Europe Automotive Glass Market Size, Share, Trends, and Forecast by Glass Type, Material Type, Vehicle Type, Application, End User, Technology, and Country, 2026-2034

Europe Automotive Glass Market Size, Share, Trends & Forecast (2026-2034)

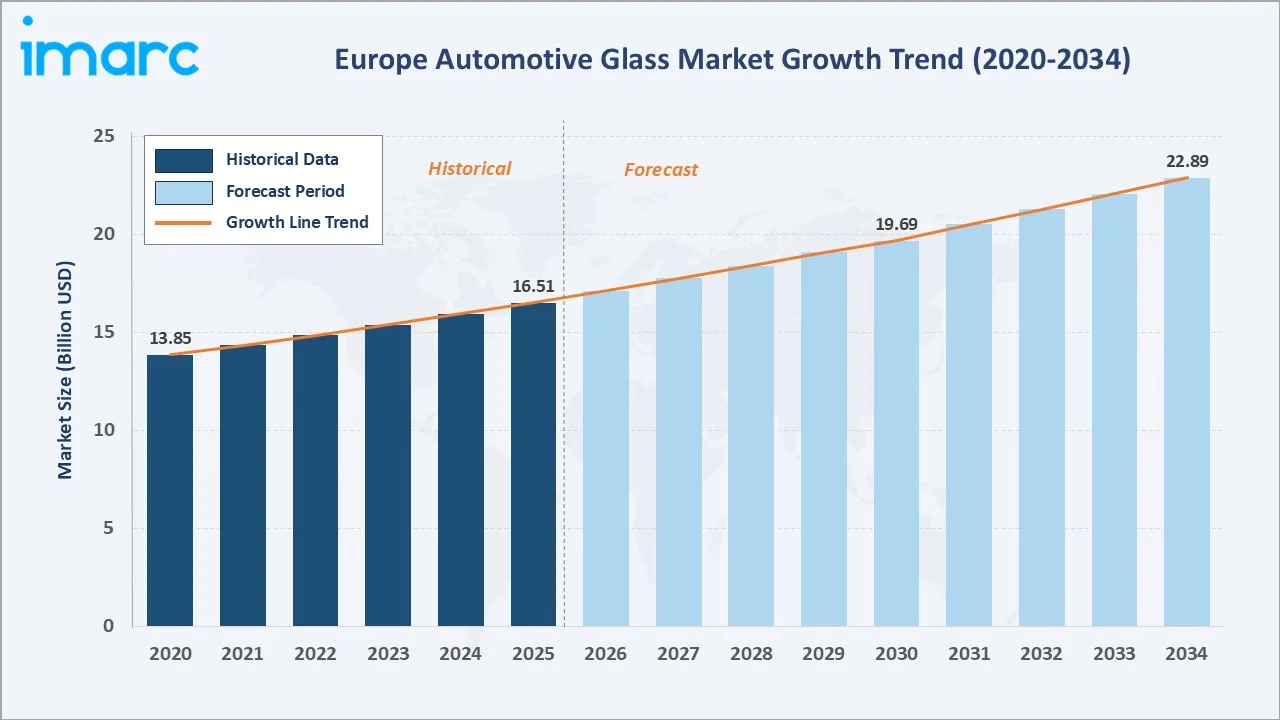

The Europe automotive glass market reached USD 16.51 Billion in 2025 and is projected to reach USD 22.89 Billion by 2034, growing at a CAGR of 3.58% during 2026-2034. The European passenger plug-in vehicle market registered nearly 298,000 units in January 2026, marking a 22% year-on-year increase from January 2025. Battery electric vehicles (BEVs) contributed approximately 195,000 registrations, while plug-in hybrid electric vehicles (PHEVs) accounted for around 102,000 units. This rapid growth in EV adoption is driving the Europe automotive glass market by increasing demand for advanced lightweight glass, panoramic sunroofs, acoustic glazing, and energy-efficient smart glass solutions used in modern electric vehicles. Laminated glass leads the glass type at 46.8%. IR PVB leads material type at 34.7%. Germany commands 22.4% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 16.51 Billion |

|

Forecast Market Size (2034) |

USD 22.89 Billion |

|

CAGR (2026-2034) |

3.58% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Glass Type |

Laminated Glass (46.8%, 2025) |

|

Dominant Material Type |

IR PVB (34.7%, 2025) |

|

Leading Country |

Germany (22.4%, 2025) |

The market expanded from USD 13.85 Billion in 2020 to USD 16.51 Billion in 2025, anchored at USD 19.69 Billion in 2030, and forecast to reach USD 22.89 Billion by 2034. COVID-19 disrupted European automotive production significantly in 2020-2021, temporarily suppressing OEM first-fit glass demand before a recovery phase from 2022. The simultaneous automotive glass market structural upgrade has driven average selling price per vehicle upward, sustaining market revenue growth above vehicle production volume growth.

To get more information on this market, Request Sample

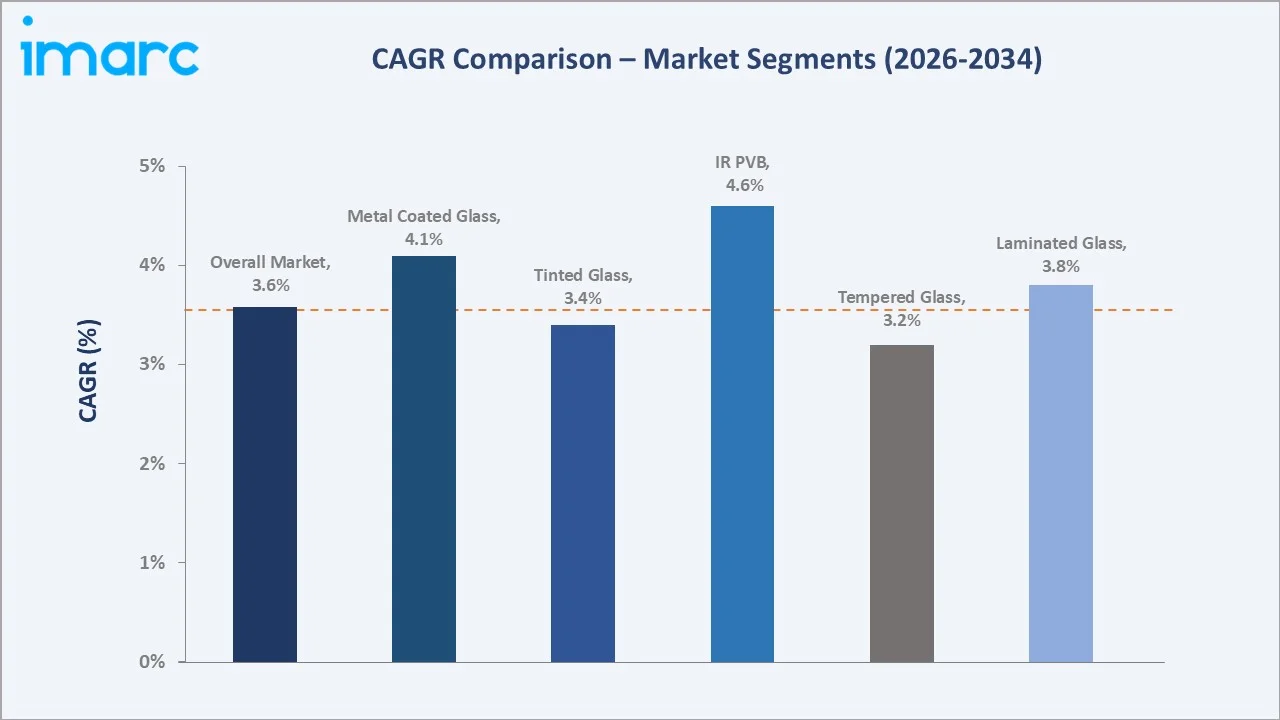

IR PVB grows fastest at ~4.6% CAGR as infrared-reflecting PVB interlayers become the European OEM standard for solar heat management in glass roofs and windshields. Metal-coated glass grows at ~4.1% CAGR as magnetron sputtering metal-oxide coating enables low-emissivity glass required for EV thermal management optimization.

Executive Summary

The Europe automotive glass market reached USD 16.51 Billion in 2025, serving Europe's vehicle production base and registered vehicle fleet requiring aftermarket glass replacement. Europe's automotive glass market operates at the intersection of the continent's most strategically important industrial sector and the most demanding technical specifications for glass performance. The market is projected to reach USD 22.89 Billion by 2034 at 3.58% CAGR.

Laminated glass at 46.8% leads as the mandatory windshield glass type throughout Europe, requiring all front windshields to use laminated glass construction. IR PVB at 34.7% of material type reflects its establishment as the dominant European premium automotive glass material, replacing standard PVB across premium vehicle platforms where thermal comfort and energy efficiency are primary selling points. Germany at 22.4% leads through its premium vehicle production concentration and the highest per-vehicle glass content value among European automotive markets.

Key Market Insights

|

Insight |

Data |

|

Dominant Glass Type |

Laminated Glass - 46.8% share (2025) |

|

Dominant Material Type |

IR PVB - 34.7% market share (2025) |

|

Leading Country |

Germany - 22.4% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Laminated glass at 46.8% sustained by mandatory windshield specification and expanding application to side and roof glass in EV platforms: European automotive glass safety regulation mandates laminated glass construction for all windshields, creating a captive market floor of approximately 1 windshield per vehicle produced or in the fleet.

- IR PVB at 34.7% reflecting the European automotive glass market's most significant material technology transition: Infrared-reflecting PVB interlayer represents the most commercially important European automotive glass material innovation. Standard PVB transmits approximately 60% of near-infrared (NIR) solar radiation, creating interior greenhouse heating; IR PVB's silver-nanoparticle or metallic-layer construction reflects 70-80% of NIR, reducing interior peak temperatures by 8-12 degrees Celsius and reducing air conditioning energy consumption by 20-35%.

- Germany at 22.4% reflecting premium vehicle production concentration, generating Europe's highest per-vehicle automotive glass value: Germany's premium automotive production generates disproportionate automotive glass revenue relative to vehicle volume through the significantly higher glass content value of premium and luxury vehicles.

Europe Automotive Glass Market Overview

Europe's automotive glass market encompasses all original equipment manufacturer (OEM) first-fit glass installed during vehicle assembly at European production facilities, plus the automotive replacement glass (ARG) aftermarket supplying damaged or deteriorated glass replacement across Europe's registered vehicle fleet. Products include windshields, sidelights, rear windscreens, glass roofs, quarter lights, and specialty glass. The market encompasses OEM-grade glass manufactured to specific automotive OEM specifications and aftermarket-grade glass manufactured to homologation standards for fleet replacement.

The ecosystem integrates float glass raw material producers, interlayer material suppliers, automotive glass manufacturers, automotive OEMs, Tier 1 automotive suppliers integrating glass subassemblies, the ARG aftermarket distribution network, and the regulatory framework. Macroeconomic factors include rising vehicle production, growing electric vehicle adoption, increasing disposable income, and stricter automotive safety regulations.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

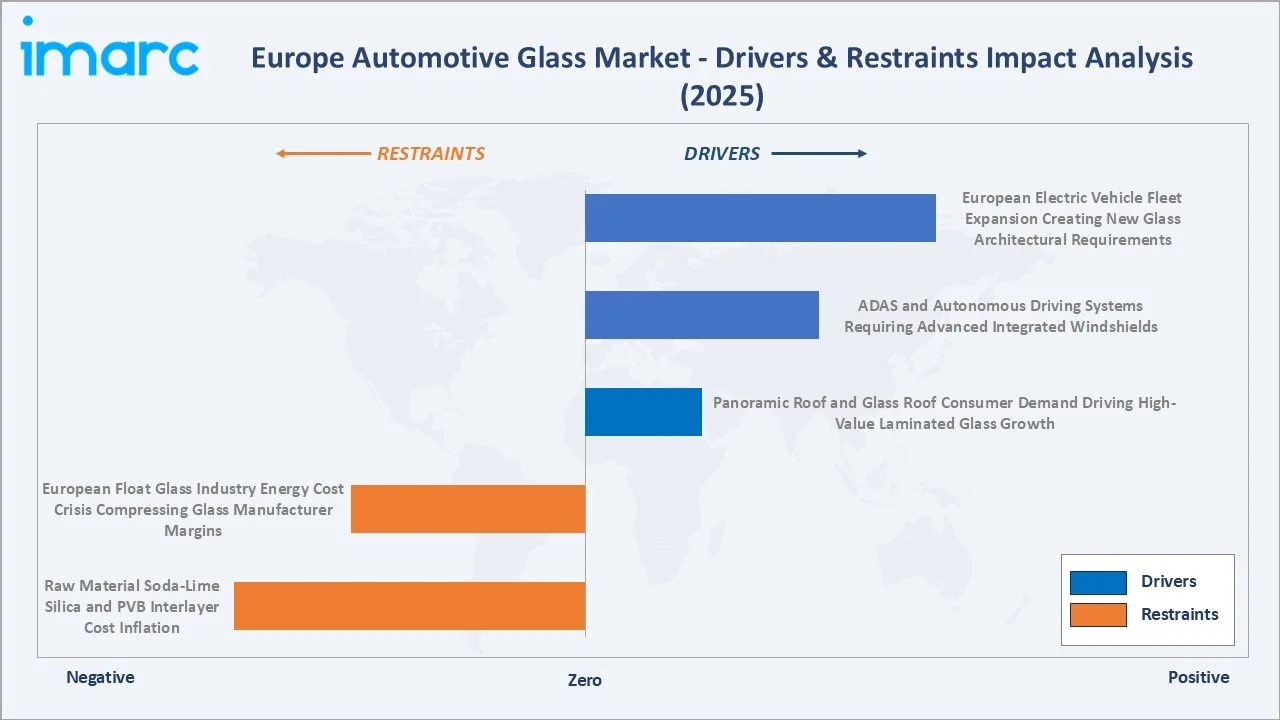

- European Electric Vehicle Fleet Expansion Creating New Glass Architectural Requirements: The European passenger plug-in vehicle market registered nearly 298,000 units in January 2026, marking a 22% year-on-year increase from January 2025. Europe's EV production trajectory is creating architectural glass requirements. EV platforms specifically benefit from: larger panoramic glass roofs replacing traditional steel roofs because EV battery packaging lowers vehicle floors, increasing headroom available for glass roof height and driving consumer preference for light-filled interiors; solar-collecting glass roofs with embedded photovoltaic cells converting glass from passive material to power-generating component; and thermal management glass reducing cabin heating load that directly competes with propulsion power for EV range.

- ADAS and Autonomous Driving Systems Requiring Advanced Integrated Windshields: The European automotive safety regulation mandate is driving OEM windshield specifications beyond simple transparency to become precision optical instruments housing camera systems, radar emitters, heating elements for sensor de-icing, and cleaning systems for optical surfaces.

- Panoramic Roof and Glass Roof Consumer Demand Driving High-Value Laminated Glass Growth: European consumer preference for panoramic glass roofs has grown from a premium-exclusive feature to a mainstream feature across premium and upper-medium segment vehicles. Each panoramic roof installation requires 1.5-3 sqm of complex curved laminated glass, commanding premium glass supplier revenue.

Market Restraints

- European Float Glass Industry Energy Cost Crisis Compressing Glass Manufacturer Margins: Europe's float glass furnaces are among the most energy-intensive industrial assets on the continent. This energy cost pressure accelerated European glass manufacturers' energy transition investments while simultaneously compressing EBITDA margins and reducing investment capacity for new automotive glass product development.

- Raw Material Soda-Lime Silica and PVB Interlayer Cost Inflation: European float glass manufacturing depends on soda-lime silica sand, soda ash, and dolomite and limestone fluxing materials. Soda ash price increases represent a direct input cost increase for float glass and PVB production.

Market Opportunities

- HUD-Compatible Laminated Windshield as the European Premium Segment Growth Engine: Head-Up Display systems, projecting driving information onto the windshield for driver reference without eye movement from the road, are expanding from premium-exclusive to upper-medium segment vehicles. Each HUD-equipped vehicle requires a specifically engineered laminated windshield with a double-wedge PVB interlayer, a defined optical zone clarity specification, and specific windshield inclination angle compatibility with the HUD projector optics.

- Smart Electrochromic Glazing for Sunroof and Privacy Glass: Smart electrochromic glazing for sunroofs and privacy glass is creating a major opportunity as automakers increasingly integrate premium comfort, energy efficiency, and smart cabin technologies into vehicles. In January 2025, Glaston and Miru Smart Technologies partnered to accelerate the development and production capabilities of next-generation dynamic electrochromic window technologies. Electrochromic glass can automatically adjust tint levels to control heat, glare, and privacy, improving passenger comfort and reducing HVAC energy consumption in EVs.

Market Challenges

- Chinese Automotive Glass Market Entry Threatening European Supplier Margin: The entry of Chinese automotive glass manufacturers is increasing pricing pressure and intensifying competition for established European suppliers. Lower-cost Chinese products are challenging profit margins, particularly in standard windshield and side-glass segments. This competitive pressure may force European companies to increase investments in innovation, premium glazing technologies, and operational efficiency to maintain market share.

- Certification Barriers Creating Long Product Development Cycles: Certification barriers extend product development timelines and increase compliance costs for manufacturers. Automotive glass products must meet strict European safety, durability, optical clarity, and environmental regulations before commercial deployment. The lengthy validation and homologation process can delay innovation adoption, slow new product launches, and reduce speed-to-market for advanced glazing technologies.

Emerging Market Trends

1. Panoramic and Full-Glass Roof Expansion Across European Vehicle Segments

Panoramic and full-glass roofs are emerging as automakers increasingly emphasize premium design, spacious cabin aesthetics, and enhanced passenger experience across both luxury and mid-range vehicles. In September 2025, Webasto Luxembourg launched the new high-tech glass production line at its plant in Grevenmacher, Luxembourg. The strategic product focuses on large-format panoramic glass roofs and pioneering technologies such as switchable glazing and ambient lighting. Growing adoption of electric vehicles and SUVs is driving demand for lightweight, UV-protective, and acoustic glass technologies.

2. ADAS Windshield Integration Creating New Technical Complexity and Value

ADAS windshield integration is emerging as advanced driver-assistance systems increasingly rely on cameras, sensors, LiDAR, and head-up display technologies embedded within vehicle windshields. This is increasing the technical complexity and value of automotive glass by requiring higher optical precision, sensor compatibility, and calibration capabilities.

3. Solar-Integrated Glazing for Vehicle Electrification Support

Solar-integrated glazing is emerging as automakers seek to improve vehicle energy efficiency and extend electric vehicle driving range. Advanced solar glass technologies can generate supplemental power for onboard systems, reduce cabin heat buildup, and lower battery load from air-conditioning systems.

4. Acoustic Laminated Glass Becoming Standard in European EV Platforms

Acoustic laminated glass is emerging as electric vehicles require enhanced cabin noise reduction due to the absence of traditional engine sound. Automakers are increasingly adopting advanced acoustic glazing in windshields and side windows to improve passenger comfort and a premium driving experience.

Industry Value Chain Analysis

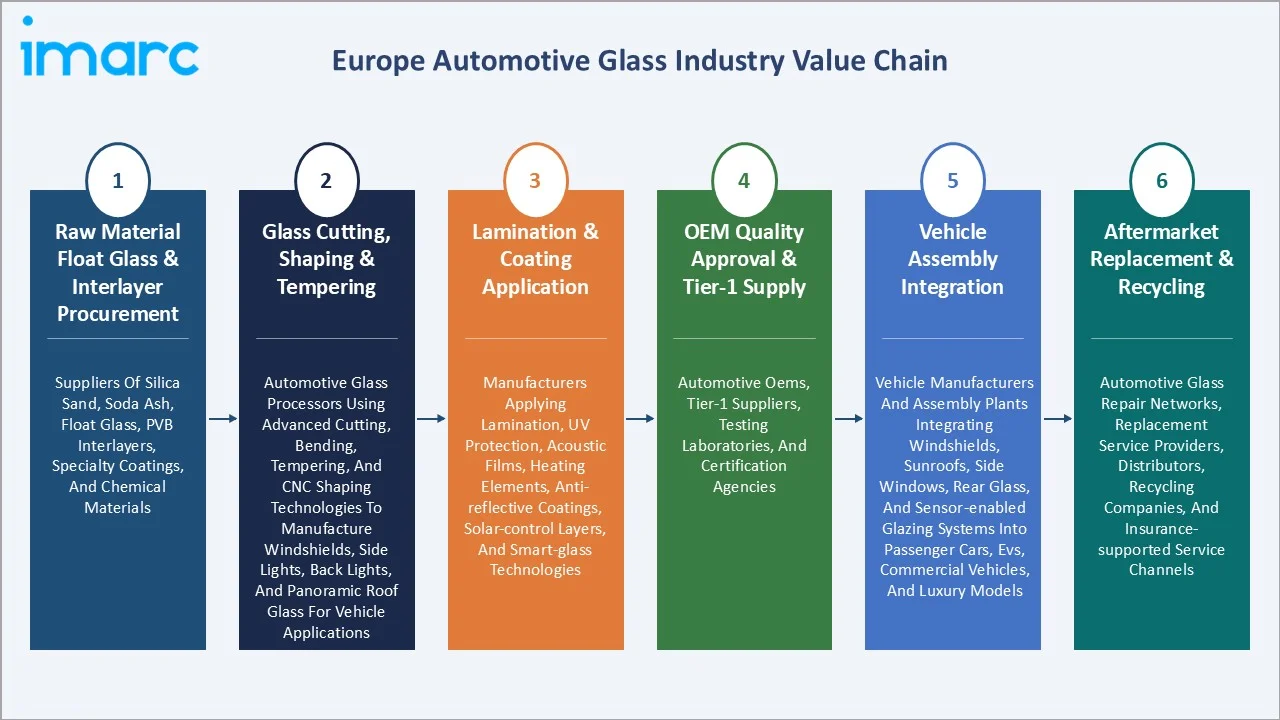

Europe's automotive glass value chain integrates raw material float glass and PVB production, glass cutting and bending, lamination and coating application, OEM quality approval and supply, vehicle assembly integration, and aftermarket replacement and glass recycling. Float glass manufacturing represents the highest capital intensity of the value chain. Automotive glass suppliers earn gross margins of 28-35% on OEM supply contracts and 35-45% on replacement glass due to higher aftermarket pricing versus OEM contract pricing.

|

Stage |

Key Participants |

|

Raw Material Float Glass & Interlayer Procurement |

Suppliers of silica sand, soda ash, float glass, PVB interlayers, specialty coatings, and chemical materials. |

|

Glass Cutting, Shaping & Tempering |

Automotive glass processors using advanced cutting, bending, tempering, and CNC shaping technologies to manufacture windshields, side lights, back lights, and panoramic roof glass for vehicle applications. |

|

Lamination & Coating Application |

Manufacturers applying lamination, UV protection, acoustic films, heating elements, anti-reflective coatings, solar-control layers, and smart-glass technologies. |

|

OEM Quality Approval & Tier-1 Supply |

Automotive OEMs, Tier-1 suppliers, testing laboratories, and certification agencies. |

|

Vehicle Assembly Integration |

Vehicle manufacturers and assembly plants integrating windshields, sunroofs, side windows, rear glass, and sensor-enabled glazing systems into passenger cars, EVs, commercial vehicles, and luxury models. |

|

Aftermarket Replacement & Recycling |

Automotive glass repair networks, replacement service providers, distributors, recycling companies, and insurance-supported service channels. |

The OEM quality approval and supply tier is European automotive glass's most structurally important commercial relationship. This approval investment creates 5-8 year supply relationships once established, providing revenue stability for approved European glass suppliers that new entrants cannot easily displace, regardless of pricing.

Technology Landscape in the Europe Automotive Glass Industry

Float Glass Manufacturing Technology

Float glass manufacturing technology enables the production of high-clarity, lightweight, and durable automotive glazing solutions on a large scale. Advanced float glass processes improve optical precision, thermal performance, and compatibility with ADAS, acoustic, and solar-control technologies. Manufacturers are also investing in energy-efficient and low-carbon production methods to align with Europe’s sustainability and automotive emission goals.

PVB Interlayer Technology

PVB interlayer technology improves vehicle safety, acoustic insulation, UV protection, and impact resistance in laminated automotive glass. In November 2024, Eastman Chemical Company announced plans to expand and upgrade its extrusion capabilities for Saflex PVB interlayer production at its Ghent, Belgium facility, with the project expected to be completed by 2026. The investment is aimed at strengthening supply capacity to meet rising demand from the automotive premium segment and supporting future growth across automotive and architectural applications.

Physical Vapor Deposition (PVD) Coating Technology

Physical Vapor Deposition (PVD) coating technology enables advanced thin-film coatings that improve solar control, heat insulation, glare reduction, and aesthetic performance. PVD-coated automotive glass supports energy efficiency and passenger comfort, particularly in electric and premium vehicles. The technology also enhances compatibility with smart glazing, infrared-reflective windshields, and advanced driver-assistance systems (ADAS) integration.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Glass Type |

Laminated Glass |

46.8% |

2025 |

|

Material Type |

IR PVB |

34.7% |

2025 |

|

Vehicle Type |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Technology |

🔒 |

🔒 |

2025 |

|

Country |

Germany |

22.4% |

2025 |

By Glass Type

Laminated glass leads at 46.8% market share (2025). Laminated automotive glass uses two glass panes bonded with a polyvinyl butyral (PVB) interlayer through autoclave pressure and heat, creating a safety glass that holds together upon impact rather than shattering into sharp fragments. Laminated glass applications are expanding from windshield-only to include acoustic laminated side glass, panoramic glass roofs, and laminated rear screens on luxury vehicles.

To access detailed market analysis, Request Sample

Tempered glass at 41.3% serves side windows, rear screens, and fixed glass in the vehicle production. Others at 11.9% encompasses electrochromic smart glass, polycarbonate glazing, and specialty glass products.

By Material Type

IR PVB leads at 34.7% market share (2025). Infrared-reflecting PVB has established market leadership as the preferred laminated glass material technology for premium European vehicle platforms, providing solar heat management in glass roofs and windshields that directly support EV cabin thermal efficiency and luxury vehicle thermal comfort specifications.

Tinted glass at 27.6% provides solar control through bulk glass coloration. Metal-coated glass at 21.8% grows at ~4.1% CAGR through EV thermal management and electromagnetic compatibility requirements for 5G and ADAS antenna integration. Others at 15.9% encompasses standard clear PVB, acoustic PVB-only products, and specialty ceramic glass applications.

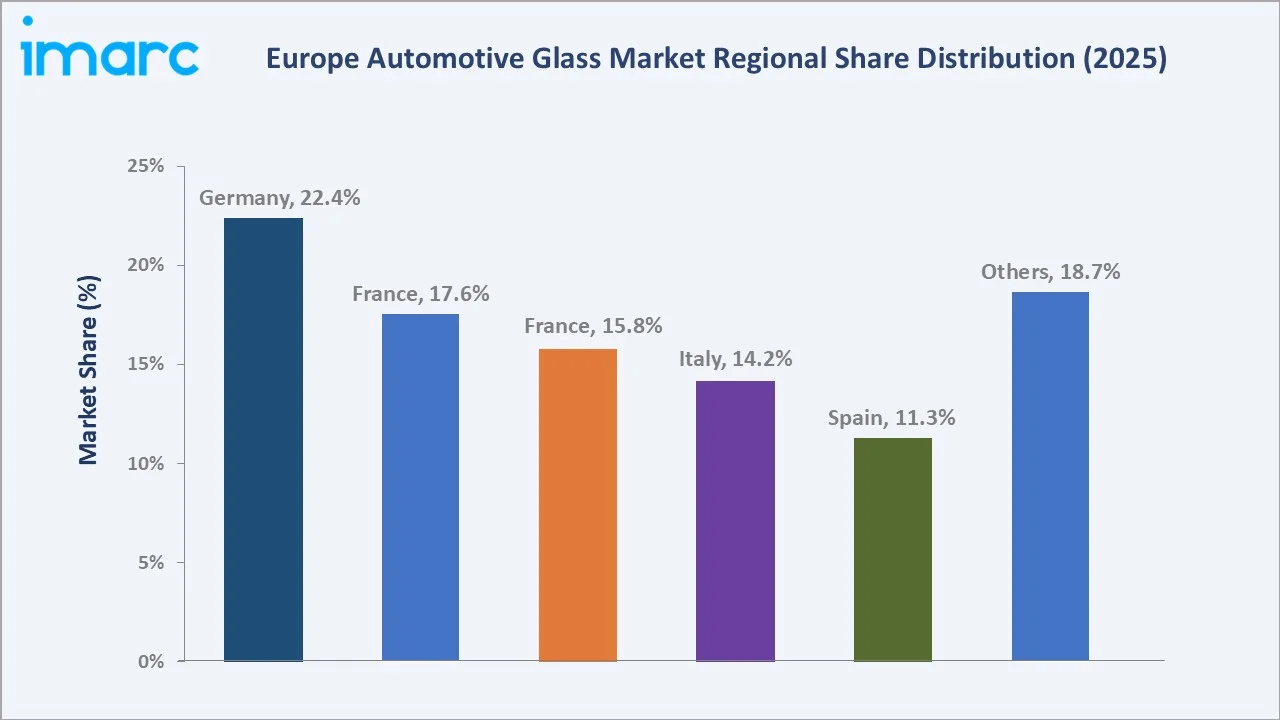

Regional Market Insights

|

Country |

Share (2025) |

Key Automotive Glass Drivers & Characteristics |

|

Germany |

22.4% |

Supported by strong vehicle manufacturing capacity, premium automotive production, and high adoption of advanced automotive technologies. |

|

France |

17.6% |

Benefits from established automotive manufacturing, growing electric vehicle production, and increasing demand for lightweight and energy-efficient glazing systems. |

|

United Kingdom |

15.8% |

Driven by premium vehicle manufacturing, rising EV adoption, and growing demand for advanced safety and acoustic glazing technologies. |

|

Italy |

14.2% |

Supported by automotive component manufacturing, luxury and sports vehicle production, and increasing adoption of panoramic roofs and premium glazing features. |

|

Spain |

11.3% |

Supporting demand for OEM automotive glass, replacement glass, and advanced windshield technologies. |

|

Others |

18.7% |

Other European countries collectively contribute through expanding automotive production, increasing electric vehicle penetration, and rising demand for lightweight, solar-control, and acoustic automotive glazing solutions across passenger and commercial vehicle segments. |

Germany's 22.4% leadership reflects the premium vehicle production concentration, creating Europe's highest per-vehicle glass content value. The German premium segment's ongoing technology leadership ensures Germany will remain the primary driver of European automotive glass technology innovation through 2034.

France at 17.6% reflects Saint-Gobain's home market advantage, supplying production closely from adjacent manufacturing facilities. The United Kingdom, at 15.8%, features domestic manufacturing heritage and network leadership. Italy, at 14.2%, brings the super-premium bespoke glass opportunity alongside Stellantis volume production. Spain, at 11.3%, hosts Europe's second-highest vehicle production volume, creating significant standard glass demand. Others at 18.7% represents Central and Eastern European production growth as Poland, Czech Republic, Slovakia, and Hungary collectively add a huge number of vehicles annually to European production volume.

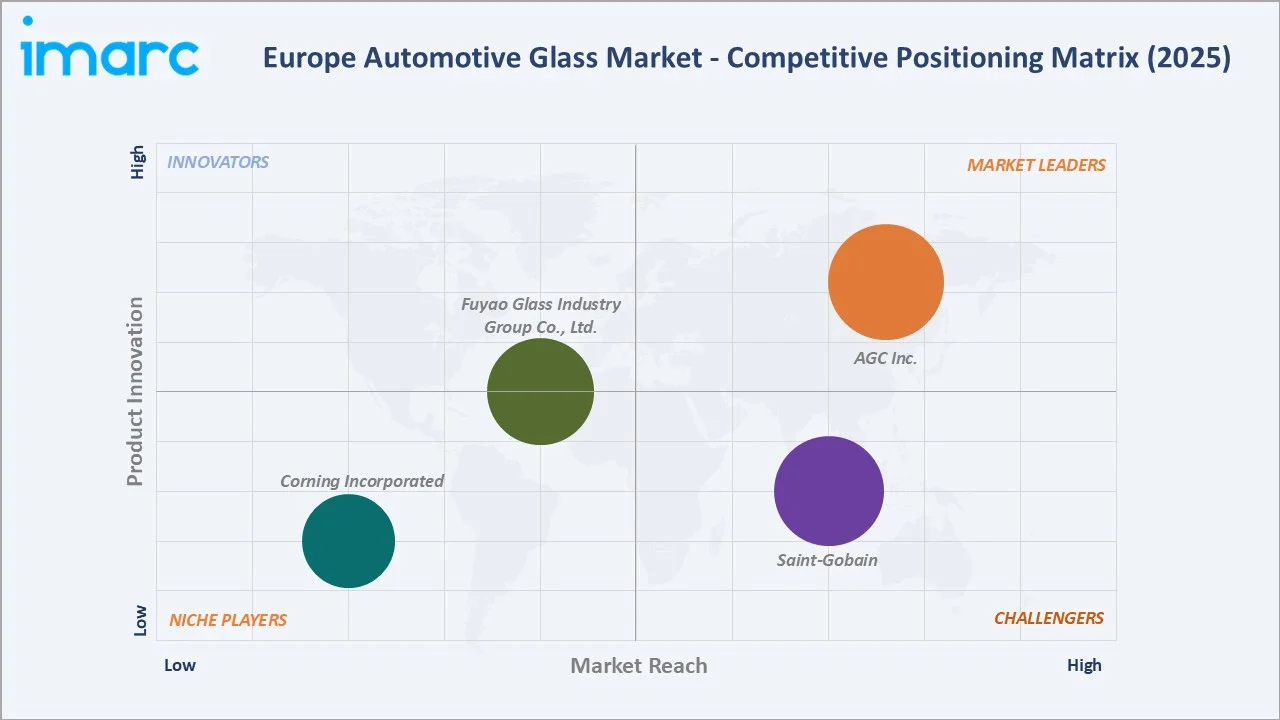

Competitive Landscape

Europe's automotive glass market operates with high concentration at the top, with AGC Automotive and Saint-Gobain Sekurit collectively commanding approximately 70-75% of European OEM first-fit automotive glass supply. This player concentration is maintained by the capital intensity of float glass manufacturing, the length of OEM qualification processes, and the supply logistics infrastructure required to serve European assembly plants from proximate glass processing facilities.

|

Company Name |

Key Brands |

Market Position |

Core Strength |

|

AGC Inc. |

AGC Automotive |

Market Leader |

In the automotive industry, the advancement of CASE technologies is accelerating. In response to this trend, AGC Automotive has become the first in the world to develop a wide range of high-performance glass. |

|

Saint-Gobain |

Saint-Gobain Sekurit |

Strong Challenger |

Saint-Gobain Sekurit has been a leading car glazing manufacturer for over 90 years. |

|

Fuyao Glass Industry Group Co., Ltd. |

Fuyao |

Established Player |

Fuyao Europe, based in Leingarten near Heilbronn, is the German subsidiary of the China Fuyao Glass Industry Group. |

|

Corning Incorporated |

Gorilla Glass |

Niche Player |

Corning’s innovative glass technologies are paving the way for electric and autonomous vehicles. |

The competitive landscape is being reshaped by Fuyao Glass's European manufacturing establishment and aggressive OEM penetration strategy, demonstrating that Chinese-headquartered automotive glass companies can achieve European OEM approval and compete at quality parity with established European suppliers at pricing 10-20% below equivalent products.

Key Company Profiles

AGC Inc.

AGC Inc. is the world's largest architectural and automotive glass manufacturer. It supplies the automotive industry with OEM and replacement glass, and also serves the transport industry (train, tram and bus glass).

- Brand: AGC AGC Automotive.

- Recent Developments: In May 2025, AGC Automotive Czech started construction on a laminated windshield production line at its Chudeřice plant. The investment will enhance the plant’s production capacity and technological capabilities, including the use of automation.

- Strategic Focus: Focuses on advanced automotive glazing technologies, lightweight and smart glass solutions, ADAS-compatible windshields, and sustainable glass manufacturing to strengthen its position in the Europe automotive market.

Saint-Gobain

Saint-Gobain Sekurit is the automotive glass division of Saint-Gobain, one of the world's oldest and largest industrial materials groups.

- Brand: Saint-Gobain Sekurit.

- Recent Developments: In February 2025, Saint-Gobain’s Sekurit Automotive Division in France partnered with Unelko after extensive laboratory and field testing of advanced glass coating solutions. Following highly positive test results, Sekurit decided to launch its Aquacontrol+ glass repellent technology across more than 17 countries using Unelko’s Invisible Shield PRO 15 coating technology.

- Strategic Focus: Focuses on expanding premium glazing solutions, enhancing automotive glass coating technologies, and developing energy-efficient smart glass systems to support next-generation mobility across Europe.

Market Concentration Analysis

Europe's automotive glass market OEM supply is highly concentrated; AGC Automotive Europe and Saint-Gobain Sekurit together hold approximately 70-75% of European OEM first-fit glass supply. This supplier concentration has been maintained by the combination of capital-intensive float glass manufacturing (creating high barriers to entry), the 18-36 month OEM qualification timelines (creating incumbency advantages for approved suppliers), and the logistics infrastructure requirements. Fuyao's successful European market entry has reduced the concentration slightly, but the established supplier OEM relationship structure remains dominant.

The ARG aftermarket is more fragmented, reflecting the lower qualification barriers and more price-competitive dynamics of the replacement glass channel versus OEM supply. Concentration dynamics may shift during 2026-2034 if: Fuyao establishes a second European manufacturing facility; Chinese glass manufacturers pursue additional European manufacturing investments beyond Fuyao; or European OEMs accelerate their in-house glass manufacturing strategies to reduce dependency on the three-supplier oligopoly for increasingly strategic ADAS and solar glass components.

Investment & Growth Opportunities

Highest Growth Investment Areas

IR PVB material glass (~4.6% CAGR), metal coated glass (~4.1% CAGR), laminated glass overall (~3.8% CAGR), electrochromic smart glass (~15-20% CAGR from smaller base), solar-integrated glass (photovoltaic, ~25% CAGR from very small base), and ADAS-integrated windshield (system value, ~8-10% CAGR as ADAS becomes standard across European vehicle segments) represent Europe's highest-growth automotive glass investment vectors. The premium glass product portfolio collectively creates the market's highest-margin growth opportunity.

Emerging Investment Opportunities

The automotive glass recycling and remanufacturing market represents an emerging opportunity as EU ELV Directive recycling target enhancements and EU Green Deal principles drive OEM and aftermarket interest in closed-loop glass supply. PVB laminated windshield recycling requires specific delamination technology investments.

Investment Themes

- Large-format laminated glass processing investment for EV roof glass supply: European automotive glass processors must invest EUR 8-15 Million per large-format bending furnace to process the 1.0-1.5 sqm curved laminated glass panels required for EV panoramic roofs. Each bending furnace serves 8-12 vehicle model programs with moderate production rates, creates compelling ROI for bending furnace capacity investment by European glass processors with existing OEM relationships.

- Electrochromic and smart glass product development for European premium OEM supply: Glass manufacturers or materials companies achieving EUR 150-250 per sqm electrochromic cost reduction (through volume production optimization and materials substitution) unlock a EUR 5-8 Billion addressable European automotive electrochromic glass market by 2034. Technology investment paths include polymer-dispersed liquid crystal (PDLC) film laminated in standard automotive glass structures (simplest technical approach) through suspended particle devices (SPD) and oxide-based electrochromic coatings (most durable but currently most expensive approaches).

Future Market Outlook (2026-2034)

The Europe automotive glass market is projected to grow from USD 16.51 Billion in 2025 to USD 22.89 Billion by 2034, delivering a 3.58% CAGR over the forecast period. The market's anchor value of USD 19.69 Billion in 2030 represents a European automotive glass industry where EV panoramic glass roofs have become standard equipment on new European vehicle registrations, IR PVB has penetrated to new European laminated glass production, and HUD-compatible laminated windshields are standard specification on all European C-segment and above vehicles.

Three structural forces define Europe's automotive glass market growth through 2034 with high certainty: the EU ICE ban mandate driving OEM EV platform investment that structurally requires larger glass roofs, acoustic glass, and EV thermal management glass technologies generating higher per-vehicle glass revenue than the equivalent ICE platforms they replace; the 5-star safety rating system's progressive integration of ADAS sensor requirements creating mandated windshield technology upgrades that sustain premium glass product adoption across all European vehicle segments; and the EU CO2 Fleet Regulation's tightening vehicle emissions limits creating OEM demand for lightweight and solar-collecting glass technologies that reduce vehicle kerb weight and supplement EV powertrain with passive solar energy recovery.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including automotive glass supply and engineering directors from AGC Automotive Europe and Saint-Gobain Sekurit; glass procurement and technical specification managers from Volkswagen Group, BMW Group, and Renault Group; ARG market operations managers from Belron International; PVB interlayer application engineers; and ADAS system integration engineers from Bosch Automotive and Continental AG working on windshield-integrated camera system development.

Secondary Research

Secondary research encompassed ACEA (European Automobile Manufacturers Association) European vehicle production statistics 2020-2025; European Commission regulation chemical compliance for automotive glass materials; individual company annual reports and investor presentations for AGC Inc., Saint-Gobain; European Flat Glass Alliance (Glass for Europe) industry statistics; and trade press publications. Over 65 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up glass type and material type models calibrated against European vehicle production volume forecasts, average glass content value per vehicle segment, and aftermarket glass demand from European registered vehicle fleet size, average vehicle age distribution, and annual glass replacement rate. Key inputs include EU CO2 regulation tightening targets, EV adoption projections by country, ADAS standard specification deployment timeline, and HUD/panoramic roof option take-rate growth by segment.

Europe Automotive Glass Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Glass Types Covered | Laminated Glass, Tempered Glass, Others |

| Material Types Covered | IR PVB, Metal Coated Glass, Tinted Glass, Others |

| Vehicle Types Covered | Passenger Cars, Light Commercial Vehicles, Trucks, Buses, Others |

| Applications Covered | Windshield, Sidelite, Backlite, Rear Quarter Glass, Sideview Mirror, Rearview Mirror, Others |

| End Users Covered | OEMs, Aftermarket Suppliers |

| Technologies Covered |

|

| Countries Covered | Germany, France, United Kingdom, Italy, Spain, Others |

| Companies Covered | AGC Inc., Saint-Gobain, Fuyao Glass Industry Group Co., Ltd., Corning Incorporated, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Europe automotive glass market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Europe automotive glass market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Europe automotive glass industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Europe Automotive Glass Market Report

The Europe automotive glass market reached USD 16.51 Billion in 2025, driven by Europe's vehicle production, expanding EV platform demand for panoramic glass roofs and IR PVB laminated windshields, ADAS camera integration requiring advanced windshield technology upgrades, the growing aftermarket serving registered European vehicles, and premiumization across German and French OEM platforms toward acoustic and solar-control glass.

The market grows at 3.58% CAGR during 2026-2034, reaching USD 22.89 Billion by 2034, driven by EV platform glass revenue uplift, HUD windshield penetration growth, EU CO2 Fleet Regulation driving lightweight and solar glass adoption, and electrochromic glass achieving mass-market cost thresholds for European upper-medium segment deployment.

Laminated glass leads at 46.8% as regulation mandates laminated construction for all European windshields, plus expanding applications to acoustic side glass and panoramic roofs.

IR PVB leads at 34.7% as the dominant European premium automotive glass material, growing fastest at ~4.6% CAGR as EV thermal management requirements and luxury comfort specifications drive IR PVB penetration from 35% to a projected 55-60% of European laminated glass by 2034.

Germany leads at 22.4% through premium vehicle production concentration, generating Europe's highest per-vehicle glass content value. Germany's premium segment drives the technology innovation that defines European automotive glass market direction.

Leading companies include AGC Inc., Saint-Gobain, Fuyao Glass Industry Group Co., Ltd., and Corning Incorporated, among others.

The market is projected to reach approximately USD 19.69 Billion by 2030, with EV panoramic roofs standard on new European registrations, IR PVB penetrating European laminated glass production, HUD windshields standard on all C-segment and above European vehicles, first mass-market electrochromic roof deployments, and ADAS windshield subassembly supply transitioning from glass-plus-brackets to complete camera-in-windshield assemblies at European OEM plants.

EV platforms create three distinct automotive glass demand upgrades: larger panoramic glass roofs providing 2-3x glass revenue per roof installation; acoustic laminated side glass replacing tempered sidelights because EVs without engine noise require glass noise attenuation; and IR PVB and metal-coated glass for thermal management.

Five key technology innovations are driving European automotive glass average selling price and margin improvement: HUD-compatible double-wedge PVB laminated windshields; IR PVB solar-heat-management laminated glass; acoustic PVB side glass for EV cabin quietness; ADAS camera-bracket integrated windshield subassembly; and electrochromic switchable roof glass.

Three priority opportunities: large format bending furnace investment for EV panoramic roof glass; ADAS windshield subassembly capability development transitioning from glass supplier to system supplier; and electrochromic glass product development targeting European premium OEM deployment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade