasingly disputed electromagnetic settings, governments are giving upgrading of their defense infrastructure top priority. The need for sophisticated electronic countermeasures and counter-unmanned aerial system solutions has increased due to the increasing number of unmanned aerial systems and sophisticated drone threats. Furthermore, real-time threat identification, adaptive jamming, and autonomous decision-making capabilities that improve operational effectiveness are made possible by the incorporation of artificial intelligence and machine learning algorithms into electronic warfare equipment. Investments in adaptable and interoperable electronic warfare systems are being accelerated by the move toward multi-domain warfare plans, which include land, air, sea, cyber, and space operations. Moreover, the expanding cyber-electromagnetic convergence is creating new requirements for comprehensive spectrum management tools and cognitive electronic warfare solutions, supporting the electronic warfare market growth.

A number of factors have contributed to the United States' rise to prominence in the electronic warfare arena. The nation continues to be the biggest defense spender in the world, supporting the ongoing acquisition and upgrade of electronic warfare systems in all branches of the armed forces. To preserve electromagnetic spectrum superiority, the US military is making significant investments in cutting-edge shipboard electronic warfare suites and next-generation electronic attack vehicles. In order to speed up the development and deployment of new capabilities in response to changing combat threats, the Army is also aggressively seeking flexible funding options for its electronic warfare portfolio. The outlook for the US electronic warfare industry is further strengthened by the increased focus on software-defined radio technologies and counter-drone electronic warfare solutions. The emphasis on counter-drone electronic warfare solutions and software-defined radio technologies further strengthens the electronic warfare market outlook for the United States.

To get more information on this market Request Sample

Electronic Warfare Market Trends:

Rising Adoption of Cognitive Electronic Warfare Systems

The increasing complexity of modern electromagnetic battlefields is driving widespread adoption of cognitive electronic warfare systems that leverage artificial intelligence and machine learning capabilities. These advanced platforms autonomously identify, classify, and respond to dynamic electronic threats in real time, eliminating the limitations of pre-programmed response libraries. Cognitive electronic warfare systems can adapt to previously unknown signal environments, enabling military forces to maintain spectrum superiority against agile adversaries employing frequency-hopping communications and adaptive radar waveforms. The technology facilitates faster decision-making cycles and reduces the cognitive burden on operators during high-intensity electronic combat scenarios. For instance, in February 2025, L3Harris Technologies completed the first flight of its new Viper Shield electronic warfare suite aboard a Block 70 F-16 at Edwards Air Force Base, advancing fighter aircraft electronic defense capabilities with enhanced jamming and situational awareness features. The growing emphasis on software-defined architectures is enabling rapid reprogramming and capability upgrades across deployed electronic warfare market forecast platforms.

Expanding Counter-Drone Electronic Warfare Capabilities

The rapid proliferation of commercial and military unmanned aerial vehicles across global conflict zones is accelerating demand for specialized counter-drone electronic warfare solutions. Armed forces worldwide are deploying advanced jamming systems, radio frequency detection networks, and electronic countermeasure suites specifically designed to detect, track, and neutralize hostile drone threats. The lessons learned from modern conflicts have demonstrated the devastating effectiveness of low-cost drone swarms against conventional military assets, prompting urgent investment in portable and vehicle-mounted counter-unmanned aerial system electronic warfare solutions. Militaries are developing layered electronic defense architectures that combine electronic jamming, radar-based detection, and cyber-electromagnetic capabilities to counter diverse drone threats simultaneously. The increasing integration of artificial intelligence into counter-drone platforms is enabling autonomous threat classification and rapid response against fast-moving aerial targets. Furthermore, the development of directed energy weapons and high-powered microwave systems is providing armed forces with cost-effective electronic warfare market trends solutions for neutralizing large-scale drone swarm attacks across contested operational environments. These electronic warfare market trends are reshaping procurement priorities globally.

Growing Multi-Domain Electronic Warfare Integration

Modern military strategies are increasingly emphasizing seamless multi-domain operations that integrate electronic warfare capabilities across land, air, sea, cyber, and space environments. Defense organizations are developing flexible and scalable electronic warfare solutions capable of operating in joint-force scenarios where electromagnetic spectrum dominance directly influences mission outcomes across all operational domains. The evolution of network-centric warfare architectures demands electronic warfare systems that can share threat information instantaneously, coordinate jamming activities across dispersed platforms, and synchronize electronic attacks with kinetic operations. The miniaturization of advanced electronic components is enabling deployment of sophisticated electronic warfare payloads on smaller platforms, including unmanned aerial vehicles and satellite constellations, significantly expanding operational reach. For instance, in September 2025, Collins Aerospace, an RTX Corporation business, was awarded a contract by the NATO Communications and Information Agency to provide its Electronic Warfare Planning and Battle Management solution, enhancing NATO electromagnetic warfare coordination across member nations. Space-based electronic warfare is also emerging as a critical frontier.

Electronic Warfare Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global electronic warfare market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product, equipment, capacity, and platform.

Analysis by Product:

- EW Equipment

- EW Operational Support

EW equipment holds 68% of the market share. EW equipment encompasses the physical hardware and integrated systems deployed by military forces to detect, intercept, jam, and counter electromagnetic signals in contested environments. This segment includes radar warning receivers, electronic support measures, jammers, decoy systems, directed energy weapons, and countermeasure dispensing systems installed across various military platforms. The demand for advanced EW equipment is driven by the increasing sophistication of adversary threats, which require continuous modernization of onboard electronic defense capabilities. Militaries worldwide are procuring next-generation EW equipment featuring software-defined architectures that allow rapid reconfiguration for different mission requirements. The growing integration of artificial intelligence into EW equipment further enhances autonomous threat identification and response capabilities in complex electromagnetic environments. Additionally, the miniaturization of advanced electronic components is enabling the deployment of powerful electronic warfare payloads on smaller platforms, including unmanned aerial vehicles and loitering munitions, expanding operational flexibility across diverse combat scenarios and broadening the scope of mission-critical electronic defense applications.

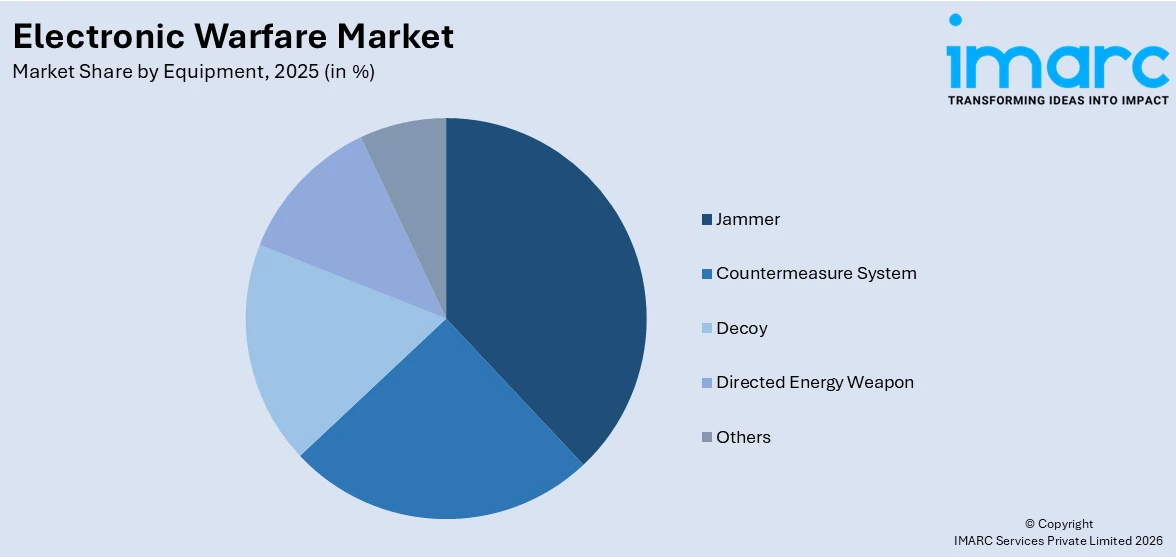

Analysis by Equipment:

Access the comprehensive market breakdown Request Sample

- Jammer

- Countermeasure System

- Decoy

- Directed Energy Weapon

- Others

Jammer leads the market with a share of 32%. Jammers are specialized electronic warfare devices designed to disrupt, degrade, or deny enemy use of the electromagnetic spectrum by transmitting interfering signals that overwhelm hostile communications, radar, and navigation systems. Advanced jamming systems now incorporate cognitive algorithms and digital radio frequency memory technology to generate highly targeted and adaptive interference patterns that are difficult for adversaries to counter through frequency-hopping or spread-spectrum techniques. The growing emphasis on stand-off and stand-in jamming capabilities across airborne, naval, and ground platforms drives sustained investment in next-generation jammer technologies. Militaries are deploying both broadband noise jammers for area denial and precision smart jammers for surgical electronic attacks against specific threat emitters. For instance, in December 2024, Raytheon was awarded a USD 590 million follow-on production contract from the U.S. Navy for the Next Generation Jammer Mid-Band system, a cooperative development program with the Royal Australian Air Force. Modular and software-upgradable jammer designs are becoming standard.

Analysis by Capacity:

- Electronic Protection

- Electronic Support

- Electronic Attack

Electronic support dominates the market, with a share of 45%. Electronic support encompasses the subdivision of electronic warfare involving actions taken to search for, intercept, identify, locate, and analyze sources of intentional and unintentional radiated electromagnetic energy for the purposes of immediate threat recognition, targeting, planning, and conducting future operations. Electronic support systems provide critical situational awareness by passively monitoring the electromagnetic environment to detect and classify radar emissions, communication signals, and other electronic signatures. The intelligence gathered through electronic support measures enables military commanders to build comprehensive electronic orders of battle and develop effective countermeasure strategies. The rising complexity of modern electromagnetic environments, characterized by dense signal traffic and sophisticated adversary emitters, is propelling demand for advanced electronic support systems featuring wideband receivers and machine learning-driven signal processing. Additionally, the shift toward network-centric warfare architectures requires electronic support platforms capable of sharing real-time threat data across distributed forces, enhancing collaborative electromagnetic situational awareness and enabling coordinated responses to emerging electronic threats across multiple operational domains.

Analysis by Platform:

- Land

- Naval

- Airborne

- Space

Airborne represents the leading segment, with a market share of 40%. Airborne electronic warfare platforms constitute the most strategically significant segment, encompassing electronic warfare systems integrated into fighter aircraft, bombers, dedicated electronic attack aircraft, helicopters, unmanned aerial vehicles, and airborne surveillance platforms. The dominance of the airborne segment reflects the inherent advantages of aerial platforms in projecting electronic warfare effects across wide areas with superior line-of-sight coverage and rapid repositioning capabilities. Modern airborne electronic warfare systems include integrated electronic support measures, self-protection suites, electronic countermeasure pods, and stand-off jamming capabilities that enable aircraft to survive and operate in heavily contested air defense environments. The development of dedicated airborne electronic attack aircraft underscores the strategic importance of aerial electronic warfare in suppressing enemy air defenses and disrupting adversary command and control networks. Additionally, the growing deployment of unmanned aerial vehicles equipped with modular electronic warfare payloads is expanding the operational reach of airborne electronic attack missions while reducing pilot risk in heavily defended electromagnetic environments.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 42% of the share, enjoys the leading position in the market. The region's dominance is supported by the United States' position as the world's largest defense spender, with comprehensive electronic warfare modernization programs spanning all military branches and service domains. The presence of leading defense contractors creates a robust innovation ecosystem that drives continuous advancement in electronic warfare technologies. North America's defense industrial base benefits from substantial research and development investments funded through the Department of Defense, defense agencies, and congressional allocations that prioritize electromagnetic spectrum superiority. Additionally, the growing emphasis on countering peer-level threats from strategic competitors is sustaining high procurement volumes for advanced electronic attack, electronic support, and electronic protection systems. The region's focus on developing next-generation cognitive electronic warfare platforms powered by artificial intelligence and machine learning algorithms is further solidifying its technological leadership. Furthermore, strong collaboration between government research laboratories, academic institutions, and private defense contractors ensures a continuous pipeline of innovative electromagnetic warfare solutions across all operational domains.

Key Regional Takeaways:

United States Electronic Warfare Market Analysis

The United States maintains its position as the dominant force in the global electronic warfare market, driven by the largest defense budget in the world and an unwavering commitment to electromagnetic spectrum superiority. The country's military modernization programs encompass comprehensive electronic warfare upgrades across air, land, naval, and space domains, with significant investments directed toward next-generation platforms and cognitive electronic warfare technologies. The U.S. Air Force is advancing its EA-37B Compass Call fleet, while the Navy continues expanding its Surface Electronic Warfare Improvement Program and Next Generation Jammer initiatives. The Army is actively pursuing agile funding mechanisms for its electronic warfare portfolio to enable rapid innovation and fielding of emerging capabilities in response to real-world battlefield threats. The emphasis on counter-drone electronic warfare solutions has become a top priority across all military branches. For instance, the fiscal year 2026 defense appropriations bill allocated USD 474.4 million for two EA-37B Compass Call electronic warfare jets, demonstrating sustained congressional support for airborne electronic attack modernization. The growing integration of artificial intelligence into electronic warfare platforms, combined with robust public-private partnerships, ensures the United States remains at the forefront of electronic warfare innovation.

Europe Electronic Warfare Market Analysis

Europe is witnessing significant growth in the electronic warfare market, driven by heightened geopolitical tensions stemming from the conflict in Eastern Europe and a renewed commitment to collective defense capabilities. The lessons learned from modern conflicts have exposed critical capability gaps in electromagnetic warfare across European NATO members, prompting accelerated investment in electronic warfare modernization programs. Major European nations, including Germany, France, the United Kingdom, and Italy, are prioritizing upgrades to their electronic warfare infrastructures, integrating advanced jamming suites into fighter aircraft and naval platforms. The European Commission's Readiness 2030 framework has identified cyber, artificial intelligence, and electronic warfare as priority capability areas, supporting defense investments across member states. The rising NATO defense spending commitments are directing substantial resources toward electronic warfare as a key area requiring urgent modernization. Collaborative programs among European defense contractors are advancing indigenous electronic warfare capabilities to reduce dependence on external suppliers. Additionally, the growing focus on interoperability among allied nations is driving standardization of electronic warfare systems across the continent.

Asia-Pacific Electronic Warfare Market Analysis

Asia-Pacific represents the fastest-growing region in the electronic warfare market, fueled by escalating security tensions across the Indo-Pacific and substantial increases in defense budgets among major economies. Countries including China, Japan, India, South Korea, and Australia are making significant investments in advanced electronic warfare capabilities to strengthen their electromagnetic spectrum dominance. The region's growth is supported by indigenous defense manufacturing initiatives, cross-border technology partnerships under alliances like AUKUS, and the modernization of airborne and naval electronic warfare platforms. For instance, India's defense budget increased by 9.5 percent to USD 78.3 billion for fiscal year 2025-2026, with a strong emphasis on indigenous electronic warfare suite development for frontline military platforms. Japan is significantly expanding its defense budget, funding electronic warfare equipment, space-based radar, and ballistic missile defense capabilities as part of its Defense Buildup Plan.

Latin America Electronic Warfare Market Analysis

Latin America is experiencing gradual growth in the electronic warfare market as regional governments seek to modernize their defense capabilities within fiscal constraints. Countries across the region are diversifying their defense suppliers and strengthening surveillance, cyber, and electronic warfare capabilities to address persistent security challenges including narco-trafficking, border surveillance, and asymmetric threats from non-state actors. Brazil leads regional electronic warfare modernization efforts through partnerships with international defense contractors, integrating advanced radar and electronic warfare suites into its frontline military platforms. The growing counter-drone threat in the region is also catalyzing investments in electronic countermeasure technologies to protect critical infrastructure and military assets.

Middle East and Africa Electronic Warfare Market Analysis

The Middle East and Africa region is witnessing expanding investment in electronic warfare capabilities, driven by ongoing regional conflicts, counter-terrorism operations, and strategic defense modernization programs. Nations across the Middle East are procuring advanced jammers, intelligence gathering systems, and electronic countermeasure platforms to bolster their electromagnetic defense capabilities against evolving threats. Several countries in the region are directing substantial investment toward domestic electronic warfare manufacturing and strategic partnerships with established defense contractors to build indigenous capabilities. African nations are increasingly recognizing the importance of electronic warfare systems for airspace protection, border security, and countering asymmetric threats from non-state armed groups.

Competitive Landscape:

The competitive landscape of the electronic warfare market is characterized by the dominance of established defense conglomerates that leverage extensive research capabilities, government partnerships, and decades of integration experience. Major industry participants are pursuing strategic mergers, acquisitions, and cross-border partnerships to expand their electronic warfare portfolios and address emerging multi-domain requirements. Companies are investing heavily in artificial intelligence-powered cognitive electronic warfare, software-defined architectures, and modular mission payload designs that enable rapid reconfiguration across diverse platform types. The growing emphasis on counter-unmanned aerial system solutions and space-based electronic warfare capabilities has opened additional competitive arenas where both traditional defense primes and agile technology startups are seeking market positions. The increasing procurement budgets across North America, Europe, and Asia-Pacific are intensifying competition for lucrative long-term defense contracts, driving continuous innovation in jamming technologies, electronic support systems, and integrated electronic protection suites.

The report provides a comprehensive analysis of the competitive landscape in the electronic warfare market with detailed profiles of all major companies, including:

- BAE Systems

- Elbit Systems Ltd

- General Dynamics Mission Systems, Inc.

- Hensoldt AG

- Israel Aerospace Industries

- L3Harris Technologies Inc.

- Leonardo S.p.A.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- RTX Corporation

- Saab AB

- Thales Group

Latest News and Developments:

- In February 2026, Lockheed Martin received a USD 249 million indefinite-delivery indefinite-quantity contract from the U.S. Navy to support the Surface Electronic Warfare Improvement Program Block II. The contract covers spares, repair services, engineering support, and depot stand-up activities tied to the integration of the Electronic Support Anti-Ship Missile Defense System. Work will be performed in Liverpool, New York, with an expected completion by February 2031.

Electronic Warfare Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | EW Equipment, EW Operational Support |

| Equipments Covered | Jammer, Countermeasure System, Decoy, Directed Energy Weapon, Others |

| Capacities Covered | Electronic Protection, Electronic Support, Electronic Attack |

| Platforms Covered | Land, Naval, Airborne, Space |

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | BAE Systems, Elbit Systems Ltd, General Dynamics Mission Systems, Inc., Hensoldt AG, Israel Aerospace Industries, L3Harris Technologies Inc., Leonardo S.p.A., Lockheed Martin Corporation, Northrop Grumman Corporation, RTX Corporation, Saab AB, Thales Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the electronic warfare market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global electronic warfare market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the electronic warfare industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Electronic Warfare Market Report

The electronic warfare market was valued at USD 20.0 Billion in 2025.

The electronic warfare market is projected to exhibit a CAGR of 3.98% during 2026-2034, reaching a value of USD 28.8 Billion by 2034.

The electronic warfare market is primarily driven by escalating geopolitical tensions across Eastern Europe and the Indo-Pacific, increasing defense budgets worldwide, growing proliferation of unmanned aerial vehicle threats requiring advanced counter-drone solutions, integration of artificial intelligence and machine learning into cognitive electronic warfare platforms, and the shift toward multi-domain warfare strategies demanding interoperable and scalable spectrum management capabilities.

North America currently dominates the electronic warfare market, accounting for a share of 42%. The region's leadership is driven by the United States' substantial defense budget, comprehensive military modernization programs, presence of leading defense contractors, and sustained investments in electromagnetic spectrum superiority.

Some of the major players in the electronic warfare market include BAE Systems, Elbit Systems Ltd, General Dynamics Mission Systems, Inc., Hensoldt AG, Israel Aerospace Industries, L3Harris Technologies Inc., Leonardo S.p.A., Lockheed Martin Corporation, Northrop Grumman Corporation, RTX Corporation, Saab AB, Thales Group, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade